Highlights - National Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

September 2018 Highlights The positive return of the MSCI AC over the year to date is due almost entirely to the U.S. U.S.-led trade wars seem to be starting to hurt the world economy. Emerging economies, highly dependent on trade, have seen earnings revisions turn negative for the first time since 2016. Policymakers must now take steps to reaccelerate it in 2019. A better-than-expected economy with upside surprise in earnings took the S&P 500 to a new high in Q3. Importantly, this new record was reached on the strength of earnings growth, not multiple expansion. Though U.S. equities are vulnerable to a cooling of the economy and to downward earnings revisions, the good news is that Federal Reserve forward guidance has become hazier about the path of policy-rate normalization after its next hike (anticipated September 26). The S&P/TSX is barely keeping afloat in 2018. After eight months the benchmark has returned a meagre 0.3%. Were it not for high-flying cannabis stocks, classified under health care, the S&P/TSX would be in the red. Until NAFTA is resolved, it is difficult to see much of an uptrend for the S&P/TSX, even though its valuation is now below the historical average for the first time in more than two years. Our asset allocation and sector rotation are unchanged this month. Trade tensions between the U.S. and its trading partners (Canada, China, Europe) coupled with the plight of emerging markets and greenback appreciation prompt us to maintain our more prudent stance recommended in June. We take some comfort from the cautious tone of the Federal Reserve about monetary policy normalization, an essential element to prolong the economic expansion. We stand ready to redeploy our excess cash if opportunities arise. Stéfane Marion stefane.marion@nbc.ca Matthieu Arseneau matthieu.arseneau@nbc.ca

Monthly Equity Monitor

Global growth is downshifting World: Distribution of trade flows by region

Merchandise trade as percentage of world total (2017)

The benchmark global equities index has been stuck since 30

%

the end of January in a tight range below its record high

25

of that month (chart).

20

World: Perspective on global equities

MSCI equity indices

15

132

Index, 2017m1=100

MSCI US

10

128

124

MSCI AC World 5

120

0

116 EM Asia Euro U.S. LATAM Africa/Middle Japan EM Europe

MSCI AC East

112 world ex. US

NBF Economics and Strategy (data via Bureau of Economic Policy Analysis or CPB)

108

World: Growth in global trade flows worst since 2016

104 World trade volumes

100 7

q/q % chg. saar

6

96

2017q1 2017q2 2017q3 2017q4 2018q1 2018q2 2018q3 2018q4 5

NBF Economics and Strategy (data via Datastream)

4

3

The positive return of the MSCI AC over the year to date 2

is due almost entirely to the U.S. (about 50% of the index). 1

0

0

As the table below shows, diffusion is pretty bad so far in -1

2018, with Europe, Japan and Emerging Markets all down -2

year to date (table). Emerging Asia, the region most -3

exposed to global trade wars, is down 3.9% year to date. -4

2015 2016 2017

Q2

2018

NBF Economics and Strategy (data via CPB)

MSCI composite index: Price Performance

Emerging economies, highly dependent on trade, were hit

Month to Quarter to Year to date hard in Q2. Volume exports declined at 2% annualized. As

date date

a result, earnings revisions have turned negative for the

MSCI AC World 0.9 3.8 3.5

MSCI World 1.1 4.3 4.4

first time since 2016 (chart).

MSCI USA 3.1 6.7 8.7

MSCI Canada -1.5 -0.3 0.4 World: Negative earnings revisions for emerging markets

3-month change in 12-month forward EPS for MSCI EM

MSCI Europe -2.6 0.5 -2.0

MSCI Pacific ex Jp -0.8 0.7 0.2 4

%

MSCI Japan -0.8 0.7 -4.0 3

MSCI EM -0.7 0.4 -3.5 2

MSCI EM EMEA -0.1 1.9 -3.0

1

MSCI EM Latin America -2.7 3.0 -1.1

0

MSCI EM Asia -0.6 -0.2 -3.9

-1

8/31/2018

-2

NBF Economics and Strategy (data via Datastream)

-3

-4

U.S.-led trade wars seem to be starting to hurt the world -5

economy. The latest CPB data confirm that global trade -6

volume was flat in Q2 — the worst quarter since 2016 — -7

as U.S. tariffs on steel and aluminum imports and the -8

2011 2012 2013 2014 2015 2016 2017 2018

retaliatory measures of affected trade partners took NBF Economics and Strategy (data via Datastream)

effect.

Adding insult to injury, The Wall Street Journal recently

reported that the Trump administration is reviewing tariff

breaks the U.S. previously granted to poorer nations to

promote their economic development. India, Thailand and

2

Monthly Equity Monitor

Brazil are the most exposed to that program. It’s not so World: Perspective on commodity prices

Copper price

much that the numbers are huge as that the move would

8,400

come on top of everything else — China-U.S. tension, USD/tonne

8,000

NAFTA, tightening of sanctions on Russia and Turkey). We

7,600

hope the White House is aware that emerging economies

7,200

account for almost 60% of world GDP (up from 42% at the

6,800

time of the Asian crisis) and that USD appreciation due to

6,400

risk-off reaction will jeopardize both global growth and

6,000

the outlook for U.S. corporate profits.

5,600

5,200

World: Emerging market account for close to 60% of global GDP

Share of GDP on a PPP basis 4,800

60 4,400

%

4,000

58

2013 2014 2015 2016 2017 2018

NBF Economics and Strategy (data via Datastream)

56

54

While China’s recently announced plan to boost infra-

52

structure spending is good news for commodity prices, the

50

longer-term outlook will depend on the commitment of

48

the large economic powers to the value of globalization.

46

We take solace from the agreement between Chinese and

44

U.S. trade negotiators to map out a road to solution of

42 Asian crisis

their trade impasse before the November 30 G20 meeting

40

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

in Buenos Aires, which Mr. Trump and Mr. Xi are scheduled

NBF Economics and Strategy (data via IMF)

to attend. However, given the acrimony of U.S.-Canada

discussions on renewal of NAFTA, rapid abatement of trade

USD: At a record vs. emerging markets

Broad dollar index (C26) vs. OITP index (19 currencies)

tensions between Washington and its trading partners

120

cannot be taken for granted.

Index, 2015 = 100

OITP

118

116

Growth is set to slow in Q3. Policymakers must now take

114

steps to reaccelerate it in 2019.

112

Broad

USD

110

108

106

104

102

100

98

2015 2016 2017 2018

NBF Economics and Strategy (data via Datastream)

These developments are bad news for commodity prices.

As the next chart shows, the price of copper is still down

18% from its June high.

3

Monthly Equity Monitor

U.S.: Immune for how long? A better-than-expected economy with upside surprise in

earnings took the S&P 500 to a new high in Q3 (chart).

The advertised near-term benefits of fiscal stimulus have

materialized. U.S. GDP growth accelerated to 4.2% in the U.S.: Equities at a record high

second quarter, with tax cuts propping up both consumer S&P 500

spending and business investment. Government outlays also 2,920

index

2,880

increased. All in all, real final sales, i.e. GDP excluding 2,840

inventories, grew at 5.3% annualized. In nominal terms 2,800

2,760

the Q2 growth was a whopping 8.4%, the strongest since 2,720

2006 (chart). So the only reason real growth did not top 2,680

5% was drag from inventories. That drag, however, is good 2,640

2,600

news for inventory rebuilding and thus for Q3 output. 2,560

2,520

2,480

U.S.: Final sales surge in Q2 2,440

Nominal final sales of domestic product

2,400

10 2,360

% (q/q, saar)

2,320

8 2017Q2 2017Q3 2017Q4 2018Q1 2018Q2 2018Q3 2018Q4

NBF Economics and Strategy (data via Datastream)

6

4

Importantly, this new record was reached on the strength

2 of earnings growth, not multiple expansion. As the chart

0 below shows, 12-month forward P/E is well off its cyclical

-2

high and is not far from its historical average.

-4

-6

-8

2002 2004 2006 2008 2010 2012 2014 2016 2018

NBF Economics and Strategy (data via Datastream)

Strong Q2 growth was a major boost for corporate profits,

as were the recently enacted corporate tax cuts. As the

chart below shows, after-tax profits in Q2 were up 16%

from a year earlier, the strongest increase in more than

five years (chart).

U.S.: Tax treatment boosts after tax profits

Corporate profits from current production: before and after tax on corporate income

18

% (y/y) After tax

16

14

12

10 Before An uncertain geopolitical picture, with the Federal Reserve

tax

8 still inclined to hike this fall (albeit modestly) despite a

6

4

strengthening of the U.S. dollar, could challenge earnings

2 growth and thus equity markets, since P/E expansion is

0

-2

very hard to come by in this mature phase of the economic

-4 cycle. As the next table shows, the bottom-up consensus of

-6

equity analysts sees robust 13.3% earnings growth over the

-8

-10 coming year.

-12

2013 2014 2015 2016 2017 2018

NBF Economics and Strategy (data via BEA)

4Monthly Equity Monitor

S&P 500 composite index: EPS Performance U.S.: What next for earnings revisions?

1-month change in 12-month forward EPS vs. CITI economic surprise index

12 months

2017 2018 2019 2020 6 120

forward % index

S&P 500 11.5 23.1 10.2 10.2 13.3 5 100

ENERGY 354.3 92.0 23.8 12.1 37.9 4 80

MATERIALS 14.7 30.1 7.3 11.7 13.3

3 60

INDUSTRIALS 4.8 20.5 12.2 11.0 14.4

CONS. DISC. 6.3 18.6 12.1 14.0 13.8 2 40

Earnings

CONS. STAP. 6.3 11.2 6.2 7.5 7.2 1

revisions

20

(left)

HEALTH CARE 8.0 14.6 8.0 9.3 10.0

0 0

FINANCIALS 6.5 32.5 9.5 10.0 15.8

IT 18.6 23.4 11.1 11.2 12.5 -1 -20

TELECOM 0.4 17.1 3.2 1.7 7.3 Economic

surprise

-2 index

-40

UTILITIES 2.7 6.8 4.7 5.0 5.4 (right)

REAL ESTATE -12.4 -10.1 0.9 6.8 -3.0 -3 -60

8/31/2018 -4 -80

2015 2016 2017 2018

NBF Economics and Strategy (data via Datastream) NBF Economics and Strategy (data via Datastream and Bloomberg)

Interestingly, close to 60% of that earnings growth over the The good news in the meantime is that Federal Reserve

coming year is expected to come from margin expansion. forward guidance has become hazier about the path of

As the table below shows, profit margins are expected to policy-rate normalization after its next hike (anticipated

increase over the next 12 months in all main sectors of September 26). The last thing we need is for the Fed to

the S&P 500 except real estate. However, that margin keep flattening the yield curve beyond an economic

expansion becomes a tall order if Washington levies more breaking point. As the chart below shows, the yield spread

import tariffs. between a 10-year Treasury and a 3-month T-Bill is currently

78 basis points. Though this is the narrowest spread in more

S&P 500 composite index: Profit margins than a decade, it is still above the danger zone of 50 basis

12-month 12-month points historically associated with bad times for equity

2017 2018 2019 2020

trailing forward markets.

S&P 500 10.5 11.9 12.5 13.3 11.5 12.3

ENERGY 4.1 6.6 7.8 8.9 5.9 7.4

MATERIALS 9.4 10.9 11.5 12.3 10.5 11.3

INDUSTRIALS 8.8 9.8 10.5 11.1 9.5 10.3

CONS. DISC. 7.1 7.8 8.2 8.8 7.6 8.1

CONS. STAP. 7.0 7.4 7.6 7.9 7.3 7.6

HEALTH CARE 9.7 10.5 10.8 11.2 10.2 10.7

FINANCIALS 14.4 18.3 19.1 20.6 17.1 18.9

IT 20.3 22.3 23.1 23.8 22.0 23.0

TELECOM 12.9 14.1 13.9 14.1 13.7 14.0

UTILITIES 11.8 12.4 12.7 13.1 12.2 12.6

REAL ESTATE 20.8 16.8 16.2 16.5 18.0 16.4

8/31/2018

NBF Economics and Strategy (data via Datastream)

So the U.S. equity market is vulnerable to a cooling of the

economy and to downward earnings revisions. As the next

chart shows, the Citi economic surprise index for the U.S.

has turned negative for only the second time since Mr.

Trump’s election, an indication of waning momentum. Canada: An uncertain outlook

Perhaps the White House will take note and reassess its

position on trade. The S&P/TSX is barely keeping afloat in 2018. After eight

months the benchmark has returned a meagre 0.3%. Were

it not for high-flying cannabis stocks, classified under

health care, the S&P/TSX would be in the red (table).

5Monthly Equity Monitor

S&P/TSX composite index: Price Performance Canada: Earnings hit a record in Q2

Trailing earnings for the S&P/TSX

Quarter to

Month to date Year to date

date 1,040

EPS

S&P TSX -1.0 -0.1 0.3 1,000

HEALTH CARE 28.4 17.0 15.1

960

IT 5.1 2.9 25.5

920

REAL ESTATE 1.9 3.5 6.4

BANKS 1.6 4.0 1.5 880

FINANCIALS 1.1 3.3 -0.1 840

INDUSTRIALS 0.6 5.4 11.4 800

TELECOM -0.9 2.9 -4.4

760

UTILITIES -1.3 -0.7 -9.1

720

CONS. STAP. -1.7 -0.9 -4.2

CONS. DISC. -3.7 -4.0 -1.7 680

ENERGY -4.0 -3.1 -0.4 640

MATERIALS -8.2 -11.9 -9.6

600

8/31/2018 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

NBF Economics and Strategy (data via Datastream) NBF Economics and Strategy (data via Datastream)

This disappointing performance is not due to lacklustre S&P/TSX composite index: EPS Performance

economic growth or disappointing profits. Market watchers

12 months

will probably be surprised to learn that despite escalating 2017 2018 2019 2020 forward

trade tensions, the most surprising economic performance S&P TSX 28.8 13.0 13.1 9.4 12.9

ENERGY 313.1 32.0 26.7 4.8 28.1

of recent weeks has been that of trade-exposed Canada. MATERIALS 66.5 14.8 17.8 12.4 16.9

As the chart below shows, the economic surprise index for INDUSTRIALS 16.0 10.8 17.9 15.5 15.7

CONS. DISC. 15.4 14.2 11.7 11.6 12.7

Canada recently surged to a six-month high.

CONS. STAP. 12.1 10.3 13.7 11.5 13.6

HEALTH CARE -30.1 -10.3 29.5 21.2 12.9

Canada: Economy continues to surprise on the upside FINANCIALS 15.4 8.8 7.6 8.6 7.5

Economic surprise index (daily data) BANKS 10.4 11.0 5.9 8.1 6.7

IT 12.4 17.8 14.7 14.5 13.2

120 Index TELECOM 3.6 7.9 5.7 7.6 6.4

100 Developed economies UTILITIES -8.9 11.2 16.7 12.1 20.1

Canada REAL ESTATE 27.6 7.9 -3.9 4.7 -0.5

80 Emerging economies

8/31/2018

60

NBF Economics and Strategy (data via Datastream)

40

20

0 In August Canada finally rejoined NAFTA negotiations only

-20 to be faced with a fait accompli: a U.S.-Mexico agreement

-40 on a revamped deal. Mr. Trump was eager to call the new

-60 pact the “U.S.-Mexico trade agreement” and drop the

-80 name NAFTA. Changing a name is one thing; scrapping an

-100 existing agreement is another. Despite Mr. Trump’s stated

2017Q3 2017Q4 2018Q1 2018Q2 2018Q3

NBF Economics and Strategy (data via Bloomberg) desire to shred NAFTA, he is unlikely to have the authority

to formally terminate the agreement without congressional

How long this will continue, now that surprises have turned approval. So we continue to think his preferred route is to

negative in both developed and emerging economies, include Canada in a three-way pact that he wants signed

remains to be seen. After fairly strong GDP growth in Q2 at the end of the month. We are looking at very intense

(+2.9% annualized) that fuelled a new high in earnings per negotiations over the next few weeks.

share, we expect economic growth to slow markedly in Q3,

Ottawa says: “Canada will only sign a new NAFTA that is

to about 1.2%. At this writing the bottom-up consensus of

good for Canada and good for the middle class." Hmm. We

equity analysts expects earnings growth of 12.9% over the

say it’s time to be pragmatic. The U.S. has stated that if

next 12 months (table). However, this expectation does

Canada refuses to negotiate, its easiest path would be to

not take into account a possible trade imbroglio in a

increase auto tariffs. As the table below shows, that would

critical sector of the economy.

expose 4.1% of Ontario’s jobs to punitive tariffs. We doubt

this is something our middle class would appreciate. It’s

time for Canada to make a few concessions.

6Monthly Equity Monitor

Canada: Considerable exposure of jobs to automotive exports to U.S.

Exposure of Canadian employment to U.S. protectionism

Table 2 ‐ Employment exposure to industry Canadian exports to U.S.

(Employment dependent on specific Canadian industry exports to the U.S. as a % of total employment ‐ 2013)

Exporting industry CA NL PE NS NB QC ON MB SK AB BC

A ‐ U.S. Protectionist rhetoric

111 ‐ 112 Crop and Animal Production 0.3% 0.0% 0.6% 0.1% 0.3% 0.1% 0.2% 0.7% 1.0% 0.4% 0.3%

3115 ‐ Dairy Products Manufacturing 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

321 ‐ Wood Product Manufacturing 0.3% 0.0% 0.0% 0.2% 0.9% 0.4% 0.1% 0.2% 0.2% 0.2% 0.9%

326 ‐ Plastics and Rubber Products Man. 0.3% 0.0% 0.0% 0.9% 0.2% 0.4% 0.4% 0.3% 0.0% 0.1% 0.1%

3311 ‐ Iron, Steel mills, Ferro Alloy Man. 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.1% 0.0% 0.0% 0.0%

3312 ‐ Steel products from purchased steel 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.0% 0.1% 0.0% 0.0%

3313 ‐ Alumina and Aluminum prod. & proc. 0.1% 0.0% 0.0% 0.0% 0.0% 0.4% 0.1% 0.0% 0.0% 0.0% 0.0%

3315 ‐ Foundries 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

335 ‐ Electrical equ., appliance and comp. man. 0.1% 0.0% 0.0% 0.0% 0.0% 0.1% 0.1% 0.1% 0.0% 0.0% 0.1%

3352 ‐ Household Appliance Man. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

3361 ‐ Motor Vehicle Manufacturing 0.9% 0.2% 0.2% 0.2% 0.3% 0.4% 1.8% 0.4% 0.2% 0.3% 0.3%

3362 ‐ Motor Vehicle body and trailer man. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% 0.0% 0.0% 0.0%

3363 ‐ Motor vehicle parts manufacturing 0.4% 0.0% 0.0% 0.0% 0.1% 0.1% 0.8% 0.1% 0.1% 0.1% 0.1%

3364 ‐ Aerospace product and parts man. 0.2% 0.0% 0.6% 0.3% 0.0% 0.5% 0.1% 0.5% 0.0% 0.0% 0.1%

Sub‐total 2.8% 0.4% 1.6% 1.9% 1.8% 2.5% 4.1% 2.4% 1.8% 1.2% 1.8%

NBF Economics and Strategy

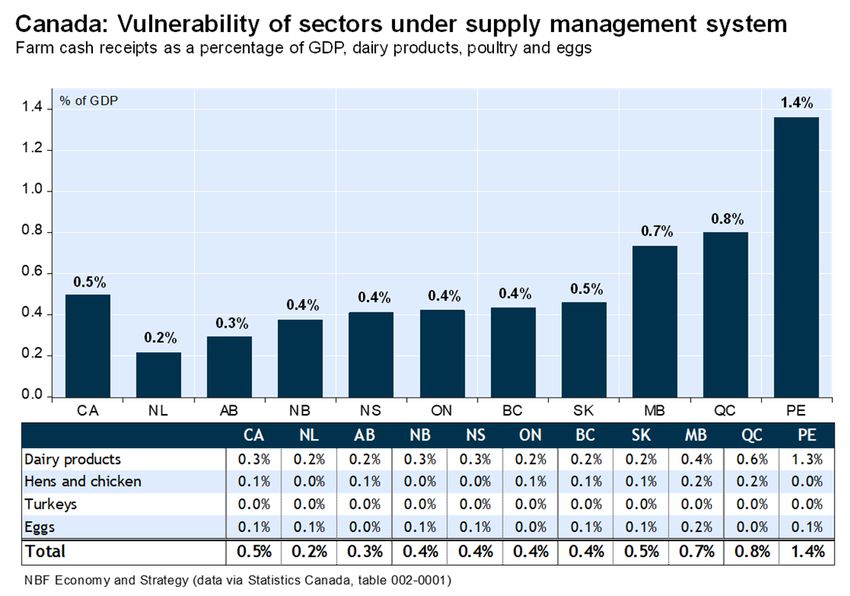

The U.S. wants changes to Canada’s agriculture supply

Another major point of contention between Canada and

management system, which includes production quotas for

the U.S. is Chapter 19, the binational panel before which

milk, eggs and poultry and tariffs of up to 300% on imports.

one of the partners can challenge the legality of the other’s

We think Canada will ultimately agree to concessions. As

trade barriers. Rulings by this panel cannot be appealed

argued by our colleague Angelo Katsoras last December,1

to domestic courts. The Trump administration maintains

this view is based on Canadian concessions in past trade

that Chapter 19 infringes on U.S. sovereignty and wants to

negotiations. For example:

revert to settling disputes in U.S. courts. While common

Under the now-collapsed Trans-Pacific Partnership, Canada ground on this issue will be difficult to find, a compromise

had agreed to a 3.25% increase in the amount of foreign might entail allowing more U.S. arbiters on the panels.

dairy products entering Canada tariff-free. The plan was The U.S. could also agree to keep this dispute panel intact

for dairy farmers to receive financial compensation for in exchange for concessions elsewhere (agriculture?).

their resulting losses.

As our colleague Angelo argued in his note of June 11,

Under the Comprehensive Economic and Trade Agreement, “NAFTA: Is a ‘bad deal’ really worse than no deal for

Canada has agreed to accept more European dairy products. Canada?,” our country can ill afford to risk a loss of

Over the next few years, tariff-free cheese imports will investment in Canada by companies uncertain of access

go from 5% to 9% of Canada's current cheese market. to the U.S. market. Canada’s difficult position is best

With the U.S. accounting for 76% of Canada’s total trade summed up in the following quote: “With NAFTA in place,

compared to just under 10% for the European Union, logic Canada is an option when globally oriented firms consider

dictates that Canada should offer concessions to the U.S. their North American strategies; without it, Canada is a

as well. smallish market that probably can be served from the U.S.

or elsewhere.”2 A working paper published August 25 by

As the next chart shows, the province most exposed to the Bank of International Settlements showed that our

concessions on supply management is P.E.I., given the country had the most to lose from a failed NAFTA

weight of dairy production in its economy, followed by (bis.org/publ/work739.htm). So until NAFTA is resolved,

Quebec and Manitoba. it is difficult to see much of an uptrend for the S&P/TSX,

even though its valuation is now below the historical

average for the first time in more than two years (chart).

1 2

See “Update on NAFTA negotiation” by Angelo Katsoras, “Canada could pay a steep price for ‘progress’ in NAFTA

December 18, 2017. talks,” Financial Post, January 30, 2018

7Monthly Equity Monitor

Canada: Perspective on valuation

12-month forward for the S&P TSX

Asset allocation

24

ratio

Our asset allocation remains unchanged this month.

22 Trade tensions between the U.S. and its trading partners

20 (Canada, China, Europe) coupled with the plight of

18

emerging markets and greenback appreciation prompt us

to maintain our more prudent stance recommended in

16

Average

June. We take some comfort from the cautious tone of

14

the Federal Reserve about monetary policy

12 normalization, an essential element to prolong the

10 economic expansion. We stand ready to redeploy our

8

excess cash if opportunities arise.

6

1990 1995 2000 2005 2010 2015

NBF Economics and Strategy (data via Datastream)

Sector rotation

Our sector rotation remains unchanged this month.

S&P/TSX : Price to 12-month forward earnings

5 year

8/31/2018 A year ago 10 year ave.

average

S&P TSX 14.4 15.6 14.4 15.6

ENERGY 16.2 23.6 23.2 30.3

MATERIALS 15.9 22.3 17.3 20.7

INDUSTRIALS 18.0 17.0 15.0 16.3

CONS. DISC. 13.8 14.2 13.3 14.3

CONS. STAP. 15.6 17.3 15.5 17.2

HEALTH CARE 23.1 8.5 13.4 11.9

FINANCIALS 11.5 11.6 11.6 11.9

BANKS 11.1 11.1 11.0 11.2

IT 25.6 22.2 16.7 20.6

TELECOM 15.3 17.0 14.3 15.9

UTILITIES 17.9 19.3 17.9 19.1

REAL ESTATE 13.4 NA NA NA

8/31/2018

NBF Economics and Strategy (data via Datastream)

8Monthly Equity Monitor

NBF Asset Allocation

Benchmark NBF Change (pp)

(%) Recommendation (%)

Equities

Canadian Equities 20 20

U.S. Equities 20 20

Foreign Equities (EAFE) 5 8

Emerging markets 5 3

Fixed Income 45 39

Cash 5 10

Total 100 100

NBF Economics and Strategy

NBF Market Forecast NBF Market Forecast

Canada United States

Actual Q42018 (Est.) Actual Q42018 (Est.)

Index Level Sep-04-18 Target Index Level Sep-04-18 Target

S&P/TSX 16,161 16,500 S&P 500 2,897 2,950

Assumptions Q42018 (Est.) Assumptions Q42018 (Est.)

Level: Earnings * 1002 1021 Level: Earnings * 151 155

Dividend 477 486 Dividend 52 54

PE Trailing (implied) 16.1 16.2 PE Trailing (implied) 19.2 19.0

Q42018 (Est.) Q42018 (Est.)

10-year Bond Yield 2.24 2.57 10-year Bond Yield 2.90 3.07

* Before extraordinary items, source Thomson * S&P operating earnings, bottom up.

NBF Economics and Strategy

9Monthly Equity Monitor

NBF Fundamental Sector Rotation - August 2018

Name (Sector/Industry) Recommendation S&P/TSX weight

Energy Market Weight 20.2%

Energy Equipment & Services Market Weight 0.6%

Oil, Gas & Consumable Fuels Market Weight 19.6%

Materials Market Weight 11.4%

Chemicals Underweight 2.3%

Containers & Packaging Market Weight 0.5%

Metals & Mining * Market Weight 2.8%

Gold Overweight 5.1%

Paper & Forest Products Market Weight 0.6%

Industrials Underweight 10.1%

Capital Goods Market Weight 2.5%

Commercial & Professional Services Underweight 1.8%

Transportation Underweight 5.7%

Consumer Discretionary Underweight 5.6%

Automobiles & Components Underweight 1.3%

Consumer Durables & Apparel Overweight 0.7%

Consumer Services Underweight 1.4%

Media Market Weight 0.9%

Retailing Underweight 1.3%

Consumer Staples Overweight 3.5%

Food & Staples Retailing Overweight 2.7%

Food, Beverage & Tobacco Overweight 0.8%

Health Care Market Weight 1.3%

Health Care Equipment & Services Market Weight 0.2%

Pharmaceuticals, Biotechnology & Life Sciences Market Weight 1.1%

Financials Market Weight 33.1%

Banks Market Weight 23.0%

Diversified Financials Market Weight 3.8%

Insurance Market Weight 6.3%

Information Technology Market Weight 4.1%

Software & Services Market Weight 3.9%

Technology Hardware & Equipment Market Weight 0.2%

Telecommunication Services Overweight 4.4%

Utilities Overweight 3.5%

Real Estate Market Weight 2.8%

* Metals & Mining excluding the Gold Sub-Industry for the recommendation.

10Monthly Equity Monitor Economics and Strategy Montreal Office Toronto Office 514-879-2529 416-869-8598 Stéfane Marion Matthieu Arseneau Warren Lovely Chief Economist and Strategist Deputy Chief Economist MD & Head of Public Sector Strategy stefane.marion@nbc.ca matthieu.arseneau@nbc.ca warren.lovely@nbc.ca Krishen Rangasamy Paul-André Pinsonnault Marc Pinsonneault Senior Economist Senior Fixed Income Economist Senior Economist krishen.rangasamy@nbc.ca paulandre.pinsonnault@nbc.ca marc.pinsonneault@nbc.ca Kyle Dahms Jocelyn Paquet Angelo Katsoras Economist Economist Geopolitical Analyst kyle.dahms@nbc.ca jocelyn.paquet@nbc.ca angelo.katsoras@nbc.ca General This Report was prepared by National Bank Financial, Inc. (NBF), (a Canadian investment dealer, member of IIROC), an indirect wholly owned subsidiary of National Bank of Canada. National Bank of Canada is a public company listed on the Toronto Stock Exchange. The particulars contained herein were obtained from sources which we believe to be reliable but are not guaranteed by us and may be incomplete and may be subject to change without notice. The information is current as of the date of this document. Neither the author nor NBF assumes any obligation to update the information or advise on further developments relating to the topics or securities discussed. The opinions expressed are based upon the author(s) analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein, and nothing in this Report constitutes a representation that any investment strategy or recommendation contained herein is suitable or appropriate to a recipient’s individual circumstances. In all cases, investors should conduct their own investigation and analysis of such information before taking or omitting to take any action in relation to securities or markets that are analyzed in this Report. The Report alone is not intended to form the basis for an investment decision, or to replace any due diligence or analytical work required by you in making an investment decision. This Report is for distribution only under such circumstances as may be permitted by applicable law. This Report is not directed at you if NBF or any affiliate distributing this Report is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it that NBF is permitted to provide this Report to you under relevant legislation and regulations. National Bank of Canada Financial Markets is a trade name used by National Bank Financial and National Bank of Canada Financial Inc. National Bank Financial Inc. or an affiliate thereof, owns or controls an equity interest in TMX Group Limited (“TMX Group”) and has a nominee director serving on the TMX Group’s board of directors. As such, each such investment dealer may be considered to have an economic interest in the listing of securities on any exchange owned or operated by TMX Group, including the Toronto Stock Exchange, the TSX Venture Exchange and the Alpha Exchange. No person or company is required to obtain products or services from TMX Group or its affiliates as a condition of any such dealer supplying or continuing to supply a product or service. Canadian Residents NBF or its affiliates may engage in any trading strategies described herein for their own account or on a discretionary basis on behalf of certain clients and as market conditions change, may amend or change investment strategy including full and complete divestment. The trading interests of NBF and its affiliates may also be contrary to any opinions expressed in this Report. NBF or its affiliates often act as financial advisor, agent or underwriter for certain issuers mentioned herein and may receive remuneration for its services. As well NBF and its affiliates and/or their officers, directors, representatives, associates, may have a position in the securities mentioned herein and may make purchases and/or sales of these securities from time to time in the open market or otherwise. NBF and its affiliates may make a market in securities mentioned in this Report. This Report may not be independent of the proprietary interests of NBF and its affiliates. This Report is not considered a research product under Canadian law and regulation, and consequently is not governed by Canadian rules applicable to the publication and distribution of research Reports, including relevant restrictions or disclosures required to be included in research Reports. UK Residents This Report is a marketing document. This Report has not been prepared in accordance with EU legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. In respect of the distribution of this Report to UK residents, NBF has approved the contents (including, where necessary, for the purposes of Section 21(1) of the Financial Services and Markets Act 2000). This Report is for information purposes only and does not constitute a personal recommendation, or investment, legal or tax advice. NBF and/or its parent and/or any companies within or affiliates of the National Bank of Canada group and/or any of their directors, officers and employees may have or may have had interests or long or short positions in, and may at any time make purchases and/or sales as principal or agent, or may act or may have acted as market maker in the relevant investments or related investments discussed in this Report, or may act or have acted as investment and/or commercial banker with respect hereto. The value of investments, and the income derived from them, can go down as well as up and you may not get back the amount invested. Past performance is not a guide to future performance. If an investment is denominated in a foreign currency, rates of exchange may have an adverse effect on the value of the investment. Investments which are illiquid may be difficult to sell or realise; it may also be difficult to obtain reliable information about their value or the extent of the risks to which they are exposed. Certain transactions, including those involving futures, swaps, and other derivatives, give rise to substantial risk and are not suitable for all investors. The investments contained in this Report are not available to retail customers and this Report is not for distribution to retail clients (within the meaning of the rules of the Financial Conduct Authority). Persons who are retail clients should not act or rely upon the information in this Report. This Report does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for the securities described herein nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. This information is only for distribution to Eligible Counterparties and Professional Clients in the United Kingdom within the meaning of the rules of the Financial Conduct Authority. NBF is authorised and regulated by the Financial Conduct Authority and has its registered office at 71 Fenchurch Street, London, EC3M 4HD. NBF is not authorised by the Prudential Regulation Authority and the Financial Conduct Authority to accept deposits in the United Kingdom.

Monthly Equity Monitor U.S. Residents With respect to the distribution of this report in the United States of America, National Bank of Canada Financial Inc. (“NBCFI”) which is regulated by the Financial Industry Regulatory Authority (FINRA) and a member of the Securities Investor Protection Corporation (SIPC), an affiliate of NBF, accepts responsibility for its contents, subject to any terms set out above. To make further inquiry related to this report, or to effect any transaction, United States residents should contact their NBCFI registered representative. This report is not a research report and is intended for Major U.S. Institutional Investors only. This report is not subject to U.S. independence and disclosure standards applicable to research reports. HK Residents With respect to the distribution of this report in Hong Kong by NBC Financial Markets Asia Limited (“NBCFMA”)which is licensed by the Securities and Futures Commission (“SFC”) to conduct Type 1 (dealing in securities) and Type 3 (leveraged foreign exchange trading) regulated activities, the contents of this report are solely for informational purposes. It has not been approved by, reviewed by, verified by or filed with any regulator in Hong Kong. Nothing herein is a recommendation, advice, offer or solicitation to buy or sell a product or service, nor an official confirmation of any transaction. None of the products issuers, NBCFMA or its affiliates or other persons or entities named herein are obliged to notify you of changes to any information and none of the foregoing assume any loss suffered by you in reliance of such information. The content of this report may contain information about investment products which are not authorized by SFC for offering to the public in Hong Kong and such information will only be available to, those persons who are Professional Investors (as defined in the Securities and Futures Ordinance of Hong Kong (“SFO”)). If you are in any doubt as to your status you should consult a financial adviser or contact us. This material is not meant to be marketing materials and is not intended for public distribution. Please note that neither this material nor the product referred to is authorized for sale by SFC. Please refer to product prospectus for full details. There may be conflicts of interest relating to NBCFMA or its affiliates’ businesses. These activities and interests include potential multiple advisory, transactional and financial and other interests in securities and instruments that may be purchased or sold by NBCFMA or its affiliates, or in other investment vehicles which are managed by NBCFMA or its affiliates that may purchase or sell such securities and instruments. No other entity within the National Bank of Canada group, including National Bank of Canada and National Bank Financial Inc, is licensed or registered with the SFC. Accordingly, such entities and their employees are not permitted and do not intend to: (i) carry on a business in any regulated activity in Hong Kong; (ii) hold themselves out as carrying on a business in any regulated activity in Hong Kong; or (iii) actively market their services to the Hong Kong public. Copyright This Report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information, opinions or conclusions contained in it be referred to without in each case the prior express written consent of NBF.

You can also read