Economic Outlook With Lower Oil Prices

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

16 February 2015

Economic Outlook With Lower Oil Prices

Michael P. Carey

Chief Economist - USA

+1 212 261 7134

michael.carey@ca-cib.com

https://catalystresearch.ca-cib.com

Crédit Agricole Corporate and Investment Bank is authorised by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and supervised by

the ACPR and the Autorité des Marchés Financiers (AMF) in France and subject to limited regulation by the Financial Conduct Authority and the

Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from us on request.

What led to the oil price decline?

• Softening global demand growth

• Strong US supply growth

• OPEC focus on market share: unlikely to implement production cuts.

Brent Crude Oil Price

(US$ per Barrel

Page 1 16 February 2015 1

Markets gradually rebalance and prices adjust higher

• Modest pick-up in global demand

2014 +0.9 MMBD +1.0 MMBD in 2015-16

• Non-OPEC supply growth, particularly from the US, slows due to lower prices and

industry investment

2014 +2.1 MMBD +0.8MMBD in 2015-16

• EIA forecasts that Brent crude oil prices will average $58/bbl in 2015 and $75/bbl

in 2016.

Page 2 16 February 2015 2

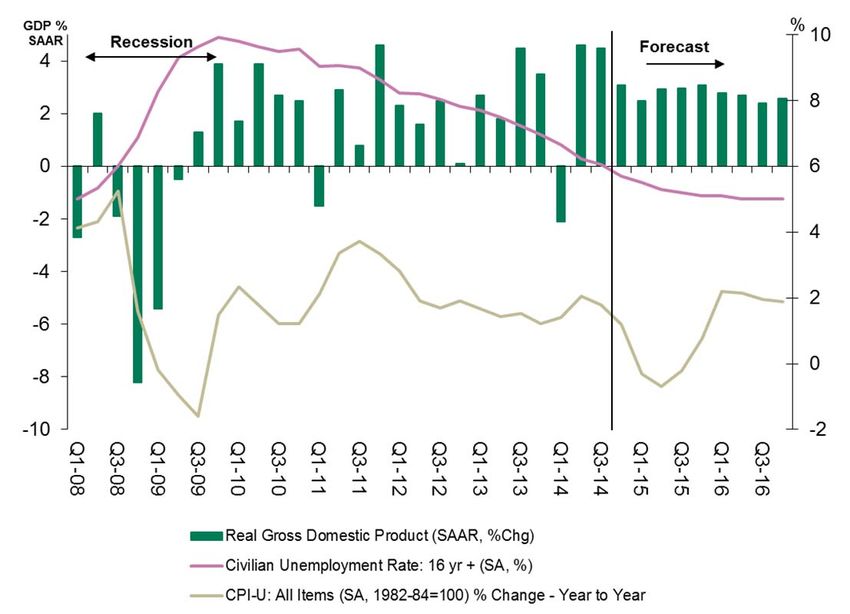

US Macro Summary Situation

Macro Economic

Road to Recovery

Growth in 2015 is expected at an above-trend pace

near 2.8% Q4/Q4. Many of the headwinds to growth, US Macroeconomic Outlook

such as fiscal drag and household deleveraging, have

abated and declines in energy prices will provide a GDP % 10

%10

GDP Recession

4 4 Recession Forecast

Forecast

strong tailwind.

8

8

Lower oil prices act similar to a tax cut, boosting 2 2

consumer spending, but they are expected to also 0 0 6

6

throttle investment in oil and gas extraction industries.

-2-2 4

4

A stronger USD is expected based on relative growth

and interest rate differentials and divergent monetary -4-4 2

2

policies vis-à-vis our trading partners. US net exports will -6-6

be negative for growth this year. -8 0

0

-8

The sharp decline in gasoline prices is expected to

-10 -2

push the top-line CPI into deflation in the spring and -10 -2

Q1-08

Q3-08

Q1-09

Q3-09

Q1-10

Q3-10

Q1-11

Q3-11

Q1-12

Q3-12

Q1-13

Q3-13

Q1-14

Q3-14

Q1-15

Q3-15

Q1-16

Q3-16

Q1-08

Q3-08

Q1-09

Q3-09

Q1-10

Q3-10

Q1-11

Q3-11

Q1-12

Q3-12

Q1-13

Q3-13

Q1-14

Q3-14

Q1-15

Q3-15

Q1-16

Q3-16

early summer of 2015. Core CPI in 2014 rose 1.7% Unemployment

Q4/Q4 and will likely see mild disinflationary pressures

over the near-term before firming later in 2015. Real

RealGross

GrossDomestic

DomesticProduct

Product(SAAR,

(SAAR,%Chg)

%Chg)

Civilian

CivilianUnemployment

UnemploymentRate:

Rate:16

16yryr++(SA,

(SA,%)

%)

The January labor market saw broad-based CPI-U:

CPI-U:All

AllItems

Items(SA,

(SA,1982-84=100)

1982-84=100)% %Change

Change- -Year

YeartotoYear

Year

improvement with greater-than-expected payroll

employment growth (+257K) with an unemployment rate Source: BEA, BLS, Haver analytics, Credit Agricole CIB

of 5.7%. Over 1 million jobs were created in the past

three months. January wage growth rebounded to

2.2% yr/yr.

Page 3 16 February 2015

US Economic Outlook Positives, Negatives

+

Decline in US gasoline prices Near-term disinflation and higher real disposable income

Robust gains in payroll employment

Lack of fiscal drag Possible fiscal stimulus?

Exceptionally accommodative monetary policy (to be gradually removed)

-

Global weakness, US net exports suffer from soft foreign demand and a stronger dollar

Negative impact on US oil and gas extraction sector

Strong dollar: foreign earnings translation effect on equity markets

Hourly earnings growth remains soft, labor market slack remains

Tight access to mortgage credit

Global and regional political pressures: Voter dissatisfaction Increased political

uncertainty increases risks of expedient (but bad) policies and instability.

?

Fed hikes prematurely

Greater access to mortgage credit

External growth falters/ deflation threat/ financial fragility

Tightening tantrum

Page 4 16 February 2015The boost to consumer spending from lower energy prices

The average household is now expected to spend about $750 less on gasoline in 2015

compared to last year because of lower prices.

EIA expects U.S. regular gasoline retail prices, which averaged $3.36/gal in 2014, to average

$2.33/gal in 2015 and rise to $2.72/gal in 2016.

Consumer spending impact will take time to show up in the figures. The cumulative effect could

take 4-6 months to show up in spending patterns. Restaurant spending likely affected before other

retail outlays. Different regional impacts.

Estimates vary, but for the US a $50 per barrel drop in oil prices could boost the level of GDP

by 0.6% to 1% over the next year or two. Caution is advised as estimates are sensitive to

assumptions on how long prices will remain low and whether the price decline reflects a demand or

supply shock.

Bank of Canada sees 1% higher US GDP by 2016. Blanchard and Gali (cited in a December 2014

IMF study) find that “the effect of a permanent (supply driven) decrease in the price of oil by 10%

leads to an increase in U.S. output by about 0.2 percent.” That would point to a 0.7% boost to

output. Such estimates offer some guidance on the magnitude of the impact but

The boost to real disposable incomes also reflects broad disinflationary effects, such as lower

transposition costs for non-energy goods and services

Lower input costs would be a positive for many firms, potentially boosting profits and non-

energy investment.

Gasoline prices are very visible for households and a price decline that is anticipated to last

for some time tends to boost consumer confidence---another support for spending growth.

Page 5 16 February 2015The downside of lower energy prices: Capex

There is a negative impact of lower energy prices from declines in oil & gas exploration

capital spending and related services.

Estimates we find credible suggest producers could cut capital expenditures by 30% in

2015. We estimate the direct impact would trim about 0.2 percentage points from

GDP growth over 2015.

However, higher-cost producers have been successful in wringing additional efficiencies out

of production costs and they will intensify efforts to lower break-even costs.

250000

Capital Expenditures on Oil and Gas Activities

200000

150000

100000

50000

Millions of Chained 2009

Dollars, SAAR

0

80 85 90 95 00 05 10 15

Source: Bureau of Economic Analysis, Haver

Source: Energy Aspects, Bank of Canada Monetary policy report.. Jan 21 2015, P3

Page 6 16 February 2015The downside of lower energy prices: 1986 redux? Oil and gas extraction and support activities employ less than ½ of 1% of total US nonfarm payrolls and last year created roughly 42K jobs, or 1.3 percent of the total 3.1 million jobs created. The employment multiplier in the oil and gas industry is estimated to be around 2.4, as other industries that provide goods and services to oil and gas companies could see layoffs. In 1986, O&G extraction employment fell about 16% by the end of the year. A similar percentage decline might trim 100K people from energy-related payrolls this year- still relatively small in a labor market that has added 267K jobs per month in 2014 and over one million jobs in the past three months alone. In 1986, real GDP slowed to 3.5% from 4.2% in 1985. However, the underlying health of the economy then was different from now given the impact of the S&L crisis in the mid-to late 80s. The Fed eased rates in 86 as inflation decelerated. Page 7 16 February 2015

The impact of lower energy prices for Fed policy We believe the reduction in labor market slack continues to push the FOMC further along the road towards rate normalization. However, the Fed continues to miss its inflation objective. “Inflation has declined further below the Committee's longer-run objective, largely reflecting declines in energy prices.” We believe that the Fed will judge near-term headline deflation as transitory and focus on core inflation when setting policy. Near-term core CPI will likely be damped by some pass-through of lower energy prices; transportation costs (airfares) and some imported goods, such as clothing, would be affected by the strengthening dollar. Nonetheless, we look for core inflation to firm later in 2015 as the economy strengthens but still fall short of the Fed’s 2% target this year. If the data play out the way we expect, the Fed could begin to gradually raise interest rates beginning as soon as the third quarter of this year Page 8 16 February 2015

The impact of lower energy prices for financial markets

Equity markets

In terms of S&P 500 EPS last year, the energy sector contributed about 11%.

The S&P consensus for 2015 EPS is +5.1% yr/yr with energy -48% and ex-energy +11.8%. *

The S&P has rallied on average 10% in the 12 months following big drops in oil prices since

the mid-70s.

Bond Markets

The energy sector accounts for about 15% of the high-yield bond market.

Lower oil prices weaken energy firms’ balance sheets and lead to tighter credit conditions.

Firms switch to cash conservation mode but some firms will not survive.

Risk already priced in? Signs of stabilization?

Attraction of high-yield bonds in a no-yield world?

*Source Evercore ISI publications

Page 9 16 February 2015Global Outlook

Oil Producers Those oil producers with sufficient foreign exchange reserves can wait out

lower oil prices but others are under extreme pressures ( Saudis vs. Venezuela)

Russia: Severe Recession

● Real GDP set to drop 5% in 2015

with inflation seen rising to 12%.

● Growth and capital flow picture

remain quite negative for 2015.

Econ minister projects $115 billion

capital outflows.

● Rate cut to ease recession. RUB

weakens further.

Page 10 16 February 2015 10Global Outlook

Eurozone macro outlook – weak, not desperate

GDP Growth 1.0%-1.5% in 2015; 1.5%-2.0% 2016

Domestic demand resilient, benefits from lower energy prices (but less of an impact

than in the US)

Fiscal austerity lessened and credit conditions to improve further

Headline deflation likely troughs at around -0.6% in Q1, core inflation running +0.6% y/y

Greece manageable on a reasonable compromise, but political contagion risks remain

ECB QE keeps downward pressure on EUR. EUD/USD forecast at 1.05 at yearend.

Emerging Markets: Big energy importers and/or oil-intensive economies should

benefit from lower oil prices.

Asian EMs better positioned given stronger balance of payment positions compared

with fragile-5 (Turkey, South Africa, India, Indonesia and Brazil). The deceleration of

China’s economic growth is a compounding negative factor for EMs

Page 11 16 February 2015 11Key Conclusions The US will likely be a significant beneficiary of lower energy prices. The impact on the US energy sector and certain regions will be negative but that is overwhelmed by positive real income gains nationally. Fed policy is expected to focus on core inflation and sees the oil price impact as transitory. Financial market impact of weakened energy sector expected to be limited. Many oil importers face other factors that are likely to limit the positive growth impact from the windfall income gains from lower oil prices this year. Oil exporting countries face a range of negative outlooks. Page 12 16 February 2015 12

Certification

The views expressed in this report accurately reflect the personal views of the undersigned analyst(s). In addition, the undersigned analyst(s) has not and will not receive any compensation for

providing a specific recommendation or view in this report.

MICHAEL CAREY

** employee(s) of Crédit Agricole Securities

(USA), Inc.

Jean-François Paren Head of Global Markets Research +33 1 41 89 33 95

Asia (Hong Kong & Tokyo) Europe (London & Paris) Americas (New York) Important: Please note that in the United States, this

TBC Sébastien Barbé David Keeble ** fixed income research report is considered to be fixed

Head of Global Markets Research for Europe and Head of Global Markets Research for the income commentary and not fixed income research.

Head of EM Research and Strategy Americas and Notwithstanding this, the Crédit Agricole CIB

+33 1 41 89 15 97 Global Head of Interest Rates Strategy Research Disclaimer that can be found at the end of

+1 212 261 3274 this report applies to this report in the United States

Macro Strategy Kazuhiko Ogata Frederik Ducrozet Michael P. Carey ** as if references to research report were to fixed

Chief Economist – Japan Senior Economist – Eurozone Chief Economist – North America income commentary. Products and services are

+81 3 4580 5360 +33 1 41 89 98 95 +1 212 261 7134 provided in the United States through Crédit Agricole

Brittany Baumann ** Securities (USA), Inc.

US Associate

+1 212 261 7140 ‡ This commentary has been produced by Credit

Interest Rates Yoshiro Sato Romain Blanchet David Keeble ** Agricole Securities (USA) Inc.’s (“CAS-USA”) Fixed

(Head: Economist – Japan IRD Strategist Global Head of Interest Rates Strategy Income FX Department and is not a fixed income

David Keeble) +81 3 4580 5337 +33 1 41 89 00 64 +1 212 261 3274 research report prepared by a research analyst.

Orlando Green Jonathan Rick ** These views may differ from those of the Research

Senior Interest Rates Strategist IRD Strategist Department.

+44 20 7214 7467 +1 212 261 4096 The material contained in this commentary is

Jean-François Perrin intended solely for accredited, expert institutional

Inflation Strategist investors and is provided for informational purpose

+33 1 41 89 94 22 only. This commentary is based on data obtained

from sources we believe to be reliable, but is not

Emerging Markets Dariusz Kowalczyk Sébastien Barbé Mark McCormick ** ‡

guaranteed as to accuracy and does not purport to

(Head: Senior Economist/Strategist – Asia ex-Japan Head of EM Research and Strategy FX Strategist

be complete. Any comments regarding the future

Sébastien Barbé) +852 2826 1519 +33 1 41 89 15 97 +1 212 261 4108

direction of financial markets is illustrative and is not

Jakub Borowski

intended to predict actual results. It should not be

Chief Economist - Crédit Agricole Bank Polska SA

+ 48 22 573 18 40

construed as advice designed to meet the particular

Alexander Pecherytsyn

investment needs of any investor, nor as an offer or

Chief Economist – Crédit Agricole Bank Ukraine solicitation to buy or sell the securities or other

+ 38 44 493-9014 products mentioned herein. Changes to assumptions

Guillaume Tresca may have a material impact on any returns detailed.

Senior Emerging Market Strategist Price and availability are subject to change without

+33 1 41 89 18 47 notice. No representation is made that any

Foreign Exchange TBC Adam Myers Mark McCormick ** ‡ transaction can be effected at the values provided.

European Head of FX Strategy FX Strategist The values provided are not necessarily the values

+44 20 7214 7468 +1 212 261 4108 carried on CAS-USA’s books.

Manuel Oliveri

FX Strategist

+44 20 7214 7469

Page 13 16 February 2015Disclaimer © 2015, CRÉDIT AGRICOLE CORPORATE AND INVESTMENT BANK All rights reserved. This research report or summary has been prepared by Crédit Agricole Corporate and Investment Bank or one of its affiliates (collectively “Crédit Agricole CIB”) from information believed to be reliable. Such information has not been independently verified and no guarantee, representation or warranty, express or implied, is made as to its accuracy, completeness or correctness. This report is a “commercial communication” as defined in article 6 of the Directive 2000/31/CE of 8 June 2000. For the avoidance of doubt, it is not a “communication à caractère promotionnel” within the meaning of the Règlement General AMF. It is provided for information purposes only. Nothing in this report should be considered to constitute investment, legal, accounting or taxation advice and you are advised to contact independent advisors in order to evaluate this report. It is not intended, and should not be considered, as an offer, invitation, solicitation or personal recommendation to buy, subscribe for or sell any of the financial instruments described herein, nor is it intended to form the basis for any credit, advice, personal recommendation or other evaluation with respect to such financial instruments and is intended for use only by those professional investors to whom it is made available by Crédit Agricole CIB. Crédit Agricole CIB does not act in a fiduciary capacity to you in respect of this report. Crédit Agricole CIB may at any time stop producing or updating this report. Not all strategies are appropriate at all times. Past performance is not necessarily a guide to future performance. The price, value of and income from any of the financial instruments mentioned in this report can fall as well as rise and you may make losses if you invest in them. Independent advice should be sought. In any case, investors are invited to make their own independent decision as to whether a financial instrument or whether investment in the financial instruments described herein is proper, suitable or appropriate based on their own judgement and upon the advice of any relevant advisors they have consulted. Crédit Agricole CIB has not taken any steps to ensure that any financial instruments referred to in this report are suitable for any investor. Crédit Agricole CIB will not treat recipients of this report as its customers by virtue of their receiving this report. Crédit Agricole CIB, its directors, officers and employees may effect transactions (whether long or short) in the financial instruments described herein for their own accounts or for the account of others, may have positions relating to other financial instruments of the issuer thereof, or any of its affiliates, or may perform or seek to perform securities, investment banking or other services for such issuer or its affiliates. Crédit Agricole CIB may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Crédit Agricole CIB is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Crédit Agricole CIB has established a “Policy for Managing Conflicts of Interest in relation to Investment Research” which is available upon request. A summary of this Policy is published on the Crédit Agricole CIB website: http://www.ca-cib.com/group-overview/financial-information.htm. This Policy applies to its investment research activity. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party without the prior express written permission of Crédit Agricole CIB. To the extent permitted by applicable securities laws and regulations, Crédit Agricole CIB accepts no liability whatsoever for any direct or consequential loss arising from the use of this document or its contents. France: Crédit Agricole Corporate and Investment Bank is authorised by the Autorité de Contrôle Prudentiel et de Résolution (“ACPR”) and supervised by the ACPR and the Autorité des Marchés Financiers (“AMF”). United Kingdom: Approved and/or distributed by Crédit Agricole Corporate and Investment Bank, London branch. Crédit Agricole Corporate and Investment Bank is authorised by the ACPR and supervised by the ACPR and the AMF in France and subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from us on request. United States of America: This research report is distributed solely to persons who qualify as “Major U.S. Institutional Investors” as defined in Rule 15a-6 under the Securities and Exchange Act of 1934 and who deal with Crédit Agricole Corporate and Investment Bank. Recipients of this research in the United States wishing to effect a transaction in any security mentioned herein should do so by contacting Crédit Agricole Securities (USA), Inc. (a broker-dealer registered with the Securities and Exchange Commission). The delivery of this research report to any person in the United States shall not be deemed a recommendation of Crédit Agricole Securities (USA), Inc. to effect any transactions in the securities discussed herein or an endorsement of any opinion expressed herein. Italy: This research report can only be distributed to, and circulated among, professional investors (operatori qualificati), as defined by the relevant Italian securities legislation. Spain: Distributed by Crédit Agricole Corporate and Investment Bank, Madrid branch and may only be distributed to institutional investors (as defined in article 7.1 of Royal Decree 291/1992 on Issues and Public Offers of Securities) and cannot be distributed to other investors that do not fall within the category of institutional investors. Hong Kong: Distributed by Crédit Agricole Corporate and Investment Bank, Hong Kong branch. This research report can only be distributed to professional investors within the meaning of the Securities and Futures Ordinance (Cap.571) and any rule made there under. Japan: Distributed by Crédit Agricole Securities Asia B.V. which is registered for securities business in Japan pursuant to the Law Concerning Foreign Securities Firms (Law n°5 of 1971, as amended), and is not intended, and should not be considered, as an offer, invitation, solicitation or recommendation to buy or sell any of the financial instruments described herein. This report is not intended, and should not be considered, as advice on investments in securities which is subject to the Securities Investment Advisory Business Law (Law n°74 of 1986, as amended). Luxembourg: Distributed by Crédit Agricole Corporate and Investment Bank, Luxembourg branch. It is only intended for circulation and/or distribution to institutional investors and investments mentioned in this report will not be available to the public but only to institutional investors. Singapore: Distributed by Crédit Agricole Corporate and Investment Bank, Singapore branch. It is not intended for distribution to any persons other than accredited investors, as defined in the Securities and Futures Act (Chapter 289 of Singapore), and persons whose business involves the acquisition or disposal of, or the holding of capital markets products (as defined in the Securities and Futures Act (Chapter 289 of Singapore)). Switzerland: Distributed by Crédit Agricole (Suisse) S.A. This report is not subject to the SBA Directive of January 24, 2003 as they are produced by a non-Swiss entity. Germany: Distributed by Crédit Agricole Corporate and Investment Bank, Frankfurt branch and may only be distributed to institutional investors. Australia: Distributed to wholesale investors only. This research, and any access to it, is intended only for “wholesale clients” within the meaning of the Australian Corporations Act. THE DISTRIBUTION OF THIS DOCUMENT IN OTHER JURISDICTIONS MAY BE RESTRICTED BY LAW, AND PERSONS INTO WHOSE POSSESSION THIS DOCUMENT COMES SHOULD INFORM THEMSELVES ABOUT, AND OBSERVE, ANY SUCH RESTRICTIONS. BY ACCEPTING THIS REPORT YOU AGREE TO BE BOUND BY THE FOREGOING. 23/01/15 Page 14 16 February 2015

You can also read