Daily Grain / Livestock Marketing Outlook 4/20/2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Daily Grain / Livestock Marketing Outlook

Written by: Jim Gerlach

4/20/2021

Early Call 8:45am EDT: Corn up 5, soybeans up 24, wheat up 5. Early Tuesday, Dow

Jones futures are starting lower, in line with lower European markets, but are still near

its recent highs. June crude oil is trading higher after China reported higher import

volumes of oil in March, including an 8.8% increase from Saudi Arabia, reported

Reuters. The U.S. Dollar Index is slightly lower and most commodities are starting

higher. Grain prices are higher led by sharply higher soybeans and soybean oil

following sharp gains in Malaysian palm oil and continued poor weather in Brazil’s

safrinah crop areas.

Grains: Soybeans for May delivery rose 1.2% to $14.49 ¾ on the Chicago Board of

Trade Monday, with near-record highs in prices failing to derail strong demand for

exports. Corn for May delivery rose 1.1% to $5.92, while wheat for July delivery fell

0.2% to $6.53 ¾. Demand rationing isn't curbing consumption of U.S. soybeans,

meaning supply is expected to grow very thin as the year progresses. The tight supplies

in the U.S. continue and with the harvest winding down in Brazil, the demand for U.S.

soybeans is expected to remain strong which will continue to drain U.S. soybean

supplies. Product availability is setting up to be a real problem by mid-summer as the

U.S. runs low on beans to crush and strong commercial demand will ultimately keep

soybeans well supported and force soybean prices higher. South American weather was

a major source of support for both corn and soybean futures Monday. Monday’s biggest

weather concern is the 2021 Brazilian corn crop. The forecasts offer limited rain for the

next two weeks amid near to above-normal temperatures with highs holding in the 80's

to lower 90's. What happens to the Brazilian corn crop is of great importance to U.S.

farmers. Any loss of the 2021 Brazilian corn crop will be directed right to the U.S. with

nearly a 1:1 relationship in terms of what Brazil does not export from August into

January, the U.S. will. While Brazilian weather was a main factor for U.S. grains futures

Monday, U.S. weather also played a part. Dry conditions in the northern Plains have

helped Minneapolis wheat but there is a lot of corn planted up north too and that is

supportive for old and new crop. While problems exist with new crop, old crop will

1

have to rally too as the market will need to price ration both crop years to make sure the

market has adequate stocks for the 2021-2022 marketing year. U.S. inspections of corn

set to be shipped to China was a main supporter for corn export inspection figures this

week. In its weekly report the USDA said export inspections of U.S. corn totaled

1.5mmt for the week ended April 15. China was again the leading destination for U.S.

corn for the week, with over 560,000mt of corn sent there.

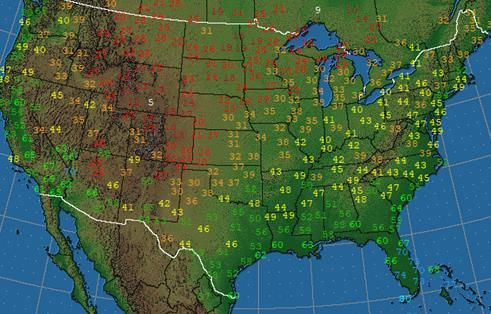

Rain/snow yesterday fell mostly in the central Plains and along the I-80 corridor (see

left map). Cold surged in the southern Plains overnight and again tonight, with an

estimated 10% of the crop in the southwest ¼ of the belt susceptible to damage. A

Midwest freeze the next 2 nights burns back SRW wheat growth, with localized losses

possible in the southern ¼ of the belt. Cold delays Midwest germination of

corn/soybeans, which likely limits freeze damage, with milder temps next week aiding

emergence in the southern 2/3rd of the belt. Rains become more active next week and

slow Midwest/Delta seedings, with the greatest delays expected in the southwest ¼ of

the Midwest (see 7-day NOAA forecast map upper right). Northern Plains showers

likely expand into ½ of the belt with a wetter risk in the 6-15 day period, aiding HRS

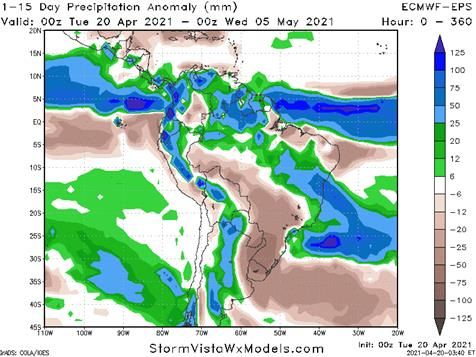

wheat germination. In Brazil, about ½ of the safrinah corn will remain in drought the

next 2 weeks (see map right), with drier

risk now in most model guidance with

patchy weekend showers. Isolated to

scattered 0.25” to 0.50” totals are forecast

for Paraná Sat-Sun with 0.25” to 1.00” in

Mato Grosso do Sul. The 00Z GEFS

model says 87% of safrinah corn in Brazil

will see under half normal rain the next

14 days, with 54% under one-fourth. 69%

and 36% of safrinha corn in Brazil had

under one-half and one-fourth its normal

rain 30 days. 45% and 5% were similarly

2

dry on the same growing day last year vs. 5% and 0% in 2019 and 12% and 0% 2018. In

Argentina, notable rains Wed-Fri stall harvest after the current, extended dry break

before turning dry again for over a week.

Bitter cold damaged jointing wheat in

western Kansas and jointing/booting

wheat in western Texas and western

Oklahoma overnight. Lows reached the

lower 20’s in northwest Kansas, the mid

20’s in the remainder of western Kansas,

western Oklahoma, and northwest Texas.

University studies show that jointing

wheat can sustain severe damage when

temps reach 24 degrees for more than 3

hours. The weekly NASS report showed that 17% of the northwest Kansas, 40% of

west-central Kansas and 71% of southwest Kansas wheat was jointing. 41% of the

Texas wheat crop was heading and extremely vulnerable. It is impossible to accurately

measure bushel losses until HRW wheat flowers so for now, the market will simply

speculate.

Despite the return of more winterlike weather across parts of the country, U.S. farmers

continued to plow ahead with corn and soybean planting last week, according to USDA

NASS' weekly Crop Progress report released Monday. As of Sunday, April 18, farmers

had planted an estimated 8% of intended corn acres. That was 2% ahead of last year's

6% and equal to the five-year average, according to NASS. Texas leads the way with

60% corn planted, Missouri is 14% planted, Illinois is at 12%, Indiana is at 7% and

Iowa is at 4% planted. Two percent of corn had emerged as of Sunday, above the five-

year average of 1% emerged for this time of year. In its first national soybean planting

report of the year, NASS estimated that 3% of the intended soybean crop had been

3

planted by week's end, slightly above 2% for both last year and the five-year average.

The three Southern states showing double-digit soybean planting progress were

Mississippi, Arkansas and Louisiana. Spring wheat planting was also running ahead of

normal, at 19% complete as of Sunday, well ahead of 7% at the same time last year and

12% for the five-year average. The state of Washington leads the way at 70% of spring

wheat planted, followed by Idaho and South Dakota, each at 46% planted. Development

of winter wheat, on the other hand, was running behind normal. Winter wheat heading

was estimated at 10% as of Sunday, behind 13% last year and 4% behind the five-year

average of 14%. For the third week in a row, winter wheat condition held steady at 53%

good to excellent, which is below last year's 57% good-to-excellent rating at the same

time. The week's highest good-to-excellent ratings for winter wheat were found in

California, Ohio and Michigan. Colorado, Texas and South Dakota had the lowest

ratings and are among the driest winter wheat states.

July corn is trading up early Tuesday as cash prices in the U.S. continue to find strong

demand throughout the country. The May contract is losing open interest as it

approaches delivery at the end of this month, but traded as high as $5.99 ¾ early

Tuesday, challenging the $6.00 mark again for the first time since 2013. Several cash

bids near $6.00 or higher are found in Iowa, Minnesota and South Dakota, areas not

normally known for strong basis this time of year. Late Monday, USDA said 8% of the

corn crop was planted and 2% of it has emerged, in line with the usual paces. Illinois is

12% planted and Iowa is at 4%. Obviously, even if weather cooperates, it is going to be

a while before new supplies come to the rescue of so many needing to buy corn now.

Tuesday morning's weather map showed precipitation falling from eastern Colorado to

northern Iowa. Temperatures are below freezing in eastern Colorado and western

Kansas, offering some threat to young crops of corn and wheat. The best rain chances

this week are in the southern Gulf states with light to moderate amounts expected in the

Eastern Corn Belt. The rest of the Corn Belt is mostly dry this week with better chances

for rain next week, especially on the eastern side. In Brazil, this week's rain forecast

remains light for southern Brazil and is a concern for the second corn crop. Technically,

the trends in July and December corn remain up with prices actively trading the high

ends of their ranges.

July soybeans are up sharply early Tuesday, punching into new high ground with cash

prices leading the way throughout the U.S. The May contract carries a roughly $.14

premium over the July with delivery coming the end of this month. It's not uncommon

to find cash prices bid above the futures board in Illinois and Indiana, but Tuesday's

morning bids are near or above even money as far west as western Iowa and

southwestern Minnesota, more signs of remarkable demand for soybeans. Late Monday,

USDA said 3% of the soybean crop was planted, slightly ahead of the five-year average

4of 2% for this time of year. Illinois and Ohio are 5% planted and Indiana is at 4%. This

week's colder temperatures are not enticing for planting activity, but there is plenty of

time for conditions to improve. This year's concern is not so much about crops getting

planted, but finding enough moisture after they are planted, especially in the western

Midwest where conditions are expected to be drier. In Brazil, where China is currently

buying its soybeans, the FOB price for May is trading at $544/mt ($14.82/bu.), the

highest price since 2014. That is incredibly strong demand for soybeans at harvest time

and keeps expectations high that China will be back later this year for more U.S.

soybeans. Technically, the trends in both May and November soybeans are up with

prices actively pushing higher.

Apparently, USDA has some clairvoyant ability to know what the Chinese are thinking

after comments made last week. There’s a lot chatter about reluctance of USDA to hike

2020/21 U.S. corn exports by more than the 75mb increase given in the last WASDE

report. This was addressed to government officials at this past week's USDA data users

meeting, where a panel was asked about leaving its estimate of China's 2020/21 corn

imports at 24mmt despite export sales suggesting a higher figure. The fact remains that

some feel USDA is forecasting China to roll over about 6mmt or 240mb of corn bought

for this year for the 2021/22 marketing season. Given still very high corn prices in

China, the fact that they are consuming every other possible feed source including

wheat and rice and a deteriorating Brazilian corn crop outlook actually suggests greater

U.S. sales to the Chinese not only this year but for the 2021/22 season as well. Current

sales on the books are 2.629 billion bushels (bb), by far the highest amount ever by this

point in the season and a whopping 98.3% of the recently upwardly revised USDA

projection of 2.675 bb, also the highest ever exceeding the prior peak of 95.7% in the

2013/14 season and just looking the fact we are just 46mb from attaining the USDA

target with 20 weeks left in this marketing year one could argue for a far higher final

overseas sales figure. The problem is that current shipments to date are 1.487 bb which

appears to be the second highest figure ever as of mid-April next to the 1.575 bb seen in

the 2007/08 season. This however is only 55.6% of the current WASDE estimate, which

is actually below average. This means every week between now and the end of August

the U.S. will have to ship over 59mb to attain this target, which many see as difficult

given that so far this year we have only averaged 46.5mb per week. This may seem

high, but in 5 of the past 6 seasons this rate has been exceeded and with the U.S.

soybean export program ending, there should be plenty of fob capacity and vessel

availability to get all of this corn moved from our shores. I would also mention that the

last 8 weeks have seen weekly corn export shipments average near 75mb/week and with

Brazil’s safrinha crop in trouble and local prices over $7.35/bushel, I expect the Chinese

to buy more/ship more than what they currently have on the books from the U.S.

5On the demand front, palm oil prices rose 2.5% overnight following positive export

data. Data from two cargo surveyors showed that April 1-20 palm oil exports rose 10.2-

12.7% on month, easing concerns about lower demand from India amid a renewed wave

of Covid-19 infections in the country. On China's Dalian exchange, September corn was

down 0.2%, July soybeans were up 0.3%, September soybean meal was up 1.1% and

September soybean oil was down 0.1%. China’s weekly wheat reserve auction saw just

411,000mt sell vs. 4.02mmt offered, easily the lowest sale rate of 2021 so far. However,

China raised the minimum sale price this week in an effort to cool demand. They also

changed the rules by allowing only end users to buy wheat, banning various traders

from buying in the auction and reselling later on their own terms. Brazil will allow duty

free imports of corn, soy oil and soymeal without tax in a highly unusual effort to cool

domestic prices following their record large soybean harvest. The 0% tax from non-

Mercosur countries will last into the end of the year. Brazilian domestic corn values

reached record highs late Monday at $7.35 as the winter corn crop withers under a dire

drought. Inflationary feed price pressures are a threat to Brazil's livestock industry,

while soy oil imports are needed for biodiesel. Black Sea wheat export values ticked

higher last week, up $1-$3/mt in Russia and $5/mt in Ukraine. Ukrainian corn values

rose $3/mt last week as well. Big U.S. basis pushes have not secured cash

soybeans/corn, which makes the shorts nervous ahead of first notice day next week.

There were reports that some Midwest processors were bidding $.90 over July soybeans

for June and could not replace that day's crush. That type of cash bidding with limited

farm sales response has the shorts in May soybeans worried that end users may stand up

for deliverable supplies.

U.S. corn exports for the week ended 4/15/21 were 1.525mmt (60.0mb), down modestly

from the previous week's 1.728mmt (68.0mb), but still significantly larger than last

year's same-week exports of 731,000mt (28.8mb) and, most importantly, better than the

roughly 51.0mb/week we estimate is needed in order to reach the USDA's 2.675 billion

bushel export projection. While there have been ongoing talk/comments about the

slower than expected loading of corn to China, the fact remains U.S. corn exports have

averaged 74.5mb (1.9mmt)/week over the last eight weeks. This week's activity

included 560,000mt shipped to China, leaving their official unshipped purchases on the

books at roughly 13.1mmt and could be closer to 14.5mmt when taking into account

sales to unknown. Cumulative export inspections of 1.545 billion bushels are up 85%

from last year's 837mb with 19 full weeks remaining in the 2020/21 marketing year.

U.S. soybean exports last week of 184,000mt (6.8mb) were down from the previous

week's 337,000mt (12.4mb), were well below last year's 552,000mt (20.3mb) and were

easily a new marketing year low as soybean exports continue to seasonally decline.

However, last week's exports were the first to fall below the average needed pace of

roughly 8.3mb/week in order to reach the USDA's 2.280 billion bushel export

6projection. Cumulative export inspections of 2.021 billion bushels are up 68% from last

year's 1.207 billion.

Hogs: Cash hogs are called steady to somewhat higher. Packers weren't overly

aggressive in Monday's cash market but seeing that slaughter speeds are running

vigorously and that pork cutouts closed higher, packers may feel more confident about

this week's market as demand remains strong. USDA’s National Average Base Hog

price was $104.94 up by $.45. The CME Lean Hog Index was another $.21 higher on

4/15 to $103.24. Pork cutout futures ended the session $1.87 to $2.25 higher for the

front months. USDA’s National Pork Carcass Cutout Value was reported at $114.08, up

by $1.99 on good movement of 329 loads. CME’s Fresh Bacon Index was quoted at

246.25 for the week ending 4/16. That was down by $4.11 but remains at record highs

for the March/April time frame. Estimated packer margins were $7.80/head for non-

integrators and $100.48/head for integrators vs. $5.29 and $96.89 the previous day.

Monday’s kill was up 0.41% vs. last week, with no comparison to last year’s Covid

plant shutdown figure.

Hogs completely diverged from cattle Monday as triple-digit gains were seen in all

contracts through July 2022. The temporary liquidation phase ran its course with futures

regaining most of the losses of Friday. The market has a way to go to regain the losses

of last week, but the strength Tuesday certainly seems to indicate that this may take

place sooner rather than later. Higher cash and higher cutouts continue to unfold as

strong demand and tightening supply permeates the market. Lean hog futures will

maintain the use of expanded limits for the Tuesday session. Pork cutouts closed higher

and Monday's slaughter is estimated at a brisk pace, which are all positive, bullish signs

to the lean hog market. June lean hogs closed $2.62 higher at $104.32, July lean hogs

closed $2.27 higher at $101.97 and August lean hogs closed $2.40 higher at $98.55.

With last week's mixed trade, the lean hog contracts were able to rally boldly through

Monday's hours and not feel immediately pressured by longtime resistance levels. So

long as domestic consumer demand can continue to shine through the market, hog

prices stand a chance at continuing to trade steady. Pork cutouts total 328.56 loads with

299.19 loads of pork cuts and 29.36 loads of trim. Pork cutout values: up $1.99,

$114.08. Monday's hog slaughter is estimated at 490,000 head -- 2,000 head more than a

week ago and 125,000 head more than a year ago. The CME Lean Hog Index for April

15: up $0.21, $103.24.

Live cattle futures slowed their descent, but pressure from feeder cattle still pushed

them into negative territory for the eighth day. Futures washed out early but rebounded

substantially from the lows. This might signal that futures have fallen low enough to

catch the interest of traders to buy back into the market. After all, cash has remained

7strong with no indication of what this week may bring. Boxed beef prices have also

remained strong. Other than the downward attitude that filtrated its way through the live

cattle complex, there wasn't much else to note about Monday's trade. A lack of trader

interest sent the contracts trading lower, and the cash cattle market is yet to be tested as

it's too early in the week for interest to have developed. April live cattle closed $0.50

lower at $120.35, June live cattle closed $0.57 lower at $118.60 and August live cattle

closed $0.50 lower at $118.65. New show lists appear to be higher in Texas, and

Nebraska/Colorado and somewhat lower in Kansas. Monday's slaughter is estimated at

119,000 head, 7,000 head more than a week ago and 32,000 head more than a year ago.

Last week's negotiated cash cattle trade totaled 88,624 head. Of that 55% (48,568 head)

are committed for delivery in the next two weeks while the remaining 45% (40,056

head) are committed for delivery in the following 15 to 30 days. Boxed beef prices

closed higher, with choice up $0.12 ($276.17) and select up $0.03 ($269.13) with a

movement of 91 loads. Cash is called steady to $1.00 higher. Feedlots have their work

cut out for them this week, but higher trade isn't completely out of the question. As

feedlots step back and see corn prices rallying amid rallying boxed beef prices, feedlots

know there is more to be had than that packers are currently paying. The recent spike in

corn prices has really come as a hinderance to the feeder cattle contracts. With cost of

gains on everyone's mind, it's hard to stomach higher corn prices while fat cattle prices

continue to dance around $120.00 live. April feeders closed $1.90 lower at $137.72,

May feeders closed $1.25 lower at $142.47 and August feeders closed $1.77 lower at

$152.77.

When writing a rather large newsletter, I start on the next day’s information

immediately after posting the current day. I say that because I wrote the following

paragraph before yesterday’s sharp gains in hogs (as well as Joe Kerns article below) as

I made an argument for why the current peak in hogs in probably not a long-term top. A

report from the Chinese government that Q1 pork production was up 31.9% from last

year spooked traders last week. Combined with a marketing year low in weekly pork

sales, some traders are deducing this is the beginning of much less Chinese pork

imports. The market is still operating under the negative technical key reversal from

April 12th to boot. Managed money is also the longest they’ve been since Nov 2017.

While I agree that an interim top has been scored, I’m not sold on a major top being in

place because the market seems to be discounting the fact that 75% of total demand is

domestic and we’re likely to see a continued surge in demand as the U.S. economy

reopens with a lot of government stimulus and Covid-inspired savings/low credit card

debt in place. Over 40% of the U.S. population has at least one shot, with 25% fully

vaccinated and about 3% of the population being vaccinated every day now. Throw in

another 10% who’ve already had the disease and the fact that most of the shots given

have heavily weighted to the most vulnerable and it’s no wonder Sunday’s deaths have

8fallen to just 310 people. Regarding China, one week does not make a trend and the last

official month of March saw pork imports up 16.1% from last year. For the quarter,

China imported 1.16mmt or up 22% from last year’s first quarter. There are widespread

reports in the media of Chinese sow losses of 20% in northern/western areas (major

areas are in the south), but official Chinese ASF reports number just six over the last

year and pig prices are down 7.2% this month and 34.2% year to date. China also says

their sow herd grew 28% in 2020. I don’t pay a lot of attention to what China says, but

rather what they do and they’ve been buying global feed grains/soybeans like crazy,

suggesting their livestock herd is growing rapidly. Look for more back and fill action,

with new buying showing up on breaks.

Apparently, noted hog economist Joseph Kerns agrees with my thinking as well, as

noted in a report issued yesterday. Pork producers have enjoyed a wild ride from hog

futures trading in the mid-$70s during the throes of COVID to the recent peak of $110

in the June 2021 contract. This $35 move in futures represents a roughly $2 million

profitability swing for every 1,000 sows of production. Those are big economic impacts

and demonstrate the leveraged nature of pork economics and the role that changes in

the revenue side represents. Given this first wrinkle in an otherwise steadily firming

market, participants have got to be asking the question of whether this is the end of the

ride or just a temporary setback. It is my opinion that it is the latter, a reprieve in a bull

market that will ultimately look like a blip on the radar of a steadily up trending market.

Let’s unbundle this one a bit. First, we are not being overrun by supply. Our sub-2.5

million head per week harvest is not putting pressure on the cash or product market.

Our supply of market-ready animals will steadily move lower (perceived inventory

derived from the recent “Hogs and Pigs” report) from here, with available numbers

ebbing at under 2.4 million head per week by Memorial Day. We are at a time of the

year when the weekly harvest traditionally slows, which normally adds strength to the

cash market. This year is no different, and it may be even a bit more pronounced in the

decline if the number of open finishing barns and demand for wean/feeder pigs is any

indication. At any rate, this is not a bearish set up.

Second, packer interest for our commodity has not waned. Make no mistake – you are in

a commodity business and the nature of the live hog trade means that the tail (the

roughly 2% of the hogs that trade in the negotiated market) tend to wag the dog (the

other 98% of the volume). Cash prices have moved steadily higher throughout this

disruption period as the packing community continues to bid for the available supply.

This is good fundamental news that warrants noting. Third, there is no place to turn in

the event that the supply of the aforementioned supply of hogs comes in short. Cold

storage supplies of pork have been running roughly 25% lower than normal for almost

an entire year. There are limited frozen stocks to pull in the event of an online

9disruption. This lack of buffer stocks will keep the stimulus/response implications of any

uptick in demand in the pork market closely correlated to the hog market. More good

news. Domestic sales in the retail and food service sector have not only rebounded, they

are establishing new highs. Certainly, a portion of this is refilling the depleted pipeline,

but the majority is likely a combination of pent-up demand meeting new stimulus money.

Prior to the issuance of the most recent round of governmental distribution, a poll was

taken in an attempt to discern just how Americans planned on handling their new-found

pennies from heaven. The top category was savings, which seems rather like a rather

noble answer to me. The second category was food. I like that answer, too, as it fits our

interests and correlates with our other observational data that domestic demand for

pork remains robust. Make no mistake – the increase in prices we have experienced

recently are primarily driven by demand. I wrote extensively on this topic last month

and still firmly believe that our demand driven market is both more sustainable and has

stronger underpinnings than a temporary supply disruption. This is all good stuff.

A lot of us hold our breath each Thursday morning at 7:30 a.m. when the export sales

numbers are released. Exports kept us together last year and holding serve year-over-

year would feel like a win. I think we have a decent chance of doing just that. Our major

export destinations have jockeyed around compared to last year, with Mexico picking

up the slack from China and sales to the Philippines making up for weakness to other

Asian destinations. The net change in sales and commitments are not markedly different

than where we sat last year and that is an impressive accomplishment given today’s

substantially higher prices. I think the bottom line on price discovery is that numbers

and statistics need to be understood in context, not just as a headline-grabbing item.

For example, what if I told you that weekly harvest was going to be 50% higher this

year compared to the same week one year ago? That would sound pronounced and on

the edge of inflammatory until you considered the denominator in my example – the

reduced run rates of last year – was the true story line. We are on solid fundamental

ground in both the cash and the cutout market. Aberrations should be considered just

that until the current picture changes.

Weather: There is a trough moving down into the Eastern U.S. with a ridge in the

West. This ridge-west and trough-east pattern will continue through most of this week.

A cutoff low is escaping underneath the ridge in the West and will move across the

southern tier of the country late this week and weekend. Models suggest that the main

trough will retreat northward next week. This will maintain an active, but progressive

pattern for next week. The U.S. and European models are fairly similar. For the outlook

period, temperatures on Sunday will be above normal in the West and near to below

normal elsewhere. Temperatures will rise and fall through the end of the period as the

10pattern goes more progressive. A system will move into the West and then the Central

next week with widespread showers.

North American Weather Highlights: Temperatures below normal will continue through

the northern Plains next week. Though showers have started to move back into the

region, amounts have not been enough to reduce drought. A system next week shows

more potential for moderate showers, but it is a long way out. Scattered showers moved

through the central/southern Plains this weekend, bringing beneficial showers to the

entire region, but also well below normal temperatures. Hard freezes were recorded in

the western half of the Plains, which may have damaged wheat. Risks for hard freezes

continue through most of the week and may get into eastern areas as well, where corn

planting has been more advanced. A system will bring scattered rain and snow showers

through the Midwest early Wednesday, along with fairly chilly low temperatures for the

next several days. Some light frosts occurred in the northern half of the region this

weekend but will be more likely widespread this week behind the front. Hard freezes

may occur for much of the region, doing damage to winter wheat and emerged corn.

Scattered showers moved through the Delta this weekend but were light, allowing soils

to drain and producers to get into the fields. A front that moves through on Tuesday

night could produce frosts for northern areas Wednesday and Thursday, potentially

causing damage to wheat and emerged soybeans. Scattered showers moved through the

Southeast this weekend, but were more pronounced along the Gulf Coast, where more

flooding has been noted. The region will be relatively dry this week, allowing any wet

soils to drain and allow for more planting progress. A front brought scattered snow

showers to the Canadian Prairies region this weekend, being moderate in Alberta but

lighter elsewhere. The entire region continues to be in drought this spring. Another front

will move through Thursday and Friday with more moderate snow showers in Alberta

but less elsewhere. The cold continues through the week but could retreat northward

next week.

Global Weather Highlights: Scattered showers fell this weekend in Brazil as a front

moved slowly northward. This is very timely for safrinha corn, but amounts were

mostly less than one inch. The showers will dry up from south to north by the middle of

this week. Another front moves through this weekend, but showers do not look to be

very widespread or heavy. The end of the wet season appears to be starting for central

Brazil as fronts start to clear the majority of the country's growing regions. This will

overall stress safrinha corn that has been planted very late. Chances for showers may be

better for southern areas as fronts tend to linger a bit longer here. Mostly dry conditions

have been noted recently in Argentina, favorable for corn and soybean harvesting. A

front will move into the country on Wednesday and bring showers into the weekend

before moving northward. Widespread moderate to heavy showers are anticipated for

11most areas, bogging down harvest progress. Scattered showers moved through eastern

areas of Europe this weekend, continuing to produce mostly favorable conditions for

developing winter grains. Colder temperatures remained across the west and north, with

patchy frosts possibly causing some damage. Another cold front later this week could

produce more frosts and freezes for northern and eastern areas through the coming

weekend, as concern for damage continues for vulnerable plants. Across the south,

warmth and periods of showers should maintain favorable conditions for reproductive

winter grains. The cold across the north and east is likely to further delay spring

planting for corn and other crops. Scattered showers moved through the Black Sea

region this weekend and temperatures have been mild, allowing for more wheat to come

out of dormancy, but cool enough to keep growth slow. Soil moisture has been good in

the region due to above-normal winter and spring precipitation, but the region could use

some warmth for more progress. A cold shot may come this weekend into early next

week, mostly for Ukraine. Temperatures are not expected to be damaging right now, but

will need to be watched. Some scattered showers moved through northern New South

Wales and southern Queensland over the weekend, but most areas of Australia remained

dry, benefiting harvest activities for cotton and sorghum. Recent rainfall in the west and

east have filled soils ahead of winter wheat planting, which should be getting underway.

Very little shower activity this week will favor all fieldwork activities. Scattered

showers fell in northeastern China ahead of soybean and corn planting, which should be

starting up in the next couple of weeks. Conditions have been mostly favorable across

the country so far this spring, though it has been overly wet across the south for rice and

sugarcane. Periods of showers this week will maintain mostly favorable conditions.

Periods of showers have continued this spring have kept conditions favorable for much

of the winter crops in northwestern India as they move through reproduction. Scattered

showers have started to develop occasionally over the interior of India well in advance

of summer planting season for cotton and soybeans, which starts with the monsoon in

June.

Macros: The macro markets were mixed as of 8:30am EDT, with Dow futures down

0.5%, the U.S. dollar index is up 0.1%, crude oil is up 0.4% and gold is unchanged. The

S&P 500 on Monday closed 0.53% lower, the DJIA lost 0.36% while the Nasdaq 100

lost 0.96%. Bearish factors included concern that the resurgence of the pandemic will

slow the pace of the economic recovery after new global Covid infections for the week

ended April 19 rose the most for a week since the pandemic began, and higher T-note

yields after the 10-year T-note yield rose 1.9 bp to 1.599%. There are 79 of the S&P 500

companies that report earnings this week. Next week will see the peak with 180 of the

S&P 500 companies reporting. The following week will see reports from 136 of the

S&P 500 companies. Q2 earnings season is off to a good start so far. Of the 44 reporting

SPX companies, 84.1% have beaten the consensus, which is much better than the long-

12term average of 65.3% and the 4-quarter average of 75.5%, according to Refinitiv. SPX

earnings growth is expected to be very strong in Q1 at 30.9% and improve to 56.2% in

Q2, before easing to 20.9% in Q3 and 14.7% in Q4. On a calendar year basis, the

consensus is for strong 27.9% earnings growth in 2021, overcoming the 12.2% decline

seen in 2020. The U.S. stock market on Monday was undercut by weakness in tech

stocks as the Nasdaq 100 index fell 0.96%. The tech sector was dragged lower by a 7%

plunge in Peloton Interactive (PTON) after U.S. regulators on Saturday warned

consumers to stop using Peloton’s Tread+ exercise machine if there are young children

or pets at home due to injuries from the machine. Also, Tesla (TSLA) closed down more

than 3% Monday after a crash Saturday of a Tesla Model S in Texas killed two people,

with conflicting information about whether the auto-pilot was on. Stocks were also

undercut by a small 2 bp rise in the 10- year T-note yield to 1.60%.

The pandemic remains on a slow boil in the U.S. and is getting worse in some areas of

the world. While the outlook is better in the U.S. due to the fast vaccination pace, the

outlook in many other parts of the world is only getting worse. The world economy will

not be able to fully recover until all countries in the world are able to get the pandemic

under control. Globally, new global Covid infections for the week ended April 19 rose

12% to 5.2 million, the most for a week since the pandemic began, according to

reporting by Bloomberg. Globally, cumulative Covid infections have risen above

142.116 million, while cumulative deaths have exceeded 3.035 million. The situation is

currently the worst in India, where the 7-day average of new Covid cases has spiked

higher from only about 10,000 in late March to the current level of about 246,810,

according to Johns Hopkins. That means that nearly a quarter of a million people are

getting the virus every day in India. That is just below the record high of 251,057 posted

in the U.S. in January. There is a new "Indian variant" called B.1.617 that is associated

with higher infection rates and lower antibody resistance. That variant is showing up in

as many as half the samples taken in India, according to Bloomberg. The Indian variant

could be a factor behind the surge.

Other countries that are seeing a sharp upward trend in new Covid infections include

Germany, Poland, Ukraine, Turkey, Iraq, Pakistan, Brazil, Argentina, Colombia, and the

Philippines. The renewed spread of the virus in recent weeks is being attributed to less-

cautious behavior, reduced government restrictions, and the spread of more-

transmissible variants. Most countries do not yet have enough vaccinated people to slow

the new-infection rate. The pandemic in the U.S. is continuing at a high level, but at

least is not getting worse. The 7-day average of new U.S. Covid infections reached a 2-

month high of 71,343 last Tuesday before tailing off to 67,680 by Sunday. The ability of

the U.S. to dampen the pandemic is due in large part to a fast average daily vaccination

rate of 3.13 million doses over the past week, according to Bloomberg's Vaccine

13Tracker. The CDC reports that 25.7% of the U.S. population has been fully vaccinated

and that 39.9% of the population has received at least one dose. The CDC this week will

continue its review of the blood clot data and whether it will allow the Johnson &

Johnson vaccinations to resume. The resumption of the one-shot J&J vaccination would

go a long way to helping more people get vaccinated quickly and dampening the

infection rate.

Major global stock markets were mostly lower Tuesday after Wall Street retreated from

record highs. London and Frankfurt opened lower, while Shanghai and Tokyo also

declined. Hong Kong and Seoul advanced. Wall Street futures gained a day after the

benchmark S&P 500 index lost 0.5% on declines for tech, bank and energy stocks.

Investor optimism has been boosted by higher corporate profits, U.S. hiring and

consumer confidence. Still, traders are uneasy about a rise in inflation and interest rates

and renewed coronavirus infections that prompted some governments to reimpose anti-

disease controls. In early trading, the FTSE 100 in London declined 0.3% to 6,982.77

and the DAX in Frankfurt lost 0.2% to 15,335.68. The CAC 40 in Paris shed 0.6% to

6,256.90. On Wall Street, futures for the S&P 500 and the Dow Jones Industrial

Average were up less than 0.1%. On Monday, the Dow lost 0.4%. Both the S&P 500

and the Dow hit highs on Friday. In Asia, the Shanghai Composite Index lost 0.1% to

3,472.94 while the Nikkei 225 in Tokyo tumbled 2% to 29,100.38. The Hang Seng in

Hong Kong gained 0.1% to 29,135.73. The Kospi in Seoul rose 0.7% to 3,220.70 while

the S&P-ASX 200 in Sydney sank 0.7% to 7,017.80. India's Sensex was up less than

0.1% at 47,978.05. New Zealand, Singapore and Jakarta declined while Bangkok

advanced. In energy markets, benchmark U.S. crude rose 82 cents to $64.25 per barrel

in electronic trading on the New York Mercantile Exchange. Brent crude, used to price

international oils, gained 90 cents to $67.95 per barrel in London. The dollar advanced

to 108.40 yen from Monday's 108.11 yen. The euro gained to $1.2070 from $1.2039.

Summary: July corn finished up $.06 ¾ at a new closing high of $5.80 ½ Monday, near

its highest spot prices in seven years with support from a combination of weather

concerns and strong U.S. demand. Monday's weather map showed snow moving across

the central Midwest, changing to rain as it reaches northern Illinois. Colder temperatures

will expand into the Corn Belt this week and dampen enthusiasm for early planting.

Heavy rain amounts across the southern Gulf states will also likely hinder planting

efforts, while the Eastern Corn Belt expects to receive moderate precipitation amounts.

Otherwise, the forecast remains mostly dry for the northern and Western Corn Belt the

next ten days. Further south, central Brazil received beneficial rain over the weekend,

but the corn crop in southern Brazil remains in need of moisture and only light amounts

are in this week's forecast. In Argentina, the corn harvest will likely be interrupted this

week by heavy rain. Earlier Monday, USDA said 60.0mb of corn were inspected for

14export last week, ahead of the pace needed for the USDA's export estimate. China

accounted for 38% of the week's total. Fundamentally, corn prices and their strong basis

continue to suggest corn supplies are tighter than USDA estimates. From a technical

view, the trends remain up for July and December corn.

July soybeans were up $.14 at a new closing high of $14.36 ½ Monday, supported by a

$4.90 gain in July soybean meal, while July bean oil was down 0.37 cent. Bull

spreading in soybeans suggested domestic demand remains active for U.S. soybeans and

the national cash basis continues to trade at its strongest level in eight years. Earlier

Monday, USDA said 6.8mb of soybeans were inspected for export, a small amount that

is no threat to the bullish export total U.S. soybeans have already amassed. It is already

well understood that export business has shifted to Brazil, where the Wall Street Journal

and the private firm AgRural report 91% of the soybean crop has been harvested. It

remains an impressive sign of demand that July soybeans on China's Dalian exchange

were up 0.4% Monday and appear well supported at the equivalent of $17.51 a bushel,

even while making large purchases from Brazil. With U.S. soybean supplies historically

tight, there is no sign yet of any significant dent in world demand for soybeans. From a

technical view, the trends for July and November soybeans remain up. November

soybeans posted a new high close of $12.84.

July KC wheat ended up $.02 ½ at $6.18 ¾, receiving light bullish influence from corn

and soybeans, but also finding support from concerns of dry weather and a return of

cold temperatures. Snow is falling across Nebraska and western South Dakota Monday

with sub-freezing temperatures expected to reach the Texas Panhandle early Tuesday

morning. Winter wheat crops have seen worse this time of year, but there's always a

chance actual conditions could be harsher than forecast. Temperatures are expected to

turn more moderate by Friday. Meanwhile, the eastern edge of the southwestern Plains

is expecting moderate precipitation this week but crops on the western edge will stay

drier and that also goes for spring wheat in the northwestern Plains and western

Canadian Prairie. September Minneapolis wheat ended unchanged at $6.76 ½. Cold

temperatures remain a slight concern in northern Europe where patchy frosts have been

reported. Crop weather conditions are mostly favorable for winter wheat in Ukraine and

southern Russia, but a massive buildup of Russian troops on Ukraine's border raises

potential for trouble in the region. According to AP and the European Union's Foreign

Policy Chief Josep Borrell, Russia has 150,000 troops near the border, the largest

deployment on Ukraine's border to date. Technically, the trends are sideways for July

KC wheat, up for July Chicago wheat and up for September Minneapolis wheat.

A/C Trading Co. does not accept orders to buy or sell by e-mail, text or any other form of social media. This material has been

prepared by a sales or trading employee or agent of A/C Trading Co. and is, or is in the nature of, a solicitation. By accepting this

communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and

agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME

15JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION

INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO

THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE

PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS

COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is

substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or

indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from

trades and statistical services and other sources that A/C Trading Co. believes are reliable. We do not guarantee that such information is

accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is

subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

16You can also read