Evidence Report 6: East Dunbartonshire - Supporting Document for Proposed Local Development Plan 2015 - East ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Supporting Document for Proposed Local Development Plan 2015 East Dunbartonshire Evidence Report 6: Retail Capacity Assessment Strategic Environmental Assessment: Environment Report Action Programme Habitats Regulations Appraisal Equality Impact Assessment Policy Background Reports Evidence Report 1: Addressing Housing Need and Demand in East Dunbartonshire Evidence Report 2: Housing Land Audit 2014 Evidence Report 3: Site Assessments Evidence Report 4: Campsie Fells Statement of Importance Evidence Report 5: Kilpatrick Hills Statement of Importance Evidence Report 6: Retail Capacity Assessment Evidence Report 7: Wind Energy Framework

and

Roderick MacLean Associates Ltd

EAST DUNBARTONSHIRE COUNCIL

EAST DUNBARTONSHIRE RETAIL

CAPACITY ASSESSMENT

AMENDED VERSION

August 2014

East Dunbartonshire Council Retail Capacity Assessment

Contents

1.0 Introduction

2.0 Planning Policy Framework

3.0 Retail Market Overview

4.0 Retail Catchment Areas & Populations

5.0 Household Survey

6.0 Convenience Expenditure & Turnover

7.0 Spare Convenience Expenditure Capacity

8.0 Comparison Expenditure & Turnover

9.0 Spare Comparison Expenditure Capacity

10.0 Conclusions

Appendices

Appendix 1: Household survey questions

Appendix 2: Convenience shopping patterns – household survey

Appendix 3: Convenience expenditure inflows from beyond East

Dunbartonshire

Appendix 4: Comparison shopping patterns - household survey

Appendix 5: Comparison expenditure inflows from beyond East

Dunbartonshire

Appendix 6: Strathkelvin Retail Park

Page 2 of 68

East Dunbartonshire Council Retail Capacity Assessment

1.0 INTRODUCTION

1.1 Ryden and Roderick MacLean Associates were instructed by East

Dunbartonshire Council (EDC) in August 2013 to undertake a Retail

Capacity Assessment for East Dunbartonshire. The retail capacity

assessment is required to inform the emerging Local Development Plan

(LDP) town centre and retail policy options.

1.2 There have been considerable changes within the retail sector, at a

national and local level since the last retail capacity study was undertaken

in 2008 (and published in 2009). That study identified limited capacity for

further convenience retailing and a larger requirement for comparison retail

floorspace and bulky goods in particular, which if satisfied would allow the

catchment to compete with centres in the surrounding area.

1.3 This report provides an up-to-date retail assessment of the need for

additional convenience and comparison retail floorspace during the

emerging LDP period (2016-2021) and establishes a benchmark against

which the impact of retail proposals contrary to the LDP can be assessed in

the future. This version of the report amends the version dated February

2014 to include a non-food retail consent in Milngavie.

Study Area

1.4 The study area, East Dunbartonshire, is located to the north of Glasgow

and bounded by the Campsie Fells and Kilpatrick Hills. It covers an area of

20,172 ha with an estimated population of 105,192 (as at 2011). The main

settlements are Bearsden, Milgavie, Kirkintilloch and Bishopbriggs and

these form the principal focus of the study.

Page 3 of 68

East Dunbartonshire Council Retail Capacity Assessment

Figure 1: East Dunbartonshire Council Area

Source: East Dunbartonshire Council

1.5 Following this introductory chapter the report is structured as follows:

Chapter 2 - Planning Policy Framework

Chapter 3 - Retail Market Overview

Chapter 4 - Retail Catchment Areas & Populations

Chapter 5 - Household Survey

Chapter 6 - Convenience Expenditure & Turnover

Chapter 7 - Spare Convenience Expenditure Capacity

Chapter 8 - Comparison Expenditure & Turnover

Chapter 9 - Spare Comparison Expenditure Capacity

Chapter 10 - Conclusions

Page 4 of 68

East Dunbartonshire Council Retail Capacity Assessment

2.0 Planning Policy Framework

Scottish Planning Policy

2.1 The most recent version of the SPP was published in June 2014. The main

change in emphasis compared to the 2010 version is the greater focus on

encouraging the diversity of uses and vitality within town centres generally,

alongside support for improvement to the quality of the centres as places to

live and work.

2.2 The ‘Town Centres First’ policy is promoted in the 2014 SPP, when

planning for uses which attract significant numbers of people, including

retail, commercial and leisure uses, offices, community and cultural

facilities. Plans should identify a network of centres (city centres, town

centres, local centres and commercial centres), explaining how they

interrelate. Health checks of town centres should be undertaken regularly

to assess their vitality and viability and strengths/ weaknesses. These

checks should be used to develop town centre strategies.

2.3 Development plans should adopt the sequential approach to preferred

locations for uses which generate significant footfall, including retailing and

other uses, in the following order of preference:

Town centres

Edge of town centres

Other commercial centres

Out of centre locations that are readily accessible by a choice of

transport.

2.4 Out of centre locations should only be considered where the town centre/

edge of centre and commercial centre options are unavailable or do not

exist, together with meeting other criteria specified in the SPP.

Development Plan

2.5 The development plan for East Dunbartonshire is made up of two parts, the

strategic development plan (SDP) - Glasgow & Clyde Valley Strategic

Development Plan (2012) and the Local Plan - East Dunbartonshire Local

Plan 2 (Adopted 31 October 2011).

2.6 The SDP is a high level document which sets out the spatial vision and

related strategic development strategy for the Glasgow city-region, up to

2035. It provides the geographical framework for local authorities to

produce their local development plans and assess planning applications.

2.7 Background Report 14 of the SDP ‘Network of Strategic Centres’ provides

the context for retailing within the city-region. This network is identified as

Page 5 of 68

East Dunbartonshire Council Retail Capacity Assessment

a hierarchy of the city centre, strategic centres and other centres and is

based on “retail offer and local strategic significance”. The intention is to

protect centres from further decline caused by a trend towards out of centre

locations driven by retailers demand for modern and larger floorplates.

2.8 Glasgow city centre sits at the top of the network hierarchy due to its

dominance in the city-region and wider area. The twenty three strategic

centres below fall into two categories – those with an important retail

function and those with a strategic function within the local authority area.

Kirkintilloch falls into the latter due to the role of its historic town centre as a

civic and cultural centre and is the only East Dunbartonshire town to be

included.

2.9 Following on from the SDP, local development plan policies should reflect

the need to ‘safeguard and promote’ the network of centres based on their

specific role and function. The relevant local policies for East

Dunbartonshire are outlined below.

2.10 East Dunbartonshire Local Plan 2 was adopted 31 October 2011 and

provides the land use framework for the East Dunbartonshire area. This

sets out the policies for the town centres, namely Milngavie, Bearsden,

Bishopbriggs and Kirkintilloch to “maintain and improve their attractiveness

as shopping and visitor destinations and to maintain and, where

appropriate, recover market share and improve centre vitality and viability”.

2.11 The local plan policies therefore seek to protect and enhance the retail

offering in the town centres, increase residential use and improve

accessibility.

2.12 East Dunbartonshire Council is preparing a new Local Development Plan

for the area which will replace the East Dunbartonshire Local Plan 2. This

is currently at the Main Issues stage and the new LDP is expected to be

completed in 2016. This study will help to inform the emerging LDP retail

planning policies.

Page 6 of 68

East Dunbartonshire Council Retail Capacity Assessment

3.0 Retail Market Overview

Retailing in Scotland

3.1 Two major trends have been affecting the retail and leisure sector: market

concentration in larger destinations at the expense of smaller locations, and

pressure on consumer expenditure as price inflation outstrips earnings

growth. The market response is very selective new investment by

successful retailers, against a wider background of failures and

rationalisations among less successful businesses. Much of the market is

now polarised between well-occupied prime destinations and weaker

locations where trade and retailer demand are much more fragile.

3.2 According to the Scottish Retail Consortium (SRC)/KPMG, sales in

Scotland during December 2013 were 1.1% higher than December 2012.

However, like-for-like sales (which discount the impact of store openings,

closures and expansions in order to measure performance across the retail

sector) decreased by 2.9% over the same period.

3.3 SRC reports that shop price deflation is having an impact upon the values

of sales and, in real terms, sales in December decreased by 0.3%. Both

food and non-food sales were lower, at 0.3% and 1.7% respectively, than

the previous December. Wages rates have not increased at the same

rates as inflation resulting in subdued consumer spending.

3.4 Trading conditions have been difficult for many retailers. 2012 was the

worst year for retailers failing since 2008. In 2013, a number of major

retailers such as Comet, Blockbusters and Jessops collapsed. Other

struggling retailers such as Dreams and HMV have been saved, either in

whole or part, after being purchased by restructuring specialists.

3.5 Value retailers, for example B & M, Poundworld, Home Bargains and

Poundland, are still expanding and actively looking for new sites. In

general however, although national multiple retailers do have property

requirements, these are very specific in terms of location and property type.

3.6 In the food sector, the most active sub-sector is the local convenience store

market, as the big four food retailers jostle for position and market share.

There are around 49,000 convenience stores in the UK but branded

grocery chains account for less than 10%. Tesco, Co-op and Sainsbury’s

are all active with Morrisons having a requirement for 300 outlets for their

‘M’ Store concept to complement their supermarkets, and have acquired

forty-nine Blockbuster stores and seven former Jessops units.

Page 7 of 68

East Dunbartonshire Council Retail Capacity Assessment

3.7 At the opposite end of the convenience store sector it is clear that the race

for space by major superstores in waning. Interest in such sites is now

highly selective and retailers are now concentrating more on effective use

of existing stores, multi-channel sales and small local outlets as mentioned

previously. There is still selective demand for large stores, but typically

4,000 – 6,000 sq m rather than up to 10,000 sq m as had been the case

until recently.

On-line Retailing

3.8 Internet spending is a fast growing part of retail expenditure. It is the main

element of special forms of trading (SFT), which also includes mail order,

telephone sales and markets, all of which are forms of non-store retail

expenditure. It reduces the expenditure available to service conventional

1

shop floorspace. Experian forecast that non-store comparison retail sales

could rise to 20.9% of total comparison spending by 2021, with little

increase beyond that, as growth tapers off. This forecast is mainly driven

by online sales.

3.9 Experian explain that part of this proportion is associated with shop

floorspace (‘click and collect’ for example), so the forecast deduction from

total comparison expenditure relating to shop floorspace should be around

15.7% at 2021, for the purpose of assessing future space requirements.

For convenience retail sales, the equivalent proportions for 2021 are 15.2%

of total convenience spending and a 4.6% reduction in floorspace, where

the big difference is probably mainly accounted for by home delivery from

existing supermarket shelves. Increased home delivery from warehouses,

for both convenience and comparison goods, will continue to affect the

requirements for conventional retail floorspace. See also sections 6 and 8.

3.10 Many major multiples now offer both online and store-based shopping with

the latter providing an essential platform for viewing the goods before

online purchases are made. This multi-channel retailing allows retailers to

provide ‘click and collect’ services attracting shoppers into high street

shops to pick up and return goods. There is, therefore, still a requirement

for physical space from such retailers.

2

3.11 The British Retail Consortium reports that internet non-food sales in

December 2013 were 19.2% higher than December 2012. Technology,

through the increased use of smartphones and tablets, has contributed to

this growth. However, it is worth noting that technology companies with a

retail offering recognise the importance of a high street presence

1

Experian Retail Planner- Briefing Note 11, Appendix 3.

2

BRC-KPMG Online Retail Sales Monitor December 2013

Page 8 of 68

East Dunbartonshire Council Retail Capacity Assessment

demonstrated, for example, by the Apple stores now found in prime

shopping destinations.

3.12 Independent retailers are increasingly offering online shopping too and this

can prove very successful for niche and specialist shops. For many small

independent retailers though, online shopping poses direct competition,

which can only be met by improved quality of offer.

Glasgow retail market

3.13 Glasgow sits at the top of the retail hierarchy and is situated around four

miles from the East Dunbartonshire Council area boundary. It remains the

second most popular retail destination in the UK after London and also

ranks second in terms of turnover. The city continues to stay ahead of

competing centres for new retail requirements. Buchanan Street is

Scotland’s prime retail destination, achieving prime rents of around £260

per sq ft Zone A and is complemented to the south by St Enoch Centre,

which recently changed ownership. The stable rental position in Glasgow

illustrates starkly the point about market polarisation; in the wider market

rents across Scotland’s top twenty retail centres have fallen by around 30%

since the start of the recession as shown in the Ryden Retail Index below

(Figure 2).

Figure 2: Ryden Retail Rental Index

3.14 As can been seen in Figure 2, rents have stabilised in 2013 but remain

19% below the 2007 peak, excluding the effects of price inflations. Many

occupiers are now trading at rents considerably in excess of current values.

This is compounded by non-domestic rates which often are not reflective of

Page 9 of 68East Dunbartonshire Council Retail Capacity Assessment

the letting market, and indeed can make units uneconomic even on

reduced rents.

3.15 Glasgow continues to stay ahead of competing centres for new retail

requirements demonstrated by the opening of Scotland’s first Forever 21

store within Land Securities’ £70 million Buchanan Quarter development in

March 2013. Land Securities has further development planned with

planning in principle consent having been secured for an extension to

Buchanan Galleries for a £300 million retail and leisure scheme. This is

expected to double the volume of retail space and provide restaurants, a

cinema and a car park. Marks and Spencer has been signed up as an

anchor tenant in a new 13,935 sq m store.

3.16 Outside the city centre, Hammerson has commenced development of its

10,700 sq m extension to Silverburn Shopping Centre comprising a 14-

screen cinema, nine restaurants and bingo hall. This follows the recent

completion of a leisure extension at the Glasgow Fort, 4,180 sq m in size,

accommodating a Vue multiplex cinema and restaurant space let to TGI

Friday’s, Prezzo, Harvester, Chiquito and Pizza Express.

3.17 In Renfrewshire, on the outskirts of Glasgow, Intu Properties has plans to

expand Braehead Shopping Centre at the cost of £200 million. This will

include a new ice skating arena, sports facilities and a 200-bedroom hotel.

3.18 Investment activity within the retail property market has been supressed

due to the continuing challenges faced by the retail sector. There is

demand for prime retail assets within the major city centres as

demonstrated by the recent purchase of 123-129 Buchanan Street, a mixed

use retail and office block, by Scottish Widows Investment Partnership for

£22.85 million. This particular deal achieved a yield of 5%, and other

recent and on-going deals across Aberdeen, Edinburgh and Glasgow have

also achieved 5% or below, despite cautious rental growth predictions

within the retail sector. Buyers are taking the opportunity to secure trophy

assets which offer scarcity and therefore viewed as easy to sell on if

required.

3.19 Secondary and tertiary locations, by contrast, are heavily discounted both

in historic terms and compared to prime locations. Yields are varied, even

for retail units in the same pitch, once factors like income security, lease

length and occupier demand are factored in.

3.20 In summary, the overall picture is of a gradually improving retail market, in

line with the wider economy, although sales are volatile month-to-month

and growth is not strong. Major malls are attracting new development but

for the large majority of towns the priority will be to stabilise occupancy

levels then gradually reduce vacancies, including some diversification away

Page 10 of 68East Dunbartonshire Council Retail Capacity Assessment

from retail and probably involving new leisure operators. Investment has

been focused mainly on prime retail locations.

East Dunbartonshire Retail Locations

3.21 The main retail locations within East Dunbartonshire are the town centres

of Bearsden, Bishopbriggs, Milngavie and Kirkintilloch, and Strathkelvin

Retail Park in Bishopbriggs. These are considered individually in further

detail below.

3.22 Bearsden has a range of retail brands represented within the town centre.

These include a few national retailers such as Optical Express, Barrhead

Travel, Majestic Wine Warehouse, McDonalds, Farmfoods, Vets 4 Pets

and M&S Simply Food as well as a selection of independent retailers

including Sinclair Pharmacy, Whiz Kids, Golfing House, Quartz Travel and

Cutting Edge Hair Design.

Figure 3: Bearsden Cross

3.23 Current Scottish Assessor Association data reports a total of 124 retail

properties in Bearsden with only five vacant units, giving a vacancy rate of

only 4%.

3.24 Supermarket provision with Bearsden consists of:

Asda at Milngavie Road,

Page 11 of 68East Dunbartonshire Council Retail Capacity Assessment

M & S Simply Food on Drymen Road,

Lidl at Baljaffray Shopping Centre,

Scotmid on Ledi Drive

Co-operative Food Store on Station Road.

3.25 The prime retail pitch in Bearsden is the area known as ‘The Cross’ where

Drymen Road and Roman Road meet and includes New Kirk Road.

3.26 Bishopbriggs town centre contains a number of retail brands, including

national chains - Boots, Greggs, Superdrug, Subway and Timpson, as well

as a range of independent retailers (including M & M Eyecare, Estetica,

Thomas Auld & Sons and Glamour Eyes), and retail services including

restaurants, cafes and financial and professional services.

Figure 4: Bishopbriggs Town Centre

3.27 Supermarkets in the town are Morrison’s (who purchased the Triangle

Shopping Centre in August 2012 and are progressing with plans to

redevelop/build a new store), Tesco Express and Asda both on Kirkintilloch

Road.

3.28 The prime retail pitch in Bishopbriggs’ town centre is the Triangle Shopping

Centre and Kirkintilloch Road.

3.29 Strathkelvin Retail Park, by Bishopbriggs, is owned by Caledonian Property

Investments and it has over 24,600 sq m of gross comparison good

retailing space.totals 29,100 sq.m. The retailers located here are listed in

Appendix 6.

Figure 5: Strathkelvin Retail Park

Page 12 of 68East Dunbartonshire Council Retail Capacity Assessment

3.30 Scottish Assessor Association data reports a total of 98 retail properties in

Bishopbriggs with no vacant units.

3.31 Kirkintilloch has a diverse range of retail brands represented in the town

centre. These include market staples such as Optical Express, Boots,

Poundland, WH Smith, Superdrug, Greggs and Shoe Zone, as well as a

wide range of independent retailers (including Sugar Plum, Sun Shack,

Cards Direct, Nysa Notions and Bargain Central), along with non-retail

services including restaurants, cafes and financial and professional

services.

Figure 6: Kirkintilloch Town Centre

3.32 Supermarket provision in the town comprises a Tesco Metro in the Regent

Shopping Centre, a Sainsbury’s on Shamrock Street, and Scotmid on

Gallowhill Road. Lidl has recently opened a store on the former bus depot

site on Milton Road in November 2013.

3.33 Scottish Assessor Association data reports a total of 189 retail properties in

Kirkintilloch with 11 vacant units, giving a vacancy rate of only 6%.

3.34 The prime retail pitch in Kirkintilloch is Cowgate, where the Regent

Shopping Centre is also located. The Regent Centre was built in 1991 and

comprises 21 retail units and a 3,012 sq m supermarket (Tesco).

3.35 Milngavie also has a selection of retail brands represented in the town

centre. These include market staples such as M&S Simply Food, Boots, M

& CO, Greggs, Costa Coffee, Optical Express, Specsavers, Iceland and

Poundstretcher, as well as a wide range of independent retailers (including

Page 13 of 68East Dunbartonshire Council Retail Capacity Assessment

Reids of Milngavie, Lingerie Boutique, Fantoosh Fish, Ruby Red, Foils and

Milngavie Bookshop).

Figure 7: Milngavie Town Centre

3.36 Supermarkets in Milngavie consist of:

Scotmid on South Mains Road,

Tesco at Gavin’s Mill (which has recently been refurbished after

plans to build a Tesco Extra store in the town were shelved in June

2013,

From 2014, Waitrose will have a presence with a new store to open

just off the Burnbrae roundabout.

3.37 Scottish Assessor Association data reports a total of 79 retail properties in

Milngavie with only one vacant unit, giving a vacancy rate of only 1%.

3.38 The prime retail pitches in Milngavie town centre are Main Street and

Station Road.

Market Activity

3.39 There are currently five units on the market in Bearsden totalling 272 sq m.

Bishopbriggs has eight units totalling 7,690 sq m available (of this 6,819 sq

m is part of the redevelopment of the B&Q unit at Strathkelvin Retail Park).

Kirkintilloch has 17 retail properties, totalling 3,378 sq m, on the market,

and Milngavie has one unit totalling 59 sq m currently available. This is

depicted in Figure 8 below:

Page 14 of 68East Dunbartonshire Council Retail Capacity Assessment

Figure 8: Retail Availability

Source: CoStar

3.40 Table 1 identifies notable recent openings and closures of retail outlets in

the East Dunbartonshire area. In common with other towns, town centres

may be losing some multiple retailers and closures such as Comet,

Peacocks and Thomas Cook are not specific to East Dunbartonshire but

are national retailer failures affecting many locations. It was recently

announced that Nike has taken 929 sq m of retail space at Strathkelvin

Retail Park, making the Park fully let.

Table 1: Retail openings and closures

Town Location Retailer Date

Openings

Bishopbriggs Strathkelvin Retail Iceland Jun 2012

Park Next Dec 2011

Frankie & Benny’s Aug 2011

Bearsden Hillfoot Road Vets 4 Pets Spring 2012

Station Road Co-operative Food October 2011

Closures

Kirkintilloch Cowgate Happit May 2012

Bishopbriggs Strathkelvin Retail Comet Dec 2012

Park Peacocks Feb 2012

Bearsden Thomas Cook Spring 2013

3.41 Table 2 shows a selection of recent deals from across the Council area. Of

these deals, 6 were in Bearsden, 4 in Bishopbriggs, 5 in Kirkintilloch and 4

in Milngavie.

Page 15 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 2: Recent retail transactions in East Dunbartonshire

Address Size (sq Comments

m)

2 Springfield Road, 58 Let in November 2013 to an undisclosed tenant on a new 10

Bishopbriggs year lease at £15,000 pa (£259 per sq m).

2 Canniesburn Toll, Bearsden 35 Let in October 2013 to Pound Plus (Helensburgh) Ltd on a new

10 year lease at £10,300 pa (£294 per sq m).

67-73 Milgavie Road, 58 Let in October 2013 to Mr Mohammed Iqbal (t/a Shish

Bearsden Tandoori) on a new 25 year lease at £11,500 pa (£198 per sq

m).

35-37 Douglas Street, 40 Let in September 2013 to an undisclosed tenant on a new

Milngavie lease on confidential terms.

1-15 Mugdock Road, 72 Let in September 2013 to Mary Easton ltd (t/a The Dress Shop)

Milngavie on a renewed 10 year lease at £9,625 pa (£134 per sq m).

Units A-F Lomond Drive, 74 Let in July 2013 to Fiona Hardie on a two year sub-lease at

Bishopbriggs £11,000 per annum (£149 per sq m).

161-163 Milngavie Road, 37 Let in July 2013 to Kitchens Direct. Asking rent £14,000 pa.

Bearsden

15-19 Cowgate, Kirkintilloch 266 Let in May 2013 to St Margaret of Scotland Hospice at £25,000

pa (£94 per sq m)

157 Kirkintilloch Road, 41 Let in May 2013 to an undisclosed tenant on a ten-year lease

Bishopbriggs at £10,000 pa (£244 per sq m)

Unit 3, 38 Stewart Street, 39 Let in March 2013 to Susan McMahon t/a The Lingerie

Milngavie Boutique on a new five year FRI lease at £10,000 pa (£256 per

sq m)

Unit 4, 38 Stewart Street, 39 Let in March 2013 to Emily Fotheringham t/a Fotheringham on

Milngavie a new five year FRI lease at £10,500 pa (£269 per sq m)

102-166 Drymen Road, 23 Let in January 2013 to Mr G McNab t/a Barbers on a sublease

Bearsden expiring in February 2022 at £11,500 pa ((£500 per sq m).

2-4 Freeland Place, 82 Let in Dec 2012 to Sun Shack. Quoting rent was £10,000 pa

Kirkintilloch

28-30 Cowgate, Kirkintilloch 133 Let in June 2012 to DEBRA on confidential terms

14 Townhead, Kirkintilloch 54 Let in May 2012 to Cash 4 Clothes on confidential terms

165 Milngavie Road, Bearsden 71 Let in March 2012 to Rettie & Co on a ten-year lease at

£15,500 pa (£217 per sq.m.

161-163 Milngavie Road, 37 Let in March 2012 to Liggy’s Cakes on a five-year lease at

Bearsden £10,000 pa (£27 per sq.m.).

1 Hillfoot Drive, Bearsden 200 Let in January 2012 to Vets for Pets. The quoting rent was

£35,000 pa (£175 per sq.m.)

3 Station Road, Bearsden 334 Let in October 2011 to The Co-Operative Group Ltd on a 15-

year lease at £75,000 pa (£224 per sq.m.).

Unit 1C Strathkelvin Retail 929 Let in September 2011 to Next Retail on a 10 year lease at

Park, Bishopbriggs £145,000 pa (£156 per sq.m.).

37 Eastside, Kirkintilloch 46 Let in June 2011 to Desiree on a one-year lease at £6,000 pa

(£130 per sq.m.).

Source : CoStar

3.42 Investment transactions provide one indicator of property market interest

and confidence. Following the property market crash, only six investment

transactions have been recorded in the region since 2010, including those

shown in Table 3 below.

Page 16 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 3: Investment Transactions

Address Size Comments

(sq m)

3 Station Road, Bearsden 334 Sold in February 2012 to a private investor for £1.15m, reflecting a net initial

yield of 6.1%. The property is let to Co-operative Group Food Limited.

56 Drymen Road, 49 Sold in August 2011 to Trygort (2) Ltd for £242,500, reflecting a net initial

Bearsden yield of 6.64%. The property is let to Dignity Funerals Ltd.

54-56 Cowgate, 350 Sold in June 2012 to Gilpak Ltd by a private investor for £416,000, reflecting

Kirkintilloch a net initial yield of 7.91%. The property is let to Lloyds Pharmacy Ltd.

95 Main Street, 44 Sold in April 2010 to Mr R Lovat by Clydesdale Bank plc for £23,500

Lennoxtown

Source: CoStar

Retail Rents

3.43 Retail rents in East Dunbartonshire vary across the town centres as detailed

in the table below:

Table 4: Retail rents in East Dunbartonshire

Town Rent Values (per sq m)

Bearsden £198 to £500

Bishopbriggs £149 to £259

Kirkintilloch £94 - £130

Milngavie £134 - £269

Source: CoStar

Retailer Requirements

3.44 Retailer requirements to locate in towns and commercial centres provide an

important indicator of market demand. Since the market downturn in 2008

however, many retailers are no longer actively seeking new premises, or

are being extremely selective. Where retailers are looking for premises,

many simply have blanket requirements covering whole regions rather than

specific requirements for named centres. These factors complicate any

assessment of demand based upon retailer requirements.

3.45 According to one data source which tracks requirements over time

Kirkintilloch had a high of 12 retailer requirements in 2004 and this has

fallen to the current three requirements. Bishopbriggs had a high of 11

retailer requirements in 2006 and this has fallen to none, likewise Bearsden

had highs of 11 retailer requirements in 2006/2007 and this has also fallen

to none.

3.46 A panel of data sources used for this study records a total of 13 different

retail requirements throughout East Dunbartonshire totalling between 2,347

– 6,511 sq.m. Table 5 below shows these requirements.

Page 17 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 5: Retail Requirements

Sector No of Size of Town(s) Pitch

reqs requirement

(sq.m gross.)

Retailers

Household goods 1 209 - 325 Kirkintilloch High Street or shopping centre

Supermarkets 3 900-1,500 Milngavie, Town centre or edge-of-centre

(discounter) 900-1,500 Bearsden,

900-1,500 Kirkintilloch

Total retail 4 2,909-4,825

Non-retail services

Restaurants / café/ 8 1,006 – 1,212 Kirkintilloch Prime or good secondary, corner

site preferred. High Street, parade

bars Bishopbriggs, or edge of town shopping. Close to

Bearsden, retail / business / transport hubs.

Edge of town, in town,out of town.

Milngavie High Street or secondary parade.

Car parts / motor 1 232 - 465 Bearsden Edge of town

factors

Total service 9

3.47 In addition to these retailer requirements in Table 5, there are two fast food

operators looking for franchises throughout the country but with no specific

towns named.

3.48 A further 11 nationwide retailers have requirements (which include non-

specifically named requirements for Scotland). Of these requirements two

are for supermarkets; three are for restaurants / café/ bars; one is for

household goods; one is for clothing, two are for pharmacy/health &

beauty; and two are for discount retailers.

Conclusions

3.49 Slow growth in the retail sector has resulted in development being primarily

restricted to prime locations. With the food sector, the development of

superstores has been declining but there is significant activity within the

convenience store sub-sector.

3.50 Occupancy levels in East Dunbartonshire are high with a diverse range of

brands represented, despite the close proximity to Glasgow. However, the

loss of retailers due to business failures and contracting national multiples

has had an impact on the town centres.

3.51 There have been a number of retail property market transactions

completed across the four towns. The vast majority of this activity has

been occupier related with only a handful of investment deals being

Page 18 of 68East Dunbartonshire Council Retail Capacity Assessment

completed. This reflects the fact that investment activity within the retail

sector is limited outside of prime retail locations such as Glasgow city

centre.

3.52 Letting activity is generally for small units and rental values vary across the

area from a low of £94 per sq m in Kirkintilloch to £500 per sq m in

Bearsden.

3.53 Latent demand from multiple retailers is weak; towns are more likely to

depend upon regional and local retailers, and complementary commercial

uses moving forward into the next LDP period.

Page 19 of 68East Dunbartonshire Council Retail Capacity Assessment

4.0 Retail catchment areas and population

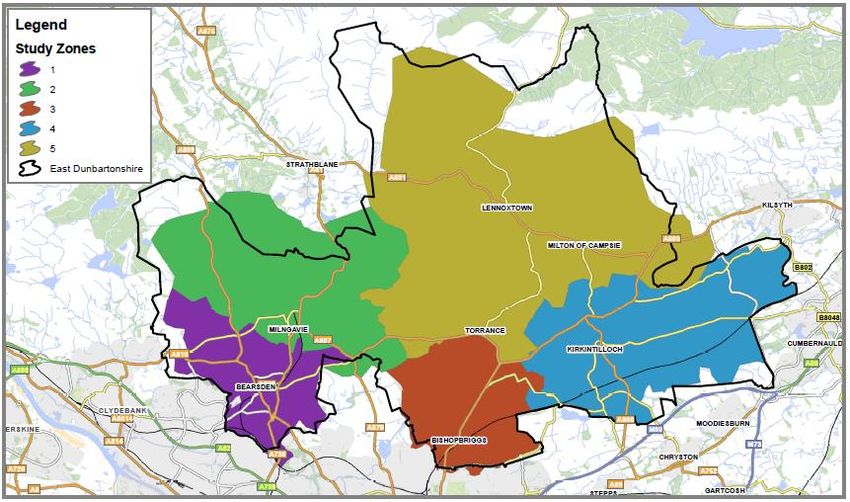

Introduction

4.1 This section shows the study area of East Dunbartonshire, subdivided into

primary retail catchment areas based on the main towns, together with the

current and projected populations of the catchments to 2016 and 2021 in

accordance with the study brief.

Convenience catchment areas and population

4.2 Map 4.1 illustrates the primary catchment areas relating to Bearsden,

Milngavie, Bishopbriggs, Kirkintilloch and the Northern Villages. These are

the same areas as applied in the 2009 Retail Capacity Study. They

comprise groups of postcode sectors which almost match the Council area

boundary, but not exactly (although with the same total population from the

old 2001 Census). Experian show a slight change in the postcode sector

boundaries that extend into the Campsie Hills within the Council area, but

this makes no difference as the extension contains no population. These

five areas are defined as zones in the recent household survey for this

study.

4.3 Table 4.1 shows the current and projected populations of the five

convenience catchment areas, incorporating the 2011 Census findings and

applying the 2010 based population projections by the Registrar General to

2021, as explained in the table footnote. Slight population decline is

projected over the period.

Comparison catchment areas and population

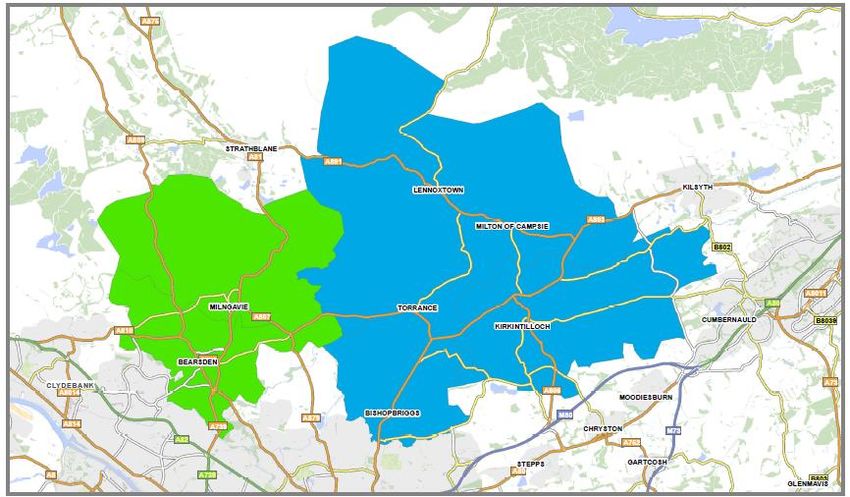

4.4 Map 4.2 illustrates the two primary comparison catchment areas in East

Dunbartonshire from the study brief. These relate to the areas within East

Dunbartonshire defined by the old Structure Plan Technical Report TR7/06

(2006). The two comparison catchment areas include: (1) Bearsden/

Milngavie and (2) Bishopbriggs/ Kirkintilloch/ Northern Villages. The areas

equate to the sum of the relevant convenience catchments. In the 2009

Capacity Study, the analysis of comparison expenditure capacity focussed

on the Council area only.

4.5 Table 4.2 shows the current and projected populations of the two

comparison catchment areas, drawing on the same sources as applied to

the convenience catchment populations.

Page 20 of 68East Dunbartonshire Council Retail Capacity Assessment

Map 4.1 Convenience Retail Catchment Areas (Study Zones)

Page 21 of 68East Dunbartonshire Council Retail Capacity Assessment

Map 4.2 Comparison Retail Catchment Areas (2)

(Bearsden/Milngavie) and (Bishopbriggs/ Kirkintilloch/ Northern Villages)

Page 22 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 4.1 East Dunbartonshire convenience catchment areas: population projections

Catchment areas 2001 ***2011 2013 2016 2021

(survey zones) Census Census based

Zone 1 Bearsden

G61-1,G61-2, G61-3,G61-4 27,967 27,136 27,025 26,803 26,378

Zone 2 Milngavie

G62-6,G62-7,*G62-8 13,846 13,434 13,380 13,270 13,059

Zone 3 Bishopbriggs

G64-1,G64-2,G64-3 23,384 22,689 22,596 22,411 22,055

Zone 4 Kirkintilloch

**G65-9,G66-1,G66-2, 31,424 30,490 30,366 30,116 29,639

G66-3,G66-4,**G66-5

Zone 5 Northern Villages

G64-4,G66-7,G66-8 11,622 11,277 11,231 11,138 10,962

Total survey area 108,243 105,026 104,597 103,738 102,093

Note:

* Postcode Sector G62-8: data included for part in E Dunbartonshire. Part in Stirling Council area is negligible

** Postcode Sector G65-9: data included for part in E Dunbartonshire (Tw echar) and G66-5- part in E Dunbartonshire only.

***Population change from 2001 to 2011 based on the recent Census 2011 release for E Dunbartonshire

2,001 2,011 2,013 2,016 2,021

E Dunbartonshire Council Area Census Census

108,243 105,026

RG 2010 based population projections 104,380 103,954 103,100 101,465

Period 2011-13 2013-16 2016-21

Change 0.9959 0.9918 0.9841

Applied to 2011 Census population 104,597 103,738 102,093

Table 4.2 East Dunbartonshire comparison catchment areas: population projections

2001 2011 2013 2016 2021

Catchment areas Census Census based

Bearsden/ Milngavie

(Zones 1 & 2) 41,813 40,570 40,405 40,073 39,437

Bishopbriggs/ Kirkintilloch/

N Villages (Zones 3,4,5) 66,430 64,456 64,193 63,665 62,656

Total survey area 108,243 105,026 104,597 103,738 102,093

Sources: as Table 4.1

Page 23 of 68East Dunbartonshire Council Retail Capacity Assessment

5.0 Household survey

Introduction

5.1 The telephone interview survey (1,000) covered the area embracing the

five zones representing the convenience catchment areas defined on Map

4.1. These zones comprise the groups of postcode sectors shown in Table

4.1, together with their populations.

5.2 Appendix 1 contains a list of the questions asked by the structured

questionnaire, together with the interview quotas by zone, which were in

proportion to the population of each zone. Interviews were conducted by

randomly generated selection of telephone numbers within each zone. The

output tables produced by RMG Clarity Market Research Ltd, together with

the associated questionnaire, are provided as separate documents to

accompany this report.

5.3 The household survey provides the best means of estimating the retail

expenditure flows into, and out of, the catchment areas shown on Maps 4.1

and 4.2, by the residents of East Dunbartonshire.

Survey findings

5.4 The following graphs and commentary refer to the most frequent responses

to the questionnaire on issues relating to shopping patterns. Also included

in the questionnaire are questions on usage and perceptions of the town

centres as places to visit, and questions on the evening economy. These

are available for separate use by the Council, as they are not central to the

retail capacity study.

5.5 For the full list of responses, reference needs to be made to the RMG

Clarity Research tabulations. Furthermore, the percentages shown in the

graphs and script of this report excludes those respondents who said don’t

know/ varies, don’t buy, internet and mail order- since the focus is on the

relative attraction to floorspace in centres/stores. Internet spending on the

different categories of goods is highlighted separately.

Most visited stores for main food shopping

5.6 The most popular superstores and supermarkets for main food shopping

are identified on the graphs overleaf:

Bearsden residents: Asda at Bearsden is the predominant attraction,

followed by Tesco in Milngavie. Morrisons at Crow Road, Glasgow and

M&S in Milngavie are also identified, but in lesser proportions;

Milngavie residents: Tesco in Milngavie is identified by nearly 71% of

the respondents, followed by ASDA at Bearsden;

Page 24 of 68East Dunbartonshire Council Retail Capacity Assessment

Main food shopping and mode of travel

Page 25 of 68East Dunbartonshire Council Retail Capacity Assessment

Bishopbriggs residents: similar proportions (about 40% each), most

often visit Morrisons and Asda at Bishopbriggs. Smaller proportions visit

Asda at Robroyston and Tesco at St Rollox;

Kirkintilloch residents: Tesco and Sainsbury’s at Kirkintilloch are the

main destinations; and

Northern Villages: the most visited stores for main food shopping

include M&S at Strathkelvin Retail Park, Sainsbury’s at Kirkintilloch,

ASDA at Bishopbriggs and Tesco at Kirkintilloch, with a more even

spread of destinations compared to the other catchments.

Mode of travel to main food destination

5.7 The graph on the previous page shows that about 76% of shoppers went to

their most visited foodstore by car, with 12% walking and 8% travelling by

bus. These findings reveal the continued primacy of the car for main food

shopping trips.

Main centres for clothing and fashion

5.8 The graphs overleaf show the most popular destinations for comparison

goods shopping by category. Residents of the Milngavie/ Bearsden

catchment mostly visit Glasgow City Centre (59%) for clothing and fashion,

followed by Braehead (18%). Only 4% identified Milngavie town centre as

their main destination. In the Bishopbriggs/ Kirkintilloch/ Northern Villages

catchment, residents identified Glasgow City Centre as their main

destination (69%), followed by Strathkelvin Retail Park (9%).

Main centres for furniture, floorcoverings and furnishings

5.9 Residents of the Milngavie/ Bearsden catchment mostly visit Glasgow City

Centre (47%) for furniture and furnishings, followed by Braehead (11%)

and Clydebank (11%). In the Bishopbriggs/ Kirkintilloch/ Northern Villages

catchment, residents identified Glasgow City Centre as their main

destination (39%), followed by Strathkelvin Retail Park (34%).

Main centres for domestic appliances

5.10 Glasgow City Centre (26%) followed by Great Western Retail Park (19%)

were identified by residents of the Milngavie/ Bearsden catchment as their

most visited centres for buying domestic appliances. In the Bishopbriggs/

Kirkintilloch/ Northern Villages catchment, residents identified Strathkelvin

Retail Park as their main destination (71%), followed by Glasgow City

Centre (14%).

Page 26 of 68East Dunbartonshire Council Retail Capacity Assessment

Main destinations for comparison goods shopping

Page 27 of 68East Dunbartonshire Council Retail Capacity Assessment

Main centres for DIY/hardware

5.11 Great Western Retail Park (36%) followed by other local shops in Milngavie

(14%) and Strathkelvin Retail Park (13%) were identified by residents of the

Milngavie/ Bearsden catchment as their most visited centres for buying DIY

and hardware. In the Bishopbriggs/ Kirkintilloch/ Northern Villages

catchment, residents identified Strathkelvin Retail Park as their main

destination (85%), followed by local shops in Bishopbriggs (3%).

Strathkelvin Retail Park is the overwhelming destination in terms of

popularity.

Main centres for personal goods

5.12 Residents of the Milngavie/ Bearsden catchment mostly visit Glasgow City

Centre (47%) for personal goods, followed by Milngavie town centre (14%)

and Braehead (11%). In the Bishopbriggs/ Kirkintilloch/ Northern Villages

catchment, residents identified Glasgow City Centre as their main

destination (54%), followed by Strathkelvin Retail Park (18%).

Internet and mail order shopping

5.13 Use of the internet and mail order shopping was not a specific question, but

the survey recorded where respondents identified the internet and mail

Page 28 of 68East Dunbartonshire Council Retail Capacity Assessment

order in their responses to the questions by type of goods. These forms of

shopping are known as special forms of trading (SFT) - see section 3. Use

of the internet and mail order accounted for significant proportions of

shopping for personal goods and domestic appliances by residents of East

Dunbartonshire, but otherwise the proportions are relatively low for other

3

goods categories, as indicated by the graph. The current UK proportion of

SFT is 12.3% for all retail goods.

5.14 In the analysis for the capacity study, the proportions of SFT are based on

national forecasts, including allowance for increasing proportions of internet

spending in the future. These sources on SFT will be more reliable than the

survey based findings, which are not applied for this reason.

5.15 The survey findings on the shopping patterns by goods type are combined

to show the patterns for all convenience goods and all comparison goods in

the following sections.

3

Experian Retail Planner, Briefing Note 11, 2013- page 19

Page 29 of 68East Dunbartonshire Council Retail Capacity Assessment

6.0 Convenience expenditure and turnover

Introduction

6.1 The analysis examines the relationships between expenditure and turnover

for each of the five catchment areas and for the Council area as a whole. It

incorporates the shopping patterns from the household survey, which

reveal the expenditure inflows and outflows from each catchment. All

values are expressed in constant 2012 prices.

Forecast convenience expenditure potential

6.2 Table 6.1 shows the forecast expenditure per capita data for East

Dunbartonshire, based on data commissioned from Experian for this study.

These forecasts take account of the socio economic structure of the area,

with UK based forecasts of change by Experian to 2016 and 2021 applied.

Account is taken of the current economic conditions and assessment of

various trend projections, which together represent Experian’s ‘central case

forecasts’.

6.3 Special forms of trading (SFT), including internet shopping, are removed

from the expenditure per capita data, so that it relates to conventional shop

floorspace, as shown in Table 6.1. The proportion of SFT is projected to

increase up to 2021- see section 3. It should be noted that the proportions

of SFT shown in this table do not include internet home delivery coming

from existing supermarket shelves.

Table 6.1 Convenience expenditure per capita forecasts for East Dunbartonshire (in 2012 prices)

2011 2013 2016 2021

£ £ £

Expenditure per capita E Dunbartonshire 2,235 2,210 2,219 2,317

excluding special forms of trading 2,192 2,154 2,148 2,211

Note:

The figure for 2011 is from Experian data commissioned for East Dunbartonshire for this study. The orignal figure w as £2,152

in 2011 prices. This has been converted to 2012 prices by a factor of 1.03850 from Experian Retail Planner,

Briefing Note 11, Appendix 4b. UK grow th rates are applied, from Appendix 4a- see below .

£ £ £ £

UK convenience spend per capita in 2010 prices 1813.7 1793.2 1801.2 1880.5

Less: special forms of trading- internet etc -1.9% -2.5% -3.2% -4.6%

From Experian Retail Planner, Briefing Note 11, central case convenience expenditure grow th forecast, Appendix 4a. The

deductions for special forms of trading are from Appendix 3, page 19

Page 30 of 68East Dunbartonshire Council Retail Capacity Assessment

6.4 Forecasts of the total convenience expenditure potential of the residents of

each catchment area are shown in Table 6.2. They dip slightly in 2016,

rising again to almost the same totals in 2021 as currently.

Table 6.2 Convenience expenditure potential of the residents of each catchment area (in 2012 prices)

2013 2016 2021

Catchment areas £million £million £million

Zone 1 Bearsden 58.2 57.6 58.3

Zone 2 Milngavie 28.8 28.5 28.9

Zone 3 Bishopbriggs 48.7 48.1 48.8

Zone 4 Kirkintilloch 65.4 64.7 65.5

Zone 5 Northern Villages 24.2 23.9 24.2

East Dunbartonshire 225.3 222.9 225.7

Note

From Table 4.1 and Table 6.1. Excludes special forms of trading, including internet spending.

Market shares by catchment area

6.5 Market shares refer to the proportions of expenditure from residents of a

defined area which is spent in that area and in other areas. Table 6.3

shows the convenience market shares for each catchment area, based on

the household survey. Details of how the patterns for main food shopping

and top-up shopping from the survey questions are combined to represent

all convenience shopping are provided in Appendix 2.

6.6 Table 6.3 shows that 55% of the residents of the Bearsden catchment do

their convenience shopping locally, with 25% going to Milngavie and 20%

to locations outside East Dunbartonshire. Some 76% of residents of the

Milngavie catchment do their shopping in the area and 18% in Bearsden,

with only 6% using stores outside the Council area. The table indicates a

significant interrelationship between Bearsden and Milngavie, but a minimal

attraction for residents of these two catchments to stores in the remaining

catchment areas.

Page 31 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 6.3 Where residents of each catchment area do their convenience shopping (market shares)

Origin- catchment areas

Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Total East

Destination Dunbartonshire

Bearsden 55% 18% 0% 1% 3% 17%

Milngavie 25% 76% 0% 1% 5% 17%

Bishopbriggs 0% 0% 83% 24% 42% 29%

Kirkintilloch 0% 0% 1% 56% 29% 19%

Northern Villages 0% 0% 0% 0% 9% 1%

Outside E Dunbartonshire 20% 6% 15% 18% 12% 16%

Total 100% 100% 100% 100% 100% 100%

Note

Based on the household survey results for main food shopping and top-up shopping, w eighted to show the composite

for all convenience shopping. Details are provided in Appendix 2. Percentages are rounded.

6.7 In the Bishopriggs catchment, the retained convenience expenditure is very

high at 83%, with most of the balance going to stores outside East

Dunbartonshire, but only 1% using Kirkintilloch. The survey indicates that

56% of the residents of Kirkintilloch do their convenience shopping locally,

with 24% going to Bishopbriggs and 18% to stores outside the Council

area. In the Northern Villages, only 9% of convenience shopping is

retained, with most going to Bishopbriggs (42%) and Kirkintilloch (29%).

The table indicates very little current attraction to Bearsden and Milngavie

from residents of the other catchment areas for convenience shopping.

Convenience expenditure and turnover in the catchment areas

6.8 The relationship between total expenditure and turnover in each catchment

is defined simply as: residents’ expenditure potential plus inflows, less

outflows equals total turnover.

6.9 Appendix 3 shows the estimates of expenditure inflows to each catchment

in detail, based on the household survey and application of the 2008 based

NSLSP data for inflows from outside East Dunbartonshire. The outflows

are derived from the current household survey.

6.10 Tables 6.4 to 6.9 show the survey based convenience expenditure and

turnover relationships for each catchment area and for East Dunbartonshire

in 2013, 2016 and 2021. High inflows to stores in the Bearsden and

Milngavie catchments from outside East Dunbartonshire are evident

(mainly to Asda and Tesco). Also, high inflows to stores in the Milngavie

catchment and the Bishopbriggs catchment from the rest of East

Dunbartonshire are also evident, which

Page 32 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 6.4 Bearsden catchment: convenience expenditure and turnover (in 2012 prices)

Zone 1 Bearsden catchment: convenience expenditure and turnover (in 2012 prices)

2013 2016 2021

% £million £million £million

Main catchment residents' expenditure potential 58.2 57.6 58.3

Add: inflows from rest of E Dunbartonshire 11% 6.6 6.5 6.6

inflows from outside E Dunbartonshire 29% 16.9 16.7 16.9

Less: outflows -45% -26.3 -26.1 -26.4

Turnover 55.3 54.7 55.4

Note

From Table 6.2 and Appendix 3

Table 6.5 Milngavie catchment: convenience expenditure and turnover (in 2012 prices)

Zone 2 Milngavie catchment: convenience expenditure and turnover (in 2012 prices)

2013 2016 2021

% £million £million £million

Main catchment residents' expenditure potential 28.8 28.5 28.9

Add: inflows from rest of E Dunbartonshire 57% 16.4 16.2 16.4

inflows from outside E Dunbartonshire 33% 9.6 9.5 9.6

Less: outflows -24% -7.0 -6.9 -7.0

Turnover 47.8 47.2 47.8

Note

From Table 6.2 and Appendix 3

Table 6.6 Bishopbriggs catchment: convenience expenditure and turnover (in 2012 prices)

Zone 3 Bishopbriggs catchment: convenience expenditure and turnover (in 2012 prices)

2013 2016 2021

% £million £million £million

Main catchment residents' expenditure potential 48.7 48.1 48.8

Add: inflows from rest of E Dunbartonshire 53% 25.7 25.4 25.7

inflows from outside E Dunbartonshire 16% 8.0 7.9 8.0

Less: outflows -17% -8.1 -8.0 -8.1

Turnover 74.2 73.4 74.3

Note

From Table 6.2 and Appendix 3

Table 6.7 Kirkintilloch catchment: convenience expenditure and turnover (in 2012 prices)

Zone 4 Kirkintilloch catchment: convenience expenditure and turnover (in 2012 prices)

2013 2016 2021

% £million £million £million

Main catchment residents' expenditure potential 65.4 64.7 65.5

Add: inflows from rest of E Dunbartonshire 11% 7.3 7.3 7.3

inflows from outside E Dunbartonshire 4% 2.8 2.8 2.8

Less: outflows -44% -28.7 -28.4 -28.7

Turnover 46.9 46.4 47.0

Note

From Table 6.2 and Appendix 3

Page 33 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 6.8 Northern Villages catchment: convenience expenditure and turnover (in 2012 prices)

Zone 5 Northern Villages catchment: convenience expenditure and turnover (in 2012 prices)

2013 2016 2021

% £million £million £million

Main catchment residents' expenditure potential 24.2 23.9 24.2

Add: inflows from rest of E Dunbartonshire 1% 0.1 0.1 0.1

inflows from outside E Dunbartonshire 0% 0.0 0.0 0.0

Less: outflows -91% -22.0 -21.8 -22.1

Turnover 2.3 2.2 2.3

Note

From Table 6.2 and Appendix 3

Table 6.9 East Dunbartonshire: convenience expenditure and turnover (in 2012 prices)

East Dunbartonshire: convenience expenditure and turnover (in 2012 prices)

2013 2016 2021

% £million £million £million

Main catchment residents' expenditure potential 225.3 222.9 225.7

Add:

inflows from outside E Dunbartonshire 17% 37.2 36.8 37.3

Less: outflows -16% -36.1 -35.7 -36.1

Turnover 226.5 224.0 226.8

Note

From Table 6.2 and Appendix 3

reflect the interrelationship with their respective neighbouring catchments.

For similar reasons, there are very high outflows from the Bearsden,

Kirkintilloch and Northern Villages catchment areas. The overall inflows

and outflows from East Dunbartonshire as a whole are almost in balance.

In fact the current outflow of 16% is slightly less than the outflow of 17.8%

estimated in the 2009 Capacity Study for 2008. There was no quoted inflow

in the previous Study.

Convenience floorspace and turnover in 2013

6.11 The current distribution of convenience floorspace in East Dunbartonshire

and in the five catchments is shown in Table 6.10, based on data provided

by the Council from their 2012 floorspace survey and sorted by the

consultants for this study. The current total of 25,094 sq m net compares to

the total of 24,645 sq m net in the 2009 Capacity Study. Average company

turnover/ floorspace ratios from the Retail Rankings 2013 are applied, with

adjustments to include VAT and remove petrol/ non- retail sales, expressed

in 2012 prices. These ratios are applied to the main supermarkets, with

estimated average ratios applied to other shops. Table 6.10 shows the total

average turnover in each catchment at average levels, based on this

method.

Page 34 of 68East Dunbartonshire Council Retail Capacity Assessment

Table 6.10 East Dunbartonshire convenience floorspace and turnover at average and actual levels

from the survey in 2013 (in 2012 prices)

Floorspace sq m Turnover Turnover

gross net £ per sq m £million

Zone 1

Bearsden Town Centre 885 595 5.1

M&S Simply Food (total 636 sq m gross) 636 445 10,234 4.6

Other town centre shops 249 149 3,900 0.6

(1) ASDA, Milngavie Rd (total 9,535 sq m gross- 60% conv) 5,721 3,433 12,055 41.4

Lidl, Baljafray (total 894 sq m gross-90% conv) 805 603 4,045 2.4

Other Bearsden out of centre shops 2,286 1,372 3,100 4.3

Total at average levels 9,697 6,002 53.2

Over-trading 4% 2.1

Total from survey (actual levels) 55.3

Zone 2

Milngavie Town Centre 7,112 4,411 38.9

Tesco- Gavin's Mill Rd (total 5,539 sq m gross 73% conv) 4,043 2,426 10,209 24.8

M&S Simply Food (total 1,590 sq m gross 90% conv) 1,431 1,002 10,234 10.3

Other town centre shops 1,638 983 3,900 3.8

Other Milngavie shops 887 532 3,100 1.6

Total at average levels 7,999 4,943 40.5

Over-trading 18% 7.3

Total from survey (actual levels) 47.8

Zone 3

Bishopriggs Town Centre 3,722 1,890 21.8

Morrisons, The Triangle (3,815 sq m gross-90% conv) 3,434 1,717 12,289 21.1

Other town centre shops 288 173 3,900 0.7

ASDA Kirkintilloch Road (total 6,104 sq m gross-70% conv) 4,273 2,564 12,055 30.9

M&S Simply Food, Strathk R Park (1,880 sq m gross-90% conv) 1,692 1,184 10,234 12.1

Tesco Express, Kirkintilloch Rd 329 247 15,945 3.9

Other Bishopriggs out of centre shops 2,388 1,433 3,100 4.4

Total at average levels 12,403 7,317 73.2

Over-trading 1% 1.1

Total from survey (actual levels) 74.2

Zone 4

Kirkintilloch Town Centre 7,402 4,441 40.7

Tesco- Regent Centre (total 3,012 sq m gross-95% conv) 2,861 1,717 10,209 17.5

Sainsbury's,Shamrock St (total 3,668 sq m gross 85% conv) 3,118 1,871 10,606 19.8

Other town centre shops 1,423 854 3,900 3.3

Other Kirkintilloch shops 1,170 702 3,100 2.2

Lenzie 1,036 622 3,100 1.9

Twechar 131 79 3,100 0.2

Total at average levels 9,739 5,844 45.0

Over-trading 4% 1.8

Total from survey (actual levels) 46.9

Zone 5

Lennoxtown 1,165 699 3,100 2.2

Milton of Campsie 242 145 3,100 0.5

Torrance 240 144 3,100 0.4

Total at average levels 1,647 988 3.1

Under-trading -26% -0.8

Total from survey (actual levels) 2.3

Total East Dunbartonshire 41,486 25,094 215.0

Over-trading 5% 11.5

Total from survey (actual levels) 226.5

Note

Gross floorspace provided by the Council, based on the Assessor- 2012

(1) The total gross floorspace of ASDA is 11,246 sq m (Assessor). In this table, the loading bay area (1,711 sq m) has been

excluced. Net floorspace- estimates by R MacLean. Estimate for Tesco Milngavie from PPC.

Page 35 of 68You can also read