FX weekly: Time to call in Steven Seagal - Nordea

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

12 August 2018

FX weekly: Time to

call in Steven Seagal

Martin Enlund | Andreas Steno Larsen

Further Turkish spill-overs to the Euro area keep us short in EURUSD and with

tensions on the rise between US and China, Russia and Turkey at the same

time, risks of an asymmetrical retaliation strike are rising. Is it time to call in

Steven Seagal?

Table 1: Our current list of convictions

First, before engaging in more esoteric stu, we oer some FX quickies for those of a tactical persuasion.

• EUR/USD: still downward biased after breakdown. Spill-overs from the Turkey

have broken the 1.1448 support which is now a new ceiling. Next support seen

at 1.12 (1.1187).

• EUR/NOK: rising liquidity a seasonal problem for the NOK even as a first rate

hike beckons. Shorts should stay away for a few more weeks. (We prefer a side-

lined approach for now)

• EUR/SEK: Swedish politics and weak inflation has paved the way for an upside

break-out. We still recommend to buy-on-dips.

• EUR/GBP: Sell on rallies above 0.90, as Bank of England doesn’t tolerate a

much weaker GBP.

• AUD+NZD: The weakness looks overdone in both, as the Chinese liquidity

injection could be helpful down the line.

Whoop-de-doo. The market was in some kind-of melt-up mode based on negative positioning and Chinese

stimulus, until it had to consider spillovers from the stued bird down south. Erdogan doesn’t want to seem to

play by the market’s (or the US’) rules: “they have got dollars, we have got our people, our right, our Allah”. At

some point, countries such as China, Russia and Turkey might decide to strike back asymmetrically (time to

call in the new man in charge of US/Russian relations, Steven Seagal?).

e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagalRecently we have actually been thinking about whether or not it was time to reduce or even change our generally EUR/USD-negative stance. For instance, positioning in dollars has come a far way since the beginning of this year, US growth will eventually decelerate vs the rest of the world, Euro-area core inflation is set to pick up this autumn, the US mid-term election could also reignite discussions about US political risks, and so on. Our ruminations have led us to keep our negative stance for now, for instance due to the likelihood of further Turkish spillovers. Chart 1: Is both EUR/USD and the US 10y yield breaking lower? We also recently argued that longer-term investors may want ponder starting to accumulate select EM assets (though definitely not TRY and ZAR). Turkey wrong-footed that idea (or postponed it…), however, and we just experienced a nasty breakdown in broader EM FX indices. Performance was far from uniform though. Asian FX held up very well over the past week, with the biggest losers vs the USD instead including TRY, RUB, ARS, BRL and – only somewhat oddly - the SEK. We still think the coming weeks and months will provide nice entry-opportunities for EM investors. If the US 10y yield breaks lower it would eventually be good news for EM & yield-chasing, though the reason why the 10y may be heading lower is not. In short, the dust from the crashing Turkey needs to settle first... e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

Chart 2: US core inflation pick-up helpful for the dollar The US inflation surprise in July, with an acceleration in core inflation (2.4% vs expectations of 2.3%), provided another reason why we have landed in the conclusion that going long EUR/USD is too early. The core inflation spread has led the EUR/USD nicely since 2008, and rising US core inflation underpins the scope for Fed hikes which in turn is helpful for the greenback. We thus keep our negative stance on EUR/USD. SEK: no currency for hawkish men When the Riksbank started with QE and negative rates, core inflation stood at 1.28%. Now, after 3.5 years (and a 12% rise in EUR/SEK), core inflation reads 1.29%. This is lower than its long-term average: since 1996, CPIF ex. energy has averaged 1.32%. One might almost conclude that engaging in inflation targeting is a fool’s errand… The disappointing inflation reading in July nonetheless indicates a flattening of the Riksbank’s rate path at the September meeting. This is hardly SEK-positive. e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

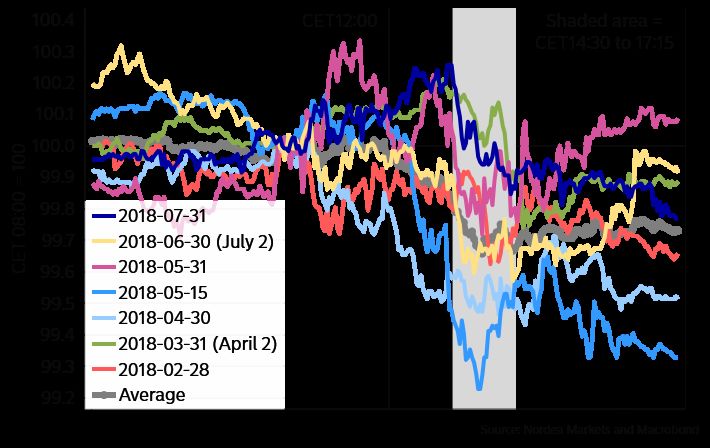

Chart 3: Swedish core inflation has risen by a very meagre 0.01pp in 3.5 years EUR/SEK’s move higher over the past week was also driven by rising attention on the Swedish election. We keep our view that EUR/SEK is a buy on dip (reasons include a soft Riksbank, a cyclical slowdown, potential for renewed housing worries and some modest potential for a political risk premium). US liquidity to be drained by 12.6bn on Wednesday We have earlier concluded that the USD tends to gain on days when the Fed's balance sheet shrinks due to maturing bonds & notes. We call these days "SOMA days", since the maturing bonds are held in the Fed's System Open Market Account. Indeed, of the SOMA days since February 28, it has been a good idea to sell EUR/USD at CET14:30 and close the position a few hours later. The hit ratio of going long DXY at CET09:00 on SOMA days, and closing the position CET17:30 is 100% since February… The next redemption is coming up on Wednesday August 15 (implying a net negative eect on US liquidity by 12.6bn). e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

Chart 4: EUR/USD intraday on SOMA days GBP: Volatility in potential Brexit outcomes has increased Sterling has been hammered (in particular versus the USD) by comments from both Mark Carney and Trade Secretary Liam Fox hinting that the implied probability of a no-deal Brexit is on the rise. At the same time as the no-deal scenario looks increasingly likely, calls for a new referendum are also gaining traction in the UK – and judging from betting markets, the implied odds of Britain actually exiting the EU by March 29 next year has fallen below 50%, in the aftermath of Carney and Fox’s comments. This development widens the potential outcome space of the Brexit-negotiation severely. Odds of a hard and sudden Brexit are on the rise and the chance of a new referendum or a material prolongation of the negotiation-process the same, while the likelihood of an orderly exit by March 29 seems to vanish by the day. This leaves a tricky scenario ahead for Bank of England, as they try to limit the downside in GBP due to inflation considerations (FX weekly: Is the cyclical momentum over-priced?). The best way to bet on GBP weakness is via short cable still (rallies above 0.90 in EUR/GBP should be sold into). e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

Chart 5: Larger implied chance of no-Brexit, but a weaker GBP. The volatility of potential Brexit outcomes has increased AUD & NZD: Classic central bank divergence? RBA joined the ranks of recent slight hawkish twists made by BoJ and BoE last week, as the newly adopted two-way communication on the AUD was confirmed. After 25 meetings in a row with cautions taken on an “appreciating AUD”, RBA opted for a change of wording on the AUD in July and now simply communicate that “AUD is trading within its recent range”. This is probably as explicit a central bank can be in terms of communicating their satisfaction with the current exchange rate level. RBNZ on the other hand kept a very dovish approach and communicated that rates will stay on hold throughout 2019-2020 and “that the next move in the OCR can be both up and down” (no shit, Sherlock). But considering their wording on the NZD “There are welcome early signs of core inflation rising. Inflation will increase towards 2 percent…. This path may be bumpy however, with one-o price changes from global oil prices, a lower exchange rate and… We will look through this volatility as appropriate, and only respond to any persistent movements in inflation.” they don’t sound like a central bank that openly invites a weaker NZD, as they would look through such one-o eects. So was the sell-o in NZD a little overdone last week? We tend to think so. The slighly diverging paths of RBA and RBNZ obviously leaves upside risks to the post 2014 trading range in AUD/NZD, but for now AUD/NZD looks a little too spiky to be a compelling long. e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

Chart 6: The RBA has feared an appreciation of the AUD for a quite a while, but no more! We wrote last week that we considered taking profit in short AUD/USD below 0.73 (we have been short since 0.80) and since we are now there, we close down our short AUD/USD. Both due to the change of communication from RBA and due to the flood of liquidity that PBoC have poured on the Chinese momentum (look at O/N SHIBOR). Within 6-9 months (as per the usual lag-time) you should expect Chinese lending growth to have picked up markedly again, due to the substantial cheapening of money that the recent SHIBOR-drop has caused. This could be seen as an AUD positive signal (as also Asian FX will likely fare better against the USD) down the line. We look into the possibilities of adding an AUD long, but decide to sit on our hands this week. e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

Chart 7: Chinese markets have been flooded with cheap CB liquidity – and SHIBOR drops as a consequence (note the reversed right-axis). Expect credit growth to pick up markedly again soon Previous FX weeklies: ·FX weekly: Is the cyclical momentum over-priced? (05 Aug) ·FX weekly: How to trade a cease-fire? (29 Jul) ·FX weekly: What's that curve? (22 Jul) ·FX weekly: The China Factor (15 Jul) ·FX weekly: Take a short trade war breather (08 Jul) ·FX weekly: Trump will never #238 (01 Jul) ·FX weekly: The USD is the best carry currency in the world (24 Jun) ·FX weekly: Dollar to provide headwinds for earning estimates (17 Jun) ·FX weekly: Fire and fury risks for the USD (10 Jun) ·FX weekly: It's not only Italy.. (03 Jun) ·FX weekly: The Sumo SOMA days (27 May) ·FX weekly: EM won't be sprinting, if the Fed is unprinting (20 May) e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

·FX weekly: The two final nails in the dovish FOMC-con (13 May) ·FX weekly: Is there anything left in the USD bull-run? (06 May) ·FX weekly: Dragon Energy (29 Apr) ·FX weekly: Relative curvature is the new king of FX (22 Apr) ·FX weekly: Why is EUR/USD not trading lower? (15 Apr) ·FX weekly: Like watching paint dry, they said (08 Apr) ·FX weekly: The list of potential USD-positives is getting longer (01 Apr) ·FX weekly: 2 reasons why EUR/USD has decoupled from rates spreads (25 Mar) ·FX weekly: Time to buy a USD lottery ticket? (18 Mar) ·FX weekly: Taxation mirror on the wall, who is the fairest of them all? (11 Mar) ·FX weekly: Trump's game of chicken (04 Mar) ·FX weekly: Will the market neglect the clutch of canaries? (25 Feb) ·FX weekly: Is the correlation break-down driven by FX hedges? (18 Feb) ·FX weekly: The liquidity tide is ebbing (11 Feb) ·FX weekly: Hawkish spectacles (04 Feb) ·FX weekly: Who will stop EUR/USD from moving higher? (28 Jan) ·FX weekly: Did the Democrats dent the Dollar? (21 Jan) ·FX weekly: Is 1.25 the new 1.20? (14 Jan) ·FX weekly: The euphoria rises (07 Jan) ·FX weekly: Paging Dr. Pangloss (01 Jan) ·FX weekly: The R-star of Bethlehem (24 Dec) ·FX weekly: A numbers game (17 Dec) ·FX weekly: The year-end liquidty shrink (10 Dec) ·FX weekly: Three reasons why EUR/USD isn't trading lower (03 Dec) ·FX weekly: Which currencies to sell if the housing downturn continues? (26 Nov) ·FX weekly: The global industrial cycle is set to weaken (19 Nov) ·FX weekly: Is high-yield a canary in the global coal mine? (12 Nov) e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

·FX weekly: Is this the end of the inflation convergence trade in EUR/USD? (5 Nov) ·FX weekly: Was that it for the EUR bulls? (29 Oct) ·FX weekly: Hawks in opposition, doves in charge (22 Oct) · FX weekly:Continued convergence or re-divergence?(15 Oct) ·FX weekly: Thingsdon't matter until they do(08 Oct) ·FX weekly:"October seasonality is strong" (01 Oct) ·FX weekly:“Is 1.20 the new 1.15?”(24 Sep) · FX weekly:Honey, I shrunk the balance sheet(17 Sep) · FX weekly: “USD liquidity will turn scarcer, but when?” (10 Sep) · FX weekly:“Strong currencies and inflation”(3 Sep) · FX weekly:“USD in the (Jackson) hole” (27 Aug) · FX weekly:“Q4 is the USD quarter”(20 Aug) · FX weekly:“In the year 2525”(13 Aug) · FX weekly:“EUR/USD ceiling or debt ceiling?”(6 Aug) · FX weekly:“Elevator up, stairs down “(30 Jul) · FX weekly:Trump “spices” up EUR/USD(23 Jul) · FX weekly:Flip-flop?(16 Jul) · FX weekly:Consolidation time?(9 Jul) · FX weekly:Hawks R Us(2 Jul) · FX weekly:Another lowflation week?(25 Jun) · FX weekly:No Fed put?(18 Jun) · FX weekly:A bouncy dollar?(11 Jun) · FX weekly:Heating up(4 Jun) · FX weekly:Summertime sadness(28 May) · FX weekly:Special counsel lessens Trumpbulence, while OPEC looms(21 May) · FX weekly:Are China worries old hat?(14 May) · FX weekly:Inflation week…(7 May) e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal

Martin Enlund Andreas Steno Larsen

Chief Analyst Global FX/FI Strategist

Martin.Enlund@nordea.com andreas.steno.larsen@nordea.com

+45 55 46 72 29

e-markets.nordea.com/article/45546/fx-weekly-time-to-call-in-steven-seagal28.9.2017 1 DISCLAIMER Nordea Markets is the commercial name for Nordea’s international capital markets operation. The information provided herein is intended for background information only and for the sole use of the intended recipient. The views and other information provided herein are the current views of Nordea Markets as of the date of this document and are subject to change without notice. This notice is not an exhaustive description of the described product or the risks related to it, and it should not be relied on as such, nor is it a substitute for the judgement of the recipient. The information provided herein is not intended to constitute and does not constitute investment advice nor is the information intended as an offer or solicitation for the purchase or sale of any financial instrument. The information contained herein has no regard to the specific investment objectives, the financial situation or particular needs of any particular recipient. Relevant and specific professional advice should always be obtained before making any investment or credit decision. It is important to note that past performance is not indicative of future results. Nordea Markets is not and does not purport to be an adviser as to legal, taxation, accounting or regulatory matters in any jurisdiction. This document may not be reproduced, distributed or published for any purpose without the prior written consent from Nordea Markets. Nordea Bank AB Hamngatan 10 SE-105 71 Stockholm www.nordea.com

You can also read