ALUMINUM ASSOCIATION: CARES ACT STIMULUS PACKAGE BRIEFING - April 9, 2020 - The ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ALUMINUM ASSOCIATION: CARES ACT STIMULUS PACKAGE BRIEFING April 9, 2020

BRIEFING: CARES ACT STIMULUS PACKAGE

Speakers

Tom Dobbins Jon Talcott E. Peter Strand

President & CEO Partner Partner

The Aluminum Association Nelson Mullins Nelson Mullins

tdobbins@aluminum.org jon.talcott@nelsonmullins.com peter.strand@nelsonmullins.com

Lauren Wilk Curt Wells Ryan Olsen

Vice President, Policy & Senior Director, Regulatory Vice President, Business Information &

International Trade Affairs Statistics

The Aluminum Association The Aluminum Association The Aluminum Association

lwilk@aluminum.org cwells@aluminum.org rolsen@aluminum.org

More Information

• Find up-to-date information and resources: www.aluminum.org/covid19

• Take action: p2a.co/aluminum

CARES Act Stimulus Package:

Summary of Loan Programs

Nelson Mullins Riley & Scarborough LLP

Jon Talcott

Peter StrandContact Information

Jon Talcott E. Peter Strand

Partner Partner

Washington, D.C. Washington, D.C.

(202) 689-2806 (202) 689-2983

(202) 460-2197 (mobile) (503) 569-7930 (mobile)

jon.talcott@nelsonmullins.com peter.strand@nelsonmullins.com

4Agenda

I. Summary of SBA Relief Programs

II. Paycheck Protection Program

III. Emergency Economic Injury Disaster Loans

IV. Title IV Loans – Mid-Sized Businesses/Main Street Lending Facility

V. Other Federal Reserve Programs

5I. Summary of SBA Relief Programs in

the Stimulus Package

6Summary

Three SBA Relief Programs in the Stimulus Package:

1. Paycheck Protection Program—

o $349 billion for eligible businesses (generally under 500 employees) to be provided under SBA’s 7(a) loan

program. Loans are 100% government guaranteed, up to $10 million based on businesses’ payroll, 2 year term

at 1%. Loan forgiveness available.

2. Emergency Economic Injury Disaster Loans (EIDLs)—

o $10 billion additional funding for EIDLs under the SBA’s Section 7(b)(2) emergency lending program. CARES Act

also waives certain EIDL requirements, such as personal guarantee and collateral requirements, and relaxes

and fast-tracks the application process.

3. Relief for certain existing SBA loans—

o The CARES Act permits the SBA to pay the principal, interest and fees on these loans for six months beginning

with the next payment due date. Loans already on deferment will receive six months of payment after the

deferral period. SBA will also encourage lenders to provide deferments and will allow lenders, for up to one

year, to extend the maturity of SBA loans in deferment beyond current limits.

7II. Paycheck Protection Program

8Paycheck Protection Program

• $349 billion

• Generally available to companies with 500 or fewer employees

o Important to consider affiliation rules

• Loans approximately equal to lesser of 10 weeks’ payroll or $10 million

• Loan forgiveness available for up to entire principal amount, subject to

reduction for workforce and wage/salary reductions

9PPP – Considerations

• Who is eligible?

• How much can you borrow?

• How much loan forgiveness is available?

• What are the permitted uses?

• Other details

• How do you apply?

10PPP – Who is eligible?

• Are you a business located in the U.S. and which operates primarily within the U.S. or makes a significant contribution to the U.S. economy through

payment of taxes or use of American products, material or labor that was in operation since February 15, 2020?

o Ineligible persons and businesses:

• Household employer • Businesses that have defaulted on SBA or federal loans and • A business whose owner is incarcerated, on probation or

• Financial business in the business of lending (such as caused a loss to the government in the last 7 years parole, subject to an indictment, criminal information,

banks) • Certain casinos or gambling businesses arraignment or has been convicted of a felony in the last 5

• Certain passive businesses owned by developers and • Private clubs or businesses that limit the number of years

landlords that do not actively use or occupy the assets memberships for reasons other than capacity • Debarred or declared ineligible from the PPP

• Life insurance companies • Government owned entities • Presently involved in a bankruptcy

• Businesses located in a foreign country • Businesses principally engaged in teaching, instructing, • Business that present live performances of a prurient

• Pyramid sales distribution plans counseling or indoctrinating religion or religious beliefs sexual nature

• Businesses primarily engaged in political or lobbying • Loan packagers deriving more than 1/3 of revenue from • Speculative businesses (such as oil wildcatting)

activities SBA loans

• Businesses engaged in illegal activity

• Are you below the size thresholds for eligibility?

o 500 or fewer employees (or such larger amount of employees if set forth in the SBA size standards)

▪ You must include affiliated companies’ employees in this calculation

o Hotel and restaurant industry, franchises listed in the SBA directory, and companies receiving financial assistance from an SBIC are exempt

from affiliation rules.

▪ For hotels and restaurants, it is 500 or fewer employees per physical location.

o Also available for traditional “small businesses” under the existing SBA size standards.

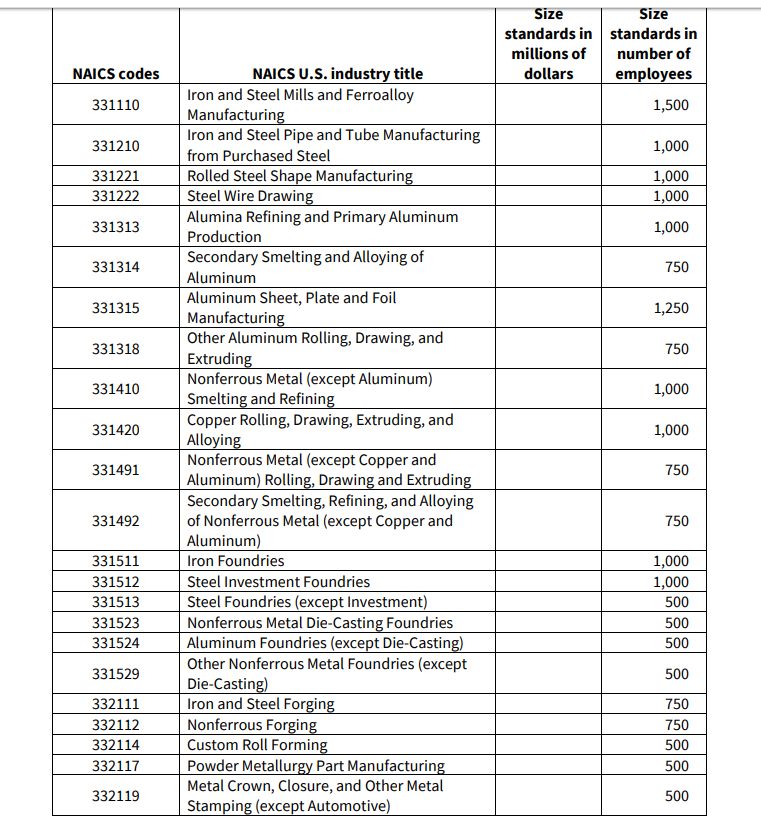

11PPP – Size Thresholds (Example)

• Some industries may have more than 500 employees based on SBA size standards:

12PPP – Affiliate Issues

• Calculation of number of employees should include all affiliates (companies controlled by any person or

entity controlling the recipient)

o Definition of “Affiliate” and “Control” is a ‘totality of the circumstances’ test, and the SBA generally takes

an expansive view of what constitutes control.

o Hotels and restaurants, certain franchises designated by the SBA, and companies that receive SBIC

funding are exempt from affiliation rules and do not need to aggregate employees.

o Private Equity or Venture Capital often problematic

• Affiliate determination is done on an entity by entity (or investor by investor) basis.

o Affiliation determined by control (i.e., when one entity controls another, or two or more entities

are controlled by a third party).

o Most common control factors: 50% or more of voting stock or negative controls, such as veto rights

that affect normal operation of the business.

▪ Minority shareholders with control factors may waive or disclaim the control and avoid affiliate

issues.

13PPP – How much can you borrow?

• Lesser of $10 million or 2.5x average total “Payroll Costs”:

monthly payments of payroll costs during 1- • Gross salary, wage, commission or similar compensation;

year period prior to date loan is made* • Payment of cash tips or equivalent;

o You can use rolling 12 months or calendar • Payment of vacation, parental, family, medical or sick leave;

year 2019 • Allowance for dismissal or separation;

• Payment required for the provision of group health care

• You can also borrow the amount of any 7(b)(2) benefits, including insurance premiums;

disaster loans borrowed between January 31, • Payment of retirement benefits; and

2020 and April 3, 2020 (subject to $10 million • Payment of state and local tax assessed on the compensation

maximum) of employees.

o If the EIDL was used towards payroll costs, Special Rules:

you MUST refinance under this provision. o Only count salary up to $100,000 (but other costs and benefits

over $100,000 may be counted).

o Do not count any compensation of an employee whose

* 12-week period ending June 30, 2019 for seasonal principal place of residence is outside of the U.S.

employers o Exclude qualified sick or FMLA leave wages for which a credit

is allowed under Families First Coronavirus Response Act.

14PPP – Loan Forgiveness

• Loan forgiveness is available for up to entire principal amount, subject to reduction based on workforce

and wage/salary reductions

o At least 75% of loan funds must be used towards payroll costs, although this requirement is not in

the CARES Act.

• Loan forgiveness amount:

o Amounts incurred or paid during first 8 weeks of loan for:

▪ Payroll costs

▪ Interest on mortgage obligations (but not principal or prepayment amounts)

▪ Rent

▪ Utilities (electricity, gas, water, transportation, telephone or internet access)

o Will be reduced proportionately to any reduction in workforce, plus reduced by any decrease in

salary/wages in excess of 25% for any employees earning less than $100,000

15PPP – Loan Forgiveness – Reduction

• Reduce the amount of forgiveness by both:

o Reduction in workforce:

▪ Divide: The average number of full-time equivalent employees per month employed during the covered period;

▪ By, at your election:

o The average number of full time equivalent employees per month employed from February 15, 2019 to June 30,

2019; or

o The average number of full time equivalent employees per month employed from January 1, 2020 to February

29, 2020.

• “Full-time equivalent” employee definition is unclear, but in the past the SBA has defined it as:

• Each employee who averages 30 hours per week counts as 1 FTE; plus

• All other employees’ hours are combined (up to 120 each), then divided by 120

o Reduction in salary/wages:

▪ The amount that total salary or wages for any employee that has decreased in excess of 25% during the covered period

as compared to the most recent full quarter during which the employee was employed before the covered period.

o Do not count any reduction of any employee that in any pay period in 2019 received wages or salary at an

annualized rate of pay more than $100,000.

• Cure provision available (see next page)

16PPP – Loan Forgiveness – Cure Provision

• Cure Provision:

o For all reduction in workforce or compensation between February 15, 2020 and April 26,

2020, you do not count such reduction against the loan forgiveness if by June 30, 2020

such reduction has been reversed.

• Example:

o Company has $6 million payroll in 2019

▪ $500,000 average payroll per month

▪ Able to borrow $1.25 million

▪ Assume payroll stays constant over next 8 weeks, that’s $1 million in forgiveness

amount

o Plus any additional amounts paid or incurred in rent, mortgage interest or utilities

▪ Subject to reduction based on workforce reductions or salary/wage reductions

17PPP – Permitted Uses

• Permitted uses of loan funds:

o Payroll costs;

o Costs related to the continuation of group health care benefits during period of paid sick,

medical or family leave, including insurance premiums;

o Salaries, commissions or similar compensations;

o Payment of interest on any existing mortgage obligations;

o Existing rent obligations;

o Utilities;

o Interest on existing debt obligations; and

o Refinancing amounts under an eligible SBA Section 7(b)(2) Disaster Loan made between

January 31, 2020 and April 3, 2020.

18PPP – Other details

• Interest equals 1%

• Two year term, with no prepayment penalty

• Administration fees are waived

• No need to demonstrate you cannot obtain credit elsewhere

• No collateral or personal guarantee required

• Deferment available for 6 months

• Loans are nonrecourse as long as used for permitted purposes

• Debt forgiveness does not count as income for tax purposes

19PPP – Next Steps

• Eligible lenders will started accepting applications for small businesses and sole

proprietorships on April 3, 2020 and will begin accepting applications for independent

contractors and self-employed individuals April 10, 2020

• Program is “first come, first served”

o Push to increase funds in next stimulus package by up to $250 billion

• Apply with current lender if possible

o Many banks are only accepting applications from existing customers

• Identify other eligible lenders:

o All current 7(a) lenders

o All insured depository institutions

o Other lenders to be determined by Treasury

o SBA website has link to find eligible lenders.

• In the meantime, consider whether a Section 7(b)(2) emergency EIDL is appropriate.

20III. Emergency Economic Injury

Disaster Loans (EIDLs)

21Emergency Economic Injury Disaster Loans

• SBA Section 7(b)(2) Emergency Economic Injury Disaster Loans (EIDLs)

• CARES Act set aside an additional $10 billion for EIDLs

• 30 year loans up to $2 million; interest rates not to exceed 4%

• Now available to small business concerns, private nonprofit organizations,

small agricultural cooperatives, and businesses with not more than 500

employees, and sole proprietors or independent contractors

• Have you suffered, or are likely to suffer, substantial economic injury as a

result of COVID-19?

22EIDLs (cont.)

• $10,000 advance available; must be paid within 3 days after SBA receives application

o Must be used for allowable purpose, including payroll, paid sick leave, cost of materials, rent or mortgage, or

other obligations that cannot be met.

o Applicant must certify they are an eligible entity

o Need not be paid back, even if subsequently denied an EIDL

• Automatic deferment through 2020

• Relaxed application and requirements

o Need not be in business for 1 year (only operational as of January 31, 2020)

o No personal guarantees for loans less than $200,000

o May grant loan based on credit score alone; no tax returns necessary

o According to SBA officials, for loans of less than $500,000, SBA will rely on certification that applicant is a small

business concern

23EIDLs (cont.)

• Applications made directly with the SBA at this link.

• A company that gets an EIDL after January 31, 2020 may be eligible to borrow

additional funds under the Paycheck Protection Program to refinance the EIDL (subject

to the $10 million cap). Check with your lender.

• 7(a) loans and 7(b)(2) loans may not be used for duplicative purposes.

24SBA Relief for Existing Loans

• Existing 7(a) loan (but not PPP loan), Section 504 loan or microloan

o SBA may pay the principal, interest and fees on these loans for six months

beginning with next payment date.

o Loans already on deferment will receive six months of payment after the deferral

period

o SBA will encourage lenders to provide deferments and will allow lenders, for up to

one year, to extend the maturity of SBA loans in deferment beyond current limits.

25IV. Title IV Loans –

Mid-sized Businesses/Main Street

Lending Facility

26Title IV Summary

• Title IV sets aside $500 billion for direct lending and other loan and guarantee

programs by the Treasury

o $25 billion for passenger airlines and related industries

o $4 billion for cargo air carriers

o $17 billion for businesses “critical to maintaining national security”

o $454 billion for lending “to provide liquidity to financial system that supports

lending to eligible business, States or municipalities”

▪ This will include Assistance for Mid-Sized Businesses (500-10,000 employees)

▪ Mnuchin says will be done through the Fed through Main Street Lending

Facility

• Subject to considerable restrictions

• Exact lending and programs are to be determined

27Title IV – Assistance to Mid-Sized Businesses

• CARES Act directs Treasury and Federal Reserve to create lending program for Mid-Sized Businesses

(500-10,000 employees)

• Section 13(3) of the Federal Reserve Act applies to these loans, including requirements relating to loan

collateralization, taxpayer protection and borrower solvency

• Mnuchin says Main Street Lending Facility will be launched this week

• Although the program has not been announced, the CARES Act does set forth certain terms and criteria:

o Interest rates less than 2%

o No principal or interest due for at least 6 months

o Loan forgiveness is prohibited

o Until one year after the date the loan is no longer outstanding, any officer or employee with 2019

total compensation of over $425,000 cannot receive increased compensation for any 12-month

period or receive severance pay or other termination benefits of more than twice his or her 2019

total compensation. Any officer or employee whose 2019 total compensation was more than

$3,000,000 cannot receive compensation greater than $3,000,000 plus 50% of the amount by

which his or her 2019 total compensation exceeded $3,000,000

o Applicants must also make significant certifications (see next slide)

28Title IV – Assistance to Mid-Sized Businesses (cont.)

• Applicants must certify

o Economic conditions make loan necessary to support ongoing operations

o Will retain 90% of workforce at full compensation until September 30, 2020

o Intends to restore at least 90% of workforce as of February 1, 2020 within 4

months of end of emergency

o Domiciled in US with significant US operations

o Not in bankruptcy

o Majority of employees in US

o No dividends or stock repurchases while loan is outstanding

o No offshoring or outsourcing jobs for 2 years after loan is outstanding

o May not abrogate collective bargaining agreement for 2 years after loan

o Neutral in union organizing for term of loan

29V. Federal Reserve Programs

30Federal Reserve Programs

• Existing Federal Reserve Programs

o Primary Market Corporate Credit Facility

o Secondary Market Corporate Credit Facility

o Term Asset-Backed Securities Loan Facility

o Money Market Mutual Fund Liquidity Facility

o Commercial Paper Funding Facility

• Newly announced Main Street Lending Facility

• CARES Act will support these programs

• To date, implemented through the Federal Reserve Bank of New York

• Other than the Primary Market Corporate Credit Facility, which provides loans to

investment grade businesses experiencing economic distress, most of these programs

appear to be aimed at stabilizing the credit markets rather than providing direct loans

to mid-sized businesses

31Main Street New Loan Facility

• Main Street New Loan Facility announced this morning

o Main Street New Loan Facility and Main Street Expanded Loan Facility (MSELF)

o Federal Reserve will purchase 95% of participations in loans (lenders retain 5%)

o Treasury will send $75 billion for the Facility and MSELF, and the combined size will

be $600 billion

• Eligible borrowers: businesses with up to 10,000 employees or up to $2.5 billion in

2019 annual revenues.

o Created or organized in the US with significant operations in the US and a majority

of employees in US.

o Borrowers may not also participate in MSELF or Primary Market Corporate Credit

Facility

• Lenders will be US insured depository institutions

• Program ends September 30, 2020 unless further extended

32Main Street Lending Facility (cont.)

• Loan Terms:

o Loans originated on or after April 8, 2020

o 4 year maturity

o Amortization of principal and interest deferred for one year

o SOFR + 250-400 basis points

o Minimum size - $1 million

o Maximum size – lesser of

▪ $25 million or

▪ An amount, when added to outstanding and committed but undrawn debt,

does not exceed 4x 2019 EBITDA

o No prepayment penalty

33Main Street Lending Facility (cont.)

• Required Attestations:

o From Lender:

▪ Proceeds will not be used to repay or refinance pre-existing loans or line of

credit made by the Lender to the Borrower

▪ Will not cancel or reduce any existing lines of credit of Borrower.

o From Borrower:

▪ Financing is required due to exigent circumstances presented by COVID-19, and

it will make reasonable efforts to maintain payroll and retain employees

▪ May not use proceeds to repay other loan balances

▪ May not repay other debt of equal or lower priority, other than mandatory

principal payment, until Main Street Loan repaid in full

▪ Will not seek to cancel or reduce any existing lines of credit

▪ Must follow statutory restrictions, such as stock repurchases and dividends

34Thank you for attending.

Visit www.nelsonmullins.com/coronavirus-resources for updates and additional resources.

35BRIEFING: CARES ACT STIMULUS PACKAGE

www.aluminum.org/signup

Aluminum Week every Friday at 8 a.m. EST

Text NATION to 52886

Virtual Spring Meeting

April 20 - 22

@AluminumNews

@DriveAluminumYou can also read