Indian Association of Investment Professionals Indian Institute of Foreign Trade, New Delhi - CFA Institute Research Challenge

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge

Hosted by

Indian Association of Investment Professionals

Indian Institute of Foreign Trade, New Delhi

1

This report is published for educational

purposes only by students competing in the

CFA Global Investment Research Challenge Havells India Limited

Date 09.11.2016 Electrical goods

NSE: HAVELLS | BSE: 517354 India

Recommendation SELL

Price Target: INR 321.4

Price 08.11.2016: INR 392.45

Downside: 18.1% Highlights

We issue a SELL rating on Havells India Limited (HIL) with a one year

target price of INR 321.4, arrived at by using the Discounted Free Cash

Flow to the Firm Method and relative valuations based on trading

Key Ratios 2016A comparables. Havells India Limited is one of the largest electrical equipment

Int Cover 15.25x manufacturers in India and classifies itself as a fast moving electrical goods

company. It operates in four major business segments viz. switchgear,

P/E 47.80x cables, LED lightings and fixtures and Electrical Consumer Durables.

P/BV 5.90x Inadequate presence in the tier 2, tier 3 and rural areas is a big factor that

P/Cash EPS 45.80x could see the company’s growth trajectory marginally stalled as the company

shows an uneven 70:30 distribution network across urban and rural regions.

M Cap/Sales 2.85x

The company is now working towards an FMCG like distribution network to

EV/EBITDA 28.42x strengthen its presence in the source markets of the future growth.

ROCE 10.60% A considerable war chest for acquisition means that the company

ROE 24.10% currently stares at c. INR 23.5 per share. This cash, lying idle and earning no

or base returns would translate into a lower return on equity (RoE), hurting

Debt/Equity 0.00x the overall profitability of the company.

EBITDA Margin 10.51% Lightings and cables business hit a roadblock as the stark plunge in the

Net Profit Margin 15.80% LED lighting prices, reducing CFL market in India and highly volatile copper

and aluminium prices have somewhat stalled the business growth that the

company was expecting to reach. Economic options in the cables segment to

Market Data cater to the increasing demand from the rural area also poses a threat of

market cannibalization.

Market Capitalization INR 244.89 bn

(in INR bn except

Shares Outstanding 624.57 mm 2015A 2016A 2017E 2018E 2019E

per share data)

Free Float 38.04% Revenues 85.69 77.14 83.81 91.62 100.98

52 Week High/Low INR 459.40/235.30

EBITDA 7.21 8.12 11.31 12.60 14.14

Avg. Monthly Volume 3,05,342.33 Net Income 3.85 12.21 8.27 9.38 10.55

Beta 0.81 Net Profit Margin (%) 4.50% 15.80% 9.87% 10.24% 10.44%

EPS 6.22 8.21 13.34 15.13 17.01

700

DPS 3 3 3 3 3

600

500 Valuation: We opine that Havells India Limited is already trading at a very

400

high P/E multiple of 31.48x and P/BV multiple of 9.57x and is expected to

300

undergo correction. This is because despite the fact that the company is

200

going in the right direction with a stronger distribution network and a

100

0

defensive core business, the market seems to have already factored that in

Oct-11 Oct-12 Oct-13 Oct-14 Oct-15 Oct-16 making the correction a strong possibility.

NIFTY SENSEX HAVELLS

Source: Bloomberg, Company Fillings

Important disclosures appear at the back of this report

2

Business Description

Chart 1.1 : Revenue Breakdown by Segment (%)

About Havells India Limited

• HIL is one of the largest electrical equipment manufacturer in India. Incorporated in

1983, the company today has crossed a billion-dollar revenue mark on consolidated

basis and classifies itself as a fast moving electrical goods company.

• The company operates businesses in four major segments – Switchgears, Cables,

Lighting and Electrical Consumer Durable.

HT • HIL is currently rated AAA by CARE and AA+ by ICRA with a stable outlook.

Product Segments

Switchgears: Under this segment HIL operates in two major segments which are

domestic MCB and modular switches and has witnessed a CAGR of 12% in last five

years and in total this segment forms the second biggest part of company’s revenue

Source: Company Fillings contributing 23.7% in FY’16 with a Y-o-Y growth of 0.55% and has the highest

contribution margin at 39.2%. The company has a market share of around 28% in

Chart 1.2 : Segment Contribution Margin (%) domestic MCB market and around 15% in modular switches market. The company also

operates under the brands Standard and Crabtree and is expanding its portfolio with the

Sylvania stake sale latest launch of Reo and Reo Bliss.

Cables: Under this segment HIL operates in both domestic and industrial cable

segments and this segment has witnessed a CAGR of 12% in last five years and forms

the biggest part of the company’s revenue, contributing almost 40.6% in FY’16 with an

overall contribution margin of 14.2%. The company has market share of almost 16% in

domestic and 10% in industrial segment. This segment witnessed a growth of 0.8% as it

was largely influenced by the commodities prices of copper as the benefits have to be

passed-on to the customers.

Lighting: Under this segment the company operates in two product categories lamps

and fixtures and has witnessed a CAGR of 12% in last five years and contributes 14.7%

to the company’s revenue with a contribution margin of 24.1%. Amongst the two

categories, fixture category (including LED) forms 70% of the segment revenue. The

company has a market share of around 14%. The major focus of the company is on the

Source: Company Fillings LED segment which witnessed 100% Y-o-Y growth and which forms 51% of the

segmental revenue. The acquisition of Promptec will boost LED and solar segment over

the coming years.

Chart 1.3 : HIL EPS and Dividend Payout Ratio

Electrical consumer durables: The segment comprises of fans, water heater and

domestics appliances and has witnessed a CAGR of 19.5% in last five years. This

segment forms 21% of the revenue in FY’16 with a Y-o-Y growth of 11% and with a

contribution margin of 25.2%. Fans forms 70% of the revenue in this segment and the

company has a market share of 15% and is the only company to produce all four types

of fans: ceiling, table, pedestal and wall fans. The company has launched various new

kitchen appliances and air coolers and has ventured into niche category of air purifiers.

The company also plans to launch solar water heaters in the coming years.

Business Description

Company strategies

Source: Company Fillings Focus on domestic markets

During the year the company divested 80% stakes in its WOS Havells Malta Ltd. and

80% stake in Havells Exim Limited for a net consideration of INR 10.87bn to continue

Growth drivers for HIL

focus on Indian operations. This divestment will improve company’s financial position

and profitability. To expand in the domestic markets and garner market shares company

Government spending on Real estate market up-tick,

infrastructure sector brand based consumerism

entered into a purchase agreement with Promptec Renewable Energy Solutions Pvt.

Ltd. to acquire a 51% stake for a net consideration of INR 291.2mm. This acquisition will

help the company to expand in LEDs and solar lightening solution.

LED pushing initiatives

High capital expenditure

like subsidies by Focus on tier 2 and tier 3 cities

being incurred by industry

Government

The company will be penetrating more in the Tier-2 and Tier-3 markets to tap-in the

Increasing electrification growth of these cities with its wider distribution reach and planning to expand to 1100

Favorable demographics of rural areas by

Government

cities from currently 700 cities having population of more than 50,000. The company

also plans to expand in the western and the southern markets which currently

Source: Student Research contributes only 15% and 25% respectively to the revenues.

Important disclosures appear at the back of this report

3

Business Description

Chart 1.4 : Marketing & Advertisement Spend of HIL

Established manufacturing base: HIL currently has 12 manufacturing units and

produces c. 92% of the products in-house which is the highest in the industry. In FY’16,

it operationalized its plant in Neemrana, Rajasthan for manufacturing of modern electric

water heater. It is in the process of setting up two more manufacturing units at Guwahati,

Assam for switchgears and Bangalore, Karnataka for cables which may be operational

by FY’18 with a total investment of INR 1.4bn. HIL has a policy of one plant one product

to focus on efficiency. The current utilization level at each plant is c. 70-80%.

Projection as a lifestyle brand: HIL enjoys a strong brand recall and operates in the

HT premium end of the market where it is targeting next generation with automation, state-

of-the-art switchgears and remote controlled electrical devices and is able to maintain

high contribution margins. These smart devices dovetail with the Govt. initiatives of

smart cities. It has consistently been spending 3-4% of revenues as advertising and

Source: Company Fillings marketing expense and has increased its hiring as a strategic move to align itself as a

FMEG brand and is continuously expanding and differentiating their product portfolio.

Chart 1.5 : Shareholder Structure (%) Augmenting distribution network for expansion: HIL has the widest network of

distributors and dealers amongst all electrical goods manufacturers. It has c. 85000

dealers + distributors, c. 100000 retailers and has exclusive chain of showrooms called

Havells Galaxy which contributes c. 12% to the revenue. Currently the company has 375

exclusive showrooms and plans to expand it to 600 showrooms by FY’18.

Shareholder structure: As on 31st March, 2016, HIL is 61.63% owned by promoters

and 38.37% owned by public. In the public holding part, 29.74% is owned by institutions

and 8.62% is owned by non-institutions. In the institutional holding part, 4.19% is held by

Domestic Institutional Investors and 25.55% is Foreign Institutional Investors.

The largest shareholder and promoter QRG Enterprises Ltd. (30.40% of shares) entered

a revised Trademark License Agreement with HIL’s pursuant to which the rights of the

brand were transferred to the company for no consideration w.e.f. April 01, 2016.

Source: Company Fillings Corporate Management:

Mr. Anil Rai Gupta became the new CMD of HIL on 13th November, 2014 after the

Chart 1.6 : Net Income (INR bn) demise of the founder and former CMD Mr. Qimat Rai Gupta. He has served the

company as Executive director and Joint Managing Director since 2006. HIL reported a

marginal increase in PAT over 2014-16 following the 80% divestment in Havells Malta

Ltd. and Havells Exim Ltd. In FY’15, HIL expanded its Board of Directors from nine to

twelve. Mr. Puneet Bhatia and Mr. Monhandas Pai were added as non-independent and

non-executive BOD, Mr. Aveent Kumar Gupta was added as whole time director, Ms.

Pratima Ram, a female director was added as an independent director.

Corporate Governance

Corporate governance

Board: The composition and election of the Board of Directors is in accordance with the

requirements of the Companies Act 2013 and the Clause 49 of Listing Agreement.

However, an area of concern is the Independence of the Independent Directors since

majority have been holding the office since a period of 5 years or more.

Source: Company Fillings

Corporate Committee: The committees have been constituted based on the

Companies Act, 2013 and Clause 49 of Listing Agreement. Meetings were duly held.

Remuneration of Key Management Director Remuneration and Shareholding: The Directors hold 8.47% shares, of which

8.26% is held in the capacity of Promoters. The remuneration to directors were within

the prescribed limits of the Companies Act 2013.

INR (mm) 2016 2015 2014

Statutory Auditors: One of the Joint Auditors appointed and proposed for re-

MD / WTD / appointment is S.R. Batliboi & Co LLP, an EY member firm, which has issued an

225.08 239.00 157.33 unqualified Auditors Report on the Standalone Financial Statements; concluding a high

Manager

level of Internal Control and adoption of good Corporate Governance practices.

Directors 6.24 5.16 1.2 Corporate Social Responsibility

The company believes that corporates have a special and continuing responsibility

Key Managerial towards social development. It has taken CSR activities through QRG Foundation, a

4.86 3.98 -

Personnel trust instituted by the group. The company has constituted a CSR committee with four

board members and has been spending 2% of the average profit for last three years for

CSR activities (INR 114.8mm in FY’16). Some of the major initiatives involves Mid-Day

Source: Company filings

Meal to 57,000 children in 672 schools, sanitation facilities in 102 schools by setting up

of 816 toilets, donation of tables & benches to Govt. schools in Haridwar.

Important disclosures appear at the back of this report

4

Industry Overview and Competitive Positioning

Chart 2.1 : GDP Growth of India (%) The Indian economy is expected to show more than 7% GDP growth

rate despite looming uncertainties

7.6

7.2

2016 saw a number of key macroeconomic activities shaping the world economy like

6.6 Brexit vote and US economy revival. The continuous volatility of the financial market

6.2

5.9 along with declining commodity prices has resulted in weak growth of the world

5.6

5.3 economy and an overall sentiment of caution amongst investors. India showed robust

growth rate of 7.6% in 2015-16, while the average global economy growth was 3.1%,

4.3

making India the fastest growing economy in the world.

2012-13 2013-14

HT 2014-15 2015-16 The outlook for Inflation in India seems positive and in the near future, it is expected to

be around the RBI’s target range of 4% +/- 2%. Both, the CPI and WPI data depicts

GDP Growth Per Capita GDP Growth that the RBI has been successful in keeping the inflation in check and in the target

Source: Economy Survey 2015-16

range of 4% - 6% over the period. The recent government policies like the revamped

PDS with JAM will improve the purchasing power in rural India, and stimulate demand

in the economy. Also, the rollout of GST bill might have a huge stimulus in the

Chart 2.2 : WPI and CPI rates in India (%) economy because of the increased margins for the suppliers as well as lower costs for

the consumers. IMF forecast the GDP growth to be 7.7% in 2017. The expected

increase in oil prices and geo-political tension between India and Pakistan together

with policy changes in US post elections might pose significant risks in the future.

Switchgear segment

The industry forms 15.9% revenue of Transmission and Distribution equipment

industry and is expected to grow at a CAGR of 19.2% till 2020

The switch-gear market is expected to grow in coming years with a push for pan India

electrification and to generate 175GW from renewable resources by 2022. The

increase in the real estate activity in Tier 2 and Tier 3 cities and a greater focus on

Source: Economy Survey 2015-16 safety will also push the growth in domestic switch-gear market currently at INR 20,000

mm. The segment has got significant thrust with opening up of sector to 100% FDI and

Chart 2.3 : Segment Growth of Electric a significant improvement in technology. The switch segment which is broadly

Equipment Industry (INR bn) classified into non-modular which accounts for INR 15bn and modular switches which

currently stands at INR 20bn is set to gain as customers look for attractive and energy

efficient switches. The top 4 players in switches account for almost 70% of the

organized market and that forms almost 75% of the total switches market.

Lighting and EESL segment

Rising personal disposable income, growing government initiatives encouraging

use of LED lights and increasing focus on smart city projects to spur growth

These factors are set to push the lighting market in India from INR 120bn in 2016 to

INR 370bn by 2020, driven mainly by the LED lighting business. Government initiatives

for energy conservation by partnering with EESL and providing LED light bulbs under

the RGGVY initiative has already provided a strong foundation for the LED business.

Electric Lamp and Component Manufacturer’s Association of India (ELCOMA) expects

the LED lighting business to grow by a CAGR of 40% over 2016–2020, which will

further drive up the lighting business which is expected to clock a CAGR of 18% over

the same period. Thus, this sector provides a gainful avenue for investment.

Source: ELCOMA Cables segment

The industry is poised to grow at a CAGR of 7-8% till year 2019 with a thrust

from infrastructure, telecommunication and power sectors.

Chart 2.4 : Lighting Industry Expected

Growth (INR bn, %) Currently domestic cable segment stands at INR 80bn and industrial cable segment

stands for INR 120bn. The major demand is likely to come from power, infrastructure

and telecom sector. With 4G spectrum allocation and a push for housing through the

setup of Rural Housing Board, demand for cable is likely to increase in the near future.

The sector is being granted 100% FDI under automatic route. The major risk for this

segment comes from imported cables from China and Commodity price fluctuations,

mainly in aluminium and copper.

Electrical consumer durables segment

Increasing investments, driven by growing demand and policy support will drive

this sector to a 10.5% CAGR over FY16-FY20

Due to the aforementioned growth drivers, further supported by increasing

electrification of rural areas, rising working age population and further penetration into

the untapped rural market, the overall market size of ECD sector in India would reach

Source: ELCOMA

INR 1375bn.

Important disclosures appear at the back of this report

5

Industry Overview and Competitive Positioning

Chart 2.5 : Competitor Operating Margins

Comparison (INR bn, %) The rural markets, which contribute 33% of the revenue, are set to grow at 25% CAGR

over the next 5 years. Modified Special Incentive Package Schemes (M-SIPS), National

Electronic Policy (2012) and relaxed FDI norms for electronic hardware manufacturing

and multi brand retail will further fuel growth. The production is expected to increase to

INR 6.9tn by 2020 and the electronics market size is expected to increase to INR 26.7tn

from INR 6.3tn during the same period. As a result, ECD sector provides a lucrative

prospect for investment.

Competitive Positioning

Production capacity – Higher capex, building newer plants and one plant one

product policy

The company has been investing in new manufacturing facilities and produces almost

92% products in-house. The company has consistently invested ~2-2.8% of revenue as

capex over years. The domestic manufacturing will benefit the company in depreciating

Source: Bloomberg

INR environment as it has the lowest levels of imports among Indian consumer

electrical companies. The current utilization capacity being 70-80% across various

plants, so the company will be in a competitive position to expand the production as

Chart 2.6 : Marketing and Advertisement demand picks up. This strong manufacturing base has led doubling the market share of

Spend of Havells v/s peers (% of revenue) HIL in almost every product segment in last 10 years. The company has maintained a

lean working capital cycle of 15 days owing to high debtors discounting and channel

financing which are off-balance sheet items. Excluding debtor discounting and channel

financing, debtor days will be in-line with the industry.

Cost leadership – Premium products and pricing

The company is dominant in premium segment and is able to charge a premium for its

products. The company is a dominant player in premium fans segment and a smaller

presence in mass market segment, company’s product line stats from INR 1,800

whereas other competitor’s product line starts from INR 1,100. In wires and cables, the

company is able to sell at a premium as compared to Finolex and Polycab. In

switchgears, the company is a market leader and has one of the highest contribution

margins in the industry. In ECD, company had launched multiple new appliances and

Source: Companies Fillings this steady widening of portfolio will be contributing to the growth in this segment in the

coming years.

Chart 2.7 : Market Structure of Segments Strength of brand – Marketing expenditure, multi-product dealership, product

portfolio

The company has a strong top of the mind recall because of the marketing campaigns

run by the company. The marketing expenditure has been one of the highest in the

industry and is around ~3% of the revenue consistently. Dealerships of the company is

a multi-product dealership unlike other competitors which are only single product

dealership. With the opening up of HIL’s Galaxy stores which are one stop stores for

HIL’s products adds to the brand visibility. HIL is the only company to be present across

the entire consumer electrical space covering from switchgears to cables to kitchen

appliances. This wide presence and the continuous expansion gives the company more

Source: Various visibility through shelf space on multi-brand retail stores

Improved Distribution network and Services- Strong connect with the electricians,

Table 2.1 : Competitor Portfolio Analysis

Dealer incentive structure, Customer services

Segment Havells Finolex Polycab CG Bajaj Philips ABB

The company has a strong focus to build a dealer network and the largest number of

dealers and distributors amongst competitors. The company had made tremendous

Cables and

* * * efforts to connect with retailers and electricians with almost 200,000 registered

Wires

electricians as they play a significant part in influencing the decision making of the

Domestic

Switchgear * * customers. The company has joined with banks to finance the working capital of the

dealers, which appears as a contingent liability on the Balance Sheet and currently

Industrial stands at INR 3.7bn. HIL’s is the only company to introduce customer services even for

Switchgear * *

the smallest SKU (Stock Keeping Unit). The cost of such a service is almost 1.5% of

Motors * * * annual revenue but helps in building a strong brand and gain customer trust.

Robust Return Ratios – High ROE, increasing cash inflows, cash lying on Balance

Capacitors * * * Sheet, High margins

Electrical

Switches * * * The company has constantly maintained one of the best RoE and RoC in the industry.

Lightening & Free cash inflow has been increasing for the firm and is expected to increase further on

Fixtures * * * * earnings growth and low working capital. It has maintained best EBITDA margins in the

Fans * * * industry. After the stake sale in Sylvania has, the company recorded an increased cash

Home

inflow and is eying a domestic acquisition to strength position in the domestic markets.

Appliances * * * *

Source: Companies Fillings

Important disclosures appear at the back of this report

6

Industry Overview and Competitive Positioning

Chart 2.8 : Porters Five Forces Analysis Innovation – In-house R&D capabilities, 185+ IPRs & 18+ patents

Competitive Rivalry

The company has been investing heavily in-house research and development and

5 continuous product development has been differentiating HIL’s from its competitors and

4 contributing towards its brand equity and premium pricing. The company has positioned

3 itself more of a lifestyle brand with the launch of home automation, remote controlled

electrical appliances. The company has launched energy efficient fans, fans with LED

Threat of new 2 Threat of

entrants Substitutes lights, Euro-II range of MCB, MCCB, Lumeno LEDs and even entry-level modular

1

switches for Tier-II and Tier-III cities. This constant innovation and increasing the churn

0 of products provides HIL’s with a competitive advantage and its higher multiple.

Investment Summary

Bargaining power Bargaining power We issue a SELL recommendation on Havells India Limited (HIL) with a target price of

of suppliers of customers

INR 321.4 using the Discounted Free Cash Flow to Firm and the relative valuation

Source: Student Research

method. This offers a 18.1% downside from its closing price of INR 392.45 on November

8, 2016. HIL would stand to gain from its highly diversified core business through a solid

Chart 3.1 : Copper and Aluminium Price Trends (INR) distribution network, which is set to improve as it continues to develop the same. The

500 seizure of payment of royalty from the current financial year will see the company gain

on its EBITDA margins as well. But the stock market seems to have already factored this

400 in and hence the stock could see considerable correction in the coming year.

300 HIL’s business is on the back foot mainly because (1) LED has seen and is expected to

continue seeing reduction in prices; (2) the cables business is being cannibalised by

200 companies providing budget options like Polycab and Finolex; (3) The switchgear

segment sees HIL as an established player only in the premium segment and its infancy

100

in the other segments could hurt the bottomline; (4) the ECD business is still a very small

0 contributor to the revenues and sees established players as a huge threat; (5) the

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 pension liabilities for the subsidiaries in Brazil and Thailand could hurt profitability.

Amongst other reasons, the government levied subsidies on LED lighting would see the

Copper Aluminium

prices fall furthers, thereby impacting the revenue despite growing volumes in the

Source: MCX SX business. Also, HIL’s decision of not competing for any EESL tender floated by the

Government of India in the coming financial year would see it lose out on its LED

Chart 3.2 : HIL Cash Balance (INR bn)

34.98 business as well. The volatility in the commodity prices, especially copper prices, will put

the margins under pressure as well.

Sylvania Stake Sale 26.86 Strong urban distribution network, but rural network is work in progress

20.19 The rural – urban distribution network is a 30:70 ratio for HIL which is somewhat

alarming, considering that the growth in a more or less flat for the coming couple of

14.70 years is expected to come from the rural and the tier-2 and tier-3 cities. The company

8.82 has recently started working on a goal towards becoming a fast moving electrical goods

7.77

(FMEG) company, trying to replicate the distribution network that the FMCG companies

boast of. But it is expected to be initially a cost intensive change as the benefits to lure

the distributors to be a part of this project could take a hit on the margins being earned

2014 2015 2016 2017E 2018E 2019E from the sales. Also, the acceptability of the premium products of HIL versus the

economic options like Finolex, Polycab, Crompton Greaves etc. is still a grey area.

Source: Company Fillings, Student Research

Huge unutilized cash reserves on the balance sheet

The sale of stake in Sylvania has added to the already built up huge cash reserves of

Chart 3.3 : HIL Manufacturing Facilities HIL. For These reserves, the company has clearly stated the intent of utilizing them to

acquire a company in the Indian market to help them reinforce their position in the Indian

markets. But the cash reserves of INR 23.54 per share sitting idle on the balance sheet

would further hurt the RoE that the company in the coming year. Also, in which business

would this acquisition be and what premium would the company be ready to pay at a

time which sees all the companies in this business trade at very high multiples, prevents

from getting any clear idea as well. The delay in realization of synergy with this possible

acquisition, as is the case with Promptec, could lead to further dampening of the returns.

The agreed sale of stake in the Brazilian and Thai business of Sylvania once it reached

profitability will add to this cash, with the possible utilization remaining nebulous.

Cables and LED business show stunted growth

The cable business is highly dependent on the copper commodity prices which have

been quite volatile in the past and is expected to remain the same in the future. This has

led to erratic and under pressure margins in the cables business, which contributes

almost a third of HIL’s revenue, yet it registered a mere 14% contribution margin, least

amongst all the businesses of HIL. The LED business too has seen volume growth but

Source: Company Fillings the stark plunge in the prices has led to a single digit growth since 2012.

Important disclosures appear at the back of this report7

Investment Summary

The migration from CFL to LED has also seen HIL needing to change the existing CFL

Table 4.1 : WACC Computation manufacturing facilities to LED manufacturing facilities. The decision to not participate in

the EESL tenders floated by the government this year on the back of inability to cater

Equity 99.30% the demand of the same could see them miss out on crucial business.

Debt 0.70% Valuation Methods

Levered Beta 0.81 We derived our target price by using 60:40 ratio of the Discounted Free Cash Flow to

Firm method and the relative valuation method.

Risk Free Rate 6.82%

Drivers of Volatility in Earnings

Market Return Rate 13.68%

The major drivers of volatility have been (1) divestment of stakes in Sylvania except

Cost of Equity 12.4% Brazil and Thailand; (2) the commodity price volatility and (3) plunging prices of LED

lighting. These are set to continue in the future, though the divestment of the remaining

Interest Rate 11.75%

stake in Sylvania is not expected to bring in similar volatility to the earnings as in the

Tax Rate 22% past. The possible acquisition or merger would also lead to volatility in the earnings,

which will further also be impacted by the synergy realization from the same.

Cost of Debt 11.75%

Possible investment risks

WACC 12%

Key risks that the investors must be aware of include regulatory risk such as delayed

Source: Bloomberg, Student Research implementation of GST. Business risk includes slowdown in real estate and

infrastructure sector, entry of new market players in business segments and upcoming

business in tier 2 and tier 3 cities. The technological risks would encompass continuing

technological constraints in LED lighting and disruption with new technologies in coming

Chart 4.1 : Havells Revenue in INR bn and Margins future. The strategic risks being faced are cannibalization of sales by technologically

105 17%

upgraded products, increased exposure to only Indian markets and expansion plans not

15.8% being as effective. The large, unutilized cash reserves also pose a financial risk. A

13.5% 13.8% 14.0% detailed discussion on each of these is provided in the Investment Risk section

85

12.0% 12.2% 12.6% 13%

65

10.5% 9.9% 10.2% 10.4% Valuation

8.4% 8.9% 9%

6.8%

45 DCF Valuation

4.5% 5% We used Discounted Cash Flows to the Firm (DCF) method to arrive at target price of

25 INR 260.1 per common share. This method requires estimation of free cash flows to all

the capital holders in the company and discounting it to arrive at an enterprise value. It is

85.69 77.26 83.81 91.62 100.98 1%

5 then adjusted with net debt to derive the equity value to finally determine the target

2015 2016 2017E 2018E 2019E price. The forecasted period is 2017-2021 for which the estimates have been drawn post

-15 -3% which a terminal value is obtained at a constant growth rate.

Revenue EBITDA Margin Revenue assumptions

EBIT Margin Net Profit Margin The revenue is projected for its 4 operating segments:

Switchgear: HIL operates in 2 sub-segments- a. Modular Circuit Breakers (TAM is c.

Source: Company Fillings, Student Research 23%) and b. Modular Switches (TAM c. 18%). The future revenues are forecasted by

estimating the market growth of these two sub-segments, expecting HIL to retain its

market share of 29% and 20% respectively in both of these sub-segments.

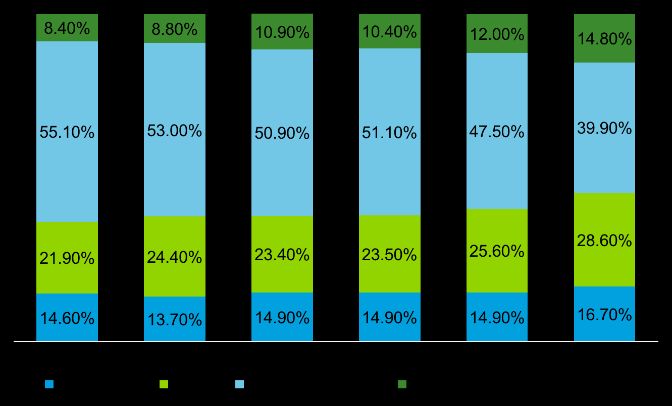

Chart 4.2 : Segment Wise Revenue Breakdown in bn Cables: HIL is a leading player in this segment. The past trends show this segment to

have become a stable business for HIL and thus it is expected to grow at a stable rate.

Lighting and Fixtures: This segment comprises of LED, CFL as the core technologies.

15.70 The remaining 20% stake in Sylvania contributes to this segment. Since the company

14.19 will be selling off this stake once it turns profitable, the revenue contribution is

10.28

12.76 considered constant as the focus is to improve the expenses side. Chile and USA

11.41

35.81 businesses are already contained, so only Brazil and Thailand subsidiaries are

33.50 considered as HIL. LED segment contributes c. 2/3rd to the domestic business and HIL

40.72 31.94

30.79 is expected to retain its market share in this fast growing market. The remaining 1/3rd of

the domestic business mainly constitutes of CFL for which the market is expected to

32.93 decrease in the future.

25.17 28.76

21.90 22.08 ECD: In ECD, c. 70% of revenue comes from fans. The future revenue is projected

according to market growth and remaining 20% is other ECD appliances like geysers for

12.79 12.86 13.94 15.17 16.54 which the overall growth of ECD market is considered a proxy for future projections.

Cost Assumptions

2015A 2016A 2017E 2018E 2019E

SG&A: These expenses are projected as a constant percentage of revenue. In future,

Switchgear Cables Lighting ECD we do not see HIL having any significant increase in its SG&A expenses as HIL is

already one of the highest spenders in advertising, comparable to the top FMCG

Source: Company Fillings, Student Research companies of India.

Employment Benefits: These expenses are projected as percentage of revenue. Since

the company is moving towards FMCG model of distribution and has huge pension

liabilities, these expenses are projected to grow at modest rate.

Important disclosures appear at the back of this report8

Valuation

Havells India Limited share price and news flow Stake sale in

Sylvania

1:5 stock split announced announced

European debt crisis impacts

Indian stock markets

HT

Market tumbles on concern Acquisition of Promptec

Markets rise as Oil and Gold prices slump due to weaker rupee announced

Cash flow assumptions

Table 4.2 : Havells Relative Valuation Depreciation and Amortization: Fixed asset turnover as percentage of revenue is taken

Company Segmental Segmental Contribution as 6 year average and is expected to remain constant in forecasted period. The D&A

Segments Revenue Revenue % Margins expense is taken as a fixed percentage of beginning Gross Fixed Assets that is calculated

by deducting the total accumulated D&A from the gross block at the end of previous year.

Sw itchgears 13.94 16.63% 37.72%

Capital Expenditure: The Capex is divided into 2 parts: - (1) Maintenance Capex- which is

Cables and Wires 25.17 30.03% 23.50% the same as D&A for that particular year and (2) Growth Capex- the remaining Capex is

classified as growth capex.

Lightening 31.94 38.11% 17.30%

Working Capital: HIL is expected to maintain its improved working cycle days. Thus, it is

ECD 12.76 15.22% 21.49% estimated by maintaining constant days of inventory for inventory forecast, days of

receivable for debtors and days of payable for creditors’ amount.

WACC assumptions

Sw itchgear Weighted Average Cost of Capital (WACC) is calculated using CAPM model. The risk free

rate of 6.82% is current yield on 10 year Indian bonds. Beta of 0.81 is calculated by

Max Median Mean

regressing the historical HIL return with respect to National Stock Exchange for a 5 year

From P/E 2017E 190.69 146.49 146.49 period. The market risk premium of 5.19% is on the basis of the Indian stock market

returns for the past 10 years. Tax rate of 22% is the current effective tax rate of company

From P/E 2018E 174.41 136.50 136.50 which will be effected once GST is applicable from April 1, 2017 but since the process of

its full implementation is under constant revision, the tax rate is considered unchanged.

Cables Using CAPM model, the WACC is 12%. HIL has negligent debt because as per guidance

the company is reserving cash and avoiding any big investments as it is looking for viable

Max Median Mean acquisition targets in ECD segment.

Price multiples

From P/E 2017E 132.69 98.21 98.21 DCF method was our principal valuation approach but we have also analysed trailing price

relatives of comparable firms.

From P/E 2018E 124.42 92.83 92.83

We found the most appropriate peer to be Finolex Cables since it is also engaged in

cables, lightings and switchgears. Majority of HIL’s business is in Lightings and Cables.

Lighting

Given the high marketing spend and the premium attached to the company’s products, HIL

has consistently posted higher Price to Earnings (P/E) ratios compared to Finolex. This

Max Median Mean

high relative P/E ratio indicate that HIL's stock will have a limited upside. HIL's historical

From P/E 2017E 87.44 67.68 67.43 performance indicates a CAGR of 39% over a 3-year period from INR 145.43/share to INR

392.45/share while that of Finolex’s CAGR is 87% from INR 65.95/share to INR 430/share

From P/E 2018E 80.11 61.01 60.62 over 3 years. This though proves that the company has been performing well but the

industry has been trading at a higher P/E with a premium attached to it.

ECD Also, a relative analysis was conducted among HIL's segmental and risk profile peers.

Bajaj Electrical and Crompton Consumer Electrical for ECD and Lightings are the most

Max Median Mean similar businesses.

Another measure for comparison is EV/EBITDA, which is appropriate in analysing the

From P/E 2017E 159.58 100.88 102.21 value of a company regardless of its capital structure. By using this method, the effect of

From P/E 2018E 141.88 95.58 94.63 depreciation policies is removed. An analysis of the EV/EBITDA ratios of these companies

reveals that HIL has been trading at a premium. The company has also provided higher

Havells India dividends as compared to its peers.

Financial Analysis

Max Median Mean

Strong revenue growth supported by solid industry growth

From P/E 2017E ₹ 570.40 ₹ 413.26 ₹414.32 The consolidated revenue of company has achieved growth almost entirely by company’s

From P/E 2018E ₹ 521.13 ₹ 385.92 ₹384.57 domestic business. With remaining 20% of Sylvania business expected to sell off soon, the

revenue CAGR is expected to improve further. Except the cable segment where due to

Source: Bloomberg

Important disclosures appear at the back of this report9

Financial Analysis

volatile copper prices the revenue growth is stabilised, other segments particularly MCB,

LED and ECD are expected to show high CAGR growth of c.12% in the 2017-2021 period.

Chart 5.1 : Forecasted Capex (INR bn) Backed by strong expectations, the volume sales are bound to increase. Though LED

3.35 segment is showing recent trends of price reduction, we believe that volume sales will

2.90

compensate for it as in India the market still has untapped regions and with growing GDP

2.60 and per-capita income, people will move towards efficient lighting in their homes.

Switchgear will continue to contribute maximum to revenue due to expected future growth

2.11 2.14

in this market. ECD Segment is expected to show highest growth in the product portfolio

Increasing margins with improvements backed by core operations

Sylvania business carried an unfunded liability of EUR 45mn. With this pension liability no

more expensed from income statement, the operating expenses are expected to improve

leading to better operating margins and net profit margins. Economies of scale and

distribution strength has enabled HIL to deliver superior margins, increasing margin from

11% in 2016 to 14.5% in 2021. The company has a number of pioneering incentives

2015 2016 2017E 2018E 2019E building a loyal dealership network vis-à-vis its peers. This is further strengthen due to

Source: Company Fillings, Student Research working capital cycle improvements. EBITDA CAGR is c. 10.7% and PAT CAGR is c. 13%.

Sustained RoE which can dip due to ineffective utilisation of cash

Though company has strong ROE performance, the increased cash on the BS is not

invested as the company is looking for acquisition target in ECD segment. This will see a

Table 5.1 : Estimating beta

dip in RoE as the leverage of the company is almost nil and the cost of equity is high. HIL

can improve RoE by equity buyback or increasing dividend payout ratio. But the model has

Co-variance 0.0078%

not assumed anything. The company has risen equity as & when required but it’s difficult

Variance of Sensex 0.0097% to see if the company will able to the same with debt as well. Currently it has low leverage

which it can use to reduce the cost of capital to increase its returns. It acquired Sylvania in

Beta 0.81 2008 when the leverage was low but wasn’t able to fully understand European markets.

Covariance has been calculated on 5 year daily returns Cash Generating Capacity is high

Due to high revenue growth, margin improvements and tighter working capital

Source: Bloomberg, Student Research management, the company is able to generate sufficient cash in the future to fund its

capex requirements as indicated by strong CFO/Capex ratios. This generation is despite

Chart 5.2 : DuPont Analysis the company paying constant dividend of INR 3 per share. This cash will be utilised in debt

repayment and maintain the dividend policy.

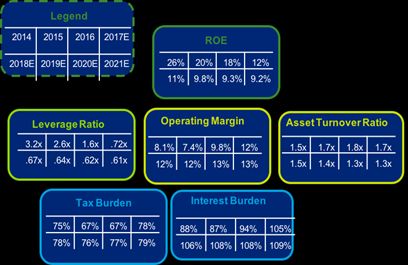

Valuation Ratios (x) 2015A 2016A 2017E 2018E 2019E 2020E 2021E

P/E 63.1x 47.8x 29.4x 25.9x 23.1x 19.9x 16.3x

P/Cash EPS 25.3x 45.8x 35.1x 25.4x 23.2x 20.9x 18.2x

P/BV 5.4x 5.9x 5.1x 4.2x 3.5x 3.0x 2.5x

EV/EBITDA 32.0x 28.4x 20.4x 18.3x 16.3x 14.4x 12.3x

EV/Sales 2.5x 2.7x 2.8x 2.5x 2.3x 2.0x 1.8x

Dividend Yield 1% 1% 1% 1% 1% 1% 1%

Earning Ratios (%) 2015A 2016A 2017E 2018E 2019E 2020E 2021E

EBITDA Margin 8.4% 10.5% 13.5% 13.8% 14.0% 14.3% 14.5%

Op. Profit Margin 6.8% 8.9% 12.0% 12.2% 12.6% 12.9% 13.3%

Net Profit Margin 4.5% 15.8% 9.9% 10.2% 10.4% 10.9% 11.5%

CFO/Capex 456.2% 248.2% 207.3% 368.5% 362.2% 350.9% 315.3%

ROE 21.2% 47.7% 24.4% 21.7% 19.6% 18.5% 18.4%

ROCE 22.4% 21.0% 23.2% 20.3% 18.5% 17.3% 16.7%

Source: Company Fillings, Student Research

ROA 7.6% 27.2% 18.5% 17.8% 16.7% 16.2% 16.6%

B/S Ratios 2015A 2016A 2017E 2018E 2019E 2020E 2021E

Current Ratio 1.3x 1.8x 2.5x 3.0x 3.5x 4.0x 4.6x

Table 5.2 : Target Share Price Estimation (INR) D/E 0.1x 0.0x 0.0x 0.0x 0.0x 0.0x 0.0x

Debtor Days 31.6 11.1 11.1 11.1 11.1 11.1 11.1

Method Weightage Price WxP Creditor Days 86.8 48.1 48.1 48.1 48.1 48.1 48.1

Inventory Days 60.9 52.1 52.1 52.1 52.1 52.1 52.1

DCF 60% 260.1 156.06 Working Capital Days 5.6 15.1 15.1 15.1 15.1 15.1 15.1

Asset Turnover 7.0x 7.0x 6.4x 6.4x 6.4x 6.4x 6.4x

Relative Valuation 40% 413.26 165.30

Per Share Data 2015A 2016A 2017E 2018E 2019E 2020E 2021E

Adj EPS 6.2 8.2 13.3 15.1 17.0 19.7 24.0

Target Price 321.26

EPS 6.2 19.7 13.3 15.1 17.0 19.7 24.0

CEPS 15.5 8.6 11.2 15.5 16.9 18.7 21.6

Source: Student Research

BVPS 72.1 66.5 77.2 92.4 110.8 131.9 157.7

DPS 3.0 3.0 3.0 3.0 3.0 3.0 3.0

Important disclosures appear at the back of this report10

Investment Risks

Risks Mitigating Factors Business Risk

Slowdown in Real Estate and Infrastructure Sector | BR1

Business and Strategy Risk With stagnancy being experienced by Real Estate developers, the Real Estate Sector

New Market Focus on Branding and Product is facing a rough patch. This might have a negative impact on the revenue of the

Entrants and Quality as consumers are moving Company, being demand for Switches, Cables and other products of the company,

cheaper towards purchases based on influenced by the growth of Real Estate and Infrastructure Sector.

substitutes could quality and Brand.

impact revenue Entry of New Market Players in Business Segments | BR2

With China being the second largest market for LED Lighting with around 25% of

Unable to tap into Introduction of new Brands to Global manufacturing capacity, the competition in the local markets might increase

New Markets of exclusively cater to the Regular and

Tier II cities having Economy Segment in the new resulting from imports from China. Also, the margins in the concerned business might

commendable markets, so as to capitalize without squeeze due to increased competition and availability of cheaper Chinese substitutes.

future potential cannibalizing sales of Premium Upcoming Market in Tier II and Tier III Cities | BR3

Brands in existing markets.

With the Company’s product portfolio priced premium amongst competitors, and with

Cannibalization of Transforming Production the premium perception amongst consumers, the Company might not be able to

sales resulting capacities, enabling them to service the growing market in Tier II and Tier III Cities with Reo and Reo Bliss Brands.

from technological produce the technologically

innovations upgraded products; meanwhile Regulatory Risk

venturing into new markets for Delayed implementation of GST | RR1

existing products

With the Goods and Service Tax Regime set to rise in India, a concrete date for

Technological Risk implementation of the new law is not yet clear. With the advent of the new Regime,

business is set to benefit from reduction in the compliances required as well as from

Import of key Undertake expansion for

components manufacture of components; in the

competitive tax rates, resulting from merging of the applicable Indirect Tax Laws. A

shorter run, mitigate exposure to delay for the Act to set in motion might squeeze the margins for a longer duration, as

price fluctuations by currency well as delay a much needed market stimulus.

forwards and price agreement

contracts. Technological Risk

Continuing Technological Constraints in LED Lighting | TR1

Disruptive Undertake expenses for developing With rapidly changing technology in the lighting business, there is a risk of

innovation in new products and upgrade existing

product lines by products with new features, so as technological disruption in the business. Apart from that, the LED Chips required are

competitors to satisfy the demand from the outsourced from other countries owing to IP constraints, poor infrastructure and

customers investment costs. Further, around half of the LEDs assembling are outsourced due to

Financial Risk volume and technology constraints.

Strategic Risk

Considerable Cash Investing cash balances in revenue

Balances at hand generating securities till a suitable Increased Market Exposure due to concentration in Indian Markets | SR1

for future expansion project is identified. A With the disinvestment from the foreign markets, the company has increased its

expansion special dividend can be considered exposure in Indian Markets. Although the disinvestment will lead to reduced

and raising funds as and when

opportunity is identified. consolidated losses from foreign subsidiaries, the over reliance on few markets might

lead into market saturation in the future.

Forex losses on Enter into Currency futures Expansion Plans might not be as effective | SR2

Future Divestment contracts to mitigate the foreign

of Sylvania currency risk arising due to inflows With two new plants under construction, the total production capacity is bound to

from future stake sale of Sylvania increase in the near future. Unfavourable market scenario might result in under-

Business utilization of total installed capacity, thus resulting reduced profitability due to higher

Operational Risk operational and maintenance costs w.r.t lower increase in contribution margin.

Financial Risk

Downtime caused Enter into insurance contracts and

by Fortuitous Performance based compensations Considerable Idle Cash in Hand realized from sale of Subsidiary | FR1

Events and plans, Plant Maintenance Contracts As on 31st March 2016, the Company held INR 14.7bn, of which INR 10.7bn resulted

Breakdown of to mitigate the potential losses from sale of 80% stake of Havells Sylvania Malta BV, a sub-subsidiary in Malta. The

Plants

cash reserves result in approx. INR 23.5 per share, which the management proposes

Risks arising from Formulate Gantt Chart and exercise to use for expansion plans in the foreseeable future. The quantum of unutilized cash

New Plants under control over work completed, and balances might result in lower profitability for the shareholders.

commission reformulate strategy for changes in

time line. Formulate strategy to

formulate market for increased

production. Implied Share Price Sensitivity to WACC and Terminal Growth Rate

Terminal Growth Rate

BR3 260.1 5.40% 5.70% 6.00% 6.30% 6.60%

Low Medium High

BR2 FR1 BR1

11.07% 294.01 307.09 321.72 338.19 356.87

Impact

SR2 RR1 11.69% 266.35 276.71 288.17 300.90 315.12

WACC 12.30% 244.02 252.43 261.63 271.76 282.95

TR1 SR1

12.92% 225.06 231.98 239.49 247.68 256.65

Low Medium High

Probability 13.53% 209.26 215.04 221.29 228.05 235.39

Source: Student Research

Important disclosures appear at the back of this report11

Appendix

Appendix 1A

Macroeconomic Outlook of India

• Government Spending: The Government of India, in tandem with its expansionary policies and Laws and on the back of a better

fiscal position, has taken steps towards stimulating growth in the Economy. The Government of India increased its Capital Expenditure to

INR 586bn for Q1FY16, at a YoY growth of 18%, with a CAGR 13.48% approx. from the Q1FY13 Capital Expenditure of INR 401bn.

Further, the Government has moved to make a higher allocation for its spending for Infrastructure development, which shall stimulate the

growth in the economy as a whole due to access better infrastructure.

• Inflation: India’s economic outlook with respect to inflation appears to be a big positive. The RBI Governors has successfully kept the

inflation rate in check with in the target range of 4% +/- 2% using its Monetary Policies, without hampering the growth potential of the

market. In the last 24 months, The average Urban and Rural Combined CPI is around 5.03%, with Urban CPI at 4.43% and Rural CPI at

5.54%. Moving around in the bracket of 3.5% to 6% in the time period, CPI has shown sharp movements with sustained momentum,

currently witnessing a downward spiral movement. With the recent 25 basis points rate cut in the repo rate, the Monetary Policy

Committee, headed by the incumbent RBI Governor, Dr. Urjit Patel has given a firm statement for the cause of economic growth,

keeping the inflation in check.

• Industry: The Industrial Growth story of India seems robust with more than Three-fourths of the months showing a positive growth in

the Index of Industrial Production (IIP) since April’14; and with an average increase of 1.7% in the IIP since April’15, the momentum is

only expected to continue in the future with a better monsoon than the last couple of years and positive government policies

• Savings & Investment: In terms of gross savings, there was 8.6% decline in household savings in 2015-16 which was more than

compensated by 17.6% increase in corporate savings resulting in constant ratio of 33%. Investment followed a similar pattern with a 15%

decline in household investments in 2014-15 marginally compensated by 5.1% increase in corporate investment resulting in 2.5%

decline in gross investment ratio

• Balance of Payments: Owing to increased FDI and decrease in oil prices, the BoP level has improved. There was a decline of 4.1%

in trade deficit levels in 2015-16 as compared to previous year. Healthy forex reserves restore the faith and certainty that India is well

prepared in advance for any future shocks most notably the chances of oil price surge

• Exchange Rate: The average exchange ratio was 66.25 in 2015, a 6.3% rise from 2014 level. This decrease in rupee value is due to

increase meltdown of global growth resulting in capital flight and less investments in country. It was further deteriorated by the rise in

demand for US dollar. But the damage has been contained due to recent RBI policies curtailing rupee depreciation

• Consumption: India has always been a consumption driven economy with its consumption trends matching to those of high income

countries. Post 2008 crisis, where the global consumption plummeted, India had a healthy consumption pattern. As per advance

estimates, provided by Economic Survey, maximum growth and contribution is given by private consumption with growth rate of 15.7% in

2015-16 and contribution of 60% to GDP

• Labour: The Indian Economic outlook looks positive in terms of labour force with a constant rising working-age population (15-65 years,

CAGR of 0.47% since 2001) and expenditure on education, ~14% of total Government Expenditure. A declining Employment to Working

Population Ratio coupled with increasing primary, secondary and tertiary education amongst the labour force has made available an

educated labour force, ready to exploit opportunities and driving growth in the future

Gross Savings and GCF (INR bn) Historical inflation trend (%)

34.6

34.3

33.8

33.4

33 33

31.6

30.8

2011-12 2012-13 2013-14 2014-15

Gross Savings Gross Capital Formation

Source: Economic Survey of India (2015-16) Source: Economic Survey of India (2015-16)12

Appendix

Appendix 1B

Switchgear Industry

• The electrical machinery industry in India is divided into three segments, namely (1) Generation machinery, (2)

Transmission machinery and (3) Distribution machinery

• Switchgear falls under the distribution machinery category and contributes about 16% of the revenue to the c. INR 1tn

industry

• From FY15 to FY22, the switch and control gear industry is set to grow at a CAGR of c. 20% and occupy nearly INR

550bn of the electrical machinery industry, outperforming the later by a huge margin

• The Indian switchgear industry manufactures the apparatus for the entire voltage range from 240kV to 800kV

• The exports market of the electrical machinery industry amounts to INR 340bn, driven mainly by the exports of cables and

boilers & parts. This provides an opportunity for the exports of cables by HIL while also opens us the possibility of

becoming an integral export

• The demand side growth drivers include capacity addition for power generation, increasing demand for backup equipment

and industrialization needs

• Government policies like de-licensing of power, reduction in tariffs ad customs and hike in duty on foreign products has

also lead to a favourable environment of growth

• Investments through increasing FDI inflows, entry of global players through joint ventures and ease of credit access has

meant that the dearth of capital is no longer a problem for the industry

India’s electrical equipment industry (INR bn) Share of major electrical equipment (2015)

966.4

710.2 723.9

646.8

490.2 499.8 506

352.6

2007 2008 2009 2010 2011 2012 2013 2015

Source: ibef Electrical Machinery industry report, October 2016 Source: ibef Electrical Machinery industry report, October 2016

Capacity addition in India in Five year plans (INR bn) Market size of switch & control gears in India (INR bn)

541.2

290.4

151.2

2015A 2017E 2022E

Source: Ministry of Power, Government of India Source: Department of heavy industry annual report13

Appendix

Appendix 1C

Cables and Wires Industry

• The wires and cable industry in India is divided into two segments, namely (1) Domestic Cables and (2) Industrial Cables,

with domestic cables forming 40% of the overall market and industrial cables forming 60% of the market and both the

segments have grown by CAGR of 6% over FY’11-15

• Wires and Cables falls under the distribution machinery category and contributes about 35.80% of the revenue to the c.

INR 1tn industry

• The industry is poised to grow at a CAGR of 7-8% till year 2019 with a thrust from infrastructure, telecommunication and

power sectors.

• The Indian wires and cables industry is highly fragmented and largely volume driven, the share of organised player is

increasing as consumers focus more quality and safety features which currently stands at 65% of the market size

• The exports market of the electrical machinery industry amounts to INR 340bn, driven mainly by the exports of cables and

boilers & parts. Cables constitutes 17% of the same

• The demand side growth drivers include capacity addition for power generation, pan India electrification.

• Wires and Cables market is highly price sensitive and operates o thin margins, and are largely linked to prices of copper

and aluminium

• Finolex is the market leader in the wires and cables industry and has pan-India presence, other players are Havells, RR

Kabels, KEI, V-Guard etc

• Dealer margins in the industry are in the range of 2-4%. Companies offers discounts on the MRP which is generally

passed on to the dealers.

Market shares in wires and cables industry in India (2015) Market size of wires and cables industry in India (INR bn)

Source: HDFC Sec Inst Research, Student Research

Source: HDFC Sec Inst Research, Student Research

Revenue of major wires and cables producers in India (INR bn)

Source: HDFC Sec Inst Research, Student Research14

Appendix

Appendix 1D

Lighting & Fixtures Industry

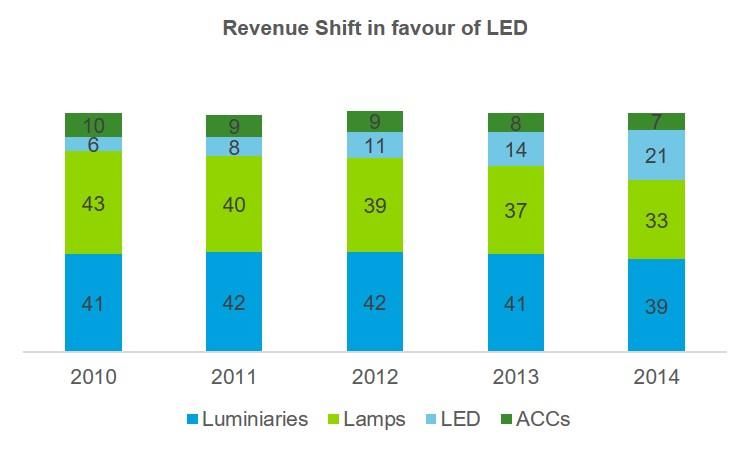

• Lighting sector contributes c.20% of the total energy consumption in India. The industry aims to reduce energy

consumption to 13% by 2020. This has led to an introduction of a series of energy efficient innovative lighting products.

Unorganised players forms 33% of the total market. The industry is classified into (i) Lamps (general lighting services

(GLS), fluorescent tube lights (FTL), compact fluorescent (CFL) and others) (ii) Luminaries (iii) Accessories, component

and gears (ACC) (iv) LED. From 2010-14, lighting industry grew at CAGR of c.17% whereas LED industry grew at 61%

CAGR proving that LED will drive the future growth of the industry

• The strong growth in lighting industry for the past 5 years has been due to movement from GLS lamps to CFL, and in the

future, the movement will be from CFL to LED (expected CAGR of 36% in 2015-20) supported by residential boom due to

rise in GDP and per capita income making LED products more affordable and government initiative to ban the sale of

incandescent lamps

• ELCOMA (Electric Light and Component Manufacturers Association of India) Vision 2020 aims to increase the domestic

manufacturing capability of LED lighting products to cater to increasing demand and reduce dependence on imports.

Currently India imports 100% of LED chips. As per ELCOMA, LED lighting will constitute ~60% (INR 216 bn) of the entire

lighting industry in India (INR 376 bn) by 2020. This is backed by government initiatives to replace all street lighting and

lights in public places to LED lights. The government launched the “100 cities LED based Domestic Efficient Lighting

Program (DELP) and National Street Lighting Program on 5th January, 2015

• Under the National Street Lighting Program, 35 million conventional street lights are to be replaced with energy efficient

LED street lights. The national DELP program also envisions replacement of 770 million incandescent bulbs with energy

efficient LED bulbs. Till date, EESL has successfully implemented the street lighting program and the DELP in 18 and 5

cities respectively

• LED bulbs cost between INR 160 and 300, CFLs INR 130 and 200 and Streetlights INR 85 per watt. The falling LED prices

and easy entry of consumer electrical equipment companies into this space has led to reduction in margins, but effect is

not severe due to cost of production showing similar decline

• Havells is focusing on high margin part of this segment. Due to this reason, the company has given the guidance of not

participating in government tenders until it can see the bulk orders providing suitable margins

Source: 18th Electric Power Survey, CEA

Source: ELCOMA Analysis

Source: HDFC Instl. Research Source: HDFC Instl. ResearchYou can also read