ESG Investing: A review - Søren Hvidkjaer Head of Department, Professor of Finance, CBS - Finsif

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ESG Investing:

A review

Søren Hvidkjær

Head of Department, Professor of Finance, CBSFocus of the Report

- and a roadmap

How do ESG strategies affect investor’s risk-

adjusted return?

– Theoretical foundation

– Classification of CSR/ESG studies

– Evidence:

• Sin stocks: Negative sector screening

• ESG ratings: Positive/negative screening

• Event studies

• Active ownership

• A meta study

– Conclusion and implication of the results

Søren Hvidkjær – Nordic SIF 19th September 2017 2Theoretical considerations for the ESG

investor

• For an equity investor who

– does not possess insider information and

– does not engage in active ownership,

• the central performance question is not whether

ESG initiatives creates value in the firm, but

rather whether the stock price accurately reflects

the value of these initiatives.

Søren Hvidkjær - Nordic SIF 19th September 2017 3Abnormal Returns to ESG Strategies – why?

• Potential drivers of positive return to ESG

1. Underreaction to ESG information

• Evidence of underreaction in other cases

• Evidence of underreaction for intangible information

2. ESG strategies have become more common

• Potential drivers of negative return to ESG

1. Demand effect: If a stock is ignored by many

investors, the price falls which implies higher

future expected return

2. Companies e.g. in the tobacco industry have

incentives to practice conservative accounting

Søren Hvidkjær - Nordic SIF 19th September

4

2017Abnormal Returns to ESG Strategies?

• Demand effect depends on

– How widespread are ESG strategies

– Slope of demand curve for stocks

• Depends on arbitrage activity

• ESG strategies can lead to a lack of diversification

– More relevant for sector exclusions than single-

stock exclusions

• ESG strategies can be costly

– Especially relevant for passive investors

Søren Hvidkjær - Nordic SIF 19th September

5

2017Corporate Governance and Active

Ownership

• Potential principal-agent problems

– Underinvestment in ESG initiatives:

• Management has short horizon (myopic) e.g. because

of career considerations.

– Overinvestment in ESG initiatives:

• Management’s social preferences are paid by the

shareholders

• Management uses stakeholder arguments for their own

gain.

• Corporate governance initiatives and active

ownership can help resolve P-A problems

Søren Hvidkjær - Nordic SIF 19th September

6

2017Studies of Financial Effects of CSR/ESG

Classification:

1. Risk-adjusted abnormal returns to ESG portfolios

2. Event studies of market reaction to ESG events

3. Relationship between ESG/CSR and accounting-

based performance measures e.g. ROA

4. Relationship between ESG/CSR and the ex ante

cost of capital to firms

Søren Hvidkjær - Nordic SIF 19th September

7

2017Evidence of Abnormal Returns for sin

stocks: Selected studies

Study Period Market Method Alpha p.a.

Hong and 1926- USA Equal weighted, FF 1-4 3-4%

Kacperczyk (2009, 2006 factor model relative to

JFE, ABS 4* F) similar stocks

Fabozzi, Ma and 1970- 21 Equal weighted, 1-factor 8-12%

Oliphant (2008, 2007 countries

JPM, ABS 2 F)

Trinks and 1991- 94 Value weighted, FF global 8-13%

Scholtens (2017, 2012 countries 4-factor (misspecification)

JBusEth, ABS 3 NF)

Hoepner and 2001- Stocks Value- and equal weighted, 3-4%

Schopohl (2016, 2015 excl. in FF 1 and 4-factor

JBusEth, ABS 3 NF) GPFG/AP

ABS rating explained p. 10 in the report. High to Low rank: 4*, 4, 3, 2, 1

Søren Hvidkjær - Nordic SIF 19th September

8

2017The Portfolio: Equal or Value Weighted?

Adamsson and Hoepner (2015) criticize Hong and

Kacperczyk for equal weighting:

– HK regress an equal- weighted portfolio of sin stocks

on a value-weighted market benchmark. This implies

that the outperformance could be driven by a small

cap performance bias rather than sin stocks

characteristics […]. This argument is founded on the

empirical observation that small stocks outperform

large stocks […]. The exceptionally good performance

could hence be due to an over-weighting of small cap

stocks and underweighting of large cap stocks.

Søren Hvidkjær - Nordic SIF 19th September

9

2017Hoepner-Schopohl

Hoepner and Schopohl’s presentation of results:

– We conduct a time-series analysis of the

performance implications of the exclusion

decisions of two leading Nordic investors,

Norway’s Government Pension Fund-Global

(GPFG) and Sweden’s AP-funds. We find that their

portfolios of excluded companies do not generate

an abnormal return relative to the funds’

benchmark index.

Søren Hvidkjær - Nordic SIF 19th September

10

2017Hoepner-Schopohl table 3

AP7 AP1–4 GPFG

Equal Value Equal Value Equal Value

(1) (2) (3) (4) (5) (6)

Panel A: CAPM model

1-factor 0.450*** 0.286* 0.373 0.346 0.425* 0.364

Alpha (2.63) (1.83) (1.19) (1.13) (1.65) (1.62)

Obs. 166 166 109 109 162 162

Adj. R2 0.83 0.77 0.73 0.39 0.67 0.59

Panel B: four -factor model

4-factor 0.361** 0.204 0.519* 0.345 0.373 0.292

Alpha (2.04) (1.23) (1.71) (1.19) (1.28) (1.17)

Adj. R2 0.85 0.78 0.76 0.47 0.67 0.60

Monthly returns. *, ** and *** indicates significance at 10, 5, and 1% level.

Søren Hvidkjær - Nordic SIF 19th September

11

2017Hoepner-Schopohl Portfolios

70

GPFG

60

AP1–4

AP7

50

No of Stocks

40

30

20

10

0

2001 2002 2003 2004 2005

Søren2006

Hvidkjær2007

- Nordic2008 2009

SIF 19th 2010 2011 2012 2013 2014 2015

September

12

2017ESG rating and Stock Returns

Borgers et al. (2013, JEF, ABS 3 F): Stocks with high ESG rating

outperformed stocks with low rating, but not in 2004-9.

Halbritter and Dorfleitner (2015, RFE, ABS 1 F/NF) confirm this and find

no return differences when extending to 2012, while Larsen (2016, F/I,

ABS 0) finds a difference from 2012-2016 in raw returns.

Søren Hvidkjær - Nordic SIF 19th September

13

2017Did the Market Underreact to ESG?

• Borgers et al show high returns for stocks with

high ESG rating around earnings announcements

in 1992-2004, but not in 2004-09

• Consistent with underreaction in the first period

followed by correct pricing in the second period.

Søren Hvidkjær - Nordic SIF 19th September

14

2017E, S or G?

Environmental Evidence

• Limited environmental evidence:

– Studies based on ratings from Innovest use very

short period

– Studies based on KLD show inconsistent results

Søren Hvidkjær - Nordic SIF 19th September

15

2017E, S or G?

Social: Employee Satisfaction

Study Period Market Data/Method Alpha p.a.

Edmans 1984-2009 U.S. large cap Value weighted 2,1-3,5%

(2011, JFE “100 best returns subtracted

ABS 4* F) companies to from comparable Return

work for in stocks (size and difference up

America” market/book equity); to 4 years after

Then FF 4-factor formation

• Underreaction to intangible information:

– Realized profit higher than analysts long term estimates

– However not abnormal returns around earnings

announcement

• Kempf-Osthoff (2005) and Statman-Glushkov (2009) report

evidence based on KLD scores consistent with Edmans

Søren Hvidkjær - Nordic SIF 19th September

16

2017E, S or G?

Governance Evidence

• What is corporate governance

– shareholder or stakeholder perspective

Study Period Market Data/Method Alpha p.a.

Bebchuk, Cohen 1990-99 USA G- and E-index Significant:

and Wang (2013, equal- and value weighted 6-14%

JFE, ABS 4* F) FF 1-4 factor

2000-08 Insignificant

Auer (2016, 2004-12 Europa Sustainalytics ratings (Did the Market Underreact to G?

• Bebchuk-Cohen-Wang show high returns to

highly ESG rated stocks around earnings

announcements in 1990-99, but not in 2000-08.

– Consistent with underreaction in the first period

and correct pricing in the second.

Søren Hvidkjær - Nordic SIF 19th September

18

2017Event studies

• How does the market react to ESG

initiatives/incidents?

Study Sample Event return

Fisher-Vanden and 117 events in 1993-2008: • EPA CL: -1% event return–

Thorburn (2011, • EPA Climate leaders equivalent to $3bn on average

JEEM, ABS 3 NF) • Ceres • Ceres: 0% event return

Krüger (2015, JFE, 2,116 events in 2001-07 • Neg. events have neg. return

ABS 4* F) from KLD • Pos. events have -/0 return

Flammer (2013, 273 WSJ articles in 1980- • Eco-harmful: Neg. return

AMJ, ABS 4* NF) 2009 classified as eco- • Eco-friendly: Pos. return

harmful or eco-friendly

Søren Hvidkjær - Nordic SIF 19th September

19

2017Event Example in Flammer (2013)

• WSJ 14/2 1991: Exxon Appears to Be Close to

Settling Valdez Suits for Less Than $1 Billion

– "It is our opinion that a $650 million settlement is

a severe undervaluation of the natural resources

damage caused by the oil spill, and that if this deal

goes through, the state and federal governments

have been severely outdealed by Exxon," said Mr.

Miller.

• Eco-friendly or eco-harmful news?

Søren Hvidkjær - Nordic SIF 19th September

20

2017Event: Interaction with G

Study Result

Fisher-Vanden and Companies with low governance (G-index):

Thorburn (2011, • Higher probability of participating in EPA CL

JEEM, ABS 3 NF) • More negative event return

Krüger (2015, JFE, Companies with low gearing and lots of liquidity (free

ABS 4* F) cash flow theory, Jensen 1986)

• More negative return to positive ESG initiatives

Søren Hvidkjær - Nordic SIF 19th September

21

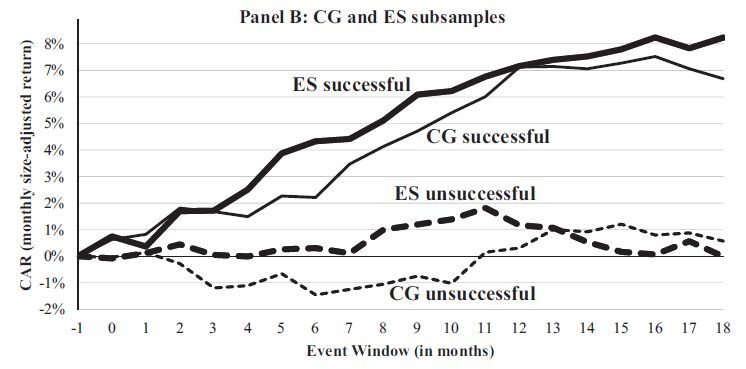

2017Active Ownership

• Potential principal-agent problems create an

opportunity for active ownership to create value

Study Sample Event return

Dimson, Karakas and 382 successful and • Success – over the following year

Li (RFS, 2015, ABS 4* 1,770 unsuccessful • 1-year abnormal ret. of 7%

F) engagements in 1999- • Higher ROA

2009 for a large ESG • More ESG investors

investor • Unsuccessful: No effect

Søren Hvidkjær - Nordic SIF 19th September

22

2017Active Ownership

Both ES and G initiatives are value creating if successful

Dimson, Karakas and Li (2015)

Søren Hvidkjær - Nordic SIF 19th September

23

2017A Meta-/Vote Count Study

• Friede, Busch and Bassen (2015, JSusFinInv, ABS

0) review meta studies of 2200 underlying

studies. They report:

– “large majority of studies reports positive

findings” between ESG and financial performance

– “the results show that the business case for ESG

investing is empirically very well founded.”

• Some reasons to be skeptical …

Søren Hvidkjær - Nordic SIF 19th September

24

2017A Meta-/Vote Count Study

• Evidence of bias in the underlying studies and

especially in the review studies.

– As an example Clark, Feiner and Viehs (2015) finds

a positive connection in 94 out of 110 studies, but

some of the classifications

• are wrong – Fisher-Vanden and Thorburn (2011)

• are due to simple cash flow effects – Krüger (2015),

Capelle-Blancard and Laguna (2010)

• double counts studies – Edmans (2011, 2012), CG

studies

Søren Hvidkjær - Nordic SIF 19th September

25

2017A Meta-/Vote Count Study

• Lots of studies shows correlation between ESG and

accounting performance measures such as ROA

– but the relevant question for an investor is if the

market has already incorporated this into the stock

price

• It is notoriously difficult to conclude causality from

correlation, especially with accounting performance

measures

– the causality question is usually ignored in the CSR

literature

Søren Hvidkjær - Nordic SIF 19th September

26

2017A Meta-/Vote Count Study

• Friede, Busch and Bassen conclude that they

– “clearly find evidence for the business case for ESG

investing. This finding contrasts with the common

perception among investors. The contrary perception

of investors may be biased due to findings of portfolio

studies, which exhibit, on average, a neutral/mixed

ESG–CFP performance relation.”

• However, compared to FBB, investors might in fact

better understand that what matters in the ”business

case” for ESG investing are indeed the results from

the portfolio studies.

Søren Hvidkjær - Nordic SIF 19th September

27

2017Conclusion and Implications 1/4

• Substantial evidence of sin stocks outperforming

– Sector based screening destroys value for

investors/savers

– Conflict of interest especially in pension funds with

mandatory participation

• between the fund manager and the savers

• among savers

– A solution to the conflict of interest requires non-

binary models

– Higher cost of capital is equivalent to a consumption

tax

• except for distribution of revenues

Søren Hvidkjær - Nordic SIF 19th September

28

2017Conclusion and Implications 2/4

• Evidence of high returns to highly ESG rated

stocks: Especially in 1991-2004, not in 2005-2012,

but maybe since 2012

– limited evidence of the E-ratings effect

– portfolios based on social screening (employee

satisfaction) have yielded abnormal returns.

– corporate governance: high return in 1990-99, but

not subsequently

• No evidence that high ratings yield low returns

Søren Hvidkjær - Nordic SIF 19th September

29

2017Conclusion and Implications 3/4

• No evidence of the stock market reacting positive

to ESG/CSR initiatives

– indicates principal-agent problems

– P-A problems can be resolved with good corporate

governance

– interpretation: High ES rating is good if G is high,

but bad if G is low (more research is needed here)

• Value in active ownership

Søren Hvidkjær - Nordic SIF 19th September

30

2017Conclusion and Implications 4/4

• ESG strategies experience strong growth

– historical evidence should be interpreted with

even greater caution

– when profitable strategies become common, the

profit disappears

– This especially applies to simple strategies such as

ESG ratings

– more sophisticated use of ESG information and

active ownership?

Søren Hvidkjær - Nordic SIF 19th September

31

2017You can also read