CASTROL INDIA LTD - MARKETSMOJO

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Castrol India Ltd November 06, 2018

Market Cap. 52 Week H/L CMP Target Price

Castrol India Ltd Rs. 12,364 Cr Rs. 162/90 Rs. 125 Rs. 155

Personal Mobility to continue to drive the growth: The Management has been focused on ‘Personal Mobility’ segment which

STOCK DATA

has been a key growth driver on account of huge traction in the two-wheelers and four-wheelers. Accordingly, the share of this

Recommendation BUY segment has increased from ~10% to ~45% driven by strong brand recognition, consistent increase in the realizations per litre

due to its B2C business model and higher blending cycles. Going forward, the company expects the segment to remain a key

Reuters Code CAST.BO

strategic priority as the rural segment of the country as it still offers a huge opportunity in the two-wheelers space. Additionally,

Bloomberg Code CSTRL IN

the drain intervals for passenger vehicles extend at a lower rate than commercial vehicles.

BSE Code 500870 Strategic collaborations to aid growth in future: During previous year, the company joined hands with a global player, 3M to

NSE Symbol CASTROLIND bring a range of market leading vehicle care products in the Indian automotive after-market. This collaboration will enable the

Face Value Rs. 5 company to offer 3M’s branded car and bike care products, such as shampoo, glass cleaners, cream wax, dashboard and tyre

Shares dressers, etc, across the country through its pan-India marketing & distribution network comprising of over 100,000

98.9 Cr

Outstanding* independent workshops & retail outlets.

Avg. Daily 20,21,471 Recent fall in crude prices to benefit the company to a great extent: A substantial portion of the base oils and additives that

Volume (6m) shares are used in manufacturing of lubricants are imported due to its shortage in the domestic market. Them being derivatives of

Price Performance (%) crude oil exposes the company to not only price risk but also to forex risk. Oil price and gross margins of lubricant companies

are inversely related.

1M 3M 6M

33 (5) (7) OUTLOOK & VALUATION

200 Days EMA Rs. 133

The lubricants industry has witnessed a huge transition from volume-to-value, yet, the Indian lubricants industry still

remains one of the fastest growing amongst the world. The leadership position of Castrol India, back-up by the robust

* On fully diluted equity Shares

international parent, strong fundamentals and consistent technological advancements keeps the company best placed

SHARE HOLDING (%) to benefit from the opportunity in Personal Mobility, Commercial Vehicles and Industrials segments. The company is

Promoters 51.0 expanding capacities and the Management is confident of stable and steady growth over the next few years. However,

FII 12.2 the unprecedented event of Covid-19 has brought the world to standstill and accordingly, we expect volumes to

witness steep fall during the current year only to register a good bounce back in the next year. Going forward, we

FI/Bank 17.6

expect company to deliver an EPS of Rs.9.1 in CY 2022; assigning a target multiple of 17x, which is below its median

Body Corporate 1.2

P/E of last 1, 3 and 5 Years; we arrive at a target price of Rs.155 showcasing an upside potential of 24% from current

Public & Others 18.1

levels with an investment horizon of 18-24 months.

Revenue EBITDA EBITDA PAT NPM A-EPS P/E P/S P/B

Y/E Mar

(Rs. Cr) (Rs. Cr) Margin (%) (Rs. Cr) (%) (Rs.) (x) (x) (x)

CY 2019 3,876.8 1,153.0 29.7% 827.4 21.3% 8.4 14.9 3.2 9.0

CY 2020 E 3,163.5 860.5 27.2% 623.8 19.7% 6.3 19.8 3.9 8.8

CY 2021 E 3,728.9 1,040.4 27.9% 762.3 20.4% 7.7 16.2 3.3 8.4

CY 2022 E 4,322.6 1,223.3 28.3% 902.4 20.9% 9.1 13.7 2.9 7.8

# Scrips part of Sushil’s Bonanza 2

April 24, 2020

Castrol India Ltd.

Company Overview

Castrol India, a step-down subsidiary (51%) of UK based BP Plc has an operating history of a hundred years in India now. It is one of the oldest and widely

known brands in the country. Though the new name ‘Castrol’ evolved in 1960 but this lubricant producer has been associated with the Indian

automotive industry soon after this industry started setting up its feet here. Today, the company is a leading lubricants company and has established

itself as a pioneer and innovator in the Indian lubricants industry.

The company operates 3 manufacturing facilities (Navi Mumbai, Silvassa, and Kolkata) and markets automotive, industrial, marine & energy lubricants,

distributed through more than 350 distributors from over 100,000 retail outlets. The company also leverages its distribution network to reach a wider

network through Castrol Bike Points, Castrol Car Care, Castrol Pit Stops, Castrol Authorized Service Associates and Independent workshops. Castrol sub-

distributors also reach additional outlets in rural markets whilst the company also directly services over 3,000 key institutional accounts. The company

has an inclusive and innovative outreach program to connect and engage with key consumers, customers and influencers.

Apart from its own production, the company also has third-party tie-ups to fill some of the products which they do not manufacture. In total, the

company has a capacity of 280 million litres across different segments. During 2019, the company produced and sold nearly 204 million litres of

lubricants and oils commanding a volume market share of ~18%. According to the Management, at the end of the calendar year, the capacity utilization

stood at ~80%. There were no significant exports by the company during the previous year barring some small quantities of its products were exported

to Malaysia, China, Thailand and Indonesia.

For the CY2019, the company reported a turnover of Rs.3,876.8 cr and an EBITDA of Rs.1,153.0 cr (EBITDA margin of 29.7%) and a net profit of Rs.827.4

cr translating into an EPS of Rs.8.37 per share. For the year, the dividend declared stood at Rs.5.50 per share (110% of FV of Rs.5)

After quitting a job at Vacuum Oil in 1899, Charles Wakefield founded CC Wakefield & Company to start a new business of selling lubricants. His

researchers found that adding a measure of castor oil resulted in oils that were runny enough to work from cold at start-up and thick enough to keep

working at very high temperatures – much required for new engines for automobile and aero-planes. They called the new product ’Castrol’. By 1960,

the name of the motor oil eclipsed the name of the company and the founder thereby, becoming, Castrol Ltd. In 1966, The Burmah Oil Company

bought Castrol and in 2000 Burmah-Castrol was purchased by BP. During 2016, BP’s wholly owned subsidiary Castrol parted stake in Castrol India in

two tranches of 11.5% in May and 8.5% in September bringing down its stake in the company to 51.0%. That time BP had divested some of its global

assets amidst weak crude oil prices which negatively impacted its bottom line. In the first half of 2016, BP had globally divested assets worth USD 1.9

bn, including the partial sale of its interest in Castrol India in May.

April 24, 2020 3

Castrol India Ltd.

Business Overview

The products of the company help in reducing friction, and thus, noise and heat generated by metallic friction in engines and motors in the automotive

industry and cutting or honing parts in industrial applications. Additionally, detergents & dispersants in a lubricant help cleaning, while anti-wear agents

help protect the metal surface from wear and tear as well as corrosion. Automotive vehicles require engine oils, transmission fluids, brake fluids,

hydraulic oils & greases, while industrial & manufacturing applications require lubricants for metal working, rust preventives & coolants.

The lubricants are manufactured by blending base oils, either mineral-based or synthetic based oils and additives, with base oil being the primary

component. They are blended following advanced formulations as per the specifications based on purpose the lubricant serves. These formulations are

also customized as per the requirements of OEMs and the industry norms. With India being a net base-oil deficit market as well as many additives are

not available locally, base oils & additives are imported on a large scale, which exposes the lubricants business to fluctuations in foreign exchange rates.

As mentioned earlier, the company through its three manufacturing facilities and other arrangements holds a total capacity of 280 Mn litres across all

the segments. Further, the company is currently undergoing an expansion at its Silvassa plant. This investment program will increase the capacity of the

plant by 50% from 80 million litres to 120 million litres by 2021. This capex program of Rs.140 Cr spanned over two years would take the total capacity

to 320 million litres.

The company enjoys strong brand power amongst consumers and mechanics. Some of the company’s iconic brands are Castrol CRB, Castrol GTX, and in

more recent times power brands like Castrol Activ, Castrol MAGNATEC and Castrol VECTON.

Source: Investor Presentation, Company Data; Sushil Finance

April 24, 2020 4

Castrol India Ltd.

Business Overview

Revenue Mix (2019) –Addressable Market Revenue Mix (2019)- Product Wise

13% 12%

Personal Mobility

Industrials

43% 45% Industrials

Bazaar

B2B CVO & Heavy

Duty

75% 12%

Volume Growth (Mn litres) Blended Realization/ litre (INR)

215.0 213.7 195.0 190.0

190.0

210.0 182.7

185.0

204.6 204.0

205.0 180.0 175.2

199.3 175.0

200.0 169.1

170.0

195.0 165.0

160.0

190.0

155.0

CY 2016 CY 2017 CY 2018 CY 2019

CY 2016 CY 2017 CY 2018 CY 2019

Source: Company Data, Sushil Finance

April 24, 2020 5

Castrol India Ltd.

Business Overview

Technology: The company has always been a pioneer in introduction of latest technologies in its product basket, thereby, recording several innovation in

its name. Castrol was the first company in the country to introduce a long-drain multi-grade engine oil approved by Maruti when it first launched its cars

in India. The company has always attempted to come up with longer drain products based on customer requirements. In the recent years, the company

had introduced a new premium product for its commercial vehicle segment, named, Castrol Vecton Long Drain. This diesel engine oil product claims to

deliver a 45% extra performance reserve that fights oil-breakdown by controlling oxidation, reducing deposits, and neutralizing harmful acids. This

means longer useful oil life, and thus substantially lower operating costs. Similarly, during 2018, the latest generation of Castrol Magnatec Stop-Start

engine oil with breakthrough Dualock technology was launched.

Branding: Apart from consistent technological up-gradations, the company focuses on branding and promotions. The company has consistently been

running television commercials, field-campaigns, and sponsorships. For the year ended December 31, 2018, the company had spent Rs.127.9 cr (3.3%)

on advertising as against Rs.112.7 cr (3.1%) in the previous year. In addition, the company also spent Rs.124.1 cr (3.2%) in 2018 as against Rs.124.6 cr

(3.5%) in 2017 on sales promotions. The numbers for 2019 were not available as the Annual Report for 2019 was not published till the time this report

was written. Going forward, the company is likely to increase this expenditure with an objective to gain market share, specially in the ‘Personal Mobility’

segment which faces stiff competition.

Royalty: The royalty to Castrol Ltd, UK is currently pegged at 3.5% of sales subject to maximum of 10% of the profits. During 2018, the company paid a

royalty of Rs.111.4 cr (2.9%) as against Rs.106.0 cr (3.0%) during the previous year.

Raw Material: A substantial chunk of the base oils and additives which are used in manufacturing of lubricants, being unavailable or deficit in the

country are imported. Most of these base-oils and additives are derivatives of crude oil and thus, the company is exposed not only to the prices of crude

oil but exchange rate well. The raw material comprises 45.1% of CY2019 sales as against 48.8% in CY2018 led by fall in crude prices & lower volumes.

Key OEM Clientele

Source: Investor Presentation, Company Data; Sushil Finance

April 24, 2020 6Castrol India Ltd.

Business Overview

Revenue & Revenue Growth EBITDA & EBITDA Margin

4,500 10.0%

1400 35.0%

4,000 8.0%

3,500 1200 30.0%

6.0% 1000 25.0%

3,000

2,500 4.0% 800 20.0%

2,000 2.0% 600 15.0%

1,500

0.0% 400 10.0%

1,000

500 -2.0% 200 5.0%

- -4.0% 0 0.0%

2013 2014 2015 2016 2017 2018 2019 2013 2014 2015 2016 2017 2018 2019

Revenue (Rs. Cr) Growth EBITDA EBITDA %

Gross Margin Earnings & Dividend Per Share

60.0% 10.00

55.0%

8.00

8.37

50.0%

7.16

6.00

6.99

6.78

45.0%

6.22

5.14

40.0% 4.00

4.80

35.0%

2.00

3.50

3.75

4.50

5.50

4.75

5.00

5.50

30.0%

2013 2014 2015 2016 2017 2018 2019 -

2013 2014 2015 2016 2017 2018 2019

Gross Margin

EPS DPS

Source: Company Data, Sushil Finance

April 24, 2020 7Castrol India Ltd.

Industry Overview

India is the third largest lubricant market after the US and China. It is also one of the fastest growing lubricant markets worldwide. The total lubricants

market is comprised of three segments - automotive, industrial and process oils. According to the industry reports, the Indian lubricants sector is a 3

billion litres market with the automotive segment holding 42% share, industrial 23%, transformer and white oils 23%, process oils 8%, and greases 4%.

Of more than 20 players present in the industry, the three public sector undertakings namely BPCL, HPCL and IOC along with leading private sector

player Castrol commands nearly 55% market share. The international brands like Total, Shell, Mobil, Valvoline, Motul command another ~20% and the

remaining ~25% is with other domestic private players like Gulf Oil Lubricants India, Tide Water Oil, Savita Oil, etc. In value terms, the entire lubricants

industry is roughly valued at USD 6.5-7.0 bn i.e. roughly Rs.50,000 cr. According to industry reports, the lubricants industry in India is expected to grow

at an annual growth of 4-5% over the next few years.

During FY19, even though the lubricant market in the country recorded a positive growth but continued to witness stiff competition among players

leading to an overall shift in perception of lubricants market from volume driven to value driven. The major factors driving the growth of the market

are the increasing vehicular population along with the growing industrial sector. During the fiscal, the overall domestic vehicles sales grew at 5.1% YoY

to 2.62 cr units including 33.77 lakh Passenger Vehicles (+2.7%), 10.07 lakh Commercial Vehicles (+17.6%), 7.01 lakh Three Wheelers (+10.3%) and

211.81 lakh two-wheelers (+4.9%). On the industrial front, the India industrial lubricant market stood at USD 1.28 bn in 2017 and is projected to grow

steady at a middle single digit growth rate on account of initiatives being taken by the government towards infrastructure development and growing

focus of manufacturers on expanding their production capacities. With huge amount being planned to spent on upgrading infrastructure facilities

across the country and developing new ports and airports are anticipated to drive the industrial lubricant market in India over the next few years.

Global Volumes Indian Volumes

24% 16% CV

30% CV 30%

Industrial Industrial

Personal Mobility

45% 52% Personal Mobility

Source: MotorIndiaOnline

April 24, 2020 8Castrol India Ltd.

Industry Overview

Industry Structure – Market Share (FY19) Domestic Sales Trend in Indian Automobile Industry (Lakhs)

250

202 212

4%

13% 3% 200 176

160 165

148

150

100

80%

50 25 26 28 30 33 34

6 5 6 5 7 5 7 5 9 6 10 7

-

FY14 FY15 FY16 FY17 FY18 FY19

Passenger Vehicles Commercial Vehicles Passenger Vehicles Commercial Vehicles

Three Wheelers Two Wheelers Three Wheelers Two Wheelers

Volume Growth in Indian Domestic Sales Export Trend (Lakhs)

30.0% 100%

80%

20.0% 21 25 25 23 28 33

60%

10.0% 40%

4 4 4 3 4

20% 1 1 1 1 1 6

0.0% 1

6 6 7 8 7 7

FY15 FY16 FY17 FY18 FY19 0%

FY14 FY15 FY16 FY17 FY18 FY19

-10.0%

Passenger Vehicles Commercial Vehicles Three Wheelers Passenger Vehicles Commercial Vehicles

Two Wheelers Total Three Wheelers Two Wheelers

Source: SIAM, Sushil Finance

April 24, 2020 9Castrol India Ltd.

Investment Rationale

Personal Mobility to continue to drive the growth: Over the last 10-15 years, the Management has been focused

on ‘Personal Mobility’ segment which has been a key growth driver on account of huge traction in the 2Ws & 4Ws. “With multiple opportunities in

Accordingly, the share of this segment has increased from ~10% to ~45% driven by strong brand recognition, personal mobility driven by

consistent increase in the realizations/litre due to its B2C business model & higher blending cycles. Going forward, increase in first time users,

the company expects the segment to remain a key strategic priority as the rural segment of the country as it still growing number of women

offers a huge opportunity in the two-wheelers space. Additionally, the drain intervals for passenger vehicles extend riders, as well as a continuing

at a lower rate than commercial vehicles. With multiple opportunities in personal mobility driven by increase in shift towards higher quality

first time users, growing number of women riders, as well as a continuing shift towards higher quality formulations formulations and lighter viscosity

and lighter viscosity grades, the company is well placed to tap this potential. The consistent investments in grades, Castrol India is well

branding and promotions is likely to drive sales & realizations resulting into top-line growth and margin expansion placed to tap this potential.”

with rising contribution. Additionally, the customized offerings of value-added packs and wider distribution reach

have also contributed to this growth. Personal mobility has been posting consistent & steady growth, thereby,

improving the product-mix and also making up for low growth in other segments like Industrials, CVO & Heavy

Duty. Further, according to Management Interview as given to MotorIndia, the contribution of personal mobility

segment is 24% globally & 16% in India also showcases the growth potential.

Strategic collaborations to aid growth in future: During previous year, the company joined hands with another

global player, 3M to bring a range of market leading vehicle care products to the Indian automotive after-market. “Through this collaboration, we

The company has collaborated with 3M India to offer the latter’s branded car and bike care products such as enter into the $200 mn vehicle

shampoo, glass cleaners, cream wax, dashboard and tyre dressers, etc. across the country through its pan-India care market in India, a move

marketing & distribution network of over 100,000 independent workshops & retail outlets. The Management which aligns with Castrol's

stated that the size of Indian vehicle care market is estimated to be around USD 200 mn (Rs.1,400-1,500 cr) and is approach to developing and

rapidly growing. Moreover, the company has tie-ups with OEMs for supply of original oils & endorsements. embracing new business models

Recently, the company had signed a strategic partnership with Renault India for supply of exclusive after- in the ever-evolving automotive

sales engine oil lubricants across it's pan-India network. Castrol India gets advantage from exclusive tie-ups with landscape,"

OEMs due to global tie-ups of auto companies with BP Plc. Furthermore, the company’s marketing endeavors also ------- Castrol India

likely to strengthen company’s business. For instance, the company had announced Castrol FastScan, a digital

incentive platform for key stakeholders including mechanics and retailers. It helps retailers/mechanics to earn,

track & redeem rewards, and receive them instantly in their bank account using IMPS, leading to significant

simplification and shortening of the incentive payment cycle from months to minutes.

April 24, 2020 10Castrol India Ltd.

Investment Rationale

Timely technological advancements continue to be a strength: As mentioned earlier, the company has been a

“Castrol has already developed a

pioneer in the lubricants industry and has registered several firsts in its name. The company has always been

proactive in matching the pace with the technological advancements changing the automotive world. The company wide range of EV fluids for

benefits from the technological and scientific expertise from BP Plc, which works through its 7 global R&D centers international markets and these

fluids will be available to Castrol

in the US, UK, Germany, China, & Japan. For instance, the company became the first Indian player to have a

India”

complete range of BS-VI compliant portfolio which is also backward compatible as this would be phased evolution

over the next few years. From a practical perspective, the BS-IV to BS-VI leap has resulted into the need of

lubricants compatible with the new after-treatment devices being adopted by OEMs, as well as the ability to

handle more stress as a result of internal emissions control technology. This means new products specially

formulated with lower sulphated ash and phosphorous while maintaining the same durability. Similarly, on electric

vehicle front, although the company believes that EV adoption will be faster but conventional internal combustion

engines are likely to co-exist, as well, for a long-time – rather the Management expects internal combustion

engines to still dominate for decade to come and grow substantially over the next decade. Nevertheless, Castrol,

globally, has already developed a wide range of EV fluids including transmission fluids, battery coolants and greases

which would be available to Castrol India proving to be a great benefit.

Robust fundamentals, strong leadership & wider reach to benefit: Castrol India is a debt free company with

As on December 31, 2019, Castrol

strong cash generation. The robust business model coupled with brand image results into strong realizations and

India is a zero-debt company and

stable profitability. The company generates healthy operating cash flows to the tune of Rs.550-650 cr annually and

holds cash and cash equivalents

most of which flows towards the dividends payout. The company has been kind in issuing bonuses as well; over the

of Rs.946.1 cr. Additionally, the

past thirty years the company has issued 8 bonuses comprising 98% of its current equity. Furthermore, as on

strong operating cash-flows flow

December 31, 2019, this zero-debt balance sheet holds cash and cash equivalents of Rs.946.1 cr translating into

to dividend payouts.

Cash Per Share of Rs.9.57. Apart from being a financially strong company, the company also enjoys benefits of

having an internationally strong parent which consistently helps the company with research and technology.

Furthermore, the company has strong distribution network of more than 350 distributors from over 100,000 retail

outlets. The company also leverages its distribution network to reach a wider network through Castrol Bike Points,

Castrol Car Care, Castrol Pit Stops, Castrol Authorized Service Associates and Independent workshops. The

premium quality, consistent branding and promotional campaigns and regular workshops and reward programs for

mechanics and garages helps the company to retain this market share. Going forward, the company is well

positioned to give away some of its margins to gain market share.

April 24, 2020 11Castrol India Ltd.

Investment Rationale

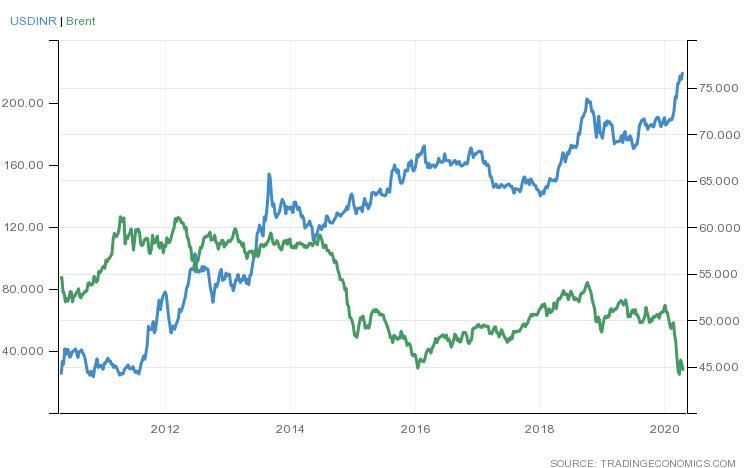

Recent fall in crude prices to benefit the company to a great extent: As mentioned earlier, a substantial chunk of

the base oils and additives which are used in manufacturing of lubricants, being unavailable or deficit in the

country are imported. Most of these base-oils and additives are derivatives of crude oil and thus, the company is

exposed not only to the prices of crude oil but exchange rate well. When oil prices decline the lubricant

companies gross margins/litre goes up. During the recent past, the crude oil prices witnessed a steep fall

nevertheless, the Indian Rupee has further weakened as well (showcased in the chart on the right side). Thus,

the margin expansion on account of substantially lower crude oil and its derivates would be partially offset by the

weak INR against USD. If base oil prices soften further or sustain at present level, it may lead to further gross

margin expansion. In any case, the gross margins are not likely to go up. Over the past decade, the change in

product-mix, technological advancements and decrease in crude oil prices led to increase in gross margins from Major fall was witnessed during

41.5% in CY 2012 to 54.9% in CY 2019. Since last one year, the Brent crude feel from ~$75/Bbl in April, 2019 to the past one month when the

~$25/Bbl in April, 2020. More importantly, the major fall was witnessed during the past one month when the price of Brent crude halved from

price of Brent crude halved from $56/Bbl in the mid of February, 2020 to $28/Bbl in mid of April, 2020. $56/Bbl in the mid of February

Brent vs USD INR Raw Material Cost, as a percentage of Revenue

70.0%

60.0%

50.0%

40.0%

30.0%

20.0% 58.5%

56.2%

57.1%

48.5%

45.4%

46.5%

48.8%

45.1%

10.0%

0.0%

2012 2013 2014 2015 2016 2017 2018 2019

Source: Trading Economics, Company Data, Sushil Finance

April 24, 2020 12Castrol India Ltd.

Peer Comparison

Sales EBITDA Net D/E CMP* 52 Week Mkt Cap Enterprise P/E P/S P/B EV/

(Rs. Cr) Margin Margin (x) (Rs.) H/L (Rs.) (Rs. Cr) Value (x) (x) (x) EBITDA

(%) (%) (Rs. Cr) (x)

Castrol India 3,877 29.7% 21.3% - 125 162/90 12,364 11,418 14.9 3.2 9.0 9.9

Gulf Oil Lubricants 1,720 17.8% 12.5% 0.47x 586 910/450 2,784 2,709 13.0 1.7 4.2 9.1

(India)

Tide Water Oil 1,375 10.8% 9.2% 0.05x 3,494 5,300/2,550 1,210 1,561 9.6 0.9 1.8 7.2

(India)

Source: Sushil Finance

Outlook & Valuation

Over the last decade, the lubricants industry has witnessed a huge transition from volume-

to-value, yet, the Indian lubricants industry still remains one of the fastest growing amongst

the world. The leadership position of Castrol India, robust back-up by the parent, strong

fundamentals and consistent technological advancements keeps the company best placed

to benefit from the opportunity in growth in Personal Mobility, Commercial Vehicles and

Industrials segments. The company is expanding capacities and the Management is

confident of stable and steady growth over the next few years. However, the

unprecedented event of Covid-19 has brought the world to standstill and accordingly, we

expect volumes to witness steep fall during the current year only to register a good bounce

back in the next year. Going forward, we expect company to deliver an EPS of Rs.9.1 in

CY2022; assigning a target multiple of 17x, which is below its median P/E of last 1 year, 3

Years and 5 Years, we arrive at a target price of Rs.155 showcasing an upside potential of

24% from current levels with an investment horizon of 18-24 months.

April 24, 2020 13Castrol India Ltd.

PROFIT & LOSS STATEMENT (Rs.Cr) BALANCE SHEET STATEMENT (Rs.Cr)

Y/E Mar. CY19 CY20E CY21E CY22E As on 31st Mar. CY19 CY20E CY21E CY22E

P,P&E (including WIP) 224.7 236.0 251.3 298.1

Revenue 3,876.9 3,163.5 3,728.9 4,322.6

Other Intangibles 2.3 1.6 1.6 1.6

Raw material cost 1,747.7 1,423.6 1,678.0 1,945.2

Other Non-current Assets 166.3 169.3 169.3 169.3

Employee cost 213.1 215.1 227.5 246.5

Inventories 304.7 253.5 298.8 346.4

Other Expenses 763.0 664.3 783.1 907.7 Trade Receivables 482.0 346.7 408.7 473.7

EBITDA 1,153.0 860.5 1,040.4 1,223.3 Cash & Bank Balances 946.1 964.3 1,008.7 1,061.5

Other Financial Assets 24.0 23.5 23.5 23.5

Depreciation 69.7 74.2 77.9 82.9

Other Current Assets 78.7 63.3 74.6 86.5

EBIT 1,083.3 786.3 962.5 1,140.4

Total Assets 2,228.8 2,058.2 2,236.1 2,460.5

Finance Costs 1.2 2.0 2.0 2.0

Equity Share Capital 494.6 494.6 494.6 494.6

Other Income 64.8 47.5 55.9 64.8 Reserves & Surplus 872.4 902.8 972.2 1,083.8

PBT 1,146.9 831.8 1,016.4 1,203.2 Provisions 21.4 15.9 15.9 15.9

Tax Expense 319.5 207.9 254.1 300.8 Other non-current - - - -

Borrowings (ST) - - - -

Adjusted Net Profit 827.4 623.8 762.3 902.4

Trade Payables 471.8 351.0 413.8 479.6

EPS 8.37 6.31 7.71 9.12

Other Financial Lia 241.2 189.8 223.7 259.4

CEPS 9.07 7.06 8.49 9.96 Other current liabilities 127.4 104.1 115.4 127.3

DPS-Not Required 5.50 6.00 7.00 8.00 Total Liabilities 2,228.8 2,058.2 2,236.1 2,460.5

Source: Company, Sushil Finance Research Estimates

April 24, 2020 14Castrol India Ltd.

CASH FLOW STATEMENT (Rs.Cr) FINANCIAL RATIO STATEMENT

Y/E Mar. CY19 CY20E CY21E CY22E Y/E Mar. CY19 CY20E CY21E CY22E

PBT 1,146.9 831.8 1,016.4 1,203.2 Growth (%)

Revenue (0.7) (18.4) 17.9 15.9

Depreciation & Amortization 69.7 74.2 77.9 82.9

EBITDA 7.7 (25.4) 20.9 17.6

Finance Cost 1.2 2.0 2.0 2.0 16.8 (24.6) 22.2 18.4

Net Profit

Chg. in Inventories 152.1 51.2 (45.3) (47.6) Profitability (%)

Chg. In Receivables (90.2) 135.3 (62.0) (65.1) EBIDTA Margin (%) 29.7 27.2 27.9 28.3

Net Profit Margin (%) 21.3 19.7 20.4 20.9

Chg. In Payables (112.3) (120.8) 62.7 65.9

ROCE (%) 79.2 56.3 65.6 72.2

Other Changes in WK - - - - 60.5 44.6 52.0 57.2

ROE (%)

Net Operating Cash Flow 1,167.4 973.6 1,051.8 1,241.4 Per Share Data (Rs.)

Capex (75.0) (85.4) (93.2) (129.7) A-EPS (Rs.) 8.4 6.3 7.7 9.1

CEPS (Rs.) 9.1 7.1 8.5 10.0

Change in current invest (10.2) - - -

BVPS (Rs) 13.8 14.1 14.8 16.0

Others 1.0 (0.7) 0.7 - Valuation

Cash Flow from Investing (85.8) (84.8) (93.2) (129.7) PER (x) 14.9 19.8 16.2 13.7

P/BV (x) 9.0 8.8 8.4 7.8

Change in Others (879.4) (870.6) (914.6) (1,058.5) 9.9 13.3 11.0 9.3

EV/EBITDA (x)

Change in Borrowings - - - - P/ Sales (x) 3.2 3.9 3.3 2.9

Turnover

Cash Flow from Financing (879.4) (870.6) (914.6) (1,058.5)

Inventory Days 64 65 65 65

Opening Cash 743.9 946.1 964.3 1,008.3 Debtor Days 45 40 40 40

Creditors Days 99 90 90 90

Cashflow during the year 202.2 18.2 44.0 53.2

Gearing Ratio

Cash at the End of the Year 946.1 964.3 1,008.3 1,061.5 D/E - - - -

Source: Company, Sushil Finance

April 24, 2020 15Research Analyst Sales:

Saurabh Jain | +91 22 4093 4004 Devang Shah | +91 22 4093 6060/62

saurabh.jain@sushilfinance.com devang.shah@sushilfinance.com

Rating Scale

This is a guide to the rating system used by our Institutional Research Team. Our rating system comprises of six rating categories, with a corresponding risk rating.

Risk Rating

Risk Description Predictability of Earnings / Dividends; Price Volatility

Low Risk High predictability / Low volatility

Medium Risk Moderate predictability / volatility

High Risk Low predictability / High volatility

Total Expected Return Matrix

Rating Low Risk Medium Risk High Risk

Buy Over 15 % Over 20% Over 25%

Accumulate 10 % to 15 % 15% to 20% 20% to 25%

Hold 0% to 10 % 0% to 15% 0% to 20%

Sell Negative Returns Negative Returns Negative Returns

Neutral Not Applicable Not Applicable Not Applicable

Not Rated Not Applicable Not Applicable Not Applicable

Please Note

• Recommendations with “Neutral” Rating imply reversal of our earlier opinion (i.e. Book Profits / Losses).

• ** Indicates that the stock is illiquid With a view to combat the higher acquisition cost for illiquid stocks, we have enhanced our return criteria for such stocks by five

percentage points.

• Stock Review Reports: These are Soft coverage’s on companies where Management access is difficult. Views and recommendation on such companies may not

necessarily be based on management meeting but may be based on the publicly available information and/or attending Company AGMs. Hence Stock Reviews may be

just one-time coverage’s with an occasional Update, wherever possible.

…

Sushil Financial Services Private Limited

Regd. Office : 12, Homji Street, Fort, Mumbai 400 001.

Phone: +91 22 40936000 Fax: +91 22 22665758

Email : info@sushilfinance.com

16Disclaimer & Disclosures :

https://www.sushilfinance.com/Disclamier/research

Member : BSE / NSE - SEBI Regn. No. INZ000165135

Research Analyst – SEBI Registration No. INH000000867

http://goo.gl/1sOHeV

This report has been furnished to you for your general information only and should not be reproduced, re-circulated, published in any media, website or otherwise, in any form or manner, in

part or as a whole, without the express consent in writing of Sushil Financial Services Private Limited. This Research Report is meant solely for use by the original recipient to whom it is sent and

is not for circulation. Any unauthorized use, disclosure or public dissemination or copying of information (either whole or partial) contained herein is prohibited.

This Report does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The recommendations,

if any, made herein are expression of views and/or opinions and should not be deemed or construed to be neither advice/offer for the purpose of purchase or sale of any securities mentioned

herein. Past performance is not a guide for future performance, future returns are not guaranteed. Opinions expressed herein are subject to change without notice. Investor should rely on

information/data arising out of their own investigations. Investors are advised to seek independent professional advice and arrive at an informed trading/investment decision before executing

any trades or making any investments. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investor may realize losses

on any investments. This Report has been prepared on the basis of publicly available information, internally developed data and other sources believed by us to be reliable. A graph of daily

closing prices of securities is available at www.nseindia.com, www.bseindia.com. Research Analyst views on Subject Company may vary based on Fundamental and Technical Research. Sushil

Financial Services Private Limited or its directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability

of such information / opinions / views. None of the directors, employees, affiliates or representatives of company shall be liable for any direct, indirect, special, incidental, consequential,

punitive or exemplary damages/loss etc whatsoever from the information/opinions/views contained in this Report and investors are requested to use the information contained at their risk.

Sushil Financial Services Private Limited (SFSPL) and its connected companies, and their respective Directors, Officers and employees or their relative, may have a long or short position in the

subject companies mentioned in the report and it may not be construed as potential conflict of interest with respect to any recommendation and related information and opinions. Reports

based on technical and derivative analysis center on studying charts company’s price movement, outstanding positions and trading volume, as opposed to focusing on a company’s

fundamentals and, as such, may not match with a report on a company’s fundamental analysis. SFPSL has different business segments/Divisions with independent research and maintains arm’s

length distance catering to different set of customers having various objectives, risk profiles, investment horizon, etc. and therefore may at times have different contrary views on stocks sector

and markets. Research Report may differ between SFSPL’s RAs on account of differences in research methodology, personal judgment and difference in time horizons for which

recommendations are made. User should keep this risk in mind and not hold - SFSPL, its employees and associates responsible for any losses, damages of any type whatsoever.

This report is not intended to be a complete statement or summary of the securities, market or developments referred to in this document. SFSPL or its affiliates or employees are under no

obligation to update the information. SFSPL or its affiliates or employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent

error in the information contained in this report.

SFSPL or its affiliates and/or its employees/its associates or his relative does not have financial interest in the subject companies. SFSPL or its affiliates and/ or its employees/its associates or his

relative may or may not have beneficial ownership of one per cent or more securities of the subject company, at the end of the month immediately preceding the date of publication of the

research report. SFSPL/its Associates/ Research Analyst have not received any compensation from the subject company in the past twelve months. Further the subject company is/was not a

client during twelve months preceding the date of distribution of the research report and the types of services provided. SFSPL or its research analyst has not served as an officer, director or

employee of the subject company. SFSPL or its affiliates and/or its research analysts have not been engaged in market making activity for the subject company.

SFSPL or its associates or its Research Analyst have not received any compensation or other benefits from the subject companies or third party in connection with the research report. SFSPL/its

Associates/ Research Analyst/ his Relatives not have any other material conflict of interest at the time of publication of the research report.

SFSPL/its Associates/ Research Analyst/ his Relatives have not managed or co-managed public offering of securities, have not received compensation for investment banking or merchant

banking or brokerage services, have not received any compensation for product or services other than investment banking or merchant banking or brokerage services from the subject

companies in the last twelve months.

There are no material disciplinary action that been taken by any regulatory authority impacting equity research analysis activities.

17You can also read