JOURNAL Investment - Cantor Fitzgerald

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

February 2020

Investment

JOURNAL

FEATURED THIS MONTH:

Asset Allocation 2020

Core Equity Portfolio: The investment case for

our preferred names

Core Funds Range: Latest updates on our

range of investment funds, ETFs and Trusts

Ethical Investing: Green Effects providing

sustainable investment returns

StockWatch: Emerging Markets, Engie

R

Cantor Fitzgerald Ireland Ltd Cantor is regulated by the Central Bank of Ireland. Cantor Fitzgerald

Ireland Ltd is a member firm of the Irish Stock Exchange and the London Stock Exchange.

We are part of leading global financial services firm Cantor Fitzgerald

FOUNDED IN 1945 25 COUNTRIES

Cantor Fitzgerald is a firm Cantor and its affiliates employ

with significant real estate, over 10,000 people in 25

capital markets, research countries.

and investment expertise.

Cantor Fitzgerald Ireland

With a proud history of stockbroking and servicing our private clients and financial advisors in Ireland since 1995, we

provide a full suite of investment services, primarily in personalised share dealing, pensions and wealth management,

fund management, debt capital markets and corporate finance. Our clients include private individuals and corporate

entities, financial institutions, investment funds, credit unions and charities.

Cantor Fitzgerald Ireland is one of the largest wealth management and stockbroking firms in the country, formed through

the acquisition of Dolmen Stockbrokers in 2012, L&P Group in 2017 and Merrion Capital Group in 2018.

DUBLIN: 75 St. Stephen’s Green, Dublin 2. Tel : +353 1 633 3633.

CORK: 45 South Mall, Cork. Tel: +353 21 422 2122.

LIMERICK: Theatre Court, Lower Mallow Street, Limerick. Tel: +353 61 436 500.

Twitter : @cantorIreland LinkedIn : Cantor Fitzgerald Ireland

www.cantorfitzgerald.ie

2 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020

CONTENTS

Welcome 4

Asset Allocation 5

Asset Allocation 2020 6

Investment Opportunities 9

Core Portfolio 10

Navigating 2020's Investment Challenges 12

Core Investment Funds 16

Core ETFs & Trusts 18

Green Effects Fund 20

Stock Watch:

Emerging Markets 22

Engie 23

Latest News 25

Market Round Up 26

Performance Data 27

Investment Returns 28

Long Term Investment Returns 29

Bond Returns 30

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 3

WELCOME...

As we move into February the normal question is where did January go? Start of the year still? We are

8.5% on the way.

A strange month of percentages in markets; Against the deteriorating macro backdrop some

copper is down 10% year to date. Oil is off 15% companies have continued to outperform, a

for the year. US long-dated bonds yield less than point of focus for our MIM colleagues and high-

short dated bonds. The decline in risk assets lighted by Pramit; the strong are getting stronger.

Ronan Reid, globally gathered pace as the deterioration in Apple, Microsoft, Coca Cola, Amazon, McDonalds

CEO,

the growth outlook became more apparent. With and Intel were all out with strong beats and sub-

Cantor Fitzgerald

the exception of the S&P which is flat on the sequent strong share price performance. They

Ireland

year, global equity markets are down on the year account for over 90% of the small beat in EPS so

and have given up most if not all of their Q4 rally. far.

This rally had reflected in part that 2019 was a

Our MIM funds have performed well on both a

year of rate cuts; 126 globally and further balance

relative and absolute basis. A broad range of

sheet expansion at the Fed, European Central

factors are driving this performance including

Bank and Bank of Japan.

stock and sector allocation, tactical trading around

Reasons for January declines include a further key themes of renewables and global payment

shut down of all activity in China (oil demand providers, overweight longer dated Euro/USD

alone has fallen 20%, global airlines suspending bonds as well as diversification into asset classes

all flights until March), Chairmen Powell’s reference such as Gold and Alternative investments which

to “elevated asset values”, a Chicago PMI which have little correlation with the overall market di-

highlights the dramatic impact that Boeing issues rection currently. A challenging backdrop but

are having, as well as the realisation of how far our MIM colleagues are doing well in 2020 after

apart the EU and UK are on a trade deal. a positive 2019.

Closer to home two unforeseen events are likely As we head toward Spring, if you feel it is time

to weigh on sentiment for Irish assets. The strong for your annual financial health check, a member

showing of Sinn Fein in the polls would be ex- of our team would be delighted to talk to you.

pected to keep international investors on the

side-lines but the January government sale of

bonds and recent price actions show it does not Ronan Reid

appear the highest priority. Also the implication CEO, Cantor Fitzgerald Ireland

of the well-publicised write-down and subsequent

gating of a number of high profile Irish commercial

property funds is likely to weigh on some local

risk appetite.

4 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020

Asset

Allocation

February 2020

Asset Allocation 2020 6

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 5

ASSET ALLOCATION

ASSET ALLOCATION 2020

January 2020

Global equities ended the month marginally higher (by just 0.2%), having been as much as 2.5% higher

in the middle of the month. The New Year began with a continuation of the optimism seen in

December, but escalating tensions in the Middle East following the US targeting of a top Iranian official

saw equity markets pull back, bond yields move lower and gold move materially higher.

Pearse MacManus, The geopolitical tensions however subsided almost as quickly as they came, the US/China trade deal

Chief Investment Officer, was finally signed and Britain passed the withdrawal agreement to leave the EU, all of which helped

Merrion Investment equity markets higher by mid-month.

Managers

Economic data to start the month also called into question the narrative that a rapid recovery was

forthcoming, the US ISM Manufacturing drifting lower from 48.1 to 47.2, along with confirmation of

the weakness in the European manufacturing PMIs.

Although overall markets were quite strong in the first part of the month, the mix within them was

extremely defensive with mega-cap tech, staples and utilities all out performing the broader index.

This pattern has been evident for some time and continues despite financial market commentators

continuously pointing to supposed economic recovery on the back of great trade progress. If this

were the case, the cyclical sectors of the market should not be lagging. We feel this price action is

further evidence that the inadvertent response to the Federal Reserve’s decision to expand their

balance sheet has driven this rally. We will be watching this trend closely over the next few weeks to

see if this source of liquidity for the market has peaked.

The second part of the month saw weakness in global equity markets, broadly ascribed to the growing

coronavirus scare in China. In particular, the market is concerned about the draconian lock down the

authorities have put in place at the most economically sensitive time of year, Chinese New Year.

Regardless of how the virus develops, this clampdown on activity will naturally have a severe economic

impact, damaging the economic recovery narrative.

Global bond yields, copper, oil and iron ore have dropped precipitously on events in China, indicating

the growing concerns for global growth. This further delays any evidence of a recovery and could

also make it difficult for China to meet its targets in its trade deal with the US. Although we do think

this virus is a trigger for a pull-back in what are over-owned, over-valued and over stretched markets

we feel it is not the only catalyst. Other events over the latter part of the month are also worth bearing

in mind and have the potential to be much longer lasting. In particular, it is no coincidence that the

weakness in the markets coincided with the direction of the Federal Reserve’s balance sheet, which

saw a small reduction over the second part of the month. Discourse amongst Federal Reserve board

members and the wider market has increased over the exact impact of their recent actions. Numerous

market commentators are now pointing to the fact, which we have been highlighting for a while, the

Fed has inadvertently over stimulated markets beyond its intention.

US politics has also taken an unexpected turn. Bernie Sanders, the most left wing of the mainstream

candidates has become the leading democratic candidate ahead of the first caucus in Iowa. Although

a Sanders presidency is still a far-off prospect, it has become much more likely than people would

have thought even a month ago.

Outlook

An acceleration in growth was priced into equity markets in the first half of 2019, with economic

acceleration expected first in H2 2019. When this acceleration didn’t materialise, it was pushed out to

Q1 2020. It appears to us that these growth acceleration hopes are likely to be pushed out again due

to the corona-virus.

6 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020

With that consensus expectation for a rapid and sustained improvement in economic growth comes

the consensus outlook for a rapid rebound in earnings. Earnings growth of approximately 10% is

expected for 2020, and looks too optimistic. In the current earnings season, ex some market-exposed

financials and technology, results for industrials and cyclicals have been mixed at best with outlooks

that can be described as hopeful with second-half-weighted recoveries. In absolute terms, earnings

have declined over the last year, leaving the entire gain in equities since end 2018 down to multiple

expansion.

As noted above, one of the key drivers in our view of the most recent move higher in equities was the

provision of liquidity by the Federal Reserve. Whilst the Federal Reserve is likely to keep its balance

sheet large, reliance on repo is likely to fade, the balance sheet will not expand continuously, yet equity

markets appear to have priced an ever-expanding balance sheet.

Ultimately, we are in a low growth, low / zero rate, high risk but highly liquid environment, which means

portfolios should be focused on factors such as high quality, sustainable structural growth, positive

earnings momentum, strong and growing dividends, regulatory tailwinds not headwinds, and insulation

from geopolitical risks. These are the factors which will continue to add value to portfolios over time.

Positioning

We remain close to the lower end of our asset allocation ranges, as concerns about economic growth,

elevated valuations and technically stretched markets encourage a defensive posture.

Within our equity holdings, we sold the residual holdings we had in the oil sector, moving from

underweight to zero. Regulatory headwinds continue to increase for carbon emitters and even despite

the supply shortages from Libya crude is unable to rally. Given how stretched stocks and sectors we

like have become we also reduced our holdings in technology space (back more towards neutral),

adding to some of our holdings in global stock exchanges and to renewable energy holdings in Europe

as the regularity tailwind for this sector continues to grow with the latest iteration of the European’s

Green ambitions.

WARNING: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 7

ASSET ALLOCATION

ASSET ALLOCATION 2020 CONTINUED

Merrion Investment Managers Core Funds

Name Risk Rating (1 - 7) Sedol Currency TER %

Merrion Multi-Asset 30 Fund 4 !"#$%&' EUR 0.68%

Merrion Multi-Asset 50 Fund 4 !"#$%%( EUR 0.68%

Merrion Multi-Asset 70 Fund 5 !"#$%)* EUR 0.68%

Merrion Investment Managers Multi-Asset Fund Performance

Name 1 Month % 3 Month % YTD % 1 Year % *3 Year % *5 Year %

Merrion Multi Asset 30 1.9 1.9 1.9 8.8 4.0 3.2

Merrion Multi Asset 50 2.1 3.2 2.1 12.2 4.6 4.3

Merrion Multi Asset 70 2.3 4.6 2.3 16.0 5.6 5.1

*Annualised Gross Returns

Source: MIM 31/01/2020.

The Merrion Multi-Asset (MMA) funds were launched in July 2015. The information includes simulated

performance for the MMA funds prior to that date, based on the asset allocation and returns of the

Merrion Managed Fund, reweighted for the MMA simulated performance.

WARNING: These figures are estimates only. They are not a reliable guide to future performance.

WARNING: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

8 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Investment

Opportunities

February 2020

Core Portfolio 10

Navigating 2020's Investment Challenges 12

Core Investment Funds 16

Core ETFs & Trusts 18

Green Effects Fund 20

Stock Watch:

Emerging Markets 22

Engie 23

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 9DISCRETIONARY STRATEGIES

CORE PORTFOLIO 2020

February 2020

The Cantor Core Portfolio registered a decline of -1.2% during January compared to a decline of -0.2%

for the underlying portfolio benchmark.

During the period there was a continued strong performance by the technology sector which was

reflected in strong gains from our Core Portfolio technology holdings specifically, Alphabet (+8.4%)

and Microsoft (+9.4%). There were also positive performances from French utility group Engie (+8.1%),

David Beaton, US casual dining group McDonalds (+9.7%) after solid fourth-quarter results and French infrastructure

Chief Investment group Vinci (+1.2%).

Officer

Elsewhere in the portfolio there was a positive performance by food group Glanbia (+2.6%) following

weakness during the final quarter of 2019 while reflecting the increased level of market volatility towards

the month-end, the holding in gold producer Newmont Corporation (+5.1%) registered a positive

performance.

These positive performances were however countered by weakness in a number of holdings,

specifically travel & leisure group Carnival (-13.2%) which was negatively impacted by uncertainty over

the coronavirus outbreak.

Related to the uncertainty surrounding the coronavirus was weakness in oil groups Total (-9.1%), Royal

Dutch Shell (-10%), Smurfit Kappa Group (-8.7%) and Fedex (-3.1%) as concerns increased about the

overall impact on global growth of the virus.

Finally, there was weakness in telecoms group BT Group (-15.7%) following a trading update, and Dalata

Hotel Group (-11.4%) as a result of a refocus on Brexit risks ahead of the UK’s departure from the EU at

the end of January.

Following a review of some of the results from our Core Portfolio constituents, we made a number of

changes at the very end of the month.

Within the energy holdings we removed the 3% holding in French oil group Total and reduced the

exposure in Royal Dutch Shell from 5% to 3%. These reductions see us move underweight the energy

sector due to a disappointing results season for the sector, the continued weakness in the underlying

price of crude oil on global growth concerns and the increasingly negative focus on the overall oil

sector as a result of environmental concerns.

Given the increased level of market volatility we increase our exposure to gold through the addition of

3% weighting to a new holding to the portfolio, the Invesco Physical Secured Gold ETF. This ETF is

almost 100% correlated to the underlying gold price and augments our existing exposure to the

commodity though our holding in Newmont Corporation.

The final change to the portfolio sees an increase in exposure to BT Group from 3% to 5%. While the

share price performance to its Q3 results was negative, we see the company's unchanged EBITDA

guidance as positive. Our intention at the outset was to add to BT Group on weakness, assuming that

over the medium term highly rated CEO Philip Jansen (ex Worldpay) will use his private equity

background to turn momentum around and create shareholder value. He is now 12 months into his

role.

10 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Core Portfolio at the 31st January 2020

Price Total Return Fwd P/E Div Yield

Stocks Weightings

31/1/2020 Year to Date FY1 (x) FY1

Alphabet Inc 1432.78 8.4% 22.2x 0.0% 2%

Verizon Communications Inc 59.44 -0.9% 11.7x 4.2% 5%

BT Group* 160.92 -15.7% 7.0x 9.4% 5%

Dalata Hotel Group Plc 4.565 -11.4% 11.6x 2.3% 2%

Amazon.Com Inc 2008.72 10.1% 50.0x 0.0% 4%

McDonald'S Corp 213.97 9.7% 25.2x 2.4% 3%

Carnival 43.53 -13.2% 9.4x 4.7% 3%

Glanbia Plc 10.53 2.6% 11.8x 2.4% 4%

Danone 72.4 -2.0% 19.0x 2.8% 3%

Royal Dutch Shell Plc* 2000 -10.0% 10.2x 7.3% 3%

Allianz Se 215.85 -1.2% 11.7x 4.3% 4%

ING Groep Nv 9.825 -8.1% 7.7x 7.0% 4%

Sanofi 86.95 -3.0% 14.8x 3.6% 3%

Pfizer Inc 37.24 -2.7% 13.4x 4.0% 5%

Vinci Sa 100.2 1.2% 17.2x 2.9% 4%

Siemens Gamesa Renewable Energy 14.405 -7.9% 29.3x 0.5% 3%

DCC Plc 6132 -5.5% 17.4x 2.3% 4%

Fedex Corp 144.64 -3.1% 13.3x 1.8% 3%

SAP Se 117.82 -2.1% 21.9x 1.4% 4%

Paypal Holdings Inc 113.89 6.7% 33.8x 0.0% 4%

Microsoft Corp 170.23 9.4% 30.8x 1.1% 3%

Smurfit Kappa Group Plc 31.28 -8.7% 11.3x 3.3% 3%

Newmont Corp 45.06 5.1% 35.6x 1.8% 3%

Invesco Physical Gold ETC 154 5.6% N/a N/a 3%

Kennedy Wilson Holdings Inc 21.56 -2.0% 11.0x 3.9% 4%

Engie 15.56 8.1% 15.2x 5.0% 5%

Greencoat Renewables Plc 1.215 2.5% 17.4x 5.1% 4%

JPMorgan Emerging Markets Trust 1002.00 -5.1% 18.3x 1.4% 3%

Current Price as at 31/1/2020. Source: Bloomberg. *SIP = Since Inclusion in Portfolio

Cantor Core Portfolio Return -1.2%

Benchmark Return -0.2%

Relative outperformance -1.0%

WARNING: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 11DISCRETIONARY STRATEGIES

NAVIGATING 2020’S

INVESTMENT CHALLENGES

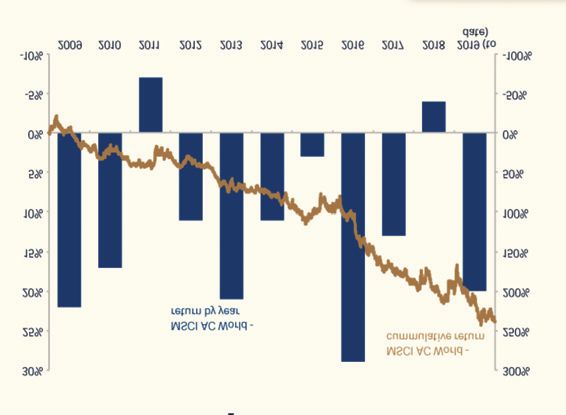

It has been an excellent decade for equity investors, as you can see from the chart below:

Pramit Ghose,

Global Strategist

Source: Refinitiv Datastream as at 29/11/2019.

For any investor who rode out the awful financial crash of 2007-2009 and/or invested in the early part

of the 2010s, they have made substantial gains. In terms of decades, the 2010s was pretty good for

equities, not the best one, but certainly a very strong one.

For many investors who have made these large capital gains, their priority in 2020 is to protect them

while still trying to make money (particularly as € deposit rates are likely to remain at zero or negative

for the next year or two, while yields of high quality European bonds are still negative). There are plenty

of concerns to navigate in 2020. Already we’re seeing Middle East tensions rise, Brexit is moving to the

next, possibly more difficult, phase, and we have the US presidential election, and the more difficult

Phase 2 of the US/China trade talks.

Despite the strong equity markets in recent years, we believe the medium-term outlook for equities

remains reasonably favourable, because of:

- low deposit rates/bond yields forcing investors to look at income yielding assets such as equities

- huge selling of equities by investors in recent years (i.e. many of the bears/sellers have sold)

- benign global growth background

Warning: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

12 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020A strong decade for the S&P

Source: Refinitiv FT Calculations

In particular we believe our Global Equity Income Fund offers investors a common-sense and tried-and-

tested conservative and lower risk way to invest in equities for the 2020s, particularly now after the

strong gains of recent years and when upside gains are likely to be restricted.

Firstly we have been running this strategy successfully since 2000.

Secondly there is an attractive dividend yield of 3.1%.

Thirdly, we believe we can grow the dividend flows by 6% to 8% a year. Why? Because the companies

we select have to pass a number of stringent financial tests to ensure their financial strength, cashflow

strength, and financial capability and management commitment to growing these dividends, no matter

what the financial environment. If we can achieve this dividend growth for the 2020s, then by 2030,

even if there are no capital gains over the decade, the return (gross) would be 44%, and the running

yield on your 2020 initial investment would have climbed to 6%.

Fourthly, which is a similar point to 3 above, we look for boring, “sleep easy at night”, reliable companies

at reasonable valuations with the financial characteristics listed in 3 above….a collection of “tortoises”

that gently but consistently march forward; companies such as Diageo, Unilever, Johnson & Johnson,

Nestlé and Mondelez.

Today, looking forward, that means we have to avoid some of the most fashionable and best momentum

companies, whose shares have performed superbly well recently and are today’s “market darlings” but

whose valuations have reached (and in some cases exceeded) extremely high valuations (and have very

low or zero dividend yields). For example, two shares we used to hold in the Global Equity Income

portfolios, Apple and Microsoft, have been performing very well, even into 2020, but their valuations

have sky-rocketed and their dividend yields have collapsed to about 1%. That doesn’t mean their shares

won’t still do well, but they don’t meet our conservative criteria any more, a huge amount of future

growth is now baked into their valuations, and in our view they are unlikely to repeat the huge share

price appreciation of recent years.

Warning: These figures are an estimate only, they are not a reliable guide to future performance.

Past performance is not a reliable guide to future performance.

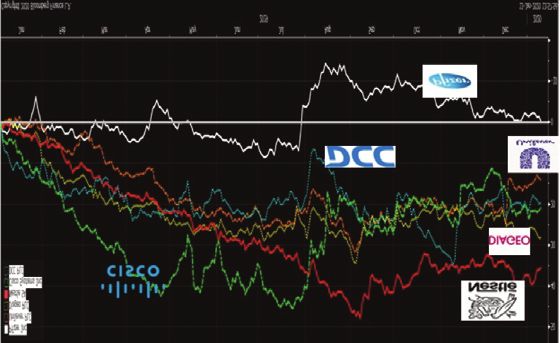

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 13We still of course want to invest in longer-term growth areas in companies that meet our criteria. In

Technology we invest in Texas Instruments (high end chips for the increasingly connected world),

Cisco (5G, cybersecurity), Intel (the cloud and the ever-voracious appetite for data centres), and

Accenture (Artificial Intelligence, increasingly digital world). In Healthcare, Danish pharmaceutical

Novo Nordisk is the leading innovator in diabetes and obesity treatments. As we hopefully move closer

to a reasonable US/China trade deal, the Chinese economy should show better growth, which would

help our Asia-exposed holdings - Louis Vuitton (luxury goods), Rio Tinto (mining), Prudential (pensions

and investments), and United Technologies (new buildings via its Carrier [heating and air conditioning]

and Otis [elevators and escalators] businesses).

Interestingly, despite the market strength in 2019 and into early 2020, we can still find a number of

quality companies whose recent updates have slightly disappointed the markets, but where we believe

the longer-term investment case remains strong. These companies have seen their share prices lag in

recent times, offering attractive opportunities to invest/top up.

Source: Bloomberg

But it’s the combination of experience, common sense, diversification, dividend yield and dividend

growth, that makes us believe the Global Equity Income Fund is an excellent investment vehicle to

navigate 2020 (and beyond).

Warning: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

14 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020R

6% INCOME GENERATING INVESTMENT

BLACKWATER RETAIL PARK

Opportunity to invest in Blackwater Retail Park, anchored by Woodie's, a Grafton Group company

KEY FEATURES

• Income yield of 6% per annum

• Secured on a real estate asset with no bank debt

• Long term income profile, underpinned by Grafton Group

• Potential to deliver capital upside from an asset management strategy

• Investment held by a tax efficient, regulated investment fund

• Expected investment term: 5 years

• Minimum investment: €100,000

• Fund is open to qualifying investors only

Warning: The income you get from this investment may go down as well as up, and will fluctuate dependent

on rental income levels and costs.

Warning: This is a high risk investment. The value of your investment may go down as well as up.

You may get back less than you invest.

Warning: If you invest in this product it is anticipated that you will not have any access to your money for

at least a five year period.

For further information or to arrange a meeting, contact:

DUBLIN 01 633 3633 | CORK 021 422 2122 | LIMERICK 061 436 500

www.cantorfitzgerald.ie

Cantor Fitzgerald Ireland Ltd is regulated by the Central Bank of Ireland. Cantor Fitzgerald Ireland Ltd is a member firm of the Irish Stock Exchange and the London Stock Exchange.INVESTMENT OPPORTUNITIES

INVESTMENT FUNDS

Our Core Funds range is a selection of funds that our investment committee feels could compliment

portfolios and enhance diversification. The Core Funds range offers investment options across

multiple asset classes and markets. Funds selected have undergone a comprehensive screening

process by our investment committee and are reviewed regularly.

Niall Sexton,

Core Investment Funds

Portfolio Equity Funds

Construction SEDOL Name

Morningstar

Rating!

Risk Rating (1 - 7) Currency TER % Yield %

Analyst Global Equity Income

B5TRT09 Veritas Global Equity Income

5 EUR 1.13 3.41

Global Equity Income

Merrion Global Equity Income - 5 EUR 0.60 0.00

Global Equity Growth

Fundsmith Global Equity Feeder

5 EUR 1.05 0.55

Global Equity - Ethical Investing

Green Effects

5 EUR 1.28 0.00

European Equity

BFNQYV8 Threadneedle European Select

5 EUR 0.83 0.00

B9MB3P9

UK Equity

B3K76Q9 J O Hambro UK Opportunities

5 GBP 0.82 3.20

US Equity

BYR8HR0 Merian North American Equity

6 EUR 0.89 0.00

Bond Funds

SEDOL Name Risk Rating (1 - 7) Currency TER % Yield %

Corporate Bond

B3D1YW0 PIMCO GIS Global Investment Grade Credit

3 EUR 0.49 3.26

Government Bond

0393238 BNY Mellon Global Bond

4 EUR 0.65 0.00

High Yield

B1P7284 HSBC Euro High Yield Bond

4 EUR 1.35 2.38

Diversified Bond

B39R682 Templeton Global Total Return

4 EUR 1.40 8.77

Alternative Funds

SEDOL Name Risk Rating (1 - 7) Currency TER % Yield %

Multi - Asset Allocation

BD6K5N2 M&G Dynamic Allocation

4 EUR 0.95 0.00

BVFMDG4 Merrion Multi Asset 30 - 4 EUR 0.68 0.00

BVFMDD1 Merrion Multi Asset 50 - 4 EUR 0.68 0.00

BVFMDL9 Merrion Multi Asset 70 - 5 EUR 0.68 0.00

Absolute Return

BH5MDY4 Invesco Global Targeted Return - 3 EUR 0.86 0.00

Source: Bloomberg. Prices as of 31/1/2020..

16 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Fund Performance

Equity Fund Performance

Name 1 Month % 3 Month % YTD % 1 Year % 3 Year % 5 Year %

Global Equity

Veritas Global Equity Income 0.68 3.33 0.68 19.42 8.75 6.96

Global Equity

Merrion Global Equity Income -0.23 2.60 -0.23 14.36 - -

Global Equity Growth

Fundsmith Global Equity Feeder 3.34 7.13 3.34 28.31 17.66 15.19

Global Equity - Ethical Investing

Green Effects 4.48 13.10 4.48 20.29 8.70 8.45

European Equity

Threadneedle European Select 0.31 5.93 0.31 26.89 11.24 7.12

UK Equity

J O Hambro UK Opportunities 0.94 2.01 0.94 8.14 4.35 5.68

US Equity

Merian North American Equity 3.89 8.84 3.89 21.14 9.32 10.02

Bond Fund Performance

Name 1 Month % 3 Month % YTD % 1 Year % 3 Year % 5 Year %

Corporate Bond

PIMCO GIS Global Investment Grade Credit 1.80 1.89 1.80 9.17 3.82 3.01

Government Bond

BNY Mellon Global Bond 3.09 1.80 3.09 11.59 3.49 2.66

High Yield

HSBC Euro High Yield Bond 0.07 1.02 0.07 7.10 3.46 3.36

Diversified Bond

Templeton Global Total Return -0.76 0.75 -0.76 -6.22 -1.91 -1.40

Alternative Fund Performance

Name 1 Month % 3 Month % YTD % 1 Year % 3 Year % 5 Year %

Multi - Asset Allocation

M&G Dynamic Allocation -1.60 1.90 -1.60 5.35 2.52 3.28

Merrion Multi Asset 30 1.90 1.90 1.90 8.80 4.00 3.20

Merrion Multi Asset 50 2.10 3.20 2.10 12.20 4.60 4.30

Merrion Multi Asset 70 2.30 4.60 2.30 16.00 5.60 5.10

Absolute Return

Invesco Global Targeted Return 1.39 2.37 1.39 3.79 -0.10 -0.28

Source: Bloomberg. Prices as of 31/1/2020..

WARNING: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 17INVESTMENT OPPORTUNITIES

ETFs & TRUSTs

Our Core ETF and Investment Trust range is a selection of active and passive collective funds which

are listed on primary exchanges. This range offers a selection of the listed investment options

available across multiple asset classes and markets.

Core ETFs & Trusts

Niall Sexton, Equity ETFs & Trusts

Portfolio Ticker Name SEDOL Currency TER % Yield % UCITS

Construction

Global Equity

Analyst

IQQW iShares MSCI World UCITS ETF B297PF5 EUR 0.50 1.59 Yes

SDGPEX iShares Global STOXX 100 Select Dividend ETF B401VZ2 EUR 0.46 4.19 Yes

European Equity

SX5EEX iShares Euro STOXX 50 ETF 7018910 EUR 0.10 2.90 Yes

SPDR® S&P Euro Dividend Aristocrats UCITS B7KHKP4 EUR 0.30 3.15 Yes

UK Equity

CTY City of London Investment Trust Plc 0199049 GBp 0.44 4.47 No

US Equity

SPY5 SPDR S&P 500 UCITS ETF B6YX5T0 USD 0.09 1.40 Yes

SPDR® S&P U.S. Dividend Aristocrats UCITS ETF B6YX5V2 USD 0.35 2.03 Yes

Emerging Market Equity

JMG JPMorgan Emerging Markets Investment Trust Plc 0341895 GBP 1.02 1.79 No

Bond ETFs & Trusts

Ticker Name SEDOL Currency TER % Yield % UCITS

Corporate Bond

EUNR iShares Euro Corporate Bond Ex-Financials ETF BSKRK39 EUR 0.20 1.09 Yes

Government Bond

EUNH iShares Core Euro Government Bond ETF B4WXJJ6 EUR 0.09 0.62 Yes

High Yield

IHYG iShares Euro High Yield Corporate Bond ETF B66F475 EUR 0.50 3.77 Yes

Commodity ETFs & Trusts

Ticker Name SEDOL Currency TER % Yield % UCITS

Precious Metals

SGLD Invesco Physical Gold ETC B599TV6 USD 0.19 0.00 No

Commodity

OILB ETFS 1 Month Brent ETF B0CTWC0 USD 0.49 0.00 No

Source: Bloomberg. Prices as of 31/1/2020..

18 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Fund Performance

Equity Performance

Name 1 Month % 3 Month % YTD % 1 Year % 3 Year % 5 Year %

Global Equity

iShares MSCI World UCITS ETF 0.18 6.17 0.18 21.60 10.47 9.19

iShares Global STOXX 100 Select Dividend ETF -1.27 2.41 -1.27 13.48 5.49 5.21

European Equity

iShares Euro STOXX 50 ETF -3.27 1.32 -3.27 19.02 7.38 5.00

SPDR® S&P Euro Dividend Aristocrats UCITS -1.89 1.43 -1.89 13.41 7.92 6.65

UK Equity

City of London Investment Trust Plc -3.92 2.68 -3.92 12.41 6.71 5.82

US Equity

SPDR S&P 500 UCITS ETF 1.13 8.07 1.13 26.10 13.45 12.31

SPDR® S&P U.S. Dividend Aristocrats UCITS ETF -1.52 2.33 -1.52 16.99 9.15 10.47

Emerging Market Equity

JPMorgan Emerging Markets Investment Trust Plc -5.83 3.94 -5.83 14.90 14.28 12.01

Bond Performance

Name 1 Month % 3 Month % YTD % 1 Year % 3 Year % 5 Year %

Corporate Bond

iShares Euro Corporate Bond Ex-Financials ETF 1.09 0.79 1.09 6.21 2.82 2.06

Government Bond

iShares Core Euro Government Bond ETF 2.36 0.58 2.36 8.15 4.00 2.41

High Yield

iShares Euro High Yield Corporate Bond ETF -0.38 1.79 -0.38 6.64 3.20 3.23

Commodity Performance

Name 1 Month % 3 Month % YTD % 1 Year % 3 Year % 5 Year %

Precious Metals

Invesco Physical Gold ETC 4.24 4.94 4.24 19.85 9.09 4.21

Commodity

ETFS 1 Month Brent ETF -13.21 -0.82 -13.21 2.14 4.56 -1.68

Source: Bloomberg. Prices as of 31/1/2020..

WARNING: Past performance is not a reliable guide to future performance. The value of your

investment may go down as well as up.

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 19INVESTMENT OPPORTUNITIES

GREEN EFFECTS FUND FACTSHEET

FEBRUARY 2020

Fund Objectives

The objective of the fund is to achieve long term capital growth through a basket of ethically screened stocks. The fund invests in a

wide range of companies with a commitment to either supporting the environment or demonstrating a strong corporate

responsibility ethos. Sectors such as wind energy, recycling, waste management, forestry and water-related businesses all feature

prominently within the fund. The fund can only invest in the constituents of the Natural Stock Index (NAI) which was set up in 1994

and currently consists of 30 global equities.

Key Information GREEN EFFECTS FUND NAV SINCE INCEPTION

Morningstar Rating ★★★

€300

Fund Inception Oct 2000

€250

NAV €248.94

€200

Minimum Investment €5,000

€150

Dealing Frequency Daily

€100

Investment Manager Cantor Fitzgerald Ireland Ltd

€50

Custodian Northern Trust

€0

Administrator Northern Trust

Sales Commission 3%

Source: Cantor Fitzgerald Ireland Ltd Research

TER % 1.24%

Investment Mgt Fee 0.75% ESMA RISK RATING

*Prices as of 31/1/2020

Source: Bloomberg & Cantor Fitzgerald Ireland Ltd Research Lower Risk 1 2 3 4 5 6 7 Higher Risk

Fund & Share Class Information Typically Lower Rewards Typically Higher Rewards

Fund Size €79.6m

LARGEST SECTOR EXPOSURE %

Fund ISIN IE0005895655

Recycling 21.96%

Fund Sedol 0589565 Manufacturing 8.09%

Bloomberg GEFINVL ID Manufacturing Paper 6.76%

Wind Power 6.47%

Domicile Ireland Energy 4.35%

Building-Heavy Construction 4.05%

Structure UCITS Fund Waste/Water Tretmnt 3.59%

Technology 3.53%

Historic Yield 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

*Fund Yield 1.35%

GEOGRAPHIC EXPOSURE %

Fund yield is historic based on full year 2017 dividend

PAN-EUROPE 36.00%

rope

income received. The fund does not distribute income to

AMERICAS 33.53%

icas

investors. All dividend income is reflected within the NAV

EUROPE 15.35%

Asia

price of the fund.

ASIA 14.40%

rope

Australia 0.47%

ralia

Total number of holdings South Africa 0.25%

frica

Number of holdings 30 0 5 10 15 20 25 30 35

Market Capitalisation Exposure CURRENCY EXPOSURE %

Large: > €3bn 60% USD 31.32%

USD

EUR 15.35%

EUR

Medium: €500m - €3bn 37% JPY 14.40%

JPY

Small: < €500m 3% GBP 13.00%

GBP

SEK 7.79%

NOK

NOK 7.75%

SEK

DKK 7.46%

DKK

BRL 2.17%

BRL

0 5 10 15 20 25 30 35

20 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Top 15 Positions Sector Exposure Compared to a Traditional Global

TESLA INC 8.76%

Equity Fund

SMITH & NEPHEW 8.09%

The fund does not invest in banks, oils, mining, metals or large cap technology stocks. From a

SVENSKA CELLULOSA 6.76% performance and relative returns perspective this is something that all investors should bear

TOMRA SYSTEMS 6.72% in mind when considering investing in the fund. The overriding investment theme from a

sectoral perspective remains that of alternative energy, water, waste management and similar

VESTAS 6.47% companies with a strong corporate social responsibility (CSR) focus in both their culture and

ORMAT 4.35% work practices.

MAYR MELNHOF 4.06%

ACCIONA 4.05% Performance As of 31/1/2020.

KURITA 3.59% 1 Month YTD 1 Year 3 Year* 5 Year*

STEELCASE 3.53%

Green Effects 4.5 4.5 20.3 8.7 8.4

KINGFISHER 3.18%

RICOH 3.05% MSCI World € 0.7 0.7 22.4 11.1 10.1

SHIMANO 2.92%

S&P 500 € 1.3 1.3 25.7 13.5 12.8

EAST JAPAN RAILWAY CO. 2.92%

STEICO 2.04% Euro STOXX 50 -2.6 -2.6 19.3 7.7 5.3

Source: Cantor Fitzgerald Ireland Ltd Research

Friends First Stewardship Ethical 1.4 1.4 28.7 13.5 11.0

Fund Sector Exposure vs MSCI World

Sectors GE MSCI New Ireland Ethical Managed -2.4 -2.4 7.9 5.4 6.4

Consumer Discretionary 15% 13%

Source: Cantor Fitzgerald Ireland Ltd Research, Bloomberg and Northern Trust.

Consumer Staples 10% 10%

Energy 0% 6%

Financials 0% 17%

Annual Returns

Health Care 16% 13%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Industrials 33% 11%

2.40% -11.25% -30.00% 9.71% 14.38% 23.95% 22.52% 6.42% -38.47% 31.28%

Information Technology 6% 16%

Telecomunications Services 0% 3% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Open Ended Fund 1% 0%

13.47% -19.61% 16.02% 19.87% 18.42% 15.72% 6.62% 6.8% -5.91% 23.34%

Utilities 7% 3%

Materials 4% 5% 2020

Real Estate 2% 3% 4.50%

Cash 5% 0%

Source: Cantor Fitzgerald Ireland Ltd Research Source: Cantor Fitzgerald Ltd Research, Bloomberg and Northern Trust

email: greeneffects@cantor.com

WARNING: Past performance is not a reliable guide to future performance. The value of your investment may go down as well as up.

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 21INVESTMENT OPPORTUNITIES

STOCKWATCH

Emerging Markets

Historically, companies with higher than average growth trends trade at a higher share valuation than

those with lower growth trends. Logically, there is a high correlation between a region’s GDP growth

and domestic companies’ earnings growth. Considering this, a rational investor could justify paying a

Darren McKinley, valuation premium for emerging market exposure. Currently emerging market valuations, 14x 2020

CFA earnings, look compelling. Assuming the Coronavirus can be contained to a H1 2020 issue, we see

Senior Equity merit in adding strategically to emerging markets in the short term, for long term gains.

Analyst.

A review of the MSCI Emerging Market Index that the US$ may have peaked with the Fed

highlights an index that is still 18% below its expected to be on hold through 2020. A weaker

peak level recorded in 2007 and has been con- dollar and lower energy prices benefit emerging

solidating sideways for over a decade. In contrast, market economies and businesses.

the S&P 500 Index is now trading 135% above

Investors have shunned emerging markets as

its peak recorded in 2008 and European equities

the trade war between USA and China unfolded.

(SXXE) are within touching distance of 2008

Tariffs negatively impacted sales in China and

index levels. At 14x 2020 earnings for the emerg-

interrupted international companies’ supply

ing market index, the comparable metric for

chain. For instance, Caterpillar reported a 14%

the USA is 18x and Europe is 12x.

fall in Asian unit sales in Q3 2019. Now that a

In 2020 consensus expects global growth of phase one deal has been done, we expect

3.2%, up from 3% in 2019. China (+6% YoY), emerging markets to benefit as much, if not

India (+6.3% YoY) and Brazil (+2.2% YoY) are more, than the USA. We wouldn’t be surprised

expected to be the key drivers of global growth to see Caterpillar report 15% growth in unit

in 2020 as the US, Europe, UK and Japan growth sales through Q4 2020. Judging by a recent

rates are expected to stall or slow. We view fund manager survey by Bank of America, other

Emerging Market growth as more structural in investors agree that emerging markets are now

nature whilst a significant portion of developed compelling and have been adding to EM ag-

market growth is more cyclical in nature, albeit gressively in January 2020.

technology is also positively impacting growth

We have been recommending that private

globally. We think there is much more downside

clients add exposure via the JPM EM Investment

risk to cyclical growth as we move toward

Trust. This instrument is a UK listed asset with a

2021/2022 and consensus forecasts imply that

risk weighting of 4. The trust has a 32.8% weight-

G10 growth momentum may have peaked.

ing in China, 20% in India and the balance

2019 was a year of rate cuts (71 rate cuts by 49 spread across other emerging markets. Its top

central banks) and further loosening of monetary holdings include TSMC, HDF, Alibaba, Tencent

policy, including balance sheet expansion at and AIA. Please ask your portfolio manager for

the Fed, ECB and BOJ. Expectations are now further information and the KID document.

JPM EM INVESTMENT TRUST 1-YEAR SHARE PRICE

Source: Bloomberg 28/01/2020

22 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Engie

Engie is a global energy and services utility company that operates in three core sectors, low

carbon electricity generation (predominately renewables and natural gas), energy infrastructures

and customer solutions.

Pierce Byrne, CFA

Investment Analyst The energy infrastructure segment, known perspective the utility sector offers stability

as the Networks division, represents c.45% of through consistent cash flow generation

the company. This segment includes LNG re- throughout the business cycle. Considering

gasification, natural gas storage and transport, the deterioration in macroeconomic data in

and electricity and natural gas distribution. FY19, falling earnings growth and other global

The Networks business offers cash flow pre- tensions the utility space is well positioned

dictability through long term government to outperform. Secondly, Engie possesses a

contracts. The Low Carbon Power Generation, significant yield of 5.5%. This is particularly at-

which represents 34% of the business, com- tractive given falling rates globally and a con-

prises of renewables power generation, thermal tinued dovish outlook from central banks. Ex-

power generation and nuclear power gener- pectations are for this dividend to grow by

ation. Engie has transformed its power gen- 5% annually. Thirdly, at its recent capital

eration business to low CO2 generation, re- markets day management outlined its medi-

sulting in 56% less CO2 emissions in 2018 um-term targets which includes 7%-9% re-

compared to 2012. Its renewables segment curring net income CAGR for the next three

(c.23% of group EBIT) generated 24 GW of years. This is particularly impressive given it

power last year. Engie expects to add c.9GW plans €6bn worth of disposals over the same

by 2021, bringing the total generation through period. A key driver of its medium-term growth

renewables to c.33GW. The Client Solutions, is renewable power generation and infras-

which represents 25% of the business, com- tructure. As mentioned, it expects to add

prises of a variety of energy services offered 9GW of wind and solar of wind and solar ca-

to businesses, consumers and territories. The pacity over the next three years (+112%). This

client solutions segments is diverse, supplying is important given the shift to cleaner fuel.

30,000 clients across public buildings and in- Along with this, it offers low carbon generation

frastructure (€6bn revenue 2018), private build- through gas. Finally, its relatively cheap. From

ings (€4.3bn), industries (€6bn) and collective a 12m forward P/E (13.5x) perspective its

housing (€2.2bn). trading in line with its historical average, a

30% discount to Iberdrola (peer) and a 13%

There are several reasons to be positive on

discount to Enel (peer).

the stock at present. Firstly, from a top down

ENGIE 1-YEAR SHARE PRICE

Source: Bloomberg 30/01/2020

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 23R

QUARTERLY MARKETS

UPDATE

DUBLIN | Thursday, 27th February 2020 | 12.45 - 1.45pm

This February we will host our Quarterly Markets Update for our private clients, over a

light lunch. We will share our thinking on markets for the year ahead, with a particular

focus on pensions and managing your investments pre and post retirement.

REGISTER YOUR INTEREST BY FRIDAY, 14th FEBRUARY

If you are a client of Cantor Fitzgerald, please email EventsIreland@Cantor.com with your account

number for reference

If you are interested in attending but are not yet a client, please indicate this in your email and we can

put you in contact with one of our advisors

www.cantorfitzgerald.ie

Twitter : @cantorIreland LinkedIn : Cantor Fitzgerald Ireland

Cantor Fitzgerald Ireland Ltd is regulated by the Central Bank of Ireland. Cantor Fitzgerald Ireland Ltd is a member firm of the Irish Stock Exchange and the London Stock Exchange.Latest News

February 2020

Market Round Up 26

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 25LATEST NEWS

MARKET ROUND-UP

Ed Murray, Senior Portfolio Manager

JANUARY 2020

Coronavirus – an interruption NEWS IN BRIEF...

to the narrative?

Australia Day – Australians dominate

world golf

What are the chances on Australia Day

Markets look stretched on fundamental valuations, trading at premiums to long term that we see two Aussies, Lucas Herbert

averages. Technically they also look overbought on the charts and this epidemic could win the European Tour event in Dubai

be the catalyst or excuse for a pullback. The lockdown in Wuhan combined with travel while on the far side of the world Marc

restrictions will certainly hit Asian activity, if we look back to the SARS outbreak in 2003. Leishman win the Farmers Insurance

Chinese GDP slowed from ~10% quarter on quarter pre SARS to 3.5% during the event in Torey Pines, San Diego.

outbreak and then rebounded to about 13%. The sectors most impacted were tourism,

retail and transport. At the end of January we are seeing no different, the big gaming

resorts like Wynn’s and Las Vegas Sands have been hit. The cruise liners and airlines

are all lower, in the luxury space the likes of LVMH and in the consumer end, Starbucks

have closed 50% of its c.4,300 stores across China, while reducing opening hours in

the remaining stores. Weakness was seen across most commodity sectors, undoing

much of the positive sentiment from the signing of the US-China trade. Oil slipped on

the prospect of a fall-off in Chinese demand for the commodity. Likewise the mining

stocks were weaker. What the impact will be is the unknown. Does this become a

global pandemic impacting global economies, many of which are fragile and reliant

on Central Bank support?

Over the past decade, the assets which rose in value at least 70% of the time when

stocks suffer major drawdowns due to growth or policy shocks are US Treasuries, Gold Kobe Bryant – RIP

and the Yen. If one believes this is an acute event like SARS, then any shakeout in the

markets could offer a good entry point into the sectors mentioned above but also

into the tech/growth sectors, that may sell off aggressively in the short term on

overstretched valuations, but offer a sustainable long term investment opportunity

for one’s portfolio.

The chart below highlights some of the moves back in 2003 during the SARS outbreak.

MARKET ROUNDUP

Slán leat a chara

The UK our closest trading partner and

ally in Europe departs the union. While

they are officially gone, the gamesman-

ship kicks off as we knuckle down to iron

out a new trade deal between the Euro-

pean Union and the UK. Thankfully we

have a good Irish man at the negotiating

Source: Bloomberg 30/01/2020.

table in Phil Hogan.

26 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Performance

DATA

February 2020

Investment Returns 28

Long Term Investment Returns 29

Bond Returns 30

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 27PERFORMANCE DATA

INVESTMENT RETURNS

Equities

Index 31/12/19 31/01/20 % Change % ytd Change 52 Week High Date

ISEQ 7183.41 6998.2 -2.6% -2.6% 7,386 10/01/2020

FTSE 7542.44 7286.01 -3.4% -3.4% 7,727 30/07/2019

DAX 13249.01 12981.97 -2.0% -2.0% 13,640 22/01/2020

Eurostoxx50 3745.15 3640.91 -2.8% -2.8% 3,814 17/01/2020

Stoxx600 (Europe) 415.84 410.71 -1.2% -1.2% 425 24/01/2020

Nasdaq (100) 8733.073 8991.512 3.0% 3.0% 9,272 24/01/2020

Dow Jones 28538.44 28256.03 -1.0% -1.0% 29,374 17/01/2020

S&P500 3230.78 3225.52 -0.2% -0.2% 3,338 22/01/2020

Nikkei 23656.62 23205.18 -1.9% -1.9% 24,116 17/01/2020

Hang Seng 28189.75 26312.63 -6.7% -6.7% 30,280 15/04/2019

China (Shanghai Composite) 3050.124 2976.528 -2.4% -2.4% 3,288 08/04/2019

India 41253.74 40723.49 -1.3% -1.3% 42,274 20/01/2020

MSCI World Index 2358.47 2342.41 -0.7% -0.7% 2,419 22/01/2020

MSCI BRIC Index 339.99 324.87 -4.4% -4.4% 354 20/01/2020

Currencies

Currency Pair % Change % ytd Change 52 Week High Date

EuroUSD 1.1213 1.1093 -1.1% -1.1% 1.1448 20/03/2019

EuroGBP 0.84593 0.84 -0.7% -0.7% 0.9325 12/08/2019

GBP/USD 1.3257 1.3206 -0.4% -0.4% 1.3514 13/12/2019

Euro/AUD 1.59713 1.65798 3.8% 3.8% 1.6787 07/08/2019

Euro/CAD 1.45668 1.46822 0.8% 0.8% 1.5223 06/03/2019

Euro/JPY 121.77 120.17 -1.3% -1.3% 127.5000 01/03/2019

Euro/CHF 1.08559 1.06888 -1.5% -1.5% 1.1477 23/04/2019

Euro/HKD 8.7323 8.6156 -1.3% -1.3% 8.9866 20/03/2019

Euro/CNY 7.8149 7.6577 -2.0% -2.0% 7.9712 26/08/2019

Euro/INR (India) 80.0858 78.7401 -1.7% -1.7% 82.1114 05/02/2019

Euro/IDR (Indonesia) 15553.76 15050.07 -3.2% -3.2% 16,254.5600 14/05/2019

AUD/USD 0.7021 0.6692 -4.7% -4.7% 0.7265 05/02/2019

USD/JPY 108.61 108.35 -0.2% -0.2% 112.4000 24/04/2019

US Dollar Index 96.389 97.39 1.0% 1.0% 99.6670 01/10/2019

Commodities

Commodity % Change % ytd Change 52 Week High Date

Oil (Crude) 61.06 51.56 -15.6% -15.6% 65.40 08/01/2020

Oil (Brent) 66 58.16 -11.9% -11.9% 75.60 25/04/2019

Gold 1517.27 1589.16 4.7% 4.7% 1,611.42 08/01/2020

Silver 17.8523 18.0425 1.1% 1.1% 19.65 04/09/2019

Copper 279.7 251.7 -10.0% -10.0% 302.05 17/04/2019

CRB Commodity Index 401.58 404.17 0.6% 0.6% 427.50 04/04/2019

DJUBS Grains Index 29.275 28.0265 -4.3% -4.3% 32.38 17/06/2019

Gas 2.189 1.841 -15.9% -15.9% 2.91 26/02/2019

Wheat 558.75 553.75 -0.9% -0.9% 592.50 22/01/2020

Corn 387.75 381.25 -1.7% -1.7% 476.00 18/06/2019

Bonds

Issuer Yield Change % ytd Change 52 Week High Date

Irish 5yr -0.312 -0.328 -0.02 -158.9% 0.29 13/02/2019

Irish 10yr 0.119 -0.144 -0.26 -52.8% 0.93 05/02/2019

German 2yr -0.601 -0.67 -0.07 8.0% -0.49 05/03/2019

German 5yr -0.473 -0.642 -0.17 85.9% 0.76 22/02/2019

German 10yr -0.185 -0.434 -0.25 -183.5% 0.21 01/03/2019

UK 2yr 0.545 0.504 -0.04 -20.2% 0.85 27/02/2019

UK 5yr 0.601 0.412 -0.19 -29.5% 1.03 28/02/2019

UK 10yr 0.822 0.524 -0.30 -30.6% 1.33 01/03/2019

US 2yr 1.5691 1.3132 -0.26 -22.7% 2.56 05/03/2019

US 5yr 1.691 1.3134 -0.38 -23.9% 2.57 04/03/2019

US 10yr 1.9175 1.5068 -0.41 -20.8% 2.77 01/03/2019

Source for all tables above: Bloomberg and Cantor Fitzgerald Ireland Ltd Research.

28 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020PERFORMANCE DATA

LONG TERM INVESTMENT RETURNS

Asset Class Performances (returns in Local Currency)

Equities

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

MSCI World Index 9.8% -40.2% 30.9% 12.5% -4.9% 16.7% 27.5% 2.9% -1.9% 5.3% 20.11% -10.44% 25.19% -0.68%

MSCI Emerging Market Index 39.7% -53.1% 78.7% 19.4% -18.2% 18.7% -2.3% -4.6% -17.2% 8.6% 34.35% -16.58% 15.38% -4.69%

China 98.0% -64.9% 82.6% -12.8% -20.2% 5.8% -3.9% 52.9% 10.5% -12.3% 6.56% -24.59% 22.30% -2.41%

Japan -10.0% -41.1% 21.1% -1.3% -15.6% 25.6% 59.4% 7.1% 9.1% 0.4% 19.10% -12.08% 18.20% -1.91%

India 48.8% -51.8% 78.5% 19.1% -23.6% 28.0% 9.8% 30.1% -5.6% 1.8% 27.91% 6.67% 13.79% -1.41%

S&P500 5.6% -37.0% 26.4% 15.1% 2.1% 16.0% 32.4% 11.4% 0.2% 9.5% 19.42% -6.24% 28.88% -0.16%

Eurostoxx50 10.4% -41.8% 27.0% -1.8% -13.1% 19.6% 22.7% 1.2% 4.5% 0.7% 6.49% -14.34% 24.78% -2.78%

DAX 22.3% -40.4% 23.8% 16.1% -14.7% 29.1% 25.5% 2.7% 9.6% 6.9% 12.51% -18.26% 25.48% -2.02%

ISEQ -24.7% -65.1% 29.8% -0.1% 2.6% 20.4% 35.7% 15.1% 31.2% -4.0% 7.99% -22.14% 31.09% -2.58%

Commodities

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Gold 31.3% 5.5% 24.0% 29.7% 10.2% 7.0% -28.3% -1.5% -10.5% 8.6% 13.68% -2.14% 18.87% 3.93%

Brent Oil 54.2% -51.4% 70.9% 21.6% 13.3% 3.5% -0.3% -48.3% -36.4% 52.4% 17.69% -19.55% 22.68% -11.88%

Crude Oil 57.2% -53.5% 77.9% 15.1% 8.2% -7.1% 7.2% -45.9% -31.3% 45.0% 12.47% -24.84% 34.46% -15.56%

Copper 5.9% -53.6% 137.3% 32.9% -22.7% 6.3% -7.0% -16.8% -24.0% 17.4% 31.73% -20.28% 6.31% -10.01%

Silver 15.4% -23.8% 49.3% 83.7% -9.8% 8.2% -35.9% -19.5% -11.3% 15.8% 7.23% -9.36% 15.32% 0.51%

CRB Commodity Index 14.1% -23.8% 33.7% 23.6% -7.4% 0.4% -5.7% -4.1% -14.6% 12.9% 2.19% -5.36% -1.86% 0.65%

Currencies

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Euro/USD 10.5% -4.3% 2.0% -6.6% -3.2% 1.8% 4.1% -12.1% -9.7% -3.1% 14.15% -4.54% -2.20% -1.06%

Euro/GBP 9.1% 30.0% -7.2% -3.3% -2.8% -2.6% 2.2% -6.5% -5.0% 15.7% 4.05% 1.17% -5.88% -0.74%

GBP/USD 1.3% -26.5% 10.2% -3.3% -0.4% 4.6% 1.9% -6.0% -4.9% -16.3% 9.51% -5.55% 4.06% -0.36%

US Dollar Index -8.3% 6.1% -4.2% 1.5% 1.5% -0.5% 0.4% 12.7% 8.9% 3.6% -9.87% 4.26% 0.32% 0.98%

Source for all tables above: Bloomberg and Cantor Fitzgerald Ireland Ltd Research

Warning: Past performance is not a reliable guide to future performance.

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 29PERFORMANCE DATA

INDICATIVE PERFORMANCE FIGURES &

MATURITY DATES FEBRUARY 2020

Cantor Fitzgerald Capital Protected Products

Cantor Fitzgerald Capital Protected Products Underlying Indicative Indicative Indicative Option A Option B Option A Option B

Asset Initial Current Underlying Asset Participation Participation Indicative Indicative

(Ticker) Strike Level Performance Rate Rate Performance Performance

EUROSTOXX 50 DOUBLE GROWTH NOTE* SX5E 2986.73 3647.53 22.12% 200% 30.00% N/a

US $ Dividend Aristocrats Bond III SPXD8UE 2255.84 2341.47 3.80% 100% 220% 3.80% 8.35%

US $ Dividend Aristocrats Bond IV SPXD8UE 2206.04 2341.47 6.14% 80% 200% 4.91% 12.28%

US $ Dividend Aristocrats Bond V SPXD8UE 2336.40 2341.47 0.22% 50% 170% 0.11% 0.37%

US $ Dividend Aristocrats Bond VI SPXD8UE 2357.33 2341.47 -0.67% 50% 140% 0.00% 0.00%

PROTECTED ABSOLUTE RETURN STRATEGIES* SLGLARA 12.05 12.00 -0.47%

CARMPAT 615.33 645.66 4.93%

ETAKTVE 128.74 142.03 10.32%

Weighted Basket 4.93% 120% 5.91% N/a

GLOBAL REAL RETURN NOTE* BNGRRAE 1.27 1.38 8.17% 150% 12.26% N/a

PROTECTED MOMENTUM BOND* MSQTDFAA 1.46 1.52 3.63% 200% 7.26% N/a

PROTECTED MOMENTUM BOND II* MSQTDFAA 1.46 1.52 3.55% 200% 7.10% N/a

PROTECTED MOMENTUM BOND III* MSQTDFAA 1.52 1.52 0.00% 200% 0.00% N/a

PROTECTED BEST SELECT BOND* SGMDBSFE 155.51 156.20 0.44% 200% 0.88% N/a

PROTECTED BEST SELECT BOND II* SGMDBSFE 152.86 156.20 2.19% 200% 4.37% N/a

PROTECTED BEST SELECT BOND III* SGMDBSFE 151.87 156.20 2.85% 200% 5.70% N/a

PROTECTED BEST SELECT BOND IV* SGMDBSFE 148.10 156.20 5.47% 200% 10.93% N/a

PROTECTED BEST SELECT BOND V* SGMDBSFE 143.95 156.20 8.51% 200% 17.02% N/a

PROTECTED BEST SELECT BOND 6* SGMDBSFE 148.01 156.20 5.53% 200% 11.07% N/a

PROTECTED BEST SELECT BOND 7* SGMDBSFE 149.98 156.20 4.14% 200% 8.29% N/a

PROTECTED BEST SELECT BOND 8* SGMDBSFE 147.95 156.20 5.57% 200% 11.15% N/a

PROTECTED BEST SELECT BOND 9* SGMDBSFE 150.42 156.20 3.84% 180% 6.91% N/a

PROTECTED STAR PERFOMERS BOND* BNPIAFST 130.53 140.96 7.99% 180% 14.39% N/a

PROTECTED STAR PERFOMERS BOND II* BNPIAFST 130.91 140.96 7.68% 170% 13.05% N/a

PROTECTED STAR PERFOMERS BOND III* BNPIAFST 133.58 140.96 5.53% 170% 9.39% N/a

PROTECTED STAR PERFOMERS BOND IV* BNPIA2MT 166.28 172.57 3.78% 200% 7.56% N/a

PROTECTED STAR PERFOMERS BOND V* BNPIA2MT 165.75 172.57 4.12% 200% 8.23% N/a

PROTECTED STAR PERFOMERS BOND VI* BNPIA2MT 166.02 172.57 3.95% 200% 7.89% N/a

PROTECTED STAR PERFOMERS BOND 7* BNPIA2MT 168.56 172.57 2.38% 200% 4.76% N/a

PROTECTED STAR PERFOMERS BOND 8* BNPIA2MT 168.78 172.57 2.25% 200% 4.49% N/a

PROTECTED STAR PERFOMERS BOND 9* BNPIA2MT 168.28 172.57 2.55% 200% 5.09% N/a

Strike and Maturity Dates for Cantor Fitzgerald Bonds:

Bond Strike Date Maturity Date

Protected Absolute Return Strategies 24/03/16 31/03/21

US $ Dividend Aristocrats Bond III 26/03/18 06/03/23

US $ Dividend Aristocrats Bond IV 31/05/19 08/05/23

US $ Dividend Aristocrats Bond V 26/07/19 03/05/23

US $ Dividend Aristocrats Bond VI 22/11/19 29/10/24

EuroSTOXX 50 Double Growth Note 24/03/16 09/04/21

Global Real Return Note 29/04/16 12/07/21

Protected Momentum Bond 27/09/19 27/09/24

Protected Momentum Bond II 22/11/19 06/12/24

Protected Momentum Bond III 24/04/20 31/01/25

Protected Best Select Bond 15/06/18 22/06/23

Protected Best Select Bond II 14/08/18 21/08/23

Protected Best Select Bond III 26/09/18 03/10/23

Protected Best Select Bond IV 02/11/18 09/11/23

Protected Best Select Bond V 21/12/18 02/01/24

Protected Best Select Bond 6 27/02/19 05/03/24

Protected Best Select Bond 7 23/04/19 30/04/24

Protected Best Select Bond 8 14/06/19 21/06/24

Protected Best Select Bond 9 16/08/19 23/08/24

Protected Star Performers Bond 27/09/16 30/09/22

Protected Star Performers Bond II 16/12/16 21/12/22

Protected Star Performers Bond III 16/03/17 22/03/22

Protected Star Performers Bond IV 24/05/17 30/05/22

Protected Star Performers BondV 26/07/17 02/08/22

Protected Star Performers BondVI 20/09/17 27/09/22

Protected Star Performers Bond 7 24/11/17 01/12/22

Protected Star Performers Bond 8 21/12/17 28/12/22

Protected Star Performers Bond 9 09/03/18 16/03/23

Source for all tables above: Bloomberg.

30 CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020Cantor Fitzgerald Kick Out Notes

Cantor Fitzgerald Bond Issue Underlying Indicative Indicative Indicative

Asset Initial Current Underlying Asset Indicative

(Ticker) Strike Level Performance Performance

REAL ESTATE KICKOUT NOTE* SPG 190.52 133.15 -30.11% Next Potential Coupon 90%

URW 233.60 123.15 -47.28%

DLR 74.80 122.99 64.43%

WELL 65.25 84.91 30.13% 0%

BRAND LEADERS KICKOUT BOND* BAS 79.09 60.88 -23.02% Next Potential Coupon 13.5%

RYA 13.49 15.51 15.02%

SAMSUNG 44800 57200 27.68%

FP 53.21 43.98 -17.35% 0%

BRAND LEADERS KICKOUT BOND II* ML 89.60 105.20 17.41% Next Potential Coupon 13.5%

RYA 12.59 15.51 23.19%

SAMSUNG 43800 57200 30.59%

RDSA NA 27.79 23.38 -15.85% 0.0%

BRAND LEADERS KICKOUT BOND III* CRH 22.38 33.93 51.61% Next Potential Coupon 11.0%

ML 84.50 105.20 24.50%

FP 46.05 43.98 -4.48%

BAS 60.72 60.88 0.26% 11%

EURO BLUE CHIP KICKOUT BOND III* ITX 31.50 30.34 -3.69% Next Potential Coupon 30.0%

BN 62.79 72.66 15.72%

ADS 183.05 282.70 54.44%

CRH 32.82 33.93 3.38% 30.0%

EURO BLUE CHIP KICKOUT BOND IV* BMW 86.69 64.12 -26.04% Next Potential Coupon 27.0%

FP 48.70 43.98 -9.69%

ADS 177.25 282.70 59.49%

CRH 33.56 33.93 1.10% 0%

EURO BLUE CHIP KICKOUT BOND V* ADS 199.95 282.70 41.39% Next Potential Coupon 22.5%

ABI 102.15 67.83 -33.60%

BAYN 107.00 73.43 -31.37%

FP 43.92 43.98 0.14% 0%

OIL & GAS KICK OUT IV RDSA 26.98 23.38 -13.34% Next Potential Coupon 10%

FP 50.33 43.98 -12.62%

BP/ 5.34 4.58 -14.28%

XOM 79.01 62.12 -21.38% 0%

OIL & GAS KICK OUT V RDSA 28.98 23.38 -19.32% Next Potential Coupon 10%

FP 49.12 43.98 -10.46%

BP/ 5.56 4.58 -17.66%

XOM 77.69 62.12 -20.04% 0%

IRISH KICK OUT 1 CRH 27.17 33.93 24.88% Next Potential Coupon 10.5%

SKG 25.10 31.38 25.02%

BIRG 5.32 4.42 -16.88%

RYA 11.41 15.51 35.99% 0.0%

IRISH KICK OUT 2 CRH 28.72 33.93 18.14% Next Potential Coupon 10.5%

SKG 24.89 31.38 26.07%

KSP 44.72 55.60 24.33%

RYA 10.81 15.51 43.54% 10.5%

IRISH KICK OUT 3 CRH 29.47 33.93 15.13% Next Potential Coupon 10.5%

SKG 28.14 31.38 11.51%

BIRG 4.35 4.42 1.66%

RYA 9.98 15.51 55.38% 10.5%

IRISH BULL & BEAR KICK OUT CRH 31.03 33.93 9.35% Next Potential Coupon 9.0%

SKG 27.16 31.38 15.54%

BIRG 3.65 4.42 20.97%

RYA 10.00 15.51 55.10% 9.0%

GOLD KICK OUT BOND NEM 38.74 45.06 16.31% Next Potential Coupon 10%

GOLD 16.89 18.52 9.65%

AU 18.93 20.36 7.55%

KL 42.01 41.13 -2.09% 10.0%

EURO FINANCIALS KICKOUT BOND* BNP 68.40 48.22 -29.50% Next Potential Coupon 20%

GLE 48.91 29.27 -40.17%

INGA 15.72 9.84 -37.43%

SAN 5.77 3.531 -38.85% 0.0%

EURO FINANCIALS KICKOUT BOND II* BNP 62.85 48.22 -23.28% Next Potential Coupon 15%

GLE 41.96 29.27 -30.26%

INGA 15.00 9.84 -34.40%

SAN 5.503 3.531 -35.83% 0.0%

CANTOR FITZGERALD IRELAND INVESTMENT JOURNAL FEBRUARY 2020 31You can also read