Adelaide Student Accommodation Demand and Supply Analysis

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Adelaide Student Accommodation Demand and Supply Analysis Prepared for: The Government of South Australia - Department for Trade, Tourism and Investment July 2019

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Table of Contents

Executive Summary ................................................................................................................................................................... 6

Introduction ........................................................................................................................................................................ 10

Adelaide Overview.............................................................................................................................................................. 11

2.1 Overview ...................................................................................................................................................................................... 11

2.2 Demographics ............................................................................................................................................................................ 12

2.3 Adelaide Student Demographics Summary ........................................................................................................................ 13

South Australian Universities Overview .......................................................................................................................... 15

3.1 The University of Adelaide ....................................................................................................................................................... 15

3.2 Flinders University ..................................................................................................................................................................... 18

3.3 University of South Australia ................................................................................................................................................... 22

3.4 Torrens University Australia Adelaide Campus................................................................................................................ 28

3.5 Full-time Student Enrolment Trends 2007 2017.............................................................................................................. 28

3.6 Beyond Universities - Other Student Markets Accessing PBSA ....................................................................................... 30

3.7 International Students by Source Market ............................................................................................................................ 33

Supply Considerations Inner Adelaide ......................................................................................................................... 35

4.1 Types of Accommodation Where do students live? ....................................................................................................... 35

4.2 Existing Student Accommodation compared with Higher Education Enrolments .................................................... 37

4.3 Pricing ........................................................................................................................................................................................... 38

Supply Considerations Bedford Park ........................................................................................................................... 41

5.1 Existing Student Accommodation ......................................................................................................................................... 41

5.2 Pricing ........................................................................................................................................................................................... 41

Supply Considerations Mawson Lakes ......................................................................................................................... 42

6.1 Existing Student Accommodation ......................................................................................................................................... 42

6.2 Pricing ........................................................................................................................................................................................... 43

Rental Market Overview ..................................................................................................................................................... 44

7.1 Adelaide CBD and North Adelaide ......................................................................................................................................... 44

7.2 Bedford Park and Surrounding Suburbs Rental Market ................................................................................................... 46

7.3 Mawson Lakes and Surrounding Suburbs Rental Market................................................................................................. 49

Location of Higher Education Students .......................................................................................................................... 52

Occupancy Rates in PBSA ................................................................................................................................................. 53

Development Pipeline ....................................................................................................................................................... 55

Major Private Operators of PBSA ...................................................................................................................................... 56

11.1 Owner Operator Model ............................................................................................................................................................. 56

Page 1

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

11.2 Third Party Operator Model ..................................................................................................................................................... 56

University Benchmark Profiles ......................................................................................................................................... 58

12.1 Existing Supply of Accommodation ...................................................................................................................................... 58

PBSA Demand ..................................................................................................................................................................... 59

13.1 Demand Forecasts ..................................................................................................................................................................... 59

13.2 Inner Adelaide Forecasts .......................................................................................................................................................... 60

13.3 Bedford Park (Flinders University) Forecasts ...................................................................................................................... 63

13.4 Mawson Lakes Forecasts.......................................................................................................................................................... 66

13.5 Summary of Demand Forecasting ......................................................................................................................................... 69

Key Constraints for the Development of Additional PBSA in Adelaide ....................................................................... 73

14.1 Supply / Demand Balance ....................................................................................................................................................... 73

14.2 Physical constraints .................................................................................................................................................................. 73

14.3 Feasibility ..................................................................................................................................................................................... 73

Legislation and Accreditation Overview ......................................................................................................................... 75

15.1 Rate rebates ................................................................................................................................................................................ 75

15.2 Student Accommodation Accreditation .............................................................................................................................. 76

Page 2

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

List of Tables

Table 1: Selected Characteristics of Residents, City of Adelaide LGA and Greater Adelaide, 2016........................................... 12

Table 2: Selected Medians, City of Adelaide LGA and Greater Adelaide, 2016 .............................................................................. 13

Table 3: Summary of International Student Enrolments in SA, 2012-2019* .................................................................................. 13

Table 4: Full Time, On-site Student Enrolments in SA, 2017 ............................................................................................................. 14

Table 5: The University of Adelaide, Number of Student Enrolments, 2017 .................................................................................. 16

Table 6: The University of Adelaide, 2018 Enrolments by Campus .................................................................................................. 17

Table 7: Flinders University, Number of Student Enrolments, 2017 ................................................................................................ 18

Table 8: Flinders University, 2018 Enrolments by Campus ................................................................................................................ 21

Table 9: University of South Australia, Number of Student Enrolments, 2017 .............................................................................. 22

Table 10: University of South Australia, 2018 Enrolments by Campus............................................................................................ 26

Table 11: International Students Enrolments in the VET and ELICOS Sectors in South Australia, 2009-2019* ..................... 31

Table 12: International Higher Education Enrolments in SA by Source Market, 2018 ................................................................. 33

Table 13: International Student Enrolments in SA by Source Market and Sector, 2018 ............................................................. 34

Table 14: Inner Adelaide Supply Analysis, 2019 .................................................................................................................................... 37

Table 15: Summary of Pricing for Residential Colleges in North Adelaide, 2019 .......................................................................... 38

Table 16: PBSA Pricing in Inner Adelaide, 2019 .................................................................................................................................... 38

Table 17: Bedford Park Supply Analysis ................................................................................................................................................. 41

Table 18: PBSA Rents at Flinders University Bedford Park Campus, 2019 ..................................................................................... 41

Table 19: UniSA Mawson Lakes Campus Supply Analysis .................................................................................................................. 42

Table 20: Summary of existing PBSA Rents in proximity to UniSA Mawson Lakes, 2019 ............................................................ 43

Table 21: Adelaide CBD and North Adelaide Market Attributes, 2016 ............................................................................................. 44

Table 22: Adelaide CBD and North Adelaide Rental Analysis, March 2019 ..................................................................................... 45

Table 23: Bedford Park and Environs Market Attributes, 2016 .......................................................................................................... 47

Table 24: Bedford Park Rental Analysis .................................................................................................................................................. 48

Table 25: Mawson Lakes Market Attributes, 2016 Census .................................................................................................................. 50

Table 26: Mawson Lakes Rental Analysis, March 2019 ........................................................................................................................ 51

Table 27: Major Owners and Operators of PBSA in Australia, 2019 .................................................................................................. 57

Table 28: Summary of SA Universities Existing Student Accommodation Analysis, 2019 .......................................................... 58

Table 29: Summary of Comparable Universities Existing Student Accommodation Analysis, 2019 ........................................ 58

Table 30: Demand Analysis (Scenario 1) Inner Adelaide Student Accommodation Demand ................................................ 61

Table 31: Demand Analysis (Scenario 2) Inner Adelaide Student Accommodation Demand ................................................ 62

Table 32: Demand Analysis (Scenario 1) Flinders University Student Accommodation Demand ......................................... 64

Table 33: Demand Analysis (Scenario 2) Flinders University Student Accommodation Demand ......................................... 65

Table 34: Demand Analysis (Scenario 1) University of SA Mawson Lakes Student Accommodation Demand .................. 67

Table 35: Demand Analysis (Scenario 2) University of SA Mawson Lakes Student Accommodation Demand .................. 68

Page 3

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Table 36: Summary PBSA Forecasts, 2020, 2025, 2030 ....................................................................................................................... 69

List of Figures

Figure 1: Location Map ............................................................................................................................................................................... 11

Figure 2: The University of Adelaide North Terrace Campus Map .................................................................................................... 17

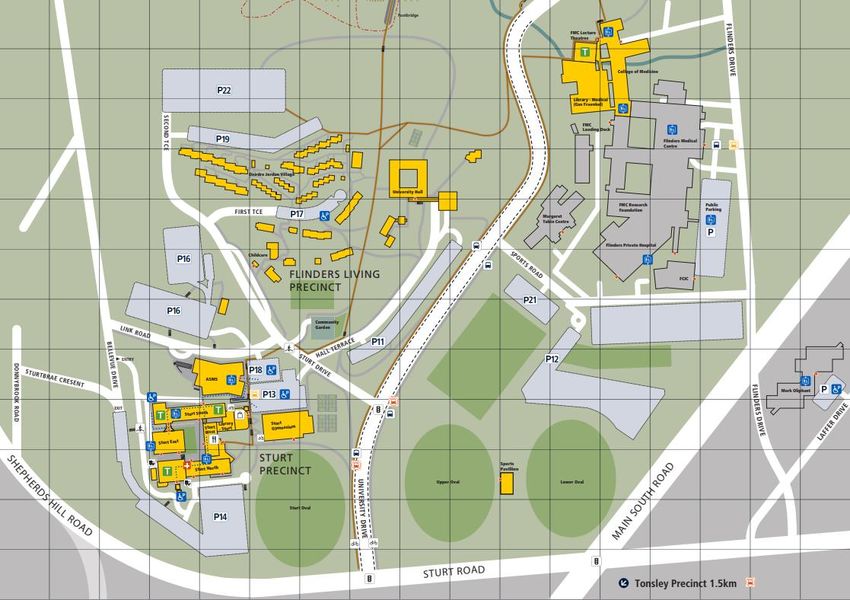

Figure 3: Flinders University Bedford Park Campus Map North and South Ridge Precincts .................................................. 20

Figure 4: Flinders University Bedford Park Campus Map Flinders Living & Sturt Precincts..................................................... 20

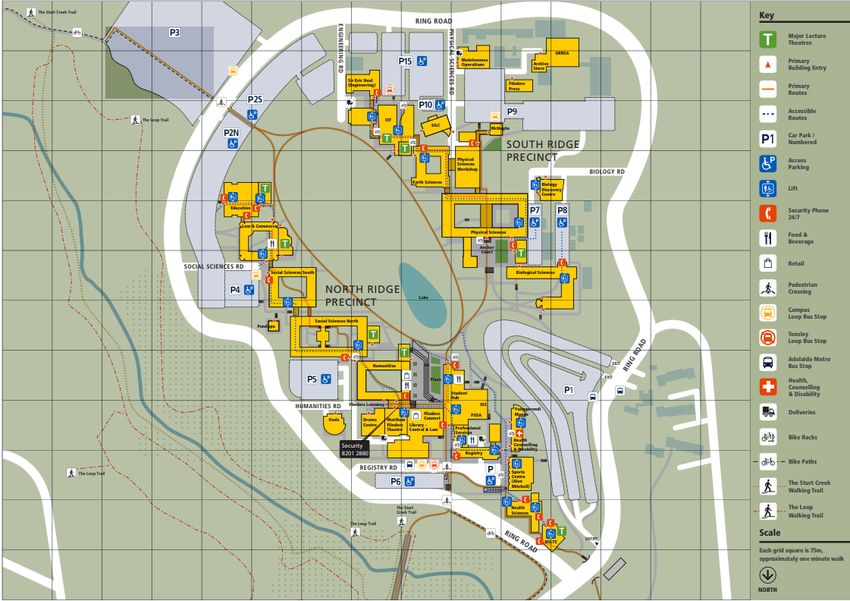

Figure 5: Tonsley Site Map ......................................................................................................................................................................... 21

Figure 6: University of South Australia City East Campus Map.......................................................................................................... 24

Figure 7: University of South Australia City West Campus Map ........................................................................................................ 25

Figure 8: University of South Australia Mawson Lakes Campus Map .............................................................................................. 27

Figure 9: Full-time On-site Enrolments at The University of Adelaide, 2007-2017........................................................................ 28

Figure 10: Full-time On-site Enrolments at Flinders University, 2007-2017.................................................................................... 29

Figure 11: Full-time On-site Enrolments at University of South Australia, 2007-2017 ................................................................. 29

Figure 12: Location Map, Adelaide ........................................................................................................................................................... 44

Figure 13: Location Map, Bedford Park .................................................................................................................................................. 46

Figure 14: Location Map, Mawson Lakes ................................................................................................................................................ 49

Figure 15: Residents attending Universities by SA2 Geography, 2016 ............................................................................................. 52

Figure 16: Inner Adelaide PBSA Supply and Demand Summary, Scenario 1 ................................................................................. 70

Figure 17: Inner Adelaide PBSA Supply and Demand Summary, Scenario 2 ................................................................................. 70

Figure 18: Bedford Park / Tonsley PBSA Supply and Demand Summary, Scenario 1 ................................................................. 71

Figure 19: Bedford Park / Tonsley PBSA Supply and Demand Summary, Scenario 2 ................................................................. 71

Figure 20: Mawson Lakes PBSA Supply and Demand Summary, Scenario 1 ................................................................................ 72

Figure 21: Mawson Lakes PBSA Supply and Demand Summary, Scenario 2 ................................................................................ 72

Page 4

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Disclaimer

The material contained in this report is confidential and was provided by JLL to the party to whom it is addressed strictly for the specific purpose to

which it refers and no responsibility is accepted to any third party.

Neither JLL nor any of its associates have any other interests (whether pecuniary or not and whether direct or indirect) or any association or

relationships with any of its associates that might reasonably be expected to be or have been capable of influencing JLL in providing this report.

Neither the whole of the report nor any part or reference thereto may be published in any document, statement or circular or in any communication

Whilst the material contained in the report has been prepared in good faith and with due care by JLL, no representations or warranties are made

(express or implied) as to the accuracy of the whole or any part of the report.

JLL, its officers, employees, subcontractors and agents shall not be liable (except to the extent that liability under statute or by operation of law

cannot be excluded) for any loss, liability, damages or expense suffered by any party resulting from their use of this report.

If a projection has been made in respect of future demand, business trends, property prices, rentals and projected take up rates, such a projection is

an estimate only and represents only one possible result therefore should at best be regarded as an indicative assessment of possibilities rather than

absolute certainties. The process of making forward projections of such key elements involves assumptions about a considerable number of variables

that are acutely sensitive to changing conditions and variations, and any one of which may significantly affect the resulting projections. This must be

kept in mind whenever such projections are considered.

JLL is not operating under an Australian Financial Services Licence. The financial analysis and conclusions contained within this report do not purport

to represent a valuation in the conventional sense. It is an exercise involving only relatively few variables, such as zoning information and a general

knowledge of background market conditions; whereas, a valuation involves a detailed investigation of the property including, where appropriate, the

nature of the locality, surrounding properties, full inspection, site peculiarities, the nature, quality and condition of improvements, comparable sales,

market trends, yields, competition, design and layout and so on. The market value could be greatly affected by such factors, and by encumbrances,

restrictions, or other impediments on Title, which have not been considered in this report. Accordingly, the financial analysis contained herein is

indicative only and not authoritative. It is merely a precursor to a formal valuation and should not be taken as a substitute for it.

Report Author

David Snoswell

Senior Director

Alternative Investments

JLL

david.snoswell@ap.jll.com

+61 414 919 476

Page 5

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Executive Summary

International education is a key economic growth sector for South Australia. I

second largest general export following wine, contributing $1.8 billion in economic activity and supporting 12,500 jobs in

2018.

South Australia attracts students from over 130 markets and has experienced an average growth rate of 6% in student

enrolments over the past five years. The South Australian Government aims to increase international student enrolments

from 38,000 in 2018 to 71,000 in 2030 through a LIVE, LEARN and STAY approach.

Increased international student enrolments will place increased demand for quality and affordability student

accommodation in close proximity to the major higher education institutions, particularly those institutions attracting

high numbers of international student enrolments.

International students play an important role in the economy, driving demand for a range of services, stimulating

activity and contributing to the vibrancy and diversity of the city. This is particularly so in the Adelaide CBD, where many

international international student community also provides valuable education

and trade links with worldwide destinations.

The focus of this report is the Greater Adelaide area, and the three major education precincts in Adelaide (Adelaide CBD,

Bedford Park and Mawson Lakes). The main campuses of the University of Adelaide and University of South Australia

(UniSA) are located in Adelaide CBD, Flinders University is in Bedford Park, and UniSA has a campus at Mawson Lakes

with a large international student base.

In terms of demand for student accommodation, full- niversities are the key

drivers of demand, accounting for the majority of full-time enrolments. In 2017, there were 59,506 full-time enrolments in

SA, including 15,360 international students.

2017 Full-time Enrolments Domestic International Total

The University of Adelaide 14,690 6,666 21,356

University of South Australia 16,150 4,705 20,855

Flinders University 13,111 3,678 16,789

Torrens University Australia 195 311 506

Total, Full-time Enrolments 44,146 15,360 59,506

Source: Department of Education & Training (uCube)

Note: Multi-modal students have been included as on-site enrolments. External (on-line) enrolments and part-time enrolments excluded

Continued growth in International Students

The number of international student enrolments in SA has continued to climb since 2012, reaching 37,965 enrolments in

2018. This is across five major sectors; Higher Education, Vocational Education and Training (VET), English Language

Intensive Courses for Overseas Students -

Preliminary enrolment data for April 2019 points to continued strong growth, particularly in the higher education and VET

sectors. Enrolment data for higher education for the year to April 2019 is 12.1% above April 2018 while enrolments for the

year to April 2019 in VET courses is 26.3% higher than April 2018.

Sector 2012 2013 2014 2015 2016 2017 2018 2019 (as at April)

Higher Education 15,192 14,733 15,449 16,314 17,519 18,806 20,686 19,218

VET 5,769 5,372 4,943 4,781 5,291 6,040 6,675 5,529

Schools 1,794 1,832 1,817 2,124 2,452 2,676 2,875 2,328

ELICOS 3,798 4,413 5,755 5,960 5,639 5,150 4,746 2,505

Non-award 1,565 1,981 2,703 2,826 3,142 2,999 2,983 1,971

Grand Total 28,118 28,331 30,667 32,005 34,043 35,671 37,965 31,551

Source: Department of Education & Training, International Enrolments released June 2019

Page 6

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Each of the main universities as well as Torrens University Australia (TUA) has reported strong growth in international

enrolments together with applications for 2019.

Who accesses Purpose Built Student Accommodation (PBSA)?

The main student groups accessing PBSA are international students enrolled at the local universities followed by

Australian university students from regional SA and interstate, who do not have family living in Adelaide.

However, students enrolled across the other education sectors are showing increased interest in PBSA, including:

• VET students

• ELICOS students

• International school students / Under-18s

Furthermore, students enrolled at suburban university campuses may choose PBSA in the CBD for its lifestyle, public

transport and access to employment. Some PBSA operators in the Adelaide CBD have indicated that these markets

account for over 20% of the student base, with marketing of their product broadening to include a wider cross-section of

the student market.

Furthermore, Chinese students are highly represented in modern PBSA. They represent the largest source group but

account for an even higher market share of international students in PBSA.

Similarly, students from more affluent Asian markets are more likely to access PBSA than students from less affluent

markets. The security offered by PBSA is an important factor, particularly for their parents.

Operators also report that students from Europe, North America and South America make up a low proportion of the

student population in PBSA.

Supply and Development Pipeline

The Table below summarises PBSA at each of the three main student markets in Adelaide.

As at Semester 1 2019, there were 4,590 beds across Inner Adelaide. This included nearly 897 beds at the five residential

colleges in North Adelaide and 3,693 beds in PBSA, primarily located in the Adelaide CBD. An additional 802 beds opened

in Semester 2 2019, including UniLodge Gray Street.

Three large projects with approval are expected to open between 2020 and 2022:

• Wee Hur Waymouth Street (787 beds). Located at 124 Waymouth Street, the site has been cleared in mid-2019.

Adelaide CBD;

• GSA North Terrace (687 beds). Located at 266-269 North Terrace. Construction has commenced. GSA is a new

market entrant to Adelaide;

• UniLodge Twin Street (510 beds). To be developed by The Hines Group. Located behind Ibis Adelaide.

By 2022, there is expected to be 7,376 student accommodation beds across Inner Adelaide.

Significantly, between 2018 and 2022, the number of new student accommodation beds in Inner Adelaide will have grown

by more than 4,200, providing a significant boost to the inner city population and businesses. The development value

alone of the eight new projects to be completed between 2018 and 2022 in the Adelaide CBD is $525 million.

By comparison, Mawson Lakes and Bedford Park have limited student accommodation. Additional PBSA to serve Flinders

University is proposed at Tonsley and in Flinders Village Bedford Park, although timing of this accommodation has yet to

be announced.

Existing Supply, New Supply, Pipeline,

Main Universities Total, 2022

Sem-1 2019 Sem-2 2019 2020-22

Inner Adelaide Adelaide; UniSA 4,590 802 1,984 7,376

Mawson Lakes UniSA Mawson Lakes 300 - - 300

Bedford Park / Tonsley Flinders University 529 - - 529

Total 5,419 802 1,984 8,205

Source: JLL

Page 7

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Pricing

Pricing for catered student accommodation in a private single room averages approximately $500 per week based on a

40-week university year.

Pricing for self-catered accommodation varies significantly based on the quality of accommodation and format. Modern

PBSA in the Adelaide CBD ranges from less than $300 per week for twin share accommodation to around $450 per week

for a large studio with ensuite. Starting prices are approximately $200 per week. Pricing includes utilities and Internet.

The private rental market provides an alternative to PBSA. With market penetration rates in PBSA of around 20% for

international university students (and lower in suburban locations), the majority of international students are accessing

private rental accommodation.

Median rents for apartments in Adelaide are competitive compared with PBSA pricing, particularly when students share

a two or three bedroom apartment. However, most PBSA provides a range of inclusions that are not typically provided in

the private rental market. These include:

• Fully furnished rooms / apartments

• Utilities and Internet

• Common areas available for the use of students, featuring recreation facilities, kitchens, study rooms etc.

• On-site staff / security

Occupancy Rates

Discussions with market operators suggest that the Adelaide PBSA market is operating at 85%-95% occupancy, which

suggests a reasonably balanced market with current supply meeting demand. Some new PBSA is yet to reach a stabilised

level of occupancy with improved occupancy levels expected over the next 12 months.

Operators of PBSA

Adelaide has attracted many of the large private owners and operators of PBSA including Urbanest, Atira, GSA and Wee

Hur.

The two main operating models for PBSA in Australia are the Owner-Operator Model and the Third Party Operator Model:

• Owner Operator Model: The recent wav

-one-

• Third Party Operator Model: For developers and investors who do not have an affiliated operational arm, a

third party operator is appointed. UniLodge is the largest established operator and offers an end-to-end model

for investors (from purchase to selling) with a dedicated property management model.

Supply - Demand Balance

The balance between supply of student accommodation and demand in 2019 is summarised below. The number of full-

time students per bed in the Adelaide CBD is lower than both Mawson Lakes and Bedford Park.

Full-time Student

Adelaide CBD Uni SA Mawson Lakes Flinders University

Enrolments, 2019

Student Profile

Domestic Students 24,963 1,794 12,713

International Students 12,311 1,556 4,492

Total Students 37,274 3,350 17,204

Accommodation Supply

Total Rooms 5,402 300 529

FT Students Per Bed 6.9 11.2 32.5

Source: Department of Education and Training, JLL

Page 8

The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Forecasts

Forecasts have been undertaken under two scenarios for each of the following locations:

• Inner Adelaide

• Mawson Lakes

• Bedford Park / Tonsley

Scenario 1 provides a base case, based largely on the existing proportion of full-time university students who are choosing

PBSA in inner Adelaide and suburban markets. Scenario 2 allows for realistic growth in market share over time.

The forecasts assume the international student market reaches 71,000 enrolments by 2030.

Beds Needed

Market Scenario Assumptions 2020 2025 2030

International Student Market Share: 20%

Domestic Market Share: 4.5%

Inner Adelaide Scenario 1 -633 -1,633 -584

Vacancy rate:7.5%

Students from beyond local universities: 15%

International Student Market Share: 20% rising to 30%

Domestic Market Share: 4.5% rising to 5.0%

Scenario 2 -278 77 2,548

Vacancy rate:7.5%

Students from beyond local universities: 15% rising to 20%

International Student Market Share: 10%

Domestic Market Share: 2.5%

Bedford Park / Tonsley Scenario 1 317 452 621

Vacancy rate:7.5%

Students from beyond local universities: 2%

International Student Market Share: 10% rising to 20%

Domestic Market Share: 2.5%

Scenario 2 365 816 1,389

Vacancy rate:7.5%

Students from beyond local universities: 2%

International Student Market Share: 15%

Domestic Market Share: 2%

Mawson Lakes Scenario 1 1 68 153

Vacancy rate:7.5%

Students from beyond local universities: 2%

International Student Market Share: 15% rising to 20%

Domestic Market Share: 2%

Scenario 2 18 173 286

Vacancy rate:7.5%

Students from beyond local universities: 2%

Source: JLL

Inner Adelaide Forecasts

• Under Scenario 1, the strong pipeline through to 2022 will provide sufficient capacity to accommodate strong

growth in international student enrolments, at least through to 2025.

• Under Scenario 2, 2,548 beds may be required by 2030. This is in addition to major approved projects that are

expected to be completed by 2022. This assumes 30% of full-time international students choose PBSA and

20% of the student base comes from outside the local universities.

Bedford Park / Tonsley

• Under Scenario 1, an additional 621 beds of PBSA will be required by 2030 based on growth in the student

population at Flinders University;

• Under Scenario 2, an additional 1,389 beds will be required by 2030. This assumes 20% of local full-time

international students choose PBSA at Flinders University.

Mawson Lakes Forecasts

• Under Scenario 1, an additional 153 beds of PBSA will be required by 2030 based on growth in the student

population at the Mawson Lakes campus of UniSA;

• Under Scenario 2, an additional 286 beds will be required by 2030. This assumes 20% of local full-time

international students choose PBSA at the Mawson Lakes campus of UniSA.

Page 9The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Introduction

The Department for Trade, Tourism and Investment (DTTI) has engaged JLL to undertake a detailed demand and supply

The SA Government has set an ambitious economic growth target of 3% growth in Gross State Product annually. It has

identified five key areas of focus to facilitate this growth including an improved business climate, government, overseas

engagement, investment and infrastructure.

International education is a major contributor to the s

largest general export worth $1.807 billion in 2018, supporting over 12,500 full-time equivalent (FTE) jobs.1 International

performance as an export, a mechanism for population

growth, a supplier of skills for growth industries and as a source of investment attraction.

SA Government has worked closely with the international education sector both directly and through the Ministerial

Advisory Committee for International Education, to set a new industry led target for growth. By 2030, international

education is targeted to grow to 71,000 international student enrolments, contributing $3.0 billion per year

economy, and supporting around 21,000 FTE jobs.

To achieve these targets, new investment will be required in student accommodation.

This report provides analysis of the student

universities and attracts the vast majority of s international student community. The future demand for student

accommodation in Adelaide is based on the state government growth targets together with recent trends in international

student growth.

JLL previously undertook a study on behalf of the Department of State Development in 2016. This report updates the

findings of the previous study.

The focus of this study is purpose-built student accommodation (PBSA) that is generally occupied by international

students in the Adelaide CBD and inner suburban region,

university campuses, being Mawson Lakes (UniSA Mawson Lakes campus) and Bedford Park / Clovelly Park (Flinders

University).

It should be noted that domestic students also create demand for student accommodation, particularly students from

country regions of SA or interstate, who cannot live at home and attend university in Adelaide. Demand from this sector

of the student market is also taken into account when determining the overall demand for new PBSA to support the future

student population.

1

ABS (Cat 5368.0.55.004); www.internationaleducation.gov.au

Page 10The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Adelaide Overview

2.1 Overview

Greater Adelaide is the capital city of SA and is the fifth largest city in Australia, with a population of circa 1.355 million as

at June 2019 (77.5% of SA The Adelaide Central Business District (CBD) is the heart of SA

commercial sectors bounded by North, East, South and West Terrace.

The main education precinct is located within the Adelaide CBD and fronting North Terrace. Within this precinct are the

University of Adelaide, the City West and City East campuses of the University of South Australia (UniSA), TAFE SA, a

number of colleges and other educational providers.

Existing student accommodation serving CBD-based education providers is located within the Adelaide CBD and North

Adelaide. However, not all of the existing accommodation is purpose built and varies significantly in quality of

accommodation and services. Accommodation in North Adelaide is primarily residential colleges, affiliated with religious

organisations, and provides catered accommodation targeting the domestic market. Accommodation in the Adelaide

CBD is typically self-catered accommodation and has been developed more recently by private PBSA operators. This

accommodation primarily targets the international student market.

Outside the CBD, UniSA has a campus in the Mawson Lakes area 15 kilometres north of the CBD and a small campus at

Magill, approximately 7km east of the CBD. Flinders University s located at Bedford Park, 12 kilometres

south of the CBD with a smaller campus at the adjoining Tonsley Innovation District.

The following map identifies the agreed study areas for this report within Adelaide.

Figure 1: Location Map

Source: Google Maps

Page 11The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

2.2 Demographics

Table 1 and 2 provides a comparison of the City of Adelaide (including North Adelaide and the Adelaide CBD) to the

Greater Adelaide Metropolitan Region. This is as at the 2016 Census.

The data highlights the following:

• The high proportion of young adults in Adelaide (C), highlighting the very large student population

• High proportion of Asian born residents, predominantly international students from markets such as China,

India and Nepal studying in Adelaide

• 27% of residents in Adelaide (C) attend university or other tertiary institutions. A further 11.6% of residents were

undertaking some form of education (but institution not stated), suggesting an even higher proportion of

residents in Adelaide (C) would be attending university

• Dominance of the rental market in Adelaide (C), with many renters anecdotally being students

Table 1: Selected Characteristics of Residents, City of Adelaide LGA and Greater Adelaide, 2016

Selected Characteristic Adelaide (C) LGA Greater Adelaide

Estimated Resident Population, 2016 23,400 1,326,400

Age Distribution

0-4 years 2.3% 5.9%

5-14 years 3.2% 11.6%

15-19 years 7.2% 6.1%

20-24 years 21.3% 6.9%

25-34 years 23.6% 13.8%

35-44 years 10.8% 12.9%

45-54 years 9.7% 13.4%

55-64 years 9.0% 12.2%

65 years & over 13.0% 17.2%

Birthplace

Australia 45.5% 68.2%

UK & Ireland 5.0% 7.5%

Europe 2.6% 4.0%

Asia 28.7% 9.8%

New Zealand 1.0% 0.8%

Other 7.1% 4.2%

Not stated 10.2% 5.4%

Education Attending

Pre school 0.5% 1.2%

Primary 2.3% 8.5%

Secondary 1.9% 5.6%

TAFE 2.3% 2.0%

University / Other tertiary 27.0% 5.7%

Other 1.1% 0.8%

Not stated 11.6% 5.7%

Total - Attending Education 46.6% 29.5%

Housing Status

Owner 21.1% 31.4%

Purchaser 17.7% 37.4%

Renter 60.2% 29.6%

Other 1.0% 1.6%

Source: JLL, Australian Bureau of Statistics 2016 Census

Page 12The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Table 2: Selected Medians, City of Adelaide LGA and Greater Adelaide, 2016

Selected Medians Adelaide (C) LGA Greater Adelaide

Median age of persons 30 39

Median mortgage repayment ($/monthly) 1,733 1,517

Median total personal income ($/weekly) 553 617

Median rent ($/weekly) 375 285

Median total family income ($/weekly) 2,026 1,591

Average number of persons per bedroom 0.9 0.8

Median total hhold income ($/weekly) 1,266 1,265

Average household size 1.9 2.5

Source: JLL, Australian Bureau of Statistics 2016 Census

2.3 Adelaide Student Demographics Summary

The number of international student enrolments in SA has continued to climb since 2012, reaching 37,965 enrolments in

2018. This comprised 20,686 higher education students with the balance made up of students enrolled in other education

sectors such as Vocational Education and Training (VET), English Language Intensive Courses for Overseas Students

(ELICOS), schools and non-award courses.

Preliminary enrolment data is available up to April 2019, which highlights that very strong growth has continued into 2019.

Year to April 2019 enrolments, which would account for the vast majority of students enrolled in the first semester of the

academic year, were 12.1% higher than the corresponding period in 2018. Higher education enrolments had already

reached 19,218 by April 2019. Based on growth in enrolments between April 2018 and April 2019, total enrolments for the

2019 calendar year should reach around 42,600 international student enrolments, with 23,500 being higher education

enrolments.

There has also been very strong growth experienced in the VET sector. Enrolments to April 2019 had already reached over

5,500, which is 26.3% higher than the corresponding period in 2018. Should this trend continue, VET enrolments in 2018

will reach over 8,400 for the 2019 calendar year.

The majority of higher education students study at the three main Adelaide-based universities: The University of Adelaide,

Flinders University and UniSA. The rest of the student population study at other private providers of higher education,

including a range of colleges and institutes. While there are small campuses of both the University of Adelaide and UniSA

outside of Adelaide, these do not attract large student numbers, with the vast majority of international students to SA

being Adelaide-based.

Table 3: Summary of International Student Enrolments in SA, 2012-2019*

Sector 2012 2013 2014 2015 2016 2017 2018 2019 (as at April)

Higher Education 15,192 14,733 15,449 16,314 17,519 18,806 20,686 19,218

VET 5,769 5,372 4,943 4,781 5,291 6,040 6,675 5,529

Schools 1,794 1,832 1,817 2,124 2,452 2,676 2,875 2,328

ELICOS 3,798 4,413 5,755 5,960 5,639 5,150 4,746 2,505

Non-award 1,565 1,981 2,703 2,826 3,142 2,999 2,983 1,971

Grand Total 28,118 28,331 30,667 32,005 34,043 35,671 37,965 31,551

Source: Department of Education & Training

* 2019 enrolment data is for year to April-19. April-19 data is 12.1% higher than April-18 data, indicating strong year-on-year growth

The strong growth in Higher Education students is expected to continue, with ambitious plans in place by the key

institutions:

• On-campus international student enrolments at the University of Adelaide is expected to rise from 7,877 in

2018 to over 10,000 in 2019.

• International student enrolments at Flinders University has increased from under 5,000 in 2017 to 5,400 in

2018, and is expected to reach around 6,000 enrolments in 2019.

• UniSA has experienced modest growth in its international student enrolments, growing from 5,400 in 2017 to

5,700 in 2018, with an estimated 6,000 enrolments in 2019.

Page 13The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

SA provides a range of benefits for international graduates from SA-based institutions, via its skilled visa pathways. This

supports the growth in international students deciding to study in the State. The key benefits of studying in SA include:

• Access to a more extensive occupation list for graduates planning to undertake post-study work;

• A eral Skilled Migration (GSM) points test by

choosing SA;

• An extra year of post-study work in SA for graduates who have maintained residence in SA;

• Flexible state nomination requirements for international graduates of SA, including incentives for long-term

residents of SA such as work experience and English language and financial capacity waivers for eligible

international graduates

• Priority processing of applications with the Department of Home Affairs. Adelaide is by far the largest

Australian city eligible for priority processing arrangements

Similarly, the international VET sector has also shown strong recent growth.

The following table provides the number of full-time, on-site students studying at higher education institutions in SA. We

note that each university has multiple campuses but the vast majority of enrolments are within Greater Adelaide. Higher

education students remain the main market for PBSA. Enrolment data by university is currently available for 2017 from

the Australian Governmen .

Total full-time on-site enrolments in the four main universities in SA was 59,506 in 2017, including 15,360 international

enrolments. The number of full-time international enrolments in SA is estimated to have grown to between 18,500 and

19,000 in 2019.

Table 4: Full Time, On-site Student Enrolments in SA, 2017

2017 Full-time Enrolments Domestic International Total

The University of Adelaide 14,690 6,666 21,356

University of South Australia 16,150 4,705 20,855

Flinders University 13,111 3,678 16,789

Torrens University Australia* 195 311 506

Total, Full-time Enrolments 44,146 15,360 59,506

Source: Department of Education & Training (uCube), Torrens University Australia

Note: Multi-modal students have been included as on-site enrolments. External (on-line) enrolments and part-time enrolments excluded

* Estimated enrolments based at Adelaide campus

Page 14The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

South Australian Universities Overview

This section provides an overview of the main universities serving SA. Our focus is on the main campuses of each

university in the Greater Adelaide region.

3.1 The University of Adelaide

The University of Adelaide is a highly regarded

tertiary education and research institution, being

ranked 106th in the world in the 2020 QS World

Eight (G8) a coalition of leading universities.

The university was established in 1874 and is the

oldest university in SA.

The University of Adelaide is ranked in the top 1% in

the world in 11 research fields. It has major strengths

in many science subjects including environmental

sciences and social sciences.

The University of Adelaide has its main campus on North Terrace and three other regional campuses. The following

statistics highlight the University of Adelaide student demographics as at 2017.

• International / domestic 28% / 72% • On campus / multi-modal / 95.6% / 2.9% / 1.5%

students off campus students

• Domestic undergraduate / 81% / 19% • Domestic full-time / 77% / 33%

postgraduate students domestic part-time students

• International undergraduate / 51% / 49% • International full-time / 88% / 12%

postgraduate students international part-time

students

The University of Adelaide has the largest percentage of international

also dominated by on-campus students (96% of student enrolments) and full-time students.

Table 5 shows the number of domestic and international students enrolled into the University of Adelaide and split

between mode of attendance (internal, external and multi-modal), type of attendance (full/part-time) and course level

(undergraduate, postgraduate, non-award/enabling courses). There is a relatively even split between postgraduate and

undergraduate international students.

Page 15The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Table 5: The University of Adelaide, Number of Student Enrolments, 2017

Internal Multi-modal External Total

Full- Part- Full- Part- Full- Part- Full- Part-

time time time time time time time time Total

Domestic

Postgraduate 1,614 1,468 117 99 57 306 1,788 1,873 3,661

Undergraduate 12,437 2,522 446 17 12,883 2,539 15,422

Non-Award / Enabling 76 100 76 100 176

Total 14,127 4,090 563 116 57 309 14,747 4,515 19,262

International

Postgraduate 3,077 505 51 9 14 30 3,142 544 3,686

Undergraduate 3,451 309 36 3,487 309 3,796

Non-Award / Enabling 49 38 2 51 38 89

Total 6,577 852 89 9 14 30 6,680 891 7,571

Total 20,704 4,942 652 125 71 339 21,427 5,406 26,833

Source: Department of Education and Training (uCube)

The University of Adelaide North Terrace Campus

Location and Facilities

main campus is located on North Terrace, within Adelaide CBD, between Frome Road and

Kintore Avenue. However, with the completion of the AHMS building (see below), its North Terrace presence now extends

further west. North Terrace is home to over 90% of the uni . Areas of focus are the Schools of

Engineering, Computer and Mathematical Sciences, Health Science, Arts, Business and Sciences. The campus also

provides Medical and Dental Schools providing a strong focus on practice-based learning to students.

The University of Adelaide allows students, staff and visitors to easily access the university via public

transport.

The university has a range of facilities such as sporting facilities in the nearby Parklands, a fitness hub, post office, library,

theatres, as well as cafes.

Strategic Plan Future Making

connected to the global world of

ideas, a magnet for talent, research that shapes the future, a 21 century education for a growing community of learners,

st

and the beating heart of Adelaide. The Plan aims to grow and diversify its student cohort, increasing its international

enrolments significantly, attracted to the university by its international reputation and standing. Part of the growth

strategy is through long-term partnerships with international universities, which will see domestic students studying

abroad as well as international students undertaking part of their degree in Australia.

Infrastructure Projects and Masterplan 2016-2035

The University of Adelaide has a strong focus on its Adelaide CBD campus, with this campus accounting for well over 90%

of its on-site enrolments.

Over the last five years, the university has invested over $500 million in major capital works, including the construction of

the University of Adelaide Health and Medical Sciences building (AHMS), its new home of medical education. The building

is situated in the heart of the new Adelaide BioMed City on North Terrace alongside the Royal Adelaide Hospital and South

Australian Health and Medical Research Institute (SAHMRI). The AHMS houses approximately 1,700 students and 600

health researchers over its 14 floors, and includes laboratories, lecture theatres, advanced simulation suites, a dental

hospital, a clinical research facility and social / study spaces.

The Campus Masterplan 2016-2035 provides guidance for the ongoing development of the universi puses

North Terrace, Waite and Roseworthy

creating a campus that is connected to the rest of the Adelaide CBD.

Page 16The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

Enrolments by Campus

Most University of Adelaide students are enrolled at its North Terrace campus, which includes students at the new

medical precinct. The North Terrace campus accounts for 96% of student enrolments. It is noted that some students

attend more than one campus, which explains that total enrolments are less than the sum of enrolments at each campus.

International enrolments at the North Terrace campus account for 29% of enrolments.

Table 6: The University of Adelaide, 2018 Enrolments by Campus

Total

Campus Domestic International Total Enrolments % Total

North Terrace 18,399 7,611 26,010 25,997 96%

Roseworthy 711 74 785 785 3%

Waite 594 274 868 868 3%

Other 931 219 74 1,150 4%

Total Enrolments n.a. n.a. n.a. 27,062

Source: The University of Adelaide

t have changed

their citizenship status during the year.

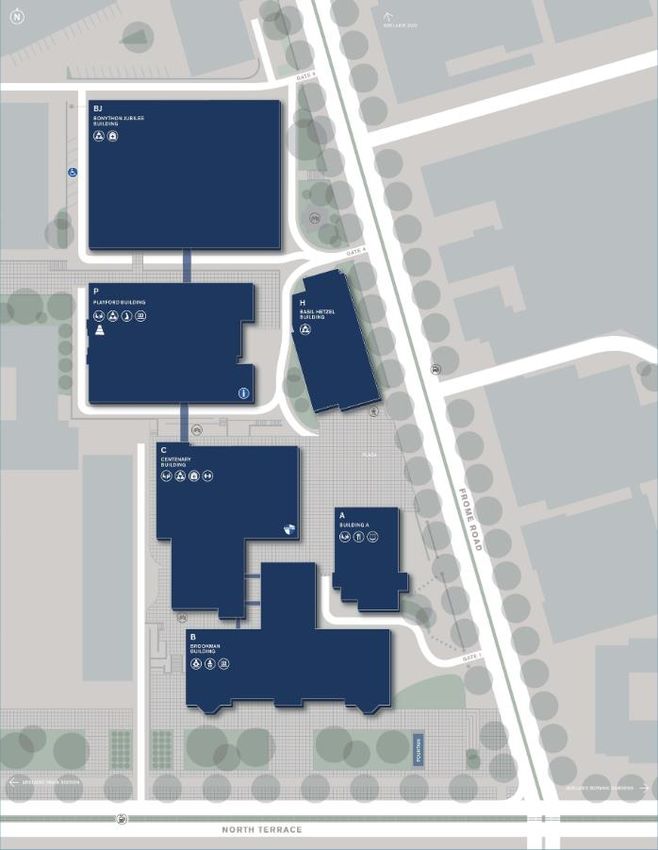

Figure 2: The University of Adelaide North Terrace Campus Map

Source: University of Adelaide

Page 17The Government of South Australia - Department for Trade, Tourism and Investment: Adelaide Student Accommodation Demand and Supply Analysis

3.2 Flinders University

Flinders University was established in 1966 and has its main

campus at Bedford Park (which is approximately 12 km from

university has a new campus at nearby

Tonsley, a smaller campus at 182 Victoria Square within

Flinders University has a strong focus on research, and was

the first university in the world to have a bachelor course in

nanotechnology. It was also the first university in Australia to

offer a graduate entry medical course.

The following statistics highlight the Flinders University student demographics as at 2017.

• International / domestic 19% / 81% • On campus / multi-modal / 78% / 9% / 13%

students off campus students

• Domestic undergraduate / 70% / 30% • Domestic full-time / domestic 66% / 34%

postgraduate students part-time students

• International undergraduate 30% / 70% • International full-time / 78% / 22%

/ postgraduate students international part-time

students

Flinders University attracts a relatively high proportion of postgraduate international students compared with both UniSA

and Adelaide.

Table 7 shows the number of domestic and international students enrolled in Flinders University and split between mode

of attendance (internal, external and multi-modal), type of attendance (full/part-time) and course level (undergraduate,

postgraduate, non-award/enabling courses).

Table 7: Flinders University, Number of Student Enrolments, 2017

Internal Multi-modal External Total

Full- Part- Full- Part- Full- Part- Full- Part-

time time time time time time time time Total

Domestic

Postgraduate 1,393 840 412 317 430 2,495 2,235 3,652 5,887

Undergraduate 9,734 2,753 988 218 85 246 10,807 3,217 14,024

Non-Award / Enabling 584 65 584 65 649

Total 11,711 3,658 1,400 535 518 2,746 13,629 6,939 20,568

International

Postgraduate 2,119 835 301 10 9 28 2,429 873 3,302

Undergraduate 1,189 170 57 3 2 1,246 175 1,421

Non-Award / Enabling 12 12 - 12

Total 3,320 1,005 358 13 9 30 3,687 1,048 4,735

Total 15,031 4,663 1,758 548 527 2,776 17,316 7,987 25,303

Source: Department of Education and Training (uCube)

Page 18You can also read