HIP LENDING HIP IS WHAT BANKING SHOULD LOOK LIKE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

HiP Lending

HiP is what banking should look like

Fast and easy lending based on real assets funded by deposits

documented on the Ethereum blockchain

HiP Interactive Property Ltd

Kai Peeters and Christopher Smith

White Paper

Version 1.1

October 2019

This document is for informational purposes only and does not constitute

an offer or solicitation to sell shares or securities in HiP Interactive Property

(HiP) (a Gibraltar company) or any related or associated company. Any

such offer or solicitation would only be made by a confidential offering

memorandum and in accordance with applicable securities and other laws.

Please read the important Risk Disclosures at the end of this White Paper.

HiP may make changes to this White Paper. Please visit hiplending.com for

the most recent version.

Abstract HiP Lending (HiP) is a modern take on banking following the well established model of existing fintech challenger bank successes (Starling Bank, Monzo, N26 and Salt Lending). Outside the technology of a strong robust banking app based platform, HiPs rise comes from its unique ability to act as a marketplace that allows users to lend and borrow against physical assets. Lenders can earn high interest rates with low risk deposit accounts, and borrowers get money without needing a good credit rating. HiP’s protocol is asset class agnostic and authenticates all transactions on the blockchain. HiP’s interests are simple, we want to build banking services that reflect true and honest interactions and investments, banking services that benefit the users themselves. Join us in bringing finance back down to Earth. Problem - Banking The Old Guard The legacy financial system favours financial institutions at the expense of their customers. Like any business, a bank’s intention is to derive as much value from its customers as possible. And with few viable alternatives, bank customers have little leverage. Fractional lending, quantitative easing, and the conflicts of interest they create have resulted in the “everything bubble”, a giant overvaluation of nearly every asset class. The world is in a precarious position. Central banks have resorted to experiments with negative interest rates, experiments that are unprecedented in more than 10,000 years of lending. These negative interest rates and the widespread perception of a coming global economic crisis have driven nearly $20 trillion of bonds into negative yield. Interest rates on deposits are less than inflation, and most bank customers have limited investment opportunities, while facing heavy fees and poor customer service. Many bank customers may have enormous assets that they cannot lend against because banks do not accept these assets as collateral. And 2.5 billion people cannot access even basic banking services. Regulation Regulation has been the primary barriers to entry for bank competitors. However with the fast and increasing accessibility to umbrella regulation, crowd-funding and peer-to-peer licences, a significant number of fin-tech startups are coming into play and eating away at the margins these banks use to enjoy. Crypto Alternatives Services outside of banking are also fast expanding, launching new and novel concepts. Bitcoin is used to send over $6 billion in a single 24 hour period, and shows no signs of relenting. Salt Lending and Celsius allow their customers to borrow without a bank account. GoldMint.io and Digix empower their users to own permissionless shares of gold. These new flexible and rapidly expanding models prove that the market has an appetite for ways to move money outside of traditional banks.

Solution - HiP Lending

Collateralized Loans

Lending against physical assets tethers finance to reality. It no longer matters whether the

borrower is lying or not: if the borrower defaults, the collateral covers both the principal and the

interest. Borrowers have skin in the game. Credit agencies become irrelevant because only the

value of the collateral matters. Volatility of the collateral value is priced into the loan to value

ratio. Debt becomes sane again.

International Transparency

Blockchain technology enables truly global information and value exchange. Using strong

cryptography and peer-to-peer networks, we can publish our data in an uncensorable way that

eliminates the telephone game issues of signal integrity. We leverage this technology to make

our loan books transparent to investors all over the world. Due diligence becomes simple with

an interface that lets you explore the loans, collateral and their supporting documentation.

Ease of Use

Users access the HiP Lending Platform via a bank-account-style interface. Borrowers can

onboard assets by first taking photographs and documenting them, then receiving a preliminary

appraisal estimate, then bringing the asset to a custodian for the final appraisal and contract.

Once the assets are onboarded, the user will be given a credit line which they can pull from and

an account they can pay back to at any time via a simple mobile app. Lenders likewise have an

account where they can put their funds and choose from a selection of investment options,

loans with different terms, different collateral.

Benefits

The HiP Lending Platform solves real problems that many people face when they want cash to

make a purchase, but do not wish to liquidate their assets. Instead of selling their assets, the

HiP Lending Platform enables the members to leverage the value of their assets, get cash,

avoid tax events and transaction fees, and maintain their long position in the assets.

Land and Expand

The initial asset class that we will lend against is gold. We have a lending business that is

already operating in Thailand as our pilot. This business is very profitable and stable. After our

digitization of this business is complete, we will expand into other asset classes and geographic

territories. Future asset classes include

● Other Precious Metals

● Real Estate

● Gems

● Corporate Stock

Future geographic regions include

● Vietnam

● Philippines

● Indonesia

● Cambodia

● Myanmar

● Laos

Collectively, these ASEAN countries have nearly $3T in GDP.

Low Risk

The physical assets we receive as collateral are liquid and can be sold to pay the principal and

interest back to the lenders, making the loans much more secure than the paper markets. The

loan-to-value ratio is chosen so that the volatility of the asset price is not a realistic threat to

capital. Fiat currency is secured using existing banking infrastructure, so we are not introducing

any new credit risks.

Currency Volatility

HiP will protect against currency downside risk by using a variety of forex hedging strategies.

These strategies may include forwards, futures, options or ETFs.

Competitive Landscape

Competitors in this space are made up of challenger banks from both the crypto and fiat world.

● Celsius Network

○ $300M in deposits

○ $2.2B in loans

○ 40K users

● Nexo.io

○ $900M lent

○ 200K loans

○ Asset Backed

● N26

○ 750K users

○ $3.5B valuation

○ No ROI on deposits

● Starling Bank

○ 500K users

○ $1.5B valuation

○ < 1% on deposits

● Monzo

○ 2M users

○ $2B valuation

○ No ROI on deposits

Go to Market - Thailand

HiP Lending was founded out of a partnership between two Thai Entrepreneurs based in

Thailand Bangkok, and HiP, a digital debt and equity marketplace. Our first loans are already

being made through an existing lending company in Thailand. This established business will

document its loan book on the HiP Asset Register to increase the visibility and accountability for

investors who may not be familiar with business in Thailand. By bootstrapping off of an existing

successful business, we ensure that there are no miracles required for the business to start

generating returns on the capital raised.

Lending in Thailand

The tradition of pawn shops that loan against gold is very old and established in Thailand. The

banks that currently finance these outlets do not use the Gold reserves themselves to

collateralise their lending, meaning there is ~$500M worth of uncollateralized gold sitting in

Thailand which can be collateralized via a small number of companies.

Market Size

The market size in Thailand alone is significant.

● Household debt is 70% of GDP

● Unregulated lending ~$180B per year

● Licensed lending of ~$138B per year

Trade War

The highly publicized trade war between the US and China is creating tremendous upheaval

across industries. Companies will soar or die based on the decisions of these world leaders.

Due to the specificity of the tariffs, the trade war could be hugely beneficial for countries within

the ASEAN (Association of South-East Asian Nations). We are already seeing both China and

US shifting production and capital out of each other into ASEAN countries. This makes Thailand

an even more attractive choice for our go-to-market.

The point above fully supports our initial start in Thailand as it can be perceived as an inroad

into ASEAN. 1

1

https://www.cnbc.com/2019/08/27/us-china-trade-war-companies-looking-to-invest-in-thailand-vietnam.html

https://www.cnbc.com/2019/08/29/vietnam-ripe-for-private-equity-investors-as-us-china-trade-war-drags.html

https://thediplomat.com/2019/09/is-southeast-asia-winning-the-us-china-trade-war-not-so-fast/

https://www.scmp.com/week-asia/geopolitics/article/2168703/chinas-trade-war-pain-can-be-aseans-gain-how-southeast-asia

https://www.scmp.com/news/china/diplomacy/article/3027242/are-chinese-companies-using-cambodia-evade-us-tariffs

Our Technological Advantage Blockchain We will use the Ethereum blockchain in two largely decoupled ways. The first is as an asset register, logging the collateralized loans in a way that can be reviewed by any potential investor, lender or even regulator. This will increase confidence in the security of deposits and decrease the asymmetry of information regarding the loans. The second way we use the blockchain is with the HIP token, which is an ERC20 token with a couple of non-standard features. IPFS The InterPlanetary File System is another “web3” technology that inserts strong cryptography into the DNA of content searching while also decoupling content from a specific server or online location. It combines distributed hash tables with novel integrations with existing DNS technology to create a peer-to-peer storage layer with small, secure links to arbitrary content. These links are cheap to put on a blockchain and remove any issues with malicious middlemen, since the link is a cryptographic hash that changes dramatically when the content is changed even slightly. Asset Register The asset register smart contract records the details of loans, including the anonymized borrowers and lenders, the loan amount, the maturity date, the interest rate and the details of the collateral, which may be anything, but will initially be gold. We use IPFS as a storage layer for complex, non-succinct data associated with the loans, such as audits of borrowers in the case of corporate loans, or other relevant documentation in the case of loans collateralized by gold. This allows us to build an interface that can sort thru the loans and display whatever is relevant to the viewer. HIP Token The HIP token is a utility token that is tied to the collateralized loan volume via a simple mechanism: additional interest. When lending, the user may choose to lock up a certain amount of HIP tokens for a period of time. During that time the lender is eligible to receive a higher interest rate, in proportion to the amount of tokens that they locked up. This proportion is chosen so that the lender is not exposed to the downside of token volatility. If the lender locks up HIP tokens and provides a proportional amount of liquidity, they will get extra interest to offset their downside exposure.

The formula for extra interest is

Additional interest = D / I

Where

- D is the dollar amount of the HIP tokens locked up at the time of lock up.

- I is the dollar value of the fiat investment. This is subject to a minimum requirement,

which is 100 x D.

For example, if a user locks up $1000 worth of HIP, they can receive an extra 1% on a loan of

$100,000. This extra interest perfectly offsets the token values at the time of lock up, so that

even if the HIP token goes to zero, the extra interest ($1000 = 0.01 * $100,000) pays for it, so

there is no financial loss.

Additional uses for the token include referral bonuses via network marketing and discounted tax

fees. As the business grows we may implement additional uses as the opportunities arise.

Tokenomics

Hold HIP, boost your interest.

The user is not required to purchase HIP tokens to lend or borrow on the HiP Platform, as this

would create unnecessary barriers to entry and would expose users to the volatility of HIP

tokens. However, there is a reward for holding (locking) tokens in parallel to lending money,

namely an increased fiat interest return. This additional return provides token holders essentially

a downside protection, while still maintaining the unlimited upside potential of the token itself. By

doing this, we expand the market of potential token holders from token speculators, a

market of about $200B in value, to the entire class of fiat investors, worth around $50T.

Locking Mechanism

Locking tokens is done from the user’s wallet. We have metamask integration to make this

simple for users, and we also support any other personal wallet that someone would like to use.

This approach allows us to reduce our exposure, since we are not holding the users’ tokens for

them. Locking is done on the HIP token smart contract, which is open source. The time duration

for which the tokens are locked is determined in advance by the user. During this time the

tokens will no longer be transferable. After the time has passed, the user may unlock the

tokens, at which point they become like normal tokens, freely transferable.

Medium of Exchange

Another way to view the token model: we pay our users with extra interest to hold our token.

This ties the value of the token to the volume of loans being issued and reduces the velocity of

the token. With this formulation, we can express the expected price in terms of the famous

medium of exchange equation MV = QP.

This equation simply counts money flow in two different ways and asserts the two different ways

must arrive at the same number. In the first term, we have M, the number of monetary units in

supply (21M Bitcoin, for example) and V, the average number of times a single unit changes

hands in a given time window, say a year. These numbers multiplied together must equal the

number of units of currency that change hands in a year. Another way to count this quantity is to

look at the number of transactions and the average price paid in those transactions. This is the

same quantity, factored differently, therefore the two sides of the equation are equal.

Let’s apply Vitalik Buterin’s version of this (https://vitalik.ca/general/2017/10/17/moe.html) to the

HIP Token, using C = QH / M, where

● C is the cost of the token

● Q is the dollar-amount of goods and services demanded by it

● H is the average hold time of the token in years

● M is the total number of tokens

The transformation from MV = QP to C = QH / M is as follows. The velocity V is the number of

times a given token changes hands in a fixed length of time. The inverse of this 1/V is the hold

time. If V is 2 transfers / year, then H = 1 /2 year per transfer. The cost C of the token is the

inverse of the price level P, which is how many tokens you need to service the demand

denominated in say dollars. If the cost of the token is $10 / token, then the price level P is 1/10

token per dollar. Swapping these variables in gives the above equation MC = QH.

For example, if there are 1B tokens and we do $200M in volume every month and 1% of that is

interest funded by token purchases, and the average loan length is 12 months, we have

C = $200M * 0.01 * 12 / 1B = $0.024

HIP tokens will be available both on the listing exchange (to be determined) and

over-the-counter (OTC) on hiplending.com.

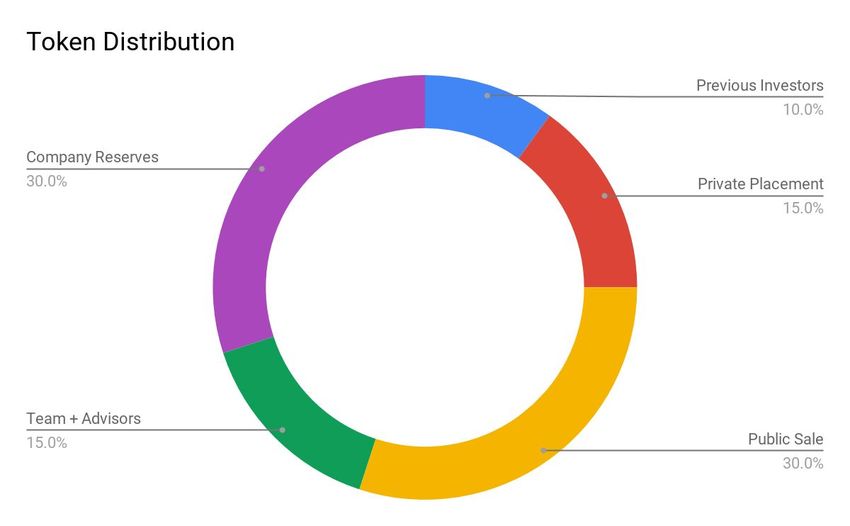

Issuance Policy

Token issuance will follow the following distribution.

- 10% already sold to previous investors

- 15% will be sold in the private sale of the IEO

- 30% will be sold during the public sale of the IEO

- 15% will go to team and advisors

- 30% will be allocated to company reserves

The other parameters for the sale:

● Token Supply: 1B (1e9)

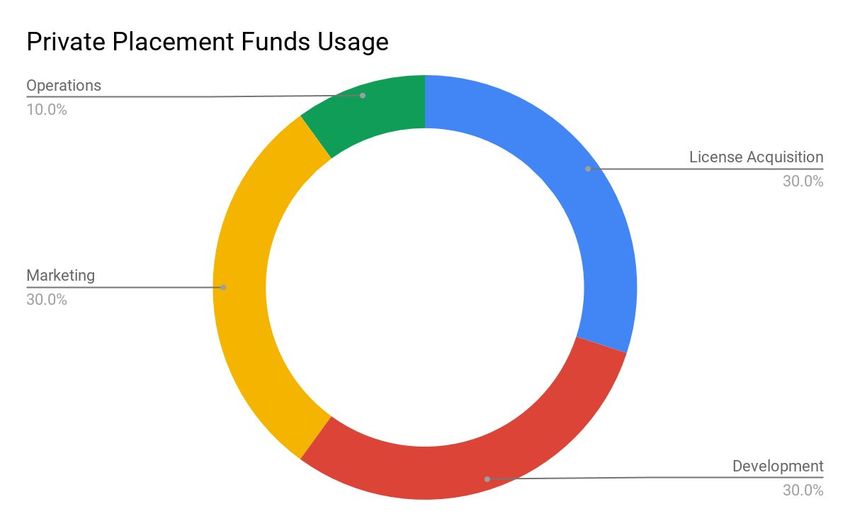

● Private Placement

○ Price: $0.0125 (-50%)

○ Soft Cap: $500K

○ Hard Cap: $1.875M

○ Money Use:

■ License Acquisition: $150K

■ Development of Platform: $150K

■ Operations: $50K

■ Marketing: $150K

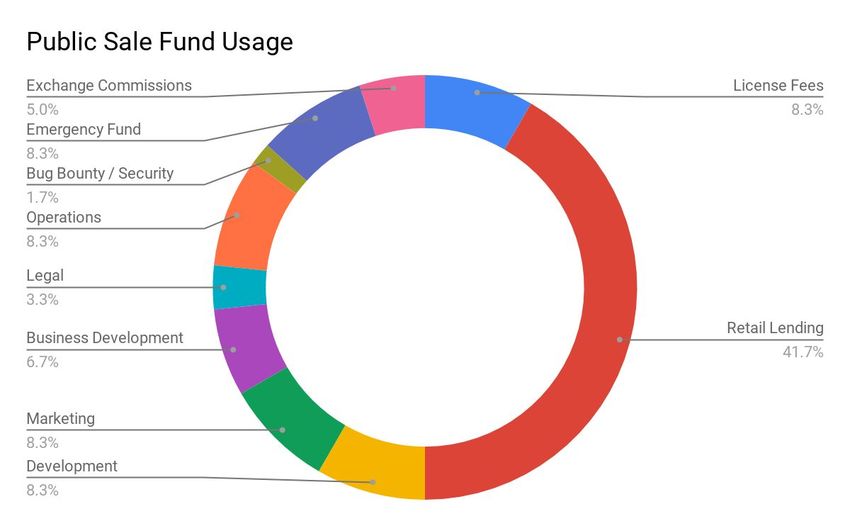

● Public Sale Price:

○ 10% at $0.015 / token (-40%)

○ 10% at $0.020 / token (-20%)

○ 10% at $0.025 / token

○ Hard Cap: $6M

○ Money Use:

■ Retail Lending - This includes money that we must put down as a deposit

for the next level of lending licenses as well as additional capital, if we

have it. Once the license is obtained, we may lend this out to retail

borrowers at interest rates up to 36%. The actual interest rate for a loan is

of course subject to market forces.

■ Exchange Commissions - This is the fee for launching the coin on CBX

■ License Fees - Obtaining the next level of licenses in Thailand will cost

about $500,000 in fees. These fees are non-refundable and mostly

non-recurring. We will use the law firm Baker McKenzie to apply for the

licenses which will cost about $200,000 and the rest is various

government fees.

■ Development - This is not very expensive. The core blockchain platform is

already built and the bank-style-interface can be purchased and

whitelabeled. Various processes in the existing gold-lending business will

be automated and abstracted for use in other asset classes as well.■ Marketing - We offer very competitive interest rates and unprecedented

transparency to international lenders. The value add for our customers is

clear, we just have to get the message to them.

■ Business Development - This includes sourcing lenders and borrowers,

both retail and corporate, and later expansion into adjacent asset classes

and geographic territories.

■ Legal - There are various legal costs related to maintaining the

contractual and regulatory/compliance framework for the business which

will occur over time as the business and its supported asset classes grow.

■ Operations - The operation of a gold lending business includes appraisal,

physical security and administration, all of which have costs.

■ Bug Bounty - We will offer a substantial bounty for independent security

researchers who may find security holes in our system. This helps offset

the cost benefit ratio of someone exploiting the bug instead of reporting it.

It can also be used as a powerful recruiting mechanism for talented

hackers.

■ Emergency Fund - This is a cushion for unexpected obstacles that may

arise.

The 30% put in reserves may be sold to lenders on our platform at a minor discount, matching

demand for higher interest rates on loans. For example, if $5M worth of loans are issued one

month, we may offer $50,000 worth of tokens for sale at a discount to those lenders, in

exchange for a better interest rate, depending on the capital needs of the business.Burner of Last Resort

Additionally, a percentage (to be determined) of the monthly revenue of the company will be

used to purchase HIP tokens from the market. These tokens will then be burned, reducing the

total supply of tokens, providing a stabilizing pressure to the price.

Security Audit

The HiP team is committed to ensuring the security of its platform. With each product release,

HiP commits to performing a security audit with both internal and external reviewers.

Additionally, there will be a Bug Bounty program that rewards developers for finding security

and other related issues.

Creating Value and Revenue

Value within the company and token economy will come with scale in liquidity and user count.

By providing class competitive Fintech banking services paying 5% + interest on all deposit

accounts HiP believes scale in number will be achieved quickly. Value is also created during the

process of regulation, both locally and internationally. HiP has secured the first licences

permissions subject to capital requirements being met.

Roadmap

● Q4 2019 - Retail Borrowers

● Q1 2020 - Corporate Loans to Gold-Shops, Micro-Lenders

● Q2 2020 - Bank Style Interface for Lenders and Borrowers

● Q4 2020 - Expansion into Real Estate, other Asset Classes

● Q4 2021 - Expansion into other ASEAN countries

Our initial product offering is bootstrapping an existing gold-lending business onto the

blockchain, providing additional transparency and accountability for the business and potential

liquidity providers. In more detail, we project our numbers below.

● Q3 2019 - Beta platform – complete

○ Between 1% and 3% interest made on all lending

● Q4 2019 - Completion of funding up to £6m

○ ~100 users

○ ~$2m lending volume

○ $2.5m is required paid-up capital for license applicant

■ Nano-Finance - $1.7M

■ Pico Plus - $430K

■ Pico - $270K

■ Custodian License - $100K

● Q1 2020○ ~1000 users

○ ~$5m lending volume

● Q2 2020 - Direct to Market Retail Offering (Thailand)

○ ~4000 users

○ ~$10m lending volume

○ Complete license acquisition

○ Increase high net worth and institutional money deposits

○ International trade liquidity provisions

○ Increase margin on all trades from 3% to 9% interest on all lending

○ Investors and liquidity returns increase from 0.75% to 5%

● Q3 2020

○ ~10k users

○ ~$20m loan volume

● Q4 2020 - Expansion into Real Estate

○ ~50k users

○ ~$50m loan volume

○ $95B Thai Real Estate Lending Market2

● Q4 2021 - Expansion into ASEAN

○ ~500k users

○ ~$100m loan volume

○ Begin lending in Vietnam and Philippines ~$550B GDP

We can take these growth estimates and plug them into the medium of exchange equation (see

above) to project growth in token value.

2

https://www.globalpropertyguide.com/Asia/Thailand/Price-HistoryAlternative Asset Classes

After having a significant amount of traction, we plan to expand the HiP platform into other asset

classes for collateral. These include, but are not limited to

● Other precious metals

● Gemstones

● Real Estate

● Corporate Shares

● Cryptocurrency

Each of these collateral classes is its own project, as they each have their own

● Security Risks

● Appraisal Processes

● Price Volatility

● Due Diligence Processes

● Legal Framework

These will be addressed as market forces and execution challenges emerge into clarity.

Nevertheless, the HiP business model is fundamentally asset class agnostic and can be applied

to anything of real world value.Early Withdrawal

As the system grows, we will be able to open up the possibility for lenders to withdraw their

investments before the loan expires. This can be done in several ways once there is sufficient

liquidity on the platform:

● The company purchases the debt from the user

● The company connects users to each other via OTC

● A secondary trading market

This increased flexibility should attract new customers and increase the loan volume, as it

reduces the barrier to entry.

Team

Kai Peeters

Prior to HiP, Kai led successful start-ups and established companies across Internet, mobile,

banking and IT. They included an IT consultancy trading within top-tier investment banks, a

social/retail marketing platform, luxury watch brand, luxury car club and a number of innovative

betting companies through social, affiliate, sports and bitcoin betting concepts, including a

bitcoin casino. They have all given me extensive and varied knowledge and experience which I

apply to drive success.

Hongthai TanHongthai is a seasoned property developer with countless large-scale real estate projects in progress and completed, including the Thananan Village housing project (924 units), Bangkok, and the Crystal Patong, Phuket. Hongthai holds a Doctorate in Hydrology from the University of Cambridge UK, with masters and bachelor degrees in economics. Hongthai is also honorary consul of Djibouti to Thailand. Hongthai heads up the HiP Thailand operation. Christopher Smith Christopher is an established crypto innovator. He has spent many years as the co-founder and CTO of crypto projects including Lunyr and BitMesh. Christopher has also developed algorithms for IOT and deep learning applications. He was a PhD candidate in Mathematics and Computer Science and holds an M.S. and B.S. in Mathematics and Computer Science respectively. Tobias Straessle

Tobias is a 35+ year veteran of the Financial Services industry having worked as CIO, COO and Management Consultant. He was involved in the development of many state-of the-art electronic trading and clearing systems for exchanges and investment banks as well as several post-merger technology integration projects of international scale. He held senior executive roles with Saxo Bank Group, UBS Investment Bank, UBP & Accenture. He was also chairman of Saxo Bank Switzerland AG and holds a M.S. in Mathematics from the Federal Institute of Technology in Zurich (ETHZ) and an M.B.A. from Northwestern University, Chicago. Most recently he is involved with several start-ups in the fintech and blockchain space. Sam Collett A lover of all things digital Sam is called on by all sorts of folks to help their business or problem, everything from ideas for an interactive theme park (really), to coming up with game ideas to judging the sanity of a startup business. He started his web career way back in '97. Since then he has worked at many award winning agencies creating many campaigns, sites, apps, games and digital things. Jaturont Jamigranont

Jaturont is an experienced operator in the field of credit in Thailand. Currently sitting as the chief operations officer of multiple credit institutions across Bangkok, Jaturont has been slowly modernizing these businesses by digitizing their daily operations. With background in information design and data visualization, Jaturont seeks to revolutionize Asia’s credit markets using HiP as a foundation. Jon Matonis A monetary economist focused on expanding the circulation of nonpolitical digital currencies, Jon also serves as an independent board director to companies in the Bitcoin, the Blockchain, mobile payments, and gaming sectors. Jon has been a featured guest on CNN, CNBC, Bloomberg, NPR, Al Jazeera, RT, Virgin Radio, and numerous podcasts. As a prominent fintech columnist with Forbes Magazine, American Banker, and CoinDesk, he recently joined the editorial board for the cryptocurrency journal Ledger. His early work on digital cash systems and financial cryptography has been published by Dow Jones and the London School of Economics.

Matt Mcgraw Matt is an entrepreneur and CEO with expertise in quickly scaling successful businesses. After leading and shepherding a versatile range of tech companies, Matt’s current focus is on technologies that disrupt hierarchies, and disseminate control of secure information to data users, ranging from individuals to enterprise clients. As CEO and co-founder of The Bureau, Matt uses his innate design thinking focus to complement a belief that good corporate governance and culture make success possible. DISCLAIMER NOT AN OFFER TO SOLICIT SECURITIES AND RISKS ASSOCIATED WITH HIP AND THE HIP APPLICATION This document is for informational purposes only and does not constitute an offer or solicitation to sell shares or securities in HiP Interactive Property Ltd or any related or associated company. Any such offer or solicitation would only be made by a confidential offering memorandum and in accordance with applicable securities and other laws. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this document does not constitute investment advice or counsel or solicitation by HiP Interactive Property or the distributor/vendor (‘Distributor’) of the HiP Tokens for investment in any security. This document does not constitute or form part of, and should not be construed as, any offer for sale or subscription of, or any invitation to offer to buy or subscribe for, any securities, nor should it or any part of it form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. HiP Interactive Property expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or

indirectly from: (i) reliance on any information contained in this document, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting therefrom. No regulatory authority has examined or approved of any of the information set out in this Whitepaper. The publication, distribution or dissemination of this Whitepaper does not imply that the applicable laws, regulatory requirements or rules have been complied with. This Whitepaper, any part thereof and any copy thereof must not be taken or transmitted to any country where distribution or dissemination of this Whitepaper is prohibited or restricted. No part of this Whitepaper is to be reproduced, distributed or disseminated without our express written permission. If you are in any doubt as to the action you should take, you should consult your legal, financial, tax or other professional advisor(s). The HiP token, or “HIP”, is a cryptographic token used by the HiP application. HIP is not a cryptocurrency. At the time of this writing, (i) with the exception of being used to boost interest on the HiP platform, HIP cannot be exchanged for goods or services, (ii) HIP has no known uses outside the HiP application, and (iii) HIP cannot be traded on any known exchanges. HIP is not an investment. There is no guarantee – indeed there is no reason to believe – that the HIP you purchase will increase in value. It may – and probably will at some point – decrease in value. HIP is not evidence of ownership or right to control. Controlling HIP does not grant its controller ownership or equity in HiP Interactive Property, or any other company, or the HiP Application. HIP does not grant any right to participate in the control, direction or decision making of HiP Interactive Property or any other company or the HiP application.

Market & Industry Information & No Consent of other Persons This Whitepaper includes market and industry information and forecasts that have been obtained from internal surveys, reports and studies, where appropriate, as well as market research, publicly available information and industry publications. Such surveys, reports, studies, market research, publicly available information and publications generally state that the information that they contain has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of such included information. Save for HiP Interactive Property, the Distributor and their respective directors, executive officers and employees, no person has provided his or her consent to the inclusion of his or her name and/or other information attributed or perceived to be attributed to such person in connection therewith in this Whitepaper and no representation, warranty or undertaking is or purported to be provided as to the accuracy or completeness of such information by such person and such persons shall not be obliged to provide any updates on the same. While HiP Interactive Property and/or the Distributor have taken reasonable actions to ensure that the information is extracted accurately and in its proper context, HiP Interactive Property and/or the Distributor have not conducted any independent review of the information extracted from third party sources, verified the accuracy or completeness of such information or ascertained the underlying economic assumptions relied upon therein. Consequently, neither HiP Interactive Property, the Distributor, nor their respective directors, executive officers and employees acting on their behalf makes any representation or warranty as to the accuracy or completeness of such information and shall not be obliged to provide any updates on the same. No Advice No information in this Whitepaper should be considered to be business, legal, financial or tax advice regarding HiP Interactive Property, the Distributor, the HiP Tokens, the HiP Interactive Property Token Generating Event and the HiP Interactive Property Wallet (each as referred to in the Whitepaper). You should consult your own legal, financial, tax or other professional adviser regarding HiP Interactive Property and/or the Distributor and their respective businesses and operations, the HIP Tokens, the HiP Interactive Property Token Generating Event and the HiP Interactive Property Wallet (each as referred to in the Whitepaper). You

should be aware that you may be required to bear the financial risk of any purchase of HiP Tokens for an indefinite period of time. Restrictions on Distribution & Dissemination The distribution or dissemination of this Whitepaper or any part thereof may be prohibited or restricted by the laws, regulatory requirements and rules of any jurisdiction. In the case where any restriction applies, you are to inform yourself about, and to observe, any restrictions which are applicable to your possession of this Whitepaper or such part thereof (as the case may be) at your own expense and without liability to HiP Interactive Property and/or the Distributor. RISK DISCLOSURES 1) Risk of Losing Access to HIP Due to Loss of Credentials The purchaser’s HIP may be associated with a HiP account until they are distributed to the purchaser. The HiP account can only be accessed with login credentials selected by the purchaser. The loss of these credentials will result in the loss of HIP. Best practices dictate that purchasers safely store credentials in one or more backup locations geographically separated from the working location. 2) Risks Associated with the Ethereum Protocol HIP and the HiP application are based on the Ethereum protocol. As such, any malfunction, unintended function, unexpected functioning of or attack on the Ethereum protocol may cause the HIP application or HIP to malfunction or function in an unexpected or unintended manner. Ether, the native unit of account of the Ethereum protocol may itself lose value in ways similar to HIP, and also other ways. More information about the Ethereum protocol is available at https://www.ethereum.org. 3) Risks Associated with Purchaser Credentials Any third party that gains access to or learns of the purchaser’s login credentials or private keys may be able to dispose of the purchaser’s HIP. To minimize this risk, the purchaser should guard against unauthorized access to their electronic devices. 4) Risk of Unfavorable Regulatory Action in One or More Jurisdictions Blockchain technologies have been the subject of scrutiny by various regulatory bodies

around the world. The functioning of the HiP application and HIP could be impacted by one or more regulatory inquiries or actions, including the licensing of or restrictions on the use, sale, or possession of digital tokens like HIP, which could impede, limit or end the development of the HiP application. 5) Risk of Alternative, Unofficial HiP Application Following the Crowdsale and the development of the initial version of the HiP platform, it is possible that alternative applications could be established, which use the same open source code and protocol underlying the HiP application. The official HiP application may compete with these alternative, unofficial HIP-based applications, which could potentially negatively impact the HiP application and HIP, including its Value. 6) Risk of Insufficient Interest in the HiP Application It is possible that the HiP application will not be used by a large number of businesses, individuals, and other organizations and that there will be limited public interest in the HiP application. Such a lack of interest could negatively impact HIP and the HiP application. 7) Risk that the HiP Application, As Developed, Will Not Meet the Expectations of HiP or the Purchaser The HiP application is presently under development and may undergo significant changes before release. Any expectations or assumptions regarding the form and functionality of the HiP application or HIP (including participant behavior) held by HiP or the purchaser may not be met upon release, for any number of reasons including mistaken assumptions or analysis, a change in the design and implementation plans and execution of the HiP application. 8) Risk of Theft and Hacking Hackers or other groups or organizations or countries may attempt to interfere with the HiP application or the availability of HIP in any number of ways, including service attacks, Sybil attacks, spoofing, smurfing, malware attacks, or consensus based attacks. 9) Risk of Security Weaknesses in the HIP Application Core Infrastructure Software The HiP application consists of open source software that is based on other open source software. There is a risk that the HiP team, or other third parties may intentionally or unintentionally introduce weaknesses or bugs into the core infrastructural elements of the HiP application interfering with the use of or causing the loss of HIP. 10) Risk of Weaknesses or Exploitable Breakthroughs in the Field of

Cryptography Advances in cryptography, or technical advances such as the development of quantum computers, could present risks to cryptocurrencies and the HiP platform, which could result in the theft or loss of HIP. 11) Risk of HIP Mining Attacks As with other decentralized cryptographic tokens, the blockchain used for the HiP application is susceptible to mining attacks, including double-spend attacks, majority mining power attacks, “selfish-mining” attacks, and race condition attacks. Any successful attacks present a risk to the HiP application, HIP, and expected proper execution and sequencing of Ethereum contract computations. Despite the efforts of the HiP team, the risk of known or novel mining attacks exists. 12) Risk of Lack of Adoption or Use of the HiP Application While HIP should not be viewed as an investment, it may have value over time. That value may be limited if the HiP application lacks use and adoption. If this becomes the case, there may be few or no markets following the launch of the platform, potentially having an adverse impact on HIP. 13) Risk of an Illiquid Market for HIP There very well may never be a secondary market for HIP. There are currently no exchanges upon which HIP would trade. If ever exchanges do develop, they will likely be relatively new and subject to poorly understood regulatory oversight. They may therefore be more exposed to fraud and failure than established, regulated exchanges for other products and have a negative impact on HIP. 14) Risk of Uninsured Losses Unlike bank accounts or accounts at some other financial institutions, funds held using the HiP application or Ethereum network are generally uninsured. In the event of any loss, there is no public insurer, such as the FDIC, or private insurer, to offer recourse to the purchaser. 15) Risk of Dissolution of the HiP Project It is possible that, due to any number of reasons, including an unfavorable fluctuation in the value of Ether, development issues with the HiP application, the failure of business relationships, or competing intellectual property claims, the HiP project may no longer be viable as a business or otherwise and may dissolve or fail to launch. 16) Risk of Malfunction in the HiP Application It is possible that the HiP application malfunctions in an unfavorable way, including one that results in the loss of HIP. 17) Unanticipated Risks

Cryptographic tokens are a new and somewhat untested technology. In addition to the risks discussed in this White Paper, there are risks that the HiP team cannot anticipate. Further risks may materialize as unanticipated combinations or variations of the discussed risks or the emergence of new risks.

You can also read