New Hanover County Partnership Advisory Group - Meeting 2 November 13, 2019 - New Hanover Regional Medical Center

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

New Hanover County Partnership Advisory Group Meeting 2 November 13, 2019

TABLE OF CONTENTS

Section Page Number

1. Approval of Minutes 3

2. Role of Advisors to the Partnership Advisory Group 4

3. Review of Process 8

4. Overview of Healthcare Landscape 11

5. NHRMC Strategic Direction 37

6. Meeting Calendar 68

7. Meeting 3 Preparation & Closing Remarks 69

Appendix 76

2 2

APPROVAL OF MINUTES 3

ROLE OF ADVISORS TO THE

PARTNERSHIP ADVISORY GROUP

4

THE ROLE OF ADVISORS TO THE PARTNERSHIP ADVISORY

GROUP

Typical advisory functions include strategic, legal and financial support based upon

strategic opportunities being explored and the stage of the exploration process

Partnership Advisory

Group

Strategic Advisor Financial Advisor

• Provide insights on national

Legal Advisor • Develop and/or review any

healthcare & hospital business • Ensure legal and regulatory financial considerations regarding

trends, and regulatory changes guidelines are followed during chosen strategic option including

• Assist in communicating long- strategic option exploration but not limited to:

term goals/objectives of NHRMC • Lay out needed legal approvals • Capital needs

• Assess strategic opportunities and timeline of legal process • Financial position and

across the spectrum from • Assess strategic option feasibility sustainability

remaining independent to based upon NHRMC structure • Financial projections

partnership arrangements and national/regional laws and • Fair market value

• Determine next steps in regulations

successfully executing NHRMC • Develop and review any legal

best-fit strategic opportunity contracts related to strategic

opportunity exploration

5 5

POTENTIAL SCOPE OF SERVICES FOR FINANCIAL ADVISOR

Prior to RFP Evaluation RFP Evaluation After Evaluation

- Fairness opinion

- Financial - Comparative

components of analysis of financial - Financial due

current state and components of diligence during

internal restructuring narrowed list of negotiations

review respondents

6 6

TIMELINE FOR FINANCIAL ADVISOR RFP

PAG Make

County/NHRMC County/NHRMC

County/NHRMC Selection

Receive Narrow List

Send FA RFP Week of

Responses Week of

November 15th December

December 2nd December 13th

16th

7 7

REVIEW OF PROCESS 8

PARTNERSHIP ADVISORY GROUP PROCESS

PHASE I PROPOSED CONTENT FOR MEETINGS

Charter Task #1 Education Charter Task #1 Education Charter Task #2 Partnership

Process Overview and Healthcare Industry Initial Goals & Objectives

Background Education and RFP Candidates

• Education Recap

• Introduction to PAG • Overview of healthcare landscape

• Discuss goals and objectives

• Introduction to NHRMC and New • NHRMC education (G&O) for NHRMC’s future and

Hanover County • PAG Process legally mandated G&O (131e)

• Overview of process and PAG

• Review list of organizations

charter

requesting RFP

Goal: PAG members understand Goal: PAG members understand • Discuss other potential partners

responsibilities, legal process, and current state of NHRMC and Goal: Develop preliminary G&O and

current state of NHRMC implications of industry trends list of prospective partners

Charter Task #2 Partnership Charter Task #3 Partnership Charter Task #4 Strategic Options

Final Goals & Objectives and Final RFP and Identification Initial Results of Strategic

Initial RFP Development of Participating Parties Options Assessment

• Review refined goals & objectives • Review refined request for • Discuss approach for Strategic

(G&O) based upon prior meeting proposal (RFP) based upon prior Options Assessment

and public hearing meeting’s feedback • Review NHRMC current strategic

• Discuss request for proposal • Assess updated list of interested plan against NHRMC achieving

(RFP) outline parties and other potential G&O (gap analysis)

strategic partners to receive RFP

Goal: Identify gaps between current

Goal: Finalize G&O and develop RFP Goal: Finalize RFP and list of strategic plan and G&O and provide

and participation criteria prospective partners for outreach opportunity for PAG questions

9 9

PARTNERSHIP ADVISORY GROUP PROCESS

PHASE I PROPOSED CONTENT FOR MEETINGS

Charter Task #4 Strategic Options Charter Task #5 Partnership Charter Task #5 Partnership

Refined Strategic Options Initial Review of RFP RFP Follow-Up Discussions

Assessment Responses and Selected Partner List

• Address PAG questions on • Review summarized RFP • Address RFP follow-up questions

Strategic Options Assessment responses and provide forum for identified in prior meeting

results from prior meeting PAG questions on responses • Review list of selected partners

• Identify solutions / investments to • Review RFP evaluation process resulting from RFP evaluation

be prioritized in RFP responses in connection to Strategic Option process defined in prior meeting

based upon results of gap analysis Assessment from prior meeting

Goal: Finalize Strategic Options Goal: Assess PAG questions on

Assessment and RFP evaluation RFP responses. Identify RFP follow- Goal: Align on selected partner list

priorities up questions based upon RFP response evaluation

Charter Task #7 Decision

Charter Task #6 Partnership

Remain Independent

Finalized Partner List for PAG Vote on

Begin development of go

Strategic Options Recommendation

forward plan to support the

• Review standalone option

• Further assess RFP responses of option to remain independent

compared to finalist partner

selected partners identified in

options

prior meeting

• Conduct vote to determine go

• Narrow selected partner list to

forward decision of remaining

identify finalists for comparison to Pursue Partnership

standalone or further assessing

stand alone options

identified partnership options with Negotiate a Letter of Intent and

LOI commence more detailed due

Goal: Finalize partner list being Goal: Finalize decision determining

considered for strategic options selected strategic option and outline diligence

key LOI expectations

1010OVERVIEW OF HEALTHCARE

LANDSCAPE

11NAVIGANT IS A NATIONALLY RECOGNIZED HEALTHCARE

CONSULTING FIRM, AND HAS PARTNERED WITH NHRMC SINCE 2004

CONSULTING

WHO WE ARE:

600+

#3

ON MODERN

PROFESSIONALS HEALTHCARE’S

LARGEST HEALTHCARE

MANAGEMENT

A MULTIDISCIPLINARY TEAM CONSULTING FIRMS

CLINICIANS FORMER GOVERNMENT LEADERS

DATA ANALYSTS FORMER INDUSTRY EXECS

KLAS 2018

Seen as strategic,

experienced, and

WHAT WE DO: • STRATEGIC ADVISORY capable of producing

• TRANSACTION ADVISORY results on time.

• OPERATIONAL IMPROVEMENT

• GOVERNMENT HEALTHCARE SOLUTIONS

DELIVERED TO: PROVIDERS AND PAYERS

ACADEMIC

HOSPITALS MEDICAL GROUPS PAYERS

HEALTH SYSTEMS

PARTNERING WITH NHRMC

ON ITS STRATEGIC PLAN

SINCE 2004

12 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDNAVIGANT IS NOW A GUIDEHOUSE COMPANY

HEALTHCARE EXPERTISE AND FEDERAL, STATE, AND LOCAL

SOLUTIONS GOVERNMENT EXPERIENCE

• STRATEGIC ADVISORY

• TRANSACTIONS

• REVENUE CYCLE

• PERFORMANCE IMPROVEMENT

13 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDGOALS FOR THIS SESSION

1. Increase familiarity with

hospital terminology and Modern Healthcare, March 2018

critical drivers of economic

success “Earlier this month, Ascension’s* Board of

Directors unanimously endorsed its new

2. Identify key macroeconomic "advanced strategic direction," CEO Tersigni

pressures facing not only told his employees, as it faces

NHRMC but other hospitals dwindling reimbursement from government

across the country and commercial payers;

3. Understand the impact that growing regulatory complexity;

each macroeconomic skyrocketing pharmaceutical costs;

pressure has on NHRMC’s shifting from inpatient to outpatient care;

ability to provide from fee-for-service to value-based care;

exceptional care for its and increasing competition.”

patients now and in the

future

*Ascension Health is the largest not-for-profit health

system in the country, with over 2,600 sites of care

in 23 states, including 151 hospitals

Source: (1) Modern Healthcare.

14 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHEALTHCARE IS GROWING AND CHANGING, PRESENTING MULTIPLE

CHALLENGES TO HEALTHCARE PROVIDERS

1 HEALTHCARE PROVIDERS ARE RECEIVING FEWER PAYMENTS FOR SERVICES

• Federal and state governments are the largest payers of hospital care, and will continue to be as

the population ages

• Governmental payers reimburse hospitals less than private payers

2 HEALTHCARE PROVIDERS ARE UNDER INCREASING REGULATORY SCRUTINY

• Hospitals have been pushed into the regulatory spotlight, with a range of regulations

3 PAYERS DRIVING SHIFT FROM FEE-FOR-SERVICE TO VALUE-BASED CARE

• Private payers are changing how they purchase care, increasingly driving value-based

arrangements and shifting costs to employees

4 DELIVERY OF CARE SHIFTING FROM INPATIENT TO OUTPATIENT SETTING

• Patients are using healthcare services differently, demanding lower costs, greater accessibility to

care, higher quality

5 IN RESPONSE TO THESE CHALLENGES, PROVIDERS HAVE INCREASED COLLABORATION

• Consolidation with other hospitals provide economies of scale and skill; greater capital pool

• Employment of physicians and alignment with physician groups (ACOs, CINs)

• Vertical affiliation with payers (narrow networks and value-based payments)

• Experimenting with innovative partnerships and restructuring of operating model

15 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHEALTHCARE CONSUMES A GROWING PORTION OF THE

COUNTRY’S GDP

Healthcare expenditures comprise 18% of the country’s GDP and have increased every year – even

during recession years – averaging 6% growth each year since 1995

Healthcare Expenditures as a Percentage of U.S. GDP

1995-2016

20%

17.9%

18% 17.3%

16% 15.4%

13.9%

14% 13.3%

12%

10%

2008

2015

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2009

2010

2011

2012

2013

2014

2016

Source: American Hospital Association, Chartbook 2018

16 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDTHE LARGEST CATEGORY OF HEALTHCARE EXPENDITURES ARE

HOSPITAL CARE AND PHYSICIAN SERVICES

Hospital Care and Physician Services comprise over half of national healthcare expenditures

National Healthcare Expenditures by Category

2016

Hospital Care

Hospital Care • Services provided in an inpatient setting by or under the

34% supervision of physicians, including medical, surgical, or

diagnostic treatment

Physician Services

Physician Services • Services provided by an individual licensed under state

21% law to practice medicine

Other

Other • Dental and non-physician professional services including

35% home health, nursing home care, some medical

equipment, etc.

Prescription Drugs

Prescription Drugs

10% • Pharmaceuticals requiring a medical prescription

2016

Source: (1) AHA Chartbook 2018.

17 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDAS PROVIDERS OF CARE, HOSPITALS AND PHYSICIANS ARE ONE

PART OF THE HEALTHCARE INDUSTRY STRUCTURE

Providers

• Deliver medical care to patients

Patients • Hospitals submit claims to

insurers for the cost to provide

medical care to patients in

facilities

• Physicians submit a separate

claim to insurers for the cost of

their services

Patients

• Consumers purchase health

insurance from payer through an

Exchange or an employer

Pharma /

Biotech

Providers Payers

(e.g. Hospitals,

Physicians) • Private health insurers (e.g.

Aetna, BCBS, United) sell plans

to consumers/patients

• Governmental payers (Medicare,

Medicaid) cover enrolled

Payers beneficiaries

(e.g. insurance companies, • Insurers pay providers for care

delivery, based on claims

Medicare, Medicaid)

submitted by providers – Fee For

Service

Source: (1) Centers for Medicare and Medicaid Services (CMS)

18 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDOVER TIME, GOVERNMENTAL PAYERS HAVE BECOME THE LARGEST

HOSPITAL PAYER WHILE REIMBURSING LESS THAN PRIVATE PAYERS

Governmental payers comprise over 60% of hospital costs, but do not pay rates necessary for

hospitals to break-even

Distribution of Hospital Cost by Payer Type Payment to Cost Ratios by Payer

1980-2016 2016

Hospital Break-even

10% 8%

14%

Private Payers 145%

33%

39%

42%

19% Medicaid 88%

13%

10%

38% 41%

35% Medicare 87%

1980 2000 2016 0% 50% 100% 150%

Medicare Medicaid Private Payers Other Payment to Cost Ratio (%)

Source: (1) AHA Chartbook 2018.

19 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHOSPITAL PAYMENTS FROM GOVERNMENTAL PAYERS HAVE

DWINDLED OVER THE PAST 20 YEARS

Declines in payments from governmental payers has put pressure on hospital contracts with private

payers to cross-subsidize costs

Hospital Payment-to-Cost Ratios by Payer Type

1995-2016

160%

149%

145%

140%

124%

120%

Hospital

104% Break-

99% even

100%

87%

94%

80%

60%

1998

2013

1995

1996

1997

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2014

2015

2016

Medicare Medicaid Private Payers

Source: American Hospital Association, Chartbook 2018

20 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDTHE INCREASING COST BURDEN ON GOVERNMENTAL PAYERS HAS

PUSHED HOSPITALS INTO THE REGULATORY SPOTLIGHT

Regulation Impact on Hospitals

Certificate of Need State regulations adopted in the 1970s designed to limit the number

(CON) and capacity of healthcare facilities (e.g. inpatient beds in hospitals)

and thus prevent excess capacity and cost inflation

Stark Law A set of federal laws which prohibit physicians from “self-referring” –

sending patients to facilities or services in which the physician or closely

related family has a financial interest

Federal Medicare Overhauled Medicare and introduced Medicare Advantage; adjusted

Modernization Act of Medicare’s hospital payment system; increased prescription drug

2003 access through Medicare Part D; introduced health savings accounts

Patient Protection Expanded patient health insurance coverage while proposing to reduce

and Affordable Care $43 billion in total funding to hospitals for uncompensated care

Act (PPACA) of 2010 between 2018 and 2025; directed Medicare to shift hospital payment

method toward value-based arrangements

Florida 2011 and 2012 In 2011, Florida reduced hospital payments by $750 million, cutting

Budgets hospital payments by 12% and eliminating price increases; in 2012

State reduced hospital payments by another 6%

Illinois SMART Act of Reduced Illinois Medicaid spending by $1.6 billion, including $240m in

2012 provider rate cuts

Source: (1) Becker’s Hospital Review; (2) US National Library of Medicine – National Institutes of Health; (3) Modern Healthcare; (4) Illinois General Assembly; (5) Florida State Budget.

21 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDRECENT AND PENDING REGULATIONS ALSO WEIGH ON HOSPITAL

AND PHYSICIAN PAYMENTS

Regulation Implication

• CMS reduced reimbursement of certain 340B Program Drugs from the average sales

price (“ASP”) plus 6% to the ASP minus 22.5% for 2018 and 2019

• Ongoing litigation from parties such as the American Hospital Association are

340B Pharmacy challenging these rate reductions and pushing for remedial measures

• Hospitals eligible for the 340B program face significant declines in reimbursements

if legislation is repealed or weakened

• Doctors, hospitals, and other clinicians will need to structure and negotiate contracts

to treat Medicaid population approximately 18% of NC population

• Five managed-care groups to receive $6 billion in annual Medicaid contracts moving

North Carolina

1.6 million people to managed-care with approximately 565,000 Medicaid patients

Managed Medicaid transitioning on November 1

• Medicaid Reform has potential to have a negative financial impact on North Carolina

hospitals

• Estimated to decrease Medicare spending on physician services by approximately

$35 to $106 Billion (-2.3 to -7.1%) over 15 years

Medicare Access and • Merit Based Incentive Payment System (MIPS)- Most participants will be required to

CHIP Reauthorization direct resources and report up to 6 quality measures

Act (MACRA) • Advanced Alternative Payment Models (APMs)- Participants receive 5% bonus and

other rewards to drive adoptions of Advanced APMs with stricter governance criteria,

performance metrics, and risk sharing

Source: (1) North Carolina Health News; (2) North Carolina Government; (3) NHRMC Website; (4) Policymed.com.

22 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDPAYERS ARE CHANGING HOW THEY PURCHASE CARE, SHIFTING TO

VALUE-BASED PAYMENTS THAT PRESS PROVIDERS TO ASSUME RISK

Pre-Admission

Hospital Payments by Type

Separate 2015-2018

payments for Services

each service

Inpatient

Services

Fee-For-

Doctor

Service

Services

Fee for Service

Post-Acute

Defined

Costs

payment

algorithms Readmissions 66% 64%

71%

77%

Pre-Admission

One payment to

Services

cover all services

for a patient Inpatient

Value Based

Payments

Services

Value-

Based Doctor 34% 36%

29%

Payment Services 23%

Hospital Post-Acute

Costs

assumes

risk Readmissions 2015 2016 2017 2018

*Fee for Service includes pay-for-performance

Source: (1) Health Care Payment Learning & Action Network (LAN) APM Measurement Effort Infographic 2016-2019.

23 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDAS AN EXAMPLE, BCBS OF NC RECENTLY LAUNCHED BLUE

PREMIER EARLIER THIS YEAR

BCBS of NC is committed to having all customers covered under Blue Premier’s

value-based care contracts within 5 years

Blue Premier is a statewide Blue Cross and Blue Shield of North Carolina (BCBS of NC) program

announced January 11, 2019 that plans to tackle 3 critical areas:

Changing how they pay for care: participating systems will share in cost savings if they meet

patient health benchmarks and share in the losses if they fall short

Putting primary care first: collaborating with Aledade to support 100s of independent primary

care physician clinics and physician-led Accountable Care Organizations (ACOs). Through ACO

arrangements, physicians will have access to technology and data analytics tools as well as a

more comprehensive view of their patients’ total cost of care, gaps in care and their experiences

throughout the care continuum

Integrate mental and behavioral health: better integrate behavioral and mental health into

primary care for more holistic, patient-centered care

The following five health systems and their ACOs have joined BCBS of NC Blue Premier program:

Source: (1) CMS; (2) BCBS NC; (3) The News & Observer.

24 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDIN ADDITION, PAYERS ARE SHIFTING A GREATER SHARE OF

HEALTHCARE COSTS TO EMPLOYEES THROUGH DIFFERENT PLANS

As employers continue shifting to high-deductible plans, employees increase their burden of costs

Average Annual Health Insurance Premiums -

Percentage of High-Deductible Health Plans

Employee Contributions

30% $6,015

$4,823

20%

$3,515

8%

2009 2014 2019 2009 2014 2019

Source: (1) Kaiser Family Foundation “2019 Employer Health Benefits Survey”

25 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHOSPITALS HAVE SHIFTED DELIVERY OF CARE AWAY FROM

INPATIENT SETTINGS BY STRENGTHENING AMBULATORY SETTINGS

As volumes shift away from the inpatient setting, health systems are expanding their reach to all

aspects of the “care continuum”, though this often requires new investments

Inpatient Admissions per 1,000 People

1995-2017

130

125

120

115

110

105

100

95

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

Total Outpatient Visits (millions)

1995-2016

800

700

600

500

400

300

200

100

0

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Source: (1) AHA Chartbook 2018; (2) Becker’s Hospital Review.

26 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDTHIS CREATES A CHALLENGE FOR SYSTEMS AS OUTPATIENT

REVENUE PER UNIT IS MUCH LESS THAN INPATIENT

Financially, it takes nearly 50 new outpatient visits to replace one inpatient admission

Distribution of Hospital Revenues (IP/OP) Average Cost by Setting

1995-2016 2017

52%

Inpatient

Inpatient $22,543

48%

Outpatient

Outpatient $478

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: (1) AHA Chartbook 2018; (2) The Institute for Health Metrics and Evaluation.

27 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHOW HAVE HEALTHCARE PROVIDERS ADAPTED?

• Healthcare providers have shifted patient care from traditional, higher-

cost hospital settings to lower-cost outpatient facilities where clinically

Managing appropriate

Settings of

• Healthcare have expanded footprint of facilities & services beyond

Care

hospital campus, providing patient-focused, seamless and high-quality

care

Embracing • Healthcare providers have increasingly formed accountable care

Changes to organizations (ACOs) and clinically integrated networks (CINs) with

Payment physician partners to participate in federal value-based contracts

Models • Healthcare providers have participated in value-based contracts with

private payers

• Many healthcare providers have sought to partner or merge with other

hospitals to gain economies of scale & skill, reduce expenses, and to

Consolidation

access capital for equipment/technology required to comply with recent

+ =

regulations

• Healthcare providers have strengthened affiliations with physician

partners, with a trend toward employing physicians (specialists as

Vertical well as PCPs)

Affiliation • Some healthcare providers have created provider-sponsored health

plans to better control hospital payments, others have increased

participation in “narrow networks”

• A few healthcare providers have experimented with new partnerships

Innovation and organizational arrangements beyond traditional hospital

services to provide better access, quality, and patient satisfaction

28 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHEALTHCARE PROVIDERS HAVE INCREASINGLY FORMED ACOS

WITH PHYSICIAN PARTNERS TO PARTICIPATE IN NEW PAYMENT

ARRANGEMENTS

Number of Accountable Care Organizations (ACOs)

2011-2017 What is an ACO?

1,000 ACOs are groups of doctors,

923

hospitals, and other health care

900 835 providers, who come together

800 voluntarily to coordinate high-quality

Number of ACOs

734

care for their patients. Hospitals

700 typically anchor an ACO.

613

600

The group seeks to coordinate care

500 440 to ensure that patients get the right

care at the right time, streamlining

400 services and preventing medical

300 errors.

200 168

ACOs collectively negotiate

58 contracts with payers to share in

100

cost savings, receiving a payment

0 when it succeeds both in delivering

2012

2011

2013

2014

2015

2016

2017

high-quality care and spending health

care dollars efficiently.

Source: (1) HealthAffairs “Recent Progress in the Value Journey” - reflects Q1 counts.

29 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHOSPITALS HAVE CONTINUED TO SEEK PARTNERSHIPS WITH

PEERS THROUGH HORIZONTAL CONSOLIDATION

Many hospitals have sought to partner or merge with other hospitals to gain economies of scale, to

gain economies of skill, to reduce expenses, and to access capital for equipment/technology

Percent of Community Hospitals in Hospital Systems

1999-2016

80%

% of Total Community Hospitals

Partnerships Continue to Expand

67%

70% Ascension • Today: 151 hospitals

• 2015: 141 hospitals

• 2010: 69 hospitals

60%

51% 3,200 Common • Today: 142 hospitals

hospitals Spirit • 2015: 144 hospitals

50% (CHI + Dignity • 2010: 115 hospitals

Health)

2,500

40% hospitals Premier Inc. • Today: over 4,000

(Group member hospitals

Purchasing • 2015: 3,400 members

30% Organization)

• 2010: 2,300 members

20%

2004

1999

2000

2001

2002

2003

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: (1) AHA Trendwatch Chartbook 2018; (2) Ascension audited financial statements; (3) Organization Webpages; (4) Elsevier.com; (5) HealthAffairs.org.

30 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHOSPITALS ARE ALSO INTEGRATING WITH PHYSICIANS PARTNERS

THROUGH INCREASED EMPLOYMENT

Hospitals have been increasingly employing physicians and acquiring physician practices to manage

a greater scope of services for patients

Percent of Physicians Employed and Practices Owned by Hospitals

2013-2018

50%

43% 44%

45% 41%

40% 36%

35% 30%

% of Total

30% 27%

30% 30% 31%

25%

20% 24%

15%

17%

10% 15%

5%

0%

2013

2014

2015

2016

2017

2018

% Physicians Employed % Practices Owned

Source: (1) Physician Advocacy Institute Physician Practice Acquisition Study 2012-2018.

31 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDINCREASED VERTICAL CONSOLIDATION / AFFILIATION IS ALSO

TAKING PLACE AS PAYERS AND PROVIDERS JOIN TOGETHER

Providers Payers

Health

Systems

Retail /

Urgent Care

Post Acute

Pharmacies

Physician Groups

M&A Other Affiliations / Relationships Same Entity

32 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHEALTH SYSTEMS ARE ALSO EXPERIMENTING WITH INNOVATION IN

DIFFERENT ARENAS

Patient Experience Care Effectiveness Social Determinants of Health

POC Survey Alluceo Fresh Food Farmacy

POC gathering tool collects consistent and standardized Care platform with connectivity to interdisciplinary mental Patients with HBA1C levels greater than 8 and identified

data on patient concerns and triggers remediation actions health team including family members as being food insecure are given a referral to access

in real time across Baylor Scott & White’s 49 hospitals healthy foods at the Farmacy

Extensivists

KP Health Connect Dedicated physician resource across inpatient episode and

post-hospitalization period to ensure a return to health CAPABLE

Patient portal with care delivery support, ancillary services

connection, health plan administration connectivity shown

to improve preventive screening rates and chronic care

Bravemind CAPABLE provides RN, Occupational Therapy, and

home improvement services to keep seniors safe at

Virtual reality (VR) based therapy for PTSD treatment home.

Our Care Wishes Sensely Partnership

Online platform to streamline the documentation of

Programmed triage protocols on Sensely

advance directives. Platform may eventually link to EHR

avatar to identify appropriate level of care

Labor & Supply Optimization Workflow Efficiency Access

Overseas Call Center Surgical Schedule Appointment Pass

Optimization Creates efficiency in the appointment check in process by

Overseas call centers in Israel and the Philippines staffed Block Scheduling Optimization (BSO) tool prevents high providing patients with a QR code that can be scanned at

with U.S. licensed nurses to address patient questions inpatient census days and optimizes use of operating rooms check in kiosks to verify demographics, pay copays, verify

and surgical robots insurance eligibility, and sign documents

Cost-Guiding Labels Home Telehealth

Command Center Home Telehealth program monitors 160 patients per

Reduced cardiac cath lab costs by implementing cost-

Operational command center that aggregates hospital month in their homes following a hospitalization to reduce

guiding labels for supplies, saving $990,000 annually

wide data in real time and leverages predictive readmits

analytics and AI to optimize throughput

eTrak VIP 360

Inova’s Concierge Medicine program provides patients

Leverages RFID tags to track mobile medical equipment with 24/7 access to care for a upfront membership fee

Source: (1) Organization Webpages; (2) Press Ganey; (3) PR Newswire; (4) Health Leaders Media.

33 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDAS NEW ENTRANTS AND TECHNOLOGY DISRUPT EXISTING

HEALTHCARE INFRASTRUCTURE, NEW MODELS EMERGE

• Established healthcare companies

expanding into adjacent

businesses (e.g., Aetna/CVS,

Optum/DaVita/WellMed, etc.) • Increased Standardization

• Large organizations directly and Efficiency (e.g., systems

offering healthcare solutions,

New

have been successful with

(Apple, Amazon / JP Morgan Chase / Entrants standardization of back-office;

Berkshire Hathaway, Verizon, Microsoft, New and with investments in IT,

etc.) physicians, and managed care)

Opportunities

• Digital health startups entering the

fray backed by significant venture for Current

capital Models

• New Configurations (e.g.,

• Next generation analytics Emerging UnitedHealthcare is now the

capabilities (e.g., big-data, predictive Healthcare largest employer of physicians.

modeling, AI) applied across clinical, social, The MA value chain looks very

behavioral and financial domains Models

different than the traditional

• The promise of “anytime, anywhere Medicare one)

access” enabled by emerging New • New Models (e.g., OneMedical -

technologies (e.g., Blockchain, Cloud Technology tech-enabled concierge primary

computing, Connected Devices, IOT) care company)

driving increased portability

• Repeatable tasks being eliminated to drive

greater productivity (e.g., workflow

automation)

34 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDTECHNOLOGY WILL CONTINUE TO CHANGE CARE DELIVERY BUT

REQUIRES FURTHER INVESTMENT AND RESEARCH

Telehealth Consumerism

• Over 70% of consumers prefer use of video • 65% of commercial insurance respondents

over visiting their primary care provider in-person considered cost a top factor when seeking care

• Accounted for approximately $22 billion in 2017 • Increasing amounts of patients using online

and it is expected to account for approximately resources to evaluate treatment options

$93.5 billion by 2026 including online reviews, ratings, and pricing

Artificial Intelligence (AI) Wearables

• Public and private sector investment in • Less than 25% (approximately 1,800) of all U.S.

healthcare AI expected to reach $6.6 billion hospitals using mobile applications

by 2021 • Wearable market projected to reach $12.1

• AI applications projected to drive annual billion by 2021 with remote monitoring

savings of $150 billion by 2026 growing to $31.3 billion by 2023

Source: (1) Definitive Healthcare

35 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDHEALTHCARE IS GROWING AND CHANGING, PRESENTING MULTIPLE

CHALLENGES TO HEALTHCARE PROVIDERS

1 HEALTHCARE PROVIDERS ARE RECEIVING FEWER PAYMENTS FOR SERVICES

• Federal and state governments are the largest payers of hospital care, and will continue to be as

the population ages

• Governmental payers reimburse hospitals less than private payers

2 HEALTHCARE PROVIDERS ARE UNDER INCREASING REGULATORY SCRUTINY

• Hospitals have been pushed into the regulatory spotlight, with a range of regulations

3 PAYERS DRIVING SHIFT FROM FEE-FOR-SERVICE TO VALUE-BASED CARE

• Private payers are changing how they purchase care, increasingly driving value-based

arrangements and shifting costs to employees

4 DELIVERY OF CARE SHIFTING FROM INPATIENT TO OUTPATIENT SETTING

• Patients are using healthcare services differently, demanding lower costs, greater accessibility to

care, higher quality

5 IN RESPONSE TO THESE CHALLENGES, PROVIDERS HAVE INCREASED COLLABORATION

• Consolidation with other hospitals provide economies of scale and skill; greater capital pool

• Employment of physicians and alignment with physician groups (ACOs, CINs)

• Vertical affiliation with payers (narrow networks and value-based payments)

• Experimenting with innovative partnerships and restructuring of operating model

36 / ©2019 NAVIGANT CONSULTING, INC. A GUIDEHOUSE COMPANY. ALL RIGHTS RESERVEDNHRMC STRATEGIC DIRECTION 37

OUR AMBITION NHRMC MISSION, VISION, AND VALUES Our Mission… Leading Our Community to Outstanding Health Vision for the Future… NHRMC is an industry leader in a new era of healthcare delivery. Our thriving community serves as a national model of achieving excellence for all. We are committed to: • Fostering a culture of transformation through empowerment, innovation, and inclusivity. • Delivering exceptional quality, affordability, and personalized experiences throughout the wellness continuum. • Advancing health and vitality for all through a community integrated model of collaboration. • Cultivating a diverse and extraordinary workforce dedicated to our mission. And Values… Ownership, Teamwork, Communication, Compassion Source: NHRMC Website and Data 3838

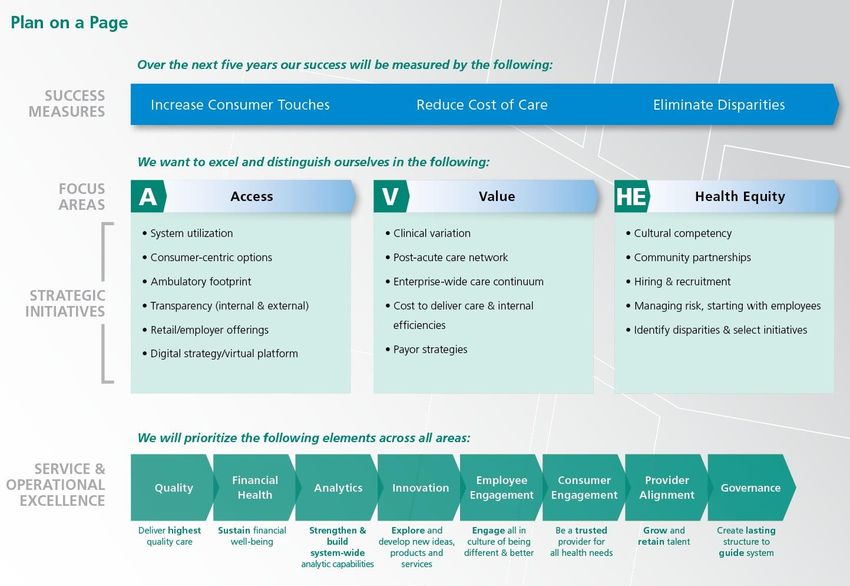

NHRMC STRATEGIC PLAN ON A PAGE MAJOR DEVELOPMENT EFFORTS: ACCESS, VALUE, HEALTH EQUITY 3939

SUMMARY OF CHALLENGES INDUSTRY AND LOCAL ➢ Need to shift business model to be ready for value-based reimbursements ➢ Timing of shift is uncertain ➢ Rapidly growing and aging population in SE NC with more intense health care needs ➢ Behavioral health (including opioid crisis) a prominent health need ➢ Care coordination, preventative and sick care, across urban and rural settings ➢ National shortage of nurses and physicians ➢ New competitors entering health care market, with substantial financial backing 4040

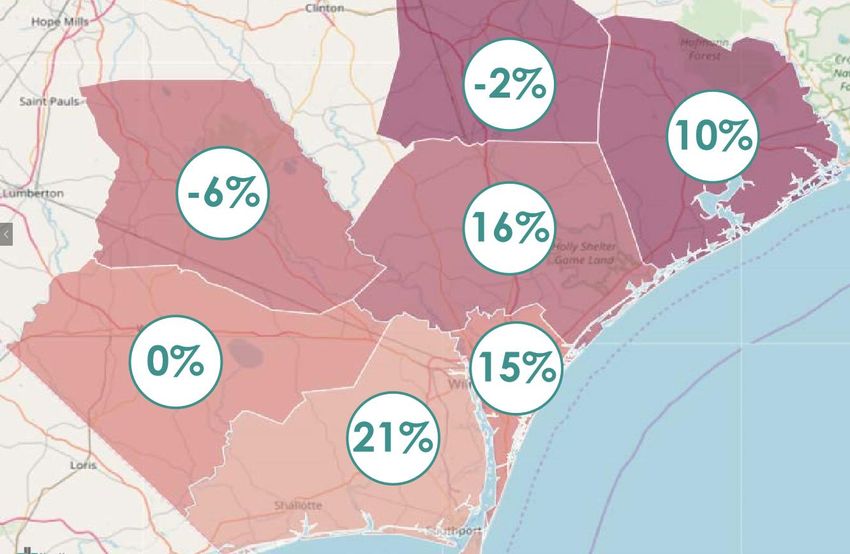

NHRMC MARKET FORCES

GROWING & AGING POPULATION

Historical Market Population Growth Projected Market Growth Projections

(2010-2018) (2017-2030)

Population Over age 65

(% Change) (% Change)

24% INPATIENT

New Hanover

14.6% 17.7%

County

Pender County 19.1% 18.0%

Brunswick

County

27.3% 31.5% 48% OUTPATIENT

North Carolina 8.9% 16.3%

EMERGENCY

54% DEPARTMENT

Source: U.S. Census Bureau

4141VOLUME DEMANDS

OCCUPANCY RATES AT 17TH STREET MAIN TOWER

Average Occupancy Rate By Unit

Ppt. Change

FY14 FY19 FY14-FY19

Adult Surgery (2) 85.1% 95.4% 10.3% Case Mix Index

Increased 10.3%

Nephrology (3) 88.8% 95.7% 6.9% 5 years

Neuro/Surgery (4) 85.6% 94.7% 9.1%

Medical (5) 92.1% 95.1% 3.0%

Hospitalists (6) 94.3% 91.3% (-3.0%)

PCU/Stoke (7) 89.5% 91.7% 2.3% Average Length

of Stay

Cardiac Med Tele (8) 84.8% 95.1% 10.3%

Increased 7.8%

Cardiac Med/Surg Tele (9) 74.5% 90.5% 16.0% 5 years

Pulmonology/Oncology (10) 88.6% 89.9% 1.3%

Average Occupancy

North Carolina Urban Hospitals 67%

4242ACCESS

AFFORDABLE CARE THAT IS EASILY ACCESSIBLE

Access

Patient will have reliable Access Goals:

• System utilization: patients receive the right service in the

access to information and right location at the right time

services in an environment • Consumer centric options: establish our system as

where the patient is the driver; consumer focused where people can learn, engage, and easily

transact their healthcare and/or wellness needs; whether it is in

the patient is empowered; the person, online or mobile

patient can receive the right • Ambulatory / facility footprint: to meet consumer

service in the right place at the expectation of quality health and wellness services that are

convenient, readily available, affordable, cost-effective, and

right time; there are multiple accessible

points of entry; the system is • Transparency: cost and quality data is available to our

internal consumers and external customers that is accessible,

price conscious, innovative, reliable, understandable, meaningful, concurrent, actionable,

transparent, proactive, and provided with context and benchmarks

collaborative, and understands • Retail / employer offerings: increase access to NHRMC

services through employer offerings and retail strategies using

the consumer mind-set innovative customer-focused developments

• Digital strategy / virtual platform: promote wellness,

improve internal efficiencies, and explore new lines of business

4343ACCESS

AMBULATORY STRATEGY

Imperative to place

Projected Population Growth By County

services to align with,

(2017-2030)

Population Duplin

growth Onslow

Bladen

Shift from

inpatient to

outpatient Pender

Columbus

Consumer Wilmington

preferences

Brunswick

4444ACCESS

FACILITY PRIORITIES

Position NHRMC main campus to be focused on

highest acuity care

NHRMC needs to move from - Centralize higher acuity care on main campus,

hub-and-spoke model centered consider moving lower acuity services to other

locations

on 17th Street campus to a - Accommodate growth in cardiovascular and

matrix model emphasizing care neurosciences

closer to home with all sites of - Ensure sufficient parking for patients

service interconnected through Offer care options that are convenient to access

- Grow services on Scotts Hill site and in other

digital strategies population-dense hubs throughout service area.

Facilities throughout are would range from advanced

ambulatory offerings to full-service community

hospitals.

- Fit to purpose Pender Memorial, Rehabilitation and

Behavioral Health hospitals

- Provide digital options

TODAY TOMORROW - Build emergency department to replace Orthopedic

Hub-and-Spoke Matrix Model Hospital ED

- Support growth of provider network in needed areas

including primary care

Ensure patients are cared for in highest quality, lowest

cost site of service for their clinical needs

4545ACCESS

FACILITY STRATEGY EVALUATION

Recent evaluation of facility plan asked

“What if we”:

• Accelerate growth of cardiovascular

and neurosciences centers at NHRMC

• Save millions of capital dollars

• Build orthopedic services in a more

accessible location, keeping outpatient

& inpatient together

Change in plan to:

• Make new patient tower Heart &

Vascular Hospital

• Expand neurosciences in existing Even with this likely pivot, $1B+ master

space facility plan required to meet region’s

• Make orthopedics anchor of new health needs over next 10-15 years

hospital in Scotts Hill

4646ACCESS

SYSTEM UTILIZATION

Manage current volume through operational Telehealth – NHRMC Home Care

improvements: • Manage patients with chronic conditions

• Care coordination (congestive heart failure, high blood pressure,

• Multidisciplinary rounds COPD or emphysema)

• Digital standardization • First year:

• Real-time location tracking system • 223 patients, 159 of whom had prior

hospitalizations

• Of those 159, only nine were readmitted for

congestive heart failure within 30 days, one-

third the rate for similar patients who were

readmitted in 2013

• Earned Critical Access Hospital Recognition by

The National Rural Health Resource Center for

Innovation

Desire to grow telehealth, but current

reimbursement environment creates

barriers for infrastructure investment

4747ACCESS

DIGITAL PLATFORM & CONSUMER-CENTRIC FOCUS

NHRMC App with interior, exterior wayfinding

Enhanced consumer functions:

• E-visits

• “Reserve my spot” for NHRMC ExpressCare

• E-Check in Future: Customer Relationship Management (CRM)

• Direct scheduling platform

Future: Price estimator for common

scheduled procedures

Growing the digital platform requires

investment to procure and install new

technology

4848VALUE

RELIABLE, HIGH QUALITY CARE DELIVERED COST EFFICIENTLY

Value

To deliver value throughout Value Goals:

• Clinical excellence: transform care delivery system by

the NHRMC system by eliminating unnecessary variation, establishing a system to

decreasing clinical variation, evaluate, implement, monitor and maintain evidence-based

standards of care to improve outcomes and reduce costs

increasing care coordination

• Post-acute care network: Create a post-acute care network

(both inpatient and allowing acute care admission to have seamless transfers of

ambulatory), using evidence- care between levels

based medicine, cost • Cost to deliver care & internal efficiencies: right care, right

time, right place; standardized pathways that allow for outlier

accounting, increasing variation; reliable, accurate data; etc.

covered lives, transparency • ACO / population health / PQP initiative: successfully drive

quality performance across the ambulatory network; Ensure

(both internally and patients receive appropriate assistance with care transitions;

externally), and provider Educate providers and ensure appropriate risk adjustment;

Evaluate and Implement value-based contracting programs

engagement

• payer strategies: seek opportunities to build capabilities to

take on more risk and move upstream on premium dollar

4949VALUE

CLINICAL EXCELLENCE

First Year Impact

• Reduced ED dental pain return visits from

8.45% to 3.48%

• Reduced length of stay for spine surgery

cases saving 190 days

• Reduced unnecessary blood transfusions by

864 units of blood, avoiding 9 complications

and saving $386,208

Outcome Examples Cost Examples • Increased use of CHF evidence-based order

Mortality

sets from 47% to 98%

Supply Costs

• Reduced cost of care for CHF patients saving

Readmissions Pharmaceuticals $692,333

Infections Over / Under Utilization • Improved appropriate use & cost efficiency for

spine braces saving $129,886

Functional Status LOS Reduction • Improved appropriate use of Acetaminophen

Morbidity saving $242,683 in 6 months

• In 3 months, Transitions Clinic has prevented

Patient Experience

15 readmissions

Advanced analytics requiring significant investment (personnel and

platforms) can accelerate quality improvement and cost reduction

5050VALUE

ACCOUNTABLE CARE

Physician Quality Partners serves as NHRMC’s ACO Physician Quality Partners –

ACO Program Performance

Medicare Shared Savings Program designed to move

system away from volume and toward value and 406 18,951 34

outcomes. Offers providers the opportunity to create an Providers Covered Lives Practices

Accountable Care Organization (ACO) for an assigned

Medicare population 95.12%

An ACO is measured across three key metrics: Quality Score (2018)

(highest available merit-based incentive,

two consecutive years)

Quality

Cost $282

Reduction in Cost of Care

Experience of Care per Beneficiary (2018)

(national average $180)

NHRMC’s ACO has successfully driven value, but $2.5 M

greater expertise, scale & investment are required Earned Shared Savings (2018)

to continue to develop population health

capabilities $5.3 M

Medicare Spending Savings (2018)

5151VALUE

PAYER STRATEGY

New Medicare Advantage Health Plan for New Hanover County

• Annual Enrollment Period started October 15

• Membership open to New Hanover County residents with coverage starting January 1, 2020

• FirstMedicare Direct in partnership with New Hanover Health Advantage is offering Medicare Advantage

and Prescription Drug Coverage plans

• These plans build on the strength of NHRMC’s network of providers and facilities to provide cost

effective care that improves the health of our community

To advance payer strategy, greater expertise in

advanced analytics and actuarial capabilities,

along with financial means and population health

capabilities to take on full risk is needed

5252HEALTH EQUITY

ATTAINMENT OF THE HIGHEST LEVEL OF HEALTH FOR ALL PEOPLE

Health Equity

We intend to improve the Health Equity Goals:

• Cultural competence: develop a team that has a deeper

overall health of the region by understanding of every segment of our community and how we

working with partners to can best care for them

eliminate the factors that lead • Hiring and recruitment: diverse, inclusive, transparent hiring

and recruitment practices to support our mission

to poor health, making • Managing risk, starting with employees: to have highly

healthcare more accessible engaged medical plan participants who have no barriers to

and equitable, and creating a receiving quality care in a timely manner at an affordable cost

for themselves and their family members

diverse and extraordinary • Community partnerships: a unified community effort to

workforce committed to advance health and wellness through collaborations with

health providers, non profits, local governments, educators,

meeting the unique needs of private businesses, faith communities, etc.

every individual • Target disparities that have wide-ranging impacts and

develop initiatives to eliminate them: create a healthcare

system where access to healthcare is equitable, health

disparities created by SDOH are eliminated, care integration is

evident across the community systems, NHRMC staff provides

culturally competent care and the staff represent a similar

composition of the community

5353HEALTH EQUITY CULTURAL COMPETENCE, HIRING & RECRUITMENT • Every Day Bias for Healthcare Professionals • Employee Resource Groups • Healthcare Explorers – inspiring future careers 5454

HEALTH EQUITY

IDENTIFYING DISPARITIES

• Screening for Social Determinants of Health

• Connecting to resources through Our Community Link / NC Care 360

Greater investment in infrastructure, community partnerships & capabilities is required

to address health disparities at a larger scale

5555HEALTH EQUITY

TARGETING DISPARITIES

NHRMC Malnutrition Pilot Malnutrition-specific 30-day Readmission Rates

30%

• Nationally, 30-day National Average

readmission rate for Malnutrition

Readmissions

malnourished patients is 25% Rate

23%

• NHRMC obtained grant to 20%

hire Clinical Outreach

Dietitian

15%

• Dietitian visits malnourished

patients in their homes to

10%

reinforce nutrition care plan

and connect to needed

resources 5%

0%

17% reduction in 30- Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19

day readmission rate Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 19-Aug

over 8-month period All-Cause 11.6% 11.2% 11.2% 11.1% 11.5% 11.2% 12.3% 11.6% 10.6% 11.2% 10.8%

Malnutrition 23.3% 25.6% 21.4% 19.8% 17.5% 14.8% 16.7% 21.5% 16.5% 18.8% 16.5%

(Jan-Aug 2019)

All-Cause Malnutrition

5656HEALTH EQUITY

COMMUNITY PARTNERSHIPS

Healthy Food

Food Pharmacy

- Provides healthy food for food insecure patients to take

home when discharged from NHRMC inpatient units

- Funding from Eastern North Carolina Food Bank and

NHRMC Foundation donors

Food Boxes

- Provided by NourishNC to patients of NHRMC Zimmer

Cancer Center and Nunnelee Pediatric Clinics

NHRMC staff participation in NourishNC food drives and

MarKids events

Housing

9th Habitat for Humanity House

Support for WARM

New Hanover County Resiliency Task Force

Address “toxic stress”

Training on Community Resiliency Model

5757HEALTH EQUITY

MANAGE RISK, STARTING WITH EMPLOYEES

Health Benefits Employee Fitness Center Employee Health and Clinic

NHRMC employee Open 24/7 $10 co-pay

contributions for health $5 per pay period for Free flu vaccines and health

benefits have remained flat employees, or $10 per pay risk assessments

for 9 years period for a family Video visits

NHRMC Medical Plan single membership

coverage employee 6,597 members

contribution $401.70 / year 700-800 visits/week

Employee Nutrition Services Employee Pharmacy Healthy Lifestyles

Free consultation and Retail setting offering some 1303 employees enrolled,

guidance from a wellness over-the-counter wellness programs for

dietitian and can enjoy many medications, and NHRMC managing condition,

healthy cooking classes pharmacists will be on site to $0 co-pay for diabetes and

Discounted fresh & healthy educate and review hypertension-related visits,

meal options delivered to 12 medications select medications &

system locations supplies

5858OTHER STRATEGIC PRIORITIES

EMPLOYEE AND PROVIDER ENGAGEMENT

Employee Recruitment, Development and Retention

• Staffing models to address our increasing acuity of patients

• RN Recruitment Center to focus on RN and CNA recruitment

• Pay rates that ensure NHRMC is competitive (highest starting rate for RNs in North Carolina)

• Benefits plans well above the market average

• Leadership development programs for different levels of leadership to build teamwork and personal

development

• Culture transformation / breakthrough training Even after almost $30M investment,

Provider Engagement more dollars needed to keep pace with

staffing and development needs

• Provider leadership training / Dyad model

• Enhanced communication tools

• Resiliency programming

Provider shortages among nearly all

levels and specialties and recruitment

costs projected to increase

5959OTHER STRATEGIC PRIORITIES

INNOVATION

NHRMC is creating an internal culture of innovation with an agile, fail-fast mentality, as well as a strong

external collaborative network locally, nationally, and internationally, designed to:

a) Encourage, generate and manage ideas from within NHRMC through our Speed of

Health business modeling program

- Delivered in either a multi-team, or tailored single-team format to internal and partner organizations

- Supported by an online platform to collect, evaluate, and manage submitted ideas from employees as

well as run "grand challenge” programs. Each year the most promising ideas will be offered mentorship

and legally appropriate investment support for start-up or product development

b) Drive an external innovation pipeline introducing and piloting the best ideas originating outside

NHRMC simultaneously identifying and addressing structural NHRMC barriers to adoption

- Examples from last year or currently in progress include a digital human health coach, tele-pharmacy,

oncology clinical decision analytics; a diabetes management platform, and molecular nutrition software

c) Develop and execute imaginative new business opportunities adjacent to the current NHRMC

business model

- This year we have examined sensor-embedded home monitoring for the elderly, community data-

sharing models to targeting SDOH, and new AI-based commercial wellness applications

d) Create new external revenue opportunities by integrating LEAN and Innovation approaches

leveraging synergies and providing co-branding and operational efficiencies

Further scale and expertise needed to proliferate and achieve

success rate that yields return on investment

6060NHRMC FINANCIAL PROJECTIONS

IMPACTS OF POTENTIAL SIGNIFICANT EVENTS

Potential Significant Event FY18 Impact ($) FY19 $ Impact ($)

340B: Impact of loss of drug discounts and

downward pressure on reimbursement $41 million $50 million

amounts

SCH: Potential Sole Community Hospital

$46 million $37.5 million

(SCH) benefit and reimbursement decreases

Sales Tax: Legislative uncertainty around

$11.8 million $12.4 million

sales tax implementation and assessment caps

Total $98.8M $99.9M

Other potential impacts:

1. Managed Medicaid (projected $20M/year reduction once implemented)

2. Disproportionate Share Hospital payments anticipated total $11.1M

reduction over next 5 years

3. CON de-regulation (would mean loss of likely only non-safety net

services like surgical procedure, imaging and possibly beds)

4. Increasing shift of inpatient care to outpatient in next 5 years

6161NHRMC FINANCIAL PROJECTIONS

PROJECTED CAPITAL CASH FLOW NEEDS

S&P: A+

FY2019 FY2020 FY2021 FY2022 FY2023 FY2024 FY25-FY35

Rating

Operating Margin 3.80% 6.98% 6.40% 5.00% 4.00% 3.00% 3.00% -

Cash Generated - $144,745 $150,908 $139,519 $126,708 $115,974 $120,099 -

Cash Projected Spend on

- ($69,558) ($171,273) ($114,721) ($103,241) ($113,227) ($149,116) ($1,585,662)

Capital

Routine - ($44,445) ($83,809) ($60,938) ($61,581) ($57,677) ($57,581) ($686,930)

Current Special

- ($25,113) ($35,551) ($1,950) $0 $0 $0 ($2,819)

Projects

Future Strategic

- $0 ($51,913) ($51,832) ($41,660) ($55,550) ($91,535) ($895,912)

Projects

Beginning Cash Balance - $763,769 $838,955 $818,590 $843,389 $866,856 $869,604 -

Ending Cash Balance - $838,955 $818,590 $843,389 $866,856 $869,604 $840,587 -

-

Days Cash on Hand 324.6 242.7 237.4 231.0 222.3 209.3 191.5 -

Demand for capital, inability to continue funding

reserves, and expected increases in operating costs

create financial headwinds

6262NHRMC CRITICAL SUCCESS FACTORS

NHRMC is clinically, financially and operationally strong today. We have great people

who are working together to improve the health and well-being of our entire community.

To build on this momentum and succeed, we need additional resources for:

To cultivate a diverse and extraordinary workforce, we need to attract and retain

People employees and providers with a work environment that is rewarding personally and

professionally

To offer consumers a seamless and personalized care experience, we need to invest in

advanced technology systems that provide digital access to services, interconnectivity

Technology

between providers, and analytics that can identify and anticipate changes that will lead to

better care and health for every population we serve

To improve the health of the region, we need to offer a wide array of services that

Expanded

promote wellness and make care easy to access and more affordable while also building

Services

our capabilities to treat the most complex conditions.

To meet the challenges of today’s growing population while also investing in new models

Financial

of care, we need access to capital and the financial strength to withstand cuts to

Security

reimbursements and fluctuations in the market.

6363GUIDING PRINCIPLES 1. Improving access to care and wellness through more consumer-centric options 2. Advancing the value of the care we provide through higher quality and lower costs, effectively managing the health of our region to not only treat the sick but keep them well 3. Achieving health equity through community partnerships and activities that remove barriers to care, enabling our residents to achieve their own optimal health 4. Supporting our staff and the culture that has made NHRMC one of the top places to work in the country 5. Partnering with providers to make southeastern North Carolina an excellent place to practice medicine so we can continue to attract talented and compassionate providers to care for our growing population 6. Driving quality care throughout the continuum and helping facilitate transitions with other providers to deliver more seamless and coordinated care models 7. Growing the level and scope of care already in place for all, regardless of ability to pay 8. Investing to ensure the long-term financial security and future of our health system 6464

REMAINING INDEPENDENT

SYSTEM CO – POTENTIAL RESTRUCTURING

Transition NHRMC into regional health (SystemCo)

• Create IRC 501(c)(3) SystemCo with County-Appointed Board

• SystemCo is new sole corporate member of NHRMC (currently no corporate member)

• Move PMH, other entities under SystemCo, to address lost revenue and other liability implications

• SystemCo may borrow, lend, capitalize more freely outside of New Hanover County

• SystemCo may focus more on strategic planning, other matters, without open meetings, books and

records (researching scope)

Current Organizational Concerns

Ability to Investments

Diplomatic

Respond to Outside of

Hurdles

Competition County

Legal Structure

Organizational

No legal

Issues Education,

structure Limited

remain bylaws

change

Create System Partial/full Education, Partial/full

Parent resolution bylaws resolution

Potential restructuring does not address need for scale,

development of capabilities, or access to capital

Source: First Tryon Advisors

6565You can also read