Earnings Season: On the road back - CommSec

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economics | March 1, 2021

Earnings Season: On the road back

Corporate Profit Reporting Season

Each ‘earnings season’ or ‘profit-reporting season’ CommSec tracks all the earnings results of S&P/ASX

200 companies to obtain a comprehensive picture of the aggregate health of Corporate Australia.

In total, 141 companies of the ASX200 index group reported half-year (interim) results for the 2020/21

year. A further 31 companies with a December 31 reporting date have issued full-year or final results. The

other ASX 200 companies have different balance dates.

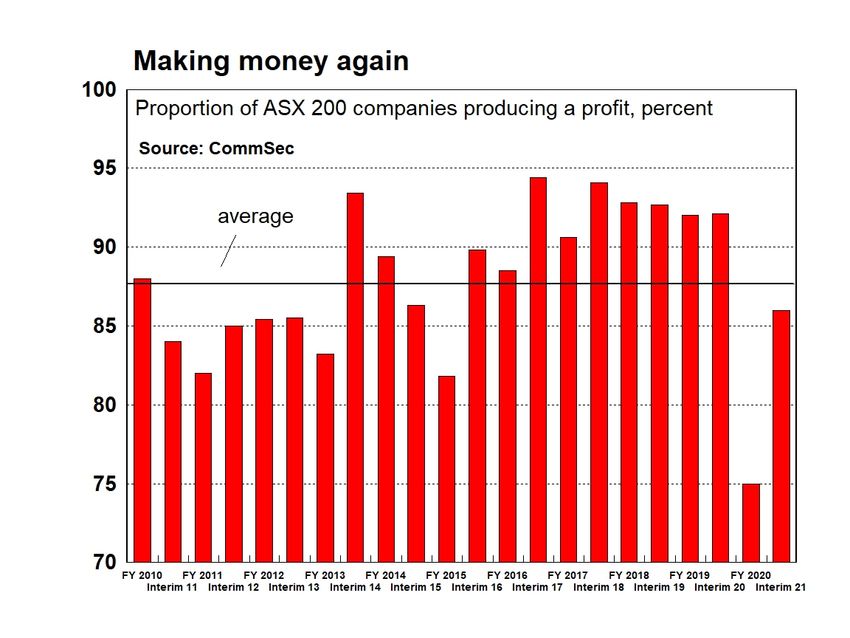

Despite the turbulent times, 86 per cent of companies reported statutory profits for the six months to

December. But aggregate interim earnings fell by 17 per cent.

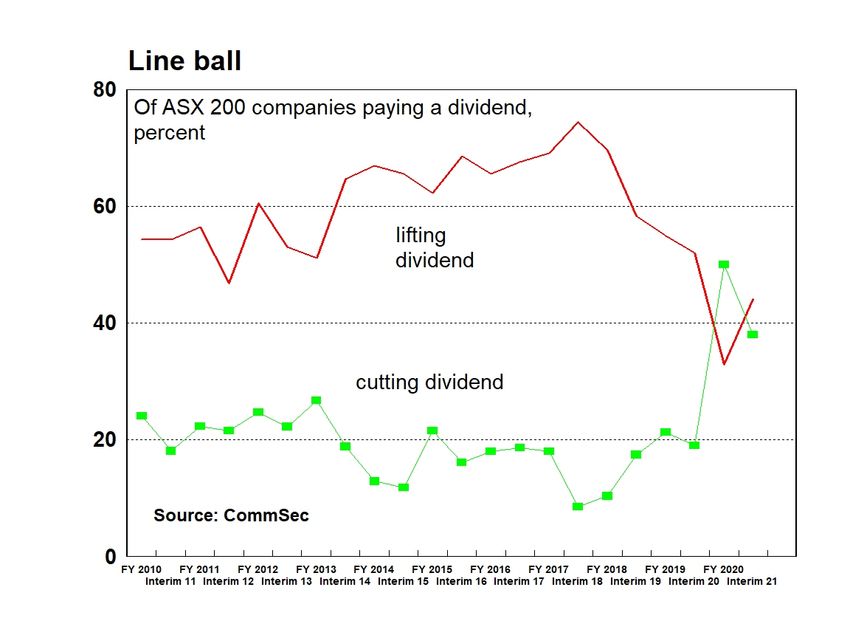

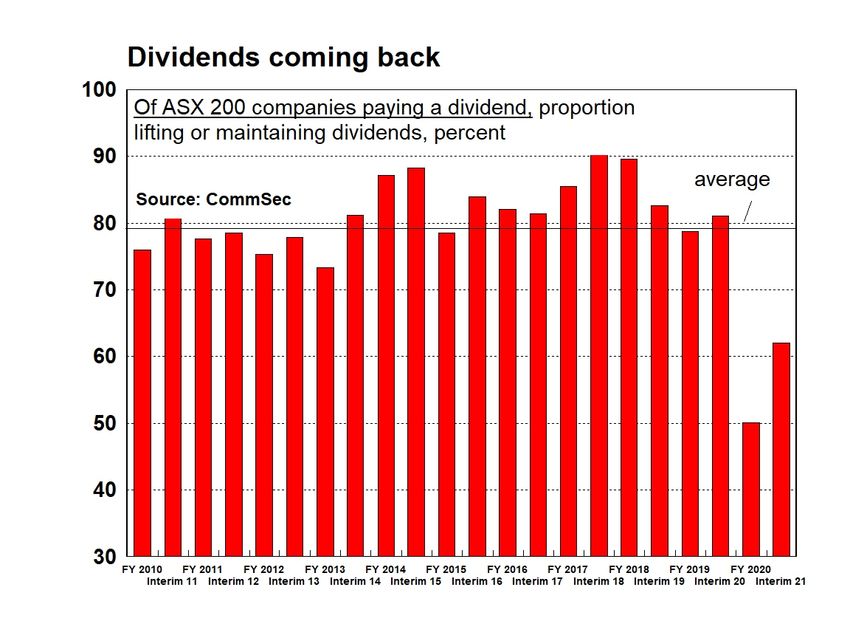

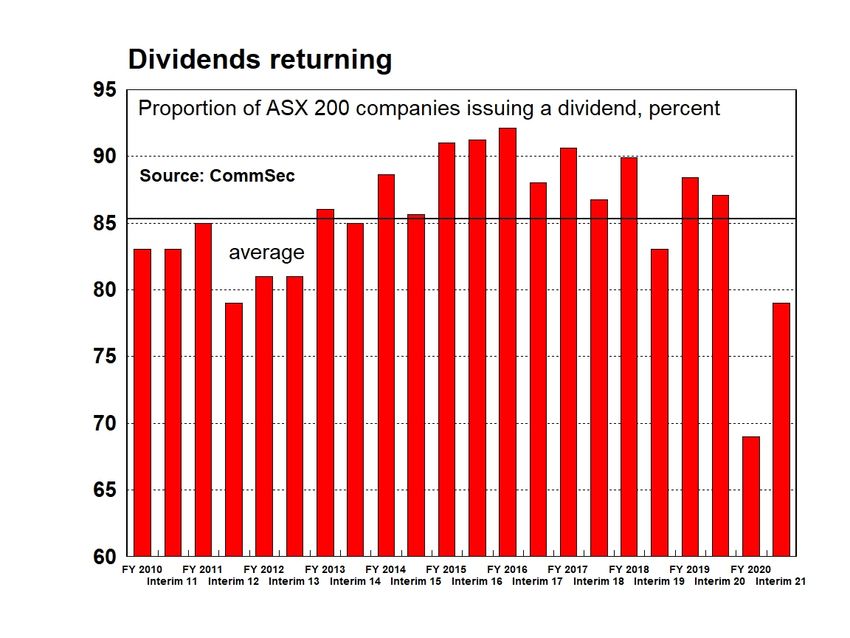

Dividends are returning. Just under 79 per cent of companies issued a dividend (long-term average 86

per cent). Aggregate dividends are actually up by 5 per cent on a year ago.

The big trend has been the lift in cash holdings. Aggregate cash holdings are up by over 50 per cent to

$124 billion. And 70 per cent of companies have lifted cash holdings over the past year. Add in the

companies reporting full year results and cash holdings stand at $166 billion.

The Profit Reporting Season

Every six months CommSec tracks the earnings of Australia’s largest listed companies. Some analysts track

whether companies have met broker expectations. That tells you little about the financial performance of

companies. And unfortunately for many companies only a few brokers ‘cover’ all the stocks.

Other analysts just track the earnings of those companies they ‘cover’ – the companies that they have detailed

information on. CommSec includes all ASX 200 companies in its macro (big picture) assessment of the reporting

season.

For some companies it has been the toughest year in living memory. Notably companies most negatively affected

have been those dependent on people mobility. Especially global mobility – companies dependent on foreign

travel such as airlines and booking companies. Local lockdowns and the closure of foreign borders have buffeted

services like hospitality, accommodation, arts &

recreation and gaming operators as well as

commercial and retail property businesses and

toll road operators.

Energy companies were hit over 2020 by lower -

often government administered - prices and

demand although 2021 is looking to be a better

year.

For others like retailers, conditions have been

arguably the best since the recovery period of

the previous economic ‘emergency’ – the global

financial crisis.

And then there are the miners, supported by

favourable commodity prices and demand,

although experiencing the headwinds of a firmer

Australian dollar. It is worth pointing out those

Aussie dollar headwinds for companies with a

significant foreign presence.

Craig James, Chief Economist; (02) 9118 1806; Twitter: @CommSec

Ryan Felsman, Senior Economist; (02) 9118 1805; Twitter: @CommSec

IMPORTANT INFORMATION AND DISCLAIMER FOR RETAIL CLIENTS

The Economic Insights Series provides general market-related commentary on Australian macroeconomic themes that have been selected for coverage by the

Commonwealth Securities Limited (CommSec) Chief Economist. Economic Insights are not intended to be investment research reports.

This report has been prepared without taking into account your objectives, financial situation or needs. It is not to be construed as a solicitation or an offer to buy or sell any securities or financial instruments, or as a recommendation and/or

investment advice. Before acting on the information in this report, you should consider the appropriateness and suitability of the information, having regard to your own objectives, financial situation and needs and, if necessary, seek

appropriate professional of financial advice.

CommSec believes that the information in this report is correct and any opinions, conclusions or recommendations are reasonably held or made based on information available at the time of its compilation, but no representation or

warranty is made as to the accuracy, reliability or completeness of any statements made in this report. Any opinions, conclusions or recommendations set forth in this report are subject to change without notice and may differ or be

contrary to the opinions, conclusions or recommendations expressed by any other member of the Commonwealth Bank of Australia group of companies.

CommSec is under no obligation to, and does not, update or keep current the information contained in this report. Neither Commonwealth Bank of Australia nor any of its affiliates or subsidiaries accepts liability for loss or damage arising

out of the use of all or any part of this report. All material presented in this report, unless specifically indicated otherwise, is under copyright of CommSec.

This report is approved and distributed in Australia by Commonwealth Securities Limited ABN 60 067 254 399, a wholly owned but not guaranteed subsidiary of Commonwealth Bank of Australia ABN 48 123 123 124. This report is not

directed to, nor intended for distribution to or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary

to law or regulation or that would subject any entity within the Commonwealth Bank group of companies to any registration or licensing requirement within such jurisdiction.

Economic Insights. Earnings Season: On the road back

The Numbers

So to the numbers. And these numbers refer to

those companies reporting half-year earnings to

December 31, 2020.

Profits

Of the 141 companies from the ASX 200 group

that reported for the six months to December

2020, 121 companies or 86 per cent managed to

produce a statutory profit (net profit after tax).

This proportion is well up on the 75 per cent of

companies reporting statutory profits (net profit

after tax) for the year to June.

Over the past decade, on average around 88 per

cent of companies have reported a profit rather

than a loss.

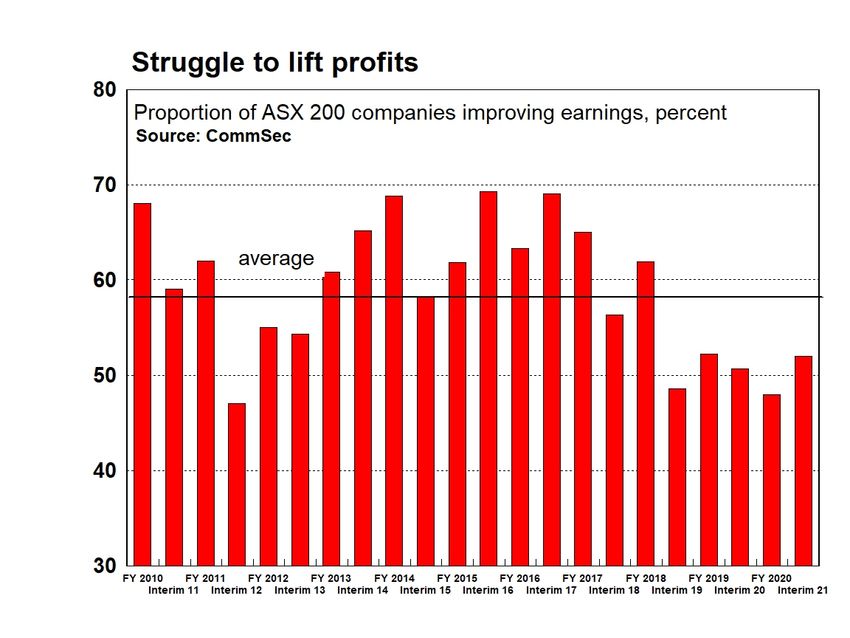

Of the companies to report a profit for the half-

year to December, 60 per cent managed to lift

earnings while 40 per cent recorded a fall in

earnings.

In aggregate (summing all the profit results), earnings are down 17 per cent on a year ago. Revenues fell in total

by just 0.9 per cent, short of the 0.1 per cent aggregate lift in expenses.

Dividends

In the six months to December 2020, 111 companies (79 per cent) elected to pay a dividend. If we go back to the

full year to June 2020, only 68 per cent of companies elected to pay a return to shareholders. The average over

the past 20 reporting seasons stands at 86 per cent. So dividends are returning, but there is still some way to go.

Almost 35 per cent of companies lifted dividends; 14 per cent held dividends steady; 30 per cent of companies cut

dividends; and 21 per cent of companies elected not to pay a dividend.

Of the 30 companies not paying a dividend, 21 similarly elected not to pay a dividend six months ago.

Of the 72 companies paying a dividend, 44 per cent lifted dividends; 18 kept the payout steady; and 38 per cent of

companies cut the dividend.

In aggregate, dividends were up 4 per cent on a year ago.

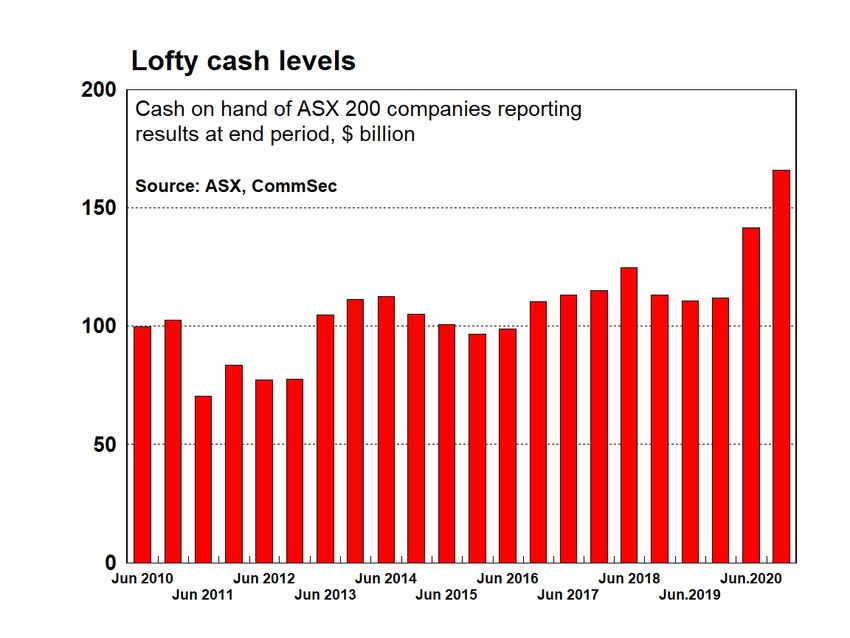

Cash

In the full-year earnings season six months ago, companies elected to trim or not pay a dividend and instead use

the cash to shore up stretched balance sheets.

Companies are paying dividends again, but they remain wary, choosing to hold more cash.

Aggregate cash at hand (cash as at December 31) was up over 50 per cent on a year ago (up from $82 billion to

$124 billion). Add in the companies reporting for the year to December and cash holdings stand at $166 billion.

Overall 70 per cent of companies lifted cash levels from a year ago, notably retailers and banks.

Themes

Usually each quarter there are a number of themes, covering a range of issues. This reporting season – just like

the last – Covid-19 has understandably dominated.

Investors are clearly more sympathetic with any lack of

earnings guidance provided. Investors have seen how

quickly conditions can change. But certainly investors

are interested in the initiatives and strategies that

companies have chosen – and those that are planned.

Six and twelve months ago there was a focus on

strengthening the capital position. But now with those

positions shored up, the question is ‘what’s next?’ and

‘what is the best use of the huge cash stockpiles?’

There is a big focus on supply chains – especially

global supply chains. Not only the response to Covid-

19 but also those companies affected by the trade

restrictions applied by China. Have diversification

efforts begun, and how successful have they been?

March 1, 2021 2

Economic Insights. Earnings Season: On the road back

There are the inevitable questions on staffing

levels, especially companies in receipt of

JobKeeper. Some companies have decided to

repay JobKeeper payments to the Government

but others are torn on the issue – arguing that

they ‘protected’ jobs.

Just like six months ago, solid retail sales have

featured over the reporting period, especially on-

line sales. Some continue to benefit from low or

lower rents. Retailers benefiting most are in

homewares, electrical or those focussed on

delivery. There was a bigger pay-off from

companies that already had invested in the on-

line presence (sales and distribution).

While retailers, supermarkets, gold, mining-more-

generally, and stay-at-home stocks have out-

performed in the COVID environment, energy,

tourism, travel-dependent companies and some

REITS have been buffeted. It’s been an uneven economic downturn and recovery.

Selected observations & notations

Rio Tinto: Iron ore unit costs to rise from US$15.40/tonne to US$17.70 in 2021.

Domino’s Pizza Enterprises: Intends to accelerate expansion.

Ingenia Communities: will repay $1.7 million of $5.1 million JobKeeper payment. Surging revenues from holiday

parks.

Adairs: Returned $6.1 million JobKeeper payment. Lifted gross margins from 61.1 per cent to 66.1 per cent.

Breville: Cut dividend as part of strategy to reduce payout ratio to 40 per cent.

ARB Corp: Won’t repay $9.8 million in JobKeeper.

BHP: Optimistic on global economic recovery and prospects for commodity prices.

SCA Property: It will take two years for earnings to reach pre-Covid levels.

Aurizon: Expansion into ports and trucks to complete supply chain.

Mineral Resources: Record iron ore sales and profits. Sharp lift in dividend.

Cimic: Back in profit but actual and projected profits miss analyst forecasts. Delays in big roads projects.

Dexus: Will continue to expand flexible space offering.

James Hardie: Strong demand for fibre cement for renovations.

Boral: Hurt by slump in apartment projects.

Altium: To use excess cash for acquisitions.

Telstra: Aim for mid-to-high single digit growth in earnings.

Downer: Plan capital return; buyback or special dividend.

Graincorp: Has diversified sales from 30 countries to 50 countries.

GPT: Plans to lift share of industrials from 20 per cent to 30 per cent.

March 1, 2021 3

Economic Insights. Earnings Season: On the road back

Seven West: Sharp focus on operating costs.

CQR: Record leasing deals at higher rents.

Cochlear: Will repay $24.6 million in JobKeeper payments.

Shaver Shop: “is in strongest shape it has ever been in.”

Coles: Expressed concern about absence of population growth to drive sales.

McGrath: First dividend since 2017; raised prospects of acquisitions.

BlueScope Steel: strongest orders in a decade; net profit up 78 per cent.

NIB Health: 16,000 more members; expects final dividend to lift to pre-Covid levels.

oOh!media: Advertising market fell 15 per cent in 2020.

CSL: Challenges ahead with fewer plasma donations.

Wesfarmers: Maintaining a strong balance sheet is prudent.

Fortescue: Up to 10 per cent of capital may be used in clean energy ventures.

Harvey Norman: Latest profit result described as “off the map”.

Beacon Lighting: Higher home prices to lift sales; profit margins doubled over the year.

Abacus Property: Swing to self-storage – strong trading conditions.

Woolworths: Focus on digital sales; absence of foreign students impacting sales.

AP Eagers: Won’t repay $130 million JobKeeper that helped save 2,000 staff.

Adbri: will be aggressive bidder for infrastructure project work.

Market reaction

Some brokers maintain estimates for companies on metrics like profits and dividends. So they determine if the

earnings results were ‘good’ or less positive on whether the companies met, beat or missed their forecasts.

In normal times, companies themselves will provide guidance on future results.

But clearly these aren’t normal times. Companies remain reluctant to provide guidance and are holding larger-

than-normal cash balances.

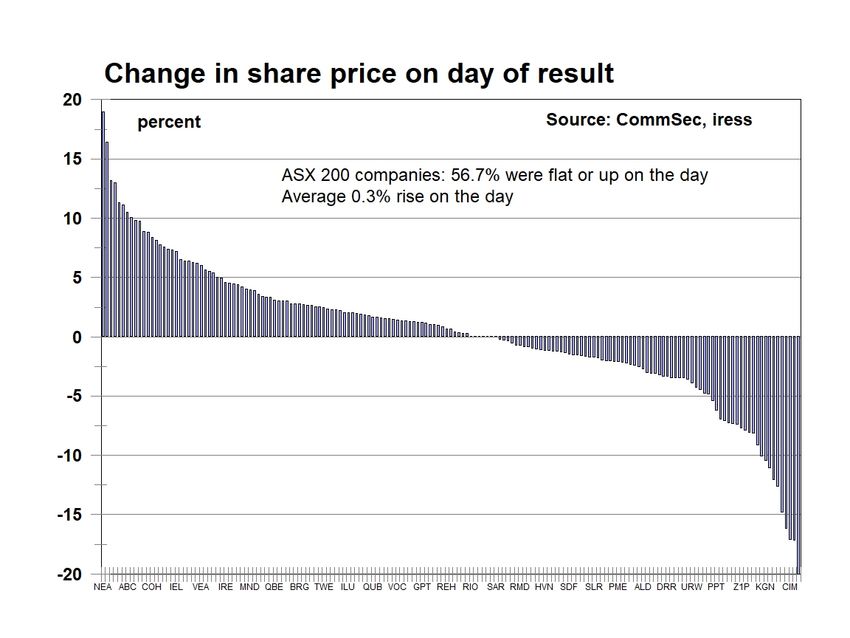

So the best way to determine whether investors are encouraged or discouraged by a company’s profit result is to

examine the sharemarket reaction on the immediate days after the report was delivered.

Overall, almost 57 per cent of ASX 200 companies that reported results saw a lift in their share price on the day of

earnings release with an average gain of 0.3 per cent and a loss of 0.1 per cent after two days.

March 1, 2021 4

Economic Insights. Earnings Season: On the road back

What are the implications for investors?

If one thing is clear in the Covid-19 environment, companies need to be agile. When the crisis hit, the priority was

on shoring up the capital base, especially by equity raisings, as well as some debt. And those companies that

acted quickly and decisively were successful. Then it was a case of having a plan on lockdowns – especially the

situation on staffing and trying to fulfil customer sales and orders.

Certainly the retailers that either had a good online presence to begin with, or were quick to put plans in place,

have been hugely successful.

We now move into a new phase. The economic recovery has been swifter than expected. Vaccines are being

rolled out in Australia as they are across the globe. That may mean that domestic lockdowns become a thing of

the past. Corporate Australia is in solid shape with strong balance sheets being maintained.

So should the extra cash held by companies be used for capital spending, mergers/acquisitions or should it be

returned to investors? As always the answer will vary across companies and sectors. But investors will be

carefully assessing the decisions made. Companies will also need to determine when earnings guidance is

reinstated. Again it will reflect on company management and strategy and the direction that companies are taking.

Of course this is still early days. Mutant strains of the virus could be less responsive to vaccines, putting us back

to square one. And the foreign borders are still closed.

There is still plenty of stimulus and support being applied to the economy. And that won’t be removed too quickly,

especially if the Reserve Bank has any say in the matter. The Reserve Bank is adhering to the view that low cash

rates will be maintained for three years. Some businesses are sceptical, given that input costs are rising and job

shortages are appearing. And the imminent tapering of JobKeeper payments poses a test to the most virus-

affected firms and industries.

Infrastructure spending will be important in driving economic recovery and will support prospects for industrials,

especially engineering and construction materials. The success in keeping the jobless rate down will be important

for consumer-focussed companies, especially retailers.

Spending on infrastructure, super-low interest rates and a home-building boom spurred on by HomeBuilder (and

state-based schemes) will provide the economy with momentum over 2021. Then there is the external factor –

China and other countries driving growth in their economies through infrastructure spending. The Biden

Administration has made infrastructure a priority policy with a focus on renewables. That means more demand for

Australian resources.

The recovery of the Chinese economy remains encouraging for mining and engineering sectors. The iron ore

price is near 9-year highs. Copper is near 9½-year highs. Oil prices are near 13-month highs.

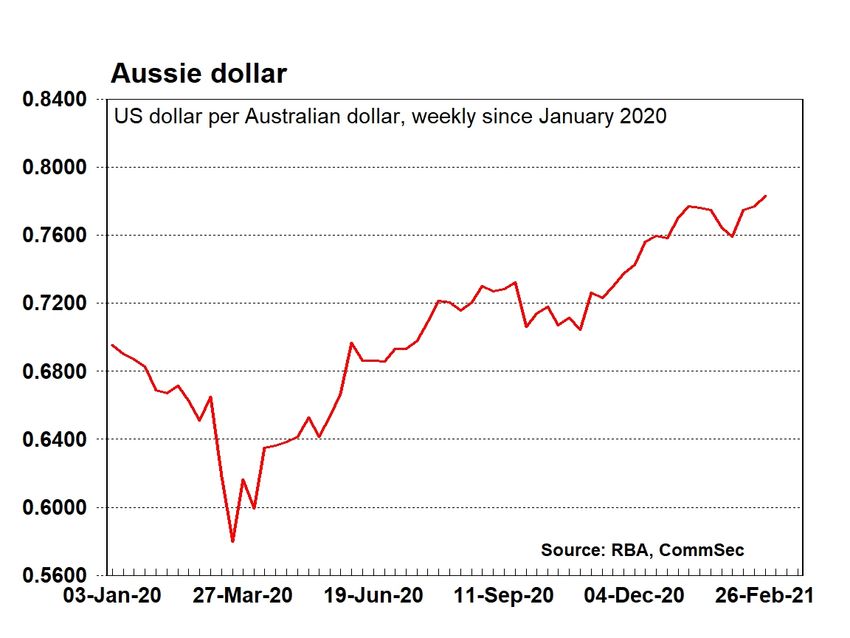

The main challenges for the resource sector are a firmer Australian dollar and the global production delays

caused by shortages of labour, parts and shipping containers. Firms are already reporting skilled labour shortages

in the building industry and border closures present challenges to agricultural harvesters reliant on temporary

overseas workers.

CommSec expects the All Ordinaries to be in a range of 7,200-7,600 by end-2020, with the range for the ASX 200

between 7,000-7,400 points. The hard part is in determining whether equities have become – or are becoming –

too expensive. While less of a challenge with ‘normal’ interest rates, it is harder to resolve the ‘cheap/dear; debate

with near zero rates. The ‘chase for yield’ is supportive of risk assets, but rising real interest rates - as inflationary

expectations mount - present the biggest near term challenge to interest rate sensitive sectors of the sharemarket.

Maintenance of fiscal and monetary stimulus will continue to support prospects for Australian companies. But

governments would like to see a transition from government support to a business-led recovery. Improving

business conditions bode well for hiring intentions and business investment. And the domestic vaccine roll-out will

also be fundamentally important to future prospects as

will be how overseas countries transition out of lockdown.

Issues to watch in coming months include lifting market

interest rates; migration (opening up of the borders);

rising cost or inflationary pressures; difficulty of accessing

stock and labour; the ‘green’ agenda of the new US

President; risk of policy errors will the roll-back of

stimulus; the rising Australian dollar; and the trade

relationship with China.

Craig James, Chief Economist, CommSec;

(02) 9118 1806; Twitter: @CommSec

Ryan Felsman, Senior Economist, CommSec;

(02) 9118 1805; Twitter: @CommSec

March 1, 2021 5

Economic Insights. Earnings Season: On the road back

March 1, 2021 6

Economic Insights. Earnings Season: On the road back

March 1, 2021 7

Economic Insights. Earnings Season: On the road back

March 1, 2021 8

Economic Insights. Earnings Season: On the road back

March 1, 2021 9

You can also read