North America Mortgage Banking 2020 - "Convergent Disruption in the Credit Industry: A Roadmap to Achieving Sustainable Competitive Advantage by ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

North America Mortgage Banking 2020 “Convergent Disruption in the Credit Industry: A Roadmap to Achieving Sustainable Competitive Advantage by 2020”

Executive Summary

Current Situation: Convergent Disruption

• Today’s Lenders are still challenged to rebuild growth, profitability and efficiency following the recent credit crisis

• To further compound lenders’ challenges, convergent disruption is leading to a structural change in the industry; Multiple disruptive

forces are converging on the Credit Industry at the same time, both from inside and from outside the Credit Industry, creating an

increasingly complex and highly dynamic future environment

Building Blocks for Success in 2020: 1. Optimization & Simplification, 2. Agility and 3. Continuous Innovation

• To avoid being marginalized as the future evolves, traditional lenders must become agile and innovative; this will help Lenders adjust to

industry changes and even help them define the industry’s future

• Three building blocks are essential for achieving sustainable competitive advantage in the “Era of Convergent Disruption”:

1. Optimization & Simplification are today’s table stakes and are the essential foundation for 2020; this building block is required

to survive

2. Agility is the new table stakes for 2020; this building block will allow lenders to succeed

3. Continuous Innovation will separate the leaders in 2020; this building block defines high performers

• Lenders that become more agile and innovative will be future high performers, potentially realizing a sustainable >3.5% Gain on Sale

Margin in 2020; this is far better than the ~2.3% margin expected for lenders that simply continue optimizing and simplifying the

current model

Successful Business Models in the “Era of Convergent Disruption”: New business models will take market

share from today’s Lenders

• Agility and product commoditization expand the business models for success in the future

• Today’s traditional Lenders could collectively lose about 35% market share by 2020 to new entrants and current players who adopt new

business models

• While traditional business models can succeed in 2020, new business models could emerge and be highly successful

Roadmap: Today’s Lenders can choose several different paths

• The choice of business model need not be a “one-size-fits-all” decision; Different business models can be adopted for different

business units

• Each business model can also deploy innovative go-to-market strategies to further increase returns

• The Table Stakes will be much higher in the Year 2020 no matter what business model is pursued; Lenders must start building the

groundwork today 2

Copyright © 2014 Accenture All rights reserved.

Current Situation

Industry Trends

Market Environment and Outlook

• Changes in interest rates drive outlook for mortgage origination market; $1.3 trillion in originations forecast

Mortgage for 2014, >60% expected to be purchase money1

Originations • Home purchase demand is anticipated to remain robust, though some seasonal slowing is expected

and Housing • Slow economic growth and fiscal uncertainty have modestly tempered the outlook for future price appreciation

• Pipeline of distressed whole loan opportunities remains strong with additional sellers emerging –

expected to remain strong through 2014

Distressed

• Home prices impact returns; expectation of continued price appreciation at a more moderate pace

Whole Loans • Alternatives to property resolution (e.g., modification, refinance) are increasingly important strategies to

maximize returns

Correspondent • Contracting origination market has led to tighter margins

Lending • A smaller market results in higher barriers to entry for new entrants

Competition • Emphasis on disciplined pricing, execution and service to maintain profitability

Jumbo • Agencies dominate the high-balance loan market; conforming loan limits likely to remain until

Private-Label mid-2014

Securitization • Limited depth of market for private-label securities – significant near-term challenge

• In the past, regulator efforts to protect consumers were prioritized by the risks consumers could pose

Mortgage to the safety and soundness of the institution if they took action, such as filing a class action lawsuit

Regulation • Under new regulatory scheme, the CFBP will judge compliance by the extent to which consumers

have access to financial products and services and that such offerings are fair, transparent, and

competitive. Today, it’s the consumer the government is out to protect, not the institution it regulates

1Source:Average of the Mortgage Bankers Association, Fannie Mae and Freddie Mac 4

Copyright © 2014 Accenture All rights reserved. mortgage market forecasts as of October 2013

Industry Trends

The benchmark 30-year FRM interest rate is projected to continue to rise over

the next two years, according to the MBA.

US Interest Rate Trending and Forecast

“

The increase in mortgage rates has pushed refinance application volume down to levels we have not seen since

early 2011. Given the expectation for rates to remain at current levels or potentially move higher, the refinance

boom we experienced over the past 12 years has…ended”

– Compass Point analyst Kevin Barker, 2013

6.0% $US Billions $450

30-Year FRM (%) Purchase Refinance

Forecast (as of December 2013)

$400

5.5%

+0.9% 5.3% 5.3%

5.2% 5.2%

5.1% 5.1% 5.1% $350

5.0% 5.0% 5.0%

5.0% 4.9% 4.9%

4.8% 4.8% $300

4.7% 4.7%

4.4%

4.5% 4.4% 4.4% 4.4% $250

4.3%

4.0% $200

4.0% 3.9%

3.8%

Recent Highlights: 3.7%

• An increased in mortgage interest rates – such as $150

conforming, 30-year fixed rate mortgages – has 3.5% 3.5%

3.5% 3.4%

caused a drop in refinance applications

$100

• Purchase volumes have remained more resilient

to higher rates and continue their upward trend

3.0% $50

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Source: www.mortgagebankers.org/NewsandMedia/PressCenter/86645.htm

5

Copyright © 2014 Accenture All rights reserved.

Today’s lenders are still challenged to rebuild growth, profitability and efficiency

following the receding credit crisis in today’s low risk/low reward environment.

Pre-Crisis Crisis Disruption

6.0% 1.4%

Gain on Sale Margin Primary Secondary Spread

Moving Forward

5.0% Lenders are still 1.2%

struggling in today’s low Manageable

Primary-Secondary Spread

risk/low reward 1.0% Risk/Higher Reward

Gain on Sale Margin

4.0% environment

• Balance rapidly increasing

0.8% investments in regulatory

3.0% compliance with

0.6% investments to build the

business

2.0%

0.4% • Focus on the Customer:

Invest in product and

1.0% customer experience

0.2%

structural innovations that

0.0% capture market share and

0.0%

proactively respond to

1Q05

3Q10

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

changing customer

-1.0% -0.2% needs, including use of

digital

High Risk/High Reward Low Risk/Low Reward • Rebuild lender reputations

• Underwriting guidelines loosened • Extreme focus on regulatory

• High volume compliance

• Record introduction of new businesses and • Limited work done to

products sustain competitive

• Government guarantee of mortgages advantages in future

• Too big to fail mentality

6

Copyright © 2014 Accenture All rights reserved.

The net cost to originate a residential mortgage has increased dramatically since

year-end 2009, including seeing a steady rise over the past five quarters.

Total Net Cost to Originate Residential Mortgage Loans Based on Un-weighted Averages

For Non-Depository US Companies

$5,000

$4,500 +97% Net Loan Production Operating Cost ($) Period Average +36% $4,573

$4,000 $4,182 $4,207

$3,500 $3,813

$3,539 $3,513

$3,360 $3,324 $3,413 $3,353 $3,310

$3,000 $3,224

$2,945

$2,500 $2,722 $2,827

$2,610

$2,324 $2,345 Key Points:

$2,000 • A re-engineered lending “factory” could cut cost of originating a mortgage by ~25+%, reversing a trend that has seen

origination costs rise by 79% since year-end 2009

$1,500

• Companies need to reduce sales/servicing costs via reduction of redundancy and automation

$1,000 • Increasing attention on technology applications: To improve efficiency and reduce costs, but also to help re-allocate

resources based on shifting demand as well as adding necessary customer/credit analytics

$500 • Rising costs with decline of mortgage brokers , which has had had a profound affect on loan origination system

providers with their customer bases shifting dramatically from broker to lender since 2008

$-

2008 x 2009 2010 2010 2010 2010 2011 2011 2011 2011 2012 2012 2012 2012 2013 2013 2013 Period

Q4 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 3Q 4Q 1Q 2Q 3Q Average

Footnote 1) The net cost to originate includes all origination operating expenses and commissions, including corporate allocated expenses, minus fee income, but excludes

secondary marketing gains, capitalized servicing, servicing released premiums and warehouse interest spread

Note: Tracked by MBA’s Quarterly Mortgage Bankers Performance Report through 3Q12

Source: The Economist, 2 March 2013: “Spread Besting” – www.economist.com/news/finance-and-economics/21572796-feds-frustration-mortgage-profits-have-been-soaring-

spread-besting

Copyright © 2014 Accenture All rights reserved. 7

Industry Trends

Since FY08, originators as a group have raised dramatically their spending on (in

order of magnitude): Outsourcing & Professional Fees, Personnel-related

expenses and IT.

Expenses of US Originators Decomposed Through 3Q13 (vs. 4Q08)

Based on Un-weighted Averages

Radius = Relative Contribution to Expenses For Non-Depository US Companies

98%

90%

% Change in Expenses Through 1Q13

Outsourcing and

Professional Fees

70%

Fulfillment

Personnel Sales Personnel

50% Production Support

Benefits Employees 44%

29% 38%

33% 32% Expense Average = +31%

30% Technology

Other

Operating Expenses

10%

-13% 15%

Occupancy &

-10% Equipment

-30%

$- $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 $1,800 $2,000

$ Cost Per Loan at 3Q13

Source: MBA Performance Report, 3013

Copyright © 2014 Accenture All rights reserved. 8

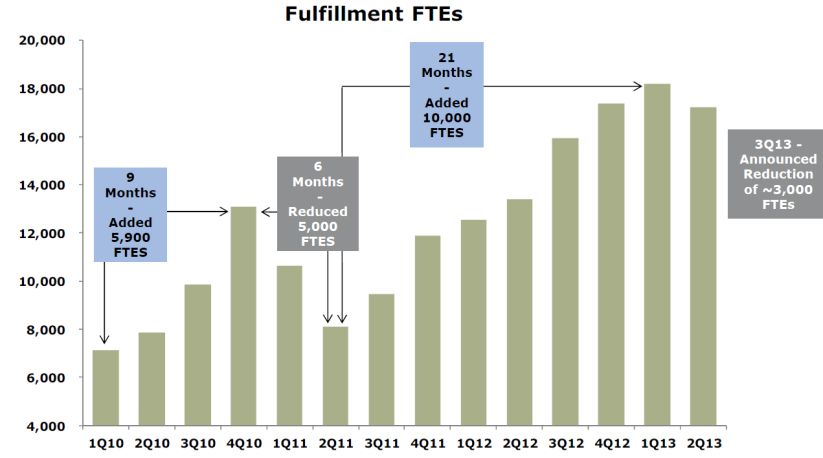

Symbolizing the volatility in managing FTE capacity in the industry, Wells Fargo

and other large bank providers are projecting large cutbacks in the foreseeable

future.

Trend of US Mortgage Industry Employment Wells Fargo FTE Trending….

Mortgage Industry Employment…

Since 1990...

Copyright © 2014 Accenture All rights reserved. 9

Source: Compass Point Research & Trading LLC analyst Kevin Barker, 11 July 2013Industry Trends

Compared to other product/services customers purchase, Mortgage Servicing

and Origination are ranked near the bottom in terms of satisfaction.

Relative JD Power Consumer Satisfaction Scores

Latest Annual US Customer Satisfaction Index Score by Category

(Based on a 1,000 point scale)

950

900 885 890 896

857

850 836 851

803 817

800 787 789 797 801

771

752 763

750 733 736

710

700 683

650

600

1st Time Home Buyers-

Internet Customer Service

US Tablet Buyers

Repeat Home Sellers

Household Insurance

Repeat Home Buyers

US Dealer Leasing

US Dealer Financing

Residential Mortgage

Captive Luxury Lenders

Self-Investor Investing

Full-Service Investor

Mass Consumer Financing

Digital Camera Buyers

Retail Banking

Captive Mass Market

Residential Home Telephone

Residential Mortgage

Smalll Business Banking

Origination

Servicing

Lenders

Sellers

Service

Source: J.D. Power and Associates, 2014

Copyright © 2014 Accenture All rights reserved. 10Industry Trends

However Mortgage Originators have seen a rebound in their customer satisfaction

and though Servicers have also seen a steady improvement, it is not as dramatic.

Relative JD Power Consumer Satisfaction Scores

Trending Annual US Customer Satisfaction Index Score by Mortgage Category

(Based on 1,000 Point Scale)

Origination Servicing

798

771

+37 Points 784

761

757

750 747

747

730 +18 Points 733

725

739 718

734

Key Origination Points: Key Servicing Points:

The use of electronic closing documents improves customer Leveling result of increase in new clients combined with new set of rules

closing satisfaction. Closing satisfaction among the 8 percent of released by the CFPB – effective January 2014 – where under new

customers who closed their mortgage using electronic documents rules, servicers are required to have systems, policies and procedures in

in person averages 830, while satisfaction among the 84 percent place to ensure customers receive the appropriate information and

of those who closed with paper documents in person is 772. support from servicers

2007 2008 2009 2010 2011 2012 2013

2007 2008 2009 2010 2011 2012 2013

Sources:

www.jdpower.com/content/press-release/c6oSdyC/2013-u-s-primary-mortgage-servicer-satisfaction-study.htm

www.jdpower.com/content/press-release/guM7kPe/2013-u-s-primary-mortgage-origination-satisfaction-study.htm

11

Copyright © 2014 Accenture All rights reserved.Proactively responding to changing customer values and needs is critical for

Lenders moving forward.

Today’s Customer Segments* Customer Trends Challenges for Traditional Providers

Consumer Unbanked & • Looking for low-cost FS alternatives, • Pitched marketing batted underway with low-

Lending Underbanked especially through digital channels cost delivery emerging disruptive providers

Youth • Frequent users of digital channels & wallets • Attract and position young customers

• Many are delaying homeownership or opting through lifecycle

to rent vs. buy • Gear mortgage and other credit products to

shifting needs of this segment

Mass Consumer • Customers are willing to switch from their • A number of emerging disruptive providers

primary-banking provider to find a lender emerging, focused on customer-led, socially

with the best rates conscious innovation

• Overall customer satisfaction with mortgage • Gear mortgage and other credit products to

lenders reaches a seven-year high, with shifting needs of this segment

satisfaction among first-time home buyers • Despite improvements, customers

improving considerably from 2012, purchasing a home, particularly 1st-time

• Many are still delaying homeownership or home buyers, continue to experience

opting to rent vs. buy difficulties understanding the loan options

available to them

Mass Affluent / • Increasingly looking for high-value, • The market opportunity for HNW customers

HNWI / Private customized wealth advice through digital is huge

Banking channels • High touch service will be critical with digital

• HNW customers will not reliant on online making fulfillment process more convenient.

applications; rather, they will want a financial • Banks focused on high net worth customers

manager who knows of their entire financial are competing for market share that was left

situation by large lenders who got out of jumbo

lending to focus on their conforming

business. As a result, a gap exists in the

market for serving these HNW customers

when it comes to mortgage

Customer segments are evolving into lifestyle/behavior segments

http://www.jdpower.com/content/press-release/guM7kPe/2013-u-s-primary-mortgage-origination-satisfaction-study.htm 12

Copyright © 2014 Accenture All rights reserved.To further compound lenders’ challenges, convergent disruption is leading to a

structural change in the industry.

• Becoming Digital on the inside of lenders and on the

outside with customers and suppliers is rapidly redefining

interactions, information flows and data transparency Digital Inside Outside

& Outside

• Ongoing industry convergence is opening the door to

new competition, new ways of doing business and new

revenue opportunities Ongoing

Expanded

Industry

• Emerging new entrants are joining the market (in many Regulation Inside Convergence

cases from different industries); they are competing in

innovative ways for customers and profitably serving

traditionally unprofitable segments

• Customers are more empowered through social media

and the prevalence of information and giving them an Subdued

Economic Structural Emerging

information edge over lender employees. Transparency Change

Outlook & New

will drive improved customer trust. Rising Rates Entrants

• Rapid consolidation continues; 20%-30% of today’s

lenders will be gone by the year 2020

• A subdued economic outlook is forecast through the

next 3 years as the Fed will leave targeted federal funds Continued Customer

rate at between 0% and 0.25% in the foreseeable future Consolidation Empowerment

and interest rates will rise

Expanded regulations may cost largest US banks a

further $104bn to resolve mortgage-related legal issues as

they try to put the costs of the subprime crisis behind them. Convergent Disruption

Also, the second largest civil settlement ever obtained by Multiple disruptive forces are converging on the Banking

the state attorneys general will cost the nation’s 5 largest Industry at the same time, both from inside and from outside

mortgage servicers, which control about 60% of a servicing the Banking Industry, creating an increasingly complex and

market, an ~$25bn to $32b 1 highly dynamic future environment with “permanent

Source: 1) Office of Mortgage Servicing Oversight. Joint State-Federal Mortgage volatility”

Servicing Settlement FAQ http://nationalmortgagesettlement.com/faq 13

Copyright © 2014 Accenture All rights reserved.A view to the mortgage industry revolution

Market Events Begin planning GSE

for GSE conservatorship

Dodd- consolidation ends?

Basel 3, QM

Frank Act and QRM rules

Non-agency Original Private-label MBS

passes in place

market collapses conservatorship market running

(Lehman) timeline ends smoothly

GSE

Subprime Conserv- GSEs US

Mortgage atorship return to Presidential GSE ‘consolidation’

Crisis begins profitability Election occurs?

2007 2009 2011 2013 2015 2017 2019 2021

Uniform GSE FHFA “NewCo” Uniform GSE Guidelines

Guidelines and strategic established to and Tech converge

Tech Standards plan build common

begin released “GSE” platform Common US mortgage

secondary market

GSE platform induced platform goes live?

Dodd-Frank Act technology changes

induced technology begin?

changes

Technology-Related Events

Source: CEB TowerGroup Retail Banking analyst Craig Focardi, 2013

14

Copyright © 2014 Accenture All rights reserved.Other industries have experienced similar levels of disruption in recent years;

many leaders emerged with entirely new business models.

In some cases traditional players completely …and in others new entrants are taking dominant roles

redefined themselves to remain relevant… as they revolutionize the customer experience.

Redefined Traditional Player Emerging Entrants • The #1 online lender and the 3rd largest

retail mortgage lender in the US

• Recognized for a 4th consecutive years for

its higher customer satisfaction (source:

JD Power)

From Ma Bell to Global Networking / IP Provider Redefining Retail • Time from application to approval

• From 1984 until 1996 AT&T was an integrated Mortgage Origination averages 17.8 days for Quicken Loans

telecom services and equipment company customers, which is 8.5 days shorter than

• As new entrants eroded traditional profits, AT&T the industry average (26.3 days)

reinvented itself from a telecom and equipment

company to a global networking leader to remain • Best available technology/ largest

relevant Redefining content provider

• Excluding its divested Advertising Solutions unit, 81% Information & • Strong brand development

($126.4B) of AT&T’s revenues in 2012 came from Advertising • Optimized user experience

these growth areas, which grew ~6% YoY • “Google is about getting the right

information to people quickly, easily

of total revenues grew nearly 6% and cheaply – and for free” (L.Page)

81% year over year

• World’s largest music platform

19% 28% 53% Redefining • First sustainable alternative to

Music Industry and music piracy

Content Distribution • Comprehensive user experience

Voice/ Wireline Data/ Wireless from online music to electronic

Other Managed IT Services devices

15

Copyright © 2014 Accenture All rights reserved.The telecom industry exemplifies how disruption can quickly and radically

alter an entire industry; Lenders must prepare for a similar, sustained era of

convergent disruption.

Evolution of the Telecom Industry (a regulated industry like Banking)

Ma Bell Era Baby Bell Era Media Era

1885 – 1983 1983 – 2003 2003 – Today

(first ~100 years) (~ 20 Years) (~10 Years)

Traditional 1885: 1941: First 1983: 1993: 1994: 1997: 2000: 2005: Today; AT&T is the

Providers AT&T installation of 7 Regional AT&T AT&T Bell Bell Atlantic SBC purchases largest communications

founded coaxial cable Bell restructures spins Atlantic merges with former parent holding company in the

in the network Operating into 3 off merges GTE and AT&T Corp. and world with phone,

is placed in Companies separate Lucent with adopts rebrands AT&T cable, wire-line data

service created in companies and NYNEX, name and managed IT

AT&T (AT&T, NCR another "Verizon" 2003: 2009: 2011: Microsoft services

New divestiture Lucent, Regional Skype Skype is buys Skype to

NCR) Bell introduced largest “generate new Today: 33%

Entrant of world's voice

carrier of revenue

Example Int’l voice opportunities” calls are on

traffic Skype

Cable Industry 1996: Comcast 2005: Comcast creates 2009: General Electric Today: Verizon

Convergence launches Comcast Comcast Interactive (GE) and Comcast Wireless to pay $1B to

Online, a broadband Media, a new division announce a buyout air NFL games over

Internet service focused on online agreement for NBC customers'

media Universal smartphones

Traditional Scale Optimize & Simplify Become more agile and digital

Telecom Example: AT&T adopts Example: AT&T restructures into 3 Continuously innovate to stay relevant

“one phone system” separate companies (AT&T, Lucent and

Player Example: AT&T is a worldwide provider of IP-based

campaign from 1907-1960s NCR) then spins off Lucent and NCR

Response communications, manages largest 4G US network, has wireless

coverage overseas and recently developed AT&T U-verse to deliver

services across mobile devices, PCs and TVs

Lessons Learned from Telecom Industry Disruptions (Credit Industry Parallels):

• The pace of change is much faster when enabled by agile, digital technology

• Leaders find innovative ways to improve the customer experience, and they continually redefine themselves (e.g., AT&T was

a telecom services and equipment company in 1983 and is a global networking leader today)

• Those companies that do not innovate and adjust to industry disruptions eventually become obsolete (e.g., NYNEX)

16

Copyright © 2014 Accenture All rights reserved.The NA Lending Industry is already experiencing disruptions of the magnitude

seen in the Telecom Industry; disruptions that completely transform an industry.

Evolution of the NA Banking / Lending Industry

Glass Steagall Era Universal Banking Era Post Credit Crisis Era

Build Specialization Scale Optimize & Simplify

Agility & Innovation On Horizon

1933 – Late 1990s Late 1990s – 2008 2009 – Today

(first ~65 years) (~ 10 Years) (~5 Years)

Traditional 1933: 1938: 1969: 1995: First 1998: 2007: 2008: Significant 2010 :GSE 2013+: S&P reports

Providers Glass– Fannie First ATM large bank LendingTree Wells Fargo consolidation conservatorship that the biggest

Steagall Act Mae installed offers online created to reintroduces • Bank of America begins US banks may

separates created; (at services provide mobile acquires Countrywide have to spend a

commercial Freddie Chemical (Wells consumers a banking

and Mac Bank) Fargo) • Wells Fargo acquires further $104bn to

centralized Wachovia resolve mortgage-

investment created location to

banking in 1970 • JPMC acquires most of related legal

receive multiple

loan offers Washington Mutual from issues as they try

FDIC’s receivership 2012: to put the costs of

New 1985: Quicken

Loans, originally 1999: • Simple (Bank) the subprime

Entrant crisis behind

Rock Financial goodmortgage.com 2008: launched – 100%

Example founded online bank them.

Mortgage, • PennyMac founded by

founded • American Express

seasoned lending

and WalMart

executives who have

focused on origiinating launch Bluebird, a

Industry 1998: Citibank 1999: Gramm– HARP-based loans prepaid debit card

Convergence merges with Leach–Bliley Act:

2012:

Travelers to form allows commercial

• Capital One acquires ING

Citicorp combining banks, investment

DIRECT in the US and

banking, securities banks, securities

rebrands its retail unit

and insurance firms, and insurance

CapitalOne 360

services companies to

consolidate • Scotiabank acquires ING Direct

Canada

Lessons Learned from Evolution of the Banking Industry

• After a decade of focusing on building scale in the 1990s, the dominance of the universal banking model is being questioned, including by

regulators who are examining “Too Big to Fail” and possible scenarios to carve up failed large full-service banks

• In the post credit crisis, banks – traditional and emerging - are focused on strategies to boost customer centricity (e.g., social media/Big Data)

17

Copyright © 2014 Accenture All rights reserved.Building Blocks for Success in 2020

To avoid being marginalized as the future evolves, traditional Lenders

must become agile and innovative; this will help Lenders adjust to

industry changes and even help them define the industry’s future.

• No longer will traditional Journey to Sustainable Competitive Advantage

practices of optimizing and

simplifying the existing Business

Performance Continuous Innovation

infrastructure and business for (Year 2020 Leaders)

improved efficiency and Agility

effectiveness yield a (Year 2020

Table Stakes)

competitive advantage; this Optimization &

simply allows lenders to survive Simplification

(Today’s Table Stakes)

• Rather, adoption of a new,

broader mindset focused on

managing change quickly and

Era of Era of

effectively is critical to compete Survival Convergent Disruption

in the increasingly complex and

Today’s Penetration 93% of lenders are here 5% of lenders are hereAs the production side of the business rebounds, lender margins continue their

steady decline – so future winners will have to focus on boosting not only their

efficiency but their agility and continuous processes to innovate.

US Mortgage Volumes & Margin Trending

Rising interest rates have reduced mortgage re-financings and income

from the sale, securitization and servicing of retail mortgage loans by

$4bn among the largest bank lenders

Quarterly Averages of US Industry’s Gain on Sale

4.0% Industry Margin 1 Purchase Refinance “Era for Convergent Disruption” $450

0.4% 3.8%

3.5% Recovery 3.7% $400 High

Performers

0.5% of the

3.0% 3.2% $350 Future

3.1% 0.4%

2.5% 2.7% 0.2% $300 Average

2.5% Performers

0.4%

2.3%

2.0% 0.3% $250

2.1%

2.0%

1.5% 1.6% $200

1.5% 1.6%

Status Quo

(continued optimization

1.0% & simplification only – $150

Not Sustainable)

0.5% $100

0.0% $50

4Q10 1Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 e2H13 O &S Agility Innovation 2020

Footnote 1): Gain on Sale as reported by Compass Point Research & Trading

Other Sources: The MBA and Accenture Research, December 2013 http://www.mba.org/files/Bulletin/InternalResource/86348_.pdf

20

Copyright © 2014 Accenture All rights reserved.Three building blocks are essential for achieving sustainable competitive

advantage in the increasingly complex “Era of Convergent Disruption.”

3. Building Blocks for Sustainable Competitive Advantage in the “Era of Convergent Disruption”

Differentiate

Through 3. Year 2020 Lender Leaders

Sustainable

2. Year 2020 Table Stakes

Competitive

3. • Become Digital: Transform IT platform to overcome rigid legacy

Advantage technology in back office and enable analytical-driven front office

Continuous • Be Customer-Driven: Make all decisions to improve the customer

innovation experience and proactively meet customer needs

Have the ideas, vision • Fulfill Self-Service vs. Channel Potential (including social media):

and leadership to proactively Maximize channel management per broker, loan officer and consumer

stay ahead of the market direct to best engage customers in sales and fulfillment using their

preferred methods (e.g., mobility, social media and online)

• Manage the New Talent Dynamic: Re-engineer human capital

Adapt platform/program to leverage best available talent internally and

Through externally on demand

• Employ Optimal and Flexible Financial Strategies: Adaptable

2. Agility portfolio and product strategy

Be able to seize opportunities

In times of change

1. Today’s Table Stakes

• Channel Fulfillment: Provide capability in all

Drive channels to serve target customers most effectively

Efficiency • Streamline and Simplify The Business: Remove

redundancies and improve processes and

Through technologies to become lean and rationalize

business, products, technology and operations

• Manage Regulatory Requirements: Handle

1. Optimization and simplification increasing regulation as a competitive advantage

• Manage Enterprise Risk Management Regime:

Be as efficient and effective as possible in current structure

Provide early-warning to emerging risk threats in

possible siloes of business

• Create Capital and Funding Strategies: Optimize

to meet business opportunities/challenges as they

Building Blocks arise

21

Copyright © 2014 Accenture All rights reserved.The building blocks are enabled by technology; lender leaders

need to balance innovation demands of the business with

ongoing scale and efficiency needs of the corporation.

Enabling Technology in the “Era of Convergent Disruption” IT Balance

Differentiate Innovate

3. Enabling Technology 3.

Continuous Business IT

Corporate

Year 2020 Lender Leaders IT

innovation (“As a

Technology As Continuous Service”)

2. Agility

Provider of Innovation

3. Drive

1. Optimization and Scale

Efficiency

Continuous simplification

innovation 2. Year 2020 Table Stakes

Have the ideas, vision Agile Information Technology

and leadership to proactively • Mobility: Extending mobility across the distribution spectrum

• Analytics and Data Velocity: Using business intelligence, data analytics and

stay ahead of the market

big data to access the right data at the right time by creating a data supply chain

• Social Collaboration: Combining customer oriented service and a highly

effective capability – Social Enterprise

• IT Infrastructure: Could include a private cloud for its loan origination system, a

VoIP phone system and paperless underwriting

• Electronic Closing Documents: improves customer closing satisfaction

2. Agility

Be able to seize opportunities 1. Today’s Table Stakes

In times of change Optimizing & Simplifying Technology

• Digital HR & Finance: Workplace Collaboration, Hyper Change

Management and Virtual Learning, Financial Performance

Analytics, and Real-time operations performance and cost to serve

monitoring

• Digital Logistics & Operations: Electronic document

management system and a Web-based LOS that includes a

module for borrowers to initiate loan applications

1. Optimization and simplification • Cyber Security & Fraud Management: Data privacy

management platform including enhanced email security tools and

Be as efficient and effective as possible in current structure digital file upload portals.

• eCustomer Interface: Loan onboarding processes with automated

workflows that collect, compare and route mortgage file data and

documents as well as real-time status alerts that give borrowers

and their real estate agents real-time status updates on their loans

Building Blocks • Imaging Technology: Allows for document collaboration across all

departments 22

Copyright © 2014 Accenture All rights reserved.Emerging Lender Business Models

A handful of the largest US lenders that did not exist five years ago have

emerged to capture >10% origination share from traditional legacy providers.

Changing Large US Lender Landscape – 2008 vs. The Present % Declines in Origination New Entrant Since 2008

Total Number of Lenders -4.6% 2.5% 484 472 611 -4.9% 1.5% 461 454 594

Total Residential Origination Volume Total Residential RETAIL Origination

($US Millions) Volume ($US Millions)

All Companies 6.4% 20.6% 1,941,536 1,424,581 13.0% 28.1% 1,158,456 904,165 627,666

Big 4 Market Share 0.5% -4.9% 45% 50% 44% 0.0% -3.7% 45% 49% 45%

Emerging Providers Market Share 10.2% 5.0% 11% 6% 1% 12.2% 4.4% 13% 9% 1%

Company Name % 5-Yr CAGR % 1-Yr CAGR LTM 2013Q2 LTM 2012Q2 LTM 2008Q2 % 5-Yr CAGR % 1-Yr CAGR LTM 2013Q2 LTM 2012Q2 LTM 2008Q2

Wells Fargo & Co. 12.3% 3.8% 490,336 472,407 274,557 14.9% 9.6% 251,883 229,922 126,030

Chase 12.0% 26.6% 212,735 168,004 120,580 24.7% 8.2% 113,870 105,253 37,758

Bank of America -4.2% 4.8% 95,534 91,190 118,519 1.0% 39.0% 95,422 68,660 90,885

Quicken Loans Inc. 68.7% 114.4% 94,250 43,952 6,890 68.7% 114.8% 94,250 43,884 6,890

US Bank Home Mortgage 21.1% 18.5% 86,946 73,397 33,441 28.4% 18.2% 24,906 21,069 7,144

CitiMortgage, Inc. -9.2% 4.3% 73,443 70,383 119,259 16.6% 64.0% 61,334 37,398 28,508

PHH Mortgage 22.4% 3.2% 56,890 55,152 20,704 23.2% 26.5% 49,894 39,434 17,553

Flagstar 27.4% 30.2% 53,171 40,829 15,860 17.0% 25.4% 3,233 2,578 1,476

BB&T 17.9% 14.7% 34,729 30,268 15,244 10.1% 12.1% 13,243 11,818 8,187

SunTrust Bank 9.5% 19.3% 34,058 28,548 21,613 11.4% 14.6% 18,265 15,938 10,654

PennyMac -- 540.4% 33,672 5,258 -- -- -- -- -- --

Provident Funding Associates 30.6% 1.9% 31,964 31,358 8,422 68.6% 21.1% 4,782 3,949 351

Fifth Third Bank 28.1% 8.2% 27,748 25,646 8,059 25.7% 2.8% 15,555 15,134 4,950

Ally Bank/ResCap (GMAC) -8.2% -46.8% 24,786 46,606 37,928 -14.7% -61.4% 4,425 11,477 9,801

Franklin American Mortgage Co. 20.4% 39.8% 23,794 17,024 9,388 34.5% 35.4% 1,037 766 236

Guaranteed Rate Inc. -- 86.2% 18,020 9,676 -- -- 86.2% 18,020 9,676 --

USAA Federal Savings Bank 20.1% 18.4% 17,932 15,151 7,189 46.2% 18.4% 17,932 15,151 2,689

PNC Mortgage 6.2% 35.0% 17,114 12,675 12,667 7.2% 35.0% 17,114 12,675 12,094

Nationstar Mortgage -- 206.4% 15,416 5,031 -- -- 148.9% 7,913 3,179 --

PrimeLending 51.4% 29.7% 14,455 11,145 1,820 51.5% 29.7% 14,455 11,145 1,814

Stearns Lending 72.8% 65.1% 14,436 8,746 938 162.4% 92.7% 2,486 1,290 20

Navy FCU 28.9% 54.1% 12,048 7,817 3,383 28.9% 54.1% 12,048 7,817 3,383

Everbank 33.1% 50.8% 11,456 7,596 2,742 56.1% 64.1% 6,290 3,834 679

United Wholesale Mortgage -- 234.6% 10,953 3,273 -- -- 87.9% 1,037 552 --

NYCB Mortgage -5.9% 7.5% 10,258 9,544 13,883 -100.0% -100.0% -- 3 124

Amerisave Mortgage Corp. -- 42.9% 10,062 7,040 -- -- 34.2% 8,507 6,340 --

M&T Mortgage 27.1% 41.2% 9,357 6,626 2,822 37.3% 40.2% 5,523 3,938 1,131

Union Bank 31.1% 8.2% 9,232 8,529 2,386 40.8% 0.5% 3,321 3,305 601

Prospect Mortgage -- 20.2% 8,883 7,389 -- -- 19.3% 8,812 7,389 --

Sierra Pacific Mortgage 23.8% 33.9% 8,464 6,322 2,913 56.6% 39.9% 2,102 1,503 223

TD Bank NA 75.2% 27.4% 8,296 6,513 503 87.2% 27.4% 8,296 6,513 361

Regions Mortgage 20.8% 15.8% 8,088 6,985 3,146 20.9% 16.2% 7,967 6,855 3,082

Manufacturers & Traders Trust Co. 8.7% 310.6% 7,761 1,890 5,107 22.0% 334.0% 4,197 967 1,552

LoanDepot.com -- 99.3% 7,704 3,866 -- -- 106.7% 7,704 3,728 --

RBS Citizens, NA 40.0% -3.8% 7,245 7,532 1,349 40.0% -3.8% 7,245 7,532 1,349

Fremont Bank 55.0% 60.0% 7,158 4,475 801 46.6% 51.0% 5,110 3,383 754

Cole Taylor Mortgage -- 125.2% 7,114 3,159 -- -- 117.3% 1,193 549 --

Sources: Accenture Research analysis using MortgageData.com, 2013 24

Copyright © 2014 Accenture All rights reserved.Over the past five years, emerging Online and Independent lenders, many of

whom did not exist during the depths of the Credit Crisis, have stolen market

share away from primarily the midsize / regional banks in the US.

Mortgage Origination Market Share Change Among US Lender Types

Wholesale and Retail Origination Combined

60%

2008 2012 2013 +0.5%

50% 0% % Market Share Change 2008-13 -21.6%

45%

40%

30%

+12.1% 23%

20% 17%

+3.7%

+5.3%

9%

10%

6%

0%

Online Small Banks Independents Midsize Banks Big 4

Sources: Accenture Research analysis using MortgageData.com, December 2013

Footnote 1): Market share data comparing each time period at the 2 nd Quarter on a trailing 12-month basis

25

Copyright © 2014 Accenture All rights reserved.Over the past five years, emerging Online and Independent lenders, many of

whom did not exist during the depths of the Credit Crisis, have stolen market

share away from primarily the midsize / regional banks in the US.

Mortgage Origination Market Share Change Among US Lender Types

Retail Origination

60%

2008 2012 2013 +0.0%

50% 0% % Market Share Change 2008-13 -20.8%

45%

40%

30%

+9.9%

20%

20% +5.3% +2.3%

15%

10% 11%

10%

0%

Online Small Banks Independents Midsize Banks Big 4

Sources: Accenture Research analysis using MortgageData.com, December 2013

Footnote 1): Market share data comparing each time period at the 2 nd Quarter on a trailing 12-month basis

26

Copyright © 2014 Accenture All rights reserved.Agility and product commoditization expand the business models for success in

the future of the mortgage origination industry.

Emerging Entrants and Adopters (Current

Current Lender Landscape – 2014

Players who Adopt new Business Models)

50+ Players

Highly Agile C. B. Independent Lenders

• Most business generated ~17% market share*

Emerging

through online/digital channels (PHH, Nationstar)

• Highly nimble

Digital

• Flexible infrastructure Lenders A. Traditional

• Social media an integral part of 6% MS Lenders

strategy

• Optimized and simplified

~425 Lenders

• Customer-centric ~77% market share*

(US Bank Home

Mortgage, BB&T,

SunTrust, USAA)

• Most business generated through Small Bank Mid-Size Big 4 Banks

traditional, physical channels Lenders Banks 4 players

• Less nimble

• Heavy infrastructure 360+ players 60+ players ~45% market share*

• Less optimized and simplified ~9% market ~23% market (Wells Fargo, Chase,

Less Agile share* share* BoA, CitiMortgage)

Specialized Large-Scale, Commodity Products

• Focused products or limited geographic focus • Commodity products (mass market focus)

• Highly customer-centric • Product and customer centric

• Higher priced • Low price

• Advice-driven • Low amount of advice

• Highly nimble • Not very nimble

• Simplified/optimized infrastructure • Large, often legacy infrastructure

• New entrants • Larger foreign entrants, but mostly traditional

• Compete largely on advice and product depth/differentiation players

• Compete largely on price

* Market shares are based on enterprise-level revenues

Sources: Accenture Research analysis using MortgageData.com, 2013

Copyright © 2014 Accenture All rights reserved. 27Today’s bank lenders could collectively lose ~20% market share by 2020 to new

entrants and current independent lenders who adopt new business models.

Potential Lender Landscape – 2020 (Status Quo Scenario)

Highly Agile B. Independent Lenders 90+ Players Emerging Lenders and Adopters (Current

~26% market Players who Adopt new Business Models)

share* ~100 players

C. Emerging

Digital ~40% market share

Lenders A. Traditional Full- Examples of who could steal market share

10+ Players Service Lenders from Traditional Lenders:

~15% market • A handful more pure play online lenders will

300+ banks

share look to take advantage of Quicken Loan’s

~60%

market dynamics

market share

Small Bank • Small/community banks that become highly

Lenders Mid-Size Big 4 Lenders agile and can now compete with larger banks

250+ players Banks 4 players (e.g., innovative credit unions)

~26% market 45+ players ~30% market • Agile / innovate independent lenders

share* ~17% market share • Retailers that continue to move into the

Less Agile share lending space

Specialized Large-Scale, Commodity Products

Market Share # of Players

Today 2020 Today 2020 Comments

Big 4 Lenders ~45% ~30% 4+ 4+ • The Big 4 Lenders will continue to manage through the complexity of increasing regulatory requirements and will

be motivated to battle for lower risk / higher margin markets (HNW)

Mid-Size ~23% ~17% 60+ 45+ • Midsize / regional leaders have lost the most market share since the credit crisis and will continue to see runoff as

Lenders they look to reposition their business models to be more competitive and unique in an increasingly fragmented

credit market

Small Bank ~17% ~26% 360+ 250+ • Though the number of small banks will continue to consolidate, the survivors (including innovate credit unions) will

Lenders continue to capture market share for customers seeking high-touch customer service

Online ~6% ~15%Through the rest of the decade, traditional lenders will increasingly need to respond

to emerging lending disruptors like Quicken, Guaranteed Rate and

Goodmortgage.com, which will look to continue to build scale.

Emerging Disruptors

Banks Disruptors Common Characteristics of

the Emerging Disruptors

Circa Circa

2020 3 2020 • Emphasize social

Optimization and responsibility

Market Simplification Scale • Focus on customer centricity

3 nimble and empowerment

Innovation • Present simpler fee structure

2 to customers

Agility • Provide personal financial

2 management tools and

Agility Innovation access to other accounts

1 • Embedded with social

media, especially Facebook

1 Scale Market entry • Leverage Big Data and

Optimization and analytics

Simplification Circa Circa

• Willingness to leverage

2013 2013

Cloud and Virtualization

29

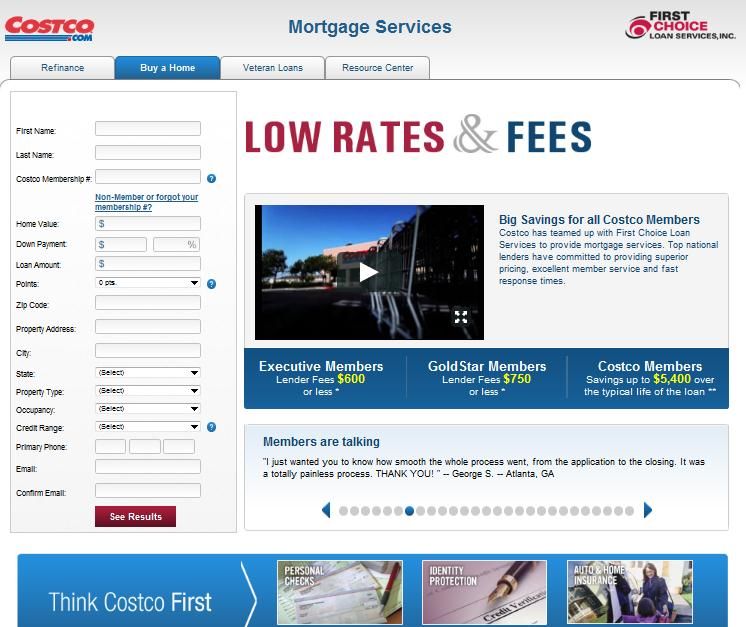

Copyright © 2014 Accenture All rights reserved.Courting customers who are fed up with their banks, Costco continue to build out

its financial services offering, after first offering mortgages in late 2010.

Costco’s Emerging FS/Credit Business www.costcofinance.com/LoginAndPricing.aspx

• Key Membership Metrics:

– 39m households

– 71.2m cardholders

– 90% renewal rate (for US and Canada)

– $2.3bn+ in cash fees for LTM

• Financial Services Proposition:

– Began making mortgages in late 2010

– Sells auto and homeowners’ insurance

– Offers credit card processing for small

businesses

– Provides financial planning

• Credit Value Proposition: Costco does not make

money on mortgages, but instead uses it as

another incentive to get people to renew their

store memberships, where Costco makes a large

chunk of its profit.

Sources: • History of Innovation:

www.fool.com/investing/general/2013/10/11/10-reasons-why-peter-

drucker-would-have-thought-co.aspx#878482 – First with its membership-fee structure

The New York Times, 13 November 2013

– Move into selling gasoline

30

Copyright © 2014 Accenture All rights reserved.While traditional business models can succeed in 2020,

two new lender business models could emerge and be highly successful.

Potential Landscape – 2020 (Emerging Model Scenario)

Possibly Today’s Largest Digital Lenders,

Digital pure plays have to adopt a broader 1 of the Big 4 Lenders, and Large Indies

infrastructure to scale and properly manage and Midsize Banks Focus on Evolving to

customer expectations a Digital Model With Scale

Highly Agile Industries Outside Lending

• Most business generated

through online/digital channels C. Emerging Digital D. Digital Hybrids 10+ Players

• Highly nimble Lenders ~20% market Best

• Flexible infrastructure 20+ Players share*

90+ Players positioned

• Social media an integral part of ~5% market share B. Independent Lenders

strategy ~15% market share* for global

• Optimized and simplified expansion

• Customer-centric

Possibly a handful of small banks

(~10) decide they will be more

E. Retail

competitive by assuming a pure play

digital approach ; might be conducive

Correspondents

Possibly

for credit unions 5-8 players Large

(Lenders + Large Retailers +

• Traditionally customer facing

Retailers) One of the

• Most business generated A. Small Bank A. Midsize A. Big 2

~10% market share Large 4 /

through traditional, physical Lenders Lenders Lenders

Largest

channels ~240 players ~40 players 2 players (Example: Costco Indies /

• Less nimble ~10% market ~15% market ~25% market partnering with one Larger

• Heavy infrastructure share share share of the Big 4) Midsize

• Less optimized and simplified

Banks

Less Agile

Specialized Large-Scale, Commodity Products

• Focused products or limited geographic focus • Commodity products (mass market focus)

• Highly customer-centric • Product and customer centric

• Higher priced • Low price

• Advice-driven • Low amount of advice

• Highly nimble • Not very nimble

• Simplified/optimized infrastructure • Large, often legacy infrastructure

• New entrants • Larger foreign entrants, but mostly traditional

• Compete largely on advice and product depth/differentiation players

• Compete largely on price

31

Copyright © 2014 Accenture All rights reserved.These new business models have the potential to be highly disruptive to the

banking industry.

Potential Landscape – 2020 (Emerging Model Scenario)

Industries Outside Lending

Highly Agile

C. Emerging Digital D. Digital Hybrids 2 3 10+ Players

Lenders ~20% market High Performers

1

20+ Players share* will be OUTSIDE

90+ Players this box (more

~5% market share B. Independent Lenders

~15% market share* agile)

A. Small Bank A. Midsize A. Big 2 E. Retail 4

Lenders Lenders Lenders Correspondents 5

~240 players ~40 players 2 players 5-8 players (Lenders

~10% market ~15% market ~25% market + Large Retailers)

share share share

~10% market share

(Example: Costco,

Sam’s Club, Home

Depot partnering with

Less Agile one of the Big 4)

Specialized Large-Scale, Commodity Products

1. Emerging Digital 2. Hybrid Digital Bank 3. Digital Hybrid 4. Retail Correspondent 5. Retail Correspondent

Scenario: Scenario: Independents: Bank Scenario: Indie Scenario:

• Example: Some small • Example: One of the Big 4 • Example: A few of the • Example: One of the Big 4 • Example: Large retailers

banks and independents banks and a few of the largest indies will see banks or midsize banks will partner with a few of the

see a competitive Midsize banks focus on advantage of focusing on a provide the lending engine large independent lenders

advantage in becoming as a going digital with scale digital value proposition behind one of the big • Market Edge: The

digital pure play • Market Edge: Gaining cost • Market Edge: Could have retailers independent lenders who

• Market Edge: Gaining cost and process efficiencies vis competitive advantage over • Market Edge: Immediate partner with retailers will

efficiencies and expanding a vis traditional lenders most lenders, especially in market share and low gain an additional

beyond legacy physical adjusting to market demand pricing across a broad distribution channel and

footprint range of products appealing higher customer brand

to existing customers awareness

32

Copyright © 2014 Accenture All rights reserved.Lenders choosing to remain Traditional Full-Service Providers

can also be successful by becoming more agile and/or large-scale.

Potential Landscape – 2020 (Emerging Model Scenario)

Industries Outside Lending

Highly Agile

C. Emerging Digital Lenders 2 3 10+ Players

D. Digital Hybrids

~20% market share* High Performers

1 20+ Players

~5% market share 90+ Players will be OUTSIDE

B. Independent Lenders this box (more

~15% market share*

agile)

F. Retail 4

A. Small Bank A. Midsize A. Big 2 Lenders

Correspondents

Lenders Lenders 2 players 5

5-8 players (Lenders

~240 players ~40 players ~25% market share

+ Large Retailers)

~10% market share ~15% market share

~10% market share

(Example: Costco,

Sam’s Club, Home

Depot partnering with

Less Agile one of the Big 4)

Specialized Large-Scale, Commodity Products

High Performing Lenders Banks will transform themselves by 2020 to become:

1. More Digital – Focus of applying digital capabilities will be on the sales process/rate shopping and consumer finance education. When it comes

to needs analysis and product fit, it will be a very customer / loan officer centric interaction. Digital capabilities can also be used in the back office

to exchange data/information and provide transparency into the life of the loan

2. Truly Customer-Driven – All decisions will be made to satisfy customer needs: this requires offering more transparency, ease of doing

business, having to request assistance once and setting and meeting expectations

3. Omni-Channel – Over half of business will be conducted through digital channels; although physical channels will still play a very important part

in the business, these banks will not rely on them for survival

4. Innovative at the Core – Innovation will be embedded in all levels of the organization to proactively stay ahead of the market; do not settle for

anything less than being a leader

5. Partnering With Leaders in Other Industries – Witnessed by the recent moves of top builder-oriented retailers, opportunities will continue

exist for lenders to partner with companies in other industries’

6. OR Large-Scale – Deliver products to the mass market at lower margins (number of products sold makes up for lower margins); costs must be

substantially reduced through reduced product complexity and streamlined technology and operations to make this work

33

Copyright © 2014 Accenture All rights reserved.The Table Stakes will be much higher in the Year 2020 no matter what

business model is pursued; Lenders must start building the groundwork today

3 Building Blocks for Sustainable Competitive Advantage

in the “Era of Convergent Disruption”

3. Year 2020

What Must Lenders Do

Leaders

TODAY to Succeed in the

3. “Era of Convergent

Continuous Disruption”?

innovation

Have the ideas, • Proactively invest in

vision and leadership

to proactively

initiatives that will build the

stay ahead of the market business rather than

reactively respond to

2. Agility 2. Year 2020 regulations, competitors and

Be able to seize opportunities Table Stakes industry changes

In times of change

• Become More Digital

• Be Customer-Driven • Fundamentally shift from a

• Fulfill Omni-Channel Potential (incl. social media)

• Manage the New Talent & Regulatory Dynamic product-oriented organization

• Employ Optimal and Flexible Financial Strategies to a customer-driven

1. Today’s organization

1. Optimization and simplification

Table Stakes

Be as efficient and effective as possible in current structure • Rebuild bank reputations

• Channel Fulfillment

• Streamline and Simplify The Business • Embrace and integrate new

• Manage Regulatory Requirements technologies, channels and

• Manage Enterprise Risk Management Regime strategies

• Create Capital and Funding Strategies

34

Copyright © 2014 Accenture All rights reserved.The US Mortgage Lender industry is managing a $18.5 trillion balance sheet.

US Household Balance Sheet – $US Billions

Residential Real Estate = $18,453

Mortgage Debt Outstanding = $9,868 Homeowner’s

Equity = $8,585

Agency Balance Sheet = Bank Balance Sheet = Non-Agency MBS = Other

= -$1 QoQ

$5,830 $2,957 $886 +$819 QoQ

-$9 YoY +$2,077

$195 YoY

Ginnie 1st Lien 2nd Lien Other* Prime Alt A Option Sub- Dramatic increases in home equity

GSE MBS = $4,490 MBS = = = = = = ARM Prime could support the issuance of

$1,340 $2,051 $748 $158 $188 $288 = $117 =$293 HELOCs, increase the amount of

loans able to refinance and

improve the mobility of

+4 QoQ +$ 18 -$17 -$22 -$2 -$12 -$11 -$7 -$8 homeowners.

-$102 YoY +$102 +$60 -$84 -$11 -$47 $56 -$25 -$46

Includes life insurance companies; pension funds, retirement funds, finance companies and REITs

Sources: Federal Reserve, Amherst Securities, Compass Point Research & Trading LLC analyst Kevin Barker, 11 July 2013

Copyright © 2014 Accenture All rights reserved. 36As customer satisfaction continues to improve steadily, mortgage lenders are still

seeing some inconsistent performances year on year with their origination cycle

times.

Trend for Residential Mortgage Origination Cycle Time & Customer Satisfaction

Total Cycle Customer Satisfaction

Time in Days • The time from application to approval averages 17.8 On Scale of 1,000

65 days for Quicken Loans customers, which is 8.5 days 780

Cycle Time shorter than the industry average (26.3 days)

61.0

• In late 2011, CitiMortgage had been adding staff,

60 streamlining its processes in effort to cut its refinance

Customer

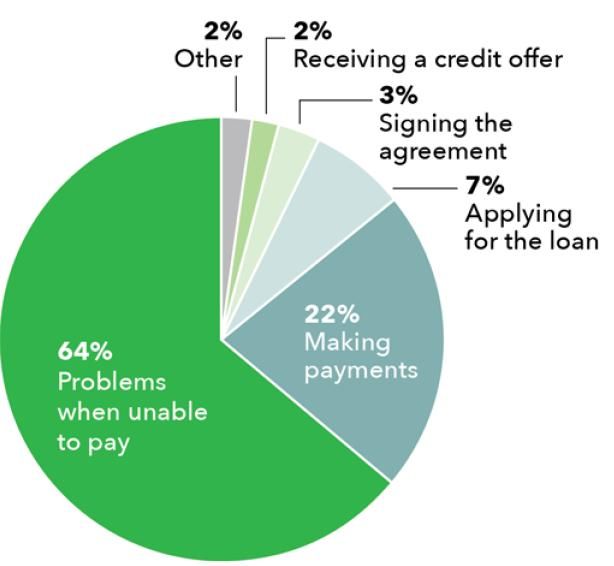

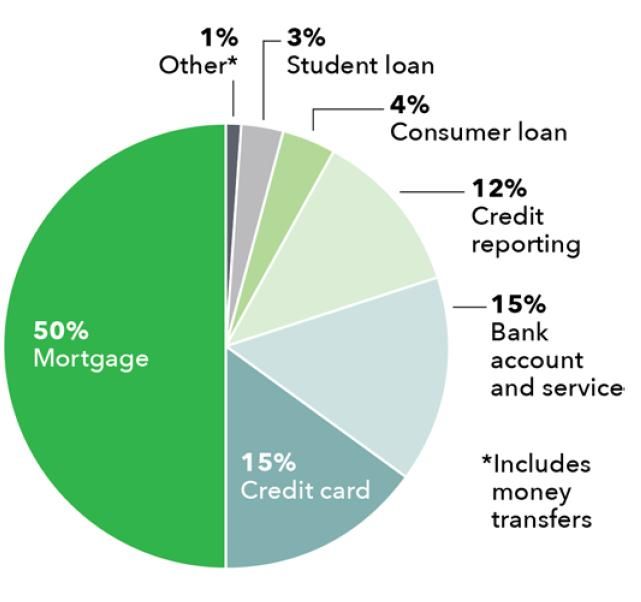

Satisfaction time from 77 days toHalf of the complaints received by the CFPB are related to mortgages.

Consumer Complains Received by the CFPB – Through June 2013

Consumer Complaints by FS Product Consumer Complaints Related to Mortgages

Between July 1, 2012 and June 30, 2013, the CFPB received ~122,000 consumer complaints.

Source: http://files.consumerfinance.gov/f/201312_cfpb_report_financial-report.pdf

Copyright © 2014 Accenture All rights reserved. 38Appendix

Gain on Sale margin assumes a mortgage is originated at going market

rate, a guarantee fee paid to GSEs, servicing fees are paid and a

mortgage is sold in the secondary market.

Gain on Sale Margin Index Decomposed 1

Inputs 4Q12 Average 1Q13 Average HARP Notes

Duration (years) 7 7 8 Assume mortgage duration

Coupons per yr 12 12 12 Monthly mortgage payment

Mortgage rates 3.43% 3.55% 4.00% Primary rate

Guarantee-fee 0.40% 0.48% 0.48% Paid to GSE

Servicing free 0.25% 0.25% 0.25% Paid to servicer

Other 0.10% 0.10% 0.10% Hedging, fall-out, etc.

Net Yield 2.68% 2.72% 3.17%

MBS Yield 2.18% 2.46% 2.30% Yield in MBS market

Net Spread 0.50% 0.26% 0.87%

Secondary Market Price $1,032.43 $1,016.70 $1,063.52 Price of bond in market

Face Value $1,000.00 $1,000.00 $1,000.00 Original value of mortgage

Priced-in Margin 3.24% 1.67% 6.35% Diff between secondary $ and

mortgage balance

Capitalization of MSR 0.90% 0.90% 0.90% Initial value of MSR created (non-

cash)

Total

1

Gain on Sale 4.14% 2.57% 7.25%

MSR capitalized at 90 bps, 30-year fixed retail originations only

Sources: Compass Point Research & Trading LLC analyst Kevin Barker, 11 July 2013; chart sources include Bankrate, Bloomberg, FHFA and Compass Point

Copyright © 2014 Accenture All rights reserved. 393.

Continuous

innovation

2. Agility

Additional information about each building block is available 1. Optimization and

simplification

in the provided links

Additional Information Business Technology

Continuous Innovation https://kxws.accenture.com/Repositories/C23/54/24/Acc http://www.accenture.com/us-en/Pages/insight-

enture_Banking_2016_v14_PRINT.pdf banking-technology-vision-reshaping-landscape-

http://www.accenture.com/us-en/Pages/insight-banking- summary.aspx

2012-revenue-growth-innovation-summary.aspx

Digital https://kxws.accenture.com/Repositories/C25/73/9/Accenture% https://kxws.accenture.com/Repositories/C23/82/64/12-

20Interactive_Banking_Social%20Engaging_Banking_3_14_13 1315_BankingCloud_v5.1_Final_May2012.pdf

.pdf https://kx.accenture.com/repositories/contributionform.as

https://kxws.accenture.com/Repositories/C25/17/54/Accenture px?path=C25/89/26&mode=read

%20Interactive_PoV_Banking_on_Digital_1_8_13.pdf

Customer Centricity https://kx.accenture.com/Repositories/ContributionForm.aspx?p http://www.accenture.com/us-en/Pages/insight-boosting-

ath=C26/36/72&mode=Read relevance-returns-digital-channel-banking-summary.aspx

Agility Omni-Channel https://kxws.accenture.com/Repositories/C23/54/24/Accenture_ http://www.accenture.com/us-en/Pages/insight-banking-

Banking_2016_v14_PRINT.pdf 2016-next-generation-banking-summary.aspx

Potential

New Talent Dynamic http://www.accenture.com/us-en/Pages/insight-going-above- http://www.accenture.com/us-en/Pages/insight-global-

beyond-banks-optimize-talent.aspx analytics-shortage-banking-summary.aspx

Optimal Financial http://www.accenture.com/us-en/Pages/insight-basel- http://www.accenture.com/us-en/Pages/insight-cfo-

consequences-summary.aspx catalyst-change.aspx

Strategies

Channel Fulfillment https://kxws.accenture.com/Repositories/C23/54/24/Accenture_ http://www.accenture.com/us-en/Pages/insight-power-

Banking_2016_v14_PRINT.pdf online-banking-channel-summary.aspx

Streamline & Simplify http://www.accenture.com/us-en/Pages/insight-banks-rise- https://kxws.accenture.com/Repositories/C25/99/9/WSS

global-transformation-challenge-summary.aspx 153_CoreBankingTop3Reasons7.pdf

http://www.accenture.com/us-en/Pages/insight-banking-2016- https://kxws.accenture.com/Repositories/C22/96/48/Win

next-generation-banking-summary.aspx ningInNewBankingEra.pdf

https://kx.accenture.com/repositories/contributionform.as

px?path=C25/93/90&mode=read

Manage Regulations http://www.accenture.com/us-en/Pages/insight-dodd-frank-act- http://www.accenture.com/us-

Optimization & strategic-tactical-implications.aspx en/blogs/regulatory_insights_blog/archive/2011/11/16/inf

Simplification ormation-management-impacts-of-recent-financial-

regulation.aspx

Manage Enterprise http://www.accenture.com/us-en/Pages/insight-rethinking-risk- http://www.accenture.com/us-en/Pages/insight-acn-

financial-institutions-partnership.aspx 2012-risk-analytics-study-insights-banking-industry.aspx

Risk

Capital & Funding http://www.accenture.com/us-en/Pages/insight-capital- http://www.accenture.com/us-en/Pages/insight-

optimization-summary.aspx navigating-complexities-liquidity-risk.aspx

Strategies http://www.accenture.com/us-

en/blogs/regulatory_insights_blog/archive/2012/03/19/regulatio

n-in-the-news.aspx

Copyright © 2014 Accenture All rights reserved. 40You can also read