Knight Therapeutics Inc - Building Canada's Leading Specialty Pharmaceutical Company

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Building Canada’s Leading Specialty Pharmaceutical Company Knight Therapeutics Inc.

Forward Looking Statements

• This document contains forward-looking statements for the Company and its subsidiaries

• These forward looking statements, by their nature, necessarily involve risks and uncertainties

that could cause actual results to differ materially from those contemplated by the forward-

looking statements

• The Company considers the assumptions on which these forward-looking statements are

based to be reasonable at the time they were prepared, but cautions the reader that these

assumptions regarding future events, many of which are beyond the control of the Company

and its subsidiaries, may ultimately prove to be incorrect

• Factors and risks, which could cause actual results to differ materially from current

expectations are discussed in the Company’s Annual Report and in the Company’s Annual

Information Form for the year ended December 31, 2018

• The Company disclaims any intention or obligation to update or revise any forward-looking

statements whether as a result of new information or future events, except as required by

law

2

Why Invest in Knight?

Disciplined capital stewardship and relentless focus on our long-term strategy

Knight’s Consistent Investment Attributes Successes at Knight to Date

Proven leadership with alignment, expertise Raised $685M at increasing valuations

and determination to build Paladin 2.0

In-licensed over 20 innovative pipeline products

from 19 companies

Proven track record of profitable growth

Acquired NeurAxon Inc. and the Neuragen® brand

and capital stewardship

Sold or out-licensed rights to Neuragen, Impavido

and NeurAxon

Proven strategy to build a profitable

specialty pharmaceutical company FDA approval for Impavido® in Mar. 2014 and sold

PRV for US$125M

Proven ability to develop a pipeline of Lent over $170M to 15 partners and generated

double-digit return

innovative, new products

Deployed over $350M of capital, to date

First-in-class corporate governance

Generated $220M of net income, to date

3

Knight’s Strategy is Working

We’ve come a long way in 5 short years

In-licensed over 20 innovative pipeline

Knight is building a specialty pharma products from 19 companies

business Current portfolio includes 17

innovative Rx products

16 of the 17 key products in Knight’s Rx

portfolio have protected IP

Knight is focused on innovative products 12 of 17 key products in Knight’s Rx

portfolio are new chemical entities

Securing Rest of World infrastructure

Knight is developing commercialization

and product rights via innovative

capabilities outside of Canada transactions (e.g. Moksha8, Triumvira)

On-track to create a leading Canadian and ROW specialty pharmaceutical company

4

Shareholder Value Creation

Knight has delivered leading returns across Canadian and Global Spec Pharma peers

• Knight has outperformed Canadian Pharma and Global Specialty Pharmaceutical Peers, and the S&P/TSX

Composite Index, on a total shareholder return basis since its public listing in Mar. 2014

− Time horizon encompasses a full market cycle, with substantial volatility and Specialty Pharma

industry headwinds from late 2014 through 2016

• Former Paladin shareholders that rolled-over to Knight in Apr. 2014 have experienced a return of 1,259%

since spin-off

Knight Canadian Pharma Peers (1) Global Spec Pharma Peers(2) S&P/TSX Index

200%

150%

Total Shareholder Return (%)

100% 91.6%

50%

31.8%

12.7%

0% 7.4%

(50%)

Note: Bloomberg as of Mar. 29, 2019; beginning date as of Mar. 3, 2014; indexes equally weighted

(1) Canadian Pharma peers include: Nuvo, BioSyent, Cipher, and HLS

(2) Global Spec Pharma peers include: Pacira, Ligand, AMAG, Eagle, Vanda, Flexion, PDL, Bausch, Amphastar, Horizon, Mallinckrodt, Akorn and Endo

5Table of Contents

I Executive Summary

II Executing on our Strategy

III Corporate Governance

IV The Jakobsohn Scheme

6I. Executive Summary Better a GUD Knight than a bad one

How Did We Get Here?

Discussions with Jakobsohn to Date Our Conclusions

Sept. 2015 Mar. 2018: Aug. 2018: Dec. 2018: Oct. 2018 – Mar. 2019: Disingenuous

Feb. 2019: independence concerns:

Knight partners with Jakobsohn advises Knight board Jakobsohn sends paper to Less than 24 hours

Jakobsohn and Goodman that categorically rejects Knight advocating a Canadian Knight after engaging Jakobsohn would appoint

Medison via Medison will Jakobsohn’s focused “Diamonds” strategy continues good constructively with himself chairman though

acquisition of 28% breach Investor separation terms, and requesting that he be faith effort to Knight’s board, he’s not, in fact,

equity interest in Rights Agreement which are appointed chairman and replace negotiate Jakobsohn publishes independent

Medison in exchange and no longer significantly 3 board members with his own separation; white paper

for a 10.5M shares of declare dividend disadvantageous to unidentified appointees Jakobsohn’s asserting a LATAM &

Knight(1) and Knight shareholders, separation ROW focused So-called "governance

reciprocal 1-seat and to the benefit of Jakobsohn demands Knight demands strategy and a $50M concerns" are raised to

board representation Jakobsohn allocate hundreds of millions of become more VC fund allocation, distract investors from

dollars on undefined Jakobsohn onerous far below his private personal agenda

managed VC fund and other requests

high risk investments

So-called strategic plan

has changed drastically

since initial private

discussions, indicating

Oct. 2015 – Dec. 2018: Mar. – Aug. 2018: Oct. 2018: Jan. 2019: Feb. 2019: that he’s just improvising

All of Jakobsohn’s Goodman makes Jakobsohn sends letter to Jakobsohn requests Jakobsohn publishes

votes support Knight’s every effort to Knight expressing, for the first Goodman allocate $300M to public letter to

board resolutions on negotiate mutual time, strategy and governance undefined VC fund that Knight’s board Lacks understanding of our

strategy, governance, agreement to concerns; Knight encourages Jakobsohn would manage in business and the pharma

product in-licensing resolve breach of him to share his nominees exchange for stopping his market outside Israel

and investment Agreement, activist campaign; Goodman

decisions culminating in Jakobsohn asserts that Knight refuses

proposed should focus on early-stage /

biotech, Canada only and Jakobsohn tells Goodman Jakobsohn is looking out

separation terms by solely for his own interest,

Jakobsohn suspend ROW strategy, to sell his 15% stake in

calling LATAM “corrupt” Knight; Goodman refuses not yours

Jakobsohn’s ever-changing agenda and refusal to engage demonstrate a clear disregard for responsible shareholder and corporate engagement

(1) Jakobsohn currently holds a 7% indirect interest in Knight via Medison Biotech (1995) Ltd. and Tzalir Holdings Ltd; he is Medison’s

controlling shareholder, with a 72% ownership interest

8What’s the Bottom Line?

Jakobsohn wants to remove Jonathan Goodman, take control of Knight without

paying shareholders a premium, and make risky, self-serving bets with your cash

The Jakobsohn Scheme

Knight Invests Jakobsohn Gambles

Value orientation and patient Bigger bets & higher, binary risk

Strategy Late-stage product focus Short-term, top-line growth,

Long-term, de-risked profitable lower profit margins

growth Unclear strategy lacks specificity

Proven and Experienced Unproven and Self-Interested

Long and successful track record No management team

Leadership Independent directors with the Misaligned strategy

right experience and expertise Motivated by 72% stake in

Aligned with Knight shareholders Medison and his private VC funds

Shareholder Value Creation Jakobsohn Value Creation

Financial Long-term focus Take control of Knight without

Disciplined approach paying a premium

Objective Use Knight’s cash to help fix

Medison and finance his VC funds

9Your Choice: Invest or Roll the Dice?

Shareholders didn’t sign up for Jakobsohn’s risky scheme

The Jakobsohn Scheme

Disciplined Approach

Make RISKY bets with UNCERTAIN outcomes

to Value

Portfolio

Make LARGE & CONCENTRATED bets

Diversification

Disciplined Approach Deploy capital with MYOPIC TOP-LINE FOCUS,

to Capital Deployment with little regard for profit

Manage Appropriate Balloon the cost structure with EXCESSIVE

Cost Structure OVERHEAD & INFRASTRUCTURE

“Mr. Goodman is the most intelligent steward of capital in the Canadian Specialty Pharmaceutical space and

has been consistent, honest and unwavering with his strategy for the company since day one.”

March 15, 2019

10Proven Leader or Unknown?

Jonathan Goodman Value of the Businesses They’ve Built Since 1995

Thousands

Regarded as one of the best specialty pharma

investors in Canada

Highly motivated to build Canada’s leading specialty

pharma company (1)

Track record of significant shareholder value creation $3.2B $1.1B $4.2B

Deep respect for shareholders and their hard earned

cash Jonathan

Goodman

Meir Jakobsohn

No experience in Canada or any country outside of (2)

Israel and Romania $0.3B

His business is struggling with declining net income

Spends most of his time on Medison, not Knight

No management team in so-called “plan” Meir

Jakobsohn

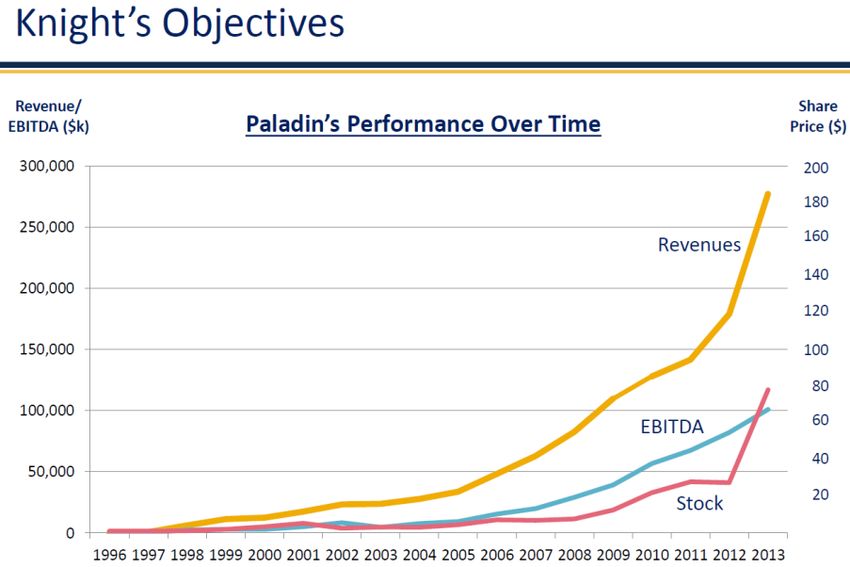

“With a consistent track record of disciplined capital deployment, Jonathan Goodman led Paladin Labs through 19 years of

consecutive record revenues, growing the share price a staggering 100-fold… we remain confident in Mr. Goodman’s ability

to replicate his former success”

March 1, 2019

(1) Paladin Labs implied equity value of C$3.2B at acquisition closing on Feb. 29, 2014 and Knight market cap of C$1.1B as at Mar. 29, 2019

(2) Implied 100% value based on Knight’s Sept. 2015 acquisition of 28.3% of Medison for C$82.0M, including contingent consideration of C$1.1M

11Whose Track Record Do You Trust?

Jakobsohn’s track record underscores his focus on short-term, top-line growth and low margins

Jonathan Goodman: Proven Profitability and Growth

• Disciplined investment approach $65 $180

− Focused on late-stage products with opportunistic approach $160

$55

to earlier stage products via de-risked structures $140

Delivering outsized returns to

Net Income ($M)

$45

• patient investors $120

Share Price ($)

Focused on long-term, profitable growth $1.50 in Mar. 1995 was worth $100

− Targets in-licensing deals with 15 year minimum term $35

$151.60 by Feb. 2014 (27.5% CAGR) 34% 35%33%

$80

− Financial profile hurdles in-line with Canadian and broader $25 23% $60

spec pharma peers 19%

$15 $40

’96 – ’08 Average: 15%

• Working hard to execute on the strategy and stay disciplined $5

$20

$-

throughout the cycle

− Reputation as a highly financially disciplined investor, having ($5)

'96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

($20)

evaluated over 1,000 product opportunities in the past 5

Net Income Net Income Margin Share Price

years

Meir Jakobsohn: Unsustainable and Deteriorating Profitability

• Short-term top-line growth

− Myopic focus on short-term, top-line growth

− Low profit margins 14%

11%

2016 - 2018

• Jakobsohn’s true agenda: gamble your money on schemes that 8% CAGR

benefit himself

(8.6%)

− Jakobsohn benefits 72 cents for every dollar Medison earns $28M $25M $21M

but only 7 cents for every dollar Knight earns – and he

wants control of both 2016 2017 2018

− Shareholders should ask: Where do his real interests lie? Net Income(1) Net Income Margin

(1) Financial information from Knight’s public disclosure; derived from Medison’s consolidated financial statements, excluding amortization of acquisition

fair value adjustments and converted to IFRS from Israeli GAAP in CAD

12What’s Next?

Two paths for Knight, but only ONE that is GUD for shareholders

The Jakobsohn Scheme

Seize control of your company, without

Long-term strategy focused on value creation paying a premium, and use your cash to

and de-risked profitable growth boost Jakobsohn’s private company

Unclear strategy that would gamble with

your capital

Disciplined investment approach throughout

the cycle

Unproven leadership motivated by 72%

stake in Medison and private VC funds

Jonathan has an extensive track record and is Has not invested any of his own money

financially aligned with Knight shareholders into Knight and has actually sold shares

Clear Choice for Shareholders:

VOTE YOUR BLUE PROXY

13II. Executing on our Strategy We never rest at Knight

Knight’s Disciplined and Clear Strategy

Rigorous diligence process underpinned by value-investing philosophy

• Building a specialty pharma company serving 17 Innovative Rx Products

Canada and select ROW

− In-licensing innovative products Equity / Debt

− Late-stage product focus In-licensed / Acquired

Transactions

− Opportunistic approach to earlier stages

via de-risked structures (e.g. equity or

debt)

• Product build-out across four key Therapeutic

Areas (TA’s)

Tenapanor

− TA platforms drive more profitable growth

within existing pillars

− Opportunistically pursue new TA’s

• Lending and fund investments are tools from

which to support the core strategy: sourcing

innovative products for Canada and ROW

• Working hard to execute

− Evaluated over 1,000 product

opportunities in the past 5 years

− Built a reputation as highly financially

disciplined

15Core Growth Strategies

• In-license innovative pharmaceuticals in Canada

• Acquire mature or “under-promoted” products from Big Pharma

In-licensing or • Develop near-term, low risk / low expense products

Acquiring • Lending and fund investment activities are tools in support of the core

Product Rights strategy

− Strategic loans to source near and long-term product pipeline

(e.g. Triumvira)

− Ceased fund investments beyond committed capital

• Partner of choice for 2nd / 3rd tier markets

• High growth countries with stable legal and regulatory systems, IP protection

Rest of World • Focus on Big Pharma’s non-core geographies / 2nd tier markets

• Partner with international operators via investment and strategic loans to

expand ROW infrastructure (e.g. Moksha8)

16Focused on Late-Stage Products

Sound diligence process focused on growing profitability while mitigating risk

• Knight takes on late-stage commercialization risk, not early-stage development risk with lower probability

of success

− Focus on later stage products (Phase II, Phase III or approved in foreign markets) with lower clinical /

regulatory risk

• Opportunistic approach to earlier stage products via de-risked structures (e.g. equity or loans)

• Jakobsohn’s publicly proposed strategy lacks clarity and has changed considerably since initial private

discussions (when his emphasis was on early stage products and venture investing)

− What’s clear is that Jakobsohn wants to make bigger bets on riskier products with Knight shareholders

taking the risk

The Jakobsohn

Scheme

Pre - IND Phase I Phase II Phase IIl NDA / Approval

Several months 1 – 2 Years 1 – 4 Years

Probability of Success: All Therapeutic Areas Across Trial Phases(1)

Phase I to Approval Phase II to Approval Phase III to Approval

Compound Likelihood of Approval 10% 17% 42%

(1) Kola, Nature Reviews-Clinical Success Rates

17Growing and Diverse Pipeline

An impressive portfolio of innovative prescription pharmaceuticals, prioritizing 4 TA’s

Therapeutic Area Product Licensor Status Transaction Date NCE IP

Marketed in CAN &

Movantik® AstraZeneca December 2016

approved in ISR

Probuphine™ Titan Marketed February 2016 -

Pain / Gastrointestinal Ibsrela™ Ardelyx Pending submission March 2018

Mytesi® Jaguar Pending submission September 2018

NeurAxon Family N/A Pre-Clinical – Phase III January 2015

Antibe Family Antibe Pre-Clinical – Phase II November 2015 -

AzaSite™ Akorn Approved July 2015 -

Ophthalmic Iluvien® Alimera Approved July 2015 -

Netildex™ SIFI Submitted August 2016 -

TX-004HR(1) TherapeuticsMD Pending submission February 2019

Women’s Health

TX-001HR(2) TherapeuticsMD Pending submission February 2019

Nerlynx® Puma Submitted January 2019

Oncology

Advaxis Family Advaxis Phase I – Phase III August 2015 Biologic

Impavido® N/A Marketed February 2014

Tenapanor Ardelyx Phase III March 2018

Other

Arakoda™ 60P Pending submission December 2015

Phase II – Pending

60P family 60P December 2015 -

submission

Note: NCE – New Chemical Entity; IP – Intellectual Property

(1) Marketed as IMVEXXY in the US

(2) Marketed as BIJUVA in the US 18Canadian Portfolio

Providing stable growth, with opportunities to leverage current footprint

Strengthening Foundation Superior sourcing and research capabilities

Growth Pillars BD focus on adding products to footprint

Opportunity to expand coverage and add new

Streamline & Expand therapeutic areas

Building for the Long-Term ROW strategy helps secure products for Canada

19Expand Geographically

Prioritizing LATAM based on size, growth and proximity

Stage 1 Stage 2

2017

700 10.0%

2022

’17 – ’22 CAGR

600 8.0% Global Growth

Market Size (USD Billions)

500

6.0%

2017-2022 CAGR

400

4.0%

300

2.0%

200

100 0.0%

0 (2.0%)

USA/CA Europe China Japan LATAM Southeast Asia ME, India, Eastern

Africa Europe

Source: IQVIA – IMS Market Prognosis March 2018

20Rest of World Strategy

Identify markets with attractive growth profiles and a high degree of fragmentation

ROW (ex-US, Target Geographies

Europe, Japan,

China) specialty

pharma will

continue to grow

• High-growth countries with expanding

access and funding for medicines

Leveraging 13+

• Stable legal and regulatory systems,

Partner of choice

licensed products in including IP protection

for 2nd / 3rd tier

markets

select international

markets • Focus on Big Pharma’s non-core

geographies / 2nd tier markets

• LATAM prioritization driven by:

− Market size

− Underlying growth drivers

Strategic investments

to increase capacity to

Deploy financial

strength and BD

− Proximity / current presence

evaluate international capabilities to − Compelling pan-American (ex-USA)

opportunities accelerate growth in “one-stop shop” commercial solution

focus markets

• Additional ROW growth levers identified

in Middle East, Africa, Eastern Europe

Diligent and calculated approach to ROW; strategy is underway

21Strategic Lending Overview

Leveraging the balance sheet to source additional products and an attractive return

Nominal

• Secured loans with life-sciences companies

Company

Loan

Balance(1)

Interest

Rate Maturity

Product

Rights

in exchange for product rights or pipeline

assets for Canada and select international Synergy US$7.5M 15% 2020

markets

60° Pharma US$6.8M 15% 2020

• Over C$170M loaned to over a dozen

strategic loan partners generating double- Crescita C$3.6M 9% 2022

digit annual return on invested capital

Medimetriks US$1.0M 13% 2019

• Lending has served a valuable role in Ember US$0.5M 12.5% n/a

securing product and pipeline assets

− Sourced a number of early-stage Moksha8 US$10.0M 15% 2024

pipeline products and two commercial

consumer health assets (Neuragen and Triumvira US$5.0M 15% 2020

Synergy family of products)

Total(2) C$44.8M

Access to in-licensed product or M&A are threshold criteria for future investment

(1) As at Dec. 31, 2018, except for Moksha8 (Feb. 15, 2019) and Triumvira (Feb. 20, 2019)

(2) Total converted to CAD using Bank of Canada exchange rates on Mar. 29, 2019

22Strategic Lending Supports Growth

Secured loans with Moksha8 (US$10M) and Triumvira (US$5M)

Securing ROW infrastructure Securing product rights

• Committed up to US$25M in strategic financing agreement. • Access to early stage, novel T cell technology with limited

Loaned US$10M to date at 15% interest rate, maturing capital at risk

early 2024, fully secured

• Issued US$5M bridge-loan at 15% interest rate maturing

• An additional US$100M loan may be issued to Moksha8 for early 2020

corporate development or acquisition of product licenses

• Own warrants representing 3.5% of the fully diluted

• Own warrants at a nominal exercise price for 5% of the common shares of Triumvira

fully diluted shares of Moksha8

• In-licensed commercial rights to Triumvira’s future

• Allows Knight access to partner in Mexico and Brazil oncology products in select territories

“The Moksha 8 transaction is consistent with Knight’s expansion

“The [Triumvira] transaction is in keeping with Knight’s targeted

strategy internationally, where it seeks strong partner companies

lending strategy. That is, on top of a 10-15% interest rate, the deal

with regional expertise. The deal also highlights a string of increased

comes attached to warrants and product rights. With licensed

business development activity by Knight recently with eight

geographies including Canada, Israel, Mexico, Brazil and Colombia,

transactions by our count in the past 12 months vs. one in the year

this is in line with Knight’s goal of expanding its presence in the

prior. We see this activity by Knight as a strong leading indicator for

large and underserved Latin American market.”

continued record revenue and shareholder value creation.”

February 19, 2019 February 21, 2019

23Strategic Funds Overview

Attractive financial return with product access upside optionality

• Fund investments were made to obtain Fund Amount Stage Geography

preferential access to innovative products Teralys C$30.0M VCAP Fund of funds Canada

for Canadian market

Domain US$25.0M Early stage N.A.

• LP financial returns have been attractive,

but fund investments have not been as Forbion €19.5M All clinical stages Europe

effective at generating product leads

− Sourced Iluvien® and Advaxis portfolio Sectoral US$13.0M Late stage to small cap Global

− Core challenges with sourcing product Sanderling US$10.0M Early stage N.A.

under fund structure (lack of “new”

opportunities, GP fiduciary duties and HarbourVest C$10.0M VCAP Fund of funds Canada

conflict with LPs)

TVM US$1.6M All clinical stages Global

• No longer investing into funds, beyond

already committed capital Bloom

C$1.5M Commercial stage Canada

Burton(1)

Genesys C$1.0M Early Stages N.A.

Total(2) C$126.7M All stages Worldwide

We’ve ceased allocating capital to funds, beyond already committed capital

(1) Bloom Burton healthcare lending trusts are managed by Stratigis Capital Advisors

(2) Total converted to CAD at Bank of Canada exchange rates as of the commitment dates; using the Mar. 29, 2019 exchange rates, total fund commitments would be C$138.0M

24A Consistent Message to Shareholders

Knight’s unwavering commitment to long-term shareholder value creation

Proven leadership with alignment, Long-Term Shareholder Value Creation Takes Time

expertise and determination to build

Paladin 2.0 What did we say in May 2015?

“We continue to execute on our value-creating strategy…while

simultaneously making a difference to the health of Canadians.

Achieving this goal will take time, but we are convinced that our

Proven track record of profitable relentless implementation of our version of the Canadian

growth and capital stewardship specialty pharmaceutical strategy will deliver handsome returns

for the patient investor.”(1)

Proven strategy to build a profitable

specialty pharmaceutical company

Proven ability to develop a pipeline

of innovative, new products

First-in-class corporate governance

(1) Knight’s Q1/2015 conference call on May 13, 2015 and May 2015 investor presentation

25III. Corporate Governance Independent, aligned with track records of success

Knight’s Board of Directors

Relevant, diverse and proven experience

James Gale Nancy Harrison Robert Lande

Chairman

Chairman Director Director

Since

Since2014

2004 Since 2014

Since 2018

CCGNC: Chair Audit: Chair

Audit: Member CCGNC: Member

Over 20 years of 26 years of experience in Over 20 years of

Pharmaceutical experience Pharmaceuticals and Life Pharmaceutical experience

Sciences Strong background in

Former investment banker

Co-founder and former Finance and

Served on eight public telecommunication

President of MSI

pharmaceutical companies Former President and CFO

Methylation

Current board member of of FXCM Group LLC., an

Former Partner and Senior online brokerage firm

Teligent Inc., a specialty

Vice President of Ventures

generic pharmaceutical Former COO of Riverridge

West Management Inc

company Capital Partners LLC., an

investment management

Positive Total Shareholder firm

Return track record

Unrivaled Leadership in the Pharma Industry

27Knight’s Board of Directors

Relevant, diverse and proven experience

Samira Sakhia Sylvie Tendler Michael Tremblay

President, & CFO

Chairman Director Director

Since

and2014

Director Since 2014 New Nominee

Audit: Member

Since 2016 CCGNC: Member

Over 40 years of

Over 20 years of A leading pharmaceutical pharmaceutical experience

Pharmaceutical experience market research specialist

Significant experience in

Strong background in Founder of the Tendler sales, marketing, and

accounting Group, a custom medical business development in the

marketing research pharmaceutical industry

Successful record in M&A

company

and strategic lending

Former President of Tokyo-

transactions, and completed Substantial experience in

based Astellas Pharma

the sale of Paladin to Endo pharmaceutical marketing

Canada Inc

International for over $3B consulting

Positive Total Shareholder

Former chairman and director

Return track record of Innovative Medicines

Canada

The Tendler Group Inc

IntrinsiQ Tendler Inc

Unrivaled Leadership in the Pharma Industry

28Aligned Executive Leadership

Jonathan Goodman has a track record of success

Under Jonathan’s leadership, Paladin Labs share price increased by 101x, creating over

Jonathan Goodman $3B of shareholder value(1)

Founder, CEO

and Director Significant skin-in-the-game via 15.3% ownership interest in Knight

Over 30 years of Personally invested over $70M in Knight’s equity offerings, representing 10% of funds

Pharmaceutical experience raised

Jonathan Goodman

Former co-founder, President Zero visibility, influence or involvement in Family Holdings

and CEO of Paladin Labs Inc Pharmascience

Paladin’s stock price increased Jonathan holds an indirect interest in Blind Trust

by 101x under his leadership Goodman Family holding company via blind ~25% equity 0.02% votes

Served on boards of five public trust structure

Goodman Family

pharmaceutical companies Family holding company manages HoldCo

Positive Total Shareholder investment decisions in its subsidiaries, not

Return track record Jonathan (virtually nil voting power) Many Subsidiaries

Complete information firewall

Pharmascience

“…Mr. Goodman is the fundamental cornerstone of our conviction in Knight… Our discussions

with current investors lead us to believe that the majority of existing stockholders share our

opinion and thus, we believe Knight's future will continue to be one that is championed by Mr.

Goodman.”

March 15, 2019

Shareholders place considerable conviction behind Jonathan’s ability to execute

(1) Paladin Labs’ market cap increased from $6M to $3.2B between Mar. 1995 until its sale to Endo in Feb. 2014

29Unassailable Governance Approach

Knight has a highly skilled and experienced Board of Directors

Knight’s board is 71% independent, excluding Meir Jakobsohn

Legal / Regulatory

Experience

Public Company

43% of Knight’s board consist of women, excluding Meir Jakobsohn

CEO/NEO Experience

18% Financial / Accounting

23%

Two fully independent committees of the board

6%

Experience

Capital Markets /

Robust board renewal process M&A Experience

Should shareholders elect Nancy Harrison and Michael 18%

Public Company Board

Tremblay at the AGM, over 70% of the board will comprise 35% Experience

directors that have been appointed over the last four years Pharmaceutical

100%

Past experience with Paladin is a strength: key understanding of

Experience

the business model

Finance Industry Experience/Knowledge

Public Company Public Company

2018 Meeting

Nominees CEO / NEO Board Legal Gender

Attendance Financial / Capital Markets / Biotechnology / Entrepreneurial

Experience Experience

Accounting M&A Pharmaceutical Experience

Jonathan R Goodman 100% ✓ ✓ ✓ ✓ ✓ ✓ M

James C Gale 100% ✓ ✓ ✓ M

Sylvie Tendler 100% ✓ ✓ ✓ ✓ F

Robert Lande 100% ✓ ✓ ✓ ✓ M

Samira Sakhia 100% ✓ ✓ ✓ ✓ ✓ F

Nancy Harrison(1) 75% ✓ ✓ ✓ F

Michael Tremblay (2)

n/a ✓ ✓ ✓ M

Meir Jakobsohn 67% × × × × × ✓ ✓ M

Equipped with the right skills to make Knight the next Paladin

(1) Nancy Harrison joined Knight’s board in Aug. 2018

(2) Michael Tremblay is a new nominee in 2019

30IV. The Jakobsohn Scheme A major risk for shareholders

The Jakobsohn Scheme

Not additive to board composition or strategic direction

• Jakobsohn would appoint himself as Chairman, though he’s not independent

− Why doesn’t Jakobsohn believe this is a conflict?

• Who will run the company under Jakobsohn’s Scheme?

Leadership &

− Recommendations conspicuously lack a management team

Governance • Director nominees have managed – but have never built – Canadian pharmaceutical companies

• The dissident slate lacks finance experience, with no director nominee capable of sitting on the

Audit Committee

• “Vision” is hardly new; Jakobsohn offers no unique strategy for Knight

− Privately, Jakobsohn was calling for massive Knight investments dedicated to venture investing

− Publicly, Jakobsohn is re-hashing many elements of Knight’s existing strategy and calling it his

own

− Redacted material lacks real substance but gives the illusion of having novel ideas

• Overstated value of “Diamonds”

Strategy − Jakobsohn’s review is oversimplified and lacks understanding of Knight and Canadian market

dynamics

− Understates risk of a concentrated portfolio with so-called “Diamonds”-only focus

• Ever-changing strategy to fit the latest narrative; he’s simply improvising

• If Jakobsohn has a real plan to deliver $500M of revenue with 20% EBITDA margins, why hasn’t he

implemented on his ailing Medison business?

The True Agenda: Take control of Knight and use your cash for Jakobsohn

32The Dissident Slate

Zero entrepreneurial pharma experience

NO entrepreneurial pharma experience

NO product acquisition experience in the pharma industry

NO capital markets / M&A experience; none capable of sitting on the Audit Committee of the board

NOT a diverse slate: only one female dissident nominee, compared with three incumbent nominees

ONLY 1 of 6 nominees reside in Canada

WEAK Total Shareholder Return track record

Ecotality Inc. and Reddy Ice Holdings Inc. filed for bankruptcy during Kevin Cameron’s tenure at the

company

Outside Public Company Finance Industry Experience/Knowledge

Average TSR Record Public Public

Company Company Entrepreneurial Gender

Dissident Slate Financial / Capital Markets Legal Biotechnology /

CEO/NEO Board Pharmaceutical

Director Roles NEO Roles Experience Experience Accounting / (M&A) Pharmaceutical

Experience

Kevin Cameron -50% ✓ ✓ ✓ M

Elaine Campbell ✓ ✓ F

Michael Cloutier 7% -50% ✓ ✓ ✓ M

Robert Oliver ✓ ✓ M

Christophe Jean 13% 17% ✓ ✓ ✓ ✓ M

A slate of followers, not leaders

33Much of Jakobsohn’s “Vision” isn’t New

Knight already pursues (or has considered) much of Jakobsohn’s so-called “strategy”

Jakobsohn Scheme “Vision” New Idea? Knight’s Existing Strategy

“Knight should focus on in-licensing This is Knight’s stated strategy

innovative products and building a

commercialization infrastructure” We’ve built a portfolio of 17 innovative Rx products

“Knight should halt all non-strategic Knight ceased allocating capital to VC funds, well

financial activities (purchasing LP interests

in venture funds and opportunistic lending

activities)”

prior to Jakobsohn’s objections

Strategic loans are a tool to source product in-

licensing opportunities (e.g. Triumvira)

“Knight can provide a comprehensive This is Knight’s stated strategy: to become the

ROW solution and become the trusted go-

to partner of any new diamond developer

for the ROW markets”

partner of choice in 2nd and 3rd tier markets

Develop ROW infrastructure via diligent and

calculated approach

“Cash should be deployed in a strategic Knight is actively seeking a number of strategic

manner to create value for shareholders;

excess cash should be returned to

shareholders”

opportunities, including in-licensing and M&A

Evaluated over 1,000 product opportunities in the

past 5 years relying on a disciplined approach

34Myopic “Diamonds” Focus a Needless Risk

Oversimplified review lacks understanding of Knight and pharmaceutical business model

Jakobsohn Scheme Allegation Market Reality

• Pharma companies mitigate risk by building diversified portfolios of products

• “Focus only on Diamonds in defined therapeutic with varying degrees of innovation, risk/pricing profile

area clusters” • Knight’s portfolio of innovative products is in line with other pharma

companies’ diversified portfolios

• Payers across the globe are struggling with declining healthcare budgets, and

• “Diamonds are less vulnerable to competition and are specifically addressing high priced medicines

pricing pressures compared to other segments of

the pharma market” • Specializing in high-valued innovative therapies does not create pricing power

in Canada; payers negotiate pricing on a product-by-product basis (no

• “Payers have stronger leverage when negotiating bundling)

with pharma companies that have non-innovative

products” • The Knight team has a track record of successfully negotiating favourable

listings

• “Diamonds commercialization demand specialized • Specializing in “Diamonds” doesn’t create a competitive advantage; available

expertise and high level of compliance and ethical pool of biotech / ex-pharma talent can be recruited by anyone

code adherence that serve as a very high barrier to • Knight’s strategy is to create a competitive advantage by offering a one-

entry for potential competitors” stop-shop commercial solution in underserved markets

• “We do not believe Knight has fully evaluated

partnering with these [redacted] companies; it

• Knight has, or is, evaluating partnering with all the redacted so-called

“missed opportunities” and companies with upcoming product approvals

should”

Knight should have a diversified product portfolio that adds value for shareholders

35Jakobsohn Proposes Risks and Losses

Acting on Jakobsohn’s scheme would add risk and create unnecessary losses

Jakobsohn Scheme Proposition Key Considerations

• Terminating license agreements for no cause would be hugely detrimental to

Exit current licensing deals for “less Knight's reputation as a partner in the industry: Knight honours its agreements!

specialized” products • Knight would forego existing and future revenue and incur losses on investments

already made (e.g. license fees, regulatory and commercial)

• An 8-year term is not sufficient to make a healthy return

Pursue in-licensing agreements with • 8-year term only affords ~5 years to launch product, recoup investment and

terms of 8 years make a healthy return, after considering ~2 year regulatory filing and review and

~1 year to build market access and reimbursement coverage

• Gross margins of 40% are too low to generate a healthy return

• Rare / orphan and oncology peers would typically feature gross margins much

Pursue “over 40% gross margin” on

higher than 40%

in-licensed products

• Jakobsohn’s recommendation for below-market terms illustrates his myopic

focus on top line with little attention to profitability

• Selling fund holdings on secondary market would require Knight to sell at a

Exit fund investments

discount, thereby incurring needless frictional costs

Found a C$500M VC fund with • GP interest will not improve product access compared to an LP interest

significant GP participation (C$50M • GPs still face the same fundamental challenge as LPs (e.g. GP fiduciary duties

from Knight) and conflict with LPs)

36Jakobsohn’s Ever Changing Strategy

No conviction in a strategy that changes after every discussion

Jakobsohn Scheme Iterations Shareholders Should Ask Themselves

Internal Discussion Public Campaign

Why Is he just

now? improvising?

October 2018

March 2019

“Knight should focus only

“Focus only on ‘Diamonds’”

on Early-stage / biotech” Who’s going to run

the company?

October 2018

March 2019

“Knight should focus only

“Prioritize ROW Markets” What will Jakobsohn

on Canada”

“LATAM is ‘corrupt’”

“Focus on LATAM” promise next?

December 2018 March 2019 What’s Jakobsohn

“Knight should allocate “Halt all non-strategic saying in private, that

capital and form VCs” financial activities” he’s not telling us?

37The Jakobsohn Scheme is a Major Risk for

Shareholders

The Jakobsohn Scheme has no leadership and hasn’t offered a unique “vision”

The Jakobsohn Scheme overstates the value of “Diamonds”-only focus and understates

the risk of placing concentrated bets on a few opportunities

Jakobsohn’s true agenda:

Take control of Knight and use shareholder cash for Jakobsohn, his ailing Medison and

his VC funds

Clear Choice for Shareholders:

VOTE YOUR BLUE PROXY

38Vote Your BLUE Proxy Now

Vote for management and direction that will deliver long-term, sustainable, profitable growth

Questions?

Need help voting?

Contact our strategic shareholder advisor and proxy solicitation agent

• Toll-Free (Within North America): 1-888-518-1552

• Collect (Outside North America): 1-416-867-2272

• Email: contactus@kingsdaleadvisors.com

39Building Canada’s leading specialty pharmaceutical company Knight Therapeutics Inc. (TSX:GUD)

You can also read