FOOD VALUE CHAIN, FROM seeds TO you - LONGPOINT ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FOOD VA LU E CHAIN, FROM seeds TO you WINTER 2018

“T he food industry has

tremendous opportunity,

as well as an obligation, to

meet the needs of new, more

sophisticated and more

demanding consumers while

satisfying shareholders’

demands for returns—

and in doin g so creating a

sustainable food supply for

the new millennium.”

– Deloitte

ta b l e o f c o n t e n ts

INTRODUCTION 4

wh ere do es yo u r fo o d c o m e from?

PA RT I : 7

Wh en fa rm to ta b l e was a s hort t r ip

PA RT I I: 10

P ro c es s ed a n d Pac k aged

by th e M i gh ty F ew

PA RT I II: 13

C h a l l en ges o f

Fres h a n d S p ec i a l

PA RT I V: 17

S u m m a ry a n d I m pact

o n Rea l Estate M a rk ets

REFERENCE NOTES 22

where does your food come from?

In a recent study, 71% of consumers noted that they make purchasing

decisions based on their understanding of a product’s full ingredient

list, and 54% said that they prioritize the source of their food. These

two factors were rated as being more important than organic labeling,

packaging, fat content, and brand. 1 For modern grocery shoppers, the

source of food matters more than ever.

To better understand the significance of these consumers procure food products, has dramatically

findings, we must first define what we mean by impacted all participants of the “food value chain.”

“source.” That is, are we referring to the original

physical source of the food (i.e., mineral, plant, Deloitte defines the food value chain as “the network

animal), the geographical location and farm where of stakeholders involved in growing, processing,

it originated, the processing plant where it was and selling the food that consumers eat – from farm

prepared, the company that packages it, the logistics to table.”2 The five key categories in this system are:

firm that distributes it, or the grocery store that sells it. suppliers of farming inputs such as seeds, fertilizer,

For consumers, the concept of “source” encompasses and equipment; food producers engaged in farming

all these elements. A global “food awakening” is and ranching; processors that handle the harvesting

driving a thirst for knowledge about the foods we eat and processing of raw foods; brands that package

along with a desire to eat healthier foods, irrespective and transport the finished food product; and grocery

of individual background, wealth level, or age. This retailers that deliver the product to the consumer.

food awakening, in addition to a global population

movement into larger cities and a shift in how

F I G U R E 1 : K E Y P L AY E R S : T H E F O O D VA LU E C H A I N

“BIG AG” GROCERY

“LEFT OF “RIGHT OF

“CONSUMER”

THE FARMER” THE FARMER”

INPUTS PRODUCERS PROCESSORS BRANDS RETAILERS

“Seeds, fertilizer, “The farmer” “The ABCDs of “CPG and “Supermarket

chem, equipment” commodities” distributors” chains”

• Dow Chemical • Livestock production • ADM • Nestle • Wal-Mart

• DuPont • Crop production • Bunge • PepsiCo • Costco

• ChemChina • Horticultural science • Cargill • Coca-Cola • Kroger

• Syngenta • Dreyfus • Unilever • Target

• Bayer • Danone • Albertsons

• Monsanto • General Mills • Publix

• John Deere • Kellogg’s • HEB

• Mars • Whole Foods

• Associated British Foods • Southeastern Grocers

• Mondelez

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 4

For the purposes of clarity, we have placed food retail Stagnating demand for traditional grocery products has

products into four major categories: Repeat, Fresh, led to huge consolidation in the realm of Big Ag, and as

Special and Frozen. Repeat refers to the packaged a result, packaged foods are increasingly controlled by

center-aisle products that have historically been the a small number of global mega-companies. As demand

mainstay of the grocery industry because they are for mass-produced packaged foods continues to stall

typically bought on an ongoing basis. If the product or decline, these same companies will focus on the

comes wrapped, in a box, or in a can, it probably falls into fresh and specialty foods categories. This process

this category. Fresh refers to perishable products such has already begun and is expected to continue into

as produce, meat, seafood, and prepared foods with the foreseeable future (Figure 5). Further, growth in

limited shelf life. These products require specialized demand for fresh and special grocery products coupled

transportation and storage. Special products are those with improved capabilities for customized delivery has

not typically stocked in mainstream supermarkets. resulted in substantial changes in the strategies of Big

These items include ethnic and locally sourced products Ag and big brand companies.

from non-national suppliers. Lastly, frozen products can

include any of the items listed above, in a frozen state.

Historically, within each category, there have been

different participants, regulations, supply chain and

logistics models, and consumer requirements. Today,

these categories and their members are all converging

in order to meet the current and projected shopping

patterns of the modern consumer.

Today, the food value chain for most products is

dominated by “Big Ag” companies: large global firms

that dominate each phase of the chain (Figure 1). For

instance, a wheat farmer (large or small) in Kansas

may grow his crop using inputs from DuPont and sell

it to Cargill, which then transports the grain to Kellogg,

which in turn processes these raw ingredients into

snack products that are sold to The Kroger Company,

which finally sells it to the consumer. The consumer can

buy the product in the store itself, click and collect at

the store, or have it delivered to his or her home.

It is important to note that each food category and

individual item within each category requires its own

distinct combination of the five components of the

food value chain. Big Ag companies, dominant in

three of the five categories, have historically operated

predominantly in the supply chain for Repeat goods, The real estate infrastructure of the food value

as this was where the most money was to be made. chain is in the process of a massive restructuring to

Fresh and Special products, which necessitate accommodate modern supply chain models. The

specialized handling, are costlier to grow and produce, impact of this evolution has been felt mostly in the

require more complex supply chain management industrial sector, where we believe industrial properties

models, and require more government oversight and will continue to move closer to population centers (see

regulation, have historically seen less demand from Longpoint Review Spring 2018). Less obvious changes

consumers. Consumer demand patterns, however, are are occurring in the grocery brick and mortar sector in

rapidly changing. the form of new concept stores, smaller stores, more

urban locations, new entrants (e.g., Lidl), increased

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 5

mergers and acquisitions among retailers (e.g., This paper examines the changing preferences of

Amazon/Whole Foods) and distributors (e.g., Unified/ today’s consumers and the evolving roles of the key

SuperValu), growing home delivery options, click and members in the food value chain, along with the

collect strategies, and growth of ethnic grocers. Thus, it resulting impact on real estate markets.

will come as no surprise that there are currently exciting

investment opportunities in almost every aspect of the

food value chain (Figure 2).

F I G U R E 2 : T R E N D S I N F O O D LO G I S T I C S

Consumer

Demand-

side

Trends

Lifestyle Trends Delivery Mechanisms Grocery Trends

Urbanization Source

Brick & Home Click &

Demographic shifts Mortar Delivery Collect Full Disclosure

Emerging consumer Instant gratification Local

technology

Easy returns Organic

Low cost Ethnic

Large selection Fresh

Supply-

side

Trends

Big AG Consolidation Brands & Retailers Go Vertical New Grocery Store Formats

Consolidation of input Consolidation of large brands (Kraft-Heinz) Rise of small limited

producers assortment chains (Aldi,

Large brands acquiring smaller brands Trader Joe’s)

Consolidation of AG

processors Investments in fresh and specialty products Rise of specialty grocer

chains (fresh & ethnic)

Increasing competition Amazon-Whole Foods merger

Rising store counts

Declining margins Costco, Walmart, Kroger vertical integration

Smaller store sizes

United Natural Foods-Supervalu merger

More urban

Supply Chain Restructuring

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 6

H i sto ry

When Farm to Table Was a Short Trip

In 1798, when English clergyman Thomas Malthus famously argued that

global population growth would ultimately outstrip the world’s food

supply, he could not have predicted the rise of mechanized agriculture,

advances in horticultural science, and the globalization of the world’s

food supply chain. 3 Agriculture around the world has evolved from a

system of family farms and local agrarian economies to a system of

mass production and global distribution on a scale unimaginable to

Malthus and his contemporaries.

The U.S. offers an ideal case study for global changes

in the food supply chain. In colonial times, the

economy was almost entirely agricultural. At least 90%

of working Americans made part or all of their living

through farming.4 Most of the food people ate came

from their own farms, or from those of their neighbors.

The advent of the Industrial Revolution, however,

along with population growth and related public policy

initiatives, heralded an era of enormous change, and

led to the transition to a mechanized and consolidated

agricultural sector. Then, in 1862, the Homestead Act

allocated 270 million acres of free land to approximately

1.6 million people. Participants were granted ownership

of a parcel once they built a home and cultivated the

land, a policy initiative that bolstered the fortunes of

many impoverished farmers in the East and Midwest.

As the agricultural economy progressed, these smaller

farms increasingly merged into larger ones.5 At the

same time, a range of technological advances led to

greater crop yields and the logistical means to deliver

them to distant locations. The McCormick reaper,

steam and gasoline-powered tractors, hybridized

corn, and coast-to-coast refrigerated shipping were all

developments that linked the agricultural economies of

previously disparate markets.6

In the mid-1900s, advances in mechanical engineering, of “combine” harvesters – used to cut, thresh, and clean

horticultural science, and transportation technology grain simultaneously – bolstered crop yields.7 Meanwhile,

accelerated the growth of the national agricultural the use of chemical fertilizers and pesticides grew

economy. Between 1930 and 1960, the number of dramatically.8 Then, in the 1960s, genetic modifications

tractors increased fivefold, while the number of farm and the cultivation of hybrid strains of corn, wheat, and

horses and mules declined by 87%. The size and efficacy rice boosted crop yields even further.9

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 8These mid-twentieth-century technological and share of the overall US population of farm laborers

scientific developments led American farm productivity declined from 41% in 1900 to 1.9% in 2000. 12

and size to double between 1948 and 1998. Grain yield

per acre for corn, a mainstay in the U.S. agricultural Thus, the current food industry is almost unrecognizable

economy, increased by more than five times in the 80- from its earlier incarnations. Food that used to travel

year period between 1936 and 2016 (see Figure TBD),11 directly from the field to the kitchen table may now

and the average farm size increased from under 200 cross multiple state and country borders before landing

acres to over 400 acres. With larger farms producing on the consumer’s table, leaving people with very little

more efficiently, the total number of farms declined knowledge of the origin of their food.

from over five million to under three million, and the

F I G U R E 3 : T H E C O R N Y I E L D “ H O C K E Y S T I C K ” 10

U.S. Corn Grain Yield Trends Since 1866

Data Source: USDA-NASS (as of Jan 2017)

200

180

2016

160

140

y = 1.8858x - 3635.8515

R 2 = 0.9166 2012

Grain yeild (bu/ac)

120

100

1988

80

60

y = 0.76x - 1452.40

R 2 = 0.72

1956–2016

40

1937–1955

1866–1936

20 2016

0

1840 1860 1880 1900 1920 1940 1960 1980 2000 2020 2040

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 9the mighty

few

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 10Processed and Packaged by the Mighty Few

Much of our traditional center aisle food today comes from “row crops”

– that is, crops that are planted in rows to accommodate mechanized

agriculture. In the increasingly consolidated food industry, Big Ag

dominates every phase of the food value chain for row crop agriculture.

Up until 2016, six supplier firms – Dow Chemical, control more than 80% of the global grains market. 20

DuPont, ChemChina, Syngenta, Bayer, and Monsanto As a result of the large market share occupied by

– controlled more than 60% of the market for these firms, row crop farmers are subject to pricing

agricultural inputs (seeds, pesticides, and herbicides). pressures from the mega-companies from which

Each of the six firms has since merged with another they source their farming inputs, as well as from the

company.13 Chemical Company and DuPont Pioneer large firms to which they sell their farming outputs.

merged in 2017, with a deal size of roughly $62 billion, Consequently, the total number of farms in the United

and the combined company now carries out functions States has declined year over year since 2007 and

ranging from materials science to agricultural farm net income has remained low, and there is little

technologies.14 ChemChina acquired Swiss company sign of this trend abating. 21

Syngenta in July 2017 for $43 billion,15 and Bayer

bought Monsanto in June 2018 for $66 billion, further Once the food has been grown and harvested, it

consolidating this segment of the market.16 Individual is transferred to a distributor, which is typically a

farmers and farming companies now source most of major global consumer package goods (CPG) brand

their inputs from one of these providers. For example, (Figure 4). At this level of the value chain, there

90% of U.S. cotton seeds come from one of these are ten global companies that control nearly every

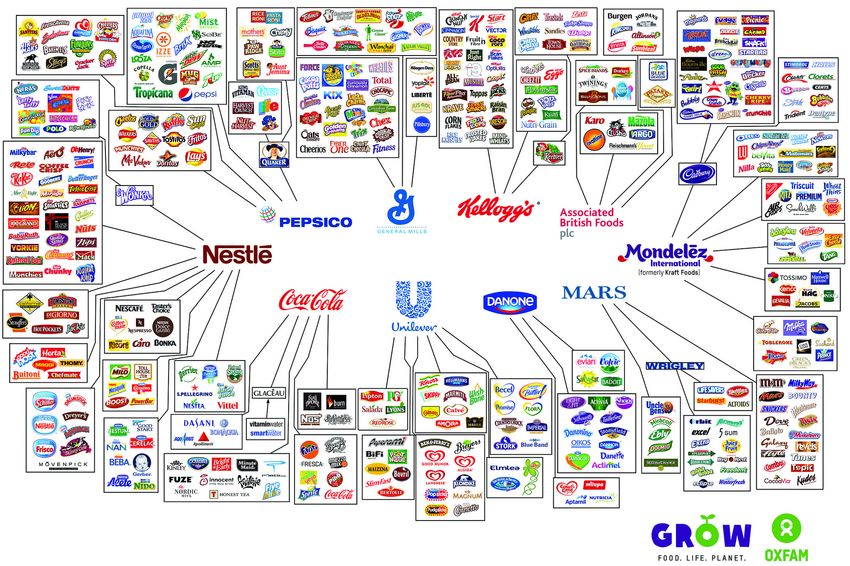

three mega-companies.17 major food and beverage brand in the world: Nestlé,

PepsiCo, Coca-Cola, Unilever, Danone, General

Just as a few companies dominate row crop Mills, Kellogg’s, Mars, Associated British Foods, and

agriculture, two types of crops dominate the US farm Mondelez.22 McKinsey & Company notes that since

production economy: corn and soybeans. In 2017, the 2011, CPG companies have witnessed declining year-

total value of production for corn was $48.5 billion, over-year growth rates, which are now in the low single

while the total value of production for soybeans was digits, as well as shareholder returns that have lagged

$41 billion. The next largest US crop is hay, at $16.2 the S&P 500. McKinsey attributes this trend to new

billion.18 The outsized production share of corn and distribution channels and buying preferences, as well

soybeans reflects the geographic farming landscape, as disruptive new brands and retailers. 23 As this arena

with corn and soybeans accounting for 172.2 million has become more competitive, firms have focused

harvested acres, while staple crops like cotton, on cutting operating costs and creating greater

sorghum, and rice accounting for a combined total of efficiency through mergers and acquisitions. A study

only 18.8 million acres harvested annually.19 Thus, a by PwC covering 115 CPG deals each valued at over

small number of crops are generating massive profits $3 billion found that the average deal size had more

for a small number of corporations at the input stage than tripled between 2014 and 2016. 24 A significant

of the food value chain. proportion of this increase can be attributed to the

trend of larger firms buying smaller brands in the

The third stage of the food value chain is also marked natural and ethnic foods category, such as Nestle’s

by a high degree of consolidation among companies acquisition of Terrafertil, Atrium Innovations, and

engaged in purchasing and processing. The “ABCDs” Tribe Mediterranean Foods.

of commodities – ADM, Burge, Cargill, and Dreyfus –

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 11Beyond industry consolidation and new concept Today’s food products come from an increasingly

brand acquisitions, some firms are vertically vast and complex web of inputs, farmers, processors,

integrating across multiple levels of the food value distributors, and supply chain logistics. However, at

chain. This is particularly true of Kraft Heinz tomato every stage of the value chain, a few industry giants

products. The value chain process begins with dominate. Long gone are the days when people grew

Heinz propriety seeds, which are supplied by the and ate their own food or bought it from their neighbor.

HeinzSeed company. 25 These seeds are incubated Today’s food may have been grown in one state and

in warehouses and subsequently planted on farms processed in another, with stops at multiple locations

located primarily in California’s Central Valley, before reaching its final destination, making it more

which supplies approximately 95% of the nation’s difficult for consumers to understand the source

processed tomato stock and one third of the entire of their food. However, in response to increased

world’s processed tomatoes. 26 After harvest, the pressure from consumers, the members of the food

tomatoes are transferred to a partner food processing value chain have begun making a more concerted

company such as Morning Star, the world’s largest effort to provide greater transparency when it comes

tomato-processing organization, which has three to food source.

facilities in the Central Valley. 27 After processing,

the refined tomato-based product is packaged and

transferred back to Kraft Heinz, which relies on a

network of 88 distribution centers nationwide to route

goods to the end buyer, which is typically a grocery

store location. 28

F I G U R E 4 : T H E G I A N T S W H O P R O D U C E YO U R F O O D

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 12F r es h a n d

s p ec i a l

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 13Challenges of fresh and special

While consumer demand for Repeat items drove the Because of the immensity of the logistical challenges

growth of Big Ag during the 20th century, demand for involved in the delivery of Fresh and Special products,

these row crops and center aisle products has been key food industry firms have been consolidating

stagnating in recent years. As consumer sentiment has vertically across the supply chain to ensure quality

steadily shifted toward fresh, organic, locally sourced and quantity. In the grocery wholesale sector, for

food, American farmers have also begun to focus on example, Supervalu bought Unified Grocers for

fresh and specialty products. 29 Although Big Ag is $390 million in 2017, giving the national wholesale

more economically efficient than smaller companies chain access to 345 independent grocery stores

and accounts for the majority of agricultural sector on the West Coast. 31 In the poultry sector, Tyson

revenue, brand companies selling Fresh and Special Foods integrated the entire supply chain – breeding

products are on the rise. In addition, the growth and stock, egg hatcheries, farms, processing facilities,

success of “healthy” grocery chains such as Whole and transportation infrastructure. In grocery retail,

Foods and Sprouts is due to locally sourced or The Kroger Company now operates seventeen dairy

natural foods branding. In the period spanning 2016 plants, ten deli and bakery plants, two beverage

to 2018, Sprouts opened 67 new retail stores, making plants, two cheese plants, one meat plant, and a fleet

it one of the fastest growing grocery retailers in the of vehicles that conduct 8,600 daily deliveries. 32 33

country. 30 Further, ethnic grocers such as Presidente, Similarly, Costco is developing a poultry processing

Cardenas Markets, El Rancho, and H Mart have facility in Nebraska that will supply the 90 million

emerged as ethnic grocery specialists, driving Publix chickens it sells per annum. In 2016, taking its cue

and Winn Dixie to convert some existing stores into from competitors such as Kroger and Albertsons,

Latin-themed banners, Publix Sabor and Fresco which operate 37 and 19 dairy manufacturing plants

Y Mas. Even traditional grocers such as Kroger, respectively, Walmart decided to enter the dairy

Walmart, and Publix have been changing the internal business with the establishment of a 250,000 square

layouts of their stores to increase local and organic foot dairy plant in Indiana. 34

offerings and provide a more expansive selection of

healthful produce.

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 14As the trend towards consolidation and vertical that maintain a safe cold storage environment for

integration continues, new, increasingly complex meat in transit. 37 The dairy supply chain is similarly

logistical infrastructure designed to deliver fresh complex. The Cabot Creamery Co-operative in New

products is emerging. Fresh products require a England transports milk in special stainless-steel

complex network of climate-controlled transportation insulated trucks from over 1,000 family farms to four

and storage infrastructure that reduces spoilage and refinement facilities (creameries). After processing,

maintains quality. In addition, specialized warehousing finished milk, yogurt, cheese, and butter products

facilities for perishables must be located near the each require their own temperature settings for the

consumer or grocery retail destination in order to journey to their final destination. 38

minimize transportation time and distance. Each

individual supplier must pass food safety checks and Produce requires similarly specialized logistical

inspections that are both rigorous and expensive. infrastructure. For example, Stemlit Fruit harvests apples

The necessity of third-party intermediaries (there are from company-owned orchards in four districts of

over 33,000 different food manufacturing companies Washington state between August and October every

in the United States) 35 for handling the sorting and year, and then packages and stores the fruit in controlled

distribution of local produce adds an additional layer atmosphere facilities. These highly specialized facilities

of complexity to procurement. 36 use nitrogen gas to reduce oxygen levels from 21%

to 2%, and maintain a strict climate of 32-36°F with 95%

In the meat supply chain, for example, cold storage humidity. While seafood products share some of the

procedures begin in the slaughterhouse, where same basic requirements, they pose their own particular

carcasses must be cooled to under 7°C (4°C for logistical challenges. Alvaro Carril of Chile-based LAN

poultry) to avoid bacterial growth and extend shelf Cargo, which transports seafood and produce from

life. A network of climate-controlled aircraft, vessels, South America to the US, notes, “Transporting salmon

trucks, and warehouse facilities are aided by is different than moving flowers, and both commodities

compressors and ventilation and insulation systems require special and differential treatment.” 39

F I G U R E 5 : B I G F O O D B R A N D S B U Y I N G O R G A N I C / N AT U R A L F O O D B R A N D S

Atrium Terrafertil

Innovations

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 15Special products that exist outside the main grocery Although the specific logistics requirements of

supply channels also depend on a specialized, often different Fresh and Special goods vary considerably,

local, supply chain. For example, the supermarket common to all is an increasingly complex web of

chain Sprouts uses a decentralized procurement management systems, transportation resources,

system to source a variety of natural and organic and industrial warehousing infrastructure needed

products. The Sprouts supply chain of 2,400 products to deliver products to consumers. If, as expected,

from over 850 vendors is primarily locally sourced, demand for these products continues to grow, then

meaning food comes from within a 500-mile radius the need for logistics systems that can safely and

of the retail store. 40 The chain accomplishes this efficiently deliver them to consumers will also increase,

feat by using dedicated regional procurement teams creating a considerable supply-demand imbalance in

that have the flexibility to buy different products in the industrial and retail real estate sectors, and thus

different locations based on availability. 41 considerable investment opportunities for Longpoint

Realty Partners.

Similarly, ethnic food suppliers are building out their

global logistics infrastructure in response to growing

demand. The shopping preferences of the two

fastest growing demographic segments in the US,

Asian-Americans and Hispanics, have spurred the

rise of alternative grocery channels. 42 For example,

Goya, the largest US-based manufacturer of Hispanic

food, offers over 2,500 products from the Caribbean,

Mexico, Spain, Central, and South America, and

operates 26 distribution facilities throughout the US,

Puerto Rico, the Dominican Republic, and Spain. 43

Similarly, products sourced by Diaz Foods, another

ethnic wholesale distributor, reach thousands of

East Coast customers by travelling through one

40,000 square foot cold storage facility and one

60,000 square foot dry storage facility, both located

in Virginia. 44 The company recently expanded its

distribution network by leasing a trucking fleet

through a partnership with Ryder, and will increase

its warehouse footprint in the near future. The

partnership enables Diaz Foods to incorporate the

most technologically advanced vehicles into its

supply chain without making the capital investment

of owning them, thereby maximizing efficiency and

minimizing costs while providing optimal delivery of

their products. 45

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 16r e a l estat e i m p l i cat i on s

Summary and Impact on Real Estate Markets

The rise of the Fresh and Special segment s The increasing complexity of the food retail

necessitates the combination of infill logistics facilities landscape and consequent rise of specialty and

and locally-relevant grocery retail concepts that can alternative format grocers has created a niche for

effectively and efficiently deliver these products third-party logistical (“3PL”) solutions. Given that

to today’s consumers. As urban brick and mortar investments in distribution real estate infrastructure

grocery retail stores grow in number and diversify by require major capital outlays with significant fixed

concept type and size, logistics industrial facilities will costs, it makes sense to aggregate the warehouse

continue to be built nearer to population centers and operations for multiple smaller firms under a few

to service more varied food value chain participants. external providers. 48 Larger supermarket chains such

as Walmart have also sought to manage expenses

In the past, the dominant grocery logistics model by moving to outside logistics companies, which

employed by major supermarket chains was to can lower labor costs by 50%. 49 Thus, over the past

own and operate their own distribution facilities, an twenty years, many grocery chains have shed their

approach intended to ensure product quality and supply chain real estate to 3PLs, which have expanded

quantity. 46 Then, in the late 20th century and early their warehousing and logistics infrastructure.

2000s, most major grocery store chains built large For example, the Kroger Company has outsourced

distribution centers one or more hours outside of over 6.7 million square feet of warehouse space

urban areas to serve stores within a broader region. (one-third of its total capacity) over a ten-year period.

Many of these facilities are still directly owned and Other chains such as Ahold, Safeway, Trader Joe’s,

managed by supermarket chains. For example, Publix A&P, Pathmark, BI-LO, and Wawa have followed suit. 50

warehouse facilities in Florida today are on average

42 years old with 383,400 square feet of space, 25- Grocery 3PLs are now expanding at a rapid rate

foot clearance height, and 54 dock-high doors. 47 to meet growing demand, driving competition

FIGURE 6: U. S. GROCERY INDUSTRY GROW TH

N u m b e r o f N at u r a l a n d

T o ta l U . S . S u p e r m a r k e t S a l e s s p e c i a lt y S u p e r m a r k e t s

($ in billions)

700 7,500

17% increase 35.6% increase

from 2011-2017 from 2011-2017

650 7,047

7,000

6,778

$612 6,616

$600

600 $588 6,500 6,386

$574

6,179

550 $549

$539 6,000

$523 5,738

500 5,500

5,197

450 5,000

400 4,500

2011 2012 2013 2014 2015 2016 2017 2011 2012 2013 2014 2015 2016 2017

Source: U.S. Census Bureau Source: Nielsen

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 18for urban industrial space. Large wholesale and USDA defines “specialty distributors” as providers

distribution companies such as C&S Wholesale of “…frozen foods, dairy products, meat and meat

Grocers, Supervalu, SpartanNash, and Sysco, which products, or fresh fruits and vegetables…[which]

tend to cater to traditional branded CPG products, operate in niche markets…”). 53 These third-party firms

have recently made significant investments in their today account for 45% of total grocery wholesale

metropolitan warehouse infrastructure. C&S, the tenth revenues. 54 That said, many key retailers have

largest private company, now has over twenty facilities chosen to invest in their own infrastructure in order to

in the Northeast alone, with most of them situated on handle the logistics of fresh and unique products. For

the outskirts of major cities such as Baltimore, New example, Amazon has invested in three million square

York, Philadelphia, and Hartford. 51 Sysco has over 120 feet of warehouse space to power its AmazonFresh

U.S. warehouses, with multiple dedicated facilities and Amazon Prime Pantry grocery delivery programs,

of varying sizes and locations for each major metro which is still only one-tenth of the warehouse space

area. For example, its South Florida footprint consists that Wal-Mart uses for specialty food distribution. 55

of smaller handling facilities located near the airport,

a 657,000 square foot facility 15 miles Northwest of Today’s brick and mortar grocery landscape reflects

Miami, and additional fresh-focused facilities in Fort these investments in logistics infrastructure. Supply

Lauderdale and West Palm Beach. 52 chain optimization and expanded infill warehousing

facilities have enabled a proliferation of small-

Growing demand for Fresh and Special grocery format supermarkets. Chains such as Aldi, Lidl, and

items and the related logistical complexities has Trader Joe’s – with average store sizes between

also bolstered the role of “specialty distributors” (the 8,000 and 15,000 square feet – have flourished in

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 19urban environments where retail space is limited. by 32% and total store sales have increased by 17%,

Aldi led the nation in the number of two-year net driven by the growth of new store concepts, sizes,

store openings between 2016 and 2018, with 171 and urban locations. This trend was made possible

new locations. 56 Larger retail chains such as Walmart by the development of an urban food logistics

have also pioneered smaller brick and mortar brands, network nationwide.

such as Walmart Neighborhood Market, which are less

than half the size of a standard Walmart Supercenter. Regardless of whether food is procured through brick

These changes in grocery store formats have and mortar stores, curbside pickup, or home delivery,

caused the median store size in the U.S. to decline real estate operators must work to understand the

by 12.2% since 2006. 57 As these smaller stores have evolving supply-chain landscape and adapt according

penetrated urban areas, over the past six years, the to the physical requirements of the food industry in

total number of U.S. grocery stores has increased the 21st century.

DWIGHT ANGELINI T O M S T I PA N O V

m a n a g i n g pa r t n e r a s s o c i at e

617 861 9761 617 861 97 72

a n g e l i n i @ l o n g p o i n t. c o m s t i pa n o v @ l o n g p o i n t. c o m

F O O D VA L U E C H A I N . F R O M s e e d s t o y o u 20ReferEnce Notes

1. “ How Consumer Demand for Transparency is Shaping the Food 19. U.S.D.A. Ibid.

Industry, The 2016 Label Insight Food Revolution Study, Label

Insight. https://www.labelinsight.com/hubfs/Label_Insight-Food-

20. P

utz, Adam. “The ABCDs and M&A: Putting 90% of the global grain

Revolution-Study.pdf?hsCtaTracking=fc71fa82-7e0b-4b05-b2b4-

supply in fewer hands.” 21 February 2018. Pitchbook.com, https://

de1ade992d33%7C95a8befc-d0cc-4b8b-8102-529d937eb427.

pitchbook.com/news/articles/the-abcds-and-ma-putting-90-of-the-

global-food-supply-in-fewer-hands.

2. “The Food Value Chain: A Challenge for the Next Century. Deloitte,

2013. https://www2.deloitte.com/content/dam/Deloitte/ie/Documents/

21. “Total number of farms in the United States from 2000 to 2017.”

ConsumerBusiness/2015-Deloitte-Ireland-Food_Value_Chain.pdf.

Statista, https://www.statista.com/statistics/196103/number-of-farms-in-

the-us-since-2000/.

3. “ Thomas R. Malthus. “Classic Readings in Economics.” Middlebury

College, History of Economic Thought, http://sites.middlebury.edu/

22. T

aylor, Kate. “These 10 companies control everything you buy.”

econ0450f10/files/2010/08/malthus.pdf.

Business Insider, 28 September 2016. BusinessInsider.com,

https://www.businessinsider.com/10-companies-control-the-food-

4. Malthus, T.R. Ibid. industry-2016-9.

5. “The Homestead Act.” History.com, https://www.history.com/this-day-in- 23. H

enrich, Jan et al. “Agility@Scale: Solving the growth challenge in

history/the-homestead-act. consumer packaged goods.” https://www.mckinsey.com/industries/

consumer-packaged-goods/our-insights/agility-at-scale-solving-the-

growth-challenge-in-consumer-packaged-goods.

6. S

pielmaker, D. M. “Growing a Nation Historical Timeline.” 21 March

2018. https://www.agclassroom.org/gan/timeline/farm_tech.htm.

24. Neely, J, Derek Townsend, and Dominic Ricketts. “Megadeals in

Consumer Packaged Goods.” 15 February 2017. Strategy+Business,

7. “Agricultural Mechanization Timeline.” National Academy of Sciences,

https://www.strategy-business.com/article/Megadeals-in-Consumer-

2018. Greatest Engineering Achievements of the 20th Century, http://

Packaged-Goods?gko=d7e96

www.greatachievements.org/?id=3725.

25. “ 57 Varieties.” Tomato Heinz Seed. http://www.heinzseed.com/new/

8. Dimitri, Carolyn, Anne Effland, and Neilson Conklin. “The 20th Century

hs_about.html.

Transformation of U.S. Agriculture and Farm Policy.” Economic

Information Bulletin Number 3, United States Department of Agriculture,

Economic Research Service/USDA,June 2005. https://www.ers.usda. 26. Daniels, Jeff. “California’s tomato business is rotten — and farmers are

gov/publications/pub-details/?pubid=44198. Page 6. seeing red.” CNBC, 28 July 2016. https://www.cnbc.com/2016/07/28/

californias-tomato-business-is-rotten--and-farmers-are-seeing-red.html.

9. A

rnold, Carrie. “The Past, Present and Future of Agriculture.”

Smithsonian Digital Studio, 30 June 2016. Smithsonian.com, https:// 27. “2017 Tomato Paste and Processed Tomato Statistics.” The

www.smithsonianmag.com/science-nature/video-past-present-and- Morning Star Packing Company, 2017. http://morningstarco.com/

future-agriculture-180959618/. statdocs/2016%20Exhibits%20Brochure.pdf.

10. N

ielsen, R.L. “Historical Corn Grain Yields for the U.S.” Purdue 28. T

rebilcock, Bob. “Keeping it nimble at Kraft Heinz.” Logistics

University, May 2017. https://www.agry.purdue.edu/ext/corn/news/ Management, 28 February 2018. https://www.logisticsmgmt.com/

timeless/yieldtrends.html. article/keeping_it_nimble_at_kraft_heinz.

11. Nielsen, R.L. Ibid. 29. A

ngelini, Herter, and Stipanov. “All Retail is not Created Equal.”

Longpoint Realty Partners Review, Spring 2017.

12. D

imitri, Effland, and Conklin. Page 2.

30. “ 2018 Directory of Supermarket, Grocery & Convenience Store

Chains.” Chain Store Guide, March 2018. http://www.chainstoreguide.

13. K

ing, Lindsay. “Five of the ‘Big 6’ agricultural corporations, including

com/csgonline/industryinformation/supermarket.pdf.

Monsanto, looking to merge.” The Fence Post, 25 April 2017. Summit

Daily, https://www.summitdaily.com/news/five-of-the-big-6-agricultural-

corporations-including-monsanto-looking-to-merge/. 31. Springer, Jon. “Supervalu completes Unified deal.” Supermarket

News, 26 Jun 2017. https://www.supermarketnews.com/retail-financial/

supervalu-completes-unified-deal.

14. “DowDuPont Fact Sheet.” DowDuPont, May 2018. http://www.dow-

dupont.com/home/default.aspx.

32. 2

016 Kroger Fact Book. The Kroger Company.

http://ir.kroger.com/Cache/1500100492.

15. “ ChemChina Clinches Its $43 Billion Takeover of Syngenta.” Reuters,

PDF?O=PDF&T=&Y=&D=&FID=1500100492&iid=4004136.

5 May 2017. Fortune.com, http://fortune.com/2017/05/05/chemchina-

syngenta-deal-acquisition/.

33. W

ells, Jeff. “Kroger launches online portal for local product suppliers.”

Food Dive, 25 September 2017. https://www.fooddive.com/news/

16. “Bayer Closes Monsanto Acquisition.” 7 July 2018. Monsanto.com, https://

kroger-launches-online-portal-for-local-product-suppliers/505721/.

monsanto.com/news-releases/bayer-closes-monsanto-acquisition/.

34. S

amuel, Steward. “Why Walmart’s getting verticaly integrated.” IGD,

17. MacDonald, James A. “Mergers and Competition in Seed and

RetailAnalysis, 28 March 2016. https://retailanalysis.igd.com/news/

Agricultural Chemical Markets.” United States Department of

news-article/t/why-walmarts-getting-vertically-integrated/i/11036.

Agriculture, Economic Research Service, 3 April 2017. https://www.ers.

usda.gov/amber-waves/2017/april/mergers-and-competition-in-seed-

and-agricultural-chemical-markets/. 35. “ Industries at a Glance: Food Manufacturing.” Bureau of Labor

Statistics, United States Department of Labor. https://www.bls.gov/iag/

tgs/iag311.htm.

18. “ Crop Values: 2017 Summary.” United States Department of

Agriculture, National Agricultural Statistics Service, February

2018. http://usda.mannlib.cornell.edu/usda/current/CropValuSu/

CropValuSu-02-23-2018.pdf.36. Wells, Jeff. “Growing pains: Why supermarkets are struggling to source 47. CoStar. Accessed 15 November 2018. http://product.costar.com/home/.

local products.” Food Dive, 6 April 2017. https://www.fooddive.com/

news/grocery--grocery-source-local-vegetables-fruit-produce/440670/.

48. “The Grocery Distribution Network in North America.” MWPVL

International, Inc. http://www.mwpvl.com/html/grocery_distribution_

37. Jeff, W. Ibid. Page 5. network.html.

38. “ Say cheese: Journey from farm to fridge.” Casale, Lucy M. The 49. “Are Grocery Retailers Increasingly Outsourcing Distribution

Boston Globe, 8 August 2017. BostonGlobe.com, http://sponsored. Operations to 3PLs?” MWPVL International, Inc. http://www.mwpvl.

bostonglobe.com/vermont-tourism/say-cheese/. com/html/retail_3pl_outsourcing.html.

39. T

erry, Lisa. “Perishable Logistics: Cold Chain on a Plane.” Inbound 50. MWPVL International. Ibid.

Logistics, 20 January 2014. https://www.inboundlogistics.com/cms/

article/perishable-logistics-cold-chain-on-a-plane/.

51. “ C&S Locations, Northeast/Mid-Atlantic.” C&S Wholesale Grocers.

http://www.cswg.com/locations-northeastmid-atlantic.

40. S

prouts Farmers Market. Form 10-K, United States Securities and

Exchange Commission, 31 December 2017. http://investors.sprouts.

52. “ Our Locations.” Sysco. https://www.sysco.com/Contact/Contact/Our-

com/Cache/392296783.pdf.

Locations.html.

41. Sprouts Farmers Market. Ibid.

53. “ Wholesaling.” United States Department of Agriculture, Economic

Research Service, 10 October 2017. https://www.ers.usda.gov/topics/

42. “Fresh Foods and Flavors: How Multicultural Consumers are Driving food-markets-prices/retailing-wholesaling/wholesaling/

Fresh Grocery Trends.” Nielson.com, 4 November 2016. http://www.

nielsen.com/us/en/insights/news/2016/fresh-foods-and-flavors-how-

54. U.S.D.A. Ibid.

multicultural-consumers-are-driving-fresh-grocery-trends.html.

55. D

astin, Jeffrey. “Even with Whole Foods, Amazon would need many

43. “History: Our Story.” Goya Foods. https://www.goya.com/en/our-

more warehouses to reshape grocery delivery.” Reuters, 23 June 2017.

company/history.

https://www.reuters.com/article/us-whole-foods-m-a-amazon-com-

logistics/even-with-whole-foods-amazon-would-need-many-more-

44. “Diaz Foods opens state-of-the-art distribution center in Virginia.” The warehouses-to-reshape-grocery-delivery-idUSKBN19E2OK.

Produce News, 6 April 2015. http://www.theproducenews.com/9-news-

section/story-cat/15532-diaz-foods-opens-state-of-the-art-distribution-

56. “ 2018 Directory of Supermarket, Grocery & Convenience Store

center-in-virginia.

Chains.” Chain Store Guide, 2018. http://www.chainstoreguide.com/

csgonline/industryinformation/supermarket.pdf.

45. “Diaz Foods and Ryder.” Ryder System Inc, Case Study, 2015. https://

ryder.com/-/media/ryder/ryder-global/expertise/case-study_diaz-foods.

57. “ Median Store Size: Square Feet.” Food Marketing Institute. https://

pdf.

www.fmi.org/our-research/supermarket-facts/median-total-store-size-

square-feet.

46. “Infrastructure of Retail Food Distribution Network Within North

America.” Wholesale Grocer’s Directory, 18 February 2017. https://

wholesalegrocersdirectory.com/infrastructure-retail-food-distribution-

network-within-north-america/.You can also read