OCEAN FREIGHT MARKET UPDATE - DHL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

PUBLIC

DHL Global Forwarding, Freight

OCEAN FREIGHT

MARKET UPDATE

February 2019

Publication Date 30th January 2019

1

PUBLIC

Contents

TOPIC OF THE MONTH

Top 12 carrier’s 2019 capacity expansion plans

HIGH LEVEL DEVELOPMENT

MARKET OUTLOOK

Freight Rates and Volume Development

ECONOMIC OUTLOOK & DEMAND DEVELOPMENT

CAPACITY DEVELOPMENT

CARRIERS

REGULATIONS

DID YOU KNOW?

? Top 15 container ports

DHL Global Forwarding | OFR Market Update | Feb 2019 2

Topic of the Month

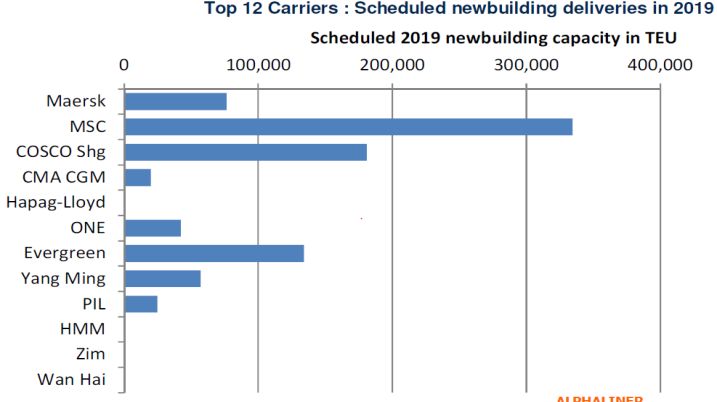

Top 12 carrier’s 2019 capacity expansion plans

Top 12 Carriers : Scheduled Newbuilding Deliveries in 2019

MSC has the largest newbuilding pipeline of all carriers this year, with some 20 orders,

aggregating a total capacity of 334,550 TEU. The carrier’s orderbook includes 8 megamax

units of 23,000 TEU, with 8 deliveries of such vessels expected for the 2 nd half of the year. All of

the megamax units are destined for the Asia-North Europe route, although no new string is

expected to be launched this year, as the 2M partners (Maersk/MSC) have announced the

extension of the rotation of six Asia-Europe strings that should take up some of these ships. The

newbuildings are also expected to cover for some of the existing ships in MSC’s fleet that will go

out of service for weeks or months for scrubber retrofitting in the 2 nd half of this year. In addition to

its substantial new ship pipeline, MSC is expected to launch a vessel jumboisation program

this year.

COSCO Shipping has the second largest vessel orderbook in 2019, with 12 units and a total

capacity of 180,970 TEU. Most of the ships are expected to be delivered in the 1st half of the

year. Notably, another 6 19,200 – 21,200 TEU units will complete COSCO Group’s current ‘megamax’ vessel program. The 6 new megamaxes are expected to

join the OCEAN Alliance’s Far East – North Europe ‘NEU3/AEU7’ loop, replacing ships of 13,000 – 14,000 TEU.

Evergreen has an orderbook of 10 ships in 2019, including 6 G-class 20,388 TEU units. The first 2 G-class megamax units will be assigned to the Asia – North

Europe CEM service, which is currently being upgraded from the 13,800-14,000 TEU size to the 20’000 TEU scale. The remaining G-class units are expected to

follow onto the same service later this year. Evergreen is also expected to launch a jumboisation program for some of its 8,500 units later this year.

Hapag-Lloyd, ZIM and Wan Hai have no new ships due for delivery in 2019. All 3 carriers will have to rely on the charter market for any capacity expansion this

year. This counts also for carrier HMM. It’s newbuilding program includes 12 ships of 23,000 TEU and 8 units of 15,000 TEU, but this will only be delivered in the

2nd quarter of 2020 and 2021 respectively.

Source: Alphaliner

DHL Global Forwarding | OFR Market Update | Feb 2019 3

PUBLIC

High Level Market Development – Supply and Demand

ECONOMIC OUTLOOK GDP GROWTH BY REGION1) DHL TRADE BAROMETER6) SUPPLY/DEMAND

SUPPLY/DEMANDGROWTH

GROWTH(ANNUALIZED),

(ANNUALIZED), IN % 2)2)

IN%

75

7%

CAGR 70

2018F 2019F 2020F 2021F 2022F 6%

(2019-22) 65

60 5% Demand

EURO 2.1% 1.6% 1.5% 1.5% 1.7% 1.6% Growth

55 4% %

MEA 2.9% 3.1% 3.4% 3.3% 3.3% 3.3%

50 3%

AMER 2.6% 2.6% 2.1% 1.8% 1.8% 2.1%

45 Ocean 2%

ASPA 4.9% 4.7% 4.5% 4.7% 4.7% 4.7% 40 Supply

Global 1%

35 Growth %

DGF World 3.3% 3.1% 2.9% 2.8% 2.9% 2.9% 30

0%

2016 2017 2018F 2019F 2020F 2021F 2022F

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

’16 ’17 ’18

WORLD CONTAINER INDEX (WCI)3) SHANGHAI CONTAINERIZED FREIGHT INDEX (SCFI)4) BUNKER PRICE INDEX5)

3,000 1,200 1,000

1,100

2,500 800

1,000

2,000

900 600

1,500 800

700 400

1,000 Actual Actual BIX 380

600

200

500 Forecast Forecast BIX MGO

500

0 400 0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

’17 ’18 ’19 ’17 ’18 ’19 17 18 ’19

1) real GDP, Global Insight, Copyright © IHS, Q4 2018 . All rights reserved. 2) Demand growth = Port-to-Port Container Traffic growth. Supply growth = Fleet Growth. Source: Drewry Maritime Research. 3) Drewry, in USD/40ft container, including BAF & THC both ends, 42 individual routes, excluding

intra-Asia routes, 5.5% predicted freight rate increase. 4) Shanghai Shipping Exchange, in USD/20ft container & USD/40ft ctnr for US routes, 15 routes from Shanghai. 5) Bunker Index, in USD/metric ton, Bunker Index MGO (BIX MGO) = avg. Global Bunker Price for marine gasoil (MGO) port prices; (BIX

380= avg. Global Bunker Price for all 380 centistoke (cSt) port prices; both index published on the Bunker Index website., Forecast based on HIS Market assumption of avg. USD70 per Brent barrel equaling Nov18 price. 6) DHL Global Trade Barometer Mar18, index value represents weighted average of

current growth and upcoming two months of trade, a value at 50 is considered neutral, expanding above 50, and shrinking below 50.

DHL Global Forwarding | OFR Market Update | Feb 2019 4

PUBLIC

Market Outlook February 2019 – Major Trades

Carriers have announced an extensive blank sailing program in anticipation of the weaker demand during Chinese New Year

EXPORT REGION IMPORT REGION CAPACITY RATE EXPORT REGION IMPORT REGION CAPACITY RATE

AMNO = + AMNO = ++

EURO AMLA

AMLA = =/- ASPA + +

ASPA + =/- EURO = ++

MENAT + =/- MENAT = +

SSA = = SSA -- ++

AMLA = + ASPA - =

AMNO ASPA

ASPA = = AMNO - -

EURO = = AMLA = -

MENAT = = EURO -- =

SSA = + MENAT - =

--(AU) = (AU)

OCEANIA

KEY

Strong

++

Moderate

+

No

=

Moderate

-

Strong

-- - (NZ) + (NZ)

Increase Increase Change Decline Decline

Source: DGF

DHL Global Forwarding | OFR Market Update | Feb 2019 5PUBLIC

Market Outlook February 2019 – Ocean Freight Rates Major Trades

Market outlook on smaller trades available in the back-up

OCEAN FREIGHT RATES OUTLOOK

overall space situation is getting tight before the Chinese New Year holiday. An extensive blank sailing program is in place from all

ASPA – EURO

alliances as a reaction to the low demand and will start from wk5 onwards.

Ocean rates remain stable resp. slightly decreasing for certain commodities and short term agreements due to the space and bunker

EURO – ASPA & MEA

development.

Space continue to be tight to Mexico & WCSA, while ESCA is manageable. Space issues expected post Chinese New Year to

ASPA – AMLA

Mexico/WCSA and ECSA due to multiple blank sailings from all carriers.

ASPA – AMNO No major rush prior Chinese New Year. Extensive blank sailings are expected between wk6 to wk8 (particularly into USEC).

Ocean rates are strong and still increasing; inland carriages in US remain problematic; congestion on USEC & CAEC causes severe

EURO – AMNO

delays into USMW area

As predicted, space is getting tight before Chinese New Year period. Carriers are also restricting low paying cargo onboard. Most of the

ASPA – MENAT

FAK rates have been extended till mid February.

ASPA – ASPA Blank sailings have been planned during the Chinese New Year period. No significant changes to the FAK rates expected.

AMNO – EURO No change with rates & Capacity in February. Space remains tight out of Houston.

Source: DGF

DHL Global Forwarding | OFR Market Update | Feb 2019 6PUBLIC

Economic Outlook & Demand Development

Danger of global economic downturn has risen, probability of a recession in 2019 still low

Fiscal stimulus coming in DE, FR & IT will lead to a temporary pickup in real GDP in Q1 ’19. UK parliament’s rejection of the Withdrawal

EURO

Agreement support cautious near-term UK growth projections.

Recent turbulences in financial markets implied that volatility had spiked, and risk spreads had widened. The partial government shutdown

AMNO

in Jan will cut an estimated 0.1 percentage point from real GDP growth, and the assumption is that losses will be recovered in Q2.

Real GDP recovered in JP in Q4 18, tanks to a rebound in domestic demand – consumer spending & capital expenditure remain solid.

However, imports increased more rapidly than exports in Q4. The scheduled increase in sales tax in Oct ’19 will contribute to volatility in

ASPA quarterly GDP growth patterns, as consumers & businesses shift purchases forward. Economic growth in CN should stabilize as the

Government’s measured stimulus policies gradually kick in. Meanwhile, exports, industrial production, & retail sales have decelerated, as

has factory price inflation.

EMERGING While currency pressures on emerging markets have eased, weakening global growth and more pessimism on commodity prices will do

MARKETS little to boost growth prospects.

JPMorgan Global PMI sank to its lowest level in 27 months. Meanwhile, optimism about the year ahead slipped to its weakest reading in 2 ½

DEMAND

years, suggesting the slowdown has further to run. Deteriorating goods trade was once again the major factor behind the slowdown.

DEVELOPMENT

Manufacturing PMIs for a number of countries (CN, FR, IT, CZ,PL, TW, MY, KR, MX, TR) are below the 50-point threshold.

Source: IHS Markit Global Executive Summary, IHS Purchasing Manager Index Manufacturing, a PMI at 50 is considered neutral, expanding above 50, and business shrinking below 50.

DHL Global Forwarding | OFR Market Update | Feb 2019 7PUBLIC

Carriers / Capacity

CARRIERS

The OCEAN Alliance members CMA CGM, COSCO Shipping, Evergreen and OOCL (part of COSCO Group) have unveiled their new ‘Day 3 Product’ that is

due to start from April 2019. It will offer 38 liner services on East – West trades, to be ensured with 330 ships, representing a total fleet capacity of 3.8 MTEU.

The 4 carriers have also decided to extend their cooperation until 31 Mar 2027. The OCEAN Alliance was launched in Apr 2017 for an initial period of 5 years with

an option for a 5-year renewal. The OCEAN Alliance ‘Day 3 Product’ is an expansion of the current ‘Day 2 Product’ with several significant enhancements,

such as, addition of a 7th Far East – North Europe loop, with a full up-grade of a 3rd string to the 20,000 TEU scale, an upgrade of the Far East – Middle

East ‘MEA5’ service to the 20,000 TEU scale. This will make the ‘MEA5’ the first service to employ megamax ships outside of the Asia – North Europe route and

an improved Vietnam coverage.

The OCEAN Alliance is expected to continue to expand at the fastest pace in 2019, compared to its rivals in 2M and THE Alliance. OCEAN Alliance’s growth

will be pushed by the scheduled deliveries of ULCS newbuilding for COSCO and Evergreen. Although MSC also has substantial pipeline of ULCS units

scheduled for delivery this year, most of MSC’s ships will be delivered in the 2 nd half of the year, while COSCO and Evergreen’s ships will be mostly delivered in

the 1st half.

ZIM and the 2M partners (Maersk and MSC) will extend their cooperation to the Transpacific North West and Asia – East med routes from March 2019,

subject to regulatory approvals. They already had concluded a 1st strategic cooperation agreement for the Asia – US East Coast trade in Jul 2018. Although this

extended cooperation will bring some changes in the services the overall trade capacity is expected to remain largely unchanged, with the 2M services to be

upsized to accommodate the ZIM volumes.

CAPACITY DEVELOPMENT

The idle containership fleet fell slightly to 561,187 TEU as at 7 Jan 2019, with healthy capacity utilization on the Asia – Europe and Transpacific routes over the

year and keeping idle capacity in check. The number of idle ships of over 12,500 TEU dropped to only 8 units compared to 13 ships in Dec 2018. This mainly due to

the return of several vessels to active duty on the Asia- Europe route, involving Maersk, CMA CGM, Hapag-Lloyd and Yang Ming tonnage. However vessel

demand is expected to fall again in February as the Lunar New Year holidays in the Far East starting on 5 Feb 2019, will put more ships out of work.

Source: Alphaliner, Dynaliners, carriers

DHL Global Forwarding | OFR Market Update | Feb 2019 8PUBLIC

Drewry’s Altman Z-Score as of 1 Dec 2018

Assets Book Value Liabilities Retained

Company Period Period Ended Units Net Sales EBIT Z-Score

Total Current of Equity Total Current Earnings

OOIL 1) 6 months 30. Jun 18 million US$ 3'115 51 9'939 3'136 4'637 5'302 1'580 4'575 2.28

AP Moeller-Maersk 9 months 30. Sep 18 million US$ 28'837 408 61'787 23'232 34'116 27'671 12'229 29'749 2.24

CMA CGM 9 months 30. Sep 18 million US$ 17'176 399 20'381 6'115 5'632 14'749 5'991 5'276 1.81

Wan Hai 9 months 30. Sep 18 million NT$ 48'185 474 75'695 26'449 34'279 41'416 19'785 11'649 1.69

Hapag-Lloyd Holding 9 months 30. Sep 18 million euro 8'428 301 15'099 1'742 6'192 8'907 3'101 3'086 1.43

NYK group 9 months 30. Sep 18 billion Yen 916 -4 2'096 502 565 1'532 604 331 1.24

K Line group 9 months 30. Sep 18 billion Yen 416 -12 1'037 322 285 753 243 102 1.18

Evergreen Marine Corp 9 months 30. Sep 18 million NT$ 120'035 -1'015 218'491 62'598 66'626 151'865 50'194 8'850 1.10

MOL group 9 months 30. Sep 18 billion Yen 620 15 2'263 415 654 1'609 532 311 0.97

Pacific International Lines 6 months 30. Jun 18 million US$ 2'244 -38 6'666 1'714 1'728 4'938 2'349 952 0.93

Yang Ming 9 months 30. Sep 18 million NT$ 103'349 -6'223 140'155 33'289 20'449 110'705 47'530 -7'037 0.71

China Cosco 2) 9 months 30. Sep 18 million RMB 82'130 1'565 227'872 64'350 54'986 172'886 95'823 10'216 0.60

Zim 9 months 30. Sep 18 million US$ 2'395 -125 1'802 630 -186 1'909 653 -1'879 -0.07

Hyundai Merchant Marine 9 months 30. Sep 18 billion Won 3'777 -493 3'419 951 337 3'082 1'059 -3'310 -0.49

The Z-Score is a statistical analysis to predict a company’s probability of failure in the next two years, using data from the company’s financial statement.

Z-Score 2.99 = company is “safe”; Z-Score between 1.8 and 2.99 = exercise caution (“grey zone”); Z-Score 1.8 = Higher risk of the company going bankrupt

(“distress zone”)

Source: Drewry Sea & Air Shipper Insight Aug 2018, 1) parent of OOCL, 2) parent of Cosco Container Lines; Z-score is calculated as follows: T1 = (Current Assets - Current Liabilities) / Total Assets, T2 = Retained Earnings / Total Assets, T3 =

Annualized EBIT / Total Assets, T4 = Book Value of Equity / Total Liabilities, T5 = Annualized Sales / Total Assets, Z-score bankruptcy rating = 1.2*T1 + 1.4*T2 + 3.3*T3 + 0.6*T4 + 1.0*T5

DHL Global Forwarding | OFR Market Update | Feb 2019 9Did you know?

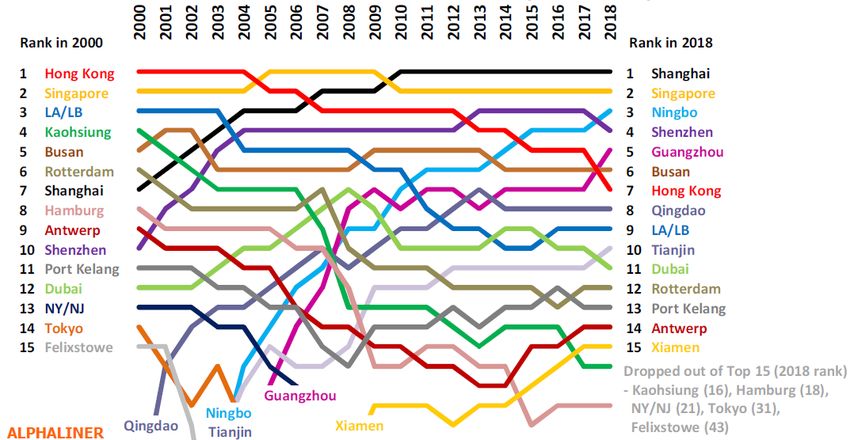

Top 15 Container Ports

Change in Top 15 Container Port Rankings 2000-2018

• The number of major ports in Asia has climbed from 8 to 11

in 18 years , out of these 11 Asian ports 7 are in China

• European ports are the big losers as their number has

reduced by half, with Hamburg and Felixstowe dropping out

of the Top 15 altogether

• Hong Kong is also suffering. Throughput has declined in 7

out of the last 10 years since its peak of 24.49 mTEU in

2008. Hongkong International Terminals (HIT), Modern

Terminals (MTL), COSCO-HIT Terminals (CHT) and Asia

Container Terminals (ACT) have therefore announced on 8

Jan the formation of the Hong Kong Seaport Alliance, a joint

operating agreement aimed at combating the decline in

container volumes

Source: Alphaliner

DHL Global Forwarding | OFR Market Update | Feb 2019 10PUBLIC

BACK-UP

11PUBLIC

Market Outlook January 2019 – Ocean Freight Rates Additional Trades (1/2)

OCEAN FREIGHT RATES OUTLOOK

EURO – AMLA Capacity unchanged, space is available, rates remain stable and are expected to slightly decrease until end of Q1

EURO – MENAT ME region shows same trend as ASPA; low space but stable rates

EURO – SSA Rates remain stable and space is available. Congestion / PSS surcharge for PODs in Nigeria from all carriers still in force

Rates in the market are stable. Space can be an issue from US Gulf Coast while bookings are 2 weeks out. USEC is in a better shape where

AMNO – MENAT

we mostly can manage to get space for the next week sailings.

Rates to South Africa and West Africa were stable for long time but direct carriers announced GRIs for February. No changes in capacity.

AMNO – SSA

Space is available. (Direct Service is currently shared by Maersk/Safmarine/MSC/HSUD).

AMNO – AMLA Fuel is raising cost slightly. Q 1 2019 outlook soft to begin the year.

Roll over and space constraints affecting entire region. MX/BR/SAWC region facing port omissions/blank sailings/congestion. Shippers are

strongly urged to provide forecasts 4-6 weeks out.

AMLA Exports Lack of trucking capacity in Mexico interrupting supply chain/extensive delays in cargo movement.

GRI’s and Emergency Fuel surcharges announced daily on all trades.

F/Time/Drop off conditions coming with a cost.

Heavy delays at several rail ramps and ports affecting export cargo. Market is stable in terms of rates for January / February. Space is tight for

AMNO – ASPA

Oceania direct services off USWC. Pre-booking 2-3 weeks ahead recommended.

Source: DGF

DHL Global Forwarding | OFR Market Update | Feb 2019 12PUBLIC

Market Outlook January 2019 – Ocean Freight Rates Additional Trades (2/2)

OCEAN FREIGHT RATES OUTLOOK

EURO MED - AMNO Unchanged / stable. Nothing to be highlighted

EURO MED – AMLA Unchanged / stable. Nothing to be highlighted

EURO MED – ASPA Unchanged / stable. Nothing to be highlighted

EURO MED – MENAT Unchanged / stable. Nothing to be highlighted

EURO MED – SSA Unchanged / stable. Nothing to be highlighted

Average weekly blank sailing for February hovers at 40-45% after a very slight peak in January this year. FAK has been extended to

ASPA-SPAC

mid/end-February as no extreme space issue is anticipated.

Source: DGF

DHL Global Forwarding | OFR Market Update | Feb 2019 13PUBLIC

Market Outlook – Volume Outlook in Main Trade Lanes, 2018 Estimate &

2019/22 Growth Forecast in %

2018e, in mTEU 2019e-2022e CAGR, in %

N O R T H N O R T H

A M E R I C A A M E R I C A

I n c l . 4.0 mTEU +2.4% 8.5 mTEU +4.7% I n c l .

M E X I C O F A R E A S T M E X I C O

2.2 mTEU +3.1% 12.8 mTEU +2.4% 18.7 mTEU +3.1%

2.0 mTEU 1.6 mTEU

+4.5% +4.3% 1.6 mTEU +4.3% E U R O P E 7.3 mTEU +3.4% 1.7 mTEU +2.2%

L A T I N L A T I N

I n c l . M E D

A M E R I C A 1.7 mTEU +2.5% 4.2 mTEU +4.6% A M E R I C A

INTRA ASIA

excl. Oceania

41.6 mTEU +4.8%

GLOBAL CONTAINER TRADE 2018e 152.6 mTEU +4.1% CAGR 2019e-2022e

Mid-term growth is mainly driven by Asian tradelanes.

Source: Seabury Nov18 update

DHL Global Forwarding | OFR Market Update | Feb 2019 14PUBLIC

Carrier Mergers, Acquisitions and Alliances

M E R G E R S A N D A Q U I S I T I O N S

United Hyundai

China CMA Hapag Hamburg Maersk Yang

Cosco OOCL Evergreen APL Arab Merchant MSC K Line MOL NYK

Shipping CGM Lloyd Süd Line Ming

Shipping Marine

HYUNDAI

CHINA COSCO SHIPPING EVER CMA CGM MAERSK LINE OCEAN NETWORK YANG

HAPAG-LLOYD MERCHANT MSC

OOCL GREEN APL MARINE Hamburg Süd EXPRESS (ONE) MING

A L L I A N C E S

F O R M E R A L L I A N C E S P R E S E N T A L L I A N C E S

MAERSK LINE OOCL

CMA CGM

MSC

MAERSK LINE CHINA SHIPPING OCEAN CMA CGM

2M OCEAN 3 2M HMM (strategic

MSC UNITED ARAB

cooperation until Apr

ALLIANCE CHINA COSCO SHIPPING

SHIPPING COMPANY EVERGREEN

2020)

HAPAG-LLOYD HYUNDAI COSCO

HAPAG-LLOYD

MOL MERCHANT EVERGREEN K-LINE

G6 MARINE CKYHE THE ALLIANCE ONE

NYK HANJIN YANG MING

OOCL YANG MING

APL SHPPING

*Source: Carriers

DHL Global Forwarding | OFR Market Update | Feb 2019 15PUBLIC

Acronyms and Explanations

2M - Carrier Alliance: Maersk / MSC Ocean 3 - Carrier Alliance: CMA, UASC, China Shipping

AMLA - Latin America OCRS - Operational Cost Recovery surcharge

AMNO - North America OOCL - Orient Overseas Container Line

AR - Argentina OWS - Overweight Surcharge

ASPA - AsiaPacific PH - Philippines

BR - Brazil PNW - Pacific North West

CAGR - Compound Annual Growth Rate Ppt. - Percentage points

CENAC - Central Amercia and Caribbean PSW - Pacific South West

CKYHE - Carrier Alliance: Cosco, K-Line, YangMing, Hanjin and Evergreen RR(I) - Rate Restoration

CNC - CNC Line (Cheng Lie Navigation Co. Ltd.) SAEC - South America East Coast

DG - Dangerous Goods SAWC - South America West Coast

DWT - Dead Weight Tonnage SOLAS - Safety of Life at Sea

EB - Eastbound SPRC - South People’s Republic of China – South China

ECSA - East Coast South America SSA - Sub-Saharan Africa

EGLV - Evergreen Marine Corp SSL - Steam Ship Line

EURO - Europe T - Thousands

FMC - US Federal Marine Commission TEU - Twenty foot equivalent unit (20‘ container)

G6 - Carrier Alliance: APL, Hapag Lloyd, Hyundai, MOL, NYK and OOCL TP - Trans Pacific

GRI - General Rate Increase TSA - Trans Pacific Stabilization Agreement

HJS - Hanjin Shipping ULCS - Ultra Large Container Ship

HMM - Hyundai USGC - US Gulf Coast

HL - Hapag -Lloyd US FMC - US Federal Maritime Commission

HSUD - Hamburg Süd USEC - US East Coast

HWS - Heavy Weight Surcharge USWC - US West Coast

IA - Intra Asia VGM - Verified Gross Mass

IPBC - India Pakistan Bangladesh Colombo VLCS - Very Large Container Ship

IPI - Inland Point Intermodal VSA - Vessel Sharing Agreement

ISC - Indian Sub Continent WB - Westbound

MENAT - Middle East and North Africa WCSA - West Coast South America

ML - Maersk Line WHL - Wan Hai

mn - Millions YML - Yang Ming Line

MoM - Month-on-Month YoY - Year-on-Year

NOO - Non-operating (vessel) owners YTD - Year-to-Date

DHL Global Forwarding | OFR Market Update | Feb 2019 16You can also read