Keynote Future of Insurance - CB Insights

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Keynote

Future of Insurance

1

22

About Me

Managing Analyst, Financial Services, CB Insights

@mlcwong | mwong@cbinsights.com

● Managing analyst at CB Insights, leading a team of research analysts

covering startup, venture capital, and corporate strategy activity and

trends in financial services

● Launched and writes CB Insights’ Insurance Tech newsletter, which

reaches 40K insurance executives and investors

● Featured in The New York Times, The Wall Street Journal, Bloomberg,

CNBC, and The Financial Times; appearances on Bloomberg TV and

Business News Network

● Magna cum laude graduate of Northwestern University

3

What We’re Going to Cover

1 2 3 4

Why change is Two types of P&C Why speed is more How incumbents

coming to P&C innovation important than ever should prioritize

4

Today, P&C insurance is a $617B market in the US

Property & casualty industry premium mix

Accident & Health

• 40% of premiums are

1% private passenger auto

• 14% of premiums are

homeowners

45%

54%

Commercial Lines Personal Lines

Source: S&P Market Intelligence, Fitch, CB Insights analysis 5

The nature of the P&C insurance industry today

sets it up for massive change

Existing business is Growth opportunities

hypercompetitive demand new approaches

6

The P&C insurance industry is becoming

more competitive every single year

Number of property & casualty filers, 2008 - 2018

2842 2831 Only 71 carriers have net

2794 written premiums >$1B

2769

2743

2706

2666

2639

2620 2606 2600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: NAIC, A.M. Best 7

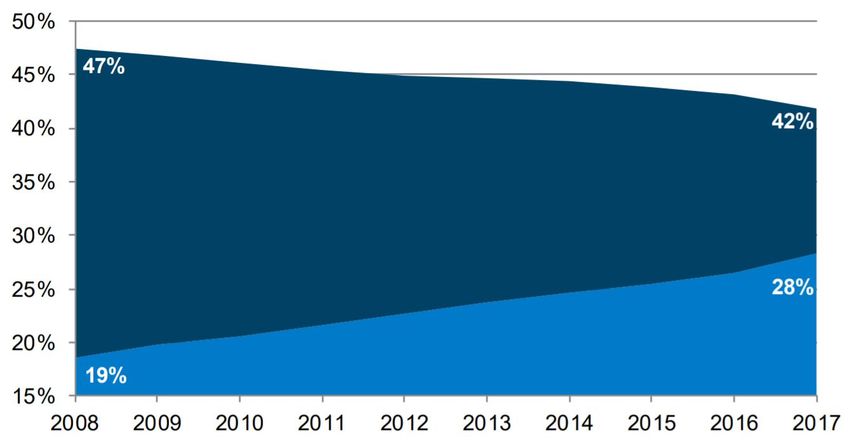

Many auto insurance incumbents are already

losing market share to direct writers

Personal auto market share over time, legacy mutuals & Allstate vs. direct writers

Source: William Blair, S&P Market Intelligence. Legacy mutuals include American Family, Farmers, Liberty Mutual, Nationwide, and State Farm. 8

The $100B small commercial market is growing,

but insurers will need to adjust to digital natives

~5% of small

business insurance is

Small $103

commercial $85 $95 bought through digital

DWP ($B) channels today.

But more than 60% of

small businesses in

Large & the US will be owned

Middle market by millennials/Gen X

by 2020.

2003 2008 2013

Source: A.M. Best, Conning, Accenture, CB Insights analysis 9

Cyber insurance is a major growth opportunity,

but has been bumpy as insurers remain cautious

Cyber insurance total direct written premiums ($B), 2016 – 2018

$2.00

$1.86

8% YoY

growth

$1.35

37% YoY

growth

2016 2017 2018

Source: S&P Market Intelligence, Fitch, CB Insights analysis 10Global insurance tech investment reached $4.15B

in 2018

Insurance tech investment trend, 2012 - 2018

Dollars ($M) Deals

$4,500 300

$3,000 200

$1,500 100

$- 0

2012 2013 2014 2015 2016 2017 2018

Source: Willis Towers Watson – CB Insights Quarterly InsurTech Briefing, Q4 2018 11P&C-focused startups are outpacing L&H startups

for investment deals

Insurance tech deal activity, P&C vs. L&H, 2012 – 2018

200

P&C

150

100 L&H

50

0

2012 2013 2014 2015 2016 2017 2018

Source: Willis Towers Watson – CB Insights Quarterly InsurTech Briefing, Q4 2018 12There are two ways

to think about tech

innovation in the

P&C industry

13Enablers Challengers

Software products and services built for Insurgents becoming insurance providers or

insurance providers distributors themselves

14Three key reasons why enabling technologies

are more powerful in P&C today

Ability to use cloud and Ability to create and access Ability to leverage

mobile in new ways new data sources advancements in AI/ML

15Insurers are adopting the use of mobile photo

estimating in the claims process at a rapid rate

The number of insurers using Snapsheet’s virtual Half of Allstate’s insured vehicles are now

auto claims technology has doubled since 2016 inspected through its QuickFoto claim mobile app

70+

60

45

35

vs.

2016 2017 2018 2019

Source: News mentions, Allstate, CB Insights analysis 16Mobile telematics providers are building up vast

datasets and aiming to shift customer behavior

Driver miles (in billions)

180

200

150

100

50

0

Source: Company blog posts, State Farm, Discovery Insure, CB Insights analysis 17Mobile is entering the property claims industry,

cutting down on time and cost

Source: CB Insights analysis 18Three key reasons why enabling technologies

are more powerful in P&C today

Ability to use cloud and Ability to create and access Ability to leverage

mobile in new ways new data sources advancements in AI/ML

19Companies are pairing the growth of geospatial

data with advances in image classification

Nearmap provides enablers with vertical In 2015, a deep neural network approach outperformed

coverage of >71% of the US population humans in the ImageNet Challenge for the first time

Source: CB Insights analysis 20450M safety inspections a year are completed

on SafetyCulture’s iAuditor app

Companies using iAuditor to conduct workplace

inspections by year

23,000

15,000

6,000

2016 2018 2019

Source: SafetyCulture, CB Insights analysis 21Three key reasons why enabling technologies

are more powerful in P&C today

Ability to use cloud and Ability to create and access Ability to leverage

mobile in new ways new data sources advancements in AI/ML

22Shift is aggregating claims data to build AI

models aimed at combating insurance fraud

Shift Technology insurance customers over time

70

45

Shift signs first

insurance

customer

2015 2017 2018

Source: Shift Technology, News mentions, CB Insights analysis 23Enablers Challengers

Software products and services built for Insurgents becoming insurance providers or

insurance providers distributors themselves

24Remember P2P insurance?

Wikipedia revision history: Lemonade homepage:

P2P Lending vs. P2P insurance Then and now

200 December 2015

150

P2P Lending

100

Today

50 P2P Insurance

0

Source: Wikipedia, Lemonade, CB Insights analysis 25The real change came from reinsurers and

carriers enabling digital MGA startups

Applying the MGA model to venture-backed Now, programs such as Munich Re Digital Partners

insurance startups used to be rare have helped venture-backed MGAs proliferate

(1999)

(2013)

(2013)

Source: CB Insights analysis, Munich Re 26Challengers are attacking incumbents across

three vectors

Cloud and mobile Use of data/AI Customer acquisition

27Root’s try-before-you-buy approach to mobile

telematics is growing fast

Root Insurance, direct written premiums ($M)

$88

$51

$33

$15

$8

$3

Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19

Source: Root, CB Insights analysis 28Coalition is taking a dynamic approach to

underwriting cyber based on cybersecurity posture

Source: Coalition, CB Insights analysis 29Hippo leverages a trove of data to pre-fill home

insurance information

Data analyzed on the back-end:

• Tax and county records

• Aerial and satellite imagery

(from different points in

time)

• Inspection reports

• Past claims reports

• Listing information

Source: Hippo, CB Insights analysis 30Next Insurance is striking partnerships across

different types of small businesses

Next Insurance now covering over

1000 classes of business

May 21, 2019

Source: Next Insurance, CB Insights analysis 31Why incumbents

need to act faster

32Insurgents are unbundling multi-line carriers

US-based startups (not exhaustive), for illustrative purposes only 33Direct writers now have their sights on small

commercial

Source: CB Insights analysis 34Big insurers are already preparing for an

autonomous future

Number of patents mentioning “autonomous vehicle”

Uber

Fort Motor Company

Toyota Motor Corporation

Waymo

General Motors

Google

Baidu

State Farm

Zoox

IBM

0 50 100 150 200 250

Source: CB Insights Patent Analytics 35How incumbents

should prioritize

threats and opportunities

36Understand that new entrants aren’t limited to

insurtech startups anymore

"The success of the auto

companies getting into the

Auto companies are getting

insurance business are probably

into the insurance business

about as likely as the success of

the insurance companies getting

into the auto business."

Source: 2019 Berkshire Hathaway Annual Meeting 37Focus on where control of your customers and

their data is changing

Online payroll platform Gusto Digital mortgage software Credit Karma Auto provides a

works with 60,000 small provider Blend processed one-stop shop for car info,

businesses, up from 50 more than $230B in mortgage such as car insurance

in 2012. loan applications in 2018. estimates, to 10M+ users.

Source: News mentions, CB Insights analysis 38Don't just copy the startup playbook, incumbents

won't always find the same opportunity for growth

Launched: 2018

Shut down: 2019

• 50% of Finn users were existing Chase

customers

• Unwilling to compete on annual % yield

• Undifferentiated on mobile banking features

39Focus on prioritizing emerging tech trends

Commercial data

Drone inspections Geospatial analytics automation Virtual auto claims Conversational AI

Market strength Market size: Commercial drones Market size: Geospatial data Market size: Natural language Earnings calls: 75+ mentions Earnings calls: Mentions of

stats to reach $3.6B by 2024 analytics to reach $74B by 2021 processing to reach $16B by of “auto claims” since the “chatbot” up +363% YoY (1H18

VC funding: Five-year high of News: Mentions of “geospatial 2021 start of 2017 vs. 1H17)

$568M in 2017 data” +45% YoY in 2017 Patents: 300+ NLP patents filed VC funding: $316M total funding

since 2016

Startups Kespry, DJI, Airware, Cape Analytics, BetterView, Groundspeed Analytics, Snapsheet, Metromile, Rasa Technologies, Spixii,

PrecisionHawk, EagleView Orbital Insight, Insurdata HyperScience, Captricity, Eigen Tractable RightIndem, Pypestream,

Technologies Automat, Ushur, Avaamo

Notable investors

Partnerships

Others: Munich Re with Others: Nephila Capital, Security Others: QBE with HyperScience, Others: Tokio Marine with Others: Helvetia with Rasa,

PrecisionHawk First with Cape Analytics Hiscox with Eigen Technologies Metromile, Ageas with Hiscox with Hi Marley

Tractable

40Focus on prioritizing emerging tech trends

Commercial data

Insurtech-as-a-service Hyperlocal weather analytics augmentation Cyber risk analytics Commercial auto telematics

Market strength News: 120 mentions of “on- Earnings call: Mentions of “bad Market size: Small business Market size: Cyber insurance Market size: Commercial fleet

stats demand insurance” since 2016 weather” +97% YoY (1H18 vs. insurance to reach $100B+ to reach $20B by 2025 telematics to reach $55B by 2021

1H17)

Startups Boost Insurance, REIN, Qover, Jupiter Intelligence, Climacell, Carpe Data, Datacubes, Planck CyberCube, Cyence Zendrive, Samara, Octo, Mobileye,

Slice, Sure Understory Weather Re, Digital Fineprint (Guidewire), Corax, Cyberwrite Nauto

Notable investors

Partnerships

Others: XL Catlin, Progressive, and Others: Pacific Specialty with Others: Zurich Insurance and Others: Munich Re with Mobileye,

Legal & General, The Co-operators Understory Weather AGCS with Cyence EMC Insurance with Octo

with Slice, Chubb with Sure

1Note: year-over-year (yoy) reflects Q1’18-Q2’18 vs. Q1’17-Q2’17 41High

TRANSITORY NECESSARY

• Corporate interest and adoption • Widespread industry and customer

adoption and investments

• Uncertainty about size of

market opportunity • Market and applications

NExTT

are understood

INDUSTRY ADOPTION

EXPERIMENTAL THREATENING

Framework

• No widespread adoption beyond • Large addressable market forecasts

pilots or early-stage companies

• Notable investment activity

• Early adopter-driven tech & trends

• Patchy/uncertain adoption

Low

Low MARKET STRENGTH High

42The NExTT framework’s 2 dimensions

Industry Adoption (y axis) Market Strength (x axis)

Signals include: Signals include:

momentum of startups market sizing forecasts earnings transcript

in the space commentary

media attention quality and number of competitive intensity

investors and capital

customer adoption investments in R&D incumbent deal making

(partnerships, customer, (M&A, strategic investments)

licensing deals)

43High

TRANSITORY

Trends seeing adoption but where there

NECESSARY

Trends which are seeing widespread

NExTT Trends

is uncertainty about market opportunity. industry and customer implementation /

adoption and where market and

We evaluate each of these trends using

As Transitory trends become more applications are understood. the CB Insights NExTT framework.

broadly understood, they may reveal

additional opportunities and markets For these trends, incumbents should The NExTT framework educates businesses about

that spur resources being deployed have a clear, articulated strategy and

emerging trends and guides their decisions in

INDUSTRY ADOPTION

towards them. initiatives.

accordance with their comfort with risk.

NExTT uses data-driven signals to evaluate technology,

product, and business model trends from conception to

maturity to broad adoption.

EXPERIMENTAL THREATENING

The NExTT framework’s 2 dimensions:

Conceptual or early stage trends with Large addressable market forecasts and

few functional products and which have notable investment activity. ● INDUSTRY ADOPTION (y axis)

not seen widespread adoption.

The trend has been embraced by early Signals include momentum of startups in the space,

Media interest and proof-of-concepts are adopters and may be on the precipice of media attention, customer adoption (partnerships,

spurred by the potential of trends. gaining widespread industry or customer customer, licensing deals).

adoption.

● MARKET STRENGTH (x axis)

Signals include market sizing forecasts, quality and

Low

number of investors and capital, investments in R&D,

earnings transcript commentary, competitive

Low MARKET STRENGTH High intensity, incumbent deal making (M&A, strategic

investments).

44High

EMERGING TRENDS IN P&C INSURANCE

TRANSITORY NECESSARY

NExTT framework

Underwriting & risk selection

Conversational Virtual auto claims

AI

Smartphone UBI Product design & distribution

Geospatial analytics

INDUSTRY ADOPTION

Drone inspections

Customer engagement

Insurtech-as-a-service Robotic process automation

Claims management & prevention

Commercial data augmentation

Commercial data automation

Cyber risk analytics

Hyperlocal weather analytics Smart home sensors

Embedded home insurance

Workplace wearables

Low

EXPERIMENTAL THREATENING

Low MARKET STRENGTH High

45You can also read