20 CHARTS FOR 2020 NEI MARKET OUTLOOK - NEI 2020 MARKET OUTLOOK - NEI Investments

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

20 CHARTS FOR 2020 NEI MARKET OUTLOOK NEI 2020 MARKET OUTLOOK 1

Great global uncertainty leads to… record high stock prices?

Opinions as of December 13, 2019

It’s been said many times that “markets hate our global sub-advisors. In one form or another, the As we look forward to the 2020s, we expect climate

uncertainty.” Well, not in 2019. charts we’ve included speak to the following main points: change and other responsible investing themes to

dominate the financial headlines. These themes will

In fact, data to November 30 show the S&P 500 hit 19 • We do not expect a global recession as central become more important to our political, regulatory and

new highs in 2019 and is on track to end the year with a banks maintain accommodative policies, with room financial systems, creating opportunity for those willing

total return of roughly 28% in U.S. dollar terms. The for governments to add fiscal stimulus if needed. to adapt and risks for those who are not. As Canada’s

S&P/TSX Composite has also been notching record leader in responsible investing, we welcome these

highs as it closes in on a year-to-date total return of 22%. • Stocks are likely to rise further, but we don’t changes and believe the 2020s will be a decade of true

And it’s not just equities powering ahead. Bonds have expect next year’s returns to be as impressive as impact, where responsible investors can help improve

also had a strong year, with some markets delivering last year’s. the world’s environmental and social conditions in

double-digit returns (as well as negative yields…). meaningful ways.

• Longer term, we expect equity leadership to rotate

All this at a time of record policy uncertainty; the U.S.- out of the U.S. and into international and emerging

China trade war; the slowest global economic growth markets, but we need more concrete evidence the

since the Great Recession; the neverending saga known global economy is rebounding before taking a

as Brexit; and a U.S. president facing impeachment and stronger stance.

an election. And now we can finally add this: a growing

acknowledgement of the risk of climate change to the • Given global uncertainties, bonds will continue to

financial system, courtesy of global central banks. be an important part of portfolios, but expect lower

returns than what we got in 2019.

So, what’s next? • We expect the policy response to climate change to

rise ever higher on the priority list of global financial

To help you prepare for client conversations about what leaders, which will in turn find its way into asset John Bai, CFA

could be in store for markets next year, we offer 20 prices, with both positive and negative impacts. VP and Chief Investment Officer

charts for 2020, assembled in collaboration with many of NEI Investments

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 2

2019: A strong year for most asset classes

Stocks and bonds performed exceptionally well in 2019. Many indices closed not just at or near the highest level of the year,

but at or near their highest levels on record.

YTD performance of 20 asset classes

30%

25%

20%

15%

10%

5%

0%

-5%

-10%

Gold

International Equity

US HY Bonds

Crude Oil (WTI)

Emerging Market Equity

US Large Cap Equity

Developed Market Equity

USD (vs. CAD)

EUR (vs. CAD)

Canadian Large Cap Equity

Global Equity (Growth)

Commodities (BoC Index)

USD (Trade Weight)

Global Equity (Value)

US IG Bonds

Canadian Cash

US Small Cap Equity

Canadian IG Bonds

Canadian Small Cap Equity

Global IG Bonds

EQUITIES FIXED INCOME COMMODITIES CURRENCIES

Source: Bloomberg and Morningstar, data as of November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 3

The economic backdrop

While we do not see recession on the horizon, we do

expect continued slower global growth in 2020

Downside risks remain elevated as uncertainty abounds

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 4Secular trends point to slower growth ahead in developed economies

Shrinking workforce + declining productivity growth = lower potential growth across developed economies. Expect this to

result in lower equity returns and the ongoing suppression of bond yields.

Working age population as % of total population Annual change in GDP per hour worked

70% 3.0%

2.5%

68%

2.0%

66%

1.5%

1.0%

64%

0.5%

62%

0.0%

60% -0.5%

1971 1976 1981 1986 1991 1996 2001 2006 2011 Canada France Germany Italy Japan UK US

Canada Euro Area Japan US All OECD 1995-2000 2000-2005 2005-2010 2010-2014 2014-2018

Source: Organization for Economic Cooperation and Development, data accessed November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 5Global growth increasingly driven by emerging economies

The growth and maturation of emerging economies will present ever-increasing investment opportunities outside

North America.

World economy breakdown

• Emerging economies made

100%

up only 25% of the world’s

economy in 1980

• By the end of 2019, emerging

75%

economies are expected to

make up 40% of world GDP

50%

25%

0%

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020 2024

Advanced Economies Emerging Economies

Source: International Monetary Fund, data accessed November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 6Emerging economies expected to grow at twice the pace of developed economies

Over the next year, the anticipated economic rebound in emerging economies could lead to outperformance of EM equities,

debt and currencies.

World DM EM • Economic growth likely to

slow further for developed

economies in 2020

4.9 • Emerging economies

3.8 expected to rebound slightly

4.4

4.2

3.2 3.2 in 2020

• Gap between developed and

emerging markets is expected

2.2 to widen, though downside

1.7 risks continue to dominate

1.4

2018 2019 2020 2018 2019 2020 2018 2019 2020

Source: Amundi Research forecast, data as of November 4, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 7U.S. economic growth driven by strong consumer spending

Despite the presence of global macro headwinds, a strong domestic economy will likely prevent a U.S.-led recession in 2020.

University of Michigan Consumer Sentiment Index

• Consumer confidence is an

120 100

important leading indicator,

90 used to estimate future

80

consumption behaviour

100

70

• Confidence tends to stem

from job security and wage

60

satisfaction, providing insight

80 50 into the labour market

40

30

60

20

10

40 0

1978 1983 1988 1993 1998 2003 2008 2013 2018

U.S. Recession

Source: Surveys of Consumers, University of Michigan, University of Michigan: Consumer Sentiment © [UMCSENT], retrieved from FRED, Federal Reserve Bank of St. Louis;

https://fred.stlouisfed.org/series/UMCSENT, November 19, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 8Uptick in key leading indicator a sign of hope

Some Composite Purchasing Managers’ Indices may have bottomed in September 2019, with a continued rebound acting

as a potential driver of further equity upside.

Composite Purchasing Managers’ Indices

• Germany and the larger

56

eurozone showing a notable

55 bounce-back

• China, emerging markets

54

rising since June 2019

53 • Developed markets overall

still headed lower – but for

52

how long?

51

50

49

48

Nov 2018 Dec 2018 Jan 2019 Feb 2019 Mar 2019 Apr 2019 May 2019 Jun 2019 Jul 2019 Aug 2019 Sep 2019 Oct 2019

Developed Markets US Eurozone Germany Emerging Markets China Expansion/contraction

Source: Bloomberg, data as of November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 9Policy uncertainty at record high, driven by trade tensions

The abatement or escalation of historically high trade tensions can have a significant impact on markets on a

day-to-day basis.

U.S. Categorical Policy Uncertainty Index

• Current concern over trade

2,000

Monetary policy

policy is having a greater impact

1,800

Fiscal Policy

on overall sentiment than any

1,600 National security

other factor in recent past

Trade policy • Risk of U.S./China trade tension

1,400

Sovereign debt, currency crises spreading to other regions –

1,200 U.S. Recession notably Europe and Japan – has

1,000 hurt business and investor

sentiment

800

600

400

200

0

1997 2000 2003 2006 2009 2012 2015 2018

Source: “Measuring Economic Policy Uncertainty” by Scott Baker, Nicholas Bloom and Steven J. Davis at www.PolicyUncertainty.com.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 10

10Monetary and fiscal policy

Central banks have responded to slowing growth by

lowering interest rates and increasing balance sheets

Additional stimulus from fiscal policy is available if needed

Central banks are increasingly turning their attention to

climate change as a key risk to financial stability

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 11

11U.S. Fed rate cuts may neutralize once-reliable recession indicator

Proactiveness of U.S. central bank is another reassuring sign that a recession may not come just yet.

U.S. yield curve, Federal Reserve rate, and recessions

• Inverted yield curve (dark blue

400bps

line falling below orange line)

20% has consistently preceded past

300bps

recessions

200bps • Overly tight monetary policy

15%

stifles economic growth, and a

100bps closer look reveals the Fed has

raised rates in the lead-up to

10%

0bps each yield curve inversion

• This time, the Fed has cut rates

-100bps

5% prior to August 2019 yield curve

-200bps

inversion, preventing a longer

and more pronounced period of

-300bps 0% inversion.

1979 1985 1991 1997 2003 2009 2015

U.S. Recession 2s10s (LHS) Fed Funds Rate (RHS)

Source: Bloomberg, data as of November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 12

12How much lower can central banks go?

With rates at rock bottom (and below zero), central banks will have to forego a primary policy tool for combatting crisis

conditions like what we saw in 2008.

Central bank policy rates

• 2019 saw another wave of

9%

global central bank easing amid

8% softening economic data and

7% escalating trade uncertainty

6% • Most developed nations

5% already have policy rates below

4%

the rate of inflation, meaning

majority of policy rates around

3%

the world are actually negative

2%

in real terms

1%

0%

-1%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Eurozone Australia Canada Japan South Korea New Zealand

Norway Sweden Switzerland UK US China

Source: Bloomberg, data as of November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 13

13New ECB president may help shift focus to fiscal policy in eurozone

Christine Lagarde may attempt to improve coordination between monetary and fiscal policies.

Public investment as % of GDP

• Christine Lagarde took over as

6.0 ECB president in November,

making the case for investing

5.0 “in a common future that is

more productive, more digital

4.0 and greener”

• Eurozone austerity measures

3.0

since 2011 have brought down

the amount of public investment

2.0 as % of GDP, so this has

significant room to grow

1.0

0.0

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Germany Ireland Spain France Italy Netherlands Portugal

Source: Eurostat, data accessed November 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 14

14Central banks acting on climate change

Almost 50 central banks and regulators have formed Central Banks and Supervisors’ Network for Greening the Financial

System, defining best practices in climate risk management.

Number of Central Banks that have adopted environmental activities by type

55 The importance of climate-related

issues for financial stability and

Green network membership

monetary policy have become

45 Green lending guidelines or green bond program

increasingly clear. This is

ESG risk incorporation

particularly true for Canada, where

35 resources play a vital role in our

economy and where the natural

25

environment is a defining feature

of our national identity.”

15 – Bank of Canada Governor

Stephen Poloz

5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

-5

Source: Bloomberg https://www.bloomberg.com/news/articles/2019-09-23/no-laughing-matter-how-climate-change-is-scaring-central-banks

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 15

15Bonds

We don’t expect double digit returns to repeat in 2020 –

we’d likely need a recession for that

We emphasize more defensive positioning:

• Higher quality investment grade credit

• Shorter duration

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 16

16Core bond yields expected to stay low

Yields should stay in a low range as major developed economies continue to experience slow growth next year; expect bond

volatility around trade concerns.

Inflation – developed economies 10-year bond yields – developed economies

4% 4%

3% 3%

2% 2%

1% 1%

0% 0%

-1% -1%

2014 2015 2016 2017 2018 2019 2020 2021 2014 2015 2016 2017 2018 2019 2020 2021

Canada U.S. Eurozone U.K. Japan Target Canada U.S. Eurozone U.K. Japan

Source: Bloomberg. Inflation data as of October 31, 2019; bond yield data as of November 30, 2019. 2019–2021 projections are based on Bloomberg consensus

estimates. Bloomberg consensus estimates for both inflation and bond yields are indicated with dotted lines.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 17

17Respect credit cycles

U.S. firms are more leveraged than ever, but this risk is not currently reflected in credit spreads.

U.S. corporate debt versus credit spreads

49 18

• Historically, high yield

spreads have been closely

16

47

correlated with an increase in

14 corporate debt

45 12 • Since the 2008 financial crisis,

loose monetary policy has

10

43 lowered borrowing costs and

8 encouraged corporations to

41 6 take on more debt

4

39

2

37 0

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

U.S. Recessions U.S. Nonfinancial corporate debt/GDP (% LHS) U.S. high yield spread (% RHS)

Source: Haver Analytics, Ned Davis Research, Bloomberg, QV Investors. Data as of December 1, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 18

18Stocks

We expect equities to outperform bonds over

the next year

Regionally, we see opportunity in international

and emerging market equities

From a style perspective, value may be making

a comeback

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 19

19U.S. by far the strongest stock market since 2009 crisis low

The longest bull market on record has helped drive the S&P 500 to a gain of more than 300%, while the S&P/TSX Composite,

MSCI World and MSCI Emerging Market indices have lagged significantly.

Total equity returns for major regions (C$)

350%

Canada

300%

U.S.

250% International

Emerging Markets

200%

150%

100%

50%

0%

-50%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source. Bloomberg, data as of November 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 20

20International equities: comparable earnings growth, cheaper valuations

While rest of the world has lagged the U.S. in terms of historical equity performance, the fundamentals favour international

equities going forward.

Equity characteristics: U.S. versus rest of world

101.0%

S&P 500

ACWI Ex US

63.0%

23.2x 20.8x

15.9% 17.0x 16.1x 16.5x

10.4x

6.7% 6.7%

0.6%

EPS Growth (trailing) EPS Growth (forward) Price/Earnings (trailing) Price/Earnings (forward) Price/Cash Flows Debt/Equity

Source: Factset, data as of November 2019. Index shown for comparison purposes only.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 21

21Lower interest rates supportive of equities

Equity risk premiums (ERP) have risen globally versus year-ago levels; ERP around the world suggest equity markets

outside the U.S. hold more opportunity.

The equity risk premium is the

difference between the earnings CANADA

ERP Sep 2019:

yield and the 10-year U.S. U.K. CHINA

ERP Sep 2019:

Treasury, representing the “extra” 5.8% ERP Sep 2019:

return you receive for owning 7.6% 5.8%

equities over bonds.

GERMANY

U.S. ERP Sep 2019:

ERP Sep 2019: JAPAN

8.3% ERP Sep 2019:

4.2% 7.8%

BRAZIL

ERP Sep 2019:

AUSTRALIA

0.8% ERP Sep 2019:

> 7%

5% – 7% 5.1%

< 5%

Numbers may not sum due to rounding. Source: FactSet, MSCI and AB, data as of September 30, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 22

22Canadian equity dividend yield higher than long bond yield

Investors can earn better income from stocks than bonds, but volatility risks are higher with stocks.

S&P/TSX dividend yield versus 10-year Govt Canada bond yield

• Bond yields and inflation have

20

both been falling on a secular

18 basis since the early 1980’s

16

• The dividend yield on the

14 Canadian stocks have slowly

12 risen over the past twenty years

10 • On a cross-asset class basis,

8 data suggest stocks are likely

6 the better investment from a

4

yield perspective, though full

2

equity valuations plus elevated

macro risk warrant a cautious

0

approach

Aug-83

Nov-84

Aug-88

Nov-89

Aug-93

Nov-94

Aug-98

Nov-99

Aug-03

Nov-04

Aug-08

Nov-09

Aug-13

Nov-14

Aug-18

Nov-19

May-82

May-87

May-92

May-97

May-02

May-07

May-12

May-17

Feb-81

Feb-86

Feb-91

Feb-96

Feb-01

Feb-06

Feb-11

Feb-16

TSX Dividend Yield Canada Long Bond Yield

Source: Bloomberg, data as of November 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 23

23Value stocks underperformance versus growth stocks near record levels

Value stocks displaying compelling risk/reward characteristics

Rolling 10-year total return difference: FAMA-French HML (value vs growth)

• Relative to growth, value

14% is experiencing its weakest

12%

performance in nearly

8 decades

10%

• Underperformance gap

8% between value and growth

exceeds that of the tech

6%

bubble and is second only to

4% the Great Depression

2% • Opportunities to find quality

and value have opened up in

0%

Tech Bubble industrials, financials and

-2% energy sectors

Great Depression Recently

-4%

1936 1941 1946 1951 1956 1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011 2016

Source: Kenneth French, QV Investors, Data as of December 31, 2018: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 24

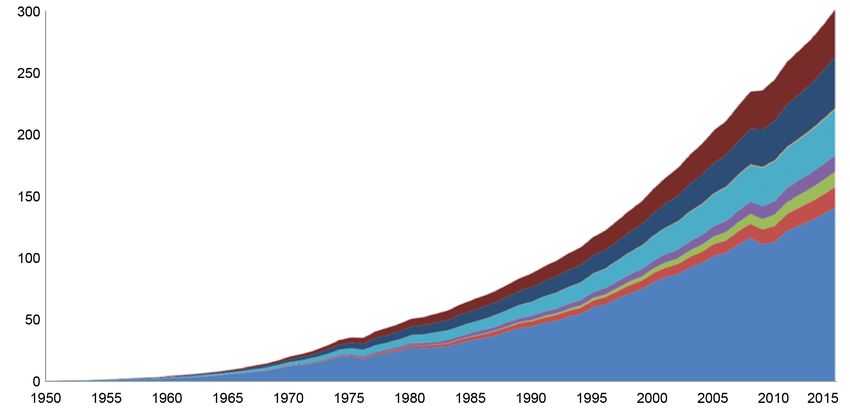

24The global plastics problem – an opportunity for the responsible investor

From 1950 to 2015, plastic waste production has soared across major sectors.

Other

Textiles The transition to a more

sustainable economy presents

Primary Plastic Waste Generation (in Mt)

Industrial Machinery

Consumer & Institutional Products opportunities for investors and

Electrical/Electronic risks to companies that choose

Building & Construction to ignore strong trends in

Transportation changing consumer preferences

Packaging for more sustainable products,

advances in technology and

innovation, changing global

regulations, and the impact of

larger societal factors.”

Source: Cosmos Magazine, “Global plastic waste totals 4.9 billion tonnes,” July 20, 2017: https://cosmosmagazine.com/society/global-plastic-waste-totals-4-9-billion-tonnes; GEYER, JAMBECK, LAW,

‘SCIENCE ADVANCES’, JULY 2017.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 25

25The “first corporate casualty of climate change”

California-based utility company PG&E named the “first corporate casualty of climate change” by The Wall Street Journal

after it sought bankruptcy protection in January 2019.

Stock Price of PG&E

• PG&E named the “first

80

corporate casualty of climate

California wildfires of late 2017 among

70 most damaging on record change” by The Wall Street

Journal

60 • After facing more than

US$30 billion in liabilities

50

related to wildfires, PG&E

40

sought bankruptcy protection

PG&E faces deeper scrutiny over

in January 2019

30 responsibility for 2017/2018 wildfires • The utility company has been

20

found responsible for the

destruction of hundreds of

10 PG&E seeks bankruptcy protection

acres of land

in Jan 2019

0

2006 2009 2012 2015 2018

Source: Bloomberg. Data as of November 27, 2019.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 26

26Too few companies reacting to the challenges of climate change

The Transition Pathway Initiative says 21% of companies do not disclose enough information to allow investors to understand

their exposure to the transition to a low-carbon economy, presenting an opportunity for shareholder engagement.

Alignment to Paris Agreement benchmarks by sector

100%

1 1 2 2 2020 should be the year when a

1 1

90%

3 2

strategic focus on climate change

5

80% 4

12 becomes a necessity and those

2

companies who are ahead of the

70%

10 trend should flourish. Investors

4 4

60% can play an important part in this

8 9

50%

9 by engaging with companies to

14 3 facilitate and encourage the

40%

14 transition, particularly in those

30% sectors which continue to lag.”

10 16

20% 3 7 8

10%

2 1

0%

1 1

Airlines Autos Aluminium Cement Paper Steel Electricity Oil & Gas

No disclosure Not aligned Paris aligned 2 degrees aligned Below 2 degrees aligned

Source: http://www.lse.ac.uk/GranthamInstitute/tpi/wp-content/uploads/2019/07/TPI-State-of-Transition-Summit-presentation-20190712.pdf

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 27

27Summary

We do not expect a global recession as central banks maintain accommodative

policies, with room for governments to add fiscal stimulus if needed.

Stocks are likely to rise further, but we don’t expect next year’s returns to be as

impressive as last year’s.

Longer term, we expect equity leadership to rotate out of the U.S. and into

international and emerging markets, but we need more concrete evidence the

global economy is rebounding before taking a stronger stance.

Given global uncertainties, bonds will continue to be an important part of

portfolios, but expect lower returns than in 2019.

We expect the policy response to climate change to rise ever higher on the

priority list of global financial leaders, which will in turn find its way into asset

prices, with both positive and negative impacts.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 28

28Summary

As we look forward to the 2020s, we expect climate change and other responsible

investing themes to dominate the financial headlines.

These themes will become more important to our political, regulatory and financial

systems, creating opportunity for those willing to adapt and risks for those who are not.

As Canada’s leader in responsible investing, we welcome these changes and believe

the 2020s will be a decade of true impact, where responsible investors can help

improve the world’s environmental and social conditions in meaningful ways.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 29

29The bottom line

We remain optimistic the economic cycle

will continue to be supportive of stocks over

bonds, though as always, we take a balanced

approach in our portfolio solutions to insulate

investors from ongoing volatility and the

potential for a more pronounced downturn.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 30

30The outlook

As we look forward to the 2020s, we

expect responsible investing themes to

dominate the financial headlines creating

opportunity for those who are willing

to adapt and risks for those who are not.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 31

31neiinvestments.com

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus and/or Fund Facts before

investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. NEI Investments is a registered trademark of Northwest &

Ethical Investments L.P. Northwest & Ethical Investments Inc., is a wholly-owned subsidiary of Aviso Wealth Inc. (“Aviso”). Aviso is a wholly-owned subsidiary of Aviso Wealth

Limited Partnership (“Aviso Wealth LP”), which in turn is owned 50% by Desjardins Financial Holdings Inc. (“Desjardins”) and 50% by a limited partnership owned by the five

Provincial Credit Union Centrals (the “Centrals”) and the CUMIS Group Limited.

Views expressed regarding a particular security, industry or market sector should not be considered an indication of trading intent of any funds managed by NEI Investments.

This material is for informational and educational purposes and it is not intended to provide specific advice including, without limitation, investment, financial, tax or similar matters.

Please consult with your own professional advisor on your particular circumstances.

The views expressed herein are subject to change without notice as markets change over time. NEI Investments endeavors to ensure that the contents have been compiled or

derived from sources that we believe are reliable and contain information that is accurate and complete. However, NEI Investments makes no representation or warranty, express

or implied, in respect thereof, takes no responsibility for any errors and omissions contained herein.

2020

NEI 2020 MARKET

MARKET OUTLOOK

OUTLOOK 32You can also read