COVID-19's Rapidly Changing Impact on Asia Pacific Electricity Markets - A Webinar for IAEE Mike Thomas, 5 June 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A Webinar for IAEE COVID-19’s Rapidly Changing Impact on Asia Pacific Electricity Markets Mike Thomas, 5 June 2020 mthomas@lantaugroup.com

Disclaimer and Credits This presentation has been prepared to facilitate general

discussion and not for support of any commercial or

business decision.

Special thanks to the entire team at The Lantau Group,

particularly: Stefan Robertsson, Xiaoran Liu, Miaosu Li,

and Liyuan Zhao. Additional support was provided by

Bobby Ditric, Paul Buckland, Chris Starling, Zander

Bischof, David Fishman, Soyeon Park, Jan Stempien, JP

Stovall, Ian Yao, Schuyler Kapnick, Sovathana Kem,

Anna Leung, and Oscar Ng.

Hong Kong | Singapore | Seoul | Perth

(and Shanghai via Nicobar Group)

1

Agenda

1. Executive Summary

2. Overview of Singapore Electricity Market

About The Lantau Group

3. Key Market Drivers

4. Modelling Results

Headline Impacts

5. Appendix

Other Points

SummaryDecades of experience in commercial and regulatory matters across the globe

Our focus and orientation

Washington DC

London

Languages:

Paris

Arabic*

Bahasa Indonesia

Bahasa Malaysia

Markets & Industry Economic Client Bengali

Impact

Transactions Insights Regulation Service Cantonese

English

We focus on We focus on We advise on We apply Our senior French

what can be what matters key projects economics and team members German

measured and to energy throughout the analysis to are actively Hindi

substantiated. stakeholders

facing changes

Asia Pacific

region and the

address

challenges

involved in the

execution of

ASIA Japanese

Khmer

We provide

objective,

in markets, rest of the facing mandates and PACIFIC Korean

technologies, world. regulators, assignments. Malayalam

independent,

regulations, commercial Mandarin

well-grounded and policies. We influence stakeholders, We own our Russian

advice for the evolution and policy company, so Serbian

decision- This is what of the energy makers. when we say Spanish

makers facing we do. sector through we are Swedish

high stakes our work and dedicated to

Tagalog

choices. expertise. our clients we Tamil

mean it. Key: Telugu&

Office Thai*

Affiliate/Senior Advisor Vietnamese*

Network Partners

*Senior Advisors

Economic, commercial, and strategy advisory for energy sector stakeholders throughout the region

3

3We draw from a diverse range of experience and expertise

Vietnam Thailand Uzbekistan Mainland China

Extensive due diligence support for new RE and Demand response pricing CNG vehicle market Curtailment study in Gansu, Jilin and West Inner Mongolia

traditional power supply resources across the evaluation

Grid solar evaluation Multiple studies on small-hydro power investment opportunity

country

Gas to power economics Coal-fired power generation and carbon policy in Zhejiang

LNG market entry studies

Market development Singapore Coal-fired power investment opportunity in Chongqing

Market modelling / development

Renewable energy Assessment of gas-fired CHP opportunities in Guangdong

Market design and regulatory

support Strategic assessment of opportunities in multiple provinces

Malaysia

Demand forecasting Green procurement options / end user market support

MESI 2.0 reforms

Commercial transactions

PPA (Green and Other)

Tariff benchmarking

Electricity/gas markets Korea

Corporate PPA support

Tariff benchmarking

LNG and gas strategy Renewable energy study for solar and wind

Third party access

Due diligence on CCGT and renewable power plants

Disputes / expert witness

Demand forecasting

Capacity/ancillary market design and evaluation

Capacity market

Commercial transactions

SMP/REC modelling and implications to IPP business

Disputes / expert witness

Gas and coal IPP opportunities

Taiwan LNG/Coal competitive procurement

Philippines

Offshore wind

Market design and development

Transaction support

Due diligence support Oman India

Corporate energy pricing

Business strategy Performance regulation Wholesale market

Market development modelling

Natural Gas Masterplan and LNG entry strategy Direct sales and corporate PPAs

Fuel switching

Distribution sector structure and regulation Market readiness and scarcity pricing

Power price forecasting

Australia Retail competition

End user pricing/invoice

tracking

Capacity market design

Indonesia Contract disputes / expert witness

Gas to power (small and large scale)

Market design and policy / reviews New Zealand

Evaluation of market entry opportunities Corporate green procurement Market development / regulation / pricing

Demand response Retail sector development

Market development

Market modelling / transaction support Gas pipeline access policy

Japan Market design and regulation Market trading and market making

Customer Solar Entry Strategy Network regulation and cost recovery Disputes / expert witness

End user pricing of gas and electricity StorageFounders, Partners, Directors

Mike Thomas Dave Carlson Stefan Robertsson

Managing Director Director Partner

mthomas@lantaugroup.com dcarlson@lantaugroup.com srobertsson@lantaugroup.com

Mike is an expert in energy markets and regulation with experience Dave is an experienced energy market operator, designer and change Stefan has over 20 years of experience in business development, M&A,

throughout the Asia Pacific region. He works with stakeholders on manager with a track record spanning Asia, Africa, Australia and New and corporate and project finance across the Asia Pacific region. Prior

matters involving regulation and market design; market evaluation; Zealand. Most recently he was a Senior Business Development to joining TLG, he spent nearly 10 years with CLP Group, where he

strategy; and commercial and regulatory disputes. He has advised Director at SGX, responsible for new initiatives in the gas and power served as head of Corporate Finance and Development for non-Hong

buyers and sellers on over 50 GW of commercial transactions and sectors. Prior to that he served for 10 years as the COO and CEO of Kong activities. He led the CLP Group Investment Committee and

associated market and business strategies. And, he has advised the Energy Market Company, EMC, the national electricity market Chaired the TruEnergy Risk Committee for CLP's Australian trading and

governments, regulators, and other stakeholders on numerous major operator for Singapore. Dave has served on and chaired many business activities. He also had significant involvement in CLP's

market and regulatory reviews and disputes. Prior to co-founding TLG, industry and governance panels to further liberalise energy markets investment activities in Mainland China, India, and South East Asia,

he was the Asia Pacific energy and environment practice leader for a including market rules covering such topics as market rules evolution, covering the full spectrum of energy assets and opportunities. Prior to

global consultancy. Mike has an MPP from Harvard Kennedy School the implementation of retail contestability, developing gas trading and CLP Stefan was with various ABB Financial Services companies in the

and a BA in economics from Carleton College. introducing electricity derivative products. US, UK, and Asia. He earned his degree in Financial Economics at the

Stockholm School of Economics.

Middle Central East

James Ooi David Kim

East Asia Asia

Partner Partner

jooi@lantaugroup.com dkim@lantaugroup.com

South SE

James Ooi has over 20 years of experience in the energy industry. He

Pacific David is a partner and director of TLG, based in Seoul, where he works

Asia Asia

is an expert in areas related to energy market design, asset valuation, with both inbound and outbound clients interested in investments in the

commercial contracting for gas and power (LNG SPA, GSA and PPAs), energy sector. He particularly focusses on new energy opportunities

corporate strategy, planning and operations, with experience across throughout the region, helping to connect Korean and global companies

Asia Pacific, the Middle East and North Africa. Prior to joining TLG, into new markets and to help other companies evaluate opportunities in

James headed the Gas & Power practice for a global consulting firm in Korea. Prior to joining TLG, Dr Kim was the Managing Director at

Asia. In addition to consulting, James brings deep operational Hanwha Energy’s Energy Solution System Division. Previously, David

experience and has held management leadership positions at major was a Partner at A.T. Kearney and a Principal at the Boston Consulting

generators and power utilities in the region. James is based in Group for over ten years. David holds a PhD in Mechanical Engineering

Singapore. James holds an MSc and BEng in Electrical Engineering from Massachusetts Institute of Technology. David is fluent in Korean

from the UK and is fluent in English, Mandarin, Cantonese and Bahasa and English.

(Malaysia and Indonesia).

5Agenda

1. Executive Summary

2. Overview of Singapore Electricity Market

About The Lantau Group

3. Key Market Drivers

4. Modelling Results

Headline Impacts

5. Appendix

Other Points

Summary

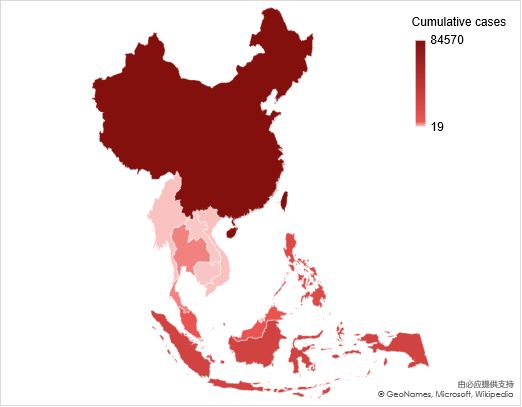

6Confirmed Cases in the Asia Pacific Region (as of May 31)

Cumulative Confirmed Cases

Mainland

ASEAN (as of May 31) China,

China

countries, 84570

Taiwan

80000

35000 Singapore

34366

5000

70000

30000

Indonesia

26473

60000

China

25000 84570

50000

Philippines

20000 18096 Taiwan

442

40000 Myanmar

224 Lao

19

15000

30000 Thailand Vietnam

Malaysia 3081 328

Philippine, 18096

Cambodia

10000 7762 125

Taiwan, 442

20000

Vietnam, 328 Thailand

Myanmar, 224 3081

5000 Brunei, 141 Brunei

10000 Malaysia

Cambodia, 125 7762 141

Lao, 19

Singapore

34366 Indonesia

0 0 26473

Ma y 04

Ma y 09

Ma y 14

Ma y 19

Ma y 24

Ma y 29

Apr 04

Apr 09

Apr 14

Apr 19

Apr 24

Apr 29

Feb 4

Feb 9

Feb 14

Feb 19

Feb 24

Feb 29

Ma r 05

Ma r 10

Ma r 15

Ma r 20

Ma r 25

Ma r 30

Jan 25

Jan 30

7

Source: WHO; Taiwan CDCAsia Pacific countries continue to be well below global mean for mortality

• COVID-19 mortality in Asia Pacific, thankfully, has been extremely low given population size and

density

Country/Region Deaths Cases Deaths per 1M % Death

population per Case

Philippines 960 18,638 9 5.15%

Japan 891 16,851 7 5.29%

Indonesia 1,641 26,940 6 6.09%

Korea 271 11,503 5 2.36%

Singapore 23 35,292 4 0.07%

New Zealand 22 1,504 4 1.46%

Australia 103 7,204 4 1.43%

Malaysia 115 7,857 4 1.46%

Mainland China 4,634 83,017 3 5.58%

Hong Kong 4 1,088 0.5 0.37%

Taiwan 7 443 0.3 1.58%

Vietnam 0 328 0 0.00%

• World deaths per 1M = 48

Data circa 1 June 2020 (https://www.worldometers.info/coronavirus/)

8Demographic differences

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Hong Kong Australia/New USA South Korea Thailand China Singapore Viet Nam Ma laysia Philippines

SAR Zealand

Under 50 Between Over 70

Older Younger

9

Source: United Nations, Department of Economic and Social Affairs, Population Division (2019). World Population Prospects 2019, Online Edition. Rev. 1.About The Lantau Group

Headline Impacts Impact on Demand

Other Points

Summary

10Hubei’s power consumption chronicles the evolution of the COVID-19 situation,

incorporating both lockdown effects and the beginning of a recovery profile

Hubei Province, China

Daily Power Consumption on Hubei Provincial Grid System

800 Jan 23

Hubei/Wuhan

Mar 16-25

movement control order Feb 18

700 Ratio of workers resume

in effective Peak existing confirmed Apr 8

work in large institutions

cases in Hubei (50,633) Exit Wuhan control

in Hubei raises from

eased

600 22-68%

Jan 20

500 Chinese

government

confirmed

GWh

400 human-to-

human

transmission

300 of coronavirus

Feb 12

Mar 25

Peak daily new deaths

200 Exit Hubei (except

in Hubei (242)

Wuhan) control eased

2020 Lunar

100 New Year

2019

Lunar

Holiday

New Year 2020 2019

Holiday

0

1-Jan 8-Jan 15-Jan 22-Jan 29-Jan 5-Feb 12-Feb 19-Feb 26-Feb 4-Ma r 11-Mar 18-Mar 25-Mar 1-Apr 8-Apr 15-Apr 22-Apr 29-Apr 6-Ma y 13-May

Weekly change in daily demand in 2020 (vs. 2019)

0%

-7% -8% -6% -5% -1% -2%

-24% -17% -16%

-36% -27%

-41% -46% -45% -39%

5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Week No.

11

Source: Hubei Statistics, Hubei DRC, DXY.cn; TLG Analysis

* Note: % difference data only available after the week commencing 27 Jan 2020.Policies aimed to contain COVID-19 in Asian Pacific countries (1 of 2)

More Region Steps Taken

Strict

• Home quarantine – exit/entry of neighborhoods regulated and closely monitored; businesses and public services, except for those serving basic living

needs, shut down; all gatherings prohibited. Violation could result in fine and/or imprisonment.

Mainland • City lockdowns – Wuhan city shut down on Jan. 23rd; other cities in Hubei Province and all over the country followed soon; inter/intra-provincial

China transportation strictly controlled.

• Border restrictions – border closed to common foreign passport holders on March 28th

• Current Status – all restrictions, except for border restriction, greatly eased/removed as of first week of May.

• Quarantine Orders – legal order issued to travelers and citizens suspected of carrying COVID-19 infection in March;

• Partial lockdown (“circuit breaker”) across the country – 85% of workplaces shutdown, with only most essential services remaining open.

Singapore

• Border restrictions – border closed to foreign visitors on March 15th

• Current status– partial lockdown recently eased (1 June); border control still in effect

New Zealand:

• Lockdown – nationwide lockdown in effect on March 26th ; businesses & schools closed, public gathering prohibited

• Home quarantine – people are required to stay at home except for absolutely necessary reasons

• Border restriction – border closed to foreigners on March 19th

New Zealand • Phased relaxation starting on May 14th

& Australia

Australia:

• Lockdown in place for two months, policies vary in different states, in most states social gathering with more than 2/10 people is not allowed; people

are required to stay at home and minimize outings, very recent easing

• Border closed to all foreigners on March 19th; policy eased on April 7th; Australian nationals not allowed to travel abroad with few exemptions

Malaysia:

• Movement control order (MCO) in place on March 18th -- closure of all government and private premises except those for essential services; prohibition

of mass gatherings; Border closed to foreigners; MCO eased on May 4th

Philippines:

Philippines,

• Partial lockdown – strict lockdown in Luzon, lockdown in certain regions/municipalities in Visayas; border closed to all foreigners; border restriction still

Malaysia

in place

& Thailand

• Metro Manila lockdown ended on Monday, June 01

Thailand:

…

• Lockdown – Partial lockdown in Bangkok since Mar. 21st; nationwide lockdown since Apr. 20th; State of emergency on Mar. 9th, curfew in place

• Border closed on April 4th

[continued…]

12Policies aimed to contain COVID-19 in Asian Pacific countries (2 of 2)

Region Steps Taken

Korea:

• No lockdown/quarantine ordered – restriction on personal activities is advised but not enforced; the Enhanced Social Distancing

…

campaign from 22 March to 19 April advising limited operation of high-risk facilities, businesses and sectors; relaxed form of social

distancing from 20 April to 5 May; transition to ‘Distancing in Daily Life’ form 6 May

Korea & • Border restrictions – entry ban to travellers from selective countries/areas with severe outbreaks, i.e. Japan, Hubei Province, China, etc.;

Taiwan all incoming Koreans and foreign nationals are subject to 14-day quarantine

Taiwan:

• Early and aggressive track, trace

• No lockdown – some businesses suspended, public gatherings restricted

• Border restriction – border closed to foreigners on March 19th

Vietnam:

• Movement control from April 1st – 22nd ; more than 30,000 business shut down

• Border restrictions – flights from China suspended on Feb. 1st, international flights on Mar. 25th , visas stopped

Less Oher

• Status quo – movement control lifted, businesses reopening

Strict ASEAN

Cambodia:

Countries

• No lockdown – state of emergency declared; New Year (Sangkran, Festival in Mid April, 2020) cancelled; some public/private zones are

closed (gyms, nightlife areas, etc)

• Border restrictions – suspending foreign visas; entry ban on selective countries with severe outbreaks, i.e. U.S., EU, Thailand, Vietnam

13Peninsular Malaysia (example): COVID-19 Impact

Number of active cases, deaths, and recoveries No. of COVID tests: 519,944 (15,391 tests per 1M population)

9,000

Pre-MCO MCO 1 MCO 2 MCO 3 MCO 4 CMCO 5 Movement Control Order (MCO) Phases

8,000

6,941 7,629

7,000 6,535 March 18 April 15 May 12*

5,851

6,000 5,305

5,000 4,119

1 2 3 4 5

4,000

2,470 April 1 April 29

3,000

2,000 1. Prohibition of mass gatherings including religious, sports,

900 social and cultural activities. All houses of worship and

1,000 25 117

22 business premises would be closed, except for supermarkets,

0

public markets, grocery stores and convenience stores.

23 y

ay

22 b

29 b

eb

14 r

21 r

28 r

ar

y

16 y

11 r

18 r

25 r

pr

2. Closure of all government and private premises except those

a

a

Ap

p

p

Ma

a

e

e

Ma

Ma

-A

-A

-A

-M

-M

-M

-M

-M

-F

-F

-F

4-

7-

2-

9-

15

involved in essential services (water, electricity, energy,

Active Case Death Recovery telecommunications, postal, transportation, irrigation, oil, gas,

fuel, lubricants, broadcasting, finance, banking, health,

Total number of cases per 1M population pharmacy, fire, prison, port, airport, safety, defence, cleaning,

Selangor: 274 retail and food supply)

3. Closure of all kindergartens, government and private schools,

Kuala Lumpur: 1,042 public and private higher education institutions, and skills

training institutes nationwide

Putrajaya: 983

4. Sanctions covering all Malaysians travelling abroad. Those

Negeri Sembilan: 682 who have returned from overseas would be required to

undergo a health check and a 14-day quarantine.

5. Restrictions on the entry of all tourists and foreign visitors into

the country

Note: *Phase 5, a conditional movement control order (CMCO), is a relaxation

Melaka: 225 40 500 1000

of MCO regulations, which allows operations of major economic sectors..

14

Source: Worldometer (29 May), Department of Statistics Malaysia, Ministry of International Trade and IndustryLockdown measures were clearly the immediate cause of reduced demand

17 March 2020 Philippines 18 March 2020 Malaysia

Enhanced Community Quarantine Movement Control Order

250 500

▼12.2 % ▼ 16.0 %

200 400

150 300

GWhs

GWhs

100 200

50 100

- -

16-Mar 17-Mar 18-Mar 19-Mar 20-Mar 21-Mar 22-Mar 16-Mar 17-Mar 18-Mar 19-Mar 20-Mar 21-Mar 22-Mar

1 April 2020 Vietnam 7 April 2020 Singapore

“Soft Lockdown Measures” Circuit breaker measures

800 200

▼ 6.8 %

▼6.2 %

600 150

GWhs

GWhs

400 100

200 50

- -

30-Mar 31-Mar 1-Apr 2-Apr 3-Apr 4-Apr 5-Apr 6-Apr 7-Apr 8-Apr 9-Apr 10-Apr 11-Apr 12-Apr

In the charts above we highlight the day to day drop in reported GWhs between the day before lockdown and the day of lockdown. However, for Vietnam and Singapore the impact was slightly delayed.

• For Singapore we measure the day to day drop based on 8 Apr (day after lockdown, and day when schools closed)

• For Vietnam we measure the day to day drop based on 3 Apr (2 days after lockdown as 2 Apr was a public holiday)

15

Source: PEMC; GSO; NLDC EVN; EMC; TLG AnalysisLockdown measures were clearly the immediate cause of reduced demand (2)

25 March 2020 New Zealand 25 March 2020 Australia

Lockdown “Stage two restrictions"

150 600

▼3.0 %

▼12.5 %

100 400

GWhs

GWhs

50 200

- -

23-Mar 24-Mar 25-Mar 26-Mar 27-Mar 28-Mar 29-Mar 23-Mar 24-Mar 25-Mar 26-Mar 27-Mar 28-Mar 29-Mar

Comparison with the 3 preceding weeks Comparison with the 3 preceding weeks

New Zealand Australia NEM

110 600

100

Lo

GWhs

GWhs

ck

do 500

wn

we

90 ek Lockdown week

80

400

Mo nday Tuesday We dnesday Thursday Frid ay Saturday Sunday

Mo nday Tuesday We dnesday Thursday Frid ay Saturday Sunday

We ek 10 (2 Mar - 8 Mar) We ek 11 (9 Mar - 15 Mar)

We ek 10 (2 Mar - 8 Mar) We ek 11 (9 Mar - 15 Mar)

We ek 12 (16 Mar - 22 Mar) We ek 13 (23 Mar - 29 Mar)

We ek 12 (16 Mar - 22 Mar) We ek 13 (23 Mar - 29 Mar)

16

Source: EA; AEMO; TLG AnalysisThe initial impact of lockdowns was then typically followed by further

consumption declines in weeks to follow

Daily Electricity “Demand” (March and April)

800

700 Average Daily “Demand”

% change Week before Week after

Daily electricity “demand” (GWh)

600 Lockdown Lockdown

▼ 7.8 % 680 GWh 627 GWh

500

400

300

▼ 29.2 % 380 GWh 269 GWh

200 ▼ 25.5 % 257 GWh 192 GWh

▼ 6.5 % 145 GWh 136 GWh

100

▼ 12.4 % 101 GWh 88 GWh

-

r r ar ar ar Ap

r pr pr pr

- Ma - Ma -M -M -M 6- 3-A 0-A 7-A

2 9 16 23 30 1 2 2

March 17 March 18 March 25 April 1 April 7

Philippines Malaysia New Zealand Vietnam Singapore

Lockdown start date

Vietnam Peninsular Malaysia Philippines (Luzon and Visayas) Singapore New Zealand

17

Source: PEMC; GSO; NLDC EVN; EMC; EA; TLG AnalysisDiversity of impacts and staging across Asia Pacific to end March

Change in March Electricity “Demand”

Average Daily Electricity “Demand”

February & March - 2019 & 2020 Y-o-Y M-o-M

Mar 2020 vs Mar 2019 Mar 2020 vs Feb 2020

.

Peninsu

Philippi Australi Malaysi

Malaysia February

Pe

n in su la

r Ma

l a

y sia

-10.0% Pe

n in su la

r Ma

l a

y sia

-8.3%

lar

a

(Peninsular) March

nes a - NEM

Australia February Au

s tra lia - N E

M

-6.6% Au

s tra lia - N E

M

-7.0%

(NEM) March

February -5.2% -1.0%

Philippines

Ph

il ip in e

s Ph

il ip in e

s

March

(Luzon and Visayas)

China

February -4.2% 16.8%

China

Ch

in a Ch

in a

March

re Zealand Korea

Singapo New South

South February

March

So

u th K o

re a

-4.0%

So

u th K o

re a

-7.6%

Korea

February

New March Ne

wZ e

a la n

d

-1.9%

Ne

wZ e

a la n

d

-4.2%

Zealand

February

March 2.4%

S in

g a p

o re

1.3%

Singapore

S in

g a p

o re

Vietnam Taiwan

February

Taiwan March Ta

iw a n

2.6%

Ta

iw a n

2.0%

Vietnam February

March 4.8%

3.0%

V ie

t n

a m

V ie

t n

a m

All countries 0 500 1,000 1,500 2,000

except China

0 5,000 10,000 15,000 20,000 February 2019 February 2020

China

March 2019 March 2020

Average Daily “Demand” (GWh)

18

Source: GSO; AEMO; PEMC; NEA; KPX; EA; EMC; MOEA BOE; Taipower Statistics; NLDC EVN; TLG AnalysisIt then just got worse (April)

Change in April Electricity “Demand”

Average Daily Electricity “Demand”

March & April - 2019 & 2020 Y-o-Y M-o-M

April 2020 vs April 2019 Apr 2020 vs Mar 2020

March

Philippine Malays

Penins

Malaysia -22.5%

ular

April -13.0%

Pe

n in su la

r Ma

l a

y sia

ia

Pe

n in su la

r Ma

l a

y sia

(Peninsular)

Philippines March

-19.8%

s

(Luzon and Visayas) April

Ph

il ip in e

s Ph

il ip in e

s

-10.8%

China

March

China April Ch

in a

0.7% Ch

in a

4.8%

Zealand

March

Singapor New

New Zealand April Ne

wZ e

a la n

d

-9.5% Ne

wZ e

a la n

d

-6.9%

March

Singapore

e

April S in

g a p

o re

-6.0%

S in

g a p

o re

-6.2%

Vietnam

Vietnam March

April V ie

t n

a m

-8.8%

V ie

t n

a m

-7.6%

Korea

South

South March

Korea April So

u th K o

re a

-6.5%

So

u th K o

re a

-6.4%

Taiwan

March

Taiwan April -2.2%

-3.4%

Ta

iw a n

Ta

iw a n

All countries

except China 0 500 1,000 1,500 2,000

China

March 2019 March 2020

0 5,000 10,000 15,000 20,000

April 2019 April 2020

Average Daily “Demand” (GWh)

19

Source: GSO; PEMC; EA; EMC; NLDC EVN; KPX; MOEA BOE; Taipower Statistics; TLG AnalysisWith more movement or adaptation, some reversion/recovery is evident

Change in May Electricity “Demand”

Average Daily Electricity “Demand”

April & May - 2019 & 2020 Y-o-Y M-o-M

May 2020 vs May 2019 May 2020 vs April2020

April

Philippines Malaysia

Peninsul

Malaysia May -11.1%

14%

ar

Pe

n in su la

r Ma

l a

y sia

(Peninsular)

Pe

n in su la

r Ma

l a

y sia

Philippines April

(Luzon and Visayas) May -13.8% Ph

il ip in e

s

Ph

il ip in e

s

13%

Singapore

April

Singapore May -8.3% -1%

S in

g a p

o re

S in

g a p

o re

Vietnam

April

Vietnam May V ie

t n

a m

1.8% V ie

t n

a m

13%

South Korea

April

South Korea May So

u th K o

re a

-0.8% So

u th K o

re a

-8%

Taiwan

April

Taiwan

May Ta

iw a n

19.8% Ta

iw a n

16%

0 400 800 1,200 1,600

April 2019 April 2020

Average Daily “Demand” (GWh)

May 2019 May 2020

20

Note: South Korea data is as of May 10th ,2020 Source: GSO; PEMC; EA; EMC; NLDC EVN; KPX; MOEA BOE; Taipower Statistics; TLG AnalysisImpact on Electricity Demand Level and Profile – Peninsular Malaysia

Daily Consumption Before and After MCO

• Movement Control Order (MCO) resulted in a 16% drop in daily GWh

450

consumption on March 18, 2020

400

• The daily consumption has experienced a slight recovery after

350

the conditional movement control order (CMCO) was

300

implemented within MCO phase 4 on May 4, 2020

250

• Total consumption in April 2020 decreased by 22.5%, compared

200

to that of the same month in the previous year March 18, 2020 May 4, 2020

150

• Peak demand in April shifted from daytime (8am – 7pm) to MCO in effect CMCO of phase 4

100 in effect

night-time (7pm – 1am)

50

0

Monthly Consumption 2019 vs 2020

TWh

0

0

0

0

0

0

0

0

0

0

02

02

02

02

02

02

02

02

02

02

12 -9.99% -22.50%

-2

-2

-2

-2

-0.79% 6.85%

-2

-2

-2

-2

-2

-2

ay

an

an

an

eb

ar

ar

ar

pr

pr

-A

-A

-M

-M

-M

-M

-J

-J

-J

-F

11.4

15

30

01

16

31

15

01

16

31

15

10 11.0 10.9 11.1

10.4 10.2

9.8 Shift in Diurnal Demand Profile (Evening Peak)

100%

8 8.6

95%

6

Load Factor

90%

4 85%

80%

2

75%

0 70%

2019 2020 2019 2020 2019 2020 2019 2020 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Jan Feb Mar Apr Hour

Apr 2020 (Post-MCO) Feb 2020 (Pre-MCO)

Before Movement Control After Movement Control

21 Apr 2019 (Pre-MCO)

Source: GSOWith Covid-19 still under control Taiwan maintains a mostly upbeat outlook

Taiwan has managed to contain the outbreak (442 confirmed cases and 7 deaths as of 31 May) without a

lockdown seen elsewhere. Taiwan’s economy is heavily reliant on exports (70% of GDP). Major export partners

includes Mainland China and HK (40%), ASEAN (18%), USA (12%), Europe (9%) and Japan (7%). In March 2020,

exports dropped to Europe, USA, and Japan but increased to Mainland and HK.

Daily New Cases (as of May 31) Taiwan 2020 GDP forecast

30

1.7% Taiwan government (28 May)

25

-1.32% IHS Markit (May)

20

0.5% S&P (4 May)

15

1.6% TIER (24 Apr)

Taiwan Institute of Economic Research

10

1.0% CIER (17 Apr)

Chung-Hua Institution Economic Research

5 -4% IMF (14 Apr)

0 1.80% ADB (3 Apr)

Ma y 04

Ma y 08

Ma y 12

Ma y 16

Ma y 20

Ma y 24

Ma y 28

Apr 02

Apr 06

Apr 10

Apr 14

Apr 18

Apr 22

Apr 26

Apr 30

Feb 2

Feb 6

Feb 10

Feb 14

Feb 18

Feb 22

Feb 26

Ma r 01

Ma r 05

Ma r 09

Ma r 13

Ma r 17

Ma r 21

Ma r 25

Ma r 29

Jan 21

Jan 25

Jan 29

-5% -4% -3% -2% -1% 0% 1% 2% 3%

Source: S&P, IMF, IHS Markit, ADB, TIER, CIER, Directorate General of Budget, Accounting and Statistics

Source: Taiwan CDC

22Taiwan’s electricity demand in April dropped due mainly due to slowing global

growth and lower temperature

Average Daily Demand by Week (Jan - May) Peak Daily Demand (Jan - May)

800 35% 800 30%

700 2020 Chinese New Year 30%

700 25%

25%

600 600 20%

20%

% changes

500 15%

% changes

500

GWh

15%

GWh

400 10% 10%

400

2019 Chinese New Year 5% 5%

300 300

0% 0%

200 200

-5% -5%

100 -10% 100 -10%

- -15% - -15%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Week No. Week No.

% 2020 2019 % 2020 2019

Average Daily Demand by Month

700 30%

600 25%

20%

500

15%

% changes

GWh

400 10%

1.9% 2.9% 5%

300 1.4%

0%

200

-5%

-3.4%

100 -10%

- -15%

Jan & Feb Ma rch April Ma y

Week No.

23

% Change 2020 2019 Source:TaipowerNever forget to check the temperature….

Taipei temperature comparison (Jan - May)

35

30

25

20

15

10 Jan Feb Mar Apr May

2019/2020

5 -3.2% -1.1% 4.7% -13.6% 7.7%

YoY

0

Ma y

Ma y

Ma y

Ma y

Ma y

Ma y

Ma y

Ma y

Ma y

Ma y

Ma y

Feb

Feb

Feb

Feb

Feb

Feb

Feb

Feb

Feb

Ma r

Ma r

Ma r

Ma r

Ma r

Ma r

Ma r

Ma r

Ma r

Ma r

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Apr

Apr

Apr

Apr

Apr

Apr

Apr

Apr

Apr

Apr

2019 2020

35

Taipei temperature comparison - April 35 Taipei temperature comparison - May

30 30

25 25

20 20

15 15

10 10

5 5

0 0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031

24 2019 2020 2019 2020

Source:Taiwan Central Weather BureauPhilippine experience highlights temperature in a different way…lockdown has

occurred during an exceptional heat wave recovering some of the lost demand

MW Luzon MW Visayas

12,000

2,200

11,000

2,000

10,000 2017

2017 1,800

9,000

Nearly 50 degrees C 1,600 July 2017

earthquake

~20% fall in Luzon (extreme heat wave) in Leyte

8,000 peak demand vs.

preceding weeks

1,400 Limited impact

7,000 1,200

6,000 1,000

More resilient offpeak demand in Visayas relative to

Unlike Visayas, offpeak demand in Luzon, likely reflecting a lower concentration of industrial

the main economic region of Luzon demand – we note, however, that quarantine measures

5,000 has also suffered a sharp decline 800 were implemented later in Visayas compared to Luzon

4,000 600

3,000 400

k.1 k.5 k.9 k.1

3

k.1

7

k.2

1

k.2

5

k.2

9

k.3

3

k.3

7

k.4

1

k.4

5

k.4

9 k.1 k.5 k.9 k.1

3

k.1

7

k.2

1

k.2

5

k.2

9

k.3

3

k.3

7

k.4

1

k.4

5

k.4

9

W W W W W W W W W W W W W W W W W W W W W W W W W W

2017 Min 2017 Max 2018 Min 2018 Max 2017 Min 2017 Max 2018 Min 2018 Max

2019 Min (YTD) 2019 Max (YTD) 2020 Min (YTD) 2020 Max (YTD) 2019 Min (YTD) 2019 Max (YTD) 2020 Min (YTD) 2020 Max (YTD)

25 Note: Years have been rebased to show Week 1 commencing from the first Monday of each year; demand figures are ex-post

Source: PEMC; TLG analysisSummary points

• Covid-19 incidence rates are still not under control across all countries, but the mortality story is

distinctively encouraging and population age demographics are favourable

• Lockdowns had by far the largest impact on demand (of course)

• Several countries are showing demand recovery, even modest growth, on a year-over-year

basis as Covid progresses and movement restrictions ease

– Mainland China’s recovery continues to show strength

– Many Asian countries are still poised get back onto a growth track, even if the rate is less than it was

– The impact of the rest-of-world economic demise is not yet clear

• In teasing out key factors, just note that February through May has highly variable weather

– Normally the peak period for markets like the Philippines

– Residential bill shock in the Philippines, for example, will be much greater

– Temperature effects also present in the data

• Because growth is already part of many (not all) Asian’ electricity systems, adaptation to a lower

rate of growth will often lead to new project deferral, restoring fundamentals sooner

26About The Lantau Group

Headline Impacts Impact on Fuel Markets

Other Points

Summary

27Fuel market “stories” are always easiest in retrospect

Dated Brent Price Outlook (Real) Year

In US$/bbl Dated

120 over

Brent

2017-2018 Year

Higher-than-expected 2014 99.0

100 production management;

sharp collapse in 2015 52.4 -47%

Venezuelan output;

2019

2016 43.7 -17%

US sanction expectations on Price declined 9% y-o-y to

US$/bbl (real terms 2020)

80 Iran; Geopolitical risks $64/bbl in 2019 amidst escalated 2017 54.4 24%

US-China trade tensions and

weaker global oil demand 2018 71.0 31%

2019 64.3 -9%

60

?

2020 39.7 -38%

2021 41.6 5%

40

2014-2016 2022 44.7 7%

Oversupply (driven by surge in US

20

output); weak demand; Saudi

policy to keep market share

2020 Recent events have

Covid-19 and Saudi/Russia been dramatic, but

we’ve seen similar year-

0 over-year changes in

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

the past

28 Notes: Forecast prices in 2020US$/bbl; 2010-2019 are actuals, forecast thereafter

Source: ICE, Based on latest market forward curves for the front 2 yearsKorea’s cost-based electricity pool market is a useful “lens” into the impact of

the most recent (short-term) fuel market disruption

Snapshot of Short Run Cost-Based Merit Order in Q3 2020 at Different Oil Prices

160

140

Price

Prices($/MWh)

at oil price $65/bbl in H1 2020 (prior expectation)

120 Prices

Price at oil price ~$52/bbl in Q1 2020 / ~$23/bbl in Q2 2020

($/MWh) Oil

100

Price ($/MWh)

80 LNG

60

Coal

40

Coal and LNG

20

Renewables Nuclear ILLUSTRATIVE

0

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Cumulative Quantity (MW)

• The chart compares typical merit order of the Korea wholesale power market – stacking renewables, nuclear, coal, LNG and oil in the order –

against the expected merit order for Q3 2020 based on outturn oil prices since Q1 2020.

• Typically, there are occasions where SRMC of high coal units coincides with low-priced LNG-based units, SRMC of LNG generation mostly sit

after coal. And, LNG often sets SMP (more than 85% of the time).

• In 2020, the impact of oil price drop in Q1 2020 on SMP is expected to be realised in Q3 2020. Associated price drop in oil-linked gas volume

would make many of LNG-using power plants competitive against coal unit, resulting in reversal of coal and gas in the merit order. (This would

be highly dependent on plant efficiencies of coal and gas power units). Accordingly, SMP currently hovering 75-85 KRW/kWh is forecast to

drop to 40-50 KRW/kWh level.

29

Note: The supply curve is a snapshot of a particular timeslot of Q3 2020, on the basis of TLG assumptions around availability of each power plant.

Source: TLG AnalysisThe outlook for oil prices has changed less than immediate disruption suggests

Dated Brent Monthly Price Dated Brent and Forward Curves

80

140

Since 2008

70

Global Financial Crisis

120 Since 2014

60

June 2014

100

October 2014

50

US$/bbl

Dated Brent fell to multi year lows of

End 2009 Since 2015

80 Jun 2015

USD/bbl

US$17/bbl on April 21, 2020

40

Jul 2018

End 2008 Feb 2019

60

30 Aug 2019

Demand reduction from Covid-19 Spot

outbreak following on from the Saudi- Brent May 2020

Russia production standoff 40

20

Jan 2016

10 20

0 0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

19

20

9

19

20

9

01

01

20

20

20

20

l-2

-2

n-

n-

r-

r-

ct

Ju

Ap

Ap

Ja

Ja

O

3031

thousands of barrels produced in the USA per day

3,500

7,000

10,500

14,000

0

1983-01-01

1984-01-01

1985-01-01

1986-01-01

1987-01-01

1988-01-01

1989-01-01

1990-01-01

1991-01-01

1992-01-01

1993-01-01

1994-01-01

1995-01-01

1996-01-01

1997-01-01

1998-01-01

1999-01-01

2000-01-01

2001-01-01

2002-01-01

2003-01-01

2004-01-01

2005-01-01

2006-01-01

Things to watch: US Oil Production (bbls per day)….

2007-01-01

2008-01-01

2009-01-01

0

20

40

60

80

100

120

2010-01-01

2011-01-01

2012-01-01

2013-01-01

2014-01-01

2015-01-01

Source: www.macrotrends.net

2016-01-01

2017-01-01

2018-01-01

Brent Price Outlook (Real)

2019-01-01

2020-01-01Dated Brent Forward Curve Evolution – a lot of strengthening lately –

particularly at the back end

Brent Forward Curve

USD/bbl As of end of May

65

14 J

an (B

efore

60 COV

ID-1 29 May

18 Feb 9) February price range

18 May

55

50

arch 20 March

6M

45 rch

1 Ma rch Long-term price saw a recovery

1 a

9M in early May because of the

Will the near term kill easing of economic restrictions

40

and expected demand recovery

so much investment

that the long-term

35

shortage risk rises?

30

25 Near-term prices continued dropping in

il

Apr

April due to depressed demand and

insufficient storage

29

20

Sep-20

Sep-21

Sep-22

Sep-23

Sep-24

Sep-25

Sep-26

Sep-27

Sep-28

Jun-20

Jun-21

Jun-22

Jun-23

Jun-24

Jun-25

Jun-26

Jun-27

Jun-28

Dec-20

Dec-21

Dec-22

Dec-23

Dec-24

Dec-25

Dec-26

Dec-27

Dec-28

Mar-21

Mar-22

Mar-23

Mar-24

Mar-25

Mar-26

Mar-27

Mar-28

Mar-29

32

Source: BloombergIn Asia Pacific, coal market impacts are strongly influenced by China

China’s annual coal import and export China’s Coal import by country in 2019

350

China became a net

300 coal importer for the United States

Vietnam Others

first time in 2009 0% 5%

0%

250 Colombia

Annual import/export (mmt)

1%

200 Canada

1% Russia

9%

150

Indonesia

100 46%

Mongolia

12%

50

0

-50 Australia

26%

-100

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Import Export Net import

Source: NDRC, World Bank Source: Bloomberg

33China’s thermal generation (coal) down 10% in January-March, but could have

been much worse, as there was also sharply reduced hydro availability

China Daily Average Generation mix 2017-19

2019 – 2020

Jan-Feb vs Mar Q1 Changes

CAGR

%

20 18.6 18.4

17.7 17.8 Total +6.4% -15.6%

17.1 16.7 17.0 Solar

15.8

15 Solar +37.5% +40.2%

Win d

Wind +15.0% +19.7%

TWh

10 Hydro

Note: Weak water flow in

Hydro +3.1% -13.6% Q1 and weak demand

Thermal both contributed to hydro

generation reduction.

5 China also probably

Thermal +5.5% -10.5% increased some storage.

Nuclear

0

Nuclear +18.5% +1.9%

2017 2018 2019 2020 2017 2018 2019 2020

Jan-Feb Ma r

6 China daily thermal coal consumption estimation

-10.3% -8.1%

yoy yoy

Million tonne

4

2

0

Jan-Feb 19 Ma r-20 19 Apr-2019 Ma y-2019 Jun-2019 Jul-2019 Aug-2019 Sep-2019 Oct-2019 Nov-2019 Jan-Feb 20 Ma r-20 20

34

Source: Generation from NBS, Demand from CEC. TLG AnalysisCoal price dynamics were less immediately responsive, but subsequently

responded to downward demand pressure

In US$/MT

Monthly Newcastle Coal Price

Newcastle Coal Price Outlook (Real)

120

100

80

USD/MT

140 2017-2018

60

Coal prices were historically strong in 40 Coal price has fallen ~32% ~59

recent years as China’s power demand

jumped 8.5% y-o-y in 2018. Coal imports 20 from a year ago to US$59/MT

120

increased 3.9% while exports fell by 0

55.3% in 2018

19

20

9

19

19

20

9

9

0

19

19

9

9

9

9

0

l-1

r-1

-1

r-2

-1

-1

-1

-1

-2

b-

b-

n-

n-

n-

g-

p-

ar

ar

ct

ov

ec

ay

Ju

Ap

Ap

Fe

Fe

Ja

Ju

Ja

Au

Se

O

M

M

N

D

M

100

US$/MT (real terms 2020)

Impacts on Fuel Markets US$/MT

Observation: If coal prices recover

80 faster than (or do not decrease as

much as) oil/gas, then gas may enjoy a

60

? more persistent advantage. This is not

a strong theme that we’ve noticed yet in

2019

China, but it would make sense.

Coal prices plunged nearly 28% y-o-y in

40 2019 to $77.5/MT on the back of 2020

slackened demand from China coupled

with switch to gas amidst the glut of Near term outlook expected to remain

cheap gas in Europe soft as concerns over weakened

economic and industrial activities place

20 growing pressure on demand.

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Notes: Forecast prices in 2020US$/MT; 2010-2019 are actuals, forecast thereafter

35 Source: ICE, Based on latest market forward curves for the front 2 yearsAbout The Lantau Group

Headline Impacts Impact on Utility Costs

Other Points

Summary

36The pandemic will have different effects in each jurisdiction – however, we can

look at the impacts for a generic utility cost structure

Generic Utility Cost Structure in SEA Before Pandemic

Other

(Retail, Operations)

100%

4%

Distribution Network Costs Over 50% of utility costs are largely fixed in the near-

16% • These are often the next term, and thus, demand destruction related to the

largest component gen pandemic will generally increase the average costs per

80% • Distribution is typically more kWh for customers corresponding to these costs (NB: not

Transmission an increase in costs, but in average rates)

costly than transmission

10%

The details of the differences between regulatory

Generation Generation Costs frameworks from one jurisdiction to the next will

(Capacity and FOM)

• These are often the largest determine the mechanics of the extent to which these

60%

23% utility cost component, often costs are passed through (future tariffs and ‘clawbacks’),

comprising around 70% of and the period over which they are passed through

total utility costs

• These are often primarily

Generation

40% (Fuel and VOM)

variable costs (~2/3rds),

mostly related to fuel, but also

contain a substantial amount of

fixed costs related to capacity Broad energy demand destruction globally has placed

payments immense pressure on energy prices, which have

47%

20% • These can vary substantially plummeted since the beginning of the year – this will drive

by jurisdiction depending on declining variable costs across jurisdictions

the generation mix and

Domestic fuel availability and

policy

0%

1

37The short-term loss of sales from reduced demand is likely to be more than

offset by the longer-term fall in fuel prices

Indicative Analysis of Cost Impacts of Pandemic

Lockdown Period Easing Period Recovery Period

(Apr – May 2020) (e.g., Jun – Dec 2020) (2021)

• The process by which demand

Fixed Cost Pressures: Demand destruction related to the pandemic will increase the burden of fixed

destruction increases end-user

Assuming Fixed Costs are ~53% of Total costs for remaining customers

tariffs will differ by regulatory

Demand Destruction: regime, and in some cases, this

-15% -5% -2% burden may be borne in part by the

(Indicative assumptions)

utilities/retailers

Impact on Average Cost: • Generally, this takes more time

(Assuming all non-fuel/VOM costs are +9.4% +2.8% +1.1% under most regulatory mechanisms

‘fixed’ in the near-term)

to impact end-user rates (lagged)

Softened fuel markets related to the pandemic will decrease sector costs for • In regulated jurisdictions, fuel cost

Fuel Cost Relief:

Assuming Fuel Costs are ~43% of Total customers savings will be passed through to

end-users, albeit with some lag

Coal Price Change*: depending on the applicable regulatory

(Newcastle, adjusted for shipping) +3% -22% -16% mechanisms

• In unregulated jurisdictions, fuel

Gas Price Change*: cost savings may not be

(Brent price change – this does not

account for new gas/LNG contract -25% -54% -41% immediately realized by retailers,

slopes or spot purchases of gas/LNG) who often hedge these, nor by

customers, who sometimes are

Fuel Cost Impact: -4.6% -16.3% -12.1% ‘locked-in’ to specific rates for a period

(Assuming fuel costs are 50/50 coal/gas)

of time

Net Cost Impact: +4.8% -13.5% -11.0%

* Pre-Pandemic price based on Jan forwards; Post-pandemic based on combination of actual spot prices (April – May 2020) and recent

38forward curves (June 2020 and beyond)Comparison of fuel price expectations / out-turn before and after the pandemic

Newcastle Coal Brent Oil

USD/MT USD/bbl

80 10% 70 0%

5% -10%

75

60

0% -20%

70

50

-5% -30%

65

-10% -40%

40

60

-15% -50%

30

55

-20% -60%

50 -25% 20 -70%

2020-Aug

2020-Sep

2021-Aug

2021-Sep

2020-Aug

2020-Sep

2021-Aug

2021-Sep

2020-Apr

2021-Apr

2020-Apr

2021-Apr

2021-Feb

2021-Feb

2020-Jul

2021-Jul

2020-Jul

2021-Jul

2020-Jun

2020-Nov

2020-Dec

2021-Jan

2021-Jun

2021-Nov

2021-Dec

2020-Jun

2020-Nov

2020-Dec

2021-Jan

2021-Jun

2021-Nov

2021-Dec

2020-Oct

2021-Oct

2020-Oct

2021-Oct

2020-May

2021-Mar

2021-May

2020-May

2021-Mar

2021-May

Change Pre-Pandemic Post-Pandemic Change Pre-Pandemic Post-Pandemic

‘Pre-pandemic’ based on forward curve beginning of February 2020

‘Post-pandemic’ based on actual spot prices through May 2020, and forward curves at beginning of May for June 2020 onwards

39About The Lantau Group

Global Financial Crisis as

Headline Impacts Comparator

Other Points

Summary

40A perspective from the Global Financial Crisis

Monthly Electricity Demand

5,000 25% 5,000 25% 25,000 25%

4,500 4,500

20,000 20%

4,000 20% 4,000 20%

17%

Monthly “Demand” (GWh)

Monthly “Demand” (GWh)

Monthly “Demand” (GWh)

3,500 3,500

Annual growth rate (%)

Annual growth rate (%)

Annual growth rate (%)

15,000 15%

3,000 15% 3,000 15%

2,500 2,500 10,000 10%

7%

2,000 10% 10% 2,000 9%

10%

5,000 5%

1,500 1,500 3%

2%

5%

1,000 5% 1,000 4% 5%

3% 3% - 0%

2% 3%

500 500 -1%

1% -2%

1%

0.1%

- 0% - 0% -5,000 -3%

-5%

07

08

09

10

11

12

06

07

08

09

10

11

12

06

07

08

09

10

11

12

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

Annual Electricity Demand Growth Rate (%) Annual Electricity Demand Growth Rate (%) Annual Electricity Demand Growth Rate (%)

Monthly Electricity Demand (GWh) Monthly Electricity Demand (GWh) Monthly Electricity Demand (GWh)

41

Source: PEMC; EMC; MOEA BOE; Taipower Statistics; TLG AnalysisDuring the GFC, for example, Philippine GDP growth stayed positive through a

15-month decline, taking ~9 months to recover from its bottom

Historical quarterly YoY real GDP growth in the Philippines

10.0% • In the 2008 Global Financial Crisis, Philippine GDP growth fell

from 5.1% to 1.1% over 15 months, with electricity demand less

impacted (the demand-GDP elasticity trended above 1)

• Whilst the nature of the exogeneous shock from COVID-19 is in many ways unique, analysis

of the GFC highlights that the recovery of GDP to pre-GFC levels took 9 months. This is not

inconsistent with the recovery currently projected by the IMF, ADB, and World Bank (see RHS)

7.5%

“V” Recovery

5.0%

2.5%

0.0%

8 08 09 09 10 10 11 11 12 12 13 13 14 14 15 15 16 16 17 17 18 18 19 19 20 20 21 21

-0 - - - - - - - - - - - - - - - - - - - - - - - - - - -

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

42 Note: Third party forecasts for GDP lack quarterly granularity..

Source: Bangko Sentral ng Pilipinas; ADB; IMF; World BankAs of now, the recovery profile is not yet clear – and probably depends most on

the nature of COVID-19 response (vaccine, treatment, herd immunity, distancing etc.)

20% Real GDP growth rate yoy

Taiwan South Korea Australia Ma inland China Ma laysia Singapore Thailand Vietnam Philippines

15%

10%

5%

0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020E

-5%

Global Financial Crisis COVID-19

-10%

43 Source: WorldBank, and BloombergSome segments (e.g. tourism) will be hurt more deeply and for longer – due to

public fear and because of less discretionary income if a prolonged recession

Forecast providers Indicator Impact of COVID-19

44% International tourist arrivals in 2020: three scenarios

International air (YoY monthly change %)

passenger traffic 80%

20

Airlines’ revenue passenger Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

56% 0

kilometers (intl. and dom.)

Monthly change, %

-20 Actual data

International tourism US$910bn (-62%)

Scenario 1

receipts Gradual opening of borders

US$1,170bn (-79%) -40 Scenario 2

and lifting travel restrictions

Scenario 3

13% -60

Global merchandise trade

volume 32% In July In Sep

-80 In Dec

World GDP -3% contraction

-100

-6% contraction Source: UNWTO

Source: ICAO, IATA, UNWTO, WTO, IMF, Note: All figures are

V-shaped recovery 2020 data compared with 2019 data, except for airport revenue

figures which are compared to 2020 business-as-usual.

U-shaped recovery

Commercial flights flow statistics

150,000 2020 domestic 2020 international 2020 not specified 2019 total

100,000

50,000

0

1-Jan 1-Feb 1-Mar 1-Apr 1-May

Source: radarbox.com

44Sorting out economic impacts will take time. For example, Thailand, hospitality

is a significant driver of electricity demand (a correlate with GDP)

Thailand

GWh Historic power consumption by industry type GWh

Historic power consumption by business type

90,000

90,000

80,000

80,000

70,000

70,000

60,000 Manufacturing (Other)

60,000

50,000

Petroleum, Natural Gas 50,000

& Petrochemicals

40,000

40,000

Food

30,000

30,000

Restaurants & Hospitality

20,000

20,000

Retail

10,000 Metals, Metal Products, and Machining

10,000

Government, Public Services, and NGOs

0

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 0

20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20

Metals, Metal Products, and Machining Food

Petroleum, Natural Gas, and Petrochemicals Manufacturing (Other) Government, Public Services, and NGOs Retail

Textiles Agriculture, F orestry, and Fishing Restaurants and Hospitality Logistics, Transportation, and Storage

Mining Other Real Estate

Wholesale Financial Institutions

Construction

45 Note: Analysis based on TLG interpretation of TSIC codes - all industry types not necessarily represented

Source: EPPO; TLG analysisChina seems likely to recover faster (at this point) but exports from ASEAN

countries depend heavily on USA and EU markets

Export from ASEAN to USA Export from ASEAN to EU28 Export from ASEAN to China

(2019) (2019) (2018)

70 50 70

60 60

40

50 50

30

Billion Euros

40

Billion USD

40

Billion USD

30 30

20

20 20

10

10 10

0 0 0

T h ys ia

do d

M nam

ei

am os

ya s

a a

Br ia

M nam

M nam

T h ys ia

ng nd

T h ys ia

ng nd

ar

ar

am es

am es

ar

on e

ilip sia

ya a

o e

ilip sia

ya a

ei

ei

Br s

Br s

ilip re

I n ilan

M pine

T h ing esi

o

o

T h I nd por

M odi

T h nd por

M odi

un

d

un

un

C La

nm

nm

nm

Ph po

C pin

C pin

Si ila

Si la

La

La

bo

Ph e

Ph ne

a

S n

a

a

et

a

ai

b

b

et

et

a

a

a

al

al

al

Vi

Vi

Vi

I

e

e

e

46 Source: USA census, European commission, and General Administration of Customs of ChinaAgenda

1. Executive Summary

2. Overview of Singapore Electricity Market

About The Lantau Group

3. Key Market Drivers

4. Modelling Results

Headline Impacts

5. Appendix

Other Points

Summary

47About The Lantau Group

Headline Impacts

Other Points Diversity

Summary

48Wide variations in industry mix – suggesting very uneven impacts likely

Percentage Share of GDP by Industry Type (2018)

Cambodia 16% 23% 40% 22%

Vietnam 16% 28% 41% 15%

Malaysia 22% 18% 52% 8%

China 29% 11% 53% 7%

South Korea 27% 17% 54% 2%

Thailand 27% 8% 57% 8%

Philippines 19% 12% 60% 9%

Taiwan 33% 4% 61% 2%

Australia 6% 25% 67% 2%

Singapore 21% 10% 69% 0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Manufacturing Non-Manufacturing Industry Services Agriculture

49 Source: WB, TW Stats, TLG analysisMarkets like Singapore, Japan, Thailand, Korea (for example) all import LNG

and will benefit (or offset pain) via lower imported fuel costs

(others like Philippines have gas linked to oil prices, and others like Taiwan, Malaysia and Vietnam import a lot of coal)

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Vic, Vietnam Indonesia Korea Ma laysia Taiwan China New Delhi, Thailand Me ra lco, WA , Tepco, Singapore

Australia India Philippines Australia Japan

Hydro Other Renewables Nuclear Coal Natural Gas Oil Other

Source: Department of the Environment and Energy - Australian Energy Statistics, Electricity of

Vietnam (EVN), Ministry of Energy and Mineral Resources Republic of Indonesia, Bureau of

50 Energy - Ministry of Economic Affairs - Taiwan, China Electricity Council, Central Electricity

Authority – India, Meralco & Department of Energy – The Philippines, TEPCO – Japan, IEA,Countries like Vietnam with remarkably high growth rates may slow down, but

are unlikely to reverse

Power demand by sector in Vietnam 05-18 CAGR of

Consumption

200 192 40 • Against the backdrop of strong economic

+9.1% growth, electricity consumption more than

180 175 trebled from 46 TWh in 2005 to 192 TWh in

35 +18.4%

159 2018 – representing a CAGR of nearly 11.7%

05-18

160 Consumption over 2005-2018 period. Peak demand is

144 30 growing at a CAGR of 10.8% during the same

CAGR

140 129 period.

+11.7%

Peak demand (GW)

Consumption (TWh)

120

115 25 • The industrial sector is the main driver of

105 +13.5% electricity demand, accounting for over half

100

95

20 (55%) of electricity consumption in 2018,

86 having grown at 13.5% CAGR since 2005.

Peak Demand

75 CAGR 10.8%

80

66 15 • The residential sector accounts for

58 approximately one third of total electricity

60 51 +13.6%

46

10

consumption, with its share having gradually

40

reduced over time. Its CAGR of 9.1% is lower

than demand growth in either the industrial or

5 commercial sectors.

20

+9.1%

• The commercial and agricultural sectors

0 0

account for a relatively small portion of

electricity demand but recorded relatively

05

06

07

08

09

10

11

12

13

14

15

16

17

18

20

20

20

20

20

20

20

20

20

20

20

20

20

20

robust CAGR 13.6% and 18.4% respectively

Residential Commercial over the 2005-2018 period.

Industrial Agriculture

Others Peak Demand

51

Source: ADB, EVN and EVN NLDCImplications will vary greatly by region, and not just by country

Power demand growth YoY

2020 Jan-Feb Northeast Grid

2020 Mar Northeast Grid 2020 April Northeast Grid

+2.4% -1.2% +0.3%

+5.4% +1.3% +1.2% +5.0%

+1.0% +1.5%

+4.9% -1.1% +5.5% -4.0% +7.0% -0.5%

+4.9% North Grid -3.3% -1.0% North Grid -3.4% +6.6% North Grid -7.2%

-8.2% -7% -0.6%

Northwest Grid -7.6% Northwest Grid -4.6% Northwest Grid -1.7%

+0.1% -4.1% -0.6% +1.4%

-9.1% -8.8% -8.6%

+1.3% -1.2% +1.4%

+6.4% -0.4%

-7.9% -0.7% +2.0%

-13.7% -6.5% +0.5%

-16.8% -6.3% +0.3%

-2.3% Central Grid - -5.4% Central Grid -0.8% +11.7% Central Grid +5.3%

-2.6% -20.0% 10.4% -12.9% -2.9% -28.3% -9.3% +4.5% -5.4% -2.3%

-7.9%

East Grid

-21.3%

-6.9% East Grid

-1.3% -0.0% East Grid

-6.7% -12.2% -8.5% +6.6%

-0.8%

-1.4% +5.9%

-5.5% -2.7% +5.1%

-7.9% -6.8% -2.5%

South Grid South Grid

+6.6% +4.3% South Grid +9.3%

-1.9%

-13.2% Central grid and -3.8%

-6.2%

+5.2%

-5.6%

costal provinces were

-4.9% hit bad, and has not -7.8% -11.7%

recovered to 2019

level in March. Almost all provinces saw

improved growth rate in April.

20%

Jan-Feb Ma r April

10%

0%

-10%

Northeast Northwest South

-20% Central Grid East Grid North Grid Grid Grid Grid

-30% lo ilin

ng

H i

Sh i

Li lia

Si ng

Be n

an

ho nan

su

jin

I n ha x i

Yu n

t

Sh ng

Sh uan

G i

H xi

ou

g

H i

G ng

Z h su

Xi ia

N ai

ng g

G an

ng

J i ai

on g

Fu i

gx

e

e

be

hu

nx

jia

na

ijin

ua ian

r M on

gx

ub

eb

n

ng

gh

gh

go

an

g

ia

qi

en

an

jia

zh

do

nn

ni

J

an

a

aa

Ti

An

an

u

ai

ch

ne nd

in

ej

ng

ua

in

j

H

H

ao

an

Ti

ng

n

ui

Ji

Q

S

ei

C

G

H

52

Source: CEC; TLG research and analysisFor some, fuel cost decreases already more than offset demand reduction

Generation Total operating Total operating Profit margin

output 2020Q1 income 2020Q1 cost 2020Q1 vs. 2020Q1 vs.

vs. 2019Q1 vs. 2019Q1 2019Q1 2019Q1

Datang International

-5.7% -2.3% -3.3% +64.3%

(601991.SH)

Huadian International

-10.8% -6.0% -9.1% +54.4%

(600027.SH)

Huaneng International

-18.5% -11.6% -11.2% -22.4%

(600011.SH)

China Resources Power

-12.5% -8.2% N/A -10.4%

(00836.HK)

Guangdong Electric

-16.2% -15.8% -13.9% -93.3%

Power (000539.SZ)

Zhejiang Zheneng

Electric Power -36.8% -34.1% -32.8% -47.6%

(600023.SH)

Note: Generation output - 完成发电量; Total operating income - 营业总收入;

Total operating cost - 营业总成本; Profit margin - 归属于上市公司股东的净利润

Source: Company announcements; TLG Analytics, Caixin

53You can also read