Economy and Property Update - South Region Committee Dr Ronnie O'Toole, Department of Finance - Institute of Banking

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

South Region Committee

Economy and Property Update

• Dr Ronnie O’Toole, Department of Finance

• Peter O’Flynn, DTZ Sherry FitzGerald Cork

23 April 2015

Dr Ronnie O’Toole

Programme Manager, National Payments Plan

Department of Finance

2

The Institute of Banking Economy Update Dr. Ronnie O’Toole 23rd April 2015 Department of Finance Rochestown Park 3 | ECONOMIC AND FISCAL OUTLOOK 2015 23rd April 2015

4 | ECONOMIC AND FISCAL OUTLOOK 2015 29 January 2015

Trading partner performance is improving

Key Points

US – benefitting from a

tighter labour market

and lower energy prices

despite stronger dollar

UK – solid recovery

driven by domestic

demand and lower oil

prices

Euro area – supported

by lower oil prices,

quantitative easing and

euro depreciation

Euro area, US and UK

combined represent

about two-thirds of Irish

exports

5 | ECONOMIC DEVELOPMENTS 2015

Currency effect is positive

Key Points

Euro has declined

considerably over the last year

against USD and sterling

This is the first-round impact of

ECB’s quantitative easing

programme

Ireland’s nominal effective

exchange rate has fallen

considerably, boosting

competitiveness

Will boost exports as Ireland

trades disproportionately with

the UK and US

6 | ECONOMIC DEVELOPMENTS 2015

Falling oil prices weighing on inflation

Key Points

3.5

Headline inflation 3.0

averaging -0.4 v core 2.5

inflation +1.0 in YTD 2.0

Significant fall in oil 1.5

prices contributed to this 1.0

fall 0.5

0.0

Depreciation of euro -0.5

against sterling should -1.0

lead to modest increases -1.5

in prices -2.0

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2015

Service prices continue

to increase and boosted unprocessed food

services

processed food

HICP

NEIG

Core HICP

energy

by water charges in

January

7

Export growth has rebounded

Key Points

Export growth of 14 per

cent recorded in Q4 –

split evenly between

goods and services

Services exports are

rising rapidly – mainly

ICT services. Strong

FDI pipeline

Goods exports have

bounced back from the

pharma ‘patent cliff’

effect of 2012-13

8 | ECONOMIC DEVELOPMENTS 2015

Domestic economy performing strongly too

Key Points

Retail sales grew by

over 6% in 2014

Car sales very strong,

but ‘core’ sales still up

3.7% last year

Tax impact is visible –

VAT rose by just under

9% in 2014

This has pushed

though to 2015. Growth

of 8% recorded in

February

9 | ECONOMIC DEVELOPMENTS 2015

Unemployment now below euro area average

Key Points

Irish employment

increased by 1.7% in

2014

Unemployment rate at

10% in March, below

euro area average since

last summer

Employment growth is

broad-based across

sectors

10 | ECONOMIC DEVELOPMENTS 2015Fiscal performance strong in 2014

Key Points

Full-year 2014 tax

performance

impressive

Tax revenue rose by

just over 9 per cent in

2014

Performance above

target across a range of

categories: labour

taxation, corporation

tax, consumption tax

Performance into 2015

is very strong. Up 13%

y-o-y in Q1

11 | PUBLIC FINANCES 2015Yields on Irish debt continue to fall

Key Points

Irish yields have

continued to fall right

into 2015

10-year yield is down

well below 1% from a

peak of 14% in July

2011

Investor sentiment

remains positive with

new record lending

rates in recent weeks

No sign of contagion

effect from Greece

12 | PUBLIC FINANCES 2015Irish Economy - Highlights

Key Points

Growth of 4.8% recorded in 2014. This makes Ireland the fastest-

growing economy in the EU last year

Consensus expectations of 4% GDP growth this year

Exports are at an all-time high, driven by both goods and services

Recovery in traded sector driven by:

Competitiveness: unit labour costs converged 20% vis-à-vis euro area since 2008. Wage

moderation has accompanied productivity improvements

Continued inflows of FDI, particularly in ICT sector

Educated workforce and openness to inward migration of skilled workers

Unemployment remains unacceptably high at 10% but has fallen from

15% in just three years. Momentum is positive

Last few years of growth driven by the export sector

Domestic economy now recovering, set to drive GDP in near term

Cost of government borrowing at an all-time low

13 | ECONOMIC DEVELOPMENTS 201514 | ECONOMIC AND FISCAL OUTLOOK 2015 29 January 2015

Department of Finance

Government Buildings

Upper Merrion Street

Dublin 2

Ireland

www.finance.gov.ie

@IRLDeptFinance

This presentation is for informational purposes only.

No person should place reliance on the accuracy of the data and should not act solely on the basis of the presentation itself.

The Department of Finance does not guarantee the accuracy or completeness of information which is contained in this document and which is

stated to have been obtained from or is based upon trade and statistical services or other third party sources. Any data on past performance

contained herein is no indication as to future performance.

No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any modelling, scenario

analysis or back-testing.

All opinions and estimates are given as of the date hereof and are subject to change.

The information in this document is not intended to predict actual results and no assurances are given with respect thereto.Peter O’Flynn

Director

DTZ Sherry FitzGerald Cork

16Outlook 2015 How will Ireland's residential and commercial property markets perform this year … and beyond? 23 April 2015

Economy, An Overview % Change 2011 2012 2013 2014 2015 f 2016 f 2017 f 2018 f Real GNP -1.6% 1.8% 3.3% 4.1% 3.6% 3.1% 3.1% 3.1% Real GDP 2.2% 0.2% 0.2% 4.7% 3.9% 3.4% 3.4% 3.4% Exports 5.4% 1.6% 1.1% 8.3% 4.8% 4.3% 4.3% 4.7% Investment -2.9% 5.0% -2.4% 14.6% 12.7% 7.6% 7.5% 5.1% Consumption -1.6% -0.3% -0.8% 1.7% 2.7% 1.4% 1.3% 1.3% Unemploymen 14.6% 14.7% 13.1% 11.4% 10.2% 9.4% 8.9% 8.1% t Rate Source: Department of Finance GDP forecast to grow by 4.7% in 2014 1

Quantitative Easing

Stimulus package of €1.1trillion by September 2016 to purchase Government

Bonds and asset-backed securities

Economic impact

• Devalue the Euro

• Fall in Interest Rates

• Increased Credit

• Inflationary

Property Impact

• Reduce bond yields

• Boosting European Property Appeal,

yield compression

• Beyond 2016, European property

attractiveness will begin to diminish

• Increase in yields in Euro area in

general

QE – Stimulus

2Central Bank

Loan to Value (LTV) for principal Loan to Value (LTV) for Buy to Loan to Income (LTI) for PDH

dwelling houses (PDH)

Let mortgages (BTLs) mortgages

• PDH mortgages for non‐first

time buyers are subject to a BTL mortgages are subject to a PDH mortgage loans are subject

limit of 80 per cent LTV. limit of 70 per cent LTV. to a limit of 3.5 times loan to

• For first time buyers of gross income.

properties valued up to This limit can only be exceeded

€220,000, a maximum LTV of by no more than 10 per cent of This limit should not be

90 per cent will apply.

the euro value of all housing exceeded by more than 20 per

• For first time buyers of loans for non PDH purposes cent of the euro value of all

properties over €220,000 a 90

per cent limit will apply on the during an annual period. housing loans for PDH purposes

first €220,000 value of a during an annual period.

property and an 80 per cent

limit will apply on any excess

value over this amount.

The cumulative monetary value of

loans for principal dwelling

purposes which breach either of

these limits should not exceed 15

per cent of the euro value of all

PDH loans on an annual basis.

3SENTIMENTS SURVEY

Survey sent to 4,000 people on our Database of buyers. Early results

indicate …

• Looking at the overall results there is quite an amount of uncertainty as to

what the effects of the new Central Bank Requirement will be.

• 50% of the total sample think that the Central Bank requirements are fair.

• 74% of FTB feel that the new regulations will have a negative effect on

people buying a property.

• 70% overall feel the new requirements will have a negative effect on

people buying a property.

• 30% of FTB feel it will mean they will delay purchasing a property and

a further 15% are unsure.

• Of those FTB with mortgage approval, 60% believe it will not delay them.

Source: Sherry FitzGerald Research

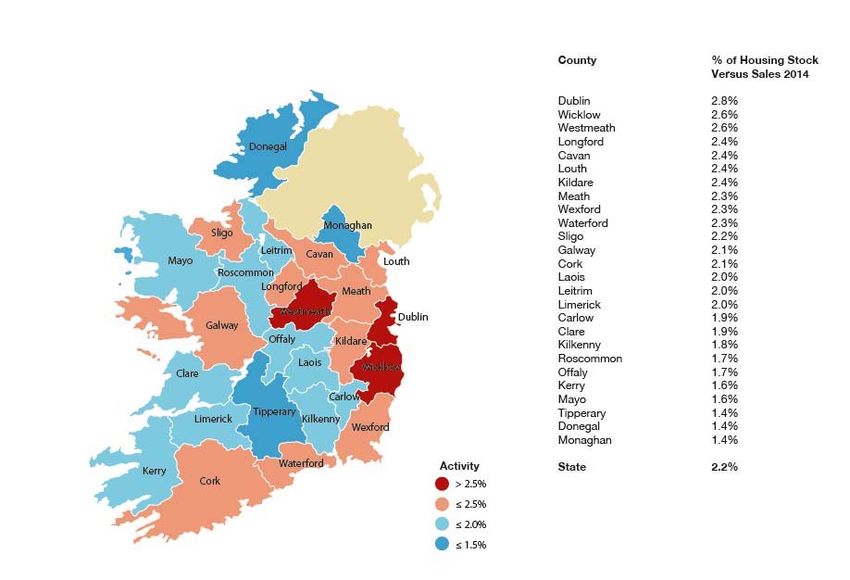

4Residential Market

County by County analysis of Market Activity, 2014

Source: Sherry FitzGerald Research

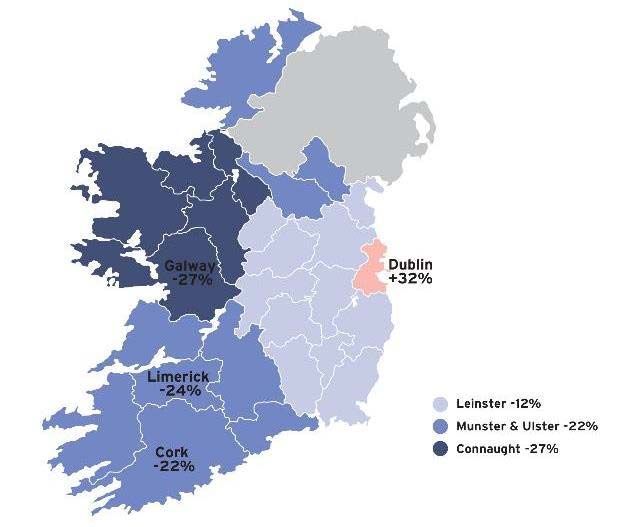

5% Change in Available Property Jan 2014 – Jan 2015

Galway

‐27%

Source: Sherry FitzGerald Research

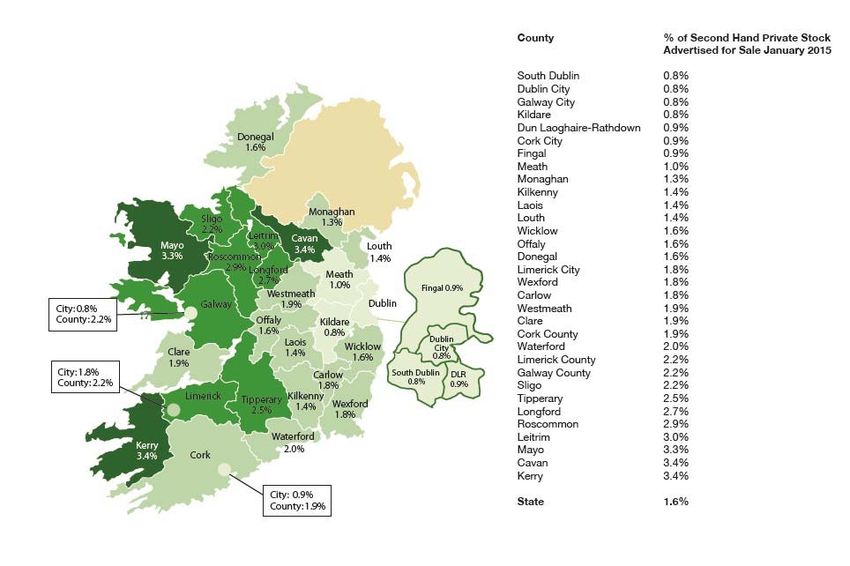

6% of Private Housing Stock Advertised

for Sale January 2015

Source: Sherry FitzGerald Research

7Profile of Vendors 2014

Nursing Home

Emigration

MBU Disability

1%

Other 3% 1%

5%

Larger House

10% Selling Investment

32%

Smaller House

10% National

Bank Repossession

11%

Relocating

14%

Executor Sale

13%

Source: Sherry FitzGerald Research

32% of Vendors “Selling Investment”

8Ireland Second Hand Market

250.0

200.0

Index Base Year = Q4 2001

150.0

100.0

50.0

0.0

Irish Market rose by 16.3% in 12 months to December 2014

92015: Base-line estimate for Price Performance – Nominal Capital Values Period Dublin Ireland 2 Years – to Q4 2016 9.4% 11.5% 5 Years – to Q4 2019 23.2% 25.7% Source: Sherry FitzGerald Research Ireland values up over 25% in Five years 10

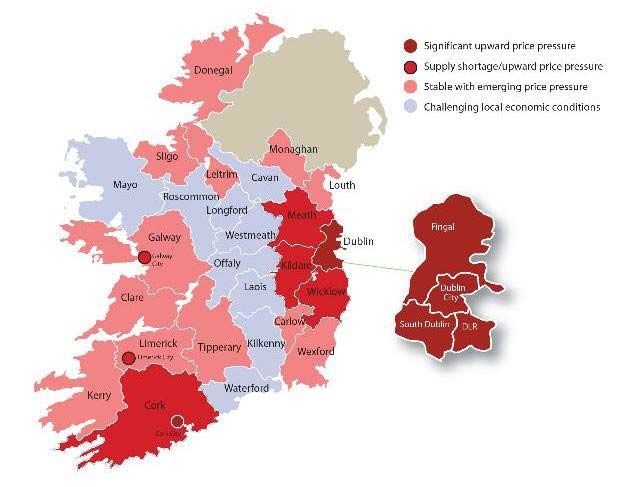

Heat Map of Market Recovery

Source: Sherry FitzGerald Research

11S err

Commercial Market, Investment and Occupier Trends • DTZ

Sherry fitzGerald

h y

]

fii.l.2014 – 2015: Improving!

Improving market confidence

Improving levels of market activity

Select – improvement in values

Building – Portfolio – Loan Sales through 2014

This trend is likely to accelerate in 2015

13Important Trends – 2014/2015

Dublin vs Cork & Regional Ireland

City Centre vs Suburbs

Modern vs Old

New buildings required - Offices, Residential

Viability challenge remains a concern

Large scale construction required

Financing - Challenge

14Comparing 2014 activity to 2015

2014 2015

€

€4.5 bn €9 bn €17 bn €30 bn Mix might be

Investment Residential Loan sales different especially

between loan sales and

activity activity investment activity

15Completed Investment Transactions

– Location Breakdown, 2014

Connaught

Munster

1%

Unknown 3%

3%

Multiple Locations

13%

Leinster

80%

Source – DTZ Sherry FitzGerald Research

16Completed Investment Transactions

– Investor Type, 2014

Private Investors

8%

Unknown Private Equity

11% Investors

34%

Joint Venture

12%

Institutions

12%

REIT

23%

Source – DTZ Sherry FitzGerald Research

17Completed Investment Transactions

– Investor Type, 2015

18S err

Cork New Business - 2014 h y ]

d

fii.l.Some 2014 Investment Sales

Property Details Image

Mathew House, • Sold September 2014

Father Mathew Street • €2,050,000

(Office) • Rent - €197,000

Anglesea House (IBRC) • Sold Quarter 2, 2014

(Office) • €2,700,000

• Disposal c. €140 per sq ft

Fullers Lodge, • Sale Agreed, Dec 2014

College Road • Excess of €2.2m

(Student Accommodation) • Gross Rent - €200,000

Building 5, • May 2014

EastGate Avenue, • €3,250,000

Little Island (Office) • Passing Rent - €320,000

20Some 2014 Investment Sales

Property Details Image

Units 1 & 2 • Sale Agreed, Dec 2014

Westside Retail • Price agreed in excess of €3.5m

Park, • Passing Rent - €385,000

Ballincollig

(Retail)

AIB, Pearse • Sale Agreed, Dec 2014

Street, Kinsale, • Price agreed in excess of €1.5m

Co Cork (Bank) • Passing Rent - €99,700

• Tenant – AIB

AIB, The • Sale Agreed Qtr4 2014

Quay, • Price - €2.2m

Waterford • Rent - €204,000

(Bank) • Tenant - AIB

Fat Face, Kinsale, • Sale Agreed, Dec 2014

Co Cork • Price agreed in excess of €900,000

(Retail) • Passing Rent - €80,000

21Irish Office Market, 2014

Source – DTZ Sherry FitzGerald Research

22Cork Market – Active Sectors

Office – Large Floorplates (Grade A):

Suburban Offices

City Centre Offices

Anchor Retail

Investments (7 years)

Suburban Housing

Agri Business

Student Accommodation

Healthcare

Hotels & Leisure

23Cork Market – More Challenged

City Centre Residential (Development)

Small Office Floorplates

Old Buildings

Small Shop Retail

Industrial

Secondary locations

(* High Risk with a mix of these

variables)

24Cork Office Market

Demand: 25,000 / 30,000 sq m annually

(c. 270,000 – 325,000 sq ft)

80% FDI/Large space enquiry

(c. 28,000 sq ft average size)

Market demand for large floor plates

– Grade A space

Good quality incubator space required

Existing FDI’s continue to grow – Tyco, EMC, VM Ware,

Apple, Lilly, Amazon

(Vacancy Rate: c. 18%)

25Cork Office – New Construction

City Centre – Albert Quay (x2), South Terrace,

Anderson Quay, Docklands

Mahon – Central Plaza/Motorola

Eastgate – M.25 Buildings

Airport – New Planning Application – 10,000 sq m

Cork Science & Technology Park

26Cork Office – Viability New Construction

City Centre: €270 p.s.m.

+

€25 + p.s.ft. +

Suburban: €215 p.s.m.+

€20 p.s.ft +

Business Parks: €190 p.s.m.+

€18 p.s.ft +

Grade A space only – no compromise

Reliant on an improving market

Domestic / Indigenous market will follow

27Industrial Market 2014/5

Weakening Euro, lower fuel costs, growth in on‐line sales, increased

exports all positive indicators for the market

The changing dynamics of the retail market will create a new driver

for the industrial sector. There is substantial year on year growth in

the click and collect market with large industrial accommodation

required to provide immediate turnaround times

Ireland will be an established hub for data centres with the climate a

main driver coupled with the access to power and data

Design and build facilities will outperform existing stock with the

main requirement arising from the pharma and tech sectors

Industrial accommodation will become more advanced with

automation and robotics and manufacturing systems

Less emphasis on Leinster - Uplift in regions

28Industrial – Values Remain Low

AV Rental: €47.50 p.s.m.

€4.40 p.s.f.

Capital Value: €50 p.s.f.

Capital Cost: €80 + p.s.f.

Not viable – Impact on Industrial Land value

Scope for ‘Build to order’ modern high bay buildings

Stronger locations – South Link Road, Little Island

improved demand

29Retail Market

Change in the ownership structure of retail in Ireland, going to lead to intense

asset management plans over next 3 -5 years.

Retail is going to be more of a partnership between landlords and tenants.

Dublin’s prime retail areas extending to surrounding streets e.g. H&M/

Abercrombie. Prime buildings as important as prime location

Redevelopment/ expansion of existing Centres: St. Stephen Green/ Liffey Valley/

The Square / Kildare Outlet Centre

Shopping Centres will evolved to provide more of a rounded experience and to

increase dwell time

Change as technology and the internet continue to evolve – click &collect,

impact likely to be greater in middle market

As more new homes are completed strong demand from occupiers for the

stronger retail parks in the larger urban centres.

30Retail – Shopping

Continued disposal of Cork Shopping Centres

Existing Retail Hubs

Anchor Retail Demand

Discount Retail Demand

Rising Household Expenditure

New Owners (Varde – Marathon – IPUT)

31Challenged Retail

Small shop

Secondary Retail

Old Building – Retail

Alternative Uses – Commercial

Change of Use to Residential

32Regional Commercial Forecast Rents

Q4 2014 Q4 2020 % Change

Cork Industrial €47.50 €60 26%

Cork Office €240 €300 25%

Cork Retail €2,000 €2,700 35%

Galway Industrial €43 €60 40%

Galway Office €193 €236 22%

Galway Retail €1,900 €2,700 42%

Limerick Industrial €38 €54 42%

Limerick Office €188 €215 14%

Limerick Retail €900 €1,350 50%

33Regional Commercial Forecast Yields

Q4 2014 Q4 2020

Cork Industrial 9.5% 9%

Cork Office 7.25% 7%

Cork Retail 6.75% 5.25%

Galway Industrial 10% 9%

Galway Office 8.25% 7%

Galway Retail 6.5% 5.5%

Limerick Industrial 10% 9%

Limerick Office 8.5% 7%

Limerick Retail 8% 5.5%

34Development Land

• Increase supply of infill sites anticipated in 2015

• Impact of Central Bank lending changes – market yet to react

• More portfolio land sales with opportunity for longer term

• Several significant housing and commercial site construction

• More transactions funded with bank debt finance

• Dublin to further consolidate its position as the two‐tier market

• Developers / land owners will broaden their horizon in terms of uses of land

i.e. multi‐family, student accommodation, nursing homes, step‐down etc.

• Regional cities and commuter towns are likely to benefit from the Central

Bank ruling

35Cork Market – Sample Land Values – Prime Locations

City Centre: €4M per acre

Suburban Retail (special): €2M per acre

Housing (South City): €400/€600,00 per acre

Office Park: €400,000 per acre

Industrial: €150,000 per acre

Agricultural: €12,000/€14,000 per acre

Very strong demand for housing land

36Residential – To Let Sector

Diminishing Supply

Major Growth in Demand

Rising Rentals – Risk

Crisis Sector – New ‘to let’ residential units are not

viable close to City Centre

Demand V Supply (Ability to deliver new stock)

New Ownership – Multi-family (Ires Reit – Kennedy

Wilson)

37Residential – New Construction

ESRI – 2,000 units per annum (Cork)

Viability Threshold – Cork City (22 locations)

Site Value – (15% not viable)

Central Bank rules

Most likely to see growth

Infrastructure Challenges – Planning - Regulation

382015 – The Growth Sectors

Retail

Grade A Offices

Development Land

Housing

Student Accommodation

Hotels / Leisure

Healthcare

39The Growth Locations

City Centre

District Centres – Mahon/Wilton/Blackpool

Satellite Towns – (Carrigaline/Ballincollig/Rail Corridor)

Ringaskiddy – (Port of Cork)

Docklands

40Slán

41Questions

59Thank you

60You can also read