Building for the Future - NOVEMBER MARKETING - Investors

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Building for the Future

NOVEMBER MARKETING

1

FORWARD-LOOKING STATEMENTS

Certain statements in this presentation contain "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 including, without

limitation, expectations, beliefs, plans and objectives regarding anticipated financial and operating results, asset divestitures, estimated reserves, drilling locations, capital expenditures, price estimates, typical well

results and well profiles, type curve, and production and operating expense guidance included in this presentation. Any matters that are not historical facts are forward looking and, accordingly, involve estimates,

assumptions, risks and uncertainties, including, without limitation, risks, uncertainties and other factors discussed in our most recently filed Annual Report on Form 10-K, recently filed Quarterly Reports on Form 10-Q,

recently filed Current Reports on Form 8-K available on our website, www.apachecorp.com, and in our other public filings and press releases. These forward-looking statements are based on Apache Corporation’s

(Apache) current expectations, estimates and projections about the company, its industry, its management’s beliefs, and certain assumptions made by management. No assurance can be given that such expectations,

estimates, or projections will prove to have been correct. A number of factors could cause actual results to differ materially from the projections, anticipated results, or other expectations expressed in this

presentation, including, Apache’s ability to meet its production targets, successfully manage its capital expenditures and to complete, test, and produce the wells and prospects identified in this presentation, to

successfully plan, secure necessary government approvals, finance, build, and operate the necessary infrastructure, and to achieve its production and budget expectations on its projects.

Whenever possible, these “forward-looking statements” are identified by words such as “expects,” “believes,” “anticipates,” “projects,” “guidance,” “outlook,” “will”, and similar phrases. Because such statements

involve risks and uncertainties, Apache’s actual results and performance may differ materially from the results expressed or implied by such forward-looking statements. Given these risks and uncertainties, you are

cautioned not to place undue reliance on such forward-looking statements, which speak only as of the date hereof. Unless legally required, we assume no duty to update these statements as of any future date.

However, you should review carefully reports and documents that Apache files periodically with the Securities and Exchange Commission.

Cautionary Note to Investors: The United States Securities and Exchange Commission (SEC) permits oil and gas companies, in their filings with the SEC, to disclose only proved, probable, and possible reserves that

meet the SEC's definitions for such terms. Apache may use certain terms in this presentation, such as “resource,” “resource potential,” “net resource potential,” “potential resource,” “resource base,” “identified

resources,” “potential net recoverable,” “potential reserves,” “unbooked resources,” “economic resources,” “net resources,” “undeveloped resource,” “net risked resources,” “inventory,” “upside,” and other similar

terms that the SEC guidelines strictly prohibit Apache from including in filings with the SEC. Such terms do not take into account the certainty of resource recovery, which is contingent on exploration success, technical

improvements in drilling access, commerciality, and other factors, and are therefore not indicative of expected future resource recovery and should not be relied upon. Investors are urged to consider carefully the

disclosure in Apache’s Annual Report on Form 10-K for the fiscal year ended December 31, 2017 available from Apache at www.apachecorp.com or by writing Apache at: 2000 Post Oak Blvd., Suite 100, Houston, Texas

77056 (Attn: Corporate Secretary). You can also obtain this report from the SEC by calling 1-800-SEC-0330 or from the SEC's website at www.sec.gov.

Certain information may be provided in this presentation that includes financial measurements that are not required by, or presented in accordance with, generally accepted accounting principles (GAAP). These non-

GAAP measures should not be considered as alternatives to GAAP measures, such as net income or net cash provided by operating activities, and may be calculated differently from, and therefore may not be

comparable to, similarly titled measures used at other companies. For a reconciliation to the most directly comparable GAAP financial measures, please refer to Apache’s third quarter 2018 earnings release and third

quarter 2018 Financial & Operational Supplement at www.apachecorp.com.

None of the information contained in this document has been audited by any independent auditor. This presentation is prepared as a convenience for securities analysts and investors and may be useful as a reference

tool. Apache may elect to modify the format or discontinue publication at any time, without notice to securities analysts or investors.

2

TABLE OF CONTENTS

Apache Overview

Portfolio Review

Permian Basin

Alpine High / Altus Midstream

International

3Q’18 Highlights & 2019 Preview

Guidance

Appendix

3

APACHE TRANSFORMATION

Focusing the Portfolio, Growing the Permian, Improving Returns

Current Portfolio 2014 3Q 2018

Total Production (Reported)(1) 647 Mboe/d 476 Mboe/d

Permian Production 159 Mboe/d 222 Mboe/d

US / Int’l Production Mix (Reported) (1) 45% / 55% 57% / 43%

Oil Production Mix (Reported) (1) 50% 51%

Capital Investment (FY) $10.7 billion $3.45 billion

Rig Count 119 rigs 33 rigs

Net Debt (Period End) $10.5 billion $7.6 billion

Shares Outstanding 376.5 MM 381.6 MM

Annualized Dividend (Period End) $1.00/Shr $1.00/Shr

(1) 2014 production includes Australia production

1Q 2015 April 2015 June 2015 September 2016 June 2017 November 2018

Canada & Australia Exit Announced Canada Exit Closed Altus

CEO / CFO

Australia LNG Alpine High Midstream

Announcement

Exit Discovery Transaction

4

APACHE TODAY

BALANCED, RETURNS-FOCUSED PORTFOLIO

On Track to Achieve Long-Term, Sustainable Double-Digit ROCE

Top-tier Permian Basin position delivering strong growth and returns

Robust free-cash-flow generating assets in Egypt & North Sea

Differential Exploration Opportunities (Lower 48 & Suriname)

DISCIPLINED FINANCIAL APPROACH

Strong balance sheet, steady dividend, no shareholder dilution

Free cash flow visibility / returning capital to shareholders

Formation of Altus Midstream to fund Alpine High buildout

CASH FLOW GROWTH DRIVERS

Double-Digit U.S. Production Growth

Material exposure to Brent crude oil pricing

Strong momentum in North Sea beginning in 4Q 2018

Alpine High cryo installation to drive liquids and margin uplift in 2019

5

A LEADER IN ESG ENGAGEMENT AND SUSTAINABILITY REPORTING

DISCLOSING THE FACTS

1 tCO2e/Mboe = metric tons of carbon dioxide equivalent per thousands of barrels of oil equivalent 4 Workforce TRIR (Total Recordable Incident Rate) includes Apache employees at all levels and contractors The 2017 Disclosing the Facts questionnaire focused on the issue of methane emissions while previous

2 The 2016 value was revised based on updated data 5 Total Recordable Incident Rate is calculated by multiplying total number of recordable questionnaires covered the following topics: toxic chemicals, water and waste management, air emissions,

3 Bbls/Boe = barrels of water withdrawn per barrel of oil equivalent produced injuries by 200,000 hours and then dividing by total person-hours worked community impacts, and management and accountability.

6

PORTFOLIO REVIEW

7

PERMIAN BASIN

Returns-Focused Growth

Strong production growth with flat rig count

Efficiencies driving shorter cycle times and lower costs

Expanding inventory with strategic testing

Upward bias to 2019 guidance

Production & Rig Count 222 50

220

202

40

190 183

177

161 30

159

160 149 148 146 20

130 17 17 16 17 18 10

16

13

100

5 7

0

1.6 MM Net Acres in the Permian Basin

3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

Avg. Production (Mboe/d) Avg. Rigs

8

MIDLAND AND DELAWARE BASIN OIL PRODUCTION

Growth to Continue into 2019

Strong well performance Key Focus Areas

Increasing efficiencies, multi-well pads / longer laterals

Midland & Delaware Basin Oil Production (Mbo/d)

Wildfire

Pecos Bend

Azalea

Dixieland

61 60

55 55

46 Powell

40

Alpine High

2Q17A 3Q17A 4Q17A 1Q18A 2Q18A 3Q18A

9

ALPINE HIGH

Developing a World-Class Rich Gas Play

Alpine High Acreage Map

Unprecedented hydrocarbon column > 5,000 ft.

Vertically stacked oil, rich gas and dry gas fairways

Scale

5,000+ locations identified

3 billion bbls / 75 Tcf of resource in place (Woodford & Barnett)

Large operated position / economies of scale

Strategically positioned to deliver NGLs and gas in scale to the

Gulf Coast

Execution Nearly tripling the number of producing wells from YE 2017 to

YE 2018

Guided 2019 Alpine High volumes to upper end of 85-100

Mboe/d range

Highly economic rich gas play; proven oil upside

Economics Liquids uplift combined with low F&D and operating costs →

strong recycle ratios ~340,000 Net Acres(1)

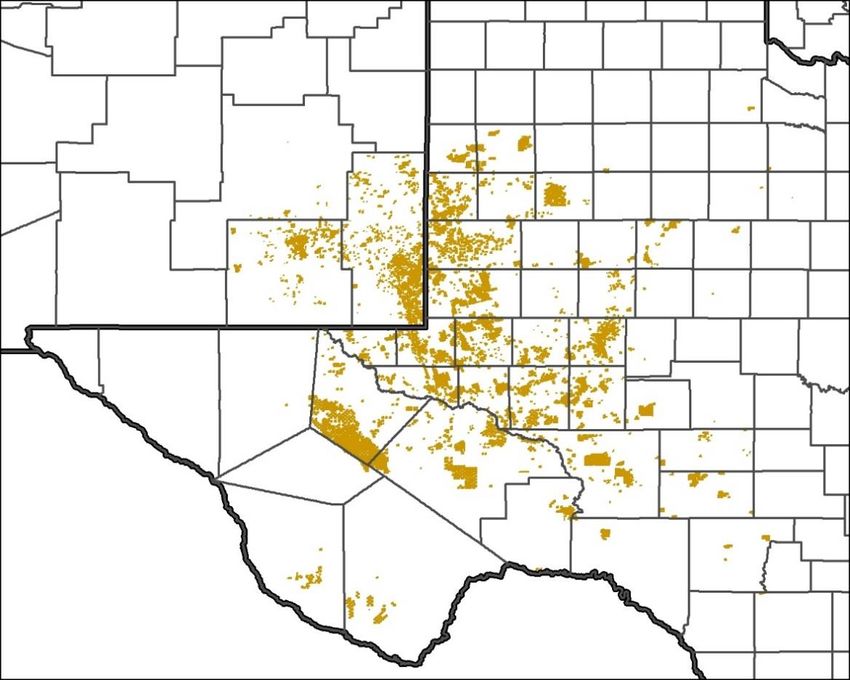

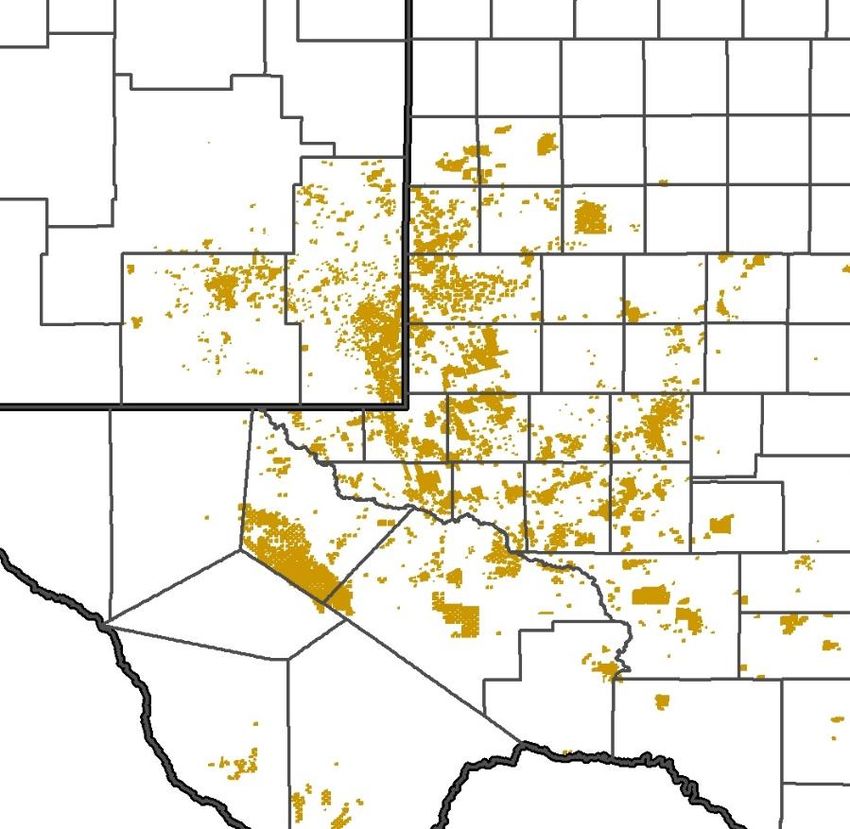

(1) Acreage as of July 1, 2018 10SIGNIFICANT INDUSTRY ACTIVITY INCREASE

FOLLOWING ALPINE HIGH ANNOUNCEMENT

September 2016 August 2018

WARD

CULBERSON

REEVES

PECOS

JEFF DAVIS

Drilled/ Drilling Count: 203

Current Permit Count: 85

Total well count: 288

Mil es

0 5 10 20

20 Miles 20 Miles

BREWSTER

PRESIDIO

APA Operated Rig Competitor Permit Wells PETRA 8/28/2018 4:23:00 PM

Competitor Wells Drilled/Drilling Apache Acreage Outline

Source: Drilling Info.

11ALPINE HIGH: TRANSITIONING TO FULL-FIELD DEVELOPMENT

Apache’s long-term methodical approach to developing Alpine High

2014 - 2016 2016 - 2017 2018 and Beyond

Formulation of concept,

concept testing and

confirmation + Areal and vertical

delineation = Transition to full field development

▪

▪

Optimized Spacing, Patterns &

Completions

Drilling Efficiencies

▪ Lifting Cost Efficiencies

Focus on reducing costs, increasing efficiency and maximizing recovery

12ALPINE HIGH PLAY EVOLUTION

September 2016 November 2018 2020 (Est.)

Rig Count 3 8 10 - 11

Cum. Wells Drilled 14 180 425 – 450 at year-end

Cum. Wells on

9 125 350 – 375 at year-end

Production

Net Production

Nm ~55 160 – 180

(Mboe/d)

Location Count 2,000 – 3,000+ 5,000+ Ongoing Testing

Confirmed Landing

2 13 Ongoing Testing

Zones

• Rich gas processing capacity: 380 MMcf/d • Rich gas processing capacity: ~1,380 MMcf/d

Altus Midstream Nm • Lean treating & compression: 400 MMcf/d • Lean treating & compression: 480 MMcf/d

• Initial cryo under construction • Five cryo plants at year end

13ALTUS MIDSTREAM: TRANSACTION OVERVIEW

Newly Formed Pure Play Permian Basin Midstream Company

Transaction closed November 9, 2018 (Ticker Symbol: ALTM)

Publicly traded C-Corp with 325MM shares outstanding (79% owned by Apache)

~$625MM in cash and zero debt, as of October 1 effective date

Future EBITDA ~ 50% Gathering & Processing and 50% pipeline ownership

14ALTUS MIDSTREAM: GATHERING & PROCESSING OVERVIEW

Pipeline Map Current Asset Highlights

Rich Gas Processing: 380 MMcf/d of capacity in

service

Lean Gas Treating / Compression: 400 MMcf/d

of capacity in service

Gathering Pipelines: ~125 miles in service

Primarily 20-30 inch pipe

Residue Pipelines / Market Connections: ~55

miles in service with 3 market connections

(Comanche Trail, El Paso Line 1600 and Trans-

Pecos Pipeline)

Key Additions by YE 2020

1 Bcf/d of cryo processing capacity

80 MMcf/d of lean gas treating and

compression capacity

> 80 miles of gathering pipeline

1 additional market connection

expected to be in service (Roadrunner)

(1) Acreage footprint depicted on map is as of July 1, 2018. 15ALTUS MIDSTREAM: JOINT VENTURE PIPELINES OVERVIEW

Pipeline Map Commentary

Altus will own options to participate

in five joint venture pipelines

15%(1) of KMI’s Gulf Coast Express

Nat Gas

33%(2) of KMI’s Permian Highway

33% of EPD’s Shin Oak

NGLs

50% of Salt Creek NGL

Crude

15% of EPIC Crude

Altus to invest ~$1.5 - $1.8 billion of

capital in JV pipeline projects

No promote paid above construction

cost for any JV pipeline project

Very attractive projects for Altus (~7x

build multiple of EBITDA, on average)

Pipelines in service by YE 2020

(1) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of

the PHP option.

(2) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised. Altus ownership expected to be no less than ~27%.

16ALTUS MIDSTREAM: CONSERVATIVE FINANCIAL PLAN

Through the end of 2020, Altus Midstream capital investment estimated at

$2.5 billion. Funding sources include:

Approximately $625 MM cash at effective date, October 1

Estimated operating cash flow of $390 MM through 2020

$800MM 5-year credit facility, with initial availability of $450 MM and eventual ability to

upsize to $1.5 billion

Access to other credit accretive capital sources: preferred equity, asset level financing and

structured equity

Altus Midstream leverage ratio forecasted at less than 3x by year-end 2020

Apache will fully consolidate Altus Midstream, but its future debt is planned to

remain non-recourse to Apache

17ALTUS MIDSTREAM: BENEFITS OF TRANSACTION TO APACHE

At $9 - $10/share, APA’s 79% ownership valued at ~$2.3 - $2.5 billion

Demonstrates Value Equity position to benefit from long-term Alpine High growth plan

Maintain control of future Alpine High midstream buildout

Estimated Altus Midstream gathering and processing investment:

Funds Future Midstream ~$180 MM in 4Q 2018 / $320 MM in 2019 / $330 MM in 2020

Investment Planned JV pipeline investment of ~$1.5 - $1.8 billion

Lower cost of capital

Enhances Capital

Incremental investments / share repurchases / debt retirement

Optionality

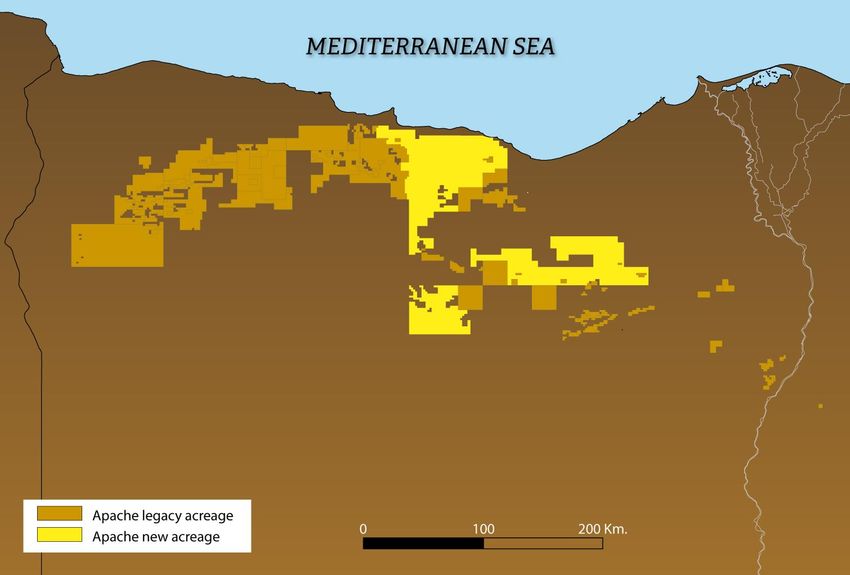

18EGYPT

Preparing for Future Growth

Country’s largest oil producer; stable gross production Apache Egypt Acreage: ~6.2 million acres

Running 12 rigs

High-density 3-D seismic program across 4 basins

▪ 2.6 million acres; ~ 38% complete

▪ State-of-the-art technology provides improved fault

definition and enhanced deep imaging

▪ Initiated seismic acquisition in new Northwest Razzak

concession

Production Brent Crude

(Mboe/d) 400 120 ($/Bbl)

100

300 350 345 334 339 334 342 338

328 330 80

200 60

40

100

98 90 88 89 87 82 80 80 78

20 New concessions expand acreage position

0 0

3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

by more than 50%

Adjusted Production Gross Production Brent Crude Pricing

19IMPACT OF RISING OIL PRICE ON EGYPT PSC’S

Cash Flow Increases, Adjusted Production Declines

Production Stable Gross Production Brent Crude / Cash Flow

(Mboe/d) ($/Bbl) ($/Boe)

400 80

Brent

350 70 Up 58%

334 339 334 342 338

330

300 60

250 50

200 40

Cash Flow/Boe

Up 73%

150 30

100 20

Adj. Production

50 89 87 10 Down 13%

82 80 80 78

- -

2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 3Q 18

Adjusted Production Gross Production Egypt Cash Flow per Boe Brent Pricing

(1) Excludes tax barrels and noncontrolling interest

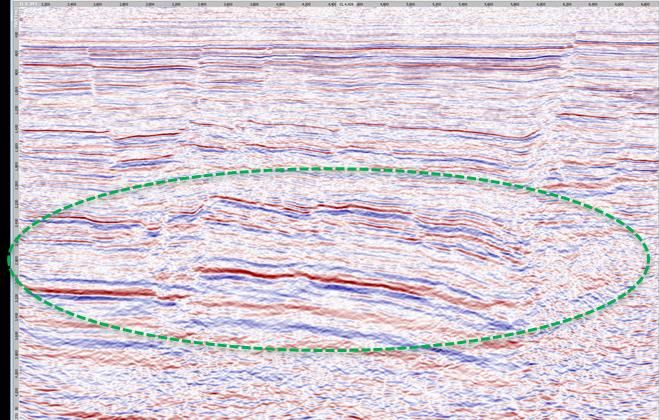

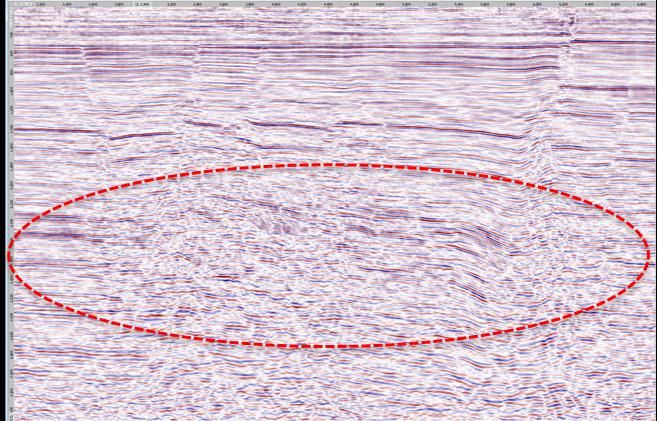

20EGYPT: STATE OF THE ART 3-D

Dramatic Improvement in Sub-Surface Imaging

2013 Vintage Seismic 2018 Vintage Seismic

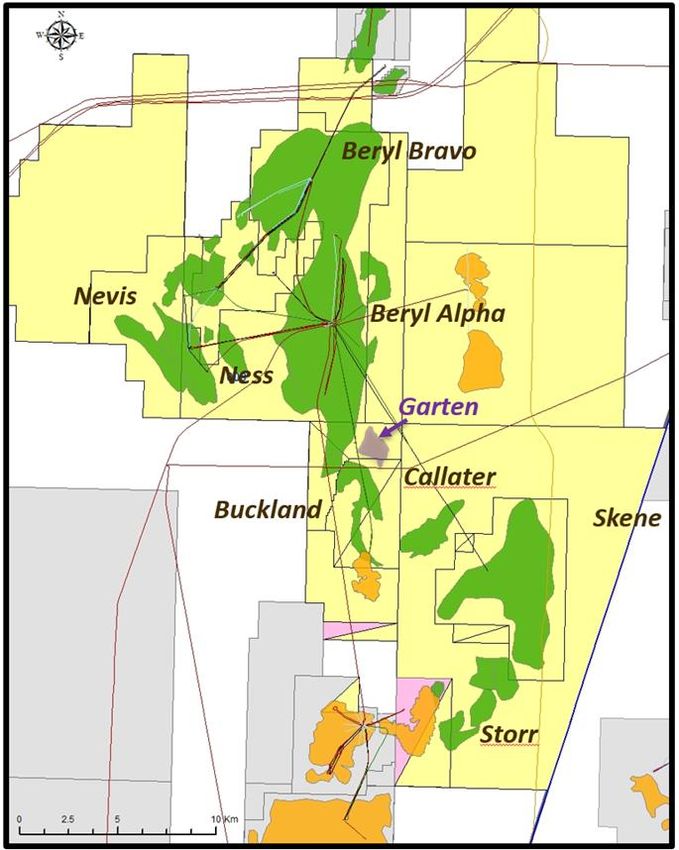

21NORTH SEA

High Margins, High Returns, Free Cash Flow

Apache North Sea Acreage

Strong leverage to premium Brent crude pricing

Best-in-class operator

3 rigs operating (2 platform, 1 semi-submersible)

Improving base oil production profile at Forties

with water flood management programs

Beryl production poised to increase

Fourth Callater well (CC2) online in 3Q 2018

First Garten well online in 4Q 2018 North Sea Production (Mboe/d)

62 70

58 55 60 58 54 54 51

3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

22NORTH SEA: GARTEN

Large Commercial Discovery in Beryl Area

North Sea Beryl Area Garten discovery well encountered more than

700’ of net oil pay in Block 9/18a Area-W

➢ Recoverable resource is expected to

exceed 10 million barrels of light oil

➢ Apache holds a 100% working interest

➢ Drilling, completion, and tieback costs

are estimated at $80 million

➢ Tied back to the Beryl Alpha platform,

6 kilometres north

Apache’s fourth commercial exploration

discovery in the Beryl area in the past three

years

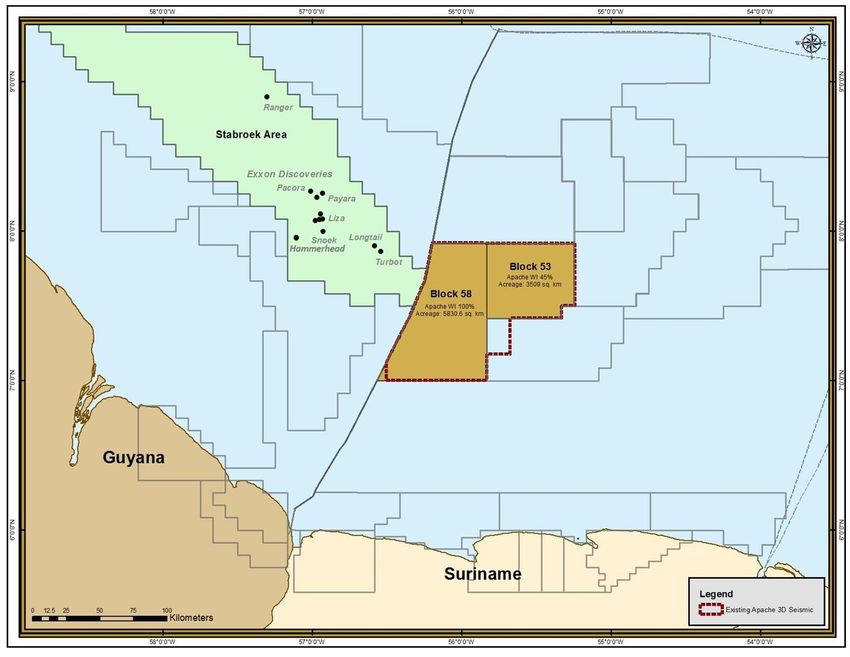

23SURINAME: HIGH IMPACT OIL EXPLORATION

Massive acreage blocks near proven

oil province

Block 58 seismic processing

complete, identifying and ranking

prospects

Block 58 Block 53

Exploration well to spud on Block 1.44 MM acres 0.87 MM acres

58 by year-end 2019

243Q HIGHLIGHTS & 2019 PREVIEW

253Q 2018 KEY METRICS

Reported Production 476 Mboe/d

Adjusted Production(1) 401 Mboe/d

Cost Incurred and GTP Capital Investment $1 Billion

Upstream Oil and Gas Capital Investment(2) $844 Million

Midstream Oil and Gas Capital Investment(2) $122 Million

Net Cash provided by Operating Activities $1 Billion

Adjusted EBITDAX(2) $1.4 Billion

Earnings Per Share $0.21

Adjusted Earnings Per Share(2)(3) $0.63

(1) Excludes production attributable to Egypt tax barrels and noncontrolling interest.

(2) For a reconciliation to the most directly comparable GAAP financial measure please refer to the third quarter 2018 Financial & Operational Supplement.

(3) Includes $(0.04) per share of dry hole expense (net of tax).

263Q 2018 HIGHLIGHTS

Net cash from operating activities up 82% year-over-year to $1 billion

Strong oil price leverage: 79% of revenue from oil, nearly 70% of oil production received Brent- or Gulf

Coast-linked pricing

Adjusted production of 401 Mboe/d exceeded guidance by 3 Mboe/d

Delivering sustained quarterly production growth

Mboe/d 3Q’17 4Q’17 1Q’18 2Q’18 3Q’18

US 208 222 232 256 273

International 146 140 135 134 128

Total 354 362 367 390 401

(1) Excludes production attributable to divested assets and Egypt tax barrels and noncontrolling interest.

Cash return on invested capital of 23% on an annualized basis through the first three quarters of 2018

Share buybacks

Repurchased 0.9 MM of common stock in September; continued into 4Q 2018

Announcing new share repurchase authorization of an additional 40 MM shares

27UPSTREAM OPERATIONAL HIGHLIGHTS

3Q adjusted total production growth of 13% and Permian oil production

growth of 16%, year over year

Full-pattern development in the Midland/Delaware basin generating

significant cost and productivity improvements

Alpine High progress:

Drilling, completion and equipment costs per lateral foot down approximately 25% year

to date from 2017, in-line with our goal

Drilled first multi-well Bone Spring / Wolfcamp oil pad

Expanding Egypt inventory: fast-track processing of ongoing seismic shoot is

delivering very promising results

Accelerating development of the Garten oil discovery in the North Sea into the

fourth quarter

28QUARTERLY PRODUCTION GROWTH

Delivering Growth on Stabilized Activity Set

Adjusted Production (Mboe/d) Permian Oil Production (Mboe/d)

421

401

390

362 367

354

133

128

134

140 135

Int’l 146

95

90 90

85 85

273 288 78

256

222 232

U.S. 208

3Q17 4Q17 1Q18 2Q18 3Q18 4Q18E 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18E

Note: Adjusted Production excludes production attributable to divested assets and Egypt tax barrels & noncontrolling interest.

29QUARTERLY OIL & GAS CAPITAL INVESTMENT

Operating at a Stable and Efficient Activity Level

Quarterly Capital Investment ($MM)

Stabilized Rig Count (33 to 36) 1) Consistent upstream capital

1,000 investment level over prior 4 quarters

122

2) 3Q’18 upstream capital increase

800 119 143 115

116 reflects:

Timing of capital activity

600

Incremental lease acquisitions &

(2) extensions

(1) (3)

844 (4)

400

724 742

800

750 3) 4Q’18E upstream capital lower

719 717

Includes ~$65MM of ongoing lease

200 acquisition investments

4) 2019 quarterly upstream capital run

- rate expected to average $750MM

3Q 17 4Q 17 1Q 18 2Q 18 3Q 18 4Q 18E 2019E

Qtrly

Upstream Capital Midstream Capital

Note: Excludes noncontrolling interest in Egypt; 4Q 2018 and 2019 Alpine High midstream capital expected to be funded by Altus upon closing.

30WHAT TO EXPECT FROM APACHE IN 2019

Upstream capital investment of ~$3.0 billion

Adjusted production at high end of 410-440 Mboe/d guidance range

15% growth in the U.S. and 10% growth overall

Continue to return capital to shareholders

Flex activity levels with commodity price, overarching goal to achieve

positive free cash flow (inclusive of dividend)

31CURRENT GUIDANCE

32ADJUSTED PRODUCTION OUTLOOK

2018 Production Guidance Update (Mboe/d)

Annual Quarterly

FY 2018 guidance increased to

395 Mboe/d representing

421 13% growth from FY 2017,

including 27% growth in the US

401

395

390

4Q’18 guidance established at

367 421 Mboe/d representing

5% growth from 3Q’18

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

Note: Excludes production attributable to Egypt tax barrels and noncontrolling interest.

33ADJUSTED PRODUCTION OUTLOOK

2018 FY & Quarterly Production Guidance Update (Mboe/d)

TOTAL COMPANY

421

401 Establishing 4Q’18 guidance of 421 Mboe/d

395 390

Increasing 2018 guidance by 1 Mboe/d to 395 Mboe/d

367

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

U.S. 288

273

262 Establishing 4Q’18 guidance of 288 Mboe/d

256

Increasing 2018 guidance by 2 Mboe/d to 262 Mboe/d

232

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

INTERNATIONAL

Establishing 4Q’18 guidance of 133 Mboe/d

133 135 134 133 Decreasing 2018 guidance by 1 Mboe/d to 133 Mboe/d

128

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

Note: Total Company and International excludes production attributable to Egypt tax barrels and noncontrolling interest. 34PERMIAN PRODUCTION OUTLOOK

2018 FY & Quarterly Production Guidance Update (Mboe/d)

PERMIAN

241

222 Establishing 4Q’18 guidance of 241 Mboe/d

212 202 Increasing 2018 guidance by 2 Mboe/d to 212 Mboe/d

183

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

PERMIAN OIL 95

90 90 90 Establishing 4Q’18 guidance of 95 Mboe/d

85 Establishing 2018 guidance of 90 Mboe/d

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

ALPINE HIGH

68 Establishing 4Q’18 guidance of 68 Mboe/d

49 Decreasing 2018 guidance by 1 Mboe/d to 44 Mboe/d

44

32

26 2018 guidance decrease attributable to facilities

downtime in early 4Q

FY18E 1Q18A 2Q18A 3Q18A 4Q18E

35APA ADJUSTED PRODUCTION AND RETURNS

2018-2020 Outlook (Mboe/d)

475 - 510

410 - 440

395

350

20% 22%

18% CROIC

CROIC

CROIC

2017A 2018E 2019E 2020E

See Glossary of Referenced Terms in Appendix for a definition of Cash Return on Capital Invested (CROIC)

36PERMIAN PRODUCTION

2018-2020 Outlook (Mboe/d)

315 - 335

245 - 260

212

158

2017A 2018E 2019E 2020E

37ALPINE HIGH PRODUCTION

2018-2020 Outlook (Mboe/d)

160 - 180

85

85 - 100

44

9

2017A 2018E 2019E 2020E

38INT’L ADJUSTED PRODUCTION

2018-2020 Outlook (Mboe/d)

Shallow Decline

144

133 125 – 140 125 – 140

2017A 2018E 2019E 2020E

Note: Adjusted production excludes Egypt tax barrels and noncontrolling interest. Comprises North Sea and Egypt production.

39APPENDIX

40ALPINE HIGH: DISTINCT SOURCE ROCK AND PARASEQUENCE

INTERVALS

3rd BONE SPRINGS

Parasequences

High frequency,

rapidly rising and

falling sea level

environment

WOLFCAMP

UNCONFORMITY PENNSYLVANIAN

Tranquil marine

Source Rock

BARNETT

environment,

gradually rising

worldwide sea level WOODFORD

conditions ORGANIC SHALE PARASEQUENCE

CARBONATE DEBRIS FLOW

DEVONIAN

ORGANIC SHALE

Woodford + Barnett + Penn 3rd Bone Springs + Wolfcamp

Thick, laterally continuous deposition Higher variability with sweet spots

Oil, wet gas and dry gas windows Oil and wet gas windows

Minimal in-situ water Water wet rock

Indigenous, organic shale Indigenous shale and migrated hydrocarbons

41ALPINE HIGH: STRUCTURAL CROSS SECTION

NORTHERN FLANK CREST SOUTHERN FLANK

Evaporites

Transgressive Parasequences

7,500’

8,500’ OIL

8720

9,500’ 9210

9420

9130

???

9700

9760

9925 10820

10215

Transgressive Source Interval

10,500’ 10100

10460

10050

1160

11,500’ WET GAS

12,500’

Devonian High Stand

13270

13,500’ 13370

13970

DRY GAS

~60 miles

Note Vertical and horizontal scales are not equivalent.

42ALPINE HIGH: GEOLOGY OF THE SOUTHERN DELAWARE BASIN

IMMATURE

South

West

Alpine High North

East

Evaporites

5,000’

OIL

Bone Springs / Wolfcamp

10,000’

Penn / Barnett / Woodford Bone Springs / Wolfcamp

WET GAS

15,000’

20,000’ Alpine High:

Stable shelf (Paleo high)

DRY GAS

Prospective section in the wet gas and oil window

25,000’

Thermal maturation controlled by depth of burial

Low clay content and low ductility

30,000’

CLAY CONTENT

15% 40%

43ALPINE HIGH: ATTRACTIVE RICH GAS ECONOMICS

Representative fully burdened economics for rich gas wells in a development scenario (4,400’ lateral)

Typical Well Upper Range Well

EUR (Bcfe) 9 - 15 EUR (Bcfe) 16 - 21

Well Cost ($MM) $4 - $6 Well Cost ($MM) $4 - $6

Product Mix Product Mix

% Oil 3% - 15% % Oil 0% - 8%

% NGL 51% - 56% % NGL 41% - 54%

Fully Burdened Economics @ $65 WTI / $3.00 HH Fully Burdened Economics @ $65 WTI / $3.00 HH

BTAX NPV-10 ($MM) $7 - $9 BTAX NPV-10 ($MM) $6 - $13

BTAX IRR % 50% - 100% BTAX IRR % 78% - 300%

Fully Burdened Economics @ $50 WTI / $2.50 HH Fully Burdened Economics @ $50 WTI / $2.50 HH

BTAX NPV-10 ($MM) $4 - $6 BTAX NPV-10 ($MM) $3 - $9

BTAX IRR % 29% - 66% BTAX IRR % 38% - 158%

Single Well Economic Assumptions:

• Prices: $65 WTI / $3.00 Henry Hub / NGL($/GAL) C2: $0.28, C3: $0.83, C4: $0.94, C5: $1.42 • Crude basis: $2.25

$50 WTI / $2.50 Henry Hub / NGL($/GAL) C2: $0.28, C3: $0.75, C4: $0.90, C5: $1.22 • NGL yields and midstream fees assume cryogenic processing

• Waha basis / Transport to US Gulf Coast markets = $0.50/MMbtu; midstream fee = $0.87/Mcf • Economics include overhead, workover, abandonment and E&P facility burdens

44ALPINE HIGH: PREMIUM CAPITAL EFFICIENCY

Top-tier recycle ratios highlight ability to generate cash and re-invest

Typical Well Upper Range Well

$/BOE

30 30 580%

recycle

433% ratio

24.78 10.49

25 recycle 25

OIL ratio

$62.75 21.16 9.79

20 20 $62.75

15 14.29 15

NGL $21.51

$24.33 11.37

10 10

5 3.30 5

$2.81

$2.84 GAS 1.96

- -

Revenue Opex Cash Margin F&D Revenue Opex Cash Margin F&D

Highly prolific wells and low costs result in impressive recycle ratios

Assumptions:

• Prices: $65 WTI; $3.00 Henry Hub; Waha basis ($0.50); NGL($/GAL) C2: $0.28, C3: $0.83, C4: $0.94, C5+: $1.42 • F&D reflects drilling, completion, and equipping

• Opex includes LOE, Gathering, Transportation & Processing, and Production taxes • Recycle Ratio: Cash Margin/F&D

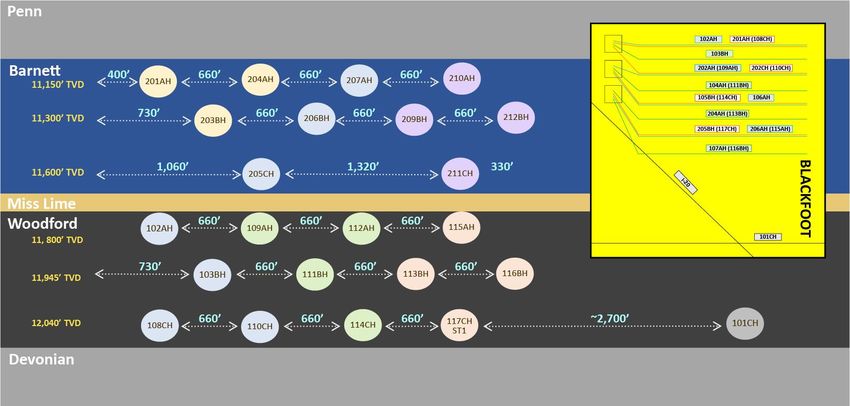

45ALPINE HIGH: DOGWOOD SPACING TEST

(NOT TO SCALE)

WELLBORES COLORED BY BATCH PAD

46ALPINE HIGH: BLACKFOOT PATTERN & SPACING TEST

(NOT TO SCALE)

To Be

Drilled

WELLBORES COLORED BY BATCH PAD

472018-2019 PERMIAN BASIN GAS POSITIONING

Production Flow Risk Price Exposure

2018 2019 2018 2019

Uncommitted Firm Transport Firm Transport

Production 9% 8% Other

12% Basin

Firm Other

Basin Firm 4%

Uncommitted Transport

7% Transport

Production 21%

21%

20%

Basis

Hedges

Contracts / Dedicated Contracts / EP Perm / Waha 20% EP Perm / Waha Basis

Sales Dedicated Sales Index Index Hedges

79% 59% 65% 60% 15%

Firm transport and other basin-based contracts generally access Gulf Coast Pricing

Waha basis hedges average approximately $0.51 per MMBtu for 4Q 2018 - 2019

482018-2019 PERMIAN BASIN OIL POSITIONING

Production Flow Risk Price Exposure

2018 2019 2018 2019

Basis

Hedges

4%

West

West Basis

Texas

Texas Hedges

Sour

Sour 24%

26% GC/Cushing

Term

29% Term Sales

Based Midland Midland

Sales 49% GC/Cushing

38% Based Based

52% Diversified Diversified Based 62%

58%

Evergreen Evergreen 14%

Sales Sales

19% 25%

▪ Term sales backed by customers’ firm transport ▪ Contracts provide various options for higher of Gulf

Coast/Cushing/Midland pricing

▪ West Texas Sour less subject to oversupply and takeaway

capacity constraints than WTI ▪ In 3Q, added 12,000 bbls/d WTI Midland basis swaps for

Q1 2019 – Q3 2019

▪ Diversified evergreen sales represent agreements with

multiple buyers across multiple systems(1)

(1) Consists of approximately 22 contracts with 10 counterparties of varying term lengths; subject to cancellation, but only with a minimum of 30 days notice. 49GLOSSARY OF REFERENCED TERMS

Capital Investment Budget: Includes exploration and production capital, gathering, transmission, and processing

capital, capitalized general and administrative expenses, capitalized interest and asset retirement obligations

settled. Excludes non-cash asset retirement additions and revisions and noncontrolling interest

CROIC (Cash Return On Invested Capital): Calculated with the numerator as cash flow from operations before

changes in working capital, excluding noncontrolling interest, with financing costs added back; and the

denominator as average debt plus average Apache shareholders’ equity

Net Debt: Total debt (long-term and short-term) less cash and cash equivalents

ROCE (Return on Capital Employed): Calculated with the numerator as adjusted earnings plus financing costs and

taxes (excluding Egypt taxes); and the denominator as average debt plus average Apache shareholders’ equity

In addition to the terms above, a list of commonly used definitions and abbreviations can be found in Apache’s form

10-K for the year ended December 31, 2017.

50You can also read