Doing Business In Egypt & Opportunities For The Italian Companies - Nasser Hamed - Consulate of Egypt Commercial Office

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Consulate of Egypt

Commercial Office

Milan

Doing Business In Egypt

& Opportunities

For The Italian Companies

Nasser Hamed

Consul for Commercial Affairs

Commercial Office of the Egyptian Consulate in Milan

Milano 4 Feb 2014

Egypt at a Glance

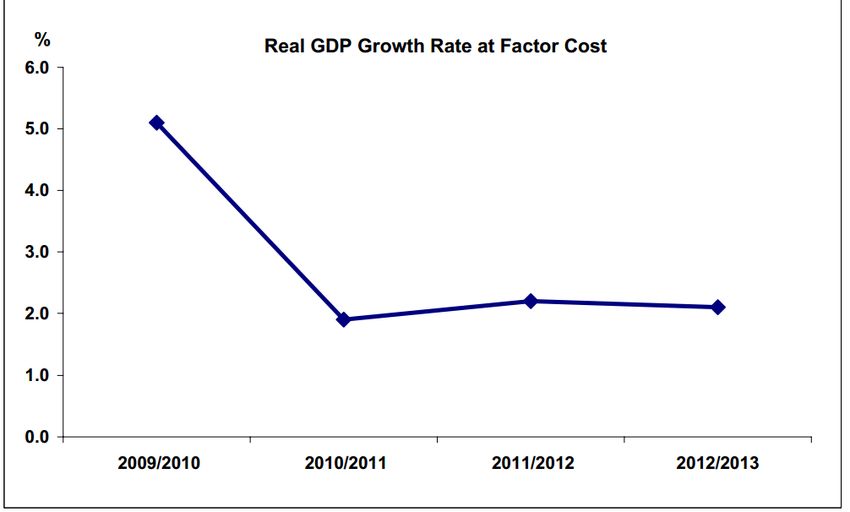

•The annual growth rate of the real GDP for the whole year of 2012/2013

registered 2.1 %, comparing to growth rate of 2.2 % recorded in 2011/2012.

•The budget deficit recorded 13.6% of GDP in FY 2012/2013 comparing to 10.7% in FY

2011/2012.

•In FY 2012/2013, Egypt's transactions with the external world unfolded an overall BOP

surplus of US$ 237.0 million against a deficit of US$ 11.3 billion a year earlier.

•The current account deficit declined in FY 2012/2013 to US$ 31.5 Bn from US$ 34.1 Bn last

year.

•The capital and financial account witnessed a net inflow of US$ 1.5 Bn in FY 2012/2013 from

a net outflow of US$ 0.5 Bn. Last fiscal year

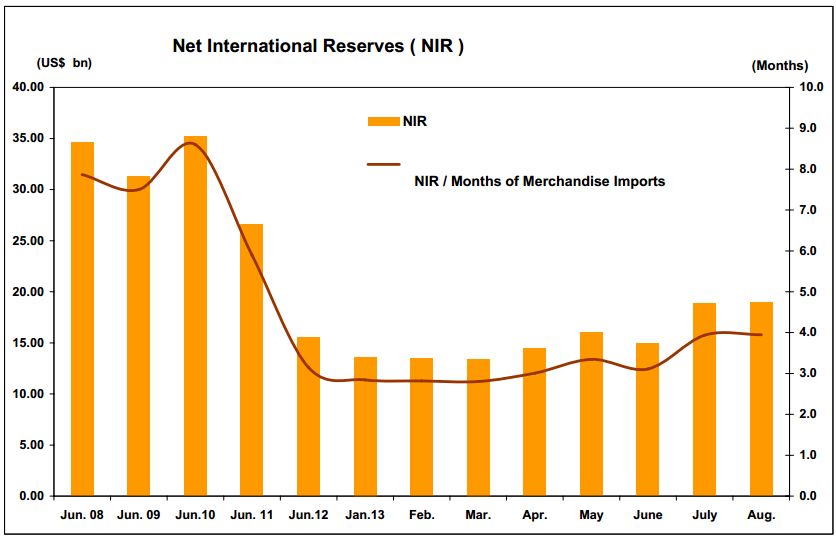

•Net international reserves have increased to US$ 17 Bn by the end of December 2013.

•In November 2013 The credit rating for the Egyptian long and short-run liabilities done by

Standard&Poors was increased from +CCC/C to –B/B with Stable outlook.

•FDI in Egypt recorded a net inflow of US$ 3 Bn. During FY 2012/2013 against US$ 4 Bn.

During FY 2011/2012, However Net FDI recorded US$ 1.2 Bn net inflow in Q1 FY 2013/2014

compared to US$ 108 mn. In Q1 FY 2012/2013.

•Annual Inflation rate has increased to 10.15% in September 2013

year on year basis Comparing to 6.2% in September 2012.

•Unemployment rates: 12.7% during FY 2012/2013.

•Exchange rate for the USD December 2013 : 6.9 EGP.

Source: CBE

GDP Composition by sector

Others

14% Agriculture

14%

Services

4%

Real estate

Oil and Gas

3%

16%

T ourism

3%

Finance

4%

Retail

11%

Industry

15%

CIT

Suez Infrastructure

3%

2% 2%

Construction

5%

T ransportation

4%

Source : Central Bank of Egypt

Macro Overview | 2013-Economic Impact

5.1%

2.2% 2.1%

1.9%

Source : Central Bank of Egypt

•Economic activity remained sluggish in 2012/2013 on the back of weak growth rates in most of

the key sectors namely manufacturing, construction and tourism , in addition to the contraction

in the petroleum sector. In the Meantime Investment levels remained low given the heightened

uncertainty that faced market participants since early 2011 and the weak credit growth to the

private sector.

•Looking ahead, downside risks that surrounded the global recovery on the back of challenges

facing the Euro and softening growth in emerging markets could pose downside risks to domestic

GDP going forward.

Macro Overview | 2013-Economic Impact

Source : Central Bank of Egypt

• Net International Reserves witnessed improvement after 30th of June.

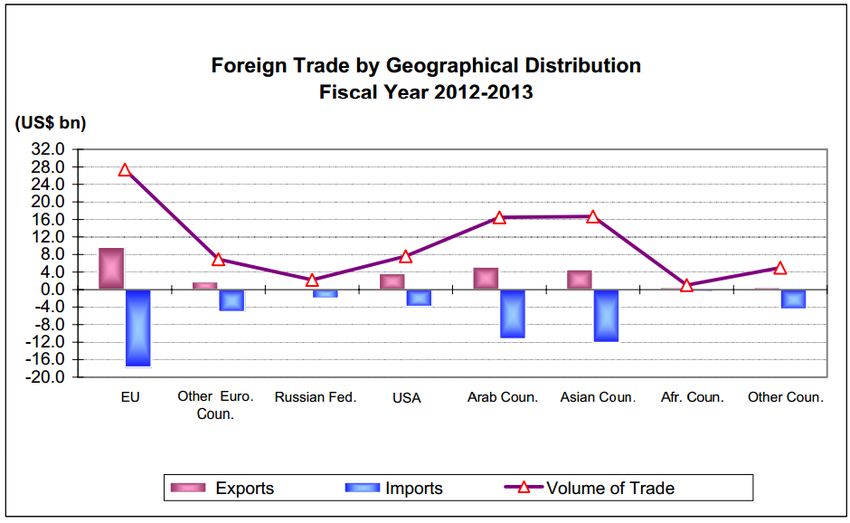

Macro Overview | 2013-Economic Impact Source : Central Bank of Egypt •Egyptian exports were worth $25.9 Bn. during FY 2012/2013 reflecting 3.6% increase in exports Compared to $ 25 Bn in FY 2011/2012. •Egyptian imports were worth $57.5 Bn. In FY 2012/2013 Reflecting 2.9% decline in imports compared to $ 59.2 Bn during FY 2011/2013. •Trade deficit decreased by 7.6% to $31.5 Bn. FY2012/2013 against $34 Bn. FY 2011/2012

Source : Central Bank of Egypt

Macro Overview | 2013-Economic Impact

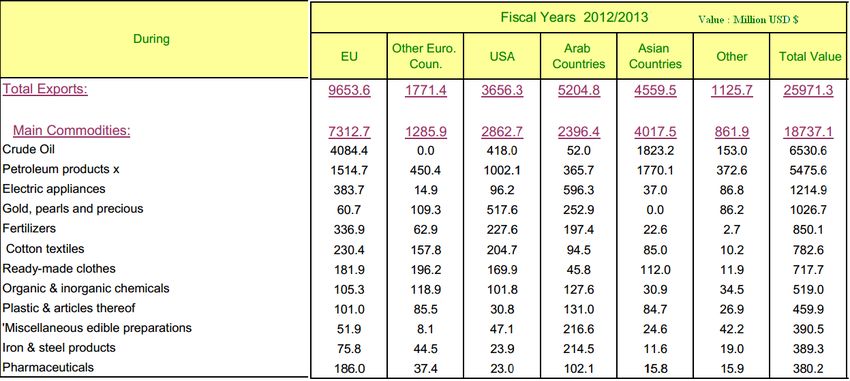

Main Exports by Commodity & Geographical Distribution

Source : Central Bank of Egypt

Macro Overview | 2013-Economic Impact

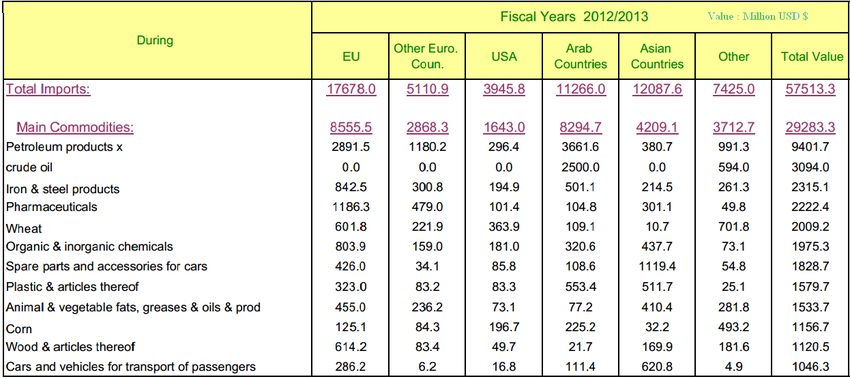

Main Imports by Commodity & Geographical Distribution

Source : Central Bank of EgyptMacro Overview | Longer-Term Outlook

Solid Investor

“New Egypt”

Fundamentals Confidence

Economic

Location Growth and

social justice

Investment

Financial and

Human Capital Monetary

Growth

Balance

Large Market Clear

Governance

Improved Macro

Solid Banking Fundamentals

System Institutional &

Reform Growth PotentialWhy Invest in Egypt ? • A sustained growth rate of 7% over the period between 2005 and 2008. • Despite being affected by the current political unrest the growth rate kept at positive levels during the past three years. • A large population (82.5 Mn in 2012) and hence a large consumer market where per capita income was at EGP 19097 ($ 2760) in 2011/2012. • At around 23.6 million in 2012, Egypt has the largest labor pool in the region with a competitive labor cost.

The Ease of Doing Business in Egypt

• The regulatory and institutional frameworks governing Foreign investment in Egypt have

seen significant overhauls in the past several years. Those reforms and protections based on

the concepts of property rights protections, equality and ease of doing business include:

Fast-track dispute resolution services for all investors.

100% foreign ownership of companies for foreigners.

Profit and dividend repatriation, dispute resolution and settlement mechanisms

implemented.

Comprehensive corporate governance principles which means the rules, processes, or

laws by which businesses are operated, regulated, and controlled. , anti-money

laundering, anti-trust and consumer protection laws.

New commercial court system now rolling out nationwide to settle business disputes.

Incorporation time slashed from an average of several months to only 72 hours.

Source: CBEThe Ease of Doing Business

Removing restrictions on minimum capital of limited liability companies and reducing

incorporation fees.

20% flat tax rate, according to the Tax Law No. 91 of 2005.

Minimum capital requirements for LLC reduced to EGP 200.

One Stop Shop which contains 53 representative offices from different authorities , taking

into consideration that the One-Stop Shops introduced at multiple locations throughout

the country;

Launching the first phase of electronic establishment of companies through the internet (in

Arabic)

Property registration fees reduces where cap is at EGP 2000

Establishing the Egyptian Credit Bureaus (i-score)

Reducing the time necessary to register property from 72 to 63 days.

Introduction of Nilex; The region’s first small cap stock exchangeInvestment Policy Framework

Category Inland Investment Investment Zones Special Economic Zones

• 20% & 40.55% for oil and gas • 20% & 40.55% for oil and gas • 5% flat tax rate on personal

companies companies income tax

Income Tax • 10 years Exemption for • 10 years Exemption for

Agriculture and animal production Agriculture and animal production • 10% tax on all activities within the

activities. activities. zone

• Custom procedures for

• 2-32% depending on the product

production input will be

Import Duties • Flat rate of 5% of the value of administered in the zone None

imported machinery and

• Equipment customs are paid in 5-

equipments

10 years installments

• No duties when exported out of

• Sales taxes are paid in 5-10 Egypt

Export Duties • 5-25% of value of all sale years installments • No duties on domestic

and Sales Tax transactions components when sold in Egypt

• Exported good are tax exempted • 10% of value of non domestic

components when sold in Egypt

• 10-20% depending on salary • 10-20% depending on salary

Payroll Tax • 5% for all salary levels

level level

Export •Depending on zone board’s

None None

Minimum decision

• Protection against expropriation • Companies established within the • Egyptian certificate of origin for

and compulsory pricing investment zones are to enjoy SEZ based exporters

Other

incentives given to both inland • Integrated custom and tax

Incentives • Full right of profit and dividend and upper Egypt investment administration, licensing, and

repatriation regimes. dispute settlement

Source : GAFILow Cost of Doing Business

• Competitive tax rates - corporate and

personal tax rates top out at only 20%

• Developed infrastructure with 15 commercial

ports in addition to 44 specialized ports to

serve importers and exporters, an expanding

airport network catering to both passengers

and cargo.

• An abundance of natural resources and

competitively priced water, power and gas.

Source: CBE, Ministry of InvestmentCompetitiveness

Competitive Access to Large

Lucrative Returns Await Manufacturing Export Domestic

Costs Markets Market

FDI Inflow

Egypt’s competitive

advantages make a compelling

case for increasing FDI in Strategic Government

Location policy

Egypt.

Comparative Wages Comparative Electricity Prices

10

Electricity prices compared to 8

Wages compared to Egypt in US$/ hr 1.6 Egypt (Cents KWatt/ hr)

1.2 7

0.7

4

0.5

Egypt India Tunisia Turkey Egypt Turkey India Tunisia

Source: AmCham, GAFI Information Center,Preferential Trade Agreements with Key

Global Markets

• The EU – Egypt Association Agreement grants Egypt preferential access to the EU market

of 500 million.

• The EFTA-Egypt Free Trade Agreements grants access to the markets of Iceland,

Liechtenstein, Norway and Switzerland in industrial and agricultural products.

• Free duty access to the US market of 300 million customers through the QIZ protocol.

• The COMESA, a common market for Eastern and Southern Africa creates a free trade area

among the 19 member states.

• AGADIR Declaration creates grants Egypt a free trade zone between Egypt, Morocco,

Jordan, and Tunisia in addition to a rules of origin advantage.

• Egypt – Turkey free trade agreement

• GAFTA: ratified by 22 Arab nations, involving the phasing out of customs and duties while

eliminating non-tariff barriers.

• MERCOSUR : access to the markets of Latin-America through a Free Trade agreements

with MERCOSUR countries.

Source: CBEPreferential Trade Agreements with Key

Global Markets

EGYPT‘Egypt 2022’ economic development plan The medium term plan • Macroeconomic stability; real growth rates to reach 3.5% by investing 291 bn. Egyptian Pounds (41 bn USD), 121 billion (17 Bn. USD) Public Investments and 170 billion (24 Bn. USD) Private. • Lunching two stimulus programs to boost the economy each one values EGP 30 Bn ($ 4.3 Bn.) without overloading the budget, in different sectors mainly the infrastructure as follows: • Reducing the budget deficit to 9% of GDP down from 13.6%. • Reducing inflation; with the aim of bringing inflation levels below 7%. • Maintaining a flexible exchange rate set by free market forces, while avoiding short term volatility.

‘Egypt 2022’ economic development plan

The plan includes :

Lunching two stimulus programs to boost the economy each one values EGP 30 Bn ($ 4.3 Bn.)

without overloading the budget, in different sectors mainly the infrastructure as follows:

housing projects(50,000 residential units),

Building 100 School

Continuing connecting 151 village through the sewage network.

building roads and bridges (17 road projects) ,

The completion of the 3rd Metro line,

Upgrading of the electricity power stations,

purchasing 600 buses for public transportation to work with natural gas,

reclaiming 32,600 agriculture acres.

Developing the government’s information technology infrastructure and , qualifying

the workforce and developing Egypt’s internal trade system to curb high prices.Public Private Partnership Projects

Tendered Project

Project Name Abu Rawash Wastewater plant

Tendering

Construction Authority For Water & Waste Water (CAPW)

Authority

Project Increase Plant capacity to fulfill required demand and raise treatment level to

Objectives meet the environmental conditions

Design, financing, raising capacity of plant from 1.2 million m3/day to 1.6

Project million m3/day and construction of an advance secondary treatment stage

Description for the Abu Rawash Wastewater Treatment Plant , and the operation and

maintenance of the whole plant with a capacity of 1.6 million m3/day.

Transaction & financial advisor: Ernyst & Young

Project

Technical advisor: CH2 MHIL

Consultants

Legal advisor: Trowers & Hamlins

Pre-feasibility

Studies European Bank for Reconstruction and Development (EBRD)

financed by:Tendered Project

Project Name Abu Rawash Wastewater plant

Private sector role: Construct, manage, operate & maintain the plant for 20

years (3 years construction + 17 years operation) and handover the plant in

excellent operational condition after contract duration

Project

Public sector role: Provide project land, influent wastewater and pay

Structure

quarterly treatment charge after starting operation phase as well as

presenting government role in monitoring, supervision and applying related

laws and ministerial decrees.

Investment

4.5 Billion EGP

Costs

Currently amending tender document and draft contract based on

changing project scope received by PPPCU from tendering authority in

October 2013.

Time Table

Expected time to finalize documents: Jan 2014

Submission of Bids: April 2014.

Contract award and signature in June 2014Projects to be tendered in Q 1/2014

Project Name Safaga Industrial Port

Tendering The Executive Organization For Industrial & Mining Projects / Ministry

Authority of Industry & Foreign Trade

Establishment of a number of value-added industrial and logistics’

projects the use of surplus of the current berth productivity and the

Project unused yards inside the port which is estimated by 719 000 m2. These

Objectives projects will be selected according to the needs of the direct and outer

hinterland (South Valley governorate), and the economic projects’ need

that will be established in the national project of the Golden triangle.

Development & Upgrade of Safaga mining port that includes a platform

for exporting crude Phosphate to be an Industrial Port through

establishment of 2 industrial zones to establish a number of value-

added industrial projects that will be needed for the port direct and

Project

outer hinterland, with the availability of logistic services (transport,

Description

sorting, storage, quality tests, packing) as follows:

- Liquid bulk terminal.

- Livestock terminal with meat processing facilities.

- Grain storage and milling terminalProjects to be tendered in Q 1/2014

Project Name Safaga Industrial Port

Pre-feasibility

Studies’ HPC Hamburg Port Consulting GmbH

Consultants

Pre-feasibility

Studies Arab Financing Facility for Infrastructure (AFFI)

financed by:

Private sector role: Construct, manage, operate & maintain the and

Project handover the first industrial zone after contract duration

Structure Public sector role: presenting government role in monitoring,

supervision and applying related laws and ministerial decrees.

Investment

100 Million USD

Costs

Pre-feasibility study has been finalized in December 2013

Time Table Tendering Procedures: March 2014 after the approval of PPP

Supreme CommitteeProjects to be tendered in Q 1/2014

Project Name Cairo Contact Centers Park (CCC)

Tendering

The ministry of Communications and Information Technology (MCIT).

Authority

Achieve the integration with the plan of Ministry of Communications and

Information Technology (MCIT) by spreading geographically (East Cairo)

for the deployment of clusters specialized in the manufacture of

communications and information technology after the success story of the

Project Smart Village (west of Greater Cairo) as development of a national project

Objectives aims to the exports development of Egypt for telecommunications services

industry, information technology and outsourcing industry.

Put Egypt on the global map of telecommunications services and

information technology and provides value-added export of approximately

($ 1.2 billion per year) in the field of outsourcing when it is completed.

The investment will start in the second quarter of 2014 through three

stages and ending in 2017. It will include the usufruct of lands with a total

Project

area of 39,000 m2 for the construction of 27 buildings on 3 stages with

Description

total land areas of (1300-1400 m2) per piece to the Egyptians, Arabs and

foreigners investors.Projects to be tendered in Q 1/2014

Project Name Cairo Contact Centers Park (CCC)

Pre-feasibility Financial consultant: Young & Ernest

Studies’ Technical consultant: WSP Middle East

Consultants Legal consultant: Trowers & Hamlins

Pre-feasibility

Studies International Finance Corporation (IFC)

financed by:

Private sector role: Design, Construct, Finance, Operate & maintain

Project Public sector role: : Provide project land and presenting government role

Structure in monitoring, supervision and applying related laws and ministerial

decrees.

Investment

Approximately 100 Million USD for the first stage.

Costs

Pre-feasibility study has been finalized in December 2013

Time Table Tendering Procedures: February 2014 after the approval of PPP

Supreme CommitteeProjects to be tendered in Q 1/2014

Project Name Nile River Bus Ferry

Tendering

General Transportation Authorization in Cairo / Cairo Governorate .

Authority

Develop the transportation service that are offered by Nile River Bus Ferry to

Project

improve the performance of services level and create an advanced level for

Objectives

services, to attract a larger segment of its users >

The Nile River Bus Ferry suffers from a high degree of deterioration where 9

boats only are in operation , and the terminals suffer from a high degree of

deterioration which reduces the numbers of users as a percentage of current

Project population. The required services are as follow :

Description 1.Purchase, finance and operate the River Transport Fleets(30 boats).

2.Develop 16 current terminals and add around 12 new terminals including :

Design, Build, Finance, Operate and Maintain .

3.Suggested project duration 30 years .Projects to be tendered in Q 1/2014

Project Name Nile River Bus Ferry

Pre-feasibility

Studies’ WSP Company (British Co) , and Mena Rail Transport Consultants

Consultants

Pre-feasibility

Studies European Bank for Reconstruction and Development ( EBRD ) .

financed by:

Private sector role: Design, build and operate the Nile River Bus Ferry system

, and maintain the fleet of Nile River Bus Ferry and its terminals through

executing a contract for the provision of services .

Project

Public sector role: Availability the rivers Nile lines, facilities and terminals to

Structure

the investor, and River Transport Authority, Ministry of Irrigation, Cairo

Governorate and the Ministry of Tourism are responsible for issuance of

required licenses.

Investment

Approximately, from 500 to 600 million EGP

Costs

Expected time to finalize Pre-feasibility study in Jan 2014

Time Table

Tendering Procedures: Q1, 2014Projects under study to be tendered

Q3/2014

Project Name Suez Canal Specialized University Hospital

Tendering

Ministry of Higher Education / Suez Canal University

Authority

The Suez Canal University aims to provide and upgrade specialized

clinical and educational services according to the international

standards and medical codes, also to resupply the shortage in the vital

Project Objectives services such as intensive care, neonatal ICU and advanced clinical

services such as neurosurgery and vascular surgery. Suez Canal

University Hospital serves five Governorates in Egypt (Port Said,

Ismailia and Suez and the North Sinai, South Sinai).

The Suez Canal specialized university hospital was built 9 years ago

with the capacity of 230 beds, the University could not operate or

Project Description refurbish or equip or furnish the building due to the lack of financing.

Suez Canal University wishes to tender the hospital building through

the PPP Program.

Pre-feasibility

Studies’ Technical Consultant: Mott MacDonald

ConsultantsProjects under study to be tendered

Q3/2014

Project Name Suez Canal Specialized University Hospital

Pre-feasibility

Studies financed Arab Financing Facility for Infrastructure (AFFI)

by:

Private sector role: Finance, refurbish, Furnish, Equip, maintain and

provide non-clinical services as catering, security, cleaning

maintenance of the building and equipment, and handover the

hospital after contract duration

Public sector role: Responsible for the provision of all clinical,

Project Structure

educational activities related to the Project and its costs. These include

medical consumables, and clinical staff (doctors, nurses, etc.),. The

Private sector will receive periodic Service Availability Payments, as

well as presenting government role in monitoring, supervision and

applying related laws and ministerial decrees.

Investment Costs TBD after finalizing the pre-feasibility studies

Based on change of scope and the number of beds from Suez

Canal University, it is expected to finalize the Pre-feasibility study

Time Table

in March 2014

Tendering Procedures: June 2014Projects under study to be tendered

Q3/2014

Project Name Hurghada Desalination Plant

Tendering Authority National Authority For Potable Water and Sewage

Provide drinking water to meet citizens’ demand in the

Project Objectives

Governorate

Construction of Hurghada desalination Plant with total capacity of

Project Description 40,000 M3/day to provide Hurghada with the necessary Water ,

the plant will be constructed on 2 phases 20,000 m3/day each

Pre-feasibility Waiting for allocation of required lands to start tendering and

Studies’ Consultants contracting the advisor

Pre-feasibility Studies

Agreement With EBRD to Finance the pre-feasibility studies

financed by:Projects under study to be tendered

Q3/2014

Project Name Hurghada Desalination Plant

Private Sector Role : Design , Finance , construct , operate & maintain

the Plant

Project Structure Public Sector Role : Provide the land of the Project and buy the full

production of the plant and presenting government role in

monitoring, supervision and applying related laws and ministerial

decrees.

Investment Costs Will be determined after finalizing the pre-feasibility studies

Estimated to Finalize the pre-feasibility study and begin the

Time Table

tendering procedures is Q3, 2014Projects under study to be tendered

Q3/2014

Project Name Sharm El Sheikh Desalination Plant

Tendering

National Authority For Potable Water and Sewage

Authority

Project

Provide drinking water to meet citizens’ demand in the Governorate

Objectives

Project Construct of Sharm El sheikh Desalination Plant With total capacity of

Description 20,000 m3/ day

Pre-feasibility

Waiting for allocation of required lands to start tendering and contracting

Studies’

the advisor

Consultants

Pre-feasibility

Studies Agreement with EBRD to Finance the pre-feasibility studies

financed by:Projects under study to be tendered

Q3/2014

Project Name Sharm El Sheikh Desalination Plant

Private Sector Role : Design , Finance , construct , operate & maintain the

Project Plant

Structure Public Sector Role : Provide the land of the Project and buy the full

production of the plant and presenting government role in monitoring,

supervision and applying related laws and ministerial decrees.

Investment

Will be determined after finalizing the pre-feasibility studies

Costs

Estimated to Finalize the pre-feasibility study and begin the tendering

Time Table

procedures is Q3, 2014Projects under study to be tendered

Q3/2014

Project Name Heliopolis / New Cairo Metro

Tendering

Cairo Governorate

Authority

Project Helping in Solving the Traffic & Transportation Problems by using an

Objectives Unutilized Methods of transportation

Redevelopment of Heliopolis / New Cairo Metro From Heliopolis To 10th

Project

District –Nasr city , and establish of a new Metro line to connect between

Description

Nasr City and American university in New Cairo City

Pre-feasibility

Technical Consultant : SNC - Lavalin

Studies’

Legal Consultant : Gide Loyrette

Consultants

Pre-feasibility

Studies World Bank

financed by:Projects under study to be tendered

Q3/2014

Project Name Heliopolis / New Cairo Metro

Private Sector Role : Construct , Manage, Operate & Maintain of the

Project

Project

Public Sector Role : Provide the necessary path of the metro line and

Structure

presenting government role in monitoring, supervision and applying

related laws and ministerial decrees.

Investment

Will be determined after finalizing the pre-feasibility studies

Costs

Estimated to Finalize the pre-feasibility study May 2014

Time Table

Expected time to begin the Tendering procedures is Q3, 2014Projects under study to be tendered

Q3/2014

Project Name Rollout & Automation of the Notarization Offices in Egypt Project

Tendering Ministry of Justice - Ministry of Communications and Information

Authority Technology

The main objective is to extend a consistent, efficient and superior

service to the Egyptian public through a fully automated and fully

integrated network of Notary Offices spread across the country. This

Project will be achieved by providing the citizens with better waiting

Objectives conditions, more professional service and an overall better

experience.

Compile and secure a national archive of the notarized transactions

performed throughout the country

Rollout & Automation of the Notarization Offices for 270 offices

around the country through upgrading the current offices and

perform necessary civil works to bring all notary offices.

Take over the current Data Centre, and perform the necessary

Project

maintenance and upgrading that is required to accommodate the load

Description increase expected to render the service throughout the country.

Provide a set of new value added services to the public through

creating online and mobile set of applications that citizens can use

remotely.Projects under study to be tendered

Q3/2014

Project Name Rollout & Automation of the Notarization Offices in Egypt Project

Pre-feasibility

Studies’ Ministry of Communications and Information Technology

Consultants

Pre-feasibility

Studies ________

financed by:

Private Sector Role : Construct , Execute the engineering works &

technology infrastructure, Manage, Operate, Maintain, Training, & follow

Project

up the services level of all the offices for Project duration.

Structure

Public Sector Role: Provide staff from the Ministry of Justice for the

notarization process, as determined by the law

Investment

Approximately 650 Million EGP

Costs

Expected time to finalize Pre-feasibility study in March 2014

Time Table

Tendering Procedures: May 2014Egypt&Italy Trade & Investment

Main Contractual Framework

Agreements: Egypt -Italy

Agreement Date of entry into force

Egypt- EU Association Agreement 2004

Action plan (ministry of Trade & Industry of 2012-2015

Egypt – Ministry of Economic Development of

Italy)

Agreement on cooperation in the maritime field 2008

MOU for Strategic Cooperation 2008

MOU between GAFI and SIMEST 2005

Agreement for the conversion of debt 2001

Protocol to support SMEs 1998

Avoidance of Double taxation Agreement 1994

Agreement to promote and protect the 1982

investments between the two partiesBilateral Trade : Egypt-Italy

(value : million euro )

Jan – Jan

Item/ Year 2009 2010 2011 2012 sep – sep variation

2012 2013

Egyptian Exports 1,422 1,888 2,528 2,296 1,828 1,362 -25.5%

Petroleum Exports 764 1,008 1,319 1,359 1,097 610 -44.4%

Non Petroleum Exports 658 880 1,209 937 731 752 2.9%

Egyptian Imports 2,617 2,936 2,590 2,863 2,033 2,013 -1.0%

Trade Volume 4,039 4,824 5,118 5,159 3,861 3,375 -12.6%

Trade Balance -1,195 -1,048 -62 -567 -205 -651 217.6%

Source:ISTATTop Egyptian Exports to Italy

during the period (2010 – 2012):

(value : million euro )

Products by HS Code chapter 2010 2011 2012 Variation %

27-MINERAL FUELS, MINERAL OILS 1,025.3 1,464.3 1,404.8 -4.06%

76-ALUMINIUM AND ARTICLES THEREOF 169.9 220.3 220.2 -0.07%

52-COTTON 79.3 99.3 88.9 -10.42%

31-FERTILIZERS 69.7 112.5 79.4 -29.40%

7-EDIBLE VEGETABLES AND CERTAIN ROOTS

AND TUBERS 75.9 87.8 67.8 -22.81%

72-IRON AND STEEL 95.4 98.6 34.2 -65.29%

25-SALT; SULPHUR; EARTHS AND STONE;

PLASTERING MATERIALS, LIME AND CEMENT 38.7 38.2 30.5 -20.20%

41-RAW HIDES AND SKINS AND LEATHER 33.0 34.7 25.1 -27.75%

62-ARTICLES OF APPAREL AND CLOTHING

ACCESSORIES 35.1 24.8 22.8 -8.00%

39-PLASTICS AND ARTICLES THEREOF 21.0 28.6 28.6 -0.23%

Source:ISTATTop Egyptian Imports from Italy

during the period (2010 – 2012):

(value : million euro )

Products by HS Code chapter 2010 2011 2012 Variation %

84 - BOILERS, MACHINERY AND MECHANICAL

APPLIANCES 1,208.7 974.3 818.4 -16.00%

27-MINERAL FUELS, MINERAL OILS AND PRODUCTS

OF THEIR DISTILLATION 311.0 419.2 856.6 104.33%

85-ELECTRICAL MACHINERY AND EQUIPMENT AND

PARTS 187.0 192.0 119.1 -37.97%

39-PLASTICS AND ARTICLES THEREOF 94.7 107.8 129.3 19.90%

29-ORGANIC CHEMICALS 125.8 91.3 47.8 -47.67%

73-ARTICLES OF IRON OR STEEL 95.1 86.5 75.5 -12.67%

72-IRON AND STEEL 108.1 63.0 74.5 18.34%

87-VEHICLES OTHER THAN RAILWAY OR TRAMWAY

ROLLING-STOCK 105.9 55.2 54.5 -1.20%

38-MISCELLANEOUS CHEMICAL PRODUCTS 64.4 60.2 76.3 26.66%

32-TANNING OR DYEING EXTRACTS 67.8 49.2 49.2 -0.06%

Source:ISTATItalian Investments in Egypt

•Total Italian Total capital 2.7 Billion US Dollar.

investments in Egypt Italian Participation 1.5 billion US Dollar.

(in 31/7/2013) Total projects 866

Italy rank 11th among foreign investors in Egypt.

•Main investment Finance, No. of companies (6), value: 919.5 Million USD.

sectors / Value of Industry, No. of companies (269), value: 254 Million USD.

Italian Shares Services, No. of companies (274), value: 192.9 Million USD.

Tourism, No. of companies (183), value: 80.1 Million USD.

Construction, No. of companies (93), value: 9.7 Million USD.

•Main investing Intesa Sanpaolo “Bank of Alexandria” – Banking & Finance

companies in Egypt Italcementi – 5 Cement Plants

ENI – Petroleum

Pirelli “Alexandria tires”

Italgen – Renewable energy

Tecnimont – Fertilizers

Techint - Constructions

Domina Group - Tourism

Cottonificio Albini “Mediterranean textiles” – Textiles

Danieli Group – Steel Industries

Edison - PetroleumTHANK YOU

ًشكرا

Consulate of Egypt

Commercial Office

MilanYou can also read