Quarterly Global Outlook - Q2 2018 Balancing Between Hopes & Fears - UOB Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Global Outlook

Q2 2018

Balancing Between Hopes & Fears

SINGAPORE FOCUS FX STRATEGY

Singapore MAS Policy Preview: It’s Time Risks And Opportunities In 2Q18

To Catch Up With Policy Normalization As USD Stays Soft

MALAYSIA FOCUS RATES STRATEGY

Rise Of China-Malaysia Relations Staying The Course On Monetary Policy While

Recognizing That Equilibrium Has Shifted In Bond Markets

INDONESIA FOCUS COMMODITIES STRATEGY

Achieving Fiscal Sustainability Key To Clear Build-Up In Net Long Positioning And

Fostering Higher Economic Growth Inventories Cap Further Meaningful Gains

CHINA FOCUS

NPC Targets Set For 2018

CONTENT

04

EXECUTIVE SUMMARY CHINA � 46

Balancing Between Hopes & Fears

HONG KONG � 47

11

FX, INTEREST RATE & COMMODITIES FORECASTS INDIA � 48

INDONESIA � 49

12 JAPAN � 50

SINGAPORE FOCUS I

Singapore MAS Policy Preview: It’s Time To Catch Up MALAYSIA � 51

With Policy Normalization

MYANMAR � 52

18 SINGAPORE � 53

SINGAPORE FOCUS II

Singapore Budget 2018: Strategies To Cope SOUTH KOREA � 54

With An Ageing Society

TAIWAN � 55

22 THAILAND � 56

MALAYSIA FOCUS

Rise Of China-Malaysia Relations VIETNAM � 57

25

INDONESIA FOCUS AUSTRALIA � 58

Achieving Fiscal Sustainability Key To

Fostering Higher Economic Growth EUROZONE � 59

NEW ZEALAND � 60

30

CHINA FOCUS UNITED KINGDOM � 61

NPC Targets Set For 2018

UNITED STATES OF AMERICA � 62

32

VIETNAM'S CONSUMER INSIGHTS FX TECHNICALS � 63

The Bright Spot In The Mekong Region

COMMODITIES TECHNICALS � 68

34

FX STRATEGY Information as of 23 March 2018

Risks And Opportunities In 2Q18 As USD Stays Soft

GlobalEcoMktResearch@UOBgroup.com

www.uob.com.sg/research

38 Bloomberg: UOBR

RATES STRATEGY

Staying The Course On Monetary Policy While

Recognizing That Equilibrium Has Shifted In Bond Markets

42

COMMODITIES STRATEGY

Clear Build-Up In Net Long Positioning And

Inventories Cap Further Meaningful Gains Scan the QR Code for a list of all our reports

EXECUTIVE SUMMARY

Balancing Between Hopes & Fears

At the start of the year, the global economy looks and sounds familiar, that’s because intellectual-property violations. Another

was still humming along and IMF upgraded it is. Right after Trump’s election victory venue for the US to force through trade

global growth as well as the outlook in late 2016, this was exactly one of the protectionism is possibly through labelling

for several major economies (many key concerns everyone had since Trump China as a “currency manipulator” in the

other international agencies did similar campaigned on a populist platform of semi-annual US Treasury FX report as an

upgrades as well). But financial markets anti-establishment, anti-free trade, anti- indirect route of forcing trade restrictions.

followed a different script. After a positive immigration, imposition of trade tariffs and The next report will be due in April 2018.

January, things went south in February tax cuts (which is seen as protectionist and

as the sudden spike in concerns about detrimental to global trade). But now, what we’re seeing from President

the possibility of a faster Fed rate hike Trump is either a fulfilling of his presidential

trajectory sent stock markets tumbling, After concentrating on domestic issues campaign pledges, creating a distraction

with a “timely” warning that volatility is not in his first year in office, Trump first from his domestic political issues, taking a

dead. announced tariffs on solar panels & risky bet to make gains in the November

washing machines in early 2018, and US mid-term elections or a combination of

That said, even though the first 3 months on 1 Mar, he announced his intention to all three. And it would be naïve to think that

of 2018 did not start out as planned and impose 25% tariffs on steel imports and Trump can keep throwing more and bigger

it probably did not hurt as much as we 10% tariffs on aluminium imports. And now “stones” at China and expect China not to

initially feared, the risk is now emanating he seems ready to take aim at China as respond. Surely Trump will get a response,

from the geopolitical space. The biggest Trump signed an executive memo on 22 and likely not a pleasant one. Our base

immediate risk is likely the escalating Mar, instructing US Trade Representative case remains that we do not expect an all-

trade tensions between US and the rest Robert Lighthizer to levy at least US$50bn out trade dispute but there is clearly a non-

of the world, in particular China. If this of tariffs against Chinese goods over zero potential risk.

US Trade In Goods Balance With Key Partners: Vulnerability To US Based On Export Exposure:

Bigger Deficit, Bigger Target For Trump China, Japan, Vietnam & India Clearly Stand Out

Source: Macrobond, UOB Global Economics & Markets Research Source: CEIC, Bloomberg, UOB Global Economics & Markets Research

200

Hong Kong

180

Singapore

Export of goods & services (% GDP)

160

140

120

100

Vietnam

80 Thailand

Taiwan Malaysia

60

EU South Korea

40

NZ Philippines India

20 Australia China

Myanmar Indonesia

Japan

0

0 5 10 15 20 25

Export to US (% total export)

Quarterly Global Outlook 2Q2018

04 UOB Global Economics & Markets Research EXECUTIVE SUMMARY

Beyond the US-led trade tensions, there hosted in Russia, that could bring some inventories in key commodities. Across

are many other geo-political developments challenges of a political nature. 1Q, copper witnessed a strong build-

that markets need to be watchful in the up in inventories across all three major

coming second quarter: And to end our executive summary with exchanges, the LME, COMEX and ShFE.

what we wish for in the coming months, to

US Special Counsel Robert Mueller’s quote from a cliché answer from another As for WTI crude oil, the on-going surge in

investigation into Russian meddling global “competition” of a different but full US shale oil production has now pushed

with the 2016 US presidential elections of Trump-related influence/interest, we US crude oil production past the 10 mio

(a stormy time for Trump?) sincerely hope for – world peace. bpd level. As such, US crude oil exports

have surged, threatening the fragility of

Japan domestic political stability being _________________________________ the OPEC led global production cap. In

rocked by a controversial government addition, net long positioning in crude oil

land sale deal implicating Japan PM FX Strategy: as implied from NYMEX futures is now at a

Shinzo Abe and Fin Min Taro Aso Risks And Opportunities In 2Q18 decade high. Overall, after the strong price

As USD Stays Soft rally last year, we now see LME copper

UK & EU Brexit negotiations seeing After more than a year of non-stop sell-off, settling into range trade at USD 6,500 to

positive developments ahead of the EU the outlook for the USD remains difficult 7,000 / MT. Similarly Brent Crude Oil will

leader’s summit (22-23 Mar) and weak. On-going flattening of the yield find it difficult to trade above USD 70 / bbl,

curve and the converging of normalization rather some consolidation within USD 60

A US-North Korea Leaders’ summit of global monetary policy are two key to 70 / bbl is in order.

potentially in May 2018 (It is unclear drivers that continue to weigh on the

whether this will be a positive or a USD. For 2Q18, we see three risks which In the precious metals space, there was a

negative for the markets?) present interesting opportunities in the FX clear falling out of favor for palladium as

space. extended net long positioning and ETF

Increasingly rocky relationship between holdings were pared off. Silver was also

Russia and G7 First, investors may need to hedge against weighed down as net long positioning was

more JPY strength to 100 against the completely erased across 1Q. Finally, as

Italian election stalemate and new USD, as concerns about reduced bond for gold, we maintain our negative view.

elections are likely, but the timing is not purchases by the BoJ persist. Second, More likely than not, gold is expected

yet settled given the persistent widening of USD vs to pull back to USD 1,200 / oz as short

HKD interest rate spread, it is increasingly term money market rates continue to rise

Malaysia likely to hold its 14th General likely that the HKD weak side convertibility further, adding to funding costs for a long

Elections in 2Q and the ruling coalition of 7.85 will be tested, but we continue to gold position.

is largely expected to win the elections expect the USD/HKD peg to hold. Third, we _________________________________

like to take this opportunity to accumulate

G7 leaders’ summit in June may be a the AUD now that it has pulled back to the Rates Strategy:

messy affair if trade tensions escalate lower end of its broader trading range. Our Aggressive End 2018

further Money Market Rates Forecast

Specific to USD/Asia, we maintain our Are Within Sight; And Expectations

Geo-politics is creating a lot of uncertainty view of two halves, i.e. once Asian For Longer Dated Bond Yields

in the outlook and the warnings have currency strength dissipates, USD/Asia Are Reset Higher

been sounded even though the economic may well stabilize and inch higher in H2. We maintain our expectations for the

fundamentals are healthy. Global monetary Ironically, any escalation of trade tensions FED to hike a total of 3 times in 2018,

policy is still on the normalising path led by may well accelerate this bottoming of though the risk of a 4th hike has increased

US Federal Reserve but politics & trade USD/Asia, as many Asian economies, considerably. After the jump in 3M US

tensions could spoil the party. China, in including China have large export engines Libor from 1.7% to 2.2% across 1Q18, our

comparison, is on the other end of the and as such, Asian currencies may well money market rate forecasts are no longer

spectrum, providing the political stability be vulnerable to any negative impact on as aggressive compared to when they

and continuity as Xi Jinping is unanimously exports. Consequently, USD/SGD is seen were made at the end of 4Q last year. As

elected as the President during the 13th stabilizing in 2Q at around 1.29, before such, we maintain our end 2018 US Libor,

National People’s Congress (NPC) drifting back up to 1.32 by End 2018. SG Sibor and SOR at 2.40%, 1.85% and

session. _________________________________ 1.65% respectively.

On balance, we believe we have more Commodities Strategy: In addition to the anticipated rise in short

to be hopeful for than to be fearful, but Build-Up In Net Long Positioning term money market rates, we also highlight

admittedly the number/degree of “fears” is And Inventories the increasing imbalances forming in

increasing. For sure, the 2018 World Cup Cap Further Meaningful Gains offshore US funding markets. These can

tournament will be a welcome distraction As a result of the Goldilocks euphoria, be witnessed from the rise in 3M CP/OIS

at the end of the 2nd quarter (14 June since the start of the year, there has been and 3M L/OIS spreads across 1Q.

to 15 July 2018) but with the Cup being a clear build-up in net long positioning and

Quarterly Global Outlook 2Q2018

EXECUTIVE SUMMARY UOB Global Economics & Markets Research 05

As for longer term bond yields, we have liveable city; caring and cohesive society; Malaysia Focus:

raised our projections. Our end 2018 and fiscally sustainable and secure future. Rise Of China-Malaysia Relations

forecast for 10Y US Treasury yield of This is a continuation Budget 2017 where China and Malaysia celebrated 40 years

2.90% has been reached, and we raise it we then observed the inclusion of the of diplomatic relations in 2014. There

to 3.20%. Similarly, we also raise our end sections on the “environment” and “fiscal has been significant strengthening of

2018 forecast for 10Y SGS from 2.45% to prudence” for the first time. China-Malaysia bilateral relations through

2.75%. trade, investments and tourism. The

Finance Minister Heng Swee Keat levels accelerated particularly in 2016

Hereafter is a brief synopsis of key Focus discussed at length with regards to rising and 2017. We anticipate a larger flow of

pieces as well as key FX and Rates views. expenditure, particularly from healthcare FDI and investments from China in the

and infrastructure, due to the rapidly ageing coming years particularly with the Belt and

_________________________________ population. This is a long term challenge Road initiative. Although there is rising

for Singapore since total fertility rate competition from Indonesia and the CLMV

Singapore Focus I: remains stubbornly low, and immigration region, Malaysia looks favourable from

Singapore MAS Policy Preview: policies remain tight. As more of the perspective of long historical friendship

It’s Time To Catch Up With population reaches retirement age and between the two countries, high level of

Policy Normalization drops out of the workforce, government’s political engagement, strong government

The Monetary Authority of Singapore revenue from direct methods of taxation cooperation, strategic geographical

(MAS) is expected to release monetary will be growing at a slower pace. To that, location, good infrastructure, and available

policy decision on the 2nd week of April he prepared the nation for a Goods & natural resources.

2018 (9th to 13th April) and we expect the Services Tax hike from 7% currently to 9% _________________________________

central bank to start policy normalization sometime between 2021 and 2025.

by allowing the SGD NEER on a mildly Indonesia Focus:

appreciating path (est: 0.5% pa) while Government’s overall budget surplus of Achieving Fiscal Sustainability

keeping the midpoint and bandwidth of the S$9.61 billion (2.1% of GDP) for FY2017 Key To Fostering Higher

policy band unchanged. was larger than initially (S$1.91 billion) Economic Growth

expected. For FY2018, the government Indonesia’s fiscal sector has shown

Our policy normalization expectation estimates a primary budget deficit of remarkable improvement over the past

is based on three key factors. Firstly, S$7.34 billion. This is thus an expansionary decade or so, leading to an investment

global and domestic growth-inflation- budget that will provide some boost to grade ratings on the country by all three

labour conditions have improved quite economic growth for FY2018. Overall major international rating agencies (Fitch,

significantly since the lows of 2015. budget balance is expected to come in at Moody’s, and finally Standard & Poor’s)

Central banks around the world today are a deficit of S$0.60 billion. as of 2017. In fact, in late 2017, Fitch

biased towards tightening, rather than _________________________________ upgraded Indonesia’s rating to BBB (Stable

loosening monetary policy stance. outlook, up from BBB- previously) and just

China Focus: months after S&P finally gave Indonesia

Secondly, the forex market seems to be China NPC Sets Targets For 2018 to long-awaited investment grade rating.

pricing in a more hawkish MAS stance The annual NPC session sets growth This puts Indonesia to be on par with

as the SGD NEER has appreciated 1.2% target for 2018 at 6.5% as expected, as the Philippines and Portugal in terms of

since the start of 2017, while our UOB this is sufficient to keep labour market its investment grade ratings. However,

SGD NEER model also shows that the in balance but fiscal stance is tightened despite the positive tones accompanying

SGD NEER had been trading consistently somewhat with the change in deficit the upgrade, most rating agencies do

above the midpoint 88% of the time in the target. Monetary policy bias remains as acknowledge that government revenue

same period. “prudent and neutral”, though targets for is still very low across peers of similar

money supply and credit are absent this ratings as of Indonesia. Looking deeper

Thirdly, the MAS had perhaps signaled a year, which means that the focus has into the revenue-expenditure dynamics

normalization inclination by removing a shifted away from quantitative increases. on the Indonesian fiscal space, we found

forward guidance word “extended” from It should be noted that an additional that reforms would be needed to ensure

its oft-used phrase “current neutral SGD measure of jobless rate target has been higher tax compliance and tax buoyancy

NEER policy is deemed appropriate for added, which is an improvement over in Indonesia. The shift of focus in fiscal

an extended period of time” in their last the existing “registered jobless rate” as expenditure into more infrastructure and

October 2017 policy statement. the broader measure takes into account social-development is duly acknowledged

_________________________________ of non-resident workers, such as migrant and applauded. However, given risks

workers from the countryside. With a of relying on external financing, the

Singapore Focus II: backdrop of steady growth environment, institutional reforms or some drastic

Singapore Budget 2018: Strategies we expect the government to accelerate measures to increase tax revenue remain

To Cope With An Ageing Society its economic reform and restructuring key to not only ensuring a sustainable

Singapore’s Budget 2018 had 4 key agenda and to look for ways to prevent fiscal, but also to foster higher GDP

areas of focus: developing a vibrant and systemic and financial risks. growth momentum and unleash further

innovative economy; smart, green and _________________________________ the Indonesian economic potential.

Quarterly Global Outlook 2Q2018

06 UOB Global Economics & Markets Research EXECUTIVE SUMMARY

Furthermore, it is by first anchoring a bund yields. From 1.25 in 2Q18, we see NZD/USD: After the Labor Party took over

sustainable fiscal posture, only then the EUR/USD climbing gradually to 1.27 in the government last October, there was

Indonesian fiscal policy can desirably 3Q18 and 1.29 in 4Q18 and 1Q19. Any an initial heavy sell-off in the NZD/USD all

adopt counter-cyclical measures to foster strength above 1.30 is unlikely for now, the way down to the bottom of the 2-year

higher economic growth in the foreseeable given that the US Federal Reserve is trading range between 0.68 and 0.75.

future. also in the process of monetary policy Investors had sold the NZD aggressively

_________________________________ normalization. on concerns of protectionist policies from

the incoming Labor government. After

Vietnam's Consumer Insights: GBP/USD: The recovery in the GBP/USD that initial knee jerk sell-off, the NZD/USD

The Bright Spot can be attributed in a large part to the on- stabilized and has reverted back to the

In The Mekong Region going support from the Bank of England current 0.73 level as immigration arrivals

Vietnam is currently experiencing one of (BoE), which hiked by 25 bps last Nov and for New Zealand picked up again. The

its fastest economic expansions in years, has signaled once again that it is likely to uncertainty at the RBNZ has also come

with gross domestic product (GDP) per hike a second time by May. However, at to an end with the appointment of Adrian

capita at current prices (Purchasing power its current level of just around 1.40, we Orr as the new governor at the end of

parity, or PPP) growth averaging 6.7% believe that the upcoming BoE rate hike Mar 18. In the meantime, NZD/USD can

over the last 3 years. Robust economic in May is largely priced in. Furthermore, be expected to grind higher towards the

growth and low unemployment rates have the BoE’s rate hikes are mostly built on top end of the above mentioned range.

propelled household income and spending the premise of rising inflation in the UK. We forecast NZD/USD at 0.74 in 2Q18,

in the country, positioning Vietnam to And the latest monthly print showed that 0.7450 in 3Q18, 0.75 in 4Q18 and 1Q19.

be one of the most promising consumer inflation in the UK has drifted further back

markets in Asia. This report looks at the down to 2.7% YoY in Feb, from its peak of ASIAN FX

emergence of the Vietnamese consumer 3.1% YoY last Nov. Going forward, amidst USD/CNY: Going forward, further CNY

and the sectors likely to benefit from the further intense Brexit discussions, growth strength will likely be capped by rising

rise of consumerism in one of the fastest outlook of the UK economy remains trade tensions with the United States.

growing economies in Asia. uncertain as the economy continues to The Trump administration is taking an

nurse a growing current account deficit. increasingly tough stance against trade

Overall, we maintain our view that GBP/ with nations that run large trade surpluses

GLOBAL FX USD will not be able to sustain gains against the United States. Given that China

USD/JPY: Going forward, we believe that above 1.40 and will drift back down from runs the largest trade surplus against the

the risk of further JPY strength is still there. here on. We forecast GBP/USD at 1.40 United States, i.e. USD 375 bn across

As highlighted in the executive summary, in 2Q18, 1.38 in 3Q18, 1.36 in 4Q18 and 2017, there are increasing concerns that

there is increasing political risk in Japan. 1Q19. the Trump administration may target

Furthermore, while BoJ Govenor Haruhiko Chinese imports next. As such, the CNY

Kuroda has been reappointed, he has yet AUD/USD: Despite RBA making clear on may be vulnerable to weakness should

to dispel increasing market concerns that multiple occasions its desire to maintain Chinese exports get negatively impacted.

the BoJ will eventually need to normalize its steady monetary policy, we continue to This also comes at a time when the US

monetary policy sooner than later. This maintain a positive outlook for the AUD/ Federal Reserve is poised to continue

was despite the fact that Japan’s inflation USD. This is mainly driven by support from its steady monetary policy normalization.

remains far from the 2% target. As such, commodities. However, across 1Q18, we Overall, we see USD/CNY inching higher

we see USD/JPY falling further to 100 in witnessed an increase in inventory and from hereon, to 6.35 in 2Q18, 6.40 in

2Q18, followed by a moderate recovery to positioning levels in various industrial 3Q18, 6.45 in 4Q18 and 6.50 in 1Q19.

103 in 3Q18, 107 in 4Q18 and 110 in 1Q19 metals like copper, limiting further strong

as the US Federal Reserve continues its upside. Similarly, amidst concerns of USD/SGD: Ahead of the widely anticipated

gradual rate hikes in the quarters ahead. strong increases in US production levels, policy normalization by the MAS in mid-

crude oil price seemed to have been April, the SGD NEER has been trading

EUR/USD: As a result of the ECB’s deft capped ahead of USD 70 / bbl. As such, predominantly at a premium above its

balancing act, EUR/USD was sandwiched AUD/USD has pulled back from its high of estimated mid-point of the current neutral

for now in-between the near term trading 0.81 in Jan18 to the current level of 0.78. range. Similarly, exacerbated by the weak

range of 1.22 to 1.25. Downside below Going forward, we believe that after the overall tone in the USD, the SGD has

1.22 is firmly supported by strong and recent pullback, further weakness may be been trading on a strong note as well.

improving macroeconomic fundamentals limited. Despite recent consolidation, key However, we believe that it may be difficult

in Eurozone. On the other hand, EUR/USD industrial metals and energy commodities for the SGD to strengthen further against

was prevented from staging a premature remain supported due to on-going strong the USD going forward. This is due to the

rally above 1.25. Overall, as we get nearer synchronized growth recovery. As such, increasing trade tensions between the

to the eventual stop in asset purchase we see mild AUD/USD strength ahead to United States and China, as trade and

towards the end of the year, we believe 0.79 in 2Q18, 0.81 in 3Q18 and 0.83 in exports from Asia are at risk of getting

that EUR/USD will appreciate slowly from 4Q18 and 1Q19. negatively impacted. This also comes

here on, in line with the gradual climb at a time when the US Federal Reserve

higher in various Eurozone and German is poised to continue its monetary policy

Quarterly Global Outlook 2Q2018

EXECUTIVE SUMMARY UOB Global Economics & Markets Research 07

normalization, with gradual rate hikes and October, followed by the BOK’s rate hike in 13,850 in 3Q18, 13,900 in 4Q18 and

on-going balance sheet reduction. In other November. Thereafter across 1Q18, USD/ 13,950 in 1Q19.

words, there may be limited downside KRW largely range traded within 1,060

for USD/SGD below 1.30. Overall, we and 1,100. The latest news of warming of USD/THB: From 36.0 in Jan 17, the

forecast USD/SGD at 1.29 in 2Q18, 1.30 ties with North Korea pushed USD/KRW THB has strengthened significantly, by

in 3Q18, 1.32 in 4Q18, 1.33 in 1Q19. back down to the lower end of this trading about 13% to the current level of 31.20

range. Going forward, while we welcome against the USD in Mar 18. Along the

USD/HKD: The interest rate differential the improving geopolitics, we believe that way, THB strength was supported by

between 3M US Libor and 3M HK Hibor the KRW may be increasingly vulnerable the abovementioned strong economic

jumped from 0.40% last December to to trade tensions with the U.S. instead rebound and export recovery in Thailand

1.05%, leading to further upside pressure as the latter is taking an increasingly across 2017. Despite current THB

on USD/HKD. At the pace which the rate tough stance on trade against countries strength, the outlook for the twin pillars of

spread widens, it is increasingly likely that which run a large trade surplus against Thailand economy, i.e. exports and tourism

the HKD will soon test sometime in 2Q, it. In addition, expectations of further rate arrivals remains strong. As such, fueled by

the weak side convertibility limit of 7.85 hikes by the BOK later in the year may on-going strong current account surplus,

against the USD but we do not see any have already been baked into the current the THB may still stay biased on the strong

risk to the peg at this stage. However, KRW strength. As such, we see risk of side in the near term. Thereafter, as the

in order to limit further weakening of USD/KRW bottoming around the current year progressed in 2H18, the USD would

the HKD towards 7.85, the HKMA now 1,060 level and trading moderately higher be able to register mild gains against the

has a delicate act of guiding domestic thereafter. Our forecasts for USD/KRW THB, as financial markets would have

rates gradually higher without disrupting going forward are 1,070 in 2Q18, 1,080 in digested the anticipated 25 bps rate hike

domestic activity and capital markets. This 3Q18, 1,090 in 4Q18 and 1,100 in 1Q19. from BoT and the US Federal Reserve

test of the 7.85 level will likely happen would have progressed with a total of

over the coming two quarters, before local USD/MYR: Previously, expectations of an 3 rate hikes across 2018. Overall, we

rates play catch up with rising US rates upcoming rate hike by BNM and strong forecast USD/THB at 31.00 in 2Q18,

and USD/HKD drift back down towards rise in crude oil prices have fueled the before a mild recovery to 31.30 in 3Q18,

7.80. Thus we forecast USD/HKD at 7.85 outright strengthening of the MYR. Now 31.50 in 4Q18 and 31.80 in 1Q19.

across 2Q18 and 3Q18, and 7.83 in 4Q18 that BNM has hiked in January, going

and 7.80 in 1Q19. forward, they are likely to remain on hold. USD/VND: Going forward, we see the US

Furthermore, given increasing supply risk Federal Reserve continuing its gradual

USD/TWD: Across 1Q, various risks from the US, it may be difficult for Brent rate hike process, with another two more

have built up against the TWD. First, the crude oil to strengthen further above rate hikes in 2H18. Overall, we see on-

growth outlook is expected to moderate USD 70 / bbl. Rather, Brent crude oil going mild VND weakness in line with

to a less stellar 2.3% this year, compared is now expected to settle within a broad rising US rates. The domestic positive

to 2.9% last year. Second, any escalation trading range of USD 60 / bbl to USD 70 drivers will limit excessive VND weakness.

of trade tensions between US and China / bbl for the coming 4 quarters. As such, Our forecasts for USD/VND are 22,800 in

will likely have a negative impact as well supported by strong export growth and 2Q18, 22,900 in 3Q18, 23,000 in 4Q18

on Taiwanese exports and consequently various positive domestic demand drivers, and 23,100 in 1Q19.

the TWD. Third, given the on-going rise the pace of MYR strengthening will likely

in US Treasuries yield, the yield spread ease going forward. Overall, we see USD/ USD/INR: With India’s monthly trade

between 10 year US Treasuries and MYR drifting lower to 3.88 in 2Q18, 3.85 in deficit widening on a quicker path since

10 year Taiwan government yield has 3Q18 and 3.80 in 4Q18 and 1Q19. March 2016, the central government

widened further from 1.50% at the start of fiscal budget deficit growing, and the RBI

the year to 1.85% now. On a related note, USD/IDR: Despite the improving domestic probably keeping the current monetary

as highlighted above, Taiwan’s real policy macroeconomics, the IDR had recently stance throughout this year, we think that

rate has dipped into negative. As such, weakened against the USD. As a result, there could not be much room for the INR

we maintain our forecast that USD/TWD USD/IDR climbed from its low of 13,300 in to continue its strong performance against

will likely bottom out nearer to the middle Jan to current level of 13,750. This is most the greenback. We forecast the USD/INR

of the year and inch back up in 2H18. likely due to pressure from rising US rates, at 65.00 in 2Q18, 65.30 in 3Q18, 65.60 in

Overall, we forecast USD/TWD at 29.40 in which typically has a negative impact on 4Q18, and 66.00 in 1Q19.

2Q18, 29.60 in 3Q18, 29.80 in 4Q18 and Asian and Emerging Market currencies

30.00 in 1Q19. with underlying current account and fiscal _________________________________

deficits. Given that our base case calls for

USD/KRW: In the final months of 2017, two more FED rate hikes this year (after GLOBAL INTEREST RATES

the KRW strengthened significantly, the recent 25 bps in Mar), 3M US Libor is FOMC: Our moderately hawkish outlook

forcing USD/KRW to retreat from 1,150 in expected to rise further towards our year- for the Fed rate trajectory in 2018 is still

October 2017 to as low as 1,060 in late end target of 2.40%. As such, we see intact as we still expect two more 25bps

December 2017. This was off the back risk of further IDR weakness in line with hikes in 2018 (after the latest March rate

of the normalization of trade and tourism the rest of Asian currencies. Overall, our hike), bringing the FFTR to 2.25% by

ties between China and South Korea last forecast for USD/IDR is 13,800 in 2Q18,

Quarterly Global Outlook 2Q2018

08 UOB Global Economics & Markets Research EXECUTIVE SUMMARY

end-2018. While we remain mindful that RBA: The RBA surprised nobody when after 15 years leading the central bank.

stronger wage & inflation expectations it held its OCR steady at a record low of Other than the usual monetary policy

could add to the risk of a more aggressive 1.5% in March. Overall, we maintain the execution, the combination of the banking

Fed in terms of policy normalization, the view that the RBA is in no hurry to move and insurance regulators into one agency,

flipside is that recent US trade policy rates as household incomes are growing PBoC’s role as a financial regulator will be

developments could warrant a more slowly and debt levels are high; and it clearer and strengthened. We maintain our

cautious Fed, at least until the cloud of seems as though the RBA will continue to view that PBoC is likely to lean on raising

trade uncertainty clears. jawbone the local currency. We also note at least one time its policy rates by end

that a key turning point was 31 January of 2Q18, with a 25bps hike from current

We also expect continuity in Fed Reserve’s – when 4Q inflation data showed both record low of 1Y lending rate at 4.35% and

balance sheet reduction (BSR) program headline and core inflation staying below 1Y deposit rate at 1.50%.

and since trimming the Fed balance the bottom of the RBA's 2-3% target. RBA

sheet is somewhat a 'substitute' for rate Governor Philip Lowe's mid-February MAS: We maintain our forecast of two

hikes, so we believe the continuation of testimony to lawmakers also made it clear more 25bps hikes by the US Fed in

BSR is a key factor the FOMC will take that the RBA will not mechanically follow 2018 after the March 2018 hike. And

into consideration and not add more rate the global trend, and can afford to be more with Singapore’s domestic interest rates

hikes beyond the 3 hikes in 2018 unless patient. following quite closely to the US rates,

we get a sharp inflation surprise. BSR we forecast the 3-month SIBOR to edge

will likely gain further traction in 2018, RBNZ: As expected, the RBNZ held its higher towards 1.70 by 2Q 2018 and

as cuts to reinvestment expand so the OCR unchanged at 1.75% in March. onward to 1.85% by the end of 2018.

aggregate annual cuts will increase from Focus will now be on the new Policy

US$30bn in 4Q 2017 to US$420bn in Targets Agreement (PTA) that Orr will RBI: The RBI had kept its repurchase rate

2018 and reach steady state of US$600bn sign with the Minister of Finance, Grant unchanged at 6% since a 25bps cut in

in 2019. We expect BSR to continue Robertson, and the review of the Reserve August 2017. We were previously having

until the Fed balance sheet is reduced to Bank Act that is currently underway. We a view that the RBI could potentially cut

aboutUS$2.5trillion by mid-2021. continue to expect the RBNZ to remain rates by another 25bps to provide support

accommodative, and do not foresee an to the economy due to the lingering after-

ECB: Overall, there is little implication OCR hike until early-2019. effects of the demonetization and GST.

to our view following the latest ECB However, the impact of both seems to

meeting. The ECB needs to end asset BOJ: Despite another status quo have worn off, while India’s GDP is growing

purchases within the next 12-15 months decision on 9 March, the spectre of above the potential rate and inflation rate

to avoid a bond shortage problem. Yet “BOJ normalization” which crept into expected to inch higher, we now think that

we see little reason, at this juncture, for market psyche in late 2017 lingers the RBI can possibly afford to keep rates

the ECB to make more fundamental on. The re-appointment of Kuroda to unchanged for the rest of 2018.

changes to forward guidance before an 2023 (and appointment of 2 new “like-

announcement on the future of QE is mined” deputies) did not help to dispel BI: We expect inflation to turn higher in

made (likely in June). This should help to normalization concerns, failing to shift the second half of this year. The most

prevent a further strengthening of the EUR market sentiment that Kuroda will stay the recent Bank Indonesia’s consumer survey

and “unwarranted tightening of monetary course and patiently keep BOJ monetary revealed the findings that households

conditions”. As for policy rates, we are not policy broadly “expansionary till 2% is expect prices to go higher starting May

anticipating any rate increases until later met”. BOJ’s cause was not helped by the of this year on the back higher electricity

in 2019. fact that the projected annual pace of JGB and gas tariffs, and possibly higher fuel

buying has continued to moderate so far and gasoline prices. Inflation is estimated

BOE: As expected, the BoE left the Bank this year. While we keep our long-held to be at a range of 2.5-4.5% for 2018,

Rate on hold at 0.50% and asset purchases view that it remains premature to expect with our current 2018 forecast is now

unchanged at GBP435bn in March. But the BOJ to normalize/taper its easing slightly revised lower to 4.0% (from 4.2%

two members of the MPC – Michael program anytime soon, because Japan is before) but remains at the upper range of

Saunders and Ian McCafferty – were the still far away from its 2% inflation target, BI’s inflation target. With the backdrop of

dissenters, voting for an immediate 25bps the uncertainty will continue unless the inflationary pressures coming fairly soon,

rate rise. We had previously been looking BOJ finds a way to reassert its “easy we reiterate our forecast for BI to stay

for the BoE to move only later part of this monetary policy” credentials. neutral for the most part of 2018 and we

year, but there are now more reasons to only pencil in currently a 25bps rate in

think a move at the next meeting in May ASIAN INTEREST RATES December 2018. Our BI rate forecast (7-

is likely. Still, we do not believe the MPC PBoC: PBoC’s prudent and neutral Day Reverse Repo) remains consistent

wants to persuade markets to expect more monetary policy stance has been with our inflation forecast and still lend

hawkish policy thereafter. Whilst a 25bps reaffirmed in the 2018 Government support to overall growth.

move in May (as opposed to August) now Work Report. The policy implementation

looks highly likely, we do not envisage any is expected to remain with the recent

further changes for the rest of this year. appointment of Yi Gang as Governor,

replacing Zhou Xiaochuan who retired

Quarterly Global Outlook 2Q2018

EXECUTIVE SUMMARY UOB Global Economics & Markets Research 09

BOK: From the real interest rate BNM: Bank Negara Malaysia (BNM) kept BOT: The Bank of Thailand (BoT) kept

perspective, the pick-up in headline the Overnight Policy Rate (OPR) at 3.25% the policy rate unchanged at 1.5% on 14

inflation should still keep the door open for on 7 March following a 25bps hike on 25 February 2018. Looking forward, the BoT

1-2 rate hikes this year. A faster pace of January. Real policy rate has widened to will likely raise the policy rate to 1.75% in

U.S. rate hikes will be another catalyst as +1.8% amid slower inflation. With regards the second half of 2018 as the economy

the Base Rate is set to fall below the Fed to forward guidance, BNM reverted to a would continue to expand steadily at

Funds Target Rate for the first time since more neutral tone. BNM kept a balanced around its potential rate, thus lessening the

2007. Although we do not think there is view such that despite renewed signs need for an exceptionally accommodative

an imminent risk of large capital outflows, of emerging volatility and rising trade monetary policy.

it will create pressure for the BOK to act tensions, they expect continuity in global

if the domestic growth outlook permits, economic expansion. BNM kept a positive SBV: The State Bank of Vietnam (SBV)

caveat on the impact of the unfolding view on the domestic economy and would maintain the policy rate at 6.25%

trade tensions. We see the next rate hike reiterated that inflation is expected to until at least the end of 2018. Currently, the

in South Korea taking place in 2Q18 (Apr/ moderate in 2018. We maintain our year- monetary policy stance is accommodative

May) and another possibly in 4Q18. The end OPR projection of 3.25%, implying no and supportive of economic activity.

reappointment of Governor Lee Ju-yeol further rate adjustments for the year. Global growth prospects will also help

is expected to maintain stability in the sustain strong merchandise exports and

monetary policy setting. keep Vietnam’s trade-reliant economy

humming this year.

Real GDP Growth Trajectory

y/y% change 2016 2017 2018F 1Q17 2Q17 3Q17 4Q17 1Q18F 2Q18F 3Q18F 4Q18F

China 6.7 6.9 6.7 6.9 6.9 6.8 6.8 6.8 6.7 6.8 6.7

Eurozone 1.8 2.3 2.3 2.1 2.4 2.6 2.7 2.5 2.5 2.3 2.2

Hong Kong 2.1 3.8 3.4 4.3 3.9 3.7 3.4 3.4 3.5 3.4 3.2

Indonesia 5.0 5.1 5.3 5.0 5.0 5.1 5.2 5.3 5.4 5.2 5.3

Japan 0.9 1.7 1.8 1.4 1.5 1.9 2.0 1.2 2.1 2.1 1.7

Malaysia 4.2 5.9 5.0 5.6 5.8 6.2 5.9 5.4 5.0 5.0 4.8

Philippines 6.9 6.7 6.8 6.4 6.7 6.9 6.6 6.7 6.7 6.6 6.9

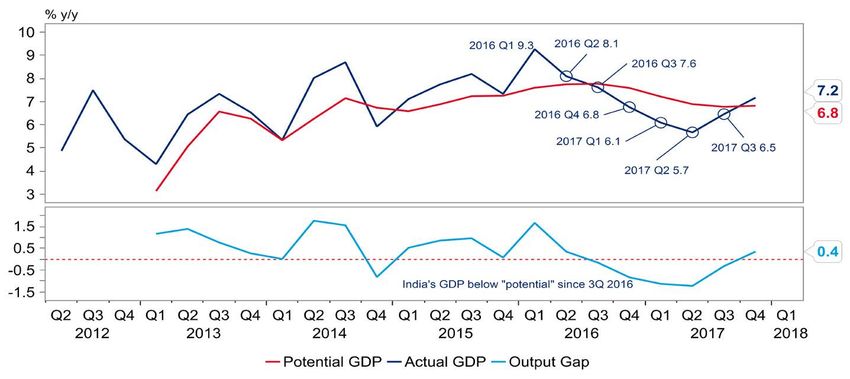

India 8.2 7.1 6.5 6.1 5.7 6.5 7.2 6.3 6.5 6.6 6.7

Singapore 2.4 3.6 2.8 2.5 2.8 5.5 3.6 3.5 3.0 2.2 2.8

South Korea 2.8 3.1 3.0 2.9 2.7 3.8 3.0 3.0 3.0 2.8 3.1

Taiwan 1.4 2.9 2.3 2.6 2.3 3.2 3.3 2.9 2.7 1.9 1.8

Thailand 3.3 3.9 4.0 3.4 3.9 4.3 4.0 4.0 4.0 3.9 4.0

US (q/q SAAR) 1.5 2.3 2.5 1.2 3.1 3.2 2.5 1.0 3.5 2.5 3.0

Source: CEIC, UOB Global Economics & Markets Research

Quarterly Global Outlook 2Q2018

10 UOB Global Economics & Markets Research

FX, INTEREST RATE & COMMODITIES FORECASTS

FX 23 Mar 18 2Q18F 3Q18F 4Q18F 1Q19F RATES 23 Mar 18 2Q18F 3Q18F 4Q18F 1Q19F

USD/JPY 105 100 103 107 110 US Fed Funds Rate 1.75 2.00 2.00 2.25 2.50

EUR/USD 1.23 1.25 1.27 1.29 1.29 USD 3M LIBOR 2.27 2.15 2.15 2.40 2.65

GBP/USD 1.41 1.40 1.38 1.36 1.36 US 10Y Treasuries Yield 2.80 2.80 3.00 3.20 3.25

JPY Policy Rate -0.10 -0.10 -0.10 -0.10 -0.10

AUD/USD 0.77 0.79 0.81 0.83 0.83

EUR Refinancing Rate 0.00 0.00 0.00 0.00 0.00

NZD/USD 0.72 0.74 0.75 0.75 0.75

GBP Repo Rate 0.50 0.75 0.75 0.75 0.75

USD/CNY 6.33 6.35 6.40 6.45 6.50 AUD Official Cash Rate 1.50 1.50 1.50 1.50 1.75

USD/HKD 7.85 7.85 7.85 7.83 7.80 NZD Official Cash Rate 1.75 1.75 1.75 1.75 2.00

USD/TWD 29.2 29.4 29.6 29.8 30.0

CNY 1Y Benchmark Lending 4.35 4.60 4.60 4.60 4.60

USD/KRW 1,081 1,070 1,080 1,090 1,100 HKD Base Rate 2.00 2.25 2.25 2.50 2.75

USD/PHP 52.34 52.50 53.00 53.50 54.00 TWD Official Discount Rate 1.38 1.38 1.38 1.38 1.50

KRW Base Rate 1.50 1.75 1.75 2.00 2.00

USD/MYR 3.91 3.88 3.85 3.80 3.80

PHP O/N Reverse Repo 3.00 3.25 3.25 3.25 3.50

USD/IDR 13,778 13,800 13,850 13,900 13,950

USD/THB 31.26 31.00 31.30 31.50 31.80 SGD 3M SIBOR 1.38 1.70 1.70 1.85 1.85

USD/MMK 1,334 1,350 1,360 1,370 1,380 SGD 3M SOR 1.59 1.50 1.50 1.65 1.75

USD/VND 22,785 22,800 22,900 23,000 23,100 MYR O/N Policy Rate 3.25 3.25 3.25 3.25 3.25

IDR 7D Reverse Repo 4.25 4.25 4.25 4.50 4.50

USD/INR 65.11 65.00 65.30 65.60 66.00

THB 1D Repo 1.50 1.50 1.75 1.75 1.75

USD/SGD 1.32 1.29 1.30 1.32 1.33

VND Refinancing Rate 6.25 6.25 6.25 6.25 6.25

EUR/SGD 1.62 1.61 1.65 1.70 1.72 INR Repo Rate 6.00 6.00 6.00 6.00 6.00

GBP/SGD 1.86 1.81 1.79 1.80 1.81

COMMODITIES 23 Mar 18 2Q18F 3Q18F 4Q18F 1Q19F

AUD/SGD 1.01 1.02 1.05 1.10 1.10

Gold (USD/oz) 1,338 1,290 1,260 1,230 1,200

SGD/MYR 2.98 3.01 2.96 2.88 2.86

Brent Crude Oil (USD/bbl) 69 60-70 60-70 60-70 60-70

SGD/CNY 4.81 4.92 4.92 4.89 4.89

6,000- 6,000- 6,000- 6,000-

JPY/SGDx100 1.25 1.29 1.26 1.23 1.21 LME Copper (USD/mt) 6,695

7,000 7,000 7,000 7,000

Quarterly Global Outlook 2Q2018

UOB Global Economics & Markets Research 11SINGAPORE FOCUS I

Singapore MAS Policy Preview: It’s Time To Catch Up

With Policy Normalization

The Monetary Authority of Singapore (MAS) is expected to release monetary policy decision on the 2nd week of April 2018 (9th to

13th April) and we expect the central bank to start policy normalization by allowing the SGD NEER on a mildly appreciating path (est:

0.5% pa) while keeping the midpoint and bandwidth of the policy band unchanged.

Our policy normalization expectation is based on three key factors. Firstly, global and domestic growth-inflation-labour conditions

have improved quite significantly since the lows of 2015. Central banks around the world today are biased towards tightening, rather

than loosening monetary policy stance.

Secondly, the forex market seems to be pricing in a more hawkish MAS stance as the SGD NEER has appreciated 1.2% since the

start of 2017, while our UOB SGD NEER model also shows that the SGD NEER had been trading consistently above the midpoint

88% of the time in the same period.

Thirdly, the MAS had perhaps signaled a normalization inclination by removing a forward guidance word “extended” from its oft-used

phrase “current neutral SGD NEER policy is deemed appropriate for an extended period of time” in their last October 2017 policy

statement.

With the upcoming April policy normalization by MAS largely priced in, we see limited downside for USD/SGD below 1.30. Furthermore,

any escalation of trade tension between US and China risk negatively impacting Asian exports and consequently is a negative for the

SGD. Overall, we see USD/SGD testing the low of 1.29 across 2Q18, before drifting back up to 1.33 by 1Q19.

The Monetary Authority of Singapore bandwidth of the policy band untouched. the uncertainties of slow global economic

(MAS) is expected to release its half-yearly We think that this is a one-and-done growth and disinflationary pressures.

monetary policy statement sometime in the deal for 2018 although we acknowledge Central banks around the world were also

2nd week of April 2018 (9th to 13th April). there could be room for another 0.5% pa adopting easy monetary policy stance then

increase in the October 2018 policy review, to support economic growth.

We expect the MAS to start the but that will be dependent on the data over

normalization of Singapore’s monetary the next few months. In the two subsequent policy meetings

policy. What this means is that the MAS (October 2015 and April 2016), the MAS

may start to allow the SGD Nominal As a recap of the current accommodative continued to reduce the SGD NEER slope

Effective Exchange Rate (NEER) to monetary cycle, it all started when the towards an eventual “neutral appreciating

embark on a mildly appreciating path MAS surprised the market by reducing the path”, a stance which it had maintained

(which we estimate at 0.5% pa from 0% slope of the SGD NEER in an off-cycle since April 2016 to date.

currently), while keeping the midpoint and policy action in January 2015 to cope with

Quarterly Global Outlook 2Q2018

12 UOB Global Economics & Markets Research SINGAPORE FOCUS IOur expectations of a change of policy Fast forward to today, things have The synchronized recovery is evident in

stance towards a “mild appreciation” SGD improved. In their World Economic both developed (advanced) and emerging

NEER slope is based on the following Outlook Update (11 January 2018), the economies.

arguments: IMF had upgraded global economic growth

forecasts for 2018 and 2019 to 3.9%, from Quoting the IMF again from the same

1. Economics: Global and domestic 3.7% previously. In the words of the IMF: report:

growth-inflation-labour conditions

have improved quite significantly “The cyclical upswing underway since mid- “Among advanced economies, growth in

since the lows of 2015. With that, 2016 has continued to strengthen. Some the third quarter of 2017 was higher than

central banks around the world today 120 economies, accounting for three projected in the fall (ie: October 2017),

are leaning more towards monetary quarters of world GDP, have seen a pickup notably in Germany, Japan, Korea, and the

policy tightening, after many years of in growth in year-on-year terms in 2017, United States. Key emerging market and

very loose monetary policy conditions. the broadest synchronized global growth developing economies, including Brazil,

upsurge since 2010.” China, and South Africa, also posted

2. Expectations: the forex market third-quarter growth stronger than the fall

seems to be pricing in a more hawkish We reproduce the IMF’s forecast during forecasts.”

MAS stance (ie: appreciating SGD their October 2017 release in Exhibit 1. It

NEER) as the SGD NEER had can be clearly seen that even in October Additionally, we also observed that both

appreciated 1.2% since the start of 2017, the IMF had expected stronger the emerging and developed economies’

2017. Moreover, our UOB SGD NEER growth and inflation worldwide, and purchasing managers’ indices are

model also shows that the SGD NEER reaffirmed it in their January 2018 review. expanding in sync, across both the

had been trading consistently above manufacturing and services sectors no

the midpoint 88% of the time in the less (Exhibits 2A and 2B).

same period.

Exhibit 1: IMF’s October 2017 Forecast For Global Growth And Inflation

3. Policy: the MAS had perhaps signaled

a similar inclination by removing a Source: Macrobond, UOB Global Economics & Markets Research

forward guidance “extended period”

from its oft-used phrase “current

neutral SGD NEER policy is deemed

appropriate for an extended period”

in their last October 2017 policy

statement.

With the three factors at play, we think that

the time is ripe for the MAS to embark on

the normalization of Singapore’s monetary

policy. We will explain in details in the

following sections.

Global Economic Recovery Is In Sync

The global economic landscape had

improved quite dramatically over the past

three years. As recent as the MAS October Exhibits 2A & 2B: Synchronised Growth In Manufacturing & Non-manufacturing PMI

2016 policy meeting, we were still very

concerned about the global deflationary Source: Macrobond, UOB Global Economics & Markets Research

environment, hard landing risk from China,

and the unknown but “surely” negative

impact from Brexit.

Domestically, policymakers were worried

about the very slow economic growth

in Singapore, disinflationary pressures,

rising labour redundancies (particularly in

the Professionals, Managers, Executives

and Technicians or PMETs segment) and

industry-specific risk factors (eg: from the

offshore & marine industries). Those were

the conditions for an accommodative and

thus dovish monetary policy: a-la neutral

SGD NEER slope.

Quarterly Global Outlook 2Q2018

SINGAPORE FOCUS I UOB Global Economics & Markets Research 13Stronger economic activities and higher

prices point to the improvement in Exhibit 3: Recovery In World Trade Since 4Q 2016

aggregate demand worldwide and this is Source: Macrobond, UOB Global Economics & Markets Research

also evident in the recovery in world trade

since 4Q 2016 (Exhibit 3).

However, this also implies higher export

and import prices across the world (Exhibit

4). Eventually, these will pass-through to

higher global consumer inflation – another

indication that central banks may need to

tighten monetary policies at a faster pace.

Our global monetary environment scan

across 52 central banks’ actions since

Mar 2017 shows a total of 18 central

banks hiking interest rates to a combined

amount of 1,846.5bps; 26 central banks

keeping interest rates unchanged; while 8

central banks cutting rates to a combined

Exhibit 4: Strongest Growth In Export and Import Prices Since August 2011

amount of 1,475bps. Collectively, there

had been an inclination for central banks to Source: Macrobond, UOB Global Economics & Markets Research

tighten rather than loosen their respective

monetary policies (Exhibit 5).

Domestic Growth Drivers

Are Improving

In Singapore, the growth-inflation-labour

dynamics had improved too.

The government’s report card on 2017

economic performance probably scored

an “A” in our opinion as actual GDP grew

3.6%, above the upper end of the initial

forecast range of 1%-3% back in early

2017.

Core inflation, the intermediate target

of the central bank when it comes to Exhibit 5: More Global Central Banks Embarking On Monetary Tightening

assessing the direction of its monetary

policy, averaged 1.5% in 2017, higher than Source: Bloomberg, UOB Global Economics & Markets Research

the 0.9% in 2016 and 0.5% in 2015.

The labour market has also been improving

as indicated by various labour market

statistics including better job vacancy-to-

unemployed persons ratio and stronger

wage growth.

On growth, another way to assess the

current economic condition is to compare

it with the potential economic growth.

If the actual GDP growth rate is higher than Note: Central banks that hiked rates since March 2017 includes (375bps: Argentina), (300bps: Egypt, Ukraine), (125bps: Mexico),

(85.5bps: Oman), (75bps: Bahrain, Canada, Hong Kong, UAE, US), (70bps: Czech Rep), (50bps: Romania), (41bps: Venezuela),

the potential GDP growth rate, then there (25bps: Malaysia, Pakistan, Qatar, South Korea, UK). Central banks that cut rates since March 2017 includes (-625bps: Brazil),

(-275bps: Colombia), (-250bps: Russia), -125bps: Peru), (-75bps: Iceland, Chile), (-25bps: South Africa, India).

is a positive output gap which may result

in a higher inflationary environment and

justifying a more hawkish monetary policy

(ie: an upward sloping SGD NEER).

Quarterly Global Outlook 2Q2018

14 UOB Global Economics & Markets Research SINGAPORE FOCUS IAs such, we compare Singapore’s quarterly

real GDP growth rate with its potential EXHIBIT 6: Finally Out Of The Negative/Weak Output Gap Trap

GDP growth rate (derived using the Source: Macrobond, UOB Global Economics & Markets Research

Hodrick-Prescott filter) and found that after

suffering from 10 consecutive quarters

of negative or weak positive output gap

(since 2Q 2014), the stronger growth spurt

of 3Q 2017 had finally pushed Singapore’s

economy into registering a positive 2.4%

output gap in that quarter (Exhibit 6).

With the uplift from stronger external

demand, overall corporate profits had been

robust and posted the strongest expansion

(6.9% y/y) since 2010 (Exhibit 7).

With profits expanding at a record pace,

businesses are more confident and

investments had also expanded for the

first time, after five consecutive quarters of

Exhibit 7: Corporate Profits Expansion At Its Strongest Since 2010

contraction (3Q 2016 to 3Q 2017) (Exhibit

8). Source: Macrobond, UOB Global Economics & Markets Research

Domestic consumption also expanded

at a healthy clip from the improvement

in the labour market conditions (low

unemployment and stronger wage growth).

Looking ahead, the government’s

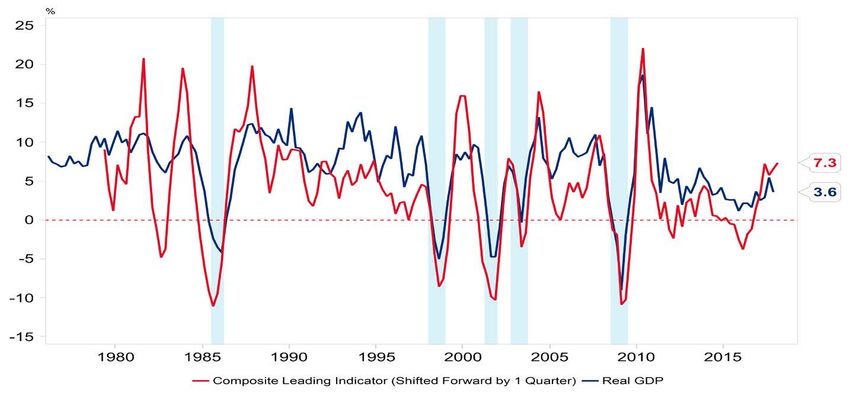

composite leading indicator (Exhibit 9),

which leads GDP growth by 1 quarter,

shows that we can expect continued

strength in economic growth.

That said, we believe that GDP growth

for 2018 could come in at a slower pace

of 2.8%, due to the high base in 2017,

and the expected slower growth in the

manufacturing sector. Exhibit 8: Continued Strength in Domestic Consumption, While Investments Expanded Finally

On inflation, Singapore’s core inflation had Source: Macrobond, UOB Global Economics & Markets Research

averaged 1.5% in 2017, higher than the

0.9% recorded in 2016 and 0.5% in 2015

(Exhibit 10).

For 2018, we forecast core inflation to

average 1.5%, while the MAS is expecting

an average of 1-2%. With prices rising at a

structurally higher level compared with the

2015-16 period, we believe that there is

some room for monetary policy to catch up

vis-à-vis SGD NEER appreciation stance.

Quarterly Global Outlook 2Q2018

SINGAPORE FOCUS I UOB Global Economics & Markets Research 15On labour market conditions, we observe

some improvements across various labour Exhibit 9: Composite Leading Indicator Points To Robust Economic Growth

market statistics. Source: Macrobond, UOB Global Economics & Markets Research

First, there had been some improvements

in labour market slack. Although there

are currently only 87 vacant jobs to every

one hundred unemployed persons, this is

an improvement from a recent low of 77

vacant jobs in 4Q 2016 (Exhibit 11).

Second, with demand for labour increasing,

we also observed that wage growth is

also on an uptrend (Exhibit 12), further

supporting domestic consumption, and

potentially generating higher pass-through

to consumer prices in the months ahead.

Expectations For Monetary Policy

Normalisation Are Rising

Exhibit 10: Core Inflation At A Structurally Higher Level Compared with 2015-16

With the improving growth-inflation-labour

conditions, the forex market had been Source: Macrobond, UOB Global Economics & Markets Research

pricing in expectations for the MAS to turn

more hawkish and to normalize the SGD

NEER slope sooner, rather than later.

Indeed, the SGD NEER had appreciated

1.2% from the start of 2017 to date and

our UOB SGD NEER had been trading

persistently above the midpoint (88% of

the time) in the same period (Exhibit 13).

This expectation was perhaps further

fueled by the MAS removing a forward

guidance word “extended period” from

its oft-used phrase “current neutral SGD

NEER policy is deemed appropriate for

an extended period” in their latest October

2017 policy statement.

Exhibit 11: Improvement In Labour Market Slack

With the above-mentioned conditions, Source: Macrobond, UOB Global Economics & Markets Research

we believe the MAS will start policy

normalization in the upcoming April

2018 meeting, where the SGD NEER

slope will be on a mildly appreciating

path (we estimate at 0.5% pa, from 0%

pa currently). We think that this is a

one-and-done deal for 2018 although

there remains a possibility of another

increase (of 0.5% pa) in the October

2018 policy review, depending on data

over the next few months.

Quarterly Global Outlook 2Q2018

16 UOB Global Economics & Markets Research SINGAPORE FOCUS ILimited Room For Further Downside

In USD/SGD Below 1.30 Exhibit 12: Wage Growth Back To Healthy Levels

As mentioned above, ahead of the widely Source: Macrobond, UOB Global Economics & Markets Research

anticipated policy normalization by the

MAS in mid-April, the SGD NEER has

been trading predominantly at a premium

above its estimated mid-point of the current

neutral range. Similarly, exacerbated by

the weak overall tone in the USD, the SGD

has been trading on a strong note as well.

As a result USD/SGD continued to head

lower across 1Q18, from 1.34 at the start

of Jan18 to current level of just around

1.31.

Going forward, we believe that it may be

difficult for the SGD to strengthen further

against the USD. Rather, with increasing

trade tensions between the United States Exihibit 13: Market Pricing In MAS Hawkishness Since April 2017

and China, trade and exports from Asia

Source: CEIC, UOB Global Economics & Markets Research

are at risk of getting negatively impacted.

Given that Asian economies have large 129 Easing Round 1 Easing Round 2 Easing Round 3 MAS kept neutral stance unchanged in

export components, there is an increasing Oct 16, Apr 17 and Oct 17 meetings

MAS shifted SGD NEER MAS shifted SGD MAS shifted SGD

risk that Asian currencies like the CNY, 127 slope from 2% to 1% in NEER slope from 1% NEER slope to

an off-cycle decision to 0.5% Neutral

KRW and including the SGD may weaken

somewhat should trade tensions rise

125

further.

123 SGD NEER was trading above

This also comes at a time when the US midpoint 88% of the time since

Federal Reserve is poised to continue Jan 2017

121

its monetary policy normalization, with

gradual rate hikes and on-going balance

sheet reduction. As such, we maintain our 119

Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18

view that it may be difficult for the SGD to

SGD NEER Upper-end: 2% Mid-Point of Estimated Policy Band Lower-end: 2%

strengthen further. In other words, there

may be limited downside for USD/SGD

below 1.30. Overall, we forecast USD/

SGD at 1.29 in 2Q18, 1.30 in 3Q18, 1.32 in

4Q18, 1.33 in 1Q19.

Quarterly Global Outlook 2Q2018

SINGAPORE FOCUS I UOB Global Economics & Markets Research 17You can also read