Barclays CEO Energy-Power Conference September 8, 2015 - Jeremy Thigpen President and Chief Executive Officer

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Barclays

CEO Energy-Power Conference

September 8, 2015

Jeremy Thigpen

President and Chief Executive Officer

www.deepwater.com

Legal Disclaimer

The statements described in this presentation that are not historical facts are forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements contain words such as "possible," "intend," "will," "if,"

"expect," or other similar expressions. Forward-looking statements are based on management’s current expectations and assumptions, and are subject

to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, actual results could differ materially from those

indicated in these forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to, statements

involving prospects for the company, expected revenues, capital expenditures, costs and results of operations and contingencies and other factors

discussed in the company's most recent Form 10-K for the year ended December 31, 2014 and in the company's other filings with the SEC, which are

available free of charge on the SEC's website at www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying

assumptions prove incorrect, actual results may vary materially from those indicated. All subsequent written and oral forward-looking statements

attributable to the company or to persons acting on our behalf are expressly qualified in their entirety by reference to these risks and uncertainties. You

should not place undue reliance on forward-looking statements. Each forward-looking statement speaks only as of the date of the particular statement,

and we undertake no obligation to publicly update or revise any forward-looking statements to reflect events or circumstances that occur, or which we

become aware of, after the date hereof, except as otherwise may be required by law. Adjusted earnings is a non-GAAP financial measure and the

reconciliation to the most comparative GAAP measure is displayed in quantitative schedules on the company’s website at www.deepwater.com.

This presentation is being issued pursuant to and in accordance with Rule 135 under the Securities Act of 1933. Investors must rely on their own

evaluation of Transocean Ltd. and its securities, including the merits and risks involved. Nothing contained herein is, or shall be relied on as, a promise

or representation as to the future performance of Transocean Ltd.

This presentation does not constitute an offer to sell, or a solicitation of an offer to buy, any securities, and it does not constitute an offering prospectus

within the meaning of article 652a or article 1156 of the Swiss Code of Obligations or a listing prospectus within the meaning of the listing rules of the SIX

Swiss Exchange. Investors must rely on their own evaluation of Transocean Ltd. and its securities, including the merits and risks involved. Nothing

contained herein is, or shall be relied on as, a promise or representation as to the future performance of Transocean Ltd.

www.deepwater.com 2

Recent Accomplishments

Continued improvement across key safety metrics

Revenue efficiency at or above 95% for last 5 of 6 quarters

Operational

Sustained improvements in cost structure and margins

Improvement Rationalized headcount and overhead reductions

Focus on out-of-service time and optimized maintenance programs

Cost effective stacking of UDW floaters

$18.6 billion in contract backlog

Financial $5.9 billion total liquidity at July 31, 2015

Retired ~$900 million of debt in July 2015

Flexibility

Deferred delivery of 7 newbuild rigs

BP/PSC Macondo settlement / insurance proceeds

Cancellation of dividend*

Fleet Robust pipeline of value-enhancing high-specification newbuilds

Eliminating exposure to non-core rigs

Renewal Continuing technical leadership

* Pending shareholder approval

www.deepwater.com 3

Sustained Operational Out-Performance

2Q15 adjusted earnings of $1.11/share on revenues of $1.9 billion

Revenue Efficiency Revenue, Adjusted EBITDA & Costs

Average Revenue Efficiency 95.3%

100% 3,000 70%

95% 60%

2,400

90% 50%

(US$ millions)

1,800

85% 40%

1,200

80% 30%

600

75% 20%

70% 0 10%

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Revenue Adj Costs* Adj EBITDA** Adj EBITDA Margin***

Continued progress on margin improvement initiatives partially offset deteriorating market conditions

*O&M plus G&A expenses, adjusted for unusual items **Revenue less Adjusted Costs ***Adjusted EBITDA divided by Revenue

www.deepwater.com 4

Industry Leading Execution

Focus on personal and process safety

Reducing non-productive time

Better planning, improved reliability, lower spend

Deliver more wells in record time

www.deepwater.com 5

Industry Leading Contract Backlog

Total backlog - $18.6 billion*

Chart Title

8.0

$6.8

7.0

6.0 Backlog recognized $5.7

through July 31, 2015

5.0

(US$ billions)

4.1

$3.9

4.0

3.0 $2.8

5.7

2.6

$1.9

2.0 1.4 $1.6

2.3

$2.7

0.3 0.5 1.7

1.0

1.5

0.8 0.5

0.3 0.1

0.2 0.3 0.2 0.1 0.1

0.0

2015 2016 2017 2018 2019 2020-27

*Contracted operating dayrate multiplied by the firm contract period for future periods as of the Fleet Status Report issued July 15, 2015

www.deepwater.com 6

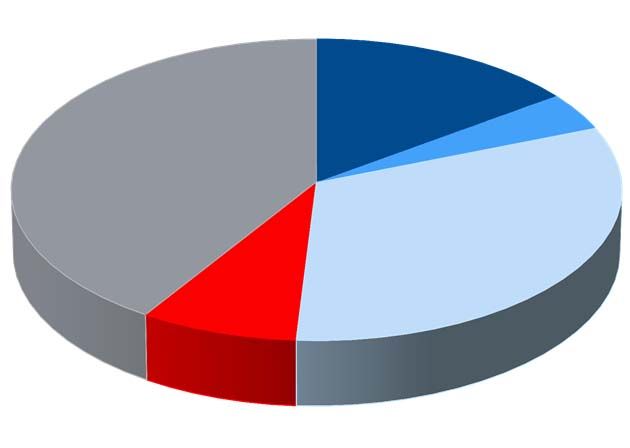

Global Market Leader

27

Ultra-Deepwater

7

Harsh Env.

6

Deepwater

13

Midwater

10

Jackup

Transocean fleet composition at August 19, 2015

www.deepwater.com 7

Challenging Market

Oil prices at post-2009 lows and rig market is oversupplied – rig fleet transformation in progress

Ultra-Deepwater Deepwater Midwater High-Spec Jackups

Deepwater Invictus Jack Bates GSF Rig 140 Transocean Honor

Global fleet utilization Global fleet utilization Global fleet utilization Global fleet utilization

86%* 72%* 76%* 84%*

Uncontracted newbuild Weakening activity with Acceleration of rig Dayrates declining as

deliveries delayed or limited prospects retirements oversupply intensifies

cancelled

* Global marketed utilization data from IHS-Petrodata as of August 25, 2015

www.deepwater.com 8

Future Imbalance From Depressed Oil Prices

$50 oil: supply and demand could be in balance in 2015, incremental demand incremental supply @ $70/bbl

but supply destruction in out-years is unsustainable mmb/d incremental supply @ $90/bbl incremental supply @ $50/bbl

2.0

$70 oil: continued reinvestment keeps market from

balancing until 2016-2017, but 2017+ undersupplied 1.0

$90 oil: longer-term price required to balance incremental 0.0

supply/demand

Approximately 30% of the potential 8mmb/d 2018 deficit -1.0

comes from deepwater sources

-2.0

Please note, this is not intended to be a commodity price forecast, merely a sensitivity analysis.

-3.0

Oil supply @ $50/bbl Oil supply @ $70/bbl

13 14 15E 16E 17E 18E

mmb/d Oil supply @ $90/bbl Total oil demand

mmb/d

98

0 -0.5 -0.2 -0.7

-0.7

96 -1.8

-1.5 -1.5

-2

94

-2.6 -2.5

92 -4

Other Onshore

Shelf

90 -6

Deepwater -3.6

88 -8 NAm Shale

86

12 13 14 15E 16E 17E 18E -10

Source: Rystad Energy, EIA, IEA, Morgan Stanley Research estimates

15E 16E 17E 18E

www.deepwater.com 9

Future Demand Requires Offshore Development

~50% of incremental new field production growth

through 2020 is related to non-OPEC offshore

Crude & Condensate Production (mmb/d) development

85

Chart Title

Non-Producing Fields Producing Fields

2.0 RoW Onshore

80

6.0 RoW Offshore

75

2.2 OPEC

1.2 NAm Land

70

Currently-producing NAm

65 unconventional fields need to add

~7mmb/d* in incremental production

to offset base decline and grow

production

60

00 03 06 09 12 15 18

Source: Rystad Energy, Morgan Stanley Research estimates *~7mmb/d = ~3.3mmb/d to offset declines + ~3.5mmb/d in net additions

www.deepwater.com 10Rig Attrition Key to Rebalance the Market

Marketed Utilization (average last 12 months)

Contract Status & Expected Demand 2005-2017 7500’+ 92.6%

All Floaters - Worldwide

4500’-7500’ 85.5%Investing in the Fleet – High Specification Assets

18 Newbuilds Added 2009-2014 12 Newbuilds in Pipeline 2016-2020

11 UDW Drillships 7 UDW Drillships

3 UDW Semisubmersibles 5 HS Jackups

4 HS Jackups

~$12B Investment ~$7B Investment

www.deepwater.com 12Asset Profile

2009 Fleet Current Fleet 2020 Projected Fleet*

% of Fleet % of Fleet % of Fleet

15% 16%

4% 24%

41% 43%

10% 55%

30%

32%

8% 11%

11%

Projected fleet includes:

11 UDW dual BOP rigs

8 UDW moored & DP capable rigs

Ultra-Deepwater Floaters

7 UDW 20k psi capable rigs

Harsh Environment Floaters

Average fleet age:

Deepwater & Midwater Floaters

2020 ~16 years*

High-Specification Jackups

Standard Jackups

2015 ~19 years

2009 ~24 years

* Estimate August 2015

www.deepwater.com 13Strong Financial Position

$18.6 billion backlog provides solid cash-generation foundation

$5.9 billion total liquidity at July 31, 2015

$2.9 billion cash

o Includes July 2015 redemption of 4.95% senior notes

$3.0 billion undrawn revolving credit facility

Re-phasing/reduction of capital spending

Continuous improvement in operating performance and costs

Cost effective stacking

www.deepwater.com 14Substantial Liquidity

12 Projected liquidity at

11 December 31, 2017

$3.7-$4.7B* ~$3.7B*

10

9

8

7

(US$ billions)

$1.9B

$3.0B

6

5 $4.0-$5.0B*

4

$2.9B

3

2

1

0

Cash at 7/31/15 Revolving Credit Operations Cash CapEx through Debt Due through Liquidity

Facility Flow 2017 2017 at 12/31/17

* Estimate

www.deepwater.com 15The Path Forward

Transocean will:

Deliver the safest, most efficient drilling services

Continue to focus on producing strong operating results through:

o Strengthening customer relationships

o Delivering best-in-class uptime and revenue efficiency

o Right-sizing the organization consistent with fleet size

o Streamlining every element of the business

Actively manage capital structure and liquidity

High grade and reposition the worldwide fleet for the industry recovery

Transocean will build upon its position as the industry’s leading offshore driller

www.deepwater.com 16Barclays

CEO Energy-Power Conference

September 8, 2015

Jeremy Thigpen

President and Chief Executive Officer

www.deepwater.comYou can also read