GUALA CLOSURES INVESTOR PRESENTATION - SPACE4 SPA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Guala Closures Investor Presentation Palazzo Parigi, Milan – 2nd May, 2018

Disclaimer This document has been prepared by Space4 S.p.A. (“Space4”), Guala Closures S.p.A. (“Guala Closures”) and Lazard exclusively for use in the presentation of the envisaged business combination between Space4 and the Guala Closures. Neither this presentation nor any part or copy of it may be transmitted into the United States or distributed, directly or indirectly, in the United States, Australia, Canada or Japan or any other jurisdiction where distribution of this presentation and of any information contained in it may be restricted by law. Persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. This document is not intended for potential investors and is not to be used or considered as on offer to purchase or subscribe for, or a solicitation of any offer to purchase or subscribe for, any securities, nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision. This document has been prepared separately from any proposed offering of securities and as such and to such extent information in this document has been reviewed and approved by Space4 and Guala Closures. The securities of Space4, before or after the business combination, have not been, and will not be, registered under the United State Securities Act of 1933, as amended (“Securities Act”), or under the corresponding rules and regulations applicable in Canada, Japan, Australia or in any other jurisdiction where an offer is unlawful absent exemption or authorization by the competent authorities and may not be offered or sold to any national, resident or citizen of the United States, Canada, Australia, Japan or any other county where an offer is unlawful absent exemption or authorization by the competent authorities. This document constitutes neither an offer of securities in Italy pursuant to article 1, (t) of the Legislative Decree No. 58 of 24 February 1998, as amended, nor an offer of securities for sale in the United States and in any other jurisdiction The information contained and the opinions expressed in this document have not been independently verified. In particular, this document contains forward-looking statements that are based on current estimates and assumptions made by the management of Guala Closures to the best of their knowledge. Such forward-looking statements are subject to risks and uncertainties, the non-occurrence or occurrence of which could cause the actual results including the financial condition and profitability of Space4 and the combined entity resulting from the envisaged business combination to differ materially from, or be more negative than, those expressed or implied by such forward-looking statements. Consequently, Space4, Guala Closures and their respective management can give no assurance regarding the future accuracy of the estimates of future performance set forth in this document or the actual occurrence of the predicted developments. The data and information contained in this document are subject to variations and integrations. Although Space4 reserves the right to make such variations and integrations when it deems necessary or appropriate, Space4 assumes no affirmative disclosure obligation to make such variations and integration and no reliance should be placed on the accuracy or completeness of the information contained in this document. No person accepts any liability whatsoever for any loss, damage or other consequences howsoever arising from the use of this document or of its contents or otherwise arising in connection therewith. By accepting this document, you agree to be bound by the foregoing limitations.

Today’s speakers

Marco Anibal Francesco Paolo Claudia

Giovannini Diaz Bove Ferrari Banfi

Chairman and Group CFO Group COO Group CMO Group FD and

Group CEO Investor Relation

Roberto Carlo Edoardo

Italia Pagliani Subert

Senior Partner Senior Partner Senior Partner 1

Table of contents 1 Introduction 2 Why Guala Closures 3 Positioning and Trends in Key Target Markets 4 Operational Excellence 5 Financial Performance 6 Transaction Description

1. Introduction

Space Holding – a history of successful combinations

• Space4 is the fourth and largest SPAC ever promoted by Space Holding listed on December 2017

on MIV (Market for Investment Vehicles) with a market capitalization in excess of Euro 500m

• Proven track record of Space Holding team, with over Euro 400m equity invested to date in three

success story IPOs: FILA, Avio and Aquafil, with a current combined market capitalization of c.

€1,7bn

– FILA total shareholders return: c. +158% (x2.6) Listed in June 2015

– Avio total shareholders return: c. +68% (x1.7) Listed in April 2017

– Aquafil total shareholders return: c. +37% (x1.4) Listed in December 2017

• Seeking for the next IPO champion: an Italian company with a leadership positioning, international

footprint, untapped growth potential, entrepreneurial talent and a strong management team

2

Source: Space4 information

Note: Data as of 24th of April 2018

Our target of choice: Guala Closures

• The Global leading producer of specialty closures for the spirits and wine

industry with almost €600m turnover

• A trusted partner to most global and local spirits and wine producers for

the last 40 years

• A business model driven by unique technology & innovation capabilities,

supported by an R&D DNA and by a state-of-the-art manufacturing

footprint spread across 5 continents

• A resilient story of growth - margins consistently at 20%+ in the last 15

years

• A natural consolidator in a fragmented market space, ready for additional

expansion opportunities

• An entrepreneurial management team with a long-lasting experience in

the sector and deeply invested in the business

A single transaction deploying €600m of cash equity for an aggregate equity value of approx. €700m

3

Source: Guala Closures information

A truly global firm >14bn Closures sold worldwide 5 Innovation Centers 27 Production sites across 5 continents 100 Countries where we have built strong client partnership >4,200 Employees 4 Source: Guala Closures information

Guala Closures leadership team

• A close-knit team working together more than 20 years

• Structured organization chart ready to sustain the future growth

Marco Giovannini, Chairman and Group CEO Anibal Diaz, Group CFO

Professional experience in packaging: 36 years Professional experience in packaging: 32 years

Joined Guala Closures Group: 1998 Joined Guala Closures Group: 2000

Francesco Bove, Group COO Paolo Ferrari, Group CMO

Professional experience in packaging: 37 years Professional experience in packaging: 36 years

Joined Guala Closures Group: 1999 Joined Guala Closures Group: 1981

5

Source: Guala Closures information

2. Why Guala Closures

Marco Giovannini

Chairman and Group CEOThe leadership team is not alone: our general managers across the world

6Guala Closures at a glance

7The world’s leading specialty closures producer

#1 player in high value-

A global champion - Euro Partner to global and Pioneer in closures Proven track record of

added closures for spirits

535m sales in FY17 local beverages players technology growth

and wine

Safety Luxury Wine Roll-on Others

Sales breakdown by product Sales breakdown by destination market Sales breakdown by geography(3)

(2)

Other (1) Non-alcoholic Africa

5% 14.0% Oceania 3%

Pharma

1% 9%

Roll-on Safety Oil &

44% Asia

28% vinegar Europe (West

13%

2% & East)

Spirits 54%

63%

Wine

20%

Wine Americas

20%

20% Luxury

3%

Source: Guala Closures information

(1) Other includes Pharma, PET and other revenues 8

(2) Non-alcoholic includes mineral water, beverage, other markets, PET and other revenues

(3) Revenues breakdown refer to countries from which the product is soldOur Mission

• Protect your brand

• Create your value

9Global counterfeiting never ends

Percentage of

counterfeit

S P I R I T S A R E T H E 4 TH L A R G E S T products in total

C O U N T E R F E I T E D P R O D U C T C AT E G O R Y manufactured

goods:

25% Audiovideo

30% OF THE ALCOHOL CONSUMED IN THE 21% Fashion

WORLD IS UNREGISTERED 20% Pharmaceutical

12% Spirits

12% Toys

* source Olajide Oyewole 10% Perfumery

5% Watches

* source INDICAM

“Illicit spirits are a huge social problem in India, both in terms of

yearly deaths and support to the illegal economy”

– Former manager, United Spirits

10A pioneer in multicomponent non-refillable systems

Model 1612A safety closure:

• High protection closure

• Includes covert and overt anti-

counterfeit technologies

• 11 components

Overcap

• Assembled at high speed HIPS

Screw Cap

ABS

Tamper-evident ring

ALUMINIUM

Sealing wad

Valve system LDPE

PC

Pourer

PC

Sleeve Glass balls

HIPS GLASS

Washer

LDPE

11

Source: Guala Closures informationSpirits: premiumisation race boosts luxury closures offer

12Reinventing closures: from commodity to high value-added

Premiumisation

Standard Luxury

Safety Highly Decorated Premium

€15 €70 €250 €125 €700 €2,200

13

Source: Guala Closures informationWine: shift from cork to screw caps

€40 €90

February 2018

14

Source: Guala Closures informationIs it the closure or the wine?

Overall impact of different closures on wine quality

More than 5 years ageing

15

Source: Guala Closures informationScrew caps: from easy-to-use to value added

16An innovative and broad product line for wine closures

Standard Premium Roll On TE

Designed to maintain Top quality closure The first Tamper Evident

quality, freshness and full with an internal system specifically

flavour thread for still wines dedicated to standard

and a premium aluminium closures

finishing

Divinum Savin Premium

WAK

Content quality Content quality Content quality

Content Quality Content Quality

preservation

preservation preservation

preservation

Content Quality

preservation

preservation

Cost Anti- Cost Anti- Cost Anti-

Cost effectiveness

effectiveness Anti tampering

tampering Cost effectiveness Anti tampering

effectiveness tampering Cost effectiveness

effectiveness Anti tampering

tampering

ProductPackaging Brand

Brand Protection

ProductPackaging Brand ProductPackaging Brand

innovation Brand Protection Brand Protection

innovation

innovation protection innovation protection innovation

innovation protection

Packaging Packaging

Packaging

exclusivity and Packaging

exclusivity and

Packaging

Packaging

exclusivity and

exclusivity

distinction and exclusivity

distinction and exclusivity

distinction and

distinction distinction distinction

Oenoseal®

Content quality

The new range of liners with different level of Content Quality

preservation

preservation

oxygen permeability rates

Cost Anti-

Cost effectiveness

effectiveness Anti tampering

tampering

Onyx Ivory Coral

ProductPackaging Brand

by Oenoseal® by Oenoseal® by Oenoseal® innovation

Brand Protection

innovation protection

Packaging 17

Packagingexclusivity and

exclusivity

distinction and

Source: Guala Closures information distinctionA pioneer, R&D DNA: 140 patents(1) / 50 projects in pipeline

Premiumization Consumer Trends and

Customer needs

strategy insights market studies

Content quality

preservation

Content Quality

preservation

Cost Anti-

effectiveness

Cost effectiveness

tampering

Anti tampering

Brainstorming Product

Packaging Brand

Brand Protection

Product design innovation

innovation protection

Materials IP Protection Packaging

exclusivity and

and technics Packaging

distinction

exclusivity and

distinction

Production tools

Aesthetical

studies

Red: spirits

Lab tests Blue: wine 18

Source: Guala Closures information

(1) Patents include industrial designs and utility modelsAlways pioneering innovative closures

Strong track record in Innovation: milestones

550 2600 Nip Cap 1612 WAK

1954 1991 2002 2008 2014

1978 1993 2003 2011 2016

1031 Sabina

1235 Spring Kirk

19

Source: Guala Closures informationBringing smart-security solutions to spirits and wine market

Guala Closures partnered with Semiconductors to develop the first “Internet-of-Closures system”

Internet-of-Closure (IoC) is

For Guala Closures

Disruptive technology

First-mover advantage

Supply management

Potential for higher margin

For Brands For Consumers

Improve brand experience Product authentication

Supply chain control Tamper evident

Story telling Channel authentication

Store locator Tasting and recipes

20Gravitas: an example of a totally proprietary specialty closure

• Heavyweight filled polymer targeting luxury closures

• Plastic versatility together with metal touch-and-feel

• Greater design freedom with a wider choice of finish and weight

Mortlach Dewar’s Royal Salute Royal Salute Johnnie Ultis Chivas Zacapa Jack Daniel’s Patron

18 years Standard Eternal Reserve Walker XR 150

2014 2014 2014 2014 2015 2016 2016 2016 2017

Thanks to Gravitas we won all of the above brands over the last 3 years

21

Source: Guala Closures informationInnovating through our Italian design approach

22Trusted partner for global players and regional champions

Global Players Regional Champions

Spirits

Wine

Other

(F&B,

Pharma)

23

Source: Guala Closures information3. Positioning and Trends in

Key Target Markets

Paolo Ferrari

Group CMOThe world’s leading global specialty closures producer

Size Major specialists

(wine & spirits

closures €m

revenues)

> €500m Large closure producers with

strong presence in W&S,

accounting for a small part of

Revenues from safety closures are 6 times greater

their business than closest competitor 6x

Major generalists

Revenues from wine screw caps are 4 times greater

than closest competitor 4x

> €50m “Regional

Large packaging champions”

companies with Core specialists

limited presence in

W&S and/or closures

Core generalists

Local producers of

standard decorative

> €10m closures

Small local players

< 20% > 60% Focus

(wine & spirits closures % revenues)

24

Source: Guala Closures information2017 revenue breakdown by market & product

Others

Pharma 6%

1%

Beverages

10% Safety

44%

Wine

20%

Spirits

63%

Roll-on Luxury

16% 3%

Source: Guala Closures information 25

Beverages includes oil & vinegar, mineral water, soft drinks and other beverages

Others include Pet, other revenuesTrends in Spirits

Different market maturity drives to different market needs

Western Markets New emerging markets

India

Africa

26Western markets: new consumer aspirations

PREMIUMISATION CRAFT FLAVOURING WELLNESS ETHICAL INTERNET

27

Source: Guala Closures informationNew emerging markets: consumer aspirations

AFFORDABLE SMALL PACKS FRIENDLY TO USE SAFETY GLOBAL BRAND LOOK-LIKE

28

Source: Guala Closures informationGrowth driven by premium and emerging markets

Global market size by value – 2011-2021 Top Regions Market size by value - 2016

US$b, CAGR 11-16 | 16-21 (%) US$b, CAGR 16-21 (%)

CAGR CAGR

4.6% 2016-21 (%) 2016-21 (%)

828.8

Asia (excl. Japan) 297.3 7.3%

5.4%

662.1 Latin America 41.0 3.2%

499.2 6.9% Africa 19.5 8.2%

508.8

357.8 West Europe 105.4 1.4%

Asia (excl. Japan),

Latin America, 227.2 North America 91.9 2.8%

Africa

East Europe 63.5 0.4%

Europe,

North America, 304.3 329.6 1.6% Japan 33.8 0.8%

281.6

Japan,

Australasia Australasia 9.7 2.5%

2011 2016 2021

29

Source: GlobalDataLeader in fast-growing end markets

# 1 globally in the fastest growing safety closures market(1) Trusted partner of top spirits producers for premium/luxury

Guala Closures’

Billion 26.0 27.0 market share(2)

Units +8.3%

16.0% 23.0%

>60%

84.0% -1.0% 77.0%

1 Safety closures

for spirits

Total market Total market

2011 2016

Standard Safety CAGR 2011-16

Reference player for the regional brands(2) Positioned in the fastest growing segments

Volume CAGR 2016A-21E closures markets(3)

Global

brand 30% Luxury +8.2%

70% Regional Safety +4.2%

brands

Source: Guala Closures information

(1) Guala Closures reference market; i.e. the market that Guala Closures was historically competing in 30

(2) Represents market share by volume

(3) Guala Closures core market; i.e. including metal screw and core cork closures (all pack types) and excluding other closuresTrends in Wine

Shift from cork to wine screw caps

# Wine Screw Caps 2008A-2021E

(billion units)

31

Source: EuromonitorIncreasing screw caps penetration

Wine screw caps global market

Penetration across Still & Sparkling Wines

Total market (excludes Other)

(billion units)

% Wine

30.2 Screw Caps

29.0 100

90

80

70 85%

60 70%

82.0% Other 77.9%

50

40 44%

42%

42.6%

30

20

22.1 18.5%

18.0% Wine

17% 16.5% 16%

% 10

Screw 8%

0

2011 Caps 2016 0 5,000 10,000 15,000 20,000 # Closures

(millions, by

bottling location)

Guala

Closures’ 1 Screw caps

market

>30% for wine

share

32

Source: Guala Closures informationWine screw caps growth drivers

Market trends Screw caps competitive advantages

Growth in export Quality Guarantor

Industrial Approach

Globalization

Supply Proximity

Growth in new emerging markets Widespread acceptance

Cost saving Superior value Proposition

the driving force behind screw cap market expansion

33

Source: Guala Closures informationWine global exports by value

Euro billions

29

28

26 26

25

23

21

20 20

18 18

16

15 15 15

12 12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

34

Note: Wine global exports by value considered as the sum of exports of 83 examined countries

Source: OIVWine production is highly concentrated in Guala Closures key countries

Main Production Countries and Guala Closures Industrial

Countries, top 8 by wine production 2016

presence

(Mhl liters)

267 Worldwide production

203

Chile 10.1 3.6 %

South Africa

10.5

3.8 %

China 11.4 4.1 %

Australia 13 4.7 %

USA 23.9 8.6 %

Spain 14.6 %

40.5

France

44.8 16.0%

Italy

49.8

18.0% Market covered by Guala Closures

2016

% of total 73.4 %

35

Source: OIVConsumption growth is expected to accelerate especially in new emerging

markets

Countries, top 7 by wine consumption (2016) Regions, expected wine consumption CAGR (2016-2020)

(Mhl liters)

CAGR

242 Worldwide consumption +2.2%

141.6

China

17.3

USA North America Europe Asia Pacific

31.8 CAGR CAGR CAGR

+1.8% +1.1% +4.0%

UK 12.9

Germany

20.2 LATAM Africa & M. East Oceania

Spain 9.9 CAGR CAGR

Europe +3.8%

Italy +4.2%

22.5

France

27.0

Growth is expected to be faster in Emerging

2016 Regions (China included)

% of

total 58.5%

Source: OIV Osservatorio Vini, Passport 36Trends in beverages: the glass bottled water market

Bottled water trends

• Bottled water market forecasted growth 2016-2021 at 3.2% CAGR

• Luxury segment growth in both western and new emerging markets

Paris Beijing

37

Source: Guala Closures informationMineral water and soft drinks markets growth

Global volumes of Mineral Water and Soft drinks glass bottles by type of closures – (2011-2021)

Mln units, CAGR 2011-16-21 (%) Others Metal Screw

Mineral Water (Glass) Soft drinks (Glass)

1.3% CAGR

-0.5% 2016-21

102.8

98.5 96.1

3.2% CAGR

1.3% 2016-21

27.2 73.5 1.0%

23.2 74.9 69.9

21.7

12.0 4.0%

9.9 9.8

13.3 15.2 2.7% 29.3 2.2%

11.8 23.6 26.2

2011 2016 2021 2011 2016 2021

Fastest growing regions Fastest growing regions

CAGR 2016-21 CAGR 2016-21

Latin Eastern North Eastern Western

China

America Europe America Europe Europe

4.9% 3.6% 27.5% 3.9% 2.1% 1.6%

38

Source: PassportGrowing luxury trend in the bottled mineral water segment

394. Operational Excellence

Francesco Bove

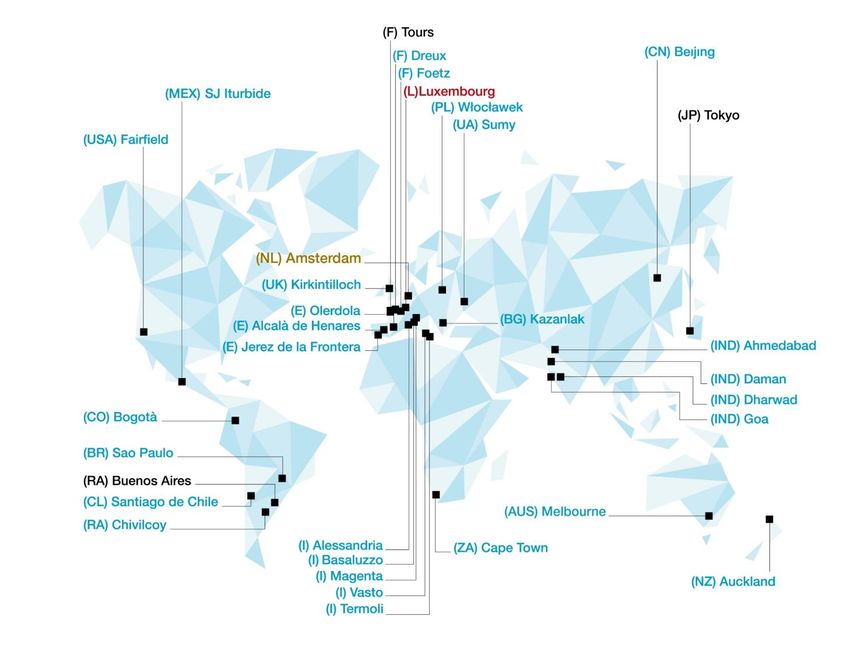

Group COOGlobal footprint to serve clients across geographies

Western Europe

(L) Luxemburg

(N) Netherlands

Eastern Europe (F) Tours

(F) Dreux

(UK) Kirkintilloch

(S) Olerdola

Western Europe (S) Alcalà de Henares

€112m (S) Jerez de la Frontera

(I) Alessandria

€74m (I) Basaluzzo

Asia (I) Magenta

€178m (I) Vasto

Americas €191m (I) Termoli

€72m Eastern Europe

(PL) Wloclawek

€76m (BG) Kazanlak

€107m (UA) Sumy

€120m Americas

(USA) Fairfield

Oceania (MEX) SJ Iturbide

(CO) Bogota

(BR) Sao Paulo

(CL) Santiago de Chile

€49m (AR) Buenos Aires

€49m (AR) Chivilcoy

Asia

€17m (CN) Beijing

(JP) Tokyo

€25m (IND) Ahmedabad

Sales offices (IND) Daman

(IND) Goa

Africa (IND) Dharwad

2017 net revenues: country from which the product is sold

2017 net revenues: country to which the product is sold Oceania

(AUS) Central West

(NZ) Auckland

Africa

27 plants and 3 sales offices in 21 countries on 5 continents (ZA) Cape Town

Source: Guala Closures information

40Full state-of-the-art manufacturing capabilities

World-class design and engineering

Vertical integration

In-house moulding

Aluminium sheet cutting and de-greasing

capabilities

High productivity

High-speed and customised assembly

Full suite of decoration capabilities

Capacity utilization and

Focus on continuous improvement and expansion

quality control

41Unique design and printing capabilities

Product

3D and Pilot Product Production

3D design

samples process tooling validation equipment

FMEA (1)

Case study: Sunrise closure

45 days for pilot

2 weeks to plastic and Closure validated Up to 9 months

3 days to print

conceptualise FMEA(1) process aluminium for scale for mould

prototypes

new design moulds to be production development

ready

c.12-18 month process from concept development to industrialisation

42

Source: Guala Closures information

(1) FMEA: Failure Modes and Effects AnalysisProprietary, in-house approach to manufacturing and related innovation

Sources of competitive advantage

In-house mould design and production capabilities

Equipment

Retention of IP rights through direct mould ownership

Long-lead time for mould development contributes to

locking in customers

In-house mould capabilities

Guala Closures Tools(1) designs and manufactures 70% of our

moulds

Moulds

Dedicated selection of components from leading world

suppliers (such as Mould Masters, Husky and Hasco)

43

Source: Guala Closures information

(1) Guala Closures Tools is located in the Guala Closures Bulgaria plant and has 55 dedicated employeesOur approach to manufacturing and production targets fully sustainable

development

Based on commitments we designed in 2011, our sustainability strategy

focuses on 3 pillars (Planet, People and Business) and 12 indicators, all

published regularly in our sustainable development annual report

44Emission reduction policies

Objective: offset part of the CO2 emissions

generated by the factories

Strategy: to fund reforestation projects

and/or convert energy produced into

renewable sources

2012 - 2018

Approximately 200,000 tonnes of CO2

compensated

Reforestation Projects

Social Reforestation programmes supported by GCG Social schools projects in India

Peru, India, Colombia, Mexico • 15,080 students of elementary schools

300,000 trees • 322 sessions

Over 5,600 people involved • 110 schools

455. Financial Performance(1)

Anibal Diaz / Claudia Banfi

Group CFO / Group FD and Investor Relation

(1) Financial performance figures have been taken from GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated

accounts after Group Structure reorganizationA consistent track record of profitable growth

Net Revenues CAGR 2007A-17A +5.1% / Adj EBITDA CAGR 2007A-17A +5.2%

(in €/m)

00.0 570 30%

521 535

497 494 488 500

00.0

418 25%

00.0 371

326 325 311

00.0 22% 20%

22% 21% 21% 21% 20% 21% 21%

20% 20% 20%

20%

00.0

103 102 106 103 111 118 15%

81 88 96

00.0 67 67 69

- 10%

2007A 2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015A 2016A 2017A 2018E (1)

Net Revenues Adjusted EBITDA Adjusted EBITDA Margin

Resilient business profile with margins consistently at 20%+ over the years

Source: Guala Closures information 46

(1) Calculated on 2018 mid-point guidanceEnhanced by M&A

Guala Closures has been able to expand via M&A consolidating its presence in new segments and strategic markets

Axiom

Technologia

Propack

70% acquired 100% acquired

Guala Closures

Danik MCG Limat

delisting

70% acquired 100% acquired Assets acquired

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Auscap Guala Closures Plastivit

CapMetal ICSA

100% Mexico 100% acquired

70% Assets

Stake increased to

acquired acquired

ESVIN 100% DGS

Assets acquired 70% acquired

Pharma Trade

100%

New markets (e.g. Australia, Successful integration

Poland, Ukraine, Africa) Consolidated market

resulting in substantial

position and captured

New segments (e.g. wine, growth and cost

further market share

pharma) synergies

Source: Guala Closures information 47Consistent growth over the years

Revenue (€m) • Revenue growth between FY16 and FY17 (+7%) was

mainly driven by a positive volume/mix effect

(impact: Euro 26.9m)

600.0

560-580 • The increase in FY17 was mainly in Western Europe

580.0

and Americas, in addition to the acquisitions of GC

560.0

534.8 France, Axiom and ICSA’s activities during 2016/17

540.0 520.5 • FY16 was affected by unfavorable trend vs FY15 in all

520.0 500.3 the main currencies to which the group is exposed

500.0 (impact: Euro 24m)

480.0 • FY18E revenues are expected to grow by 6.6%(2) vs

460.0 FY17 mainly as a results of the investments in new

2015A 2016A 2017A 2018E

products, technology and capacity increase

Revenue at constant 2017 FX (€m) undertaken in FY17

CAGR 15A-17A +3.8%

496.0 497.9 534.8

• At constant exchange rates (2017), revenues grew by

a CAGR of 3.8% in FY15-17

2015A 2016A 2017A

Revenue Bridge (€m)

2.1

(24.2) (4.2) 10.0

(1.1) 7.3

(2.3) (0.3) 26.9 534.8

520.5

500.3

(1)

(1)

Volume/Mix

Volume/Mix

FX impact

Price

Other

Price

Other

perimeter

Revenues

Revenues

Revenues

Change in

2015 Net

2016 Net

2017 Net

FX impact

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group Structure reorganization 48

Note: (1) Guala Closures Management Analysis. FX impact includes translation effect, partially offset by operational measures

(2) Based on 2018 mid-point guidanceResilient EBITDA and EBIT margins

Adj. EBITDA (€m)

% margin 20.4% 20.5% 20.7% 20.7%(1)

• The increase in Adj. EBITDA in FY17 was mainly

115-121 driven by revenue growth in Western Europe and

106.4 110.6 America despite an average higher cost of

102.5

aluminium

• FY17 EBITDA has been adjusted by Euro 7.4m

non recurring costs mainly related to the M&A

sale process

• At constant exchange rates 2017, Adj. EBITDA

CAGR FY15A-17A is + 5.6%

2015A 2016A 2017A 2018E

Adj. EBIT (€m)

% margin 13.2% 14.3% 14.4%

• Adj. EBIT CAGR FY15A-17A equal to +5.8% (at

77.1 current exchange rates)

68.8 71.5

• Slight increase in D&A in FY17 compared to

previous year mainly related to the impairment of

an asset held for sale for €1.8m

2015A 2016A 2017A

49

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

Structure reorganization

(1) Based on 2018 mid-point guidanceNet Financial Expenses and Net Income

Net Financial Expenses (€m)

Net interest

7.6% 7.0% 5.4%

expenses % of • On Nov 2016, Guala Closures reimbursed its

gross debt(1) existing bonds and issued a €510m Floating Rate

53.8

48.6 Senior Secured Note with maturity in 2021 and a

10.4 41.4 Euro 65m RCF substantially reducing its cost of

7.0

4.8 debt

10.0

• Net financial expenses for FY2016 including Euro

41.7 38.6 10m of financial expenses for debt refinancing

31.4

• Current Bond and RCF facilities expected to be

refinanced in the context of the business

2015A 2016A 2017A combination with Space4

Net interest expenses Other (2) Interest on debt refinancing

Net Income(3) (€m) and Margin on Revenues (%)

7.0%

29.0

5.0% • In FY15-16 Net Income was strongly impacted by

24.0 4.9% (4)

3.0%

significant net financial expenses accounting for

19.0 Euro 49m and Euro 54m respectively

0.9%

14.0 ~25-31 1.0% • Tax losses carried forward amount to c. Euro 190m

(0.9%) (0.7%)

9.0 with a potential tax benefit of Euro 46m for which

(1.0%)

4.0

no deferred tax assets have been accrued so far

4.8 (3.0%)

(1.0) (3.7)

(4.7)

(6.0) 2015A 2016A 2017A 2018E (5.0%)

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group Structure reorganization 50

Note: (1) Gross debt equal to total financial liabilities excluding financial liabilities vs minority. Net interest expenses adjusted for net interest expense for debt

refinancing (c. €10m in FY16); (2) Other includes exchange rate gains/losses, derivatives and other financial items (3) Including minorities (4) Based on 2018 mid-pointNWC and Capex evolution

Net Working Capital (€m)

113.5

87.0 90.8

82.7 • NWC recorded an increase in FY17 mainly due to

67.3 67.9

102.4 • integration of the acquired companies

86.9 89.1

• higher year-end DSO compared to the

(67.1) (66.2) (71.7) historical average year-end level

2015A 2016A 2017A

• increase in inventories driven by an

Trade Receivables Inventory Trade Payables

exceptional higher aluminium stock at year

end and higher finished and semi-finished

Days 2015A 2016A 2017A products

Inventory 45 46 51

Trade receivables 58 61 63 • Increasing NWC days driven by growing DOI(1) and

Trade payables (45) (45) (44)

DSO(2)

Net Working Capital 59 62 70

Capex (€m) and % on Net Revenues

6.2%

40 5.4% 7.00%

4.3%

35 31.2 5.00%

28.7

30 3.00%

22.6 6.3 • FY17 Recurring Capex relating mainly to European

25 6.3 1.00%

2.7 subsidiaries

20 -1.00%

15 -3.00% • FY17 Expansion Capex refer mainly to new

24.9 22.4 product investments such as Nip Cap 2 2nd step in

10 19.9 -5.00%

India and a new closure technology

5 -7.00%

0 -9.00%

2015A 2016A 2017A

Recurring Capex (paid) Expansion Capex (paid) % on Net Revenues

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group Structure reorganization

Note: (1) Days Of Inventories (2) Days Sales Outstanding 51Net Financial Position and Net Invested Capital

Net Financial Position(1) (€m) and Net Financial Position / Adj. EBITDA

• The increase in NFP in FY17 was affected by €17.6m of

cash outflows for the acquisitions carried out in the year,

600.0 552.5 530.0 (2) 15.0xthe exceptional increase in NWC, c. €5m of extraordinary

497.6 514.8

13.0xcosts mainly due to the “exit” process and due diligence

500.0

11.0xcosts for c. €4m of transactions costs for the refinancing

400.0

9.0x

carried out in November 2016

300.0 •

7.0x From 2018 onwards, cash flow is expected to benefit

4.7x 5.0x 5.0x ~350 (3.0x)(2)

5.0x

from:

200.0 Post cash

contribution 3.0x • EBITDA increase

1.0x • efficiency in WC

100.0 at BC

0.0 -1.0x • lower net interest expenses

2015A 2016A 2017A 2018E • FY18 NFP estimated on the basis of the expected c. €180m

cash contribution from Space4

Net Invested Capital (€m) & Adjusted ROIC(3) (%)

ROIC(3) 26.8% 27.3% 27.3%

800.0

700.0 612.6 618.3 644.3

600.0

500.0 €317m

356.2 356.6 362.2 from the delisting PPA

400.0

300.0

200.0 49.8 54.4 74.3

100.0 206.6 207.3 207.8

0.0

2015A 2016A 2017A

(4)

Fixed Assets NWC & Other Goodwill

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group Structure reorganization 52

Note: (1) Including fair value of the put option in favor of GC Ukraine NCI accounting for Euro 16.8m at year end 2017; (2) Based on 2018 mid-point guidance

(3) Calculated as Adj. EBIT / (Net Invested Capital net of Goodwill); (4) Goodwill arising from take private in 2008 and other acquisitionsPresentation wrap-up

Marco Giovannini

Chairman and Group CEOKey growth levers – Organic Growth

The luxury closure market is the main growing market

Facilitate shift towards

1 luxury

worldwide with major premium brands gaining share

across major markets

Far East: second region for Spirits market growth

Pursue further

2 geographic expansion Southern Africa: new middle class, financially healthier,

supports growth in locally produced spirits

The craft Spirits Market, supported by the millennials

Ride emerging market

3 trends

consumer trend, is heavily growing in the US, but also

spreading in Europe

Changing a simple product like a bottle to a connected

Enable emerging digital

bottle

4 requirements and

opportunities

Consumer engagement interaction, but also track &

trace, product certification and even marketing data

acquisition

53

Source: Guala Closures informationSubstantial external growth opportunities now possible

Main objectives

Improve product mix in order

Entering new markets and Increase footprint and solidify

to reach out new clients /

exploring new segments presence in larger countries

product niches

M&A Pipeline

Pharma, Labels

West Europe East Europe Americas Asia Oceania and Dispensing

Systems

Capacity increase Entry the Belarussian Penetration in the US Penetration in the Actionable

fast growing end opportunities to Further relevant

for aluminium and market and further and expansion of

growth opportunities

luxury closures expansion in Russia capabilities in Mexico markets of the Asian consolidate

region leadership in Australia in other segments

and Chile

Wine & Spirits New Verticals

54

Source: Guala Closures informationEntrepreneurial talent combined with strong local teams

55Macallan re-package: a innovative new closure for this icon single malt

Launched in February 2018

56A compelling investment proposition

1

#1 Worldwide

solution provider &

partner to global and

local clients

5 Advanced 2

Entrepreneurial

technology and

management team

innovation driven

with a long-lasting

business model with

experience in the

unmatched

sector

capabilities

4 3

Operational

excellence distributed

Multiple growth

throughout a global

levers

manufacturing

platform

576. Transaction Description

Transaction overview

The business combination will be in the form of a merger of Guala Closures into Space4

Space4 will deploy all of its financial resources, investing alongside Peninsula, Quaestio and management

Key Objectives

#4 public company in

• Listing on the STAR segment of the Italian Stock Exchange as a public Italy on the STAR

company with a market cap of c. €700m @ Euro 10 per share segment(2)

4

• Enhance capital structure substantially lowering current leverage by

maximum c. €180m(4) to 3.0x and reducing related costs

#5 on the STAR

segment by free float(1)

• Provide capital structure to fund external growth and continue

5

investing in the business

• Provide Space4 investors with a unique opportunity to pursue #13 on the STAR

segment by market

accelerating growth in a very attractive and resilient sector

cap(3)

13

Source: Guala Closures information, Space4 information

(1) In % of total outstanding shares. Excluding utilities and financial services

(2) By market capitalization. Public company defined with +50% free float in the STAR segment. Excluding utilities and financial services

58

(3) Excluding utilities and financial services

(4) Assuming no withdrawal rights above €15m back-stop provided by Peninsula and Quaestio and including €25m management capital increaseValuation

• Approach: DCF and trading multiples • Approach: Net Asset Value

• Equity Value: €504m • Space4 NAV of €10 per share at business

• Implied Enterprise Value: €1,079m(1) combination(5) corresponding to c. €528m

• Implied multiples on 2018E financials: • The withdrawal right price has been set at

– EV / EBITDA multiple: c. 9.1x(2) €9.903 per Space4 share

– P / E multiple pre-money: c. 23.7x(3)

– P / E multiple post-money: c. 19.7x(3)(4)

Source: Guala Closures information, Space4 information

(1) Calculated including Net Financial Position (€552.5m), employees’ benefits (€6.4m) and minorities (€16.4m) as of Dec-17

(2) Based on 2018 mid-point guidance 59

(3) Excluding minorities

(4) Assuming a cash contribution of c.€180m from Space4, co-investors and Management. Assuming 3.5% interest rate after refinancing and the use of tax assets

(5) Including first tranche of special shares conversionCurrent shareholding structures

Management Private Equity Investors

14.8% 85.2%

of which 8.6%

in class B shares

GCL Holdings SCA

• Ordinary shares (#50,000,000) listed on MIV

100%

• Special shares (#1,250,000)

– No entitlement to ordinary dividends, no voting rights

– 4.5-to-1 conversion in ordinary shares at certain triggers

Guala Closures S.p.A. • Market warrants (#20,000,000)

– Strike price: €10.0 with maximum underlying #4,651,000

shares

– 2 warrants every 10 shares delivered to shareholders at

Class B multiple voting shares key features: IPO – currently listed

– 2 warrants every 10 shares to be assigned at business

• Same economic rights combination(1)

• Triple voting rights (3:1) with respect to ordinary shares • Sponsor warrants (#2,500,000)

• Non transferable: 1:1 conversion into ordinary shares in case of – Strike price: €13.0 (cash exercise)

sale to third parties

• Owned exclusively by the management

Source: Guala Closures information, Space4 information

60

(1) Only assigned to shareholders that do not exercise any exit rights at business combinationKey transaction steps

3 key steps occurring simultaneously upon merger completion

1 2 3

Acquisition Management Capital Increase Merger

• Space4 jointly with Peninsula and • €25m reserved capital increase • Merger of Guala Closures into

Quaestio acquires 81.2% interest in fully underwritten by Guala Space4 with the resulting company

Guala Closures for a total cash Closures Management to be assuming the name of Guala

consideration of €409m(1) from GCL subscribed at closing Closures

SCA • Shares will be cum warrants (1m) • Guala Closures shareholders (i.e.

• Following Acquisition, GCL SCA will giving the rights to the holders to Peninsula, Quaestio, Management

own 14.8% and private equity subscribe for a new share for every and residual Private Equity

investors will maintain 4.0% of warrant post business combination Investors) receive 0,675381 new

Guala Closures share capital at a price of Euro 13 per share Space4 shares in exchange for each

• Guala Closures management team Guala Closures share

total investment Euro 100m(2) – Price per Guala Closures share

equal to €6.75381,

corresponding to an equity value

of €504m

– Space4 price per share of €10.00

Total net cash contribution into Guala Closures of c. Euro 180m (Pro Forma NFP/EBITDA18E 3.0x)

Source: Guala Closures information, Space4 information 61

(1) Including €349m from Space4, €50m from Peninsula and €10m from Quaestio

(2) Including contribution of current management shareholding (€75m) and management capital increase (€25m)Pro-forma shareholding structure

Economic Rights Economic Rights

@ Business Combination Fully Diluted @ €13 p.s.(1)

Space Holding Space Holding

Quaestio 3.9% Key Managers Quaestio 7.2% Key Managers

2.8%(2) 14.1% (Voting rights: 23.7%) 2.7% (2) 12.7% (Voting rights: 21.4%)

Peninsula

7.1% Private Equity Peninsula Private Equity

Investors 6.4% Investors

2.8% 2.6%

Investors Investors

Space4 (3) Space4 (3)

(free float) (free float)

69.3% 68.5%

• Out of the 14.1% of the Guala Closures share capital, Key Managers will own c.6.1% in class B shares with multiple voting rights (3/1)

• Lock-up obligations for key shareholders: Key Management (18 months), Space Holding (12 months), Peninsula (9 months), Quaestio (9

months), Private Equity Investors (6 months)

Source: Guala Closures information, Space4 information

Note: Scenario without exercise of withdrawal rights

(1) Pro-forma for the conversion of special shares at €13 and exercise of market warrants (i.e. excluding pre-exercise of sponsor warrants and management warrants)

(2) @BC Quaestio shareholding includes 1.4% shares owned through initial investment in Space4 and 1.4% through direct investment. @ 13€ Quaestio shareholding

62

includes 1.4% through initial investment in Space4 and 1.3% through direct investment

(3) Excluding QuaestioTransaction timeline

2018

16 April Space4 and Guala Closures Board of Directors approved the transaction

Today’s investor

presentation

28 May Space4 ordinary and extraordinary shareholder meeting to approve the transaction

14/15 June End of period for the exercise of the withdrawal right by Space4 shareholders

28/29 July End of creditor opposition period

End of July -

Merger effectiveness and transition to the STAR segment

Beginning of August

63

Source: Guala Closures information, Space4 informationBest-in-class corporate governance

Board of Directors will consist of 9 members

• Space4 has implemented a Corporate Governance system in line with the market best practice for listed companies, that will be retained after

the Business Combination

Shareholder agreement in place to define Board appointments

• 9 Directors overall, of which:

i. 4 appointed by Guala Closures’ management

ii. 2 (of which 1 Independent) appointed by Space Holding

iii. 2 Independent Directors, appointed, by mutual agreement, by Guala Closures management / Space Holding

iv. 1 Director appointed by Peninsula

• Supervisory Board: 1 Statutory Auditor appointed by Space Holding

64

Source: Guala Closures information, Space4 informationGuala Closures: a unique investment for our Space4 shareholders

• The Global leading producer of specialty closures for the spirits and wine

industry with almost €600m turnover

• A trusted partner to most global and local spirits and wine producers for

the last 40 years

• A business model driven by unique technology & innovation capabilities,

supported by an R&D DNA and by a state-of-the-art manufacturing

footprint spread across 5 continents

• A resilient story of growth - margins consistently at 20%+ in the last 15

years

• A natural consolidator in a fragmented market space, ready for additional

expansion opportunities

• An entrepreneurial management team with a long-lasting experience in

the sector and deeply invested in the business

A single transaction deploying €600m of cash equity for an aggregate equity value of approx. €700m

65

Source: Guala Closures informationAppendix

Resulting shareholding structure of the business combination

SCENARIO WITHOUT EXERCISE SCENARIO WITH MAXIMUM EXERCISE

OF WITHDRAWAL RIGHTS OF WITHDRAWAL RIGHTS

– NO exercise of withdrawal right – Maximum exercise of withdrawal right equal to €162.5m

– No back-stop – Back-stop equal to €15m (€10m from Peninsula and €5m from

Quaestio)

– Cash contributed into Guala : c. €180m – Cash contributed into Guala: c. €33m

Space Holding Space Holding

Quaestio 3.9% Key Managers Quaestio 5.0% Key Managers

2.8% 14.1% (Voting rights: 23.7%) 4.5% 17.8% (Voting rights: 29.2%)

Peninsula

7.1% Private Equity Peninsula

Investors 10.8%

2.8% Private Equity

Investors

3.6%

Investors Investors

Space4 Space4

(free float) (1) (free float) (1)

69.3% 58.3%

• In case of no withdrawal the total cash contribution will be c. €180m (Pro Forma NFP/EBITDA18E 3.0x)

• In case of maximum withdrawal the total cash contribution will be reduced to c. €33m (Pro Forma NFP/EBITDA18E 4.2x)

Source: Guala Closures information, Space4 information 66

(1) Excluding QuaestioRevenues bridge by geographic region

2016-2017 Net Revenues bridge by geography (FX stable at FY17 average)

(0.4) 1.7

(3.4) 19.3

534.8

19.7

497.9

Asia

Africa

Europe

Americas

Oceania

Revenues

Revenues

2016 Net

2017 Net

2015-2016 Net Revenues bridge by geography (FX stable at FY17 average)

(0.9) (3.2)

(5.0) 3.8

7.3

496.0 497.9

Asia

Oceania

Revenues

Revenues

Africa

Europe

Americas

2015 Net

2016 Net

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

67

Structure reorganizationRevenue by geographic region

Revenue by geography (reported)

(€/m)

534.8

520.5

500.3 500.3 17

19.3

14.4 14.4 48.6

49.9

48.7 48.7

107

96.6 89.3 89.3

70.4 71.9

74.8 74.8

284.4 273.1 273.1 290.4

2015 2016 2016 2017

Europe Asia Americas Oceania Africa

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

68

Structure reorganizationOperating costs

Operating Costs FY15–FY17

(€/m)

447.7

430.0 2%

3% 411.1

3%

22%

22%

23%

21% 22%

22%

13% 14%

14%

23% 23%

22%

18% 17% 16%

FY15 FY16 FY17

Plastic consumptions Aluminium consumptions Other Raw Material Costs for Services Personnel Expenses Other Operating Costs

Cost of raw material

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

69

Structure reorganizationIncome Statement 2015-2017

Data in €/m 2015A 2016A 2017A

Net Revenues 520.5 500.3 534.8

growth % 6.7% (3.9%) 6.9%

Change in inventory of FG/SF goods 3.1 1.3 6.9

Value of Production 523.6 501.5 541.7

Other operating income 9.7 10.2 9.3

Costs for raw materials (233.3) (218.4) (236.0)

% of Net Revenues (44.8%) (43.7%) (44.1%)

Costs for services (91.1) (88.5) (100.2)

% of Net Revenues (17.5%) (17.7%) (18.7%)

Personnel expenses (94.0) (93.8) (100.6)

% of Net Revenues (18.1%) (18.8%) (18.8%)

Other operating costs (11.6) (10.4) (10.9)

% of Net Revenues (2.2%) (2.1%) (2.0%)

EBITDA 103.3 100.7 103.2

margin % 19.8% 20.1% 19.3%

EBITDA adjusted 106.4 102.5 110.6

margin % 20.4% 20.5% 20.7%

Amort., deprec. and impair. losses (37.6) (31.0) (33.5)

D&A as a % of Capex 178.0% 100.4% 111.0%

EBIT 65.7 69.7 69.7

margin % 12.6% 13.9% 13.0%

EBIT adjusted 68.8 71.5 77.1

margin % 13.2% 14.3% 14.4%

Exchange rate (3.9) (2.5) (9.1)

Derivatives and other finan items (3.1) (2.4) (0.9)

Net interest expenses (41.7) (49.0) (31.4)

Total net financial expenses (48.6) (53.8) (41.4)

EBT 17.0 15.9 28.3

margin % 3.3% 3.2% 5.3%

Income taxes (21.7) (19.6) (23.5)

Taxes as a % of EBT (127.6%) (123.0%) (83.1%)

Net income (4.7) (3.7) 4.8

margin % n.m. n.m. 0.9%

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

70

Structure reorganizationBalance Sheet 2015-2017

Data in €/m 2015A 2016A 2017A

Intangible assets 376.7 374.0 377.2

PP&E 186.1 189.9 190.7

Held for sale - - 2.1

Fixed assets 562.8 563.9 570.0

Inventories 67.3 67.9 82.7

Inventories days 45 46 51

Trade receivables 86.9 89.1 102.4

Trade receivables days 58 61 63

Trade payables (67.1) (66.2) (71.7)

Trade payables days (45) (45) (44)

Net working capital 87.0 90.8 113.5

Derivatives (1.1) 0.1 (0.2)

Other assets/liabilities (28.6) (28.9) (31.4)

Other assets/liabilities as a % of Revenues (5.5%) (5.8%) (5.9%)

Employee benefits (5.7) (6.2) (6.4)

Other provisions (1.8) (1.3) (1.2)

Net invested capital 612.6 618.3 644.3

Financial liabilities 546.6 554.3 577.4

Financial liabilities vs minority 13.5 15.9 16.8

Financial assets (0.6) (0.7) (1.1)

Cash & cash equivalents (61.9) (54.7) (40.6)

NFP 497.6 514.8 552.5

Total equity 115.0 103.5 91.8

Source of financing 612.6 618.3 644.3

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

71

Structure reorganizationCash Flow Statement 2015-2017

Data in € / m 2015A 2016A 2017A

Adjusted EBITDA 106.4 102.5 110.6

Change in NWC 10.1 (7.8) (27.7)

Other operating 1.2 1.5 (3.0)

Taxes (21.8) (22.2) (22.8)

Change in net financial indebtedness from operating activities 96.0 74.0 57.0

Net capex paid (22.6) (31.2) (28.7)

Capex as a % of net revenues (4.3%) (6.2%) (5.4%)

Acquisitions - (1.1) (11.1)

Change in net financial indebtedness used in investing activities (22.6) (32.3) (39.8)

Acquisition of non-controlling interest (0.7) - (1.1)

Acquisition of initial Guala Closures France SAS indebtedness - (0.7) -

Acquisition of initial Axiom Propack Pvt Ltd indebtedness - - (5.4)

Net interest expenses (41.7) (38.6) (31.4)

Exceptional financial costs for debt restructuring - (10.4) -

Transaction costs not yet paid / (paid) for the debt refinancing - 3.8 (3.8)

Derivatives and other fin. items (4.7) (3.5) (0.6)

Capital increase - - 0.8

Dividends paid (3.9) (6.3) (6.8)

FX impact (2.5) (0.7) (1.7)

Change in net financial indebtedness used in financing activities (53.4) (56.4) (49.9)

Exceptional (9.9) (2.6) (5.1)

Total change in net financial indebtedness 10.1 (17.2) (37.7)

Source: GCL Holdings consolidated accounts - to be considered as a proforma of Guala Closures Group consolidated accounts after Group

72

Structure reorganizationCash generation

Consolidated Free Cash Flow and Net Cash Flows Trend

50

43.7

40 37.3

30

20

14.9

10.6 11.9

8.5

(€m)

10

4.1 4.9

1.4

0

(1.2)

(6.0) (5.2)

(10)

(9.7)

(12.6)

(20)

(18.6)

(20.8)

(30)

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Free Cash Flow Net Cash Flow

Source: Management consolidated cash flow

73

Note: Free cash flow is operating cash flow net of capex paidLeading position across geographies

Product Lines Product Breakdown Market Positioning Major Clients

A Safety

4%

Pharma 1

16%

Wine

West Europe Roll-On

41%

Roll-On & 1 2

Others

7% Luxury

Europe Wine

(West & East) 32% Safety 1 2

54%

13% Wine

Safety

Roll-On &

1

51%

Others

East Europe

Luxury Roll-On

1%

1

35%

Safety

74

Source: Guala Closures information

Note: Revenues breakdown refer to countries from which the product is soldLeading position across geographies (cont’d)

Product Lines Product Breakdown Market Positioning Major Clients

B Safety Luxury

18% Wine 1 1

Americas 16%

3% Roll-On & Roll-On

Others

1 2

Luxury

20% 63% Wine

1 3

Safety

C 1%

Asia Roll-On &

Others Safety

13% 1

99%

Safety

75

Source: Guala Closures information

Note: Revenues breakdown refer to countries from which the product is soldLeading position across geographies (cont’d)

Product Lines Product Breakdown Market Positioning Major Clients

D

Roll-On

Wine

Oceania 1

9%

80%

Wine

1

Roll-On &

Others

20%

E 2% Safety

Pharma

1

42%

Africa

Wine

Roll-On

3% 1

Roll-On &

50% Other

Wine

Safety

2

5%

76

Source: Guala Closures information

Note: Revenues breakdown refer to countries from which the product is soldAfter years of bulk driving export top producing countries are pushing

bottled export; due to strong localization, this can benefit GLC

Wine Worldwide export per type (2006-2016) Top 7 (*) Producing Countries (2016 vs. 2017)

(Mhl liters) (Bn liters)

€18Bn €23Bn €29Bn

CAGR CAGR

06-16 11-16 -5.2%

3.1 2.9

2.0% 102.7

Bulk

93.4 8,3 +7.2% +0.7%

6,2

84.0

4.0

2016 2017

39,5 +3.2% +0.3%

34,3

29,0

6.1%

4.1 4.4

51,0 53,0 54,9

+0.8% -1.0% Bottled

2006 2011 2016

Sparkling Bulk (>2lt) Bottled 2016 2017

Source: OIV World Wine Production – e I Numeri del Vino; (*) China has no relevant export 77Sustainability program results 2011-2015

Program started in 2011

Program based on 12 indicators

Perimeter: Italy Business Unit

Implemented Best Practices and Internal Communication

15 objectives achieved or outperformed

ENVIRONMENTAL SOCIAL ECONOMIC

CO2 emissions - 36.6% Accidents - 41.7% OEE 74.8%

Energy consumption - 44.0% 2 hours training on New patentable ideas 26

Sustainability 100%

Water consumption - 52.2% Claims 0.08%

Waste - 76.5%

Scraps - 68.1%

78Sustainability program 2016-2020

Implement sustainability program throughout the Group

Program based on 12 indicators and 21 objectives

Perimeter: the whole Group

Strategic Key Objectives

CO2 Emissions - 25% Accidents - 15%

Energy Consumption - 25% 2 hours Training on Sustainability 100%

Water Consumption - 20% ISO 14001 certification 100%

Production Scraps - 30% ISO 22000 certification 100%

Waste in landfill 0 Sedex accreditation 100%

79You can also read