Investor Presentation - Citi Global Property CEO Conference March 2019 - Park Hotels & Resorts

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation

Citi Global Property CEO Conference

March 2019

Waldorf Astoria Orlando Hilton Chicago Hilton Hawaiian Village Waikiki Beach Resort

Mission

To be the preeminent lodging REIT,

focused on consistently delivering superior,

risk-adjusted returns for stockholders through

active asset management and a thoughtful external

growth strategy, while maintaining a strong

and flexible balance sheet

2|

Pillars of our Corporate Strategy

Aggressive Asset Management

⚫ Continually improve property level operating performance

⚫ Consistently implement revenue management initiatives to optimize market pricing /

segment mix

Hilton Chicago

Prudent Capital Allocation

⚫ Allocate capital effectively by leveraging scale, liquidity and M&A expertise to create value

throughout all phases of the lodging cycle

⚫ Employ an active capital recycling program—expanding our presence in target markets with

a focus on brand and operator diversification, while reducing exposure to slower growth

assets/markets

Hilton Waikoloa Village

⚫ Target value enhancement projects with strong unlevered ROI yields

Strong and Flexible Balance Sheet

⚫ Preserve a strong and flexible balance sheet, with a targeted leverage ratio of 3x to 5x

⚫ Maintain strong liquidity across lodging cycle and access to multiple types of financing

⚫ Aspire to achieve investment grade rating

Juniper Hotel Cupertino, Curio Collection

3|

Corporate Strategy: Delivering Results

Strategic Pillars 2018 Scorecard

✓ RevPAR: +2.9% → 65bps above peers

Operational ✓ Margins(1): +60bps → 60bps above peers

Excellence ✓ Grouping Up: +80bps to 32% for Pro forma

Comp Top 25 hotels(2)

Hilton New York Midtown

✓ Asset Sales: 13 non-core assets for $519M at a

blended 13x 2017 EBITDA multiple; International

Capital

exposure decreased to just 1% of EBITDA

Allocation

✓ Buyback: Bought back 14M shares at a significant

discount to NAV ($24.85/share) for $348M

✓ Leverage: Net leverage of just 3.7x Hilton Waikoloa Village

Strong Balance

✓ Liquidity: $1.2B of liquidity

Sheet

✓ Debt: 5.6 years maturity; 4.1% average debt cost

✓ Performance: Outperformed hotel REITs(3) by

1,380bps and S&P 500 by 390bps

Results

✓ Dividends: $2.74/share (~$555M+ paid out);

recently increased dividend by 4.6% Casa Marina, a Waldorf Astoria Resort

Note: Peers include all publicly-traded, full-service hotel REITs with a market cap over $1 billion

(1) See Appendix for our definitions and for reconciliations to comparable U.S. GAAP measures. Our definition of Hotel Adjusted EBITDA margin may not

be comparable to similarly titled measures of our peers. Based on most recently available / restated financial statements from their respective

quarterly earnings releases.

4 | (2) Pro forma to exclude Hilton Chicago O’Hare, which is no longer part of Park’s portfolio due to the expiration of its ground lease on 12/31/18

(3) Includes all publicly-traded hotel REITs with a market cap over $1 billion

Park’s Investment Thesis: Well Positioned in 2019

✓ Our Comp Top 25 RevPAR (90% of EBITDA(1)) in ‘18 was

$188—5% above peers

High Quality

Portfolio ✓ 2018 RevPAR growth of 2.9% → 65bps above peers

✓ 2.3% weighted average supply exposure through 2020 →

80bps below peers

✓ 2019E RevPAR growth of 2% to 4% → 120bps above peers

Signia Hilton Bonnet Creek

Sector ✓ 2019 Group pace for consolidated portfolio → 10%+

Leading

Fundamentals ✓ 2019 Group pace for HI, SF, Chicago and NYC → 14%+

✓ 2020 Group pace → 9%

Margins to

✓ Despite rising cost pressures, margins estimated to

Improve in ‘19 increase 30bps (midpoint) or 50bps+ above peer group

average

Waldorf Astoria Orlando Golf Club

✓ At 3.7x net leverage and $1.2B of liquidity, ample liquidity

Financial to execute on our strategic initiatives with a long-term

Flexibility targeted leverage ratio of 3x to 5x

✓ Park has developed a near-term track record of success:

Track Record

✓ Generated sector-leading total returns for share-

of Success holders since spin (+2,670bps vs all hotel REIT peers);

✓ While narrowing the valuation gap with peers

Parc 55 San Francisco - a Hilton Hotel

5 | Note: Peers include all publicly-traded, full-service hotel REITs with a market cap over $1 billion

(1) Represents 2018 Adjusted EBITDA

Park Team

Chairman, President

& CEO

Tom Baltimore

Executive Management

EVP, CFO & EVP, GC EVP, Asset

EVP, D&C EVP, HR EVP, CIO

Treasurer Management

Carl Mayfield Tom Morey Jill Olander Matt Sparks

Sean Dell’Orto Rob Tanenbaum

Senior Management

SVP, FP&A SVP, CAO SVP, Strategy SVP, Tax

Diem Larsen Darren Robb Ian Weissman Scott Winer

Park Management Board of Directors

➢ 25 years average experience among senior ➢ Best-in-class board including former CEOs and

leadership CFOs of Fortune 500 Companies

➢ Total of ~90 employees at Park Headquarters ➢ Significant REIT experience across industries

6|

2018 Accomplishments

Operating Results:

6.5% 2.9% 60bps 80bps to 32.0%

Comp Hotel Pro forma Comp Top

AFFO/Shr Comp

Adj EBITDA 25 Group Revenue

Growth RevPAR

Margin Mix(1)

Capital Allocation:

13 $519M $1.4B $348M

# of Hotels Asset Sale HNA 14M Shares

Sold(2) Proceeds(2) Secondary Bought Back at

Offering Discount to NAV

Shareholder Returns:

-0.5% 1,380bps 7.7% 9.3%

2018 PK’s Relative 2018 PK Annual Increase

Total Outperformance Dividend in PK Dividend

Return(3) vs. Peers (4) Yield (3)

Since early 2017, Park has returned nearly $1.9B of capital to shareholders(5)

(1) Pro forma to exclude Hilton Chicago O’Hare, which is no longer part of Park’s portfolio due to the expiration of its ground lease on 12/31/18

(2) In February 2019, Park sold the Pointe Hilton Squaw Peak Resort for $51M, bringing total assets sold to 14 for total proceeds of $570M

(3) As of 12/31/18

7| (4) As of 12/31/18; peers include all publicly-traded, full-service hotel REITs with a market cap over $1 billion

(5) Return of capital includes both dividends and stock repurchase

Park Continues to Outperform

Total Return Performance Since Spin: 1/4/17

40.0% 36.5%

35.0%

30.0% 28.4%

+2,670bps vs.

Total Returns

Hotel REIT Peers

25.0%

20.0%

15.0% 11.4% 11.1%

9.8%

10.0%

5.0%

0.0%

PK S&P 500 HST RMZ Hotel REITs(1)

Total Return Performance: YTD 2019

25.0%

20.7%

20.0% 18.4% 18.2%

+230bps vs. Hotel

Total Returns

15.0% 12.9%

11.8%

10.0% REIT Peers

5.0%

0.0%

PK Hotel REITs(1) HST RMZ S&P 500

Source: FactSet; data as of 2/26/19

8| (1) Peers include all publicly traded hotel REITs with a market cap over $1 billion

4Q18 Performance and 2019 Outlook

4Q18 Operating Results

3.6% 40bps 3.8% 23%

Comp Comp Hotel Group Increase in

RevPAR Adj EBITDA Revenues ‘Other Hotels

Margin Revenues’(1)

2019 Outlook

Metric Guidance

Comp RevPAR Growth: +2.0% to +4.0%

Comp EBITDA Margins: +0bps to +60bps

Adjusted EBITDA: $745M to $775M

Note: Guidance as of 2/27/19. Not being updated or reconfirmed via this presentation.

9 | (1) Ancillary hotel revenues for our comparable hotels

Company Highlights

Park Hotels & Resorts is a leading lodging real estate investment trust with a diverse portfolio of iconic and

market-leading hotels and resorts with significant underlying real estate value in top U.S. markets

2018

Leading Properties(1) Performance(2)

52 premium-branded hotels and iconic resorts with nearly 31,000 well-maintained rooms 82%

Total

85%+ of rooms in luxury and upper-upscale segments Occupancy

26 properties with 25k+ sq. ft. of meeting space and 9 properties with 125k+ sq. ft. of

meeting space $212

Total ADR

$174

Room RevPAR

$208

Avg. Room

RevPAR

DoubleTree Hotel Washington DC – Crystal City Waldorf Astoria Orlando

of Top 10

Assets(3)

Hilton Miami Airport Hilton Boston Logan Airport

(1) As of 2/27/19

(2) Total consolidated Hotel Occupancy, ADR and RevPAR; excludes unconsolidated joint ventures and non-comparable hotels, unless otherwise noted

10 | (3) Top 10 TTM RevPAR includes Hilton Waikoloa Village, which is non-comparable in 2018Size and Scale: Park Twice the Size of Most Lodging REITs(1)

Park is the second largest publicly traded Lodging REIT

$20.0

Full Service $17.7

$18.0

Mixed & Limited Service

$16.0

$14.0

Enterprise Value (B)

$12.0

$10.0

$9.1

$8.0 $7.5

$6.7

$6.0 $5.6

$5.2

$4.8

$3.9

$4.0 $3.4

$3.0

$2.3 $2.5 $2.5

$2.0 $1.6

$1.3

$0.0

BHR CLDT INN CHSP HT DRH XHR SHO AHT APLE RLJ RHP PEB PK HST

Source: Public company filings as of 12/31/18 and S&P Global. Market data as of 2/26/19

11 | (1) Assumption excludes HST from calculationDiversified Asset Types & Markets

High Barrier to Entry Urban Select Suburban and

and Convention Hotels Landmark Resorts Strategic Airport Hotels

Hilton Hawaiian DoubleTree Hotel

New York Hilton Hilton San Francisco Hilton Waikoloa Hilton Boston Logan

Village Waikiki Beach Washington DC –

Midtown Union Square Village Airport

Resort Crystal City

1,878 rooms 1,921 rooms 1,110 rooms (1) 599 rooms

2,860 rooms 627 Rooms

Waldorf Astoria Orlando/

Hilton New Orleans Casa Marina, a Hilton McLean Tysons

Hilton Chicago Hilton Orlando Hilton Miami Airport

Riverside Waldorf Astoria Resort Corner

1,544 rooms Bonnet Creek 508 rooms

1,622 rooms 311 rooms 458 rooms

1,511 rooms

Note: room count as of 12/31/18

(1) Includes approximately 470 rooms that became part of HGV as part of the spin-off and that we reserved exclusive rights to occupy and operate.

12 | At the end of December 2019, we are required to release these rooms back to HGV for its renovation and usePortfolio Diversification(1)

Location Type(2): Markets(2): Revenue Segmentation:

Suburban San Diego, 3% Int'l, 1% Other

Contract

5% 2%

Key West, 4% 5%

DC Metro, 4%

Airport Chicago, 4%

13% Group

31%

Honolulu, 20%

Resort

44% Waikoloa, 4%

New York, 7%

Orlando, 13%

Urban Transient

38% 62%

New Orleans,

7% San Francisco,

13%

⚫ Over 80% Urban / Resort ⚫ 45% exposure to Hawaii, San Francisco, DC and Key ⚫ Park’s “Grouping Up” strategy targets

exposure West – all with less than 2% projected supply 400 bps shift in Group demand

⚫ Continuing to reduce Airport / growth over next 2 years among Top 25 hotels

Suburban exposure via capital ⚫ 13% exposure to San Francisco, which is projected to ⚫ Removing Chicago O’Hare, Comp 2018

recycling initiatives Top 25 group mix was 32%, or 80bps

see a 78% increase in convention center room

nights in 2019, totaling over 1.2M room nights comparable improvement over 2017

⚫ Target markets include DC, Boston, Miami and SoCal ⚫ Transient strategy of 50/50 split

between Leisure and Corporate

⚫ International exposure at just 1%, down from 5% demand

prior to 2018 dispositions

(1) Calculated using results for the year ended 12/31/18 for the hotels we currently own or have an ownership interest in; pro forma to exclude YTD

2019 dispositions as well as removal of Hilton Chicago O’Hare, which is no longer part of Park’s portfolio due to the expiration of its ground lease

on 12/31/18

13 | (2) Calculated using total Hotel Adjusted EBITDA, which includes pro rata share of EBITDA from JVs as well as EBITDA from non-comparable hotels.

See Appendix for definitions and reconciliations of these measures to comparable U.S. GAAP measuresPark Portfolio: Well Insulated from Supply

~2.3% Supply Growth for Park Supply Growth Exposure for Lodging REITs(1)

2 Park Portfolio: Well

⚫ Against a backdrop of increased US supply

Insulated from Supply

Full-service REIT Supply Exposure –

Weighted Avg Supply

growth in Top 25 Markets, Park is well 4.7% STR Top 25 Markets

Growth '19 - '20

positioned relative to its peers

⚫ With outsized exposure to Oahu, San 3.2% Peer Avg. 3.1%

3.1% 3.0% 2.9%

Francisco and Orlando, Park anticipates just 2.8% 2.7% 2.6%

2.3% average annual supply growth through 2.3%

2020, or 80bps lower than its peer group

average

RHP CHSP DRH PEB HST XHR SHO BHR PK

Favorable Supply Picture for Park through 2020(1)

20.0% National Supply Growth Average: 1.9%

15.0%

10.0%

7.3% 7.3% 6.7%

5.6% 4.9%

5.0% 4.1% 3.9% 3.8% 3.7% 3.1% 2.7% 2.2% 2.2% 2.0% 1.9% 1.7% 1.6%

0.5%

0.0%

Supply Growth PK 2018 Adjusted EBITDA (%) National Supply Growth

Note: Charts presented above based on CBRE and Park estimates

(1) Supply Growth data from CBRE’s Mar - May 2019 Hotel Horizons forecasts for Upper Priced hotels; represents average of 2019 and 2020 supply

14 | forecasts. Park’s Adjusted EBITDA represents 2018 data and includes pro rata share of unconsolidated JVs; pro forma for Park’s current portfolioGrouping Up Strategy

2018 vs. Peak Group Mix Group Up to 35%

45% • Strategic goal is to drive group mix higher

by another 400bps to an optimal mix of ~35%

40%

40% for Park’s Top 25 hotels

38%

35% • Why Group Up:

35%

Group Mix

32% 1) Build a base in large, big box hotels to

30% effectively shrink the hotels for less rooms

30%

to sell each night

25%

2) Drive overall ADRs by yielding up on

23%

transient rates

20% 3) Benefit from highly profitable

Top 10 Portfolio Hotels 11-25 Top 25 Hotels catering/F&B from higher rated groups

Current Group Mix Peak Group Mix*

4) Drive margins higher

* Denotes prior annual peak group revenue mix from 2005 – 2018; Current Group Mix represents

pro forma comparable 2018 Hotels 11-25 and Top 25 portfolio (excludes Hilton Chicago O’Hare)

2019 Group Pace(1): Park’s Portfolio + Primary Park Markets

30.0%

23.4%

2019 Group Pace

25.0%

20.0% 17.2%

15.0% 10.4% 8.8% 7.9%

10.0% 6.4%

5.0%

3.0% 2.2%

0.0%

PK Comp. PK Comp. No SF Hawaii San Fran Chicago New York New Orleans Orlando

2019 Convention Calendar: 2% 78% 35% 33% 20% 5%

15 | (1) Group pace as of 12/31/18Closing the Margin Gap: 60bps in 2018; Est’d 50bps in 2019

Comp. Hotel Adj. EBITDA Margins(1): 2018 + 2019E Change

100 bps

110bps+ of Relative

Y/Y Change in Hotel Adj. EBITDA Margin

80 bps

30 bps

Improvement

60 bps

40 bps

60 bps

20 bps

-2 bps

bps

-19 bps

-20 bps

-40 bps

Park Peers(2)

2018A 2019E(1)

• In 2018, Park’s Comparable Hotel Adjusted EBITDA margin improved 60bps to 28.8% vs. a 2bps drop for our full-

service Hotel REIT peers. In 2019, we are forecasting another 30bps improvement in our margins (at the mid-point of

guidance) vs. a 19bps decline for the peer set average, at the midpoint of their guidance. In aggregate, that would

amount to ~110bps+ of relative improvement over a two-year period

• For every 50bps of margin improvement, EBITDA increases by ~$14 million, accounting for approximately $170

million of value creation(3)

(1) See Appendix for our definitions and for reconciliations to comparable U.S. GAAP measures. Our definition of Hotel Adjusted EBITDA margin may not be comparable to similarly titled measures of our peers.

Based on most recently available / restated financial statements from their respective quarterly earnings releases

16 | (2) Peers include HST, SHO, CHSP, DRH (did not provide ‘19 margin guidance), PEB, XHR and RHP (did not provide ‘19 margin guidance)

(3) Assumes a 12.0x valuation multipleIn Focus: Top 25 Portfolio (~90% of Adj. EBITDA)

Top 25 hotels(1) drive overall quality and performance of portfolio

2018 RevPAR(2) 2018 Adjusted EBITDA ($000)

$195 $190 $800,000

$190 $754,000

$750,000

$185

$180 $700,000 $667,000

$174

$175

$650,000

$170

$165 $600,000

$160

$550,000

$155

$150 $500,000

PK Pro forma PK Top 25 Pro forma PK Top 25 PK

2018 Group Mix(2) 2018 Hotel Adjusted EBITDA/key

32.5% $35,000

32.0% $31,600

32.0%

$30,000

31.5% $24,900

31.0% $25,000

30.5% 30.2% $20,000

30.0%

$15,000

29.5%

29.0% $10,000

PK Pro forma PK Top 25 PK Pro forma PK Top 25

(1) Top 25 hotels pro forma to exclude Hilton Chicago O’Hare, , which is no longer part of Park’s portfolio due to the expiration of its ground lease on

12/31/18

17 |

(2) Represents comparable 2018 operating statistics for Park’s portfolio as of 12/31/18Market Spotlights: 2019 Momentum

Over 50% of Park’s 2018 Adjusted EBITDA generated from 3 markets that are expected to solid performance in 2019

Hawaii San Francisco Florida

2018 Financials 2018 Financials 2018 Financials

RevPAR $221 RevPAR $235 RevPAR $173

Hotel Adjusted EBITDA $191.5M Hotel Adjusted EBITDA $99.3M Hotel Adjusted EBITDA $130.6M

% Adjusted EBITDA 25% % Adjusted EBITDA 13% % Adjusted EBITDA 17%

2019 Park Hawaii 2019 Park San Francisco 2019 Park Florida

23% 17% 3%

Group Pace Group Pace Group Pace

⚫ Nearly 4,000 rooms & 385,000SF of ⚫ Nearly 3,000 rooms & 160,000SF of ⚫ Nearly 3,300 rooms & 322,000SF of

meeting space across two hotels meeting space across two hotels meeting space across six hotels

⚫ Strong ramp-up in performance ⚫ Group pace projected to be ~17% in ⚫ Diversified exposure to the state

projected for 2019 in Waikoloa as the 2019, building off strong uptick in across three markets (Orlando, Key

island’s visitation normalizes group throughout 2018 (started the West and Miami)

following 2018’s disruption from the year at 7% group pace, finished at ⚫ Bonnet Creek complex’s meeting

volcano 16%) space expansion expected to begin

⚫ Southwest Airlines expected to ⚫ Moscone Center projected to see a in Q4, adding ~70,000SF of meeting

begin service to Oahu first half of 78% increase in convention room space by 2021. Rebrand of Hilton

2019; additional routes to other nights in 2019, totaling over 1.2M Bonnet to Signia Hilton should help to

Hawaiian islands to follow room nights drive additional group demand

⚫ Oahu supply growth of just 0.5% ⚫ San Francisco supply growth of 1.6% ⚫ Orlando supply growth of 2.2%

projected for next 2 years(1) projected for next 2 years (1) projected for next 2 years, while Key

West has little to no supply growth (1)

18 | (1) Supply Growth data from CBRE’s Mar - May 2019 Hotel Horizons forecasts for Upper Priced hotels; represents average of 2019 and 2020 supply

forecastsAmazon to Concentrate Around Park’s DoubleTree

DoubleTree Crystal City located directly across the street from 4.1M SF Amazon cluster

As part of its HQ2 expansion into Crystal City (Arlington, VA), DoubleTree Hotel Washington

Amazon purchased 4.1M SF of development rights from JBG, Name DC - Crystal City

directly adjacent to our Doubletree Crystal City hotel. Keys 627

Open Date Jun-73

Meeting Space (SF) 31,000

YTD Sep '18 RevPAR $124

RevPAR Index 104.1%

The Amazon Effect:

627-room DoubleTree • Seattle CBD Tract RevPAR recorded 7.6% CAGR

from 2010 – 2017, coinciding with development

of Amazon’s headquarters campus

• The Arlington, VA Tract RevPAR CAGR during

same time period was just 0.8%

$180

Annual RevPAR(1)

$160

$140

4.1M SF of Amazon $120

Development Rights $100

$80

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Seattle CBD Arlington

19 | (1) Tract data provided by STRROI Projects

How We Evaluate ROI Projects

• Asset management teams work with property management and Design & Construction to identify

opportunities

• Projects underwritten based on expected risk adjusted returns that range from a minimum of 15-20%

IRRs for larger projects and expected paybacks within 1-2 years for smaller projects

• Consultants may be engaged for larger projects ahead of approving the project

Near Term Projects Mid Term Projects Longer Term Projects

Completed/Committed Under Review In Planning/Concepting

HLT Santa Barbara Asset Repositions HLT Hawaiian Village

Converted and repositioned from Master planning (branding; retail;

DoubleTree (completed April 2018) HLT Bonnet Creek Repositioning amenities) including development of

Up-brand to Signia Hilton ½-acre Ala Moana parcel

WA/HLT Bonnet Creek

Addition of ~70k sq. ft. of meeting WA Reach Resort Conversion HLT New Orleans

space Renovate and reposition to a Curio Development and/or sale of 7-acre

‘Whale’ lot and other parcel and 2-acre

DT San Jose Conversion surface lot parking area

Renovate and reposition as a Hilton

Other smaller projects evaluated within the portfolio over time:

• Energy Initiatives: Co-generation plants; LED lighting

• Labor / Productivity: Union buyouts; labor management systems; digital key

• F&B: Installation of Grab ‘N Go market concepts

20 |Completed ROI Project: Hilton Santa Barbara Beachfront Resort

Conversion from a DoubleTree to a Hilton

⚫ 360-room beachfront resort on 24 acres in Santa Barbara, CA

⚫ Prime location in Santa Ynez wine country with in-house winery

⚫ Upbranding to a Hilton expected to attract higher-rated group business and

better yield transient business

⚫ $14M renovation cost(1) ($38,000/key) completed in April 2018

⚫ 4Q18 RevPAR increased +25.9%; projected 2019 RevPAR growth in mid- to

high teens

Scope

⚫ Guestrooms: case goods; soft goods

⚫ Guest bathrooms: conversion of 160 bathtubs to walk-in showers; case goods, soft

goods

⚫ Public space: lobby; meeting space (mainly soft goods); and repositioning of F&B to

include new Grab ‘N Go

Old lobby: Renovated lobby:

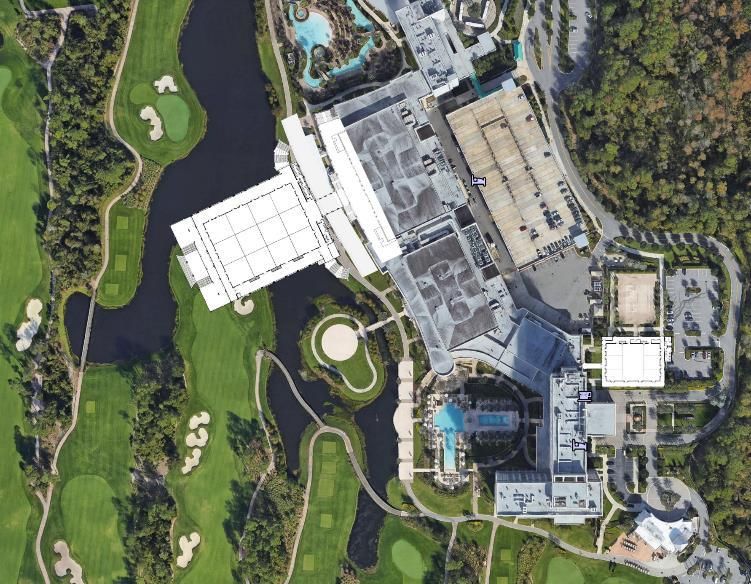

21 | (1) Park owns a 50% interest in the Hilton Santa Barbara Beachfront Resort; as such its pro-rata investment in the renovation was $7MFuture ROI Project: Bonnet Creek Meeting Space Addition

Bonnet Creek: Development Rights

⚫ Group meeting business is a key demand source for the 1,009-room

Hilton and 502-room WA Bonnet Creek, although both properties offer

less meeting space per guestroom than their key competitors

Opportunity: Additional Meeting Space

⚫ Current plans call for the construction of ~70,000 sq. ft. of meeting

space across 2 new meeting space platforms including:

⚫ ~35,000 sq. ft. ballroom adjacent to existing Hilton meeting

space complex

⚫ ~9,000 sq. ft. ballroom adjacent to the Waldorf Astoria

⚫ Approximately $70M investment in 2019-2021 expected to generate

approximately $13.5M of additional EBITDA/year once stabilized,

yielding a 5-yr unlevered IRR of 20%+

⚫ Upbrand the Hilton Bonnet Creek to newly-announced Signia Hilton

brand

Proposed Hilton Ballroom

and meeting space

Proposed Waldorf Ballroom

22 |Capital Recycling Efforts Improve Portfolio Quality

Phase I Asset Sales: 2018

• In 2018, Park sold 13 non-core hotels ($40M of EBITDA in

2017) for nearly $520M, or 13x 2017 EBITDA

• Improvement to portfolio quality: Pro-forma 2017(1)

RevPAR increased +$6 (to $169), while international

exposure decreased to 1.5% (from 5.5%)

Phase II Asset Sales: 2019

• Sold Pointe Hilton Squaw Peak Resort for $51M

• Currently marketing an additional 5 to 8 assets for sale

• Average RevPAR is 30% below portfolio average

• Projected capex savings of $90 - $100M

Portfolio Transformation with Capital Recycling Initiatives

Phase I Asset Phase II Asset

2017 2018 2019E(2)

Sales Sales (YTD)

Hotels 67 13 54 1 52

Rooms ~35,300 ~3,200 ~32,000 ~560 ~30,000

RevPAR(3) $163 $108 $174 $118 $179-183

EBITDA/key(4) $25,100 $14,100 $27,800 $10,100 —

(1) Pro-forma 2017 represents portfolio metrics without Phase I Assets

(2) 2019E represents portfolio as of 2/27/19 and guidance provided 2/27/19; 860-room Hilton Chicago O’Hare Airport ground lease expired 12/31/18

(3) 2017, 2018 and 2019E represent consolidated comparable RevPAR; 2019E based on guidance provided 2/27/19. RevPAR for Phase I Asset Sales

23 | represents 2017 RevPAR, while RevPAR for Phase II Asset Sales (YTD) represents 2018 RevPAR

(4) Represents EBITDA/key for the respective consolidated comparable portfolioStrong and Flexible Balance Sheet

Debt Capital Structure Overview(1) Debt Maturity Schedule(1)

$ % of Weighted Avg.

Debt

Amount Total Cost of Debt

CMBS (secured) $2,000 68% 4.2%

Term Loan A (Unsecured) (2) 750 25% 4.0%

Consolidated JV Debt 207 7% 4.2%

(secured)

Revolver(2) 0 0 4.0%

⚫ $236 million of unconsolidated JV debt (pro rata)

Total Debt $2,957 100% 4.1%

Liquidity Profile Fixed vs. Floating Net Debt to Adjusted EBITDA(3)

⚫ Ample liquidity with $410 million(4) of cash 8.0x 7.2x

available as of 12/31/18 7.0x

Net Debt to EBITDA

Floating 6.0x 5.1x

4.7x

⚫ 42 unencumbered hotels, or 63% of Adjusted 26% 5.0x

3.8x 3.7x

4.0x 3.5x

EBITDA(5) 2.9x

3.0x

1.8x

Fixed, 2.0x 1.2x

⚫ In addition to cash, Park has access to an 1.0x

74%

undrawn $1 billion revolving credit facility 0.0x

BHR RHP PEB CHSP PK XHR DRH HST SHO

Source: FactSet

(1) As of 12/31/18. Figures exclude pro rata share of Unconsolidated JVs, unamortized deferred financing costs, discounts and capital lease obligations

(2) Term Loan A (L + 1.45%) and Revolver (L + 1.50%) as of 12/31/18

(3) Calculations based upon the latest Consensus estimates. See Appendix for definitions and reconciliations of these measures to comparable U.S. GAAP measures

24 | (4) When factoring in the 4Q18 dividend payment of $1.00/share, our pro-forma cash balance would be approximately $210 million

(5) For the year ended 12/31/18; 40 hotels and 63% of EBITDA as of 2/26/19Attractive, Well Covered Dividend

Park’s Quarterly Dividends and Respective Yield(1) Peer REITs: Current Dividend Yield(2)

$0.80 8.0% 7.0%

6.5% 6.3%

$0.70 7.0%

6.0%

Annualized Dividend Yield

$0.60 6.0%

5.5%

Quarterly Dividend

$0.27 5.5% 5.4%

Dividend Yield

$0.50 5.0% 5.7% 5.1%

$0.12

5.0%

4.6% 4.7% 4.6%

$0.40 4.0% 4.5%

4.1% 4.1%

$0.30 3.0% 4.0%

$0.43 $0.43 $0.43 $0.43 $0.43 $0.43 $0.43 $0.43 $0.45 3.5%

$0.20 2.0%

3.0%

$0.10 1.0%

2.5%

$0.00 0.0% 2.0%

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19E PK XHR CHSP BHR SHO DRH PEB HST RHP

Source: FactSet Source: FactSet

Dividend and Payout Ratio Analysis

⚫ Park paid a fourth quarter 2018 cash dividend of $1.00/share on January 15th to stockholders of record as of December 31,

2018. Of this, $0.70/share represents the fourth quarter payment based on results of operations, and $0.30/share represents gains

from the sale of Park’s assets during 2018

⚫ On February 22nd, Park declared a quarterly cash dividend of $0.45/share to be paid on April 15th to stockholders of record as of

March 29th, an increase of 4.6% in the quarterly “regular way” dividend

Park has paid a total of $7.37/share in cash + stock dividends in its first two years, totaling $1.5B

(1) 4Q 2017 dividend includes a $0.12 per share ‘top-off’, which translated into an AFFO payout ratio of 67.5%. 4Q 2018 dividend includes a $0.27 per share ‘top-off’ amount and a $0.30 per share component

related to additional gains from 2018 asset sales, which translated into an AFFO payout ratio of 67.2%. Yield excludes both the $0.45 per share special dividend announced on 5/18/18 and the $0.30 per share

component included in the 4Q 2018 dividend

(2) Based on 2/26/19 closing prices; For PK, the 5.7% yield assumes a quarterly dividend run-rate of $0.45/share, or $1.80 on an annualized basis, while the 6.3% yield includes the 4Q 2019 incremental top-off

dividend of $0.65/share at the midpoint of our guidance range, or $1.99/share on an annualized basis

25 |Brand Strategy Maximizes Revenue and Profitability

Brands Matter: Park will focus on owning hotels and resorts in the luxury and upper upscale segments

Benefits of Partnering with Brands

Consistent quality through a branded product should

allow Park to achieve higher RevPAR and margins as a

result of:

Worldwide

Group Sales

⚫ Recognizable product compared to independent hotels

struggling to differentiate their offerings

⚫ Worldwide reservation systems

Strong

⚫ Loyalty programs help to drive recurring sales, while RevPAR

lowering new customer acquisition costs Loyalty

Premiums

Programs

⚫ Hilton (~85M members) and Marriott, including

Starwood (~120M members), have over 50%

of sales stemming from customers within

loyalty programs

⚫ Ability to achieve increased direct-to-consumer sales

minimizing OTA / wholesale commissions and

increasing revenue to Park Effective Worldwide

⚫ Significantly lower distribution costs for OTA business Brand Reservation

given negotiating power of brands Segmentation Systems

⚫ More effective competition against Airbnb, particularly

with respect to frequent travelers who appreciate the

reliability and security of branded hotels

26 |Appendix

Hilton Sao Paulo

27 |ESG: Corporate Responsibility

Public Disclosure of Materials FY 2017 Performance Highlights(1):

• Park’s “Responsibility” webpage launched Hotel Portfolio:

Jan ’19

• Extensive new disclosure on Environmental 4.46 13.59 100%

and Social metrics and initiatives Greenhouse Portfolio ISO

Gas Emission Energy 14001, 9001

• Approved corporate governance Intensity Intensity and 50001

enhancements, including proxy access and (kg/sf) (kw hrs/sf) Certified

majority voting standard in director elections

• Information made publicly available to

ensure more accurate representation of ~$445k 84% ~$35k

Park’s ESG initiatives to third party ratings Cost Savings Cost Savings

Waste

agencies like ISS, MSCI and from Energy Diversion from Water

Sustainalytics Efficiency Rate Efficiency

Projects Projects

New Publications

Corporate HQ:

• 2018 Annual Corporate

Responsibility Report

$270k 90% 400+

• Environmental Policy

Charitable Associate Volunteer

• Human Rights Policy Contributions(2) Satisfaction(2) hours(2)

• Vendor Code of Conduct

28 | (1) Represents Park’s portfolio as of 12/31/17, which consisted of 67 hotels with over 32,000 rooms

(2) FY 2018 data; represents first year to track these metricsCase Study: Bonnet Creek Complex

Asset Management partnered with property team to further drive awareness of the resort given the unique

attributes of the 1,009-room Hilton and 502-room Waldorf Astoria (WA)

• WA Orlando Focus on Luxury: Hired 2 luxury sales managers & instituted cross-selling with Casa Marina

Sales/ • Implemented lead-sharing platform with other hotels owned by Park in Orlando

Mktg • Opportunity to upbrand Hilton to Signia by Hilton, Hilton’s new upper-upscale, meetings-focused

brand – similar to a JW Marriott

Revenue • Created 250 “Fireworks View” room types with premium rates

Mgmt

• Created 12 additional keys – 8 at the Hilton and 4 at the Waldorf in early 2017: $400K incremental EBITDA

• Created 5 new Jr. Suites at the Hilton by splitting Parlor Rooms: $150K incremental EBITDA

Oper. • LED Lighting: estimated $600K savings per year and 40% IRR

Analysis • Laundry: estimated $150K of annual savings

• Re-bid parking contract: estimated incremental $700K annually

Waldorf Astoria Orlando Hilton Orlando Bonnet Creek

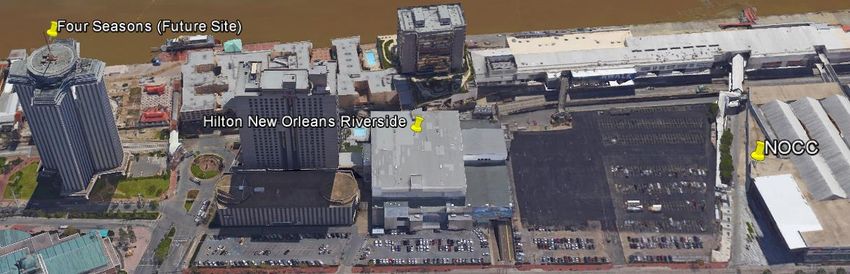

29 |Future ROI Projects: New Orleans

Hilton New Orleans Riverside: Development Rights/Land Sale

Hilton New Orleans Riverside

⚫ 1,622 room hotel with 130,000 sq. ft. of meeting space

⚫ Adjacent to the 3 million sq. ft. New Orleans Ernest N. Morial Convention Center (NOCC) – 6th largest in the US

Opportunity: Excess Land

⚫ Whale Lot: 7-acre parking lot separates Hilton Riverside and NOCC (square yellow box)

⚫ Sale of Plot: Potential future expansion of the NOCC providing doorstep access to our hotel

⚫ Development: Land would need to be entitled, but there is a wide range of potential development opportunities on the site

with the building height set by FAR. Total buildable square footage could be well in excess of 1 million sq. ft.

⚫ WTC surface parking (rectangular yellow box): aggregate ~2 acres of developable land

‘Whale’ Lot

WTC Garage

30 |Guidance

2019 Guidance and Assumptions

(unaudited, dollars in millions, except per share amounts)

2019 Outlook

as of February 27, 2019

Metric Low High

Comparable RevPAR Growth 2.0% 4.0%

Comparable RevPAR $ 179 $ 183

Net income $ 294 $ 323

Net income attributable to stockholders $ 286 $ 315

Diluted earnings per share $ 1.42 $ 1.56

Adjusted EBITDA $ 745 $ 775

Comparable Hotel Adjusted EBITDA margin change 0 bps 60 bps

Adjusted FFO per share - Diluted $ 2.91 $ 3.05

• Hilton Waikoloa Village will be included in Park’s comparable hotels as its room count is expected to remain consistent

throughout 2019 as compared to 2018;

• General and administrative expenses are projected to be $44 million, excluding $15 million of non-cash share-based

compensation expense;

• Fully diluted weighted average shares are expected to be 202.3 million;

• Includes $8 million of Adjusted EBITDA from the Caribe Hilton representing a partial year of operations, for which Park

expects to be covered by business interruption insurance resulting from the hotel being closed for a portion of 2019

following the damage caused by Hurricane Maria; and

• Excludes potential future acquisitions and dispositions, which could result in a material change to Park’s outlook.

Guidance 2019 Guidance and Assumptions (unaudited, dollars in millions, except per share amounts) 2019 Outlook as of February 27, 2019 Metric Low High Comparable RevPAR Growth 2.0% 4.0% Comparable RevPAR $ 179 $ 183 Net income $ 294 $ 323 Net income at tributable to stockholders $ 286 $ 315 Diluted earnings per share $ 1.42 $ 1.56 Adjusted EBITDA $ 745 $ 775 Comparable Hotel Adjusted EBITDA margin change 0 bps 60 bps Adjusted FFO per share - Diluted $ 2.91 $ 3.05 Hilton Waikoloa Village will be included in Park’s comparable hotels as its room count is expected to remain consistent

throughout 2019 as compared to 2018; General and administrative expenses are projected to be $44 million, excluding $15 million of non-cash share-based compensation expense; Fully diluted weighted average shares are expected to be 202.3 million; Includes $8 million of Adjusted EBITDA from the Caribe Hilton representing a partial year of operations, for which Park expects to be covered by business interruption insurance resulting from the hotel being closed for a portion of 2019 following the damage caused by Hurricane Maria; and Excludes potential future acquisitions and dispositions, which could result in a

material change to Park’s outlook. PARK HOTELS & RESORTS 20

31 |Guidance (continued)

EBITDA and Adjusted EBITDA

Year Ending

(unaudited, in millions) December 31, 2019

Low Case High Case

Net income $ 294 $ 323

Depreciation and amortization expense 278 278

Interest income (8) (8)

Interest expense 130 130

Income tax expense 13 14

Interest expense, income tax and depreciation and amortization included in equity

in earnings from investments in affiliates 23 23

EBITDA 730 760

Share-based compensation expense 15 15

Adjusted EBITDA $ 745 $ 775

NAREIT FFO and Adjusted FFO

Year Ending

(unaudited, in millions except per share data) December 31, 2019

Low Case High Case

Net income attributable to stockholders $ 286 $ 315

Depreciation and amortization expense 278 278

Depreciation and amortization expense attributable to

noncontrolling interests (4) (4)

Equity in earnings from investments in affiliates (18) (18)

Pro rata FFO of equity investments 31 31

NAREIT FFO attributable to stockholders 573 602

Share-based compensation expense

Guidance (continued) EBITDA and Adjusted EBITDA Year Ending (unaudited, in millions) December 31, 2019 Low Case High Case Net income $ 294 $ 323 Depreciation and amortization expense 278 278 Interest income (8) (8) Interest expense 130 130 Income tax expense 13 14 Interest expense, income tax and depreciation and amortization included in equity in earnings from investments in affiliates 23 23 EBITDA 727 757 Share-based compensation expense 15 15 Adjusted EBITDA $ 745 $ 775

15 15

Adjusted FFO attributable to stockholders $ 588 $ 617

(1)

Adjusted FFO per share - Diluted $ 2.91 $ 3.05

Weighted average diluted shares outstanding 202.3 202.3

(1) Per share amounts are calculated based on unrounded numbers.

32 |Non-GAAP Financial Measures

EBITDA and Adjusted EBITDA

Three Months Ended Year Ended

(unaudited, in millions) December 31, December 31,

2018 2017 2018 2017

Net income $ 55 $ 61 $ 477 $ 2,631

Depreciation and amortization expense 69 71 277 288

Interest income (2) — (6) (2)

Interest expense 33 31 127 124

Income tax expense (benefit) 10 (2) 23 (2,346)

Interest expense, income tax and depreciation and

amortization included in equity in earnings 6 6 26 24

EBITDA from investments in affiliates 171 167 924 719

Loss (gain) on sales of assets, net 2 (1) (96) (1)

Gain on sale of investments in affiliates(1) — — (107) —

(Gain) loss on foreign currency transactions (1) — 3 4

Transition expense — 4 3 9

Transaction expense 2 2 2 2

Severance expense — 1 2 1

Share-based compensation expense 4 4 16 14

Casualty loss (gain) and impairment loss, net — 24 (1) 26

(2)

Other items 6 (21) 8 (17)

Adjusted EBITDA $ 184 $ 180 $ 754 $ 757

(1) Included in other (loss) gain, net in the consolidated statement of operations.

(2) For 2017, includes $18 million of distributions received from investments in affiliates in excess of the investment balance that were included within equity in earnings from investments in

affiliates in the consolidated statement of operations.

33 |Non-GAAP Financial Measures (continued)

Comparable Hotel Adjusted EBITDA and Comparable Hotel Adjusted EBITDA Margin

Three Months Ended Year Ended

(unaudited, dollars in millions) December 31, December 31,

2018 2017 2018 2017

Adjusted EBITDA $ 184 $ 180 $ 754 $ 757

Less: Adjusted EBITDA from investments in affiliates 9 10 45 45

Less: All other(1) (13) (12) (52) (46)

Hotel Adjusted EBITDA 188 182 761 758

Less: Adjusted EBITDA from hotels disposed of — 9 1 33

Less: Adjusted EBITDA from non-comparable hotels 12 6 44 44

Comparable Hotel Adjusted EBITDA $ 176 $ 167 $ 716 $ 681

(1)

Includes other revenues and other expenses, non-income taxes on REIT leases included in other property-level expenses and corporate general and administrative expenses

in the consolidated statement of operations.

Three Months Ended Year Ended

December 31, December 31,

2018 2017 2018 2017

Total Revenues $ 686 $ 686 $ 2,737 $ 2,791

Less: Other revenue 19 17 72 64

Less: Revenues from hotels disposed of — 34 17 131

Less: Revenues from non-comparable hotels(1) 41 34 161 184

Comparable Hotel Revenues $ 626 $ 601 $ 2,487 $ 2,412

(1)

Includes revenues from Park's non-comparable hotels and rental revenues from office space and antenna rent leases located at our hotels.

Three Months Ended Year Ended

Decem ber 31, Decem ber 31,

2018 2017 Change (1) 2018 2017 Change (1)

Comparable Hotel Revenues $ 626 $ 601 4.2% $ 2,487 $ 2,412 3.1%

Comparable Hotel Adjusted EBITDA $ 176 $ 167 5.8% $ 716 $ 681 5.2%

Comparable Hotel Adjusted EBITDA margin 28.2% 27.8% 40 bps 28.8% 28.2% 60 bps

(1)

Percentages are calculated based on unrounded numbers.

34 |Non-GAAP Financial Measures (continued)

Historical Comparable Hotel Adjusted EBITDA – 2018

The financial information below is for the 44 comparable hotels owned as of December 31, 2018.

Three Months Ended Full Year Full Year

(unaudited, dollars in millions) March 31, June 30, September 30, December 31, December 31, December 31,

2018 2018 2018 2018 2018 2017

Net income $ 149 $ 218 $ 55 $ 55 $ 477 $ 2,631

Depreciation and amortization expense 70 69 69 69 277 288

Interest income (1) (1) (2) (2) (6) (2)

Interest expense 31 31 32 33 127 124

Income tax (benefit) expense — 13 — 10 23 (2,346)

Interest expense, income tax and depreciation and

amortization included in equity in earnings from

investments in affiliates 7 5 8 6 26 24

EBITDA 256 335 162 171 924 719

Gain on sales of assets, net (89) (7) (2) 2 (96) (1)

(1)

(Gain) loss on sale of investments in affiliates — (108) 1 — (107) —

(Gain) loss on foreign currency transactions (1) 4 1 (1) 3 4

Transition expense 2 — 1 — 3 9

Transaction expense — — — 2 2 2

Severance expense — 1 1 — 2 1

Share-based compensation expense 4 4 4 4 16 14

Casualty loss (gain) and impairment loss, net — — (1) — (1) 26

Other items 2 (1) 1 6 8 (17)

Adjusted EBITDA 174 228 168 184 754 757

Less: Adjusted EBITDA from investments in affiliates 12 14 10 9 45 45

Less: All other(2) (12) (14) (13) (13) (52) (46)

Hotel Adjusted EBITDA 174 228 171 188 761 758

Less: Adjusted EBITDA from hotels disposed of 1 — — — 1 33

Less: Adjusted EBITDA from non-comparable hotels 14 13 5 12 44 44

Comparable Hotel Adjusted EBITDA $ 159 $ 215 $ 166 $ 176 $ 716 $ 681

(1) Included in other (loss) gain, net in the consolidated statement of operations.

(2) Includes other revenues and other expenses, non-income taxes on REIT leases included in other property-level expenses and corporate general and administrative expenses.

35 |Non-GAAP Financial Measures (continued)

Historical Comparable Hotel Revenues – 2018

The financial information below is for the 44 comparable hotels owned as of December 31, 2018.

Three Months Ended Full Year Full Year

(unaudited, dollars in millions) March 31, June 30, September 30, December 31, December 31, December 31,

2018 2018 2018 2018 2018 2017

Total Revenues $ 668 $ 731 $ 652 $ 686 $ 2,737 $ 2,791

Less: Other revenue 17 17 19 19 72 64

Less: Revenues from hotels disposed of 17 — — — 17 131

Less: Revenues from non-comparable hotels(1) 44 41 35 41 161 184

Comparable Hotel Revenues $ 590 $ 673 $ 598 $ 626 $ 2,487 $ 2,412

(1) Includes revenues from Park's non-comparable hotels and rental revenues from office space and antenna rent leases located at our hotels.

36 |Non-GAAP Financial Measures (continued)

Historical Comparable Hotel Adjusted EBITDA – 2017

The financial information below is for the 44 comparable hotels owned as of December 31, 2018.

Three Months Ended Full Year Full Year

(unaudited, dollars in millions) March 31, June 30, September 30, December 31, December 31, December 31,

2017 2017 2017 2017 2017 2016

Net income $ 2,350 $ 115 $ 105 $ 61 $ 2,631 $ 139

Depreciation and amortization expense 70 73 74 71 288 300

Interest income — (1) (1) — (2) (2)

Interest expense 30 31 32 31 124 181

Income tax (benefit) expense (2,281) (19) (44) (2) (2,346) 82

Interest expense, income tax and depreciation and

amortization included in equity in earnings from

investments in affiliates 5 7 6 6 24 24

EBITDA 174 206 172 167 719 724

Gain on sales of assets, net — — — (1) (1) (1)

(Gain) loss on foreign currency transactions (1) 4 1 — 4 (3)

Transition expense 1 1 3 4 9 26

Transaction expense — — — 2 2 —

Severance expense — — — 1 1 —

Share-based compensation expense 3 4 3 4 14 —

Casualty loss (gain) and impairment loss, net — — 2 24 26 15

Impairment loss included in equity in earnings from

investments in affiliates — — — — — 17

Other items — 2 2 (21) (17) 36

Adjusted EBITDA 177 217 183 180 757 814

Less: Spin-off adjustments(1) — — — — — 49

Less: Adjusted EBITDA from investments in affiliates 9 15 11 10 45 44

Less: All other(2) (12) (11) (11) (12) (46) (34)

Hotel Adjusted EBITDA 180 213 183 182 758 755

Less: Adjusted EBITDA from hotels disposed of 4 9 11 9 33 1

Less: Adjusted EBITDA from non-comparable hotels 17 11 10 6 44 82

Comparable Hotel Adjusted EBITDA $ 159 $ 193 $ 162 $ 167 $ 681 $ 672

(1) Includes adjustments for incremental fees based on the terms of the post spin-off management agreements.

(2) Includes other revenues and other expenses, non-income taxes on REIT leases included in other property-level expenses and corporate general and administrative expenses in the

consolidated statement of operations.

37 |Non-GAAP Financial Measures (continued)

Historical Comparable Hotel Revenues – 2017

The financial information below is for the 44 comparable hotels owned as of December 31, 2018.

Three Months Ended Full Year Full Year

(unaudited, dollars in millions) March 31, June 30, September 30, December 31, December 31, December 31,

2017 2017 2017 2017 2017 2016

Total Revenues $ 684 $ 733 $ 688 $ 686 $ 2,791 $ 2,727

Less: Other revenue 13 16 18 17 64 23

Less: Revenues from hotels disposed of 26 35 36 34 131 —

Less: Revenues from non-comparable hotels(1) 57 48 45 34 184 334

Comparable Hotel Revenues $ 588 $ 634 $ 589 $ 601 $ 2,412 $ 2,370

(1) Includes revenues from Park's non-comparable hotels and rental revenues from office space and antenna rent leases located at our hotels.

38 |Non-GAAP Financial Measures (continued)

Net Debt and Net Debt to Pro-forma Adjusted EBITDA Ratio

(unaudited, in millions)

December 31, 2018 December 31, 2017

Debt $ 2,948 $ 2,961

Add: unamortized deferred financing costs 10 12

Long-term debt, including current maturities and excluding

unamortized deferred financing costs 2,958 2,973

Add: Park's share of unconsolidated affiliates debt,

excluding unamortized deferred financing costs 233 236

Less: cash and cash equivalents 410 364

Less: restricted cash 15 15

Net debt $ 2,766 $ 2,830

Pro-forma Adjusted EBITDA(1) $ 751 $ 717

Net debt to Pro-forma Adjusted EBITDA ratio 3.7x 3.9x

(1) See slide 18 for Pro-forma Adjusted EBITDA at December 31, 2018. Pro-forma Adjusted EBITDA excludes results from the 13 hotels disposed of in 2018.

39 |Non-GAAP Financial Measures (continued)

Pro-forma Adjusted EBITDA

Year Ended

(unaudited, in millions) December 31,

2018 2017

Net income $ 477 $ 2,631

Depreciation and amortization expense 277 288

Interest income (6) (2)

Interest expense 127 124

Income tax (benefit) expense 23 (2,346)

Interest expense, income tax and depreciation and amortization

included in equity in earnings from investments in affiliates 26 24

EBITDA 924 719

Gain on sales of assets, net (96) (1)

Gain on sale of investments in affiliates(1) (107) —

Loss on foreign currency transactions 3 4

Transition expense 3 9

Transaction expense 2 2

Severance expense 2 1

Share-based compensation expense 16 14

Casualty (gain) loss and impairment loss, net (1) 26

Other items 8 (17)

Adjusted EBITDA 754 757

Less: Adjusted EBITDA from hotels disposed of 1 33

Less: Adjusted EBITDA from investments in affiliates disposed of 2 7

Pro-forma Adjusted EBITDA $ 751 $ 717

(1) Included in other (loss) gain, net in the consolidated statement of operations.

40 |Definitions EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA Margin Earnings before interest expense, taxes and depreciation and amortization (“EBITDA”), presented herein, reflects net income excluding depreciation and amortization, interest income, interest expense, income taxes and interest expense, income tax and depreciation and amortization included in equity in earnings from investments in affiliates. Adjusted EBITDA, presented herein, is calculated as EBITDA, as previously defined, further adjusted to exclude: • Gains or losses on sales of assets for both consolidated and unconsolidated investments; • Gains or losses on foreign currency transactions; • Transition expense related to the Company’s establishment as an independent, publicly traded company; • Transaction costs associated with hotel acquisition or disposition costs expensed during the period; • Severance expense; • Share-based compensation expense; • Casualty and impairment losses; and • Other items that management believes are not representative of the Company’s current or future operating performance. Hotel Adjusted EBITDA measures hotel-level results before debt service, depreciation and corporate expenses of the Company’s consolidated hotels, including both comparable and non-comparable hotels but excluding hotels owned by unconsolidated affiliates, and is a key measure of the Company’s profitability. The Company presents Hotel Adjusted EBITDA to help the Company and its investors evaluate the ongoing operating performance of the Company’s consolidated hotels. Hotel Adjusted EBITDA margin is calculated as Hotel Adjusted EBITDA divided by total hotel revenue. EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA margin are not recognized terms under United States (“U.S.”) GAAP and should not be considered as alternatives to net income (loss) or other measures of financial performance or liquidity derived in accordance with U.S. GAAP. In addition, the Company’s definitions of EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA margin may not be comparable to similarly titled measures of other companies. The Company believes that EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA margin provide useful information to investors about the Company and its financial condition and results of operations for the following reasons: (i) EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA margin are among the measures used by the Company’s management team to make day-to-day operating decisions and to evaluate its operating performance between periods and between REITs by removing the effect of its capital structure (primarily interest expense) and asset base (primarily depreciation and amortization) from its operating results; and (ii) EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA margin are frequently used by securities analysts, investors and other interested parties as a common performance measure to compare results or estimate valuations across companies in the industry. EBITDA, Adjusted EBITDA, Hotel Adjusted EBITDA and Hotel Adjusted EBITDA margin have limitations as analytical tools and should not be considered either in isolation or as a substitute for net income (loss) or other methods of analyzing results as reported under U.S. GAAP. 41 |

Definitions (cont’d) Net Debt Net debt, presented herein, is a non-GAAP financial measure that the Company uses to evaluate its financial leverage. Net debt is calculated as (i) long-term debt, including current maturities and excluding unamortized deferred financing costs; and (ii) the Company’s share of investments in affiliate debt, excluding unamortized deferred financing costs; reduced by (a) cash and cash equivalents; and (b) restricted cash and cash equivalents. The Company believes Net debt provides useful information about its indebtedness to investors as it is frequently used by securities analysts, investors and other interested parties to compare the indebtedness of companies. Net debt should not be considered as a substitute to debt presented in accordance with U.S. GAAP. Net debt may not be comparable to a similarly titled measure of other companies. Net Debt to Pro-forma Adjusted EBITDA Ratio Net debt to Pro-forma Adjusted EBITDA ratio, presented herein, is a non-GAAP financial measure and is included as it is frequently used by securities analysts, investors and other interested parties to compare the financial condition of companies. Net debt to Pro-forma Adjusted EBITDA ratio should not be considered as an alternative to measures of financial condition derived in accordance with U.S. GAAP and it may not be comparable to a similarly titled measure of other companies. Comparable Hotels The Company presents certain data for its consolidated hotels on a comparable hotel basis as supplemental information for investors. The Company defines its comparable hotels as those hotels that: (i) were active and operating in the Company’s portfolio since January 1st of the previous year; and (ii) have not sustained substantial property damage, business interruption, undergone large-scale capital projects or for which comparable results are not available. The Company presents comparable hotel results to help the Company and its investors evaluate the ongoing operating performance of its comparable hotels. Of the 46 hotels that are consolidated as of December 31, 2018, 44 hotels have been classified as comparable hotels. Due to the conversion of a significant number of rooms at the Hilton Waikoloa Village to HGV timeshare units in 2017, and due to the effects of business interruption from Hurricane Maria at the Caribe Hilton in Puerto Rico and the continued effects from business interruption, the results from these properties were excluded from comparable hotels in 2018. The Company’s comparable hotels also exclude the 12 consolidated hotels that were sold in January and February 2018. Pro-forma Certain financial measures and other information have been adjusted to reflect the effects of hotels disposed of during the periods presented. When presenting such information, the amounts are identified as “Pro-forma.” 42 |

About Park and Safe Harbor Disclosure About Park Hotels & Resorts Inc. Park (NYSE: PK) is the second largest publicly traded lodging real estate company with a diverse portfolio of market-leading hotels and resorts with significant underlying real estate value. Park’s portfolio consists of 52 premium-branded hotels and resorts with over 30,000 rooms, primarily located in prime U.S. markets with high barriers to entry. Visit www.pkhotelsandresorts.com for more information. Forward-Looking Statements This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements include, but are not limited to, statements related to Park’s current expectations regarding the performance of its business, financial results, liquidity and capital resources, the effects of competition and the effects of future legislation or regulations, the expected completion of anticipated acquisitions and dispositions, the declaration and payment of future dividends and other non-historical statements. Forward-looking statements include all statements that are not historical facts and, in some cases, can be identified by the use of forward-looking terminology such as the words “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “projects,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words. Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ materially from those expressed in these forward-looking statements. You should not put undue reliance on any forward-looking statements in this presentation and Park urges investors to carefully review the disclosures Park makes concerning risk and uncertainties in Item 1A: “Risk Factors” in Park’s Annual Report on Form 10-K for the year ended December 31, 2018, as such factors may be updated from time to time in Park’s periodic filings with the SEC, which are accessible on the SEC’s website at www.sec.gov. Except as required by law, Park undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Supplemental Financial Information Park refers to certain non-generally accepted accounting principles (“GAAP”) financial measures in this presentation, including Funds from Operations (“FFO”) calculated in accordance with the guidelines of the National Association of Real Estate Investment Trusts (“NAREIT”), Adjusted FFO, FFO per share, Adjusted FFO per share, Earnings before interest expense, taxes and depreciation and amortization (“EBITDA”), Adjusted EBITDA, Hotel Adjusted EBITDA, Hotel Adjusted EBITDA margin, Net debt and Net debt to Pro-forma Adjusted EBITDA ratio. These non-GAAP financial measures should be considered along with, but not as alternatives to, net income (loss) as a measure of its operating performance. Please see the schedules included in this presentation including the “Definitions” section for additional information and reconciliations of such non-GAAP financial measures. 43 |

You can also read