CBRE Research - Tourism Investment

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CBRE Research

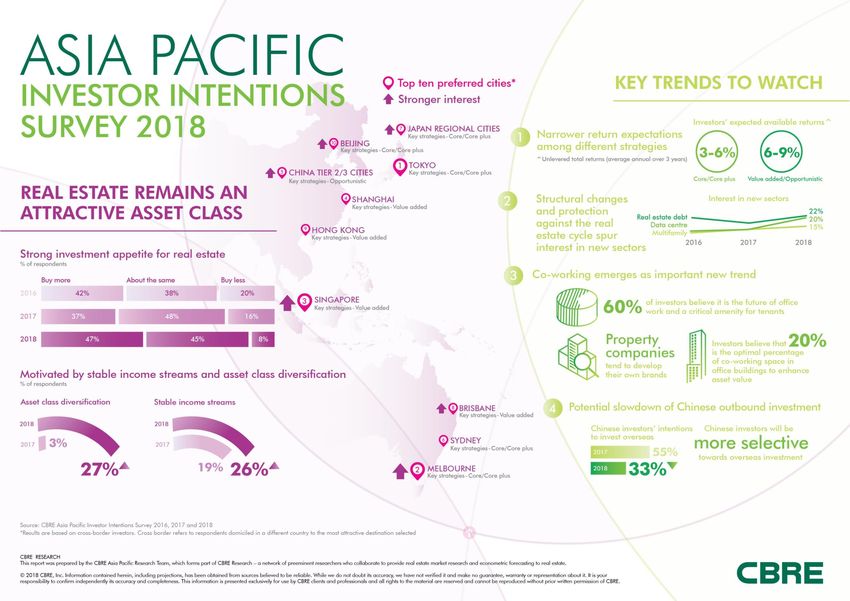

Asia Pacific Investor Intentions Survey 2018

Executive Summary

04

Real estate remains an attractive asset

class

05

Key trends to watch

12

Respondent’s profile and

22

survey methodology

© 2018 CBRE, INC. CBRE RESEARCH | 2

Asia Pacific Investor Intentions Survey 2018 © 2018 CBRE, INC. CBRE RESEARCH | 3

Asia Pacific Investor Intentions Survey 2018

EXECUTIVE SUMMARY

• Investor appetite for Asia Pacific real estate remains robust in 2018, driven by the twin objectives of securing stable income streams and asset class

diversification.

• While concerns about potential global and local economic shocks weakened for the second consecutive year, investors are more concerned

about higher property prices.

• The high price of core assets and search for higher returns continues to drive investors towards core-plus/good secondary and value-added assets.

This year marked the first time that value-added has overtaken prime core as the most preferred asset.

• Investor focus is broadening away from the traditional preferred markets of Shanghai, Sydney and Tokyo. Several cities are attracting attention, led

by Singapore, Melbourne, Brisbane and regional cities in China and Japan.

• The survey found narrower return expectations among different strategies, pointing to more competition for assets offering high single digit

unlevered returns.

• The industrial and logistics sector is seeing a substantial increase in investor interest, driven by structural changes including e-commerce growth and

the development of modern logistics facilities into an institutional investment product. Investor demand for multi-family owing to high housing prices

and declining home ownership affordability across the region.

• With occupiers increasingly demanding flexible leasing terms and space usage, many investors hold the view that co-working is the future of office

work environment and an amenity for tenants. Most investors believe that up to 20% is the ideal proportion of co-working space in a single office

building to enhance its value.

• Although Asian outbound investment continues to eclipse previous records and Chinese investors still comprise the largest source of capital,

Chinese outbound investment is expected to slow this year.

© 2018 CBRE, INC. CBRE RESEARCH | 4

REAL ESTATE REMAINS AN ATTRACTIVE ASSET CLASS

Asia Pacific Investor Intentions Survey 2018

STRONG INVESTOR APPETITE FOR REAL ESTATE

Investor appetite for Asia Pacific real estate Figure 1: Purchasing activity intentions over the past three years

remains robust. An overwhelming 92% of

respondents indicate that their investment

activity in 2018 will be the same or greater 100%

compared to 2017.

92%

Real estate fund managers display stronger 84%

intentions to purchase more this year, a finding 80%

supported by CBRE Research’s The Next Wave 80%

of Capital Deployment report published in

January 2018, which estimated that

approximately US$53 billion of real estate private

equity capital will be deployed into Asia Pacific

60%

% of respondents

real estate by 2020.

40%

20%

0%

2016 2017 2018

Buy more About the same Buy less

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2016, 2017 & 2018

© 2018 CBRE, INC. CBRE RESEARCH | 6Asia Pacific Investor Intentions Survey 2018

DRIVEN BY STABLE INCOME STREAMS AND RISK DIVERSIFICATION

Investor demand for real estate is being motivated Figure 2: Main motivation for investing in real estate compared to last year

by the objective of securing stable income streams

and asset class diversification.

In comparison with other asset classes including

equities, bonds, direct real estate and real estate

securities, direct real estate has provided more

stable returns over the past decade while also

being less volatile. This, together with the higher

volatility in equities and bonds witnessed since the

beginning of this year, is strengthening investor 27% 26% 26%

appetite for direct real estate investment.

19% 18%

As interest rates gradually move into the upward

cycle, there will be limited room for further yield

compression to drive value growth. For the second

consecutive year, less investors selected capital

value growth as the major motivation to invest in 3%

real estate.

Asset class diversification Stability of income stream Capital value growth

2017 2018

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2017 & 2018

© 2018 CBRE, INC. CBRE RESEARCH | 7Asia Pacific Investor Intentions Survey 2018

INVESTORS’ CONCERNS SHIFT TOWARDS PROPERTY PRICING

The improved global and regional economic Figure 3: Greatest threat to property markets 2017 - 2018

outlook is fostering a more optimistic attitude

among investors. Several export-orientated

economies in the region including China, Japan,

Hong Kong, South Korea and Singapore recorded Global and local economic shock

better-than-expected economic growth last year

thanks to the recovery of global trade.

Concern about potential global and local

Property is overpriced

economic shocks weakened for the second

consecutive year. In contrast, investors are more

concerned about property prices. Rising interest

rates are expected to place pressure on asset

prices, especially now that property yields have

Faster than expected rises in interest rates

already moved below pre-crisis levels and the gap

between property yields and long-term

government bond yields has narrowed further.

Global political instability

2018

Overbuilding leading to excess supply

2017

0% 10% 20% 30% 40% 50% 60%

% of respondents

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2017 & 2018

© 2018 CBRE, INC. CBRE RESEARCH | 8Asia Pacific Investor Intentions Survey 2018

STOCK IS AVAILABLE BUT PRICING IS HARD TO JUSTIFY

The limited availability of product and asset pricing Figure 4: Biggest obstacle to acquiring assets over the past three years

have traditionally been the major obstacles facing

real estate investors. This year, investors displayed

greater concern about high asset prices amid what Asset Pricing Asset Availability

is still an intensely competitive market for prime

commercial real estate in Asia Pacific.

The investor pool continues to broaden, and now

44%

consists of traditional players such as property

38%

companies, REITs and real estate funds, along with

institutional capital and high net worth investors

looking for asset diversification.

35%

Concern about the availability of stock weakened

this year, with more investors indicating that they

are willing to sell. However, investors still find it hard

to justify current pricing.

24%

CBRE Research foresees that slower rental growth

expected in 2018, together with the expectation of

higher interest rates, could prompt investors to

adopt a less aggressive stance towards 18%

underwriting. 16%

2016 2017 2018

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2016, 2017 & 2018

1 Institutional capital includes insurance companies, pension funds and sovereign wealth funds

© 2018 CBRE, INC. CBRE RESEARCH | 9Asia Pacific Investor Intentions Survey 2018 INVESTORS FOCUS ON CORE-PLUS AND VALUE-ADDED The high price of core assets and search for higher returns continues to drive investors towards core-plus/good secondary, which entails investing in prime assets in non-core areas or non-prime assets in core areas, and value-added assets. This year’s survey marked the first time that value-added has overtaken core as the most preferred asset. Investors are exploring different ways to create value through asset enhancement, such as incorporating retail elements or rent-paying amenities into office buildings. Other strategies include upgrading through interior and exterior renovation and conversion to alternative use. Figure 5: Preferred investment strategy 2016 - 2018 Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2016, 2017 & 2018 © 2018 CBRE, INC. CBRE RESEARCH | 10

Asia Pacific Investor Intentions Survey 2018

STRONGER INTEREST IN SINGAPORE, MELBOURNE AND REGIONAL

CITIES IN JAPAN AND CHINA

Figure 6: Top ten preferred cities for

investment (cross-border* only) Japan remains the top destination for investment, with Tokyo

ranking as the most preferred city. Investors are also displaying

strong interest in regional cities such as Osaka and Fukuoka.

Both cities offer solid fundamentals as well as higher entry

yields.

Melbourne eclipsed Sydney as the most attractive city in

Australia, a result due to its stronger rental growth supported

by tight vacancy. Brisbane received stronger interest from

cross-border investors considering counter cyclical plays, with

office rents recently bottoming-out after a five-year correction

and expected to recover over the next two years.

The office market recovery helped propel Singapore to

among the top three destinations for cross-border investors for

the first time since the survey began in 2014. As Grade A assets

are scarce and aggressively priced, investors are focusing on

office properties with upgrading potential as Grade A rents will

continue to grow.

Shanghai continues to be the most desired market in China,

with transaction volume rising to an historical high in 2017. Tier II

cities with strong fundamentals such as Hangzhou, Nanjing

and Chengdu are also gaining more traction from investors.

Note: *Cross border refers to respondents domiciled in the different country as the

most attractive destination selected

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2018

© 2018 CBRE, INC. CBRE RESEARCH | 11KEY TRENDS TO WATCH

Asia Pacific Investor Intentions Survey 2018

#1: NARROWER RETURN EXPECTATIONS AMONG DIFFERENT

STRATEGIES

This year’s survey asked investors to estimate total Figure 10: Investors’ views of total unlevered total returns available in Asia Pacific

unlevered returns available in the Asia Pacific real

estate market. The results indicated narrower 3-6% 6-9% 9-12%

1-3% 12%+

return expectations among different strategies.

Core / core-plus investors estimate most available Core/Core-plus

returns at 3-6%, while value-added investors

expect 6-9%. Opportunistic investors anticipate 6-

12%. The low yield environment and overlapping

investment strategies mean that these

expectations are below those that were held

previously. Value-added

CBRE Research advises investors to consider that

there will be more competition for assets offering

a return profile of around 6-9%. High-risk profile

investors are seeking value-added assets as a low

risk opportunistic strategy to achieve target Opportunistic

returns.

Legend

Less available Most available

Note: ^Unlevered total returns (average annual over 3 years)

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2018

© 2018 CBRE, INC. CBRE RESEARCH | 13Asia Pacific Investor Intentions Survey 2018

#2: A THEMATIC SECTOR FOCUS

The industrial and logistics sector is seeing an Figure 11: Preferred sectors for investment 2016 - 2018

increase in investor interest, largely at the

expense of retail. This is being driven by structural

changes including e-commerce growth and the

40%

development of modern logistics facilities into an

institutional investment product.

E-commerce High housing prices

growth driving creating demand

interest in logistics for rental

Investor appetite for multi-family is rising as high

housing prices create strong and stable demand assets apartments

for rental accommodation. Japan has long 30%

been the sole destination for multi-family

investment in Asia Pacific, but China is beginning

% of respondents

to offer considerable opportunities, supported by

government initiatives to develop the rental

housing market. Australia is also a potential

destination for the multi-family sector, with 20%

fundamentals appearing attractive for both

domestic and international investors.

10%

0%

Office Industrial & Logistics Retail Multifamily Hotels

2016 2017 2018

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2016, 2017 & 2018

© 2018 CBRE, INC. CBRE RESEARCH | 14Asia Pacific Investor Intentions Survey 2018

HIGH HOUSING PRICES DRIVE DEMAND FOR MULTI-FAMILY

The jump in popularity of multi-family is Figure 12: Millennials’ attitudes toward renting property

being driven by declining homeownership

affordability. Surging property prices are

63%

outstripping wage growth and making it

difficult for Asia Pacific millennials to

accumulate the necessary capital to buy

their own home. 63% of respondents to

CBRE Research’s Asia Pacific Millennials

Survey published in 2016 said that they were agreed that this

forced to rent homes due to being unable generation is forced to

to buy them. rent as buying a

property is out of reach

Median housing prices in tier I cities in Asia for most

Pacific are more than 10 times greater than

average household incomes. The higher the

price multiple to income, the more likely it is

for millennials to either live at home with

their parents or rent accommodation. Figure 13: Median housing price to annual household income ratio

Some investors are already exploring rental

apartment opportunities in Beijing, Shanghai

and Hong Kong, as these markets have a

high housing price to income ratio

compared to other tier-1 cities in the region.

Target end-users are typically young

professionals who have been working for

two to three years.

Source: Demographia, Q3 2015, MSCI, December 2015, Asia Pacific Millennials Survey, CBRE Research, October 2016

© 2018 CBRE, INC. CBRE RESEARCH | 15Asia Pacific Investor Intentions Survey 2018

INTEREST IN NICHE SECTORS IS RISING

Investor demand for niche sectors is growing Figure 14: Top five alternative sectors among investors

further due to rapid structural changes,

relatively higher initial yields and comparative Major country focus

immunity to real estate cycles.

Demographic changes are piquing investors’ Retirement

Living

interest in retirement living, healthcare and

student accommodation. Ageing populations

in Japan and China will create more demand

for retirement living and trigger demand for Healthcare

healthcare. Singapore is another potential

market for healthcare due to its status as a

medical tourism hub in Southeast Asia.

Opportunities to invest in student

accommodation lie mainly in Australia. Data Centre

Interest in data centres increased significantly

in this year’s survey, amid rapid growth in data Real Estate

usage. Opportunities to acquire data centres Debt

mainly exist in markets with large populations

such as China, India and Japan, while

Singapore holds considerable appeal as a

regional focal point for Southeast Asia. Student Living

Real estate debt is generating stronger interest 0% 5% 10% 15% 20% 25%

among investors after weakening in last year’s

survey. The coming years will see significant

2018 2017 2016

debt refinancing pressure, particularly in

China, where US$75 billion of corporate bonds

will need to be refinanced by listed Chinese

real estate companies between 2018-2020. Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2016, 2017 & 2018

© 2018 CBRE, INC. CBRE RESEARCH | 16Asia Pacific Investor Intentions Survey 2018

#3: CO-WORKING EMERGES AS IMPORTANT NEW TREND

Figure 16: Occupier trends that investors believe have the most Figure 17: Locations where occupiers intend to increase their

impact on real estate value space over the next two years

Flexible space 42% Office in major business

districts

Diversification from traditional Office in decentralised

office/retail properties locations

Smart buildings Co-working centre 33%

Co-living CBD office

Experiential retail Campus

Last-mile logistic Serviced office

Automation Business park

0% 10% 20% 30% 40% 50% 0% 10% 20% 30% 40% 50%

With capital value growth increasingly being driven by income growth, it is essential that investors gain a thorough understanding of occupier

requirements. When asked to identify the occupier trends exerting the greatest impact on real estate value, investors selected space that can be

procured quickly, with little capital investment and at very flexible terms.

This finding aligns with occupiers’ naming co-working centres as their third most preferred location for expansion over the next two years. Occupiers

are no longer bound to CBD offices when considering new space, with their growing preference for flexible space increasingly being reflected by

actual office take up in major Asia Pacific office markets.

Source: Asia Pacific Occupier Survey, CBRE Research, March 2018, Asia Pacific Investor Intentions Survey 2018, CBRE Research, March 2018

© 2018 CBRE, INC. CBRE RESEARCH | 17Asia Pacific Investor Intentions Survey 2018

INVESTORS BELIEVE FLEXIBLE SPACE IS THE FUTURE

With occupiers increasingly demanding Figure 18: Why does co-working appeal to investors?

flexible leasing terms and space usage,

many investors hold the view that flexible

space is the future of office work

environment. Future of office work 32%

Some owners are offering co-working as an

amenity for existing tenants in the same

building, providing occupiers with the

flexibility to take space both on a traditional

lease and also on a co-working basis.

In general, investors looking to gain their

An amenity for

tenants 28%

exposure to the co-working trend intend to

partner with third-party co-working operators

as they are still evaluating and testing the

sustainability of the flexible space concept.

Property companies are opting to develop

20%

and operate their own co-working brands as Enhance long term

an amenity and component of their overall

tenant mix. Examples include Swire

building income

Properties’ Blueprint in Taikoo Place in Hong

Kong and SOHO China’s SOHO 3Q in its

office portfolio in Beijing and Shanghai.

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2018

© 2018 CBRE, INC. CBRE RESEARCH | 18Asia Pacific Investor Intentions Survey 2018

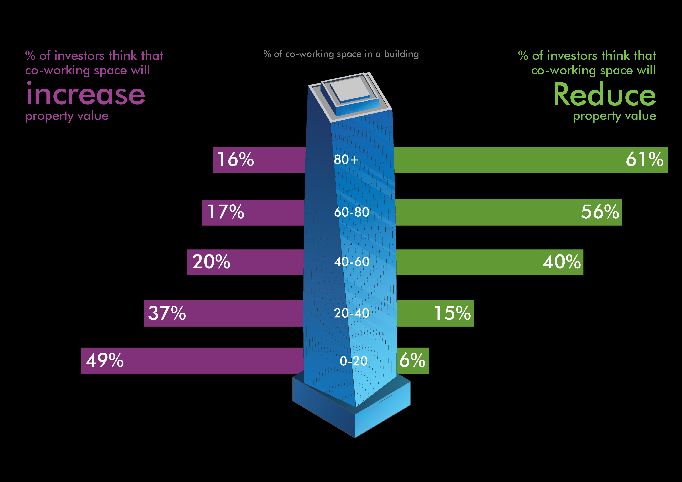

UP TO 20% IS THE OPTIMAL PERCENTAGE OF CO-WORKING SPACE IN

AN OFFICE BUILDING TO ENHANCE ITS VALUE

Most investors believe that up to 20% is the Figure 19: What proportion of co-working space impacts building value?

ideal proportion of co-working space in a

single office building to enhance its value. If

more than 40% of space in a single building is

allocated to co-working, investors believe its

value will be negatively affected.

Although some lower grade office buildings

have recorded value appreciation after

being repositioned to co-working, overall

investors are unwilling to allocate too much

space to this amenity. Only 39% of co-working

operators are profitable globally.

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2018

© 2018 CBRE, INC. CBRE RESEARCH | 19Asia Pacific Investor Intentions Survey 2018

#4: POTENTIAL SLOWDOWN OF CHINESE OUTBOUND INVESTMENT

Although Asian outbound investment continues Figure 20: Chinese outbound investment intentions 2017 vs 2018

to eclipse previous records and Chinese

investors still comprise the largest source of

capital, CBRE Research expects to see a

continuation of the slowdown in Chinese

outbound investment first witnessed in H2 2017 More than the amount in 2017

following the introduction of new capital

controls.

This year’s survey indicates that Chinese

The same amount as in 2017

investors are less keen to invest overseas in 2018.

While overall interest remains reasonably firm,

fewer investors intend to invest more than they

did in 2017. Government scrutiny of overseas

real estate acquisitions will continue this year,

with another set of capital controls coming into Less than the amount in 2017

effect in March 2018. Real estate investment will

subject to an additional layer of examination.

CBRE Research expects to see a stronger focus No intentions to invest oversesas

on Belt & Road countries and industry-related

asset classes such as warehouses, industrial

parks and ports, supported by more flexible

regulatory treatment. Redeploying offshore 0% 10% 20% 30% 40% 50% 60% 70%

capital is expected to drive some investment

transactions, but any purchases will be 2018 2017

considered carefully as they will also be subject

to closer regulatory scrutiny.

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2018

© 2018 CBRE, INC. CBRE RESEARCH | 20Asia Pacific Investor Intentions Survey 2018

CONCLUSION

Although asset pricing poses a major obstacle,

“Despite high valuations, investors remain keen to purchase real estate

for risk diversification. Investors’ focus is on

property remains an income growth as capital value appreciation

will increasingly be driven by income growth.

attractive asset class given The high price of core assets and search for

its stability and risk higher returns will continue to drive investors

towards core-plus/good secondary and value-

diversification. Investors in added assets. Investors are set to shift their

focus away from the traditionally preferred

the Asia Pacific real estate markets of Shanghai, Sydney and Tokyo to other

locations including Singapore, Melbourne,

market will display strong Brisbane and regional cities in China and

Japan.

demand in 2018” Other key trends this year will include investors

reducing their return expectations; a more

thematic sector focus; stronger interest in co-

working; and the continued slowdown in

Chinese outbound investment.

© 2018 CBRE, INC. CBRE RESEARCH | 21SURVEY PROFILE

Asia Pacific Investor Intentions Survey 2018

RESPONDENT’S PROFILE & SURVEY METHODOLOGY

The fifth annual CBRE Investor Intentions Survey Figure 21: Profile of respondents

focuses on the forward looking views of real

estate investors in Asia Pacific and was carried

out online between 15 November 2017 and 31

January 2018.

A total of 366 responses were received. 82% of

respondents were companies domiciled in Asia

Pacific and the other 18% were domiciled

primarily in Western Europe, the Middle East and

North America.

For the purpose of analysis, CBRE Research

categorised some investors into groups. These

included:

Funds or asset managers (35% of respondents)

and private equity firms (4%) which collectively

accounted for 39% of respondents.

Listed property companies & listed REITs (15%),

Developers (13%), and private property

companies & unlisted REITs (11%), which

collectively accounted for 39% of respondents.

Sovereign wealth funds, insurance companies,

pension funds and family offices, which

collectively accounted for 13% of respondents.

CBRE Research used the broad categorisation Note:

Real estate funds include funds or asset managers and private equity firms

“investor” to denote this group.

Investor includes insurance company, pension fund, sovereign wealth fund and private individual investors / family office.

Other include property consulting firms, legal firms, aged care, civil Construction, hotel operators, logistics and retailer.

Source: Asia Pacific Investor Intentions Survey, CBRE Research, March 2018.

© 2018 CBRE, INC. CBRE RESEARCH | 23Asia Pacific Investor Intentions Survey 2018

CAPITAL MARKETS CONTACTS

ASIA PACIFIC

Rob Blain

Executive Chairman

rob.blain@cbre.com

ASIA

KOREA

Tom Moffat Don Lim SOUTHEAST ASIA CAPITAL ADVISORS

Executive Director Senior Director

tom.moffat@cbre.com.hk don.lim@cbrekorea.com SINGAPORE JAPAN

Jeremy Lake Junichiro Muto

Executive Director Senior Director

NORTH ASIA jeremy.lake@cbre.com.sg junichiro.muto@cbre.com.jp

GREATER CHINA TAIWAN

Alan Li Andrew Lin THAILAND

Managing Director Senior Director Kulwadee Sawangsri GLOBAL CAPITAL MARKETS

alan.li@cbre.com.cn andrew.lin@cbre.com Executive Director

kulwadee.sawangrsi@cbre.co.th

Yvonne Siew

HONG KONG SOUTH ASIA Executive Director

Stanley Wong INDIA VIETNAM yvonne.siew@cbre.com

Executive Director Gaurav Kumar Phuong Hang Dang

stanley.wong@cbre.com.hk Managing Director Managing Director

gaurav.kumar@cbre.co.in hang.dangphuong@cbre.com

INDUSTRIAL & LOGISTICS

JAPAN

Roderick Gerstman Nikhil Bhatia Xuan Quynh Nguyen Dennis Yeo

Associate Director Managing Director Investment Manager Managing Director

roderick.gerstman@cbre.co.jp nikhil.bhatia@cbre.co.in quynh.nguyen@cbre.com dennis.yeo@cbre.com

PACIFIC

DEBT & STRUCTURED FINANCE

AUSTRALIA NEW ZEALAND

Bruce Baker Mark Coster Andrew Stringer Steven Lim

Senior Managing Director Senior Managing Director National Director Senior Director

bruce.baker@cbre.com.au mark.coster@cbre.com.au andrew.stringer@cbre.co.nz steven.lim@cbre.com.au

© 2018 CBRE, INC. CBRE RESEARCH | 24Asia Pacific Investor Intentions Survey 2018

For more information about this report, please contact:

RESEARCH

Henry Chin, Ph.D. Leo Chung, CFA Karie Kwan

Head of Research, Asia Pacific Capital Markets Specialist, Asia Pacific Associate Director, Asia Pacific

henry.chin@cbre.com.hk leo.chung@cbre.com.hk karie.kwan@cbre.com.hk

For more information regarding global research, please contact:

Nick Axford, Ph.D. Richard Barkham, Ph.D., MRICS

Global Head of Research Global Chief Economist

nick.axford@cbre.com richard.barkham@cbre.com

Henry Chin, Ph.D. Jos Tromp Spencer Levy

Head of Research, Asia Pacific Head of Research, EMEA Head of Research, Americas

henry.chin@cbre.com.hk jos.tromp@cbre.com spencer.levy@cbre.com

Follow CBRE

CBRE RESEARCH

This report was prepared by the CBRE Asia Pacific Research Team, which forms part of CBRE Research—a network of preeminent researchers who collaborate to provide real estate market research and econometric forecasting to real estate.

All materials presented in this report, unless specifically indicated otherwise, is under copyright and proprietary to CBRE. Information contained herein, including projections, has been obtained from materials and sources believed to be reliable at the date of publication.

While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. Readers are responsible for independently assessing the relevance, accuracy, completeness and currency of the information of this publication.

This report is presented for information purposes only exclusively for CBRE clients and professionals, and is not to be used or considered as an offer or the solicitation of an offer to sell or buy or subscribe for securities or other financial instruments. All rights to the material are

reserved and none of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party without prior express written permission of CBRE. Any unauthorized publication or redistribution of CBRE research

reports is prohibited. CBRE will not be liable for any loss, damage, cost or expense incurred or arising by reason of any person using or relying on information in this publication.

To learn more about CBRE Research, or to access additional research reports, please visit the Global Research Gateway at reports www.cbre.com/research-and-reports

©2018

© 2018 CBRE,

CBRE, Inc. INC. CBRE RESEARCH | 25Asia Pacific Investor Intentions Survey 2018 © 2018 CBRE, INC. CBRE RESEARCH | 26

You can also read