Our leadership in smart beta and Factor investing positions PowerShares for strong future growth - September 2016

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Our leadership in smart beta and Factor investing positions PowerShares for strong future growth September 2016

Forward-looking statements This presentation, and comments made in the associated Web cast today, may include “forward-looking statements.” Forward-looking statements include information concerning future results of our operations, expenses, earnings, liquidity, cash flow and capital expenditures, industry or market conditions, AUM, acquisitions and divestitures, debt and our ability to obtain additional financing or make payments, regulatory developments, demand for and pricing of our products and other aspects of our business or general economic conditions. In addition, words such as “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “projects,” “forecasts,” and future or conditional verbs such as “will,” “may,” “could,” “should,” and “would” as well as any other statement that necessarily depends on future events, are intended to identify forward- looking statements. Forward-looking statements are not guarantees, and they involve risks, uncertainties and assumptions. There can be no assurance that actual results will not differ materially from our expectations. We caution investors not to rely unduly on any forward-looking statements and urge you to carefully consider the risks described in our most recent Form 10-K and subsequent Forms 10-Q, filed with the Securities and Exchange Commission. You may obtain these reports from the SEC’s website at www.sec.gov. We expressly disclaim any obligation to update the information in any public disclosure if any forward-looking statement later turns out to be inaccurate. All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This presentation is provided for informational purposes only and is not to be construed as an offer to buy or sell any financial instruments and should not be relied upon as the sole factor in an investment making decision. As with all investments there are associated inherent risks. Please obtain and review all financial material carefully before investing. This does not constitute a recommendation of the suitability of any investment strategy for a particular investor. The opinions expressed are based on current market conditions and are subject to change without notice. Past performance is not a guarantee of future results. All products and services mentioned in this document are made available via affiliated entities of Invesco Ltd. 2 US10880

Our speakers today Dan Draper Lorraine Wang Eric Pollackov Global Head of Head of Global Head of Global ETF Invesco PowerShares ETF Products & Research Capital Markets 3

Agenda Introduction Factor-based investing ETF market landscape Smart beta ETFs Product strategy & research Institutional Capital markets Questions 4

Introduction 5

We manage Invesco with a single focus: to help clients achieve their investment objectives Every client has a unique set of investment objectives, which can be achieved in a variety of ways Invesco’s comprehensive range of high-conviction investment capabilities has been constructed over many years to help clients achieve their investment objectives Our fundamental and factor-based methodologies aim to deliver client outcomes that go beyond the limitations of traditional passive investing and benchmark-centric active management We believe this high-conviction approach provides better tools to build portfolios in a more precise and impactful way 6

We’ve positioned our business ahead of

client demand trends

Client demand themes Invesco’s positioning

Search for yield In 2007, began expansion of global fixed income platform, which

today supports the full range of single-sector and multi-sector

capabilities

Continue to expand the full range of income-related capabilities,

including equities, fixed income and alternatives

“Barbelling” and the Continued to expand our comprehensive range of all-weather, high-

shift to passive, beta conviction capabilities

and ETF products Began factor investing in 1983

Added PowerShares in 2006 – smart beta line remains broadest,

most diverse in the industry

Continue to accelerate our ETF business globally

Multi-asset strategies Introduced risk parity strategy in 2008

and absolute return Built new Invesco Perpetual multi-asset team beginning in 2012;

expanding to new markets

Invesco Quantitative Strategies (IQS) added global market neutral

capability in 2008

7

We’ve positioned our business ahead of

client demand trends

Client demand themes Invesco’s positioning

Growing demand Entered direct real estate business in 1991; completed the

for alternatives globalization of our real estate capabilities by adding the Asia team

in 2010

Expanded into private equity through WL Ross & Co. in 2006

Continued to broaden our range of alternative strategies with the

launch of more than 40 liquid alternatives offerings globally

beginning in 2011; today the range represents one of the most

comprehensive lineups in the industry

Increasing demand Invesco Solutions builds and manages goal-oriented, multi-asset

for solutions and new strategies aligned to client outcomes

advice models Early entrant into the digital advice space through the addition of

Jemstep in 2016

8

We enable outcomes that help clients around the

world achieve their investment objectives

Our comprehensive range of investment capabilities …

Equity Fixed Income and Balanced Alternative

Money Market

$349B AUM $269B AUM $47B AUM $116B AUM

Global/Multi-Region Multi-Sector Traditional Directional Strategies Macro Strategies

Global Global Agg/Core Plus Global Balanced Long/Short Equity Global Macro

Global ex Domestic Multi-Sector Credit Domestic Balanced Private Equity

Relative Value/

Emerging Markets Strategic Income Bank Loans

Non-Traditional Absolute Return

Regional/ Single-Sector Risk Parity Inflation-Protection Market Neutral Equity

Single Country Investment Grade Target Maturity Commodities Unconstrained Bond

Asian/Asia ex Japan High Yield Target Risk Public Real Estate

Financial Structures

Australian Structured Securities Custom Solutions Securities

Credit Arbitrage

Greater China Convertibles Private Real Estate

Opportunistic

Japanese Municipal Bonds

European/UK

Specialty

US

EM Debt

Canadian

Stable Value

Sector-Based Global Liquidity

… are delivered through diverse investment vehicles …

Institutional Collective Mutual funds Exchange-traded

Unit investment trusts (UITs)

separate accounts trusts (open/closed-end, on/offshore) funds (ETFs)

Private Sub-advised Separately managed accounts/ Variable

Customized solutions

placements portfolios Unified managed accounts insurance funds

… to enable key outcomes that help our clients around

the world achieve their investment objectives

Income Capital preservation Growth

* All data as of June 30, 2016.

9

We help clients build better portfolios through

high-conviction investing

High conviction

Fundamental Benchmark

Fundamental active

centric

Benchmark-centric Strategies constructed through active security selection to

fundamental strategies generate alpha

Factor-based Traditional Factor-based

Smart beta

beta active

Replication of market- Transparent, rules-based Strategies that

cap-weighted strategies that provide systematically apply active

benchmarks alternatives to market-cap- insights to target specific

weighted indices by isolating risk/return expectations

specific factors to provide

exposure and/or seek to

mitigate risk

Passive Active

10Our entire organization is focused on helping

clients achieve their investment objectives

Success driver Invesco position

Deep Deep knowledge of clients and their evolving needs

understanding Comprehensive, all-weather, high-conviction, fundamental and factor investing

of client needs product line

Demonstrated ability to combine a broad range of capabilities to construct portfolios

aligned with client investment objectives by channel and by region

Pure focus on No competing lines of business to support

investment Strong investment reputation

management

Independence

Infrastructure and client support platforms that enable our investors to spend more

time focused on investing

Experienced, Specialized, stable investment teams with discrete investment perspectives and

stable and experience across diverse market cycles

accountable Disciplined, repeatable investment philosophy and processes

investment

leadership Strong risk management and oversight

Compensation aligned with performance and client interests

Organizational Broad and deep global presence in key markets

strength Solid margins, financial strength, and resources to ensure long-term investment in

the business

6,500+ highly engaged and motivated employees focused on client needs

Proven management team with a solid track record

Source: Data as of June 20, 2016.

11Invesco’s ability to help clients achieve their

objectives differentiates us in the market

It is the totality of our organization that makes Invesco highly differentiated in the

marketplace and positions us for growth and success over the long term

Independent Depth and breadth of Diversification across

capabilities channels, asset classes

and geographies

Search for yield

Barbelling (factor and

fundamental investing) Channels

Multi-asset solutions and

absolute return

Asset classes

Growing demand for Geographies

alternatives

Increasing demand for

solutions

For illustrative purposes only

12Invesco is an innovative leader in factor investing

with $150B in AUM and 40 years’ experience

Factor based investment strategies

Invesco Quantitative Invesco Unit Trust

PowerShares

Strategies (IQS)

$96.1bn in AUM $34.5bn in AUM $19.2bn in AUM

4th largest ETF provider* Global presence with teams 2nd largest unit trust provider

Factor-based smart beta across four continents Factor-based smart beta

pioneer since 2003 Factor-based active packaged in unit trusts

11 investment professionals since 1983 since 1975

140 ETFs 43 investment professionals 19 investment professionals

Globally delivered through 74 unit trusts

mutual funds, collective trusts

and separate accounts

Differentiating attributes

Diverse, time-tested investment strategies

All vehicles available to meet investor needs

Product specialists and field wholesaler depth

Education and thought leadership support

*Bloomberg L.P. Data as of June 30, 2016

Source: Data as of June 30, 2016.

13Factor-based investing 14

Which is better – active or passive?

Invesco believes this is the wrong question to ask A more

important

At Invesco, we believe in striving for superior client question: “are

experience through high-conviction investing – going you willing to

beyond the limitations of traditional passive investing and settle for

benchmark-centric active management average”

High conviction means our fundamental-based active

managers trust their research, have confidence in their

discipline and build portfolios that are a reflection of their

beliefs – not benchmarks

It also means that our factor-based active and smart

beta strategies go beyond the traditional, market-cap-

weighted passive benchmark approach

15Moving the industry from “Mass Production” to

“Mass Customization”

Invesco believes this is occurring largely due to Factor investing

supports a

Investors behavioral biases better

diversified

Harvesting of Factor Risk Premium portfolio

Stronger expression of Investment views

More efficient risk-adjusted performance

Evolution away from cap-weighted benchmarks

16Factor investing is to look at the investable

world through a particular lens

What is a Factor?

A factor is a quantifiable characteristic of an asset

– Can be directly observable characteristics such as size, momentum or value

– Can refer to statistical relationships such as the part of price moves that can be

explained by a variable such as inflation, consumption, etc.

They explain the return and risk characteristic of portfolios

Are often associated with a risk premium that investors receive for either bearing an

undesirable return profile (i.e. low returns in bad times) or for behavioral reasons that

prevent arbitrage of such factors

What is Factor Investing?

Factor investing is to look at the investable world through a particular lens

Tradable securities (e.g. stocks) are used as the instruments to achieve the factor

exposures

A factor portfolio may target exposure to a single factor or a combination of factors

Similar to other investments, factors possess observable risk and return profiles

Diversification & Factor Allocation involves the choice of allocation across factors in a

way that trades off these risk and return profiles to achieve particular investment goals

17Factor strategies should have a robust investment case and be implemented using well designed products Investment case Evidence – empirical evidence must support the Factor Belief – understand the economic and/or behavioral rational Sustainability – consider the factor is likely be competed away in the future Well designed products Systematic – a repeatable process that does not signify discretionary management Broad – large opportunity set to minimize risk coming from individual securities Simple – transparent and only as complicated as needed to achieve investment goals Cost effective – fees and costs should be considered in all stage of the process 18

ETF Market Landscape 19

We believe our leadership in smart beta/factor

investing positions PowerShares for strong

future growth

PowerShares is a pioneer of smart beta ETFs with a launch of its Our leadership

multi-factor range of Intellidex ETFs in 2003 – today’s smart betain smart

range of 93 ETFs is over $42B in AUM

beta/factor

Over the past 13 years PowerShares has created the most investing keeps

comprehensive range of smart beta and factor ETFs in the industry us competitive

– spanning equities, fixed income and alternatives

against existing

Over 70% of our smart beta and factor ETFs have greater than a players/new

5 year historical track record

entrants and

PowerShares has successfully partnered with a number of positions us for

Invesco’s active investment teams to create leading ETFs, e.g., future growth

senior bank loans and real estate

and success.

PowerShares is well positioned to become a leading component

provider for emerging packaged solutions, e.g. Rhode Island 529

plan, digital advice, etc.

PowerShares is one of a handful of ETF players with global

capabilities highlighted by local ETF platforms in the U.S., Canada

and EMEA

PowerShares is investing in strong and scalable infrastructure in

preparation for the expected high growth of smart beta and factor

ETFs in the future

Source: PowerShares Global ETF Products & Research, as of June 30, 2016.

204th largest US ETF provider:

Focused on smart beta & access

Top 3

ETF Industry Products

No. of AUM Market 12 Month Net as a %

Rank Firm Description Products ($B) Share Flows ($B) of AUM

1 iShares Diversified 340 873 39% 91 19%

2 Vanguard Low Cost 70 540 24% 76 27%

3 State Street SPY, GLD + Sector SPDRs 164 434 19% 20 54%

4 PowerShares Smart beta + Access 140 96 4% 0 17%*

5 Schwab Low Cost 21 48 2% 14 37%

6 WisdomTree Dividend Weighted 96 38 2% (14) 51%

7 First Trust Smart beta 103 37 2% (3) 24%

8 Guggenheim Access 76 28 1% (2) 43%

9 Van Eck Access 55 28 1% 2 56%

10 ProShares Access 150 26 1% 5 25%

*Ex-QQQ, 49% with QQQ included

Source: Bloomberg L.P. Data as of June 30, 2016.

21ETF industry flows are positive across all

categories though total flows were flat vs. 2014

Domestic calendar year net flows 2016 flows are

300 currently at $67B

(6/30/16)

250

Fixed Income

200

products are

leading 2016

Net flows ($B)

150

flows with $17B

100

50

0

2010 2011 2012 2013 2014 2015

Total industry flows

Source: Bloomberg L.P. Data as of Dec. 31, 2015. Net flow differences may be due to rounding.

22ETF industry trends

1

Global ETF asset growth continues

Total global ETF AUM = $3.2 trillion*

US constitutes 73% of globally managed AUM

Global landscape for ETFs continues to expand with new opportunities coming from various regions

including other parts of NA and Asia Pacific

2

“Smart beta” strategies are growing faster (on a 3YR & 10YR CAGR) than the overall ETF market

and represent 12% of the US ETF market

Growing use of smart beta strategies by both institutional and retail investors in the US

Non-US investor demand is at an early stage (remains in the “awareness” stage)

Rapidly growing adoption of factor investing within smart beta. Factor investing, multi-factor strategies

have led smart beta fund launches (84) 2015 through YTD 2016 (9)

3

Rapidly growing smart beta competition from large existing competitors and new entrants

including traditional active asset managers

Proliferation of new smart beta launches

Crowded market with existing players makes it challenging for new entrants to differentiate their

messaging

4

Investors’ quest for yield, low volatility and quality investment continues

Fixed income has led all categories in terms of flows over the last 12 months, attracting over $87 billion

in flows between both taxable and municipal based products

Rising apprehension related to traditional bond investing is prompting investors to diversify their fixed

income holdings and turn to alternative multi-asset (including dividends, preferreds, international bond,

real estate, equity income, MLPs etc.)

Investors continue to flock to managed volatility products and have been adopting other factors including

momentum and quality gaining popularity more recently

Source: PowerShares Global ETF Products & Research, as of June 30, 2016.

*Source: ETFGI as of June 30, 2016.

23ETF industry trends (cont’d)

Department of Labor (DOL) proposed fiduciary rule for retirement accounts

5 US retail advisors and RIA’s are likely to see increased pressure to steer client toward low cost passive

product with the advent of the new DOL ruling

ETFs may benefit from the DOL rule

Growing use of smart beta & factors by institutions and advisors

6 Increasing demand from some institutions, including sovereign wealth funds and pensions, to factor

investing strategies away from alternatives

Institutional demand for ETFs are growing at a faster rate than retail in the US driven in large part by

increasing demand in fixed income and factor ETFs

Active ETF’s potential to be a growth driver remains untapped

7 The first non-transparent active ETF launched this year was met with a lot of skepticism to date has very

little volume and minimal assets

Different transparency standards and other operational differences between active ETFs and mutual funds

are key inhibitors

Active ETFs represent only 1% of industry assets and 3% of 12 month flows

More providers filed for non-transparent active ETF exemption

Source: PowerShares Global ETF Products & Research, as of June 30, 2016

24Smart beta ETFs 25

Growth of index-based investing

1890s 1920s 1970s 1990s 2000s

First price First market cap First index First smart beta

First ETF (1993)4

weighted index2 weighted index2 mutual fund3 ETF (2003)5

For illustrative purposes only.

From 2010 to 2015

Smart beta ETFs captured over 22%

of US ETF equity inflows and now

represent 12% of total industry

assets.1

We anticipate that this trend will

continue in 2016.

1 Source: Bloomberg, L.P. as of June 30, 2016

2 Source: S&P Dow Jones Indices, djindexes.com

3 Vanguard, vanguard.com

4 State Street Global Advisors, spdrs.com. 5) Guggenheim , Guggenheiminvestments.com; PowerShares,

PowerShares.com. An investor cannot invest directly in an index.

26Common industry definitions

“The common thread among [smart beta ETFs] is that they seek to either

improve their return profile or alter their risk profile relative to more

traditional market benchmarks.” 1

– Ben Johnson, Director of Passive Funds Research, Morningstar

Common definitions for smart beta ETFs

Also known as:

Alternative Beta

Alternative Indexing

Based on Strategic Beta

Predetermined Rules, Not Market Can Track a Advanced Beta

Systematically Cap Weighted Variety of Factors

Rebalanced

1 Source: “The Strategic Factor of Smart Beta” Morningstar Magazine, April/May 2014

Beta is a measure of risk representing how a security is expected to respond to general market movements.

Smart beta: an alternative and selection index based methodology that may outperform a benchmark or

mitigate portfolio risk, or both in active or passive vehicles. Smart beta funds may underperform cap-

weighted benchmarks and increase portfolio risk.

27PowerShares definition

Employing features of

both worlds:

May outperform a

benchmark*

Replicates an index with

rules-based methodology

Provides broad market

Passive exposure

cap-weighted Smart beta Active

Ability to potentially

reduce risk through

diversification beyond a

single security**

Liquidity1

Lower costs2

Transparency3

Beta: is a measure of risk representing how a security is expected to respond to general market movements.

Smart beta: an alternative and selection index based methodology that may outperform a benchmark or mitigate portfolio risk, or

both in active or passive vehicles.

*Smart beta funds may underperform cap-weighted benchmarks and increase portfolio risk. There is no assurance that

an investment strategy will outperform or achieve its investment objectives.

** Diversification does not guarantee a profit or eliminate the risk of loss.

1 Liquidity: Shares are not individually redeemable and owners of the shares may acquire those shares from the Fund and tender

those shares for redemption to the Fund in Creation Unit aggregations only, typically consisting of 50,000, 75,000, 100,000 or

200,000 shares.

2 Low Cost: Since ordinary brokerage commissions apply for each buy and sell transaction, frequent activity may increase the cost

of ETFs.

3 Transparency: ETFs disclose their holdings daily.

28Like everything else, how we invest has evolved

Alpha Alpha Alpha

Smart

beta/factor

investing

Beta Beta

Time

For illustrative purposes only and should not be deemed as an asset allocation recommendation.

29Global financial crisis

The global financial Coming out of 2008, many of our

crises created: clients have placed a renewed

emphasis on:

Extreme market uncertainty Tactical asset allocation

(vs. buy & hold strategic

Record-high volatility asset allocation)

Sharp portfolio drawdowns Intraday liquidity1

Steep capital gain tax Daily transparency2

consequences

Cost3

Tax efficiency4

1 Liquidity: Shares are not individually redeemable and owners of the shares may acquire those shares from the

Fund and tender those shares for redemption to the Fund in Creation Unit aggregations only, typically

consisting of 50,000, 75,000, 100,000 or 200,000 shares.

2 Transparency: ETFs disclose their holdings daily.

3 Cost: Since ordinary brokerage commissions apply for each buy and sell transaction, frequent activity may

increase the cost of ETFs.

4 Tax Efficiency is a measure of performance for an investment or a fund that is calculated by dividing the after-

tax return by the pre-tax return. PowerShares does not offer tax advice. Please consult your own tax advisor

for information regarding your own tax situation.

30Core PowerShares competencies To be a global leader requires strength and presence in both the retail and institutional channels PowerShares maintains unique competitive advantages (US advisor market, smart beta, innovation, brand) Fast moving and fierce competition requires ETF leaders to be bold and nimble ETFs present a unique asset management opportunity to globally “passport” a product line Specialized and strong infrastructure (e.g., portfolio implementation, investment operations & technology, trading, product development, and legal) is a critical competitive edge in scaling an ETF business globally Organizational alignment, focused investment, governance, and accountability are necessary 31

The smart beta market has grown faster than the

overall ETF industry over the past 10 years

ETF growth rates ETF industry has

grown from

1400%

$426B in 2007 to

1200% 2.3T in 2016

1000% Smart beta AUM

has grown from

800%

an AUM of $21B in

600% 2007 to $273B in

2016

400%

200%

0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Industry Growth Smart Beta Growth

Source: PowerShares Product Strategy & Research, as of June 30, 2016.

32Demand for smart beta ETFs has continued to

increase and is projected to reach $602B in 2020

ETF AUM by investing style Smart beta

2016 2020 industry AUM is

1% 1% currently $272B

12% 15%

Smart beta ETFs

are expected to

18% 15% grow to 15% of

the ETF market

69% 69% by 2020

Investing style percentage Investing style percentage

Pure passive 69% Pure passive 69%

Passive access 18% Passive access 15%

Smart beta 12% Smart beta 15%

Active 1% Active 1%

Source: Bloomberg L.P. Data as of June 30, 2016. Invesco estimates based on 3-Year CAGRs.

33PowerShares YTD net flows into smart beta are

the most diverse (11% HHI) amongst our

largest smart beta competitors

Net Flows ($M) YTD Herfindahl- Herfindahl-

Market

AUM Market Hirschman Hirschman

Rank Provider Share

($B) Share Index* Index*

% June YTD 1 Yr

Change (AUM) (Flows)

1 iShares 60 22.6% 3,009 13,962 18,239 5.95% 16% 25%

2 PowerShares 42 15.7% 885 2,712 2,929 0.89% 6% 11%

3 WisdomTree 36 13.6% (2,378) (10,328) (13,229) -6.44% 13% 14%

4 Vanguard 36 13.6% 672 2,924 3,287 1.29% 52% 53%

5 State Street 29 11.1% 16 (1,657) (222) -0.87% 25% 17%

6 First Trust 24 9.1% (284) (3,107) (4,707) -1.93% 5% 23%

7 Guggenheim 15 5.8% 123 (882) (2,145) -0.52% 41% 30%

8 Schwab 8 3.2% 492 1,666 3,022 0.65% 28% 20%

Northern Trust

9 4 1.4% 67 797 949 0.27% 21% 46%

FlexShares

10 Goldman Sachs 2 0.6% 154 695 1,556 0.27% 21% 35%

Remainder 8 3.2% 402 1,225 1,132 0.44% N/A 46%

Total 264 100% 3,157 8,007 10,811

*Herfindahl-Hirschman Index is a measure of the firm’s AUM or Flow concentration by product. A lower value indicates the firm’s AUM or flows are

diversified across their product line. Calculation: where si is the market share of firm i in the market, and N is the number of firms.

Source: PowerShares Global ETF Products & Research, as of June 30, 2016

View includes FoF for all firms

34Smart beta pioneers since 2003

PowerShares industry leadership in first-to-market ETF innovation:

Total Funds

in PowerShares

Year Index Methodology Introduced PowerShares ETF Example (Ticker) Family¹

2003 Quantitative Constructed Dynamic Large Cap Value (PWV) 15

International Dividend International Dividend AchieversTM (PID) 1

2005

Fundamentals Weighted Equity FTSE RAFI US 1000 (PRF) 15

2006 Share Buybacks Buyback AchieversTM ( PKW ) 2

Emerging Sovereign Debt Emerging Markets Sovereign Debt (PCY ) 2

2007 Momentum DWA Momentum (PDP) 15

Options S&P 500® BuyWrite Portfolio (PBP) 1

High Quality Weighted S&P 500® Quality (SPHQ)² 2

2010 Fundamentals Weighted/Fixed-Income Fundamental High YieldTM Corporate Bond (PHB) 3

Yield Weighted REIT KBW Premium Yield Equity REIT Portfolio (KBWY) 1

Volatility-Weighted S&P 500® Low Volatility (SPLV) 10

2011

Beta-Weighted S&P 500® High Beta (SPHB) 3

Multi-Strategy Alternative Multi-Strategy Alternative Portfolio (LALT 1

2014

Laddered Corporate Bond LadderRite 0-5 Year Corporate Bond (LDRI) 1

1 Represents the number of funds in the PowerShares ETF Family that utilize the corresponding methodology

introduced.

2 On March 18, 2016, at the close of markets, changes to the Fund's name were made. For more information

about the changes, please see the Funds’ prospectus.

35Product Strategy & Research 36

We believe our product line is well positioned

to succeed

Product innovation is in our DNA

The strength of our product line offers competitive

advantages

Transform product innovation into “client innovation”

37Product innovation is in our DNA

Single focus on leading the smart beta ETF revolution since 2003,

with major product innovations

Pioneered the first factor- The first smart beta Invented the first smart beta

based equity ETF in 2003 commodity ETF in 2006 fixed income ETF in 2007

Nine of our top 10 ETFs are first-to-market/first-of-its-kind

Ticker Fund AUM ($M) First to market/First of its kind

SPLV Powershares S&P 500 Low Volatility Portfolio 7,645

BKLN PowerShares Senior Loan Portfolio 5,188

PGX PowerShares Preferred Portfolio 4,717

PRF PowerShares FTSE RAFI US 1000 Portfolio 4,314

PCY Powershares Emerging Markets Sovereign Debt 3,835

Portfolio

SPHD PowerShares S&P 500 High Dividend Low Volatility 2,677

Portfolio

DBC PowerShares DB Commodity Index Tracking Fund 2,404

PGF PowerShares Financial Preferred Portfolio 1,842

PRFZ PowerShares FTSE RAFI US 1500 Small-Mid Portfolio 1,480

PDP PowerShares DWA Momentum Portfolio 1,433

Source: PowerShares Global Products & Research, as of August 31, 2016.

38While the barriers to entry for ETFs are low, the barriers to gain scale are high due to first mover advantages There is a significant first mover advantage in ETFs - the first mover gets an automatic, and potentially insurmountable boost in assets The rationale for first mover advantage is due to liquidity, size and familiarity with the ticker Industry statistics had shown that in 71% of all product segments, the first mover had the most assets Subsequent entrants tend to compete with a first mover fund on price though not always successfully We spend a lot of time and effort developing first-of-its-kind ETFs. Among the 20 largest PowerShares ETFs, 17 were first-to-market ETFs, 13 of them are still the leaders in the space they cover Source: PowerShares Global Products & Research, as of August 31, 2016. 39

Strong product development track record

We raised $21 billion from new products launched over the last five years,

the 2nd highest in the industry.

Product development trend (2011-2016)

Total AUM raised from # new products

new product launches ($B) launched

iShares 107.8 174

PowerShares 21.2 41

Schwab 17.8 10

Vanguard 15.9 7

SSgA 13.5 73

First Trust 12.8 60

Guggemheim 6.0 28

Van Eck 4.9 35

ProShares 4.8 59

WisdomTree 2.9 56

Source: PowerShares Global Products & Research, as of August 19, 2016.

40Our product line offers competitive advantages

A diverse, all-weather line-up of 141 ETFs covering major asset classes and

strategies to help meet investors’ changing needs.

PowerShares product line by asset class

Int'l Equity

$6 B

Fixed Income

$22 B

US Equity

$73 B

Commodities

& Currencies

$6 B

A complete tool box to facilitate the delivery of value-added solutions

Minimizes product concentration risk

41We are well positioned to participate in fixed

income growth

We have $22B in fixed income ETFs and rank #4 in industry’s fixed income AUM

YTD, net flow into fixed income ETFs makes up 64% of our total and is the industry’s

3rd highest

Our 19 fixed income ETFs cut across markets, credit and duration spectrum. Seven of

our fixed income ETFs have AUM>$1B due to early mover advantage

Latest innovation: PowerShares Variable Rate Investment Grade Portfolio

Fixed Income

AUM ($B) YTD Net Flows ($B)

iShares 232.5 35.9

Vanguard 103.8 16.9

State Street 42.7 3.7

PowerShares 21.6 4.8

PIMCO 12.1 0.8

Guggenheim 8.4 1.5

Van Eck 8.2 2.2

Schwab 6.4 1.7

Northern Trust 2.6 0.1

First Trust 2.2 1.0

WisdomTree 0.8 (0.1)

Source: Bloomberg L.P. Data, as of August 31, 2016.

42Our product line is diverse

Our product line consists of tools to help investors:

Extract alpha and/or manage risk - smart beta ETFs

Gain precise market exposures - Access ETFs

PowerShares product line by strategy

Access

Smart beta Access ex-QQQ

Non-market cap weighted $21 B Market-cap weighted

Single factor building Exposure to:

blocks Sectors

Multi-factor Industries

Fundamental or equal Smart beta Themes

weighted $44 B

Top 3 PowerShares ETFs: QQQ Top 3 PowerShares ETFs:

S&P 500 Low Volatility $40 B QQQ

FTSE RAFI US 1000 Bank Loan Portfolio

S&P 500 High Dividend Preferred Portfolio

Low Volatility

Source: PowerShares Global Products & Research, as of August 31, 2016.

43Our product line has continued to gain scale

The number of our billion-dollar ETFs has increased from 8 to 19

over the last five years

Number of PowerShares ETFs with AUM > $1 Billion

19

8

2011 2016

Source: PowerShares Global Products & Research, as of August 31, 2016.

44Our smart beta line-up is well established

Scale: The 2nd largest provider with $44 Billion in smart beta AUM

Breadth: The broadest smart beta line-up with 85 ETFs. Top competitors’ smart beta

AUM are concentrated in dividend ETFs.

Track record: The most number of smart beta ETFs with track record > 5 years

Depth: The most number of smart beta ETFs with AUM > $500M

The 2nd Largest The Broadest The Most The Most

smart beta Provider smart beta Line-Up Number of SB ETFs Number of SB ETFs

with at least a 5-yr with AUM>$500M

Track Record

15% 19%

21% 35%

$44B 85 62 20

smart beta smart beta

in smart beta smart beta

ETFs with at ETFs with

AUM ETFs

least a 5-year AUM>$500M

track record

PowerShares as % of Industry

Source: PowerShares as of August 31, 2016. The smart beta category includes ETFs that have an alternative and

selection index based methodology that seeks to outperform a benchmark or reduce portfolio risk, or both. Industry

remainder represents all ETF products that meet this criteria, excluding PowerShares smart beta products. Smart

beta funds may underperform cap-weighted benchmarks and increase portfolio risk. Beta is a measure of risk

representing how a security is expected to respond to general market movements.

45Transform product innovation into “client

innovation”

Leverage our diverse, all-weather line-up to build product loyalty through

differentiated, value-added client engagement tools and services.

Portfolio Thought leadership &

Digital offering

construction research

Custom ETF solutions Online platform will Smart beta

to meet specific be a key channel

objectives/outcome driving demand for Factor investing

ETFs

Factor DNA analysis

ETFs and digital

advice may benefit

from the new DOL

rule

Exploit synergies

between

PowerShares and

Jemstep to offer

superior online

experience

46Institutional 47

US Institutional demand for ETFs is growing faster than retail Certain institutional channels are increasingly adding ETFs to improve risk budgeting and liquidity profiles of their portfolios and trading strategies PowerShares and Invesco have strong global capital markets relationships with the sell-side which we can further leverage to reach institutional clients PowerShares is currently under-represented in its coverage of institutional clients versus major competitors and the overall industry average PowerShares strength in smart beta ETFs is a unique differentiator to institutions who are increasingly becoming accepting of the benefits of smart beta solutions (e.g., low volatility, high momentum, etc.) 48

Outlook for institutional use

A majority of institutional decision makers plan to increase use of

smart beta ETFs

Expected change in the next 3 years

Somewhat/Significantly Decrease Neither Increase or Decrease

Somewhat/Significantly Increase

Smart Beta ETFs 3% 38% 59%

Market Cap Index 13% 39% 48%

Active ETFs 8% 53% 40%

Leveraged/Inverse ETFs 12% 70% 18%

Evolution of Smart Beta ETFs, Market Strategies International, as of January 2016

49Institutions plan to increase use of smart beta ETFs

Which types of smart beta ETFs will you likely begin using in the next three years?

Current Usage Expected Usage (Next 3 years)

64% 63%

62%

60%

55%

51%

44% 43%

40% 39% 40% 39%

35%

25%

20% 20%

1% 1%

High Dividend Low Volatility Fundamental Weight Equal Weight High Beta Enhanced Fixed Currency-Hedged Momentum Other

Income

“Forty-five percent of all institutional decision-makers expect to allocate more assets to smart

beta funds moving forward -- proof of the growing acceptance and understanding of the

category. Even among those who haven’t yet used a smart beta ETF, 3 in 10 expect to do so.”

* Evolution of Smart Beta ETFs, Market Strategies International, as of January 2016

Evolution of Smart Beta ETFs, Market Strategies International, as of January 2016

50In the institutional channels, ETFs are often used

when there is a high priority for liquidity,

transparency or convenience

Strategy Objective Pensions, Consultants Insurers OCIO, asset Hedge

Endow. & mgrs & MFs Funds

found

Transition Management Maintain exposure while searching for X X X

new managers

Rebalancing Reduce implementation time to change X X X X

exposures in asset classes

Cash Equitization Maintain liquidity while remaining fully X X X X

invested

Portfolio Completion Aims for portfolio diversification and X X X X X

seeks to minimize benchmark risk

while maintaining performance

objectives.

Securities Lending Potential for additional return X X X

Tactical Adjustments to Over - or underweight certain styles, X X X X

Asset Allocation regions or countries on the basis of

short term view

Long / Short ETF Obtain long or short exposure X

Applications

Taxable Plans Benefit from the tax efficiency of ETFs X X

Fixed Income Duration Fine-tune the target duration and X X X X X

and Credit Adjustments credit quality of fixed income portfolios

Small Institutional Implement the desired asset allocation X X X

Plans regardless of plan size

Source: Invesco

51PowerShares is skewed to retail ownership given

its historical focus on Advisors and smart beta

strategies

We maintain a strong retail

100%

distribution focus

90%

Institutions have not yet fully

80% 42%

embraced smart beta. Only 24%

70% 57%

of firms surveyed in our Cogent Study

used smart beta with an average 60%

allocation of 7% 50%

40%

30% 58%

20% 43%

10%

0%

PowerShares Industry

Institutional Assets Retail

Source: FactSet 13F data as of June 30, 2016.

Source: Cogent Research/PowerShares Institutional Survey, October 2013.

52US Institutional use of smart beta ETF strategies

is expected to increase

53% of institutional clients Reasons for using smart beta ETFs Reasons for not using smart beta ETFs

surveyed in our Cogent

(Top 5) (Top 5)

Study expected to increase

Outperforms

smart beta usage (higher market 31%

Lack of

34%

familiarity

than any other segment) indexes

PowerShares smart beta Lack of

Diversification 18% history/ 12%

has the longest track track record

record in smart beta

space, with competitive

Reduce

performance record volatility/beta

18% No need 11%

Not part

Alternative

of our

weighting 18% 10%

investment

of assets

strategy

Better asset Prefer active

13% 9%

risk return management

Source: Cogent Research/PowerShares Institutional Survey, October 2013

53Capital Markets 54

ETF Capital Markets are a critical component of

the ETF ecosystem

It is imperative to be well coordinated and aligned with both internal and

external functions in order to leverage the opportunity within ETF capital

markets

Sales Marketing

Capital

Markets

Product Portfolio

Development Management

Strong ETF Capital Markets coordination helps ensure liquid markets and a

better client experience

55Department mandate Our core functions Liquidity & Execution Services: The liquidity and execution services team is in place to help financial advisors and institutional clients navigate the ETF trading process. The team helps clients assess the potential liquidity of PowerShares ETFs, developing a client- specific trading strategy and evaluating the potential impact of a trade Market Maker & Authorized Participant Relationship Management: As ETFs trade in the secondary market and cannot be purchased directly through the ETF issuer, efficient trading is dependent on the ETF market maker community. The PowerShares Global Capital Markets team works with various market making firms, A.Ps and other sell side firms to ensure these parties may effectively make markets in PowerShares products. In addition, the team continuously monitors secondary market activity, assessing and tracking market maker performance, evaluating spreads and monitoring trading activity Research & Content: The PowerShares Global Capital Markets team provides actionable market commentary to our clients. This involves assimilating and distilling high quality buy side and sell side research into ETF investment strategies and providing market perspectives Sales Support: Maintain a strong pulse on sales challenges and opportunities as well as support various sales teams across all channels by providing subject matter expertise 56

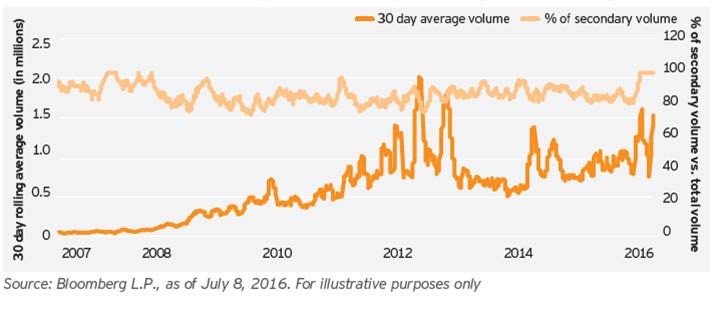

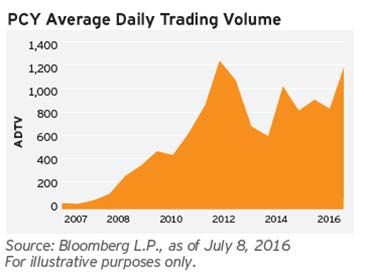

How are we ensuring a seamless client experience? Cost of owning an ETF: Operating Expense Ratio (OER), Trade Commission, Transaction Costs – Bid/Ask spreads Example using PowerShares Emerging Markets Sovereign Debt ETF 57

Bid Ask Spreads make up a key component of the

ETF investment wrapper

ABC ETF

OER1 Commission Bid/Ask Spread

Total Cost

XYZ ETF

OER1 Commission Bid/Ask Spread

Total Cost

1 Operating Expense Ratio

For illustrative purposes only

58We believe our leadership in smart beta/factor

investing positions PowerShares for strong

future growth

PowerShares is a pioneer of smart beta ETFs with a launch of its

multi-factor range of Intellidex ETFs in 2003 – today’s smart beta

Our leadership

range of 93 ETFs is over $42B in AUM in smart

beta/factor

Over the past 13 years PowerShares has created the most

comprehensive range of smart beta and Factor ETFs in the investing

industry – spanning equities, fixed income and alternatives keeps us

Over 70% of our smart beta and factor ETFs have greater than a

competitive

5 year historical track record against

existing

PowerShares has successfully partnered with a number of

Invesco’s active investment teams to create leading ETFs, e.g., players/new

senior bank loans and real estate entrants and

PowerShares is well positioned to become a leading component

positions us for

provider for emerging packaged solutions, e.g. Rhode Island 529 future growth

plan, digital advice, etc. and success.

PowerShares is one of a handful of ETF players with global

capabilities highlighted by local ETF platforms in the U.S., Canada

and EMEA

PowerShares is investing in strong and scalable infrastructure in

preparation for the expected high growth of smart beta and Factor

ETFs in the future

Source: Invesco as of June 30, 2016

59Questions 60 II-PS-PPT-1I 09/16

You can also read