Reinvestment Opportunity, is it Time? - Dave Robertson, Partner Treasury Strategies Inc.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Reinvestment Opportunity, is it Time? Presented by: Dave Robertson, Partner Treasury Strategies Inc. Mike Lipinski, Vice President Global Treasury Management BMO Harris Bank Windy City Summit, June 7, 2012

Corporate Cash in Selected Regions

£0.75T

1

U.S. Corporate Cash Growing

Faster than GDP

2

Corporate Cash as % GDP by Region

Country / Region 2000 2011

United Kingdom 26% 50%

Eurozone 15% 21%

United States 10% 14%

Source: Treasury Strategies estimate

3

Sources of Corporate Cash:

Past 6 Months

Sources of Cash (U.S.) Dec-10 Jun-11 Dec-11

Positive cash flow from operations 94% 92% 87%

Debt issuance (medium and long-term) 20% 15% 18%

Reduction of inventories 46% 3% 14%

Sale of company assets, divestitures 6% 14% 14%

Increased short-term borrowing 9% 16% 10%

Equity issuance 6% 3% 5%

Reduction in dividends 0% 1% 1%

Source: Treasury Strategies, Inc. Quarterly Corporate Cash Survey™, December 2011

4Uses of Corporate Cash:

Past 6 Months

Uses of Cash (U.S.) Dec-10 Jun-11 Dec-11

Capital expenditures 27% 33% 39%

Acquisitions 9% 19% 28%

Debt redemption (medium and long-term) 14% 21% 18%

Pay down of short-term borrowing 14% 10% 17%

Negative cash flow from operations 55% 22% 16%

Equity repurchase, stock buyback 10% 18% 14%

Increased inventories 18% 5% 11%

Increased pension fund contributions 0% 12% 7%

Increased dividends or special dividends 5% 5% 5%

Source: Treasury Strategies, Inc. Quarterly Corporate Cash Survey™, December 2011

5What Do Treasurers Say About Risk?

Past Six Next Six

U.S. Only Months Months

(Dec-11) (Expected)

Maturity Structure

Shorter 28% 5%

Longer 5% 12%

About the Same 66% 83%

Credit Risk

More

22% 10%

Conservative

Less

3% 7%

Conservative

About the Same 75% 83%

Source: Treasury Strategies, Inc. Quarterly Corporate Cash Survey™, December 2011

6Maturity Structure

U.S. corporations hold almost 75% of total liquidity in overnight investments,

money funds and bank deposits.

Source: Treasury Strategies, Inc. Quarterly Corporate Cash Survey™, December 2011

7Instruments

U.S. corporations hold approximately 75% of total liquidity in bank accounts (DDA,

MMDA/Savings, and Sweep) or money market mutual funds.

% of Holdings by Instrument (U.S.

Dec-11

Only)

DDA Accounts 38%

Money Market Mutual Funds 23%

MMDA/Savings Accounts 12%

Government Securities 7%

Sweep Accounts 7%

Other Instruments 13%

Source: Treasury Strategies Inc. Quarterly Corporate Cash Survey™, December 2011

8What Treasury Strategies

Clients Are Saying

“Issuing debt earlier than

“Improved cyclical needed to take advantage

performance and cautious “Reduction of operating of low interest rates. Cash

capital investment.” expenses. Lower than from operations better than

expected interest rates historically. Expect cash

projected to remain constant position to slowly draw

for next 3 years.” down as capital

expenditures are made.”

“We had a temporary hold in

investing long term. Cash

should start to decrease in “…we are positioning a

2012 into longer term portion of the portfolio to

take advantage of “We initiated several

investments.”

potential rising rates 18- revenue cycle initiatives

24 months down the that increased cash

road.” collections. We expect it to

remain at the new level.”

“Our company is

continuously growing

“Holding higher

organically and “1) Decrease in

liquidity to insulate

through acquisition.” personnel. 2) Extended

from business

volatility.” payment periods for

accounts payable.”

9What Treasury Strategies

Clients Are Saying

“Equity issuance coupled “An investment decision was made to “Steady profitable

with increased cash flow issue CP and keep the proceeds in growth.”

from ops. Expected to cash on deposit with the banks. Until

remain this way for the future seems ‘clearer,’ I would

foreseeable future.” imagine the balances will stay high

“We build up in

through early next year.”

preparation for large

pension funding.”

“We have monetized non-strategic

investments on the balance sheet “Less opportunities to invest. “We increased our cash levels

to maintain cash levels. We are Why take risk if the return is during the financial crisis to

cutting cost to increase cashflow negligible?” ensure liquidity. We have

going forward.” already begun to bring them

back to a normal level.”

“Increase in net income and limited

capital expenditures. Cash should

“Near‐zero interest rates.

continue to increase this year, but

Opportunity to offset bank fees

at a slower pace.”

using earnings credits.”

10How Management of

Corporate Cash is Changing

Current market dynamics encourage corporate treasurers to move more quickly to

the third generation of corporate treasury where they are the financial nerve center

of the corporation.

Past Next

Changes to Corporate Treasury (U.S.)

6 Months 6 Months

Increasing reliance on cash forecasting 47% 43%

Implementing new technology for cash

15% 31%

management

Formally modifying investment policies 30% 20%

Formally modifying risk management policies 8% 5%

Source: Treasury Strategies, Inc. Quarterly Corporate Cash Survey™, December 2011

11What Do Treasurers Say About Risk?

Past Six Next Six

U.S. Only Months Months

(Dec-11) (Expected)

Hedges of FX

Exposures

Increasing 3% 3%

Decreasing 12% 15%

About the Same 86% 83%

Source: Treasury Strategies, Inc. Quarterly Corporate Cash Survey™, December 2011

12Redenomination Risk

• What will happen if the eurozone does not remain intact?

• Low probability x Significant impact = Cause for concern

• The slim probability of a collapse, combined with the severe magnitude of its impact,

makes the expected value a material concern for many global companies.

• It is now incumbent upon financial managers, perhaps even a fiduciary responsibility, to

consider this issue.

• Scenarios

• Single country exit

• Multi-country exit

• Total breakup

13Redenomination Risk

• Key Issues

• Denomination of obligations

• Jurisdiction

• Sovereign immunity

• Levels of impact

• Primary

• Secondary

• Overall economy

14Treasury Strategies Advice to Clients

• Key themes emerging from our work with Corporate Treasurers

• Review and clarify investment policies in the “gray areas”

• Shorten maturities

• Increase credit quality

• Move assets into insured bank deposits

• Move assets into money market funds (MMFs)

• Issue commercial paper - as much as market will absorb

• Issue debt securities - as much as market will absorb

• Improve treasury technology tools

• Improve cash forecasting

Disclaimer: Treasury Strategies recommendations are situation specific and based upon careful, individual analysis. The advice cited above may or

may not be appropriate for your specific situation.

15Managing Redenomination Risk

Treasury Strategies advises our clients to institute a five step process in evaluating

the implications of a eurozone breakup:

1. Conduct a complete assessment of all primary and secondary eurozone exposures.

2. Stress test these exposures under the three scenarios of a single country exit, multi-country exit and

full dissolution.

3. Amend or clarify all contracts as appropriate.

4. Implement as many natural hedges as feasible.

5. Structure financial hedges to manage the remaining risks.

Disclaimer: Treasury Strategies recommendations are situation specific and based upon careful, individual analysis. The advice

cited above may or may not be appropriate for your specific situation.

16FDIC Changes

• Under proposed change banks will be charged insurance premiums based on net

assets (total assets less tangible equity)

• FDIC has option to adjust rate as much as 15 basis points not to exceed 35 basis

points, based on its own judgment of a bank’s risk

• Temporary Unlimited Deposit Insurance non-interest bearing transaction accounts

2011-2012

Source: Initial and Total Base Assessment Rates FDIC 12 CFR part 327

Risk Category I Risk Category II Risk Category III Risk Category IV Large and Highly

Complex

Institutions

Initial Base 5-9 14 23 35 5-35

Assessment rate

Unsecured debt (4.5)-0 (5)-0 (5)-0 (5)-0 (5)-0

adjustment

Brokered deposit ….. 0-10 0-10 0-10 0-10

adjustment

Total Base 2.5-9 9-24 18-33 30-45 2.5-45

Assessment Rate

17Reg Q Repeal – ECR vs Interest Rate

• Banks provide choice post July 2011

• Interest-bearing commercial accounts will trigger 1099INT for interest income earned throughout the

year

• Interest-bearing commercial accounts for 2011-2012 will have limited FDIC coverage at $250k

DDA/non- MMDA Corporate NOW Money Market Eurodollar Repo/MMDA Interest- Fixed Income Separate

interest Mutual Fund Sweep Sweep bearing Investment Managed

bearing Sweep transaction Portfolio

transaction account

account

Cash Operating Reserve Operating Operating Operating Operating Operating Reserve, Reserve,

Type Restricted, Restricted,

Strategic Strategic

Liquidity/ daily weekly daily daily to 90days daily daily daily daily to > 90 days 90 days > 360

Duration + days +

FDIC Unlimited $250,000 limit $250,000 limit Unlimited on DDA Unlimited on Unlimited on $250,000 None None

Coverage portion– None on DDA portion– DDA portion– limit

invested None on $250k limit on

invested interest

portion

Yield ECR Interest Interest Dividends Interest Interest ECR/Interest Interest/Cap Interest/Cap

Type gains/Divs gains/Divs

IRS None 1099INT 1099INT 1099DIV 1099INT 1099INT 1099INT 1099DIV/INT & 1099DIV/INT

other & other

Restrict None Limited to 6 Limited to non-profit; Limits dictated by Base amount Base amount None Client Investment Client

disbursements sole proprietorships portfolio selected required prior required prior Policy/risk Investment

/month to sweep to sweep tolerance Policy/risk

tolerance

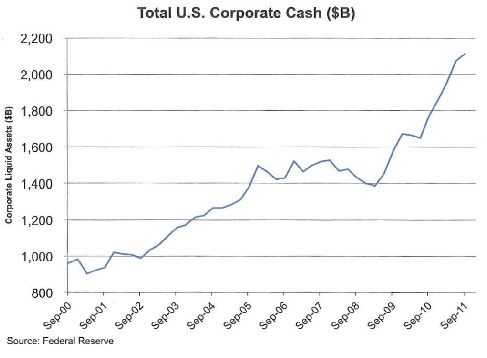

18Corporate Cash Levels

U.S. Federal Reserve: U.S. Corporate Cash a/o 9/30/11 was $2.11T

19U.S. Sets Money-Market Plan WSJ 2/7/12

A Shrinking Pie – 2a7 Funds SEC Aims to Stabilize $2.7 Trillion Industry; Critics Say

Rules Would Cut Returns

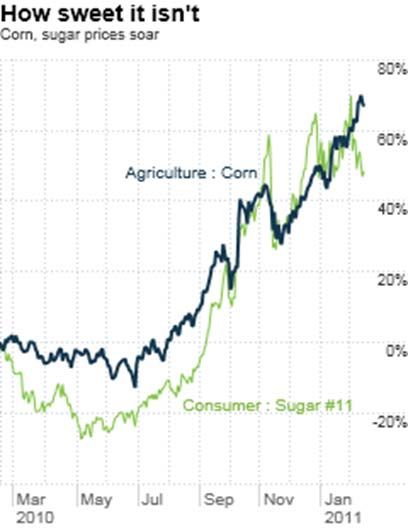

20Rising Commodity Prices

Source: Fortune.com 2/16/11

21OTC and Exchange Traded Derivatives The Economist Financial

Plumbing & Promises 2/27/12

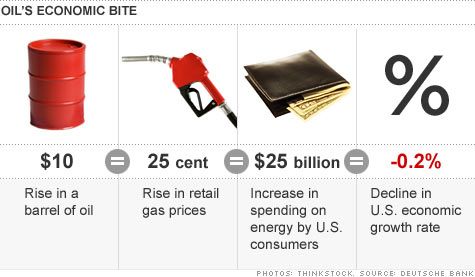

22Rising Commodity Prices

Economy faces new threats

By Chris Isidore, senior writerFebruary 24, 2011:

4:02 PM ET

Source: CNN Money.com 2/24/11 By Chris Isidore, senior writerFebruary 24, 2011: 4:02 PM ET

23Oil Price Spike Biggest Threat to Economy

Iran-fueled oil price spike biggest threat to economy

By Steve Hargreaves @CNNMoney April 11, 2012: 9:24 AM ET

Fear that a confrontation with Iran would push oil prices to $200 a barrel eclipses European debt crisis,

China slowdown as biggest threat to the economy. CNN Money 4/11/12

24Unemployment Forecast

President Ronald Reagan and Vice

President George H. Bush in

January 1983, when the

unemployment rate fell to 10.4

percent from 10.8 percent, the first

decline that large in five years.

Source: The New York Times 2/3/11

25DOL Study - Deeper Recessions, Slower

Recoveries Source: Bureau of Labor Statistics. The Washington Post. Published on April 10, 2012, 9:11

Labor force study predicts deeper recessions and slower recoveries

26Appendix / Sources

• Business Finance Magazine.com

– Managing Health Care Refrom Decision Making 12/21/11

• CNN Money and Fortune.com

– How Sweet it Isn’t ,Corn, sugar prices soar, 2/16/11 Source:

– Oil tops $106 a barrel, 3/7/2011

– States with the Worst Tax Burdens, 2/24/11, Tax burden falls for the first time in decade, Source: Tax Foundation Study Based on 2009 Data

– State & Local Tax Burdens, All States, 2009, 2/24/11, Source: Tax Foundation calculations based on data from the Bureau of Economic Analysis, The Census Bureau, The Council on State

Taxation, the Travel Industry Association, the Department of Energy and others

– Fed predicts weak recovery for several years, Fed’s Economic Outlook, 11/23/10, Source: Federal Reserve

– Emerging Markets are Hot – Place Your Bets, 2/1/11

– Mortgage Rates Fall to Record Lows 12/15/11

– Young Workers Getting Hired Again 12/1/11

– November Jobs Report 12/2/11

– Biggest Market Risk: Middle East Turmoil 4/7/11

– The Fight Just Gets Dumber 4/8/11

– Euro drops below $1.30 mark 12/14/11

– Federal Revenue Sources 4/12/11

• CFO.com

– Easier Access, The amount of credit extended by suppliers to their trade customers has reached its highest level since January 2007, 2/7/11, Source: National Association of Credit

Management’s Credit Managers’ Index.

• Economist

– America’s GDP 4th qtr 2011 12/16/11

• FDIC.gov

– Initial and Total Base Assessment Rates FDIC 12 CFR part 327

• Forbes

– Ten Ways Small Businesses can Lower Health Care Costs (and hire more people) in 2012 12/5/11

• McClatchy Newspapers

– What gives? U.S. Corporations Rebounding from 2008 Financial Crisis 3/27/11

• Oliver Wyman

– Price Shocks; Commodity price increases in 2010, by percentage

• The New York Times

– Most Regions Experience Modest Growth, 3/3/11, Source: Fed’s Beige Book info collected before 2/18/11

– Largest One-Month Declines in U.S. Unemployment Rate 1965-2010, 2/3/11, Source: Bureau of Labor Statistics via Haver Analytics

– Keeping it Temporary, Net Private Sector Jobs Added, Source: Bureau of Labor Statistics

– Housing Construction, 11/17/11

• Treasury Strategies Inc.

– Quarterly Corporate Cash Survey December 2011

• Wall Street Journal

– A Shriking Pie, Money fund assets, 1/1/11, Source: iMoneyNet

– Czechs Wary of Joining Troubled Euro, 7/9/10

– What the Health Care Law Will Mean for your Small Business, 12/7/11

• Washington Post

– GDP Grew at Fastest Pace in 1.5 years 12/16/11

27Disclaimer

• BMO Harris Bank is a trade name used by BMO Harris Bank N.A. Banking deposit and loan products and services are

provided by BMO Harris Bank N.A. Member FDIC.

• Brokerage products are offered through Harris Investor Services, Inc. (HIS), a registered broker/dealer, member

FINRA/SIPC, and SEC-registered investment advisor. Insurance products are offered through Harris Bancorp

Insurance Services, Inc. (HBIS). Investment banking services are provided by BMO Capital Markets Corp. (BMOCMC)

and BMO Capital Markets GKST, Inc. (GKST), a Municipal Bond Dealer and member FINRA and SIPC. Financial

planning and investment advisory services are provided by Sullivan, Bruyette, Speros & Blayney, Inc. (Harris SBSB),

an SEC registered investment advisor. Family Office Services are provided by Harris myCFO, Inc. Investment advisory

services are offered by Harris myCFO Investment Advisory Services LLC (Harris myCFO), an SEC-registered

investment advisor and wholly-owned subsidiary of Harris myCFO, Inc. Stoker Ostler Wealth Advisors (Stoker Ostler) is

an SEC-registered investment advisor. Investment advisory services to institutional clients are provided by Harris

Investment Management (HIM) or its wholly-owned subsidiary HIM Monegy (Monegy), SEC-registered investment

advisors. Products offered by HIS, HBIS, BMOCM, Harris SBSB, Harris myCFO, Stoker Ostler, HIM, and Monegy,

which are affiliated companies and wholly owned subsidiaries of BMO Financial Corp., are NOT INSURED BY THE

FDIC OR ANY FEDERAL GOVERNMENT AGENCY, NOT A DEPOSIT OF OR GUARANTEED BY ANY BANK OR

BANK AFFILIATE, MAY LOSE VALUE. The purchase of insurance or an annuity is not a condition to any bank loan or

service. Not all products and services are offered in every state and/or location.

• Third party web sites may have privacy and security policies different from BMO Harris Bank. Links to other web sites

do not imply the endorsement or approval of such web sites. Please review the privacy and security policies of web

sites reached through links from BMO Harris Bank web sites.

28You can also read