Netflix, Inc. (NFLX) - Small Cap IR

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

RESEARCH REPORT:

PUBLISHED APRIL 23, 2014

If there is anything that is universal across the world, it is certainly people’s love of media content –

specifically movies and television. In fact, last year global movie ticket sales set a new record rising to

$35.9 billion. Considering nearly 70% of that total came from international markets outside the US, it is

safe to say that we are not the only ones enjoying our own movies. Although only up 5% from 2012,

international movie ticket sales are up 33% from five years ago. Meanwhile, ABI Research put out a

report earlier this year saying that worldwide pay-TV subscribers are expected to exceed 1.1 billion by

2019, aided by the help of the increasing internet protocol television (IPTV) segment.1 At the end of

2013, there were approximately 903.3 million pay-tv subscribers worldwide which generated nearly

$250 billion in service revenue. Separately, IPTV operators reported roughly 92 million subscribers

generating around $37 billion in service revenue. Although a CAGR of only 4% for the overall market is

not as impressive as the 18.5% YoY growth experienced in the IPTV operators alone (their CAGR is

expected to be closer to 10%), it clearly demonstrates increasing demand in general over the next

several years.2

Ultimately, when you are talking about a $300+ billion global market annually between movies and TV,

there is a significant push to grab every dollar you can from that market. One such company that has

revolutionized the movie and TV industry while continually growing its subscriber base is Netflix – a

company that nearly every person on Earth knows about and is easily identified by their bright red

envelopes.

Netflix, Inc. (NFLX) is an internet television network with more than 48 million members in over 40

countries across the world. The company operates in three segments: domestic streaming, international

streaming, and domestic DVD. Whereas the domestic and international streaming segments derive

revenues from monthly subscription services consisting solely of streaming content, the domestic DVD

segment (only available in the US) derives revenues from monthly subscription services consisting solely

of DVD-by-mail (which includes both regular DVDs and Blu-ray discs). The company also develops its own

content and original series, such as House of Cards and Orange is the New Black. Their core strategy is to

grow their streaming subscription business domestically and internationally while improving their

members’ experience by expanding streaming content and extending streaming service to even more

internet-connected devices.

REVOLUTIONIZING THE INDUSTRY:

Netflix has been – and continues to be – in the news a lot. Between winning content deals; calling out

Comcast’s merger with Time Warner Cable; activist investor participation (see: Carl Icahn); competition

with Amazon; raising subscription prices; the botched proposal to split the DVD and streaming

businesses in 2011; and volatility among the stock price performance (i.e. -78% drop in 2011 and

1

Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

subsequent 600% rise), one thing is clear – NFLX has received a lot of press. And rightfully so as the

company has single-handedly revolutionized the way we view and consume media content.

In just a few short years, Netflix has essentially done to movies and TV what Apple has managed to do to

music and cell phones – disrupt the industry and change the game. Nowadays, the term

“bingewatching” is associated with NFLX while nearly every internet-capable device must be Netflix-

capable as well. Internet streaming, on-demand, movies, and television are now all synonymous with

Netflix. When Blockbuster arrived on the scene in 1985, it changed the way we watched movies at

home. Now, less than 30 years later, Netflix has put Blockbuster out of business. While there is no

guarantee that NFLX will be around 30 years from today, the company has by no means reached its peak

and has plenty of room to grow for the foreseeable future.

As with any subscription-based service, NFLX is highly dependent upon existing and future subscribers

for current and future revenue. Out of the nearly 7 billion people on this Earth, only 48 million people

currently subscribe to NFLX. That is less than 0.7% of the worldwide population. Obviously NFLX is only

currently accessible to a small part of the world as internet access isn’t even available to certain areas

still. However, as internet access becomes more prevalent – aided significantly by the growth of mobile

– NFLX will inevitably follow in some areas. And while I’m not talking about NFLX having a billion

subscribers anytime soon if ever, the ability for the company to double its base is very probable –

especially when you consider the fact that HBO has about 130 million subscribers. Given both the

market size (in population and revenue potential) and that market’s thirst for media content, NFLX is

primed to quench that thirst over the coming years. Ultimately, with any stock, the growth potential is

what gets people excited. Couple that with real, growing and quality earnings and you have a recipe for

success.

SUBSCRIBER GROWTH:

Overall, in looking at NFLX’s subscriber growth, it is easy to see that while its domestic DVD segment has

been clearly declining, its streaming segments (both domestic and international) have been consistently

growing – at a fairly decent clip too.

Subscriber Growth 2013 2012

Domestic Streaming 23% 25%

International Streaming 79% 229%

Domestic DVD -16% -26%

Source: NFLX Form 10-K, December 31, 2013

Additionally, on a quarterly basis over the past two years, membership in domestic streaming has

increased on average by 5.4%, while international streaming has risen almost 20% QoQ. Meanwhile,

domestic DVD membership has decreased by about 5% on average each quarter.

2Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

June Sept Mar June Sept Dec Mar

30, 30, Dec 31, 31, 30, 30, 31, 31,

MEMBERSHIP GROWTH 2012 2012 2012 2013 2013 2013 2013 2014 AVG

5.43%

Domestic Streaming Member Growth 2.26% 4.86% 8.15% 7.47% 2.17% 4.31% 7.49% 6.74%

19.74%

Intl. Streaming Member Growth 18.24% 18.96% 41.99% 16.68% 8.47% 18.60% 18.96% 16.04%

-5.06%

Domestic DVD Member Growth -8.42% -6.86% -4.44% -2.93% -5.95% -4.79% -3.05% -4.01%

Source: NFLX Q1 14 Financial Statements, http://ir.netflix.com

Netflix also acknowledges that they suffer from seasonality issues as illustrated above, and as a result it

should be expected that subscriber growth in Q2 and Q3 of this year will likely be lower than the

previous two quarters. The company also recently stated that given the higher growth rates in the

international segment, seasonality there is less of an issue than in the domestic segment. Overall,

however, I expect the company to continue to grow at their longer-term averages as they continue to

add subscribers – especially in their international streaming segment.

It does appear that the company’s efforts to expand their international segment have worked well too.

The company recently announced that out of its current subscriber base of 48 million roughly 26% of

those subscribers are from outside the US – more than double the split just two years ago.

Mar 31, June 30, Sept 30, Dec 31, Mar 31, June 30, Sept 30, Dec 31, Mar 31,

Revenue Breakdown 2012 2012 2012 2012 2013 2013 2013 2013 2014

Domestic Streaming 88.4% 86.9% 85.3% 81.6% 80.3% 79.4% 77.2% 75.4% 73.8%

International Streaming 11.6% 13.1% 14.7% 18.4% 19.7% 20.6% 22.8% 24.6% 26.2%

Source: NFLX Q1 14 Financial Statements, http://ir.netflix.com

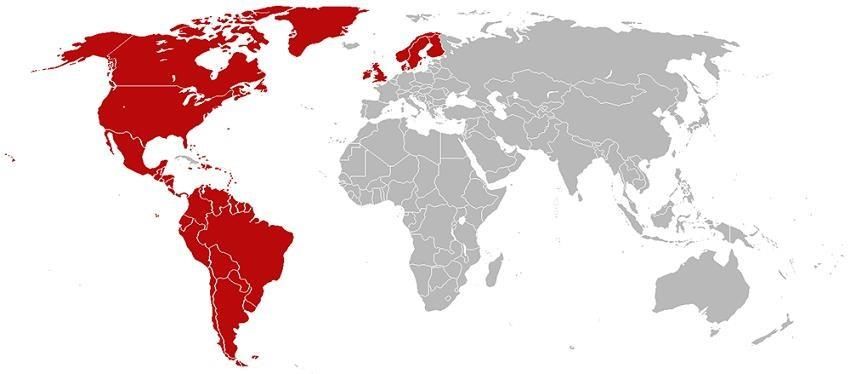

Growth in the international segment is expected to continue as the company recently announced its

intention to expand and launch in France and Germany. For now, however, the company’s presence is

mainly confined to the Western hemisphere (as illustrated below) and some European countries.

Considering the company’s first foray into the international markets began only in September 2010,

NFLX has made considerable progress overseas, and should continue to do so in the future.

3Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

NOTE: Countries where Netflix is currently available are highlighted in red. Source:

bestofnetflix.com, July 2013

EARNINGS QUALITY:

While there are many analysts and investors who argue that the company’s growth in international

markets is a reason to invest in the company, one of the biggest criticisms of NFLX has been the fact that

its international segment continues to operate at a loss. While that is certainly true, the company has

been making tremendous strides in turning that segment around and even expects to achieve

profitability this year. Given the improving performance of the international segment over the last

several quarters, I believe that is highly likely.

In fact, just two years ago, the international streaming segment was operating at a -236% operating

margin compared to only -13% this past quarter. That’s quite an improvement over just two short years.

Moreover, margins in the domestic streaming segment have improved as well over the past two years

rising from about 14% at the end of March 2012 to 25% in March 2014. Meanwhile, the domestic DVD

segment has even slightly improved over the same time period and most recently posted margins in-line

with its quarterly average of roughly 48%. So, yes, the international segment is still losing money, but it

is losing significantly less money than it has in the past AND it should post a profit in the near future.

Mar 31, June 30, Sept 30, Dec 31, Mar 31, June 30, Sept 30, Dec 31, Mar 31,

AVG

OPERATING MARGIN 2012 2012 2012 2012 2013 2013 2013 2013 2014

20.30%

Domestic Streaming 14.31% 16.41% 17.21% 19.24% 20.57% 22.55% 23.75% 23.44% 25.20%

-85.50%

Intl. Streaming -236.46% -137.64% -118.82% -103.21% -54.16% -39.68% -40.59% -25.87% -13.10%

5.70%

Total Streaming -5.49% -0.34% 0.53% 1.27% 6.97% 10.21% 10.43% 12.09% 15.60%

47.87%

Domestic DVD 45.71% 45.90% 48.16% 50.14% 46.65% 46.74% 48.09% 51.67% 47.73%

Source: NFLX Q1 14 Financial Statements, http://ir.netflix.com

4Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

Furthermore, in breaking down the three segments by revenue, costs of revenues, and marketing costs

over the past three years, there are several things to note. First, international streaming revenues have

been growing by over 100% the past two years, while increases in content costs have been slowing

(from 80% to 39%) over the same time period. Further, although marketing costs jumped in 2012 (in the

international segment), they seemed to have stabilized across all segments in 2013. Moreover, domestic

streaming revenues continued to rise while costs were fairly stable. Only in the domestic DVD segment

did revenues decline as subscriber growth has been negative the last few years due to the rising

popularity of streaming. This decline, however, was met by a similar decrease in costs. Overall, I believe

the trends displayed below are positive for the company going forward and should help drive earnings

quality in the future.

Revenues 2013 2012 2011

Domestic Streaming 63% 61% 54%

Intl Streaming 16% 8% 3%

Domestic DVD 21% 31% 42%

Costs of Revenues 2013 2012 2011

Domestic Streaming 60% 59% 60%

Intl Streaming 25% 18% 10%

Domestic DVD 15% 23% 30%

Marketing Costs 2013 2012 2011

Domestic Streaming 55% 55% 68%

Intl Streaming 42% 43% 30%

Domestic DVD 2% 2% 1%

Source: NFLX Form 10-K, December 31, 2013

CONTENT COSTS:

Without a doubt the company’s largest expenditure (as expected) has, and will continue to be, the

expansion of its content library. Rising content costs (both through licensing and NFLX’s own original

programming) are the most important factors affecting the company’s overall profitability.

5Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

Although somewhat volatile over the years (and recent quarters), overall the costs of content growth

have only slightly outpaced that of revenue growth on average. However, it does appear that the

company has gotten better at managing those costs while growing revenue at a meaningful pace. It is

my belief that the company will only get better over time and the trend indicated below is relatively

optimistic for NFLX going forward.

ANNUAL

34.78% 46.19% 20.86% 13.28% 22.34% 29.52% 48.17% 12.61% 21.22% 27.66%

68.48% 34.84% 25.36% 15.78% 18.57% 25.76% 50.33% 28.73% 17.40% 31.69%

2005-12 2006-12 2007-12 2008-12 2009-12 2010-12 2011-12 2012-12 2013-12 AVG

Revenue Growth

Costs of Content Growth

QUARTERLY

6.57% -0.68% 2.18% 1.80% 4.42% 8.36% 4.39% 3.46% 6.24% 8.09% 4.48%

7.08% 8.52% 3.04% 3.11% 4.98% 4.45% 3.71% 4.91% 2.65% 7.02% 4.95%

2011-12 2012-03 2012-06 2012-09 2012-12 2013-03 2013-06 2013-09 2013-12 2014-03 AVG

Revenue Growth

Costs of Content Growth

Source: Morningstar

VALUATION:

I do hate the expression “priced for perfection” and perhaps that may be the case with NFLX at current

valuations, but considering historical valuations, the stock isn’t as expensive as it has been in the past.

More importantly, NFLX is somewhat different from other stocks when looking at it on a valuation basis.

As with most technology stocks, valuations often do get out of control and it is tough to really value a

company that trades at a P/E of around 200. Compared to its normalized ratios, NFLX does indeed

appear to be overvalued at current levels. However, following both the optimistic earnings release on

Monday afternoon and the nearly 20% drop in the stock’s price over the past 6 weeks or so, I do believe

the company will push higher from these levels of around $350/share.

6Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

Furthermore, using today’s closing price of $353.50 and growing revenue, earnings, and EBITDA at the

company’s 10-year average growth rates, NFLX’s valuation looks more reasonable (and investable). Sure,

there are risks to proper execution by the company as well as a still-expensive valuation 18 months out,

but when you look at the historical valuations and the company’s potential growth in revenue, earnings,

and EBITDA, the company is somewhat attractive. Lastly, it does bode well for the stock as the

enterprise value (EV) of the company (especially a technology company) is currently trading at less than

6x this year’s EBITDA. It is important to realize, however, that this is due primarily to the company’s high

amortization expenses tied to the company’s content library.

OTHER ISSUES:

As mentioned earlier, NFLX is heavily dependent upon the media content they currently have the rights

to as well as their ability to purchase future rights to media content at reasonable prices. The company is

also heavily dependent on the technology customers utilize to access NFLX’s online library, as well as the

internet broadband capabilities of their customer’s internet service providers (ISPs). Further,

government regulations and net neutrality laws may threaten NFLX’s business model in the future.

Moreover, given NFLX’s increasing expansion into international markets, there are additional economic,

political, and regulatory risks that the company may face. These risks extend beyond the different laws

and specifics regarding certain content licenses and adoption to include foreign currency exchange risks,

adverse tax consequences in other countries, different user/data protection and privacy laws, low

usage/penetration of internet connected devices, and the availability of reliable broadband connectivity

for expansion.

Additionally, although competition is fierce – especially between NFLX and Amazon Prime – having one

service doesn’t necessarily mean you cannot have the other. To me, NFLX and AMZN are sort of like

movie studios that compete with each other, but still make money by offering different movies. In this

case, the “movies” are the various movie/TV content that available on each platform. Further, NFLX is

offered on all the various internet-connected devices such as Apple TV, Roku, and even the

newlyintroduced Amazon TV. Further, the news today concerning the agreement between Amazon and

HBO should not affect Netflix’s business as much as the market would have you believe given the 5%

sell-off as a result. Investors in NFLX should be aware of dramatic price swings such as these following

7Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

news surrounding content licensing deals as shares are known to be volatile (in both directions) during

these times.

Lastly, while some investors and analysts are wary of NFLX’s recent decision to raise prices $1-2/month, I

believe the price increase will not affect subscriber growth all that much. Although some people may be

more hesitant to sign up for $8.99 (or $9.99) per month instead of the current $7.99 per month price, as

long as the price doesn’t go over the psychologically-important $10 level, new adds will remain

competitive. It should also be noted that even a $2 increase per month is the same 25% price increase

that new subscribers to Amazon Prime’s service were just hit with recently (increasing from $79/yr to

$99/yr). Further, I would not be surprised if this quarter saw an increase in new subscribers who wanted

to avoid the impending price increase as those members will not experience a price increase for a

“generous amount of time” per NFLX management.

CONCLUSION:

Ultimately, the tremendous growth potential both here in the US and abroad is significant and should

further propel the stock higher. In the near-term, performance is likely to be volatile – mostly due to

general market factors and the “guilt-by-association” mentality that has plagued the momentum names

(see: TSLA, CMG, FB, etc.) as of late. Over the longer-term, however, I believe NFLX will continue to do

well as they better manage their content costs and continue to grow subscribers. While I definitely

would prefer a lower current valuation, the recent 20% correction in shares of NFLX makes it a more

compelling buy at these levels. In the end, it is tough to bet against the pioneer in an industry (see:

Apple) – especially one that has proven it can execute well on a consistent basis.

Sources:

1 ABI Research. “Worldwide Pay-TV Subscribers to Exceed 1.1 Billion in 2019 with Increasing IPTV Market

Share.” 22 January 2014.

2 Ibid.

8Netflix, Inc. (NFLX)

Rating: BUY

Good Long-Term Investment Despite High Valuation

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this

article myself, and it expresses my own opinions. I am not receiving compensation for it, and I have no business relationship with

any company whose stock is mentioned in the article.

The information contained herein is not intended to be investment advice and does not constitute any form of invitation or

inducement by Michael Maggi, CFA and Money by Maggi to engage in investment activity. Neither the information nor any

opinion expressed constitutes a solicitation for the purchase or sale of any security. Securities, financial instruments, strategies,

or commentary mentioned herein may not be suitable for all investors and this material is not intended for any specific investor

and does not take into account an investor’s particular investment objectives, financial situations or needs. Any opinions

expressed herein are given in good faith, are subject to change without notice, and are only current as of the stated date of

their issue. Prices, values, or income from any securities or investments mentioned in this report may fluctuate, and an investor

may, upon selling an investment lose a portion of, or the entire principal amount invested. Past performance is no guarantee of

future results. Before acting on any recommendation in this material, you should consider whether it is suitable for your

particular circumstances and, if necessary, seek professional advice.

This report may contain certain forward-looking statements and information, as defined within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, and is subject to the Safe Harbor created by those

sections. This material contains statements about expected future events and/or financial results that are forward-looking in nature

and subject to risks and uncertainties. Such forward- looking statements by definition involve risks, uncertainties and other factors,

which may cause the actual results, performance or achievements of mentioned company to be materially different from the

statements made herein.

COMPLIANCE PROCEDURE

Content is researched, written and reviewed on a best-effort basis. This document, article or report is written and authored by Michael

Maggi, CFA. An outsourced research services provider represented by Michael Maggi, CFA, provided Small Cap Specialists, LLC this

article or report. However, we are only human and are prone to make mistakes. If you notice any errors or omissions, please notify us

below. Small Cap Specialists, LLC and BrokerBank Securities, Inc. are not entitled to veto, interfere or alter the articles, documents or

report once created and reviewed by the outsourced research provider represented by Michael Maggi, CFA.

NO WARRANTY OR LIABILITY ASSUMED

WTSL has not compensated Small Cap Specialists, LLC, BrokerBank Securities, Inc., or Michael Maggi, CFA for the creation or

dissemination of this report. Small Cap Specialists, LLC and BrokerBank Securities, Inc., is not responsible for any error which may be

occasioned at the time of printing of this document or any error, mistake or shortcoming. Small Cap Specialists, LLC and BrokerBank

Securities, Inc. do not hold any positions in WTSL. No liability is accepted by Small Cap Specialists, LLC and BrokerBank Securities, Inc.

whatsoever for any direct, indirect or consequential loss arising from the use of this document. Small Cap Specialists, LLC and

BrokerBank Securities, Inc. expressly disclaims any fiduciary responsibility or liability for any consequences, financial or otherwise

arising from any reliance placed on the information in this document. Small Cap Specialists, LLC and BrokerBank Securities, Inc. do not

(1) guarantee the accuracy, timeliness, completeness or correct sequencing of the information, or (2) warrant any results from use of

the information. The included information is subject to change without notice.

Small Cap Specialists, LLC is the party responsible for hosting the full analyst report. BrokerBank Securities in the party responsible for

issuing the press release and Michael Maggi, CFA, is the author of research report. Small Cap Specialists, LLC has compensated Michael

Maggi, CFA two hundred dollars and fifty dollars for the right to disseminate this report. BrokerBank Securities has been compensated

one hundred dollars to issue press release by Small Cap Specialists, LLC. Information in this report is fact checked and produced on a

best efforts basis by Michael Maggi, CFA.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

9You can also read