Brexit: An overview of the direct and indirect tax implications - Please disable pop-up blocking software before viewing this webcast - Grant ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Please disable pop-up

blocking software before

viewing this webcast

Brexit: An overview of the

direct and indirect

tax implications

September 24, 2019

12:00PM – 1:30PM ET

Speakers

David Sites Imran Khan Matt Stringer

Head of International Tax Transfer Pricing, Partner Head of International Tax

Grant Thornton US Grant Thornton UK Grant Thornton UK

Adam Jackson Karen Robb

Head of Brexit & Political Risk Advisory Indirect Tax, Partner

Grant Thornton UK Grant Thornton UK

© 2019 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 2

Learning objectives

Define what the current political climate is surrounding

1 Brexit, including how we got here, what the current

landscape looks like and what the future holds.

Identify the anticipated direct tax implications and how

2 this fits together with the wider international tax

landscape.

3 Identify the anticipated indirect tax implications.

4 Identify transfer pricing implications.

© Grant Thornton LLP. All rights reserved. 3

Brexit An overview Adam Jackson Head of Brexit and Political Risk Advisory E: Adam.E.Jackson@uk.gt.com Twitter: @Adam_E_Jackson

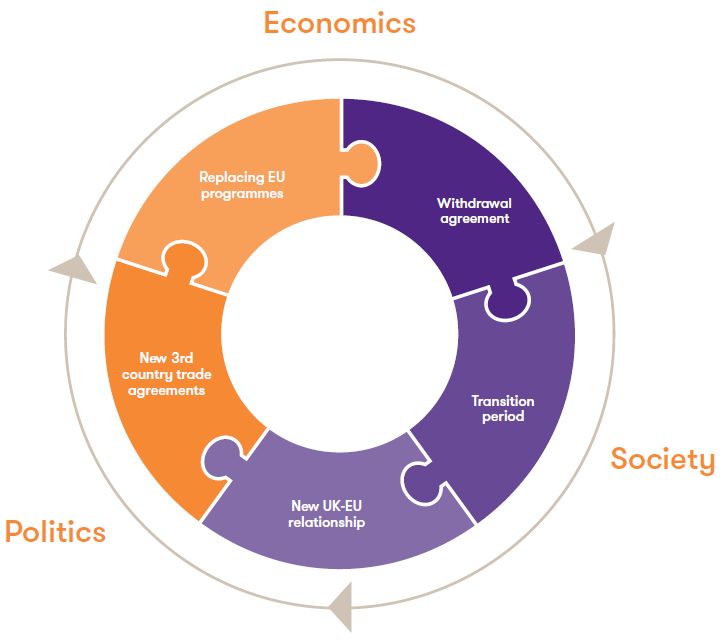

Brexit: what on earth is going on?

© Grant Thornton LLP. All rights reserved. 5

What is Brexit?

© Grant Thornton LLP. All rights reserved. 6

Brexit – three possible outcomes

A B C

‘No Deal’ Brexit ‘Deal’ Brexit No Brexit

UK leaves the European Union UK agrees a deal with the EU and UK decides to cancel Brexit and

to trade on WTO terms. enters a transition period. During this remain in the European Union.

the UK negotiates its new relationship Political divisions will remain

There is no transition period. with the EU that will start at the earliest and we may see more radical

from Jan 2021. domestic reform.

Short term disruption, long term Short term stability, long term Short term stability, long term

uncertainty uncertainty uncertainty

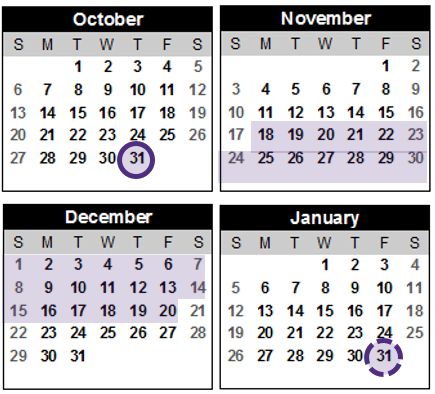

© Grant Thornton LLP. All rights reserved. 7Timeline – a busy three months

ahead

• Brexit October 31 – January 31

• Election before Christmas (from

November 18)

As a high impact and medium probability

outcome, we recommend clients with any

operations, investment or customers in the

UK have active contingency plans for a

no-deal Brexit on October 31

No-deal Brexit is also a high probability for

January 2020

© Grant Thornton LLP. All rights reserved. 8How does this affect you?

© Grant Thornton LLP. All rights reserved. 9Prepare for Brexit

Continuity, Compliance and Cost

Continuity Compliance Cost

Minimise disruption Ensure your Take action to

during Brexit organization, products mitigate costs and

and services comply protect cashflow

with new rules and

processes

© Grant Thornton LLP. All rights reserved. 10Key risks and opportunities

Based on our experience of working with clients, we have identified the following

as common risks and opportunities that a no-deal Brexit could create.

Market access Supply chain New products Acquisitions

NewMarket access for

trade barriers Supplydisruption

Cross border chain and Supporting customers’

New products Acquisitions

Opportunity to acquire

goods and services impact on core operations Brexit needs under-valued assets

New trade barriers for Cross border disruption and Supporting customers’ Opportunity to acquire

goods and services impact on core operations Brexit needs under-valued assets

Cumulative cost People Foreign exchange Competitive advantage

Greater need to cost

Cumulative reduce Retention

Peopleand Increased

Foreign international

exchange How does youradvantage

Competitive exposure

costs and optimise recruitment of staff competitiveness compare to competitors?

working

Greater needcapital

to reduce Retention and Increased international How does your exposure

costs and optimise recruitment of staff competitiveness compare to competitors?

working capital Risks and opportunities from a tax perspective follow…

© Grant Thornton LLP. All rights reserved. 11Be prepared for wider political change

in the UK

Post election policy directions

Tax People Business Infrastructure Public services Climate change Trade Relations

Conservative

• Employee led • Increased • Review High

• Market

skills and competition Speed Rail? • Market • US trade

• Tax cuts provision /

training • Reduced • Continue incentives deal?

outsourcing

• Social mobility regulation Heathrow?

• Tackling

• • • •

Common

Minimum Cross- Increased Zero carbon

•

ground

BEPS Common-

wage £10/hr? • Audit market Pennine / spending on by 2050

• Digital wealth

• End free reform local education and • Regulatory

services countries?

movement transport health action

tax

• “Social • Nationalisation • Halt

Labour

• Public • EU trade deal

• Higher justice” • Controls on Heathrow? • Deliver by

sector • Ethical foreign

taxes • Employee public sector • Continue High government

solutions policy

ownership contractors Speed Rail?

© Grant Thornton LLP. All rights reserved. 12Brexit Indirect tax implications Karen Robb Indirect Tax, Partner E: Karen.Robb@uk.gt.com

Indirect taxes – status quo

Non-EU goods EU Goods

– Import declaration – Frictionless border

– Customs Duty and VAT payments UK – No customs duty

Border

– Customs controls and inspections – No adverse VAT cashflow

Non-EU Goods in free

Goods circulation

Goods in free

EU Goods

circulation

© 2019 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 14Brexit: Key issues and considerations

Supply chain implications

• Need to keep products moving

• Additional administration

• Just in time sensitive production

Reduced working capital

• Additional VAT locked up?

• Increased absolute costs (duty isn’t recoverable)

Impact on price and profitability Interacts with

• Pass the costs on – reduced price competitiveness? broader tax

issues, such

• Bear the costs – margins might be lower? as transfer

pricing

© Grant Thornton LLP. All rights reserved. 15Indirect tax - No-deal Brexit impact

• Customs entries on EU goods

• Customs duties and Import VAT on imports and exports

• Double duties on goods moving across EU/non-EU borders multiple times

• UK content no longer counts towards EU origin

© Grant Thornton LLP. All rights reserved. 16Brexit: Pressure at ports?

• Implications for all ~ 135 UK ports and airports

• Many airports and deep sea ports already handle ROW

goods – customs systems and infrastructure

• Biggest impacts for “Roll-on / Roll-off” ports (ferry ports)

– not used to volumes and frequency, and undertaking a

number of additional checks and controls

• Critical for trade, business continuity, local and national

economies, continuity of critical goods such as food and

medicines

© Grant Thornton LLP. All rights reserved. 17HMRC – “Transitional Simplified

Procedures”

• HMRC has announced Transitional Simplified Procedures (“TSP”)

to make importing easier for a period if the UK leaves the EU

without a deal

• Can be used at all UK ports, not just ferry ports

© Grant Thornton LLP. All rights reserved. 18Eligibility requirements

To register you must:

• Have an EORI number

• Be established in the UK:

o Your company has a registered office in the UK or

o Your company has a permanent place of business in the UK where

business activities are undertaken

• Import goods from the EU into the UK

© Grant Thornton LLP. All rights reserved. 19HMRC – “Transitional Simplified

Procedures”

For non-‘controlled’ goods, trader expected to make customs declaration within their

commercial records

• A supplementary declaration will then have to be submitted to HMRC by the fourth

working day of the following month after the goods arrived into the UK

A trader needs to register with HMRC before using TSP

• A requirement to have an Economic Operator Registration and Identification (“EORI”)

number to apply for TSP

• Can also appoint a Customs agent to complete Customs declarations on the trader’s

behalf

• There is also a requirement to have an UK deferment account to pay any customs

duties that are due

© Grant Thornton LLP. All rights reserved. 20UK temporary tariff schedule

• The UK has recently published the tariff schedule that is intended to

be in place for 12 months following a no-deal Brexit

• Once the UK future trade policy is established, the permanent tariff

schedule is expected to be published

© Grant Thornton LLP. All rights reserved. 21UK temporary tariff schedule

Average UK Day 1

Product

no-deal MFN Tariff

Minerals 0.2%

Chemicals 0.1%

Plastics 0.1%

Wood 0.0%

Paper 0.0%

Animal skins 0.2%

Footwear 0.0%

Building materials 0.3%

Ceramics 1.2%

Glassware 0.2%

Precious metals and stones 0.0%

Base metals 0.0%

Machinery, electronics &

0.0%

instruments

Vehicles and transport 2.9%

Arms and ammunition 0.0%

Miscellaneous products 0.0%

© Grant Thornton LLP. All rights reserved. 22Duty and VAT Deferment

• Taxes must be ‘paid or secured’ to release goods from customs

• Possible to defer duty and import VAT until 15th of following month through

duty deferment account

• Bank guarantee required

• Must obtain approval and Deferment Approval Number from HMRC

• New announcement – UK VAT registered businesses can automatically

defer VAT and account for on VAT return

© Grant Thornton LLP. All rights reserved. 23Special Procedures to minimize

Customs Duty and VAT

• Types of Customs Special Procedures:

o Customs Warehousing

o Temporary Admission and End-Use

o Inward and Outward Processing

• Authorization required

• Improved cash flow / absolute duty savings

© Grant Thornton LLP. All rights reserved. 24Customs warehousing

• Public or private customs warehouse

• Defers payment of import VAT and duty where goods are imported

from outside EU / UK until goods are ‘removed’ from the warehouse

• Cash flow advantage

• Interaction with other reliefs

© Grant Thornton LLP. All rights reserved. 25Temporary Admission and End-Use

Temporary Admission:

• Relief from import duty

• No alterations or processing of goods

• Maximum period applies

• E.g. Professional equipment, items for auction, goods for testing, clinical trials

End-Use Relief:

• Favourable rates of duty for specific industries

• No processing required to be able to be used for prescribed end use

• Evidence of prescribed end use

• Military, aircraft, ships, bicycles and shrimps!

© Grant Thornton LLP. All rights reserved. 26Inward and Outward Processing

Inward Processing:

• Relieves import VAT and customs duty

• Import from outside of EU and re-export to outside EU (will include UK post-Brexit)

• Limited time for processing to take place

Outward Processing:

• Relieves import VAT and customs duty

• Import from non-EU country where goods have been produced from previously

exported EU goods.

• Limited time to process before duty and tax become payable

© Grant Thornton LLP. All rights reserved. 27What should businesses be thinking

about?

• Start with your supply chain. Does it include movement of goods through UK and / or EU?

• Calculate VAT and duty impact

o Are you better or worse off?

o What’s the impact on customers taking delivery in UK or EU?

• What do you want to achieve?

o BAU?

o Cost reduction?

o Keep goods flowing?

• No regrets actions

o TSP

o Simplifications

o EORI and VAT registrations

• Consider interactions with broader tax issues, such as transfer pricing

© Grant Thornton LLP. All rights reserved. 28Brexit Direct tax implications Matt Stringer Head of International Tax E: Matt.TA.Stringer@uk.gt.com Twitter: @AccioGin

Overview of the direct tax implications

EU Directives: withholding taxes

Wider international EU Directives:

implications re-organizations

Direct tax

implications

Other treaty Group structures

issues

EU State Aid

© 2019 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 30EU Directives

Parent / Subsidiary Directive – relief from WHT

on dividends

Interest & Royalties Directive – relief from WHT

Benefits on interest and royalties

of EU

EU Merger Directive – relief from charges on

Directives certain cross-border reorganizations

Anti Avoidance and Mutual Assistance

Directives

© 2019 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 31EU Directives

Implications of a no-deal Brexit:

• Loss of EU Directives – UK no longer treated as EU member state

• Some transposed into UK law already and more likely to be, so shall stay.

However, EU countries are unlikely to amend their domestic law to include the

UK as an EU member state

• Double tax treaty network

© Grant Thornton LLP. All rights reserved. 32Withholding tax

Impact of UK not being an EU Member State

In relation to UK withholding taxes on payments to EU Member States, HMRC

released guidance on March 21, 2019 which states that the UK will continue to

apply the EU Directives to payments from UK companies to Member States.

This means that there should be no increased UK withholding tax cost on any

interest and royalty payments to Member States. Payments which previously

qualified for the Directive exemptions should continue to qualify. NB: Clearance

process remains in place for interest payments (but not for royalties).

Member States are unlikely to take the same approach – so the relief above only

applies to payments from the UK.

© Grant Thornton LLP. All rights reserved. 33Withholding tax

Impact of UK not being an EU Member State

The impact of moving from the Parent-Subsidiary Directive & Interest and Royalties Directive onto rates agreed

with Double Tax Treaties (i.e. these are the domestic rates, as reduced by the relevant Double Tax Treaty)

Country Dividends Interest Royalties

If shareholding ≥25%, at 5% If shareholding >50%, 10%

0%

Austria Otherwise, 15% Otherwise, 0%

If shareholding ≥10%, at 0%

0%/10% 0%

Belgium Otherwise, 10%/15%

For certain dividends 0% If shareholding ≥10%, 0%

5%

Bulgaria Otherwise 5%/15% Otherwise 5%

If shareholding ≥25%, 5%

5% 5%

Croatia Otherwise 10%/15%

5% for film royalties

0% 0%

Cyprus Otherwise, 0%

If shareholding ≥25%, 5%

0% 0%/10%

Czech Republic Otherwise, 15%

Key: Unless EU country acts to treat the UK as a Member State, there will be a Brexit impact – payments

from EU to UK companies will most likely result in increased costs

Unless EU country acts to treat the UK as a Member State, then depending on facts, there may be a

Brexit impact – payments from EU to UK companies may result in increased costs

There should not be a Brexit impact – payments under treaty should not result in any additional costs

© Grant Thornton LLP. All rights reserved. 34Withholding tax

Impact of UK not being an EU Member State

The impact of moving from the Parent-Subsidiary Directive & Interest and Royalties Directive onto rates agreed

with Double Tax Treaties (i.e. these are the domestic rates, as reduced by the relevant Double Tax Treaty)

Country Dividends Interest Royalties

If shareholding ≥25%, 0%

0% 0%

Denmark Otherwise, 15%

Estonia 0% 0%/10% 0%

Finland 0% 0% 0%

If shareholding ≥10%, 0%

0% 0%

France Otherwise, 15%

If shareholding ≥10%, 5%

0% 0%

Germany Otherwise, 10%/15%

Greece 15% 0% 0%

If shareholding ≥10%, 0%

0% 0%

Hungary Otherwise, 10%/15%

Key: Unless EU country acts to treat the UK as a Member State, there will be a Brexit impact – payments

from EU to UK companies will most likely result in increased costs

Unless EU country acts to treat the UK as a Member State, then depending on facts, there may be a

Brexit impact – payments from EU to UK companies may result in increased costs

There should not be a Brexit impact – payments under treaty should not result in any additional costs

© Grant Thornton LLP. All rights reserved. 35Withholding tax

Impact of UK not being an EU Member State

The impact of moving from the Parent-Subsidiary Directive & Interest and Royalties Directive onto rates agreed

with Double Tax Treaties (i.e. these are the domestic rates, as reduced by the relevant Double Tax Treaty)

Country Dividends Interest Royalties

For certain qualifying companies 0%

0% 0%

Ireland Otherwise, 5%/15%

If shareholding ≥10%, 5%

10% 8%

Italy Otherwise, 15%

If shareholding ≥25%, 5%

10% 5%/10%

Latvia Otherwise, 15%

If shareholding ≥25%, 5%

10% 5%/10%

Lithuania Otherwise, 15%

If shareholding ≥25%, 5%

0% 0%

Luxembourg Otherwise, 15%

Malta 0% 0% 0%

If shareholding ≥10%, 0%

0% 0%

Netherlands Otherwise, 10%/15%

Key: Unless EU country acts to treat the UK as a Member State, there will be a Brexit impact – payments

from EU to UK companies will most likely result in increased costs

Unless EU country acts to treat the UK as a Member State, then depending on facts, there may be a

Brexit impact – payments from EU to UK companies may result in increased costs

There should not be a Brexit impact – payments under treaty should not result in any additional costs

© Grant Thornton LLP. All rights reserved. 36Withholding tax

Impact of UK not being an EU Member State

The impact of moving from the Parent-Subsidiary Directive & Interest and Royalties Directive onto rates agreed

with Double Tax Treaties (i.e. these are the domestic rates, as reduced by the relevant Double Tax Treaty)

Country Dividends Interest Royalties

If shareholding ≥10% for 2 consecutive years, 0%

5% 5%

Poland Otherwise, 10%

If shareholding ≥25%, 10%

10% 5%

Portugal Otherwise, 15%

If shareholding ≥25%, 10%

10% 10%/15%

Romania Otherwise, 15%

If shareholding ≥25%, 5%

0% 10%

Slovakia Otherwise, 15%

If shareholding ≥20%, 0% If shareholding ≥20%, 0%

5%

Slovenia Otherwise, 15% Otherwise, 5%

If shareholding ≥10%, 0%

0% 0%

Spain Otherwise, 10%/15%

If shareholding ≥10%, 0%

0% 0%

Sweden Otherwise, 5%/15%

Key: Unless EU country acts to treat the UK as a Member State, there will be a Brexit impact – payments

from EU to UK companies will most likely result in increased costs

Unless EU country acts to treat the UK as a Member State, then depending on facts, there may be a

Brexit impact – payments from EU to UK companies may result in increased costs

There should not be a Brexit impact – payments under treaty should not result in any additional costs

© Grant Thornton LLP. All rights reserved. 37Withholding tax

Impact of UK not being an EU Member State

Call to action:

• Review any reliance on EU Directives for cross border dividend, interest or

royalty payments

• Think about making best use of Directives before Brexit – NB dividends

• Admin burden: updated clearances (even where 0% rate under treaty)

© Grant Thornton LLP. All rights reserved. 38Practical examples

• Generally no tax credit available for

UK Co foreign dividend withholding tax in the

UK

• German Co dividend attracts a 5%

WHT (at best) under double tax treaty

Dividend payment from date of Hard Brexit

German

Co

WHT leakage

© Grant Thornton LLP. All rights reserved. 39Other EU Directives

Impact of UK not being an EU Member State

EU Mergers Directive ceases to apply, removing tax relief for certain cross border

re-organization activity.

Member States may have clawback provisions for prior reliance after UK

company is deemed to exit an EU grouping.

© Grant Thornton LLP. All rights reserved. 40Group structures

Implications of a no-deal Brexit:

• Do EU-wide tax groupings or consolidations cease to apply?

• Risk of claw back of previously claimed reliefs and inability to claim future

reliefs

• Some EU Member States have a CFC exemption for EU resident companies –

may be lost for UK subsidiaries post-Brexit

• There may be other EU references in domestic tax code of other EU Member

States that would now exclude the UK

© Grant Thornton LLP. All rights reserved. 41EU state aid

Implications of a no-deal Brexit:

• The EU State Aid rules prevent advantages being given on a selective basis by government

authorities which may distort competition (e.g. if tax rebates are given to certain industries)

• Post-Brexit, the UK may no longer be bound by these rules

• Certain UK tax rules are restricted by these rules, for example:

• SME R&D tax relief

• Creatives industries reliefs

• CFC Finance Company exemption (re recent European Commission challenge)

• Post-Brexit – more freedom for UK to relax restrictions and incentivize taxpayers, subject to usual

WTO restrictions

© Grant Thornton LLP. All rights reserved. 42US withholding tax

Impact of UK not being an EU Member State

A number of US treaties include an Equivalent Beneficiaries sub-clause in the Limitation on

Benefits clause. This generally allows a Contracting State to qualify for treaty benefits

where other tests are failed (e.g. the Active Trade or Business test), but a parent company

is in an EU/EEA Member State or is a party to NAFTA and that parent company would itself

qualify for treaty benefits.

Brexit may remove UK companies from such a clause (i.e. no longer EU, nor NAFTA),

meaning any reliance on the Equivalent Beneficiaries sub-clause is not sufficient.

Could lead to 30% US WHT in certain circumstances.

© Grant Thornton LLP. All rights reserved. 43Practical examples

• Domestic rate of WHT in US for royalties is

30%

UK Co • Relief available to reduce this to 0% under the

US-Luxembourg double tax treaty

• LOB clause may deny relief

• Historically where no Lux Active Trade or

License of IP

Business, reliance could have been placed on

the UK’s Active Trade or Business as an

Equivalent Beneficiary in an EU Member State

Lux Co US Co • If UK is no longer an EU Member State, Lux

Co may lose treaty benefits

Can apply to

other forms of

Royalty payment 30% WHT leakage payment and

scenarios

© Grant Thornton LLP. All rights reserved. 44Brexit Transfer pricing implications Imran Khan Transfer Pricing, Partner E: Imran.Khan@uk.gt.com

Transfer pricing considerations

TP considerations arise from two Brexit related scenarios

1. Business restructurings which arise 2. Post-Brexit restructuring steady-

as a direct consequence of Brexit state transactions

Key issue

Key issue

Is there a need, at arm’s length, for

What are the arm’s length pricing

one-off/on-going compensation

outcomes, where do profits and value

(“Exit”) – such compensation would

reside post-Brexit, is this defensible?

be subject to UK taxation

© Grant Thornton LLP. All rights reserved. 46Transfer pricing considerations

1. Business restructuring 2. Steady-state transactions

• Transfers, in particular of intangibles/IP • Arm’s length pricing for new steady-

such as: state transactions such as:

Customer contacts/relationships/list Licensing of intangibles

Supplier contracts Sale of goods

Marketing intangibles, e.g. trade marks Provision of services

Trading intangibles, e.g. technology

Licenses

Interacts with

Other rights such as authorizations other areas of

• Termination or substantial renegotiation of tax, such as

customs duties

terms and conditions

• Significant change in profit potential

© Grant Thornton LLP. All rights reserved. 47Transfer pricing considerations

1. Business restructuring 2. Steady-state transactions

Key considerations

In reaching appropriate and defensible views it is important to consider:

• Legal arrangements, rights and obligations between the related parties

pre and post Brexit

• Underlying substance of the functions, assets and risks of the parties,

how this influences exit and on-going pricing valuations

• Bargaining positions of the related parties

• Options realistically available to the parties

© Grant Thornton LLP. All rights reserved. 48Transfer pricing considerations

Practical example

Brexit related TP considerations apply to a wide range of industries and sectors. Taking the example of a

pharmaceutical business, set out below are potential TP considerations.

1. Brexit related business restructuring – 2. Post-restructuring transactions

transfers to EU related parties of:

• Customer contracts • License of intangibles by

UK entity – e.g. trade

• Supplier contracts Should the UK entity marks

How should

receive, at arm’s • Provision of services by UK such

• Marketing length, any entity – e.g. strategic transactions be

authorizations compensation for management priced at arm’s

transfer of intangibles length?

• Certifications – e.g. to EU related parties? • Remuneration in UK/EU

QP release entities – e.g. distributions,

QP release etc

© Grant Thornton LLP. All rights reserved. 49Any questions?

© Grant Thornton LLP. All rights reserved. 50Speakers

David Sites Imran Khan -Matt Stringer

Head of International Tax Transfer Pricing, Partner Head of International Tax

Grant Thornton US Grant Thornton UK Grant Thornton UK

Adam Jackson Karen Robb

Head of Brexit & Political Risk Advisory Indirect Tax, Partner

Grant Thornton UK Grant Thornton UK

© 2019 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 51Disclaimer

• This Grant Thornton LLP presentation is not a comprehensive analysis of

the subject matters covered and may include proposed guidance that is

subject to change before it is issued in final form. All relevant facts and

circumstances, including the pertinent authoritative literature, need to be

considered to arrive at conclusions that comply with matters addressed in

this presentation. The views and interpretations expressed in the

presentation are those of the presenters and the presentation is not intended

to provide accounting or other advice or guidance with respect to the matters

covered

For additional information on matters covered in this presentation, contact

your Grant Thornton LLP adviserDisclaimer

**********************

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the U.S. Internal

Revenue Service, we inform you that any U.S. federal tax advice contained in this PowerPoint is not intended or written

to be used, and cannot be used, for the purpose of (a) avoiding penalties under the U.S. Internal Revenue Code or (b)

promoting, marketing or recommending to another party any transaction or matter addressed herein.

*********************

The foregoing slides and any materials accompanying them are educational materials prepared by Grant Thornton LLP and are not intended as

advice directed at any particular party or to a client-specific fact pattern. The information contained in this presentation provides background

information about certain legal and accounting issues and should not be regarded as rendering legal or accounting advice to any person or entity.

As such, the information is not privileged and does not create an attorney-client relationship or accountant-client relationship with you. You

should not act, or refrain from acting, based upon any information so provided. In addition, the information contained in this presentation is not

specific to any particular case or situation and may not reflect the most current legal developments, verdicts or settlements.

You may contact us or an independent tax advisor to discuss the potential application of these issues to your particular situation. In the event that

you have questions about and want to seek legal or professional advice concerning your particular situation in light of the matters discussed in

the presentation, please contact us so that we can discuss the necessary steps to form a professional-client relationship if that is warranted.

Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter

addressed herein.

© 2018 Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd. All rights reserved. Printed in the U.S. This material is the

work of Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd.Thank you for attending

To retrieve your CPE certificate

• Respond to the online evaluation form. Please note, you may need to disable pop-up blocking software to complete

this evaluation.

• Print your CPE certificate and retain for your records. Participants are responsible to maintain CPE completion

records.

• Those receiving CPE will also receive the certificate at the email address used to register for the webcast.

• We are unable to grant CPE credit in cases where technical difficulties preclude eligibility. CPE program sponsorship

guidelines prohibit us from issuing credit to those not verified by the technology to have satisfied the minimum

requirements in monitoring response and viewing time.

If you experience any technical difficulties, please contact 877.398.9939 or email GTWebcast@centurylink.com

© Grant Thornton LLP. All rights reserved. 54Thank you for attending

www.grantthornton.com twitter.com/GrantThorntonUS linkd.in/GrantThorntonUS

Visit us online.

For questions regarding your CPE certificate, contact

CPEEvents@us.gt.com

© Grant Thornton LLP. All rights reserved. 55You can also read