Relevant aspects and inconsistencies of the New Annual Tax Statement for legal entities 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Relevant aspects and inconsistencies of

the New Annual Tax Statement for legal

entities 2019

Background

The Tax Administration Service (Servicio de Administración Tributaria) has made available to taxpayers a

platform named “New Annual Tax Statement” (“Nueva Declaración Anual”) (hereinafter the “Tool”) in order

to file the statement for tax year 2019. It is worth mentioning that, unlike previous tax years, when prior

versions could be used simultaneously with the most recent version, it has become an active Tool for the

filing in connection to year 2019 and, regarding years 2018 and previous years, the former platform must

be used to file and consult.

As a part of our support services for the determination of the annal income tax for legal entities and filling

out the annual statement we have identified some inconsistencies and/or relevant aspects to be considered.

Our suggestion is to access as soon as possible to the annual statement tool in order to review and validate

the default information preloaded to a certain closing date and to make the relevant cross checking with

the worksheets or reports created to determine the annual income tax, as well as the base for the statutory

employees profit sharing (PTU), as appropriate.

For a further understanding, please find below the illustration on the most relevant point (NOTE: The

following images are merely for illustration purposes.):

Preloaded default information up to a certain closing date

To the issue date of this newsletter, preloaded information is for the purposes of interim payments and

withholdings to 20/02/2020 and in connection to the digital invoices (CFDI) for payroll to 02/02/2020.

To pre-fill your annual statement, Tax Administration

Service has the following information:

• Interim payments and payment of

withholdings up to closing date: 20/02/2020

• CFDIs for payroll up to closing date:

20/02/2020

ACCEPT

IMAGE 1

Consequently, it is important to consider that SAT has suggested, through the frequently asked questions,

that in the event that the preloaded income information regarding interim payments does not match, the

taxpayer must file a supplementary tax statement, expecting the following results:

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

opinion of the already expressed.

o If the statement did not result in a payable amount, this will be reflected the following day.

o If a payable amount resulted, it shall be reflected within a 48 hour-term after the payment

is made at an authorized Credit Institution.

Accordingly, we recommend considering such terms, review the information and, as the case may be, file

supplementary statements and bear in mind that the tool will be updated to acknowledge such changes.

Income which was not previously declared

A shown in the next image, the nominal income heading is preloaded with the information from interim

payments to December, 2019.

Regardless of the nominal income heading, there is a heading named “Income which was not previously

declared” (“Ingresos no manifestados anteriormente”), which has created certain confusion and doubt

regarding the information to be included therein.

Income Authorized deductions Calculation Payment Additional information

Fields with star (*) are mandatory

*Nominal income DETAIL

Advance payments from clients, previous years (-)

*Annual inflation adjustment (+) CAPTURE

Income which has not been previously declared (+)

*Did you receive income from abroad?

Total accruable income (=)

IMAGE 2

To this regard, the SAT has expressed through its frequently asked questions document that the income to

be informed in such heading are those to be accrued, pursuant to the law, until the annual tax statement,

for example:

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

opinion of the already expressed.

• Incentives applied to interim payments and

• Business trusts.

In our opinion, the heading is also aimed at taxpayers applying Rule 3.2.4 Option to accrue income for

total or partial collection of the price, or even certain items that may be in conciliation (such as recovery

of previously deducted doubtful accounts, profit for liquidation and merging of companies).

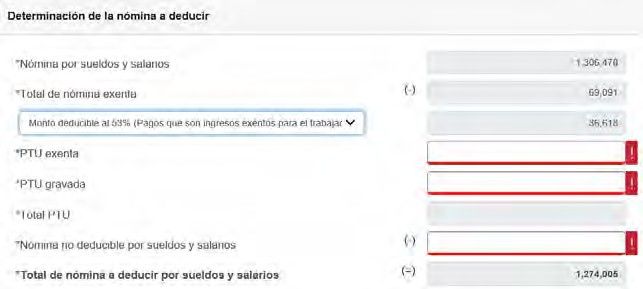

Authorized Deductions – PTU as part of the deduction of wages and salaries

Statutory Employees Profit Sharing (Participación de los Trabajadores en las Utilidades or PTU) paid during

the year is a subtracting concept of accruable income1, i.e. it is not part of the authorized deductions.

We have observed that the tool to file the annual tax statement considers the heading of wages and salaries

as authorized deductions (preloaded amount), with the possibility of capturing certain information, such as

the heading for exempt PTU and levied PTU. The latter is considered within the total payroll amount to be

deducted.

The image below shows examples of how this is visualized in the tool:

I. Without PTU information

Determination of the payroll to be deducted

*Payroll for wages and salaries

*Total exempt payroll (-)

Deductible amount up to 53% (payments which are exempt income to

employee)

*Exempt PTU

*Levied PTU

*Total PTU

*Non-deductible payroll for wages and salaries (-)

Total payroll to be deducted for wages and salaries (=)

IMAGE 3

1 Article 9, section I of the Mexican Income Tax Law in force.

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

opinion of the already expressed.

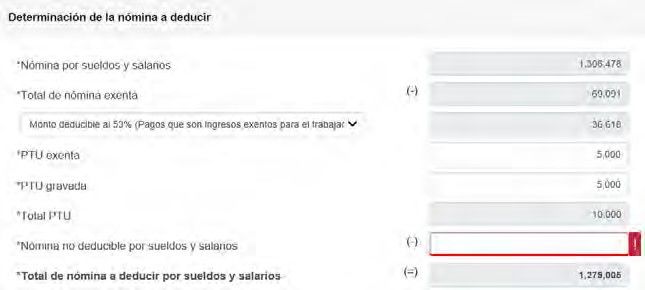

II. With PTU information: the total amount of the payroll to be deducted for wages and salaries is

added with the levied PTU.

Determination of the payroll to be deducted

*Payroll for wages and salaries

*Total exempt payroll (-)

Deductible amount up to 53% (payments which are exempt income to

employee)

*Exempt PTU

*Levied PTU

*Total PTU

*Non-deductible payroll for wages and salaries (-)

Total payroll to be deducted for wages and salaries (=)

IMAGE 4

It is important to mention that the information related to levied and exempt PTU is not preloaded; therefore,

each taxpayer must include the corresponding information. However, these concepts are deemed as a

deduction for payroll, which is not correct, as it is an independent concept to be subtracted. This is

confirmed in the section corresponding the determination of the income, where such concept is found

separate from deductions.

Authorized Deductions – Exempt travel allowances

It has been observed in the tool that the total exempt income receives the treatment as a partial deduction

pursuant to section XXX of article 28 of the Income Tax Law (deduction to al 53% or 47%, as appropriate).

To this regard, it must be considered that exempt income includes travel allowances registered when an

employee timely evidences the expenses made on behalf of the employer, which receive a specific

deduction treatment, as they are expenses pertaining to the employer in its capacity as direct income tax

payer.

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

opinion of the already expressed.

Authorized Deductions – Total payroll differences

The field for wages and salaries shows an amount preloaded in accordance to the information of the payroll

CFDIs and allows to see the detail of the monthly summary of the “Total payroll”, “Exempt payroll” and the

difference between “Income tax withheld” and “Income tax paid”, as depicted in the image below:

Total payroll for wages and salaries

Month Total payroll Exempt payroll Income tax withheld Income tax paid Difference

January

February

March

April

May

June

July

August

September

October

November

December

IMAGE 5

Since the system does not allow to edit the fields, it is suggested to review and verify, as soon as possible, if

there are differences. In the event of identifying inconsistencies, supplementary statements should be filed

in order to update the information or else make or correct any record on or before February 29th, 2020,

according to the provision of Tax Administrative Rule 2.7.5.7. For this purpose, the time in which the tool is

updated must be considered, as mentioned hereinabove.

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

opinion of the already expressed.Additional Data – PTU Produced during the fiscal year

Article 9, last paragraph of the Income Tax Law sets forth the mechanism to calculate the PTU of the fiscal

year, eliminating for said purposes the non-deductibility of the payments which constitute an exempt

income to employees, as illustrated below.

Accruable Income

( - ) Authorized Deductions

( - ) No-deductible items (Art. 28, sec. XXX of Income Tax Law

( = ) PTU Base

However, it has been identified that the Tool automatically considers the “total exempt wages and benefits”

in the field of additional data (see image 4 herein) and not the corresponding deductible percentage.

PTU produced during the fiscal year considered in this statement

Accruable income

Non-deductible wages and exempt benefits (-)

Authorized deductions (-)

PTU base (=)

PTU rate %

PTU to be distributed (=)

IMAGE 6

Accordingly, we suggest performing a detailed review in order to avoid a distorted PTU determination. For

example, in this case the distortion mentioned in the previous point is also observed, due to travel

allowances provided to employees which are registered as exempt after being evidenced.

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

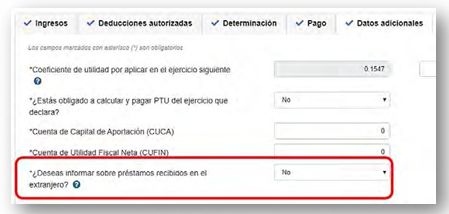

opinion of the already expressed.Additional Data – Information on loans received from abroad

Pursuant to article 76, section VI, an informational statement regarding loans granted or guaranteed by

foreign residents must be filed through Appendix 4 of the DIM during February. Nevertheless, the Tool

contains the following question: Do you wish to inform about loans received from abroad?

Income Authorized deductions Calculation Payment Additional information

Fields with star (*) are mandatory

*Profit coefficient to be applied in the following fiscal year

*Are you obliged to calculate and pay PTU in connection to the fiscal No

year stated?

*Capital Contributions Account (CUCA)

*Net Tax Profit Account (CUFIN)

*Do you wish to inform about loans received from abroad? No

IMAGE 7

In our opinion, provided that if this obligation has been fulfilled through the DIM during February, there

should be no obligation to provide this information again, especially if the question presents it as optional.

If the taxpayer wishes to provide information on the loans, new fields appear in order to capture the relevant

information, which corresponds to the information requested in Appendix 4 of the DIM:

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

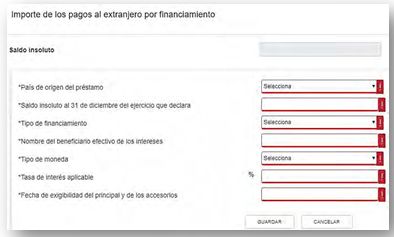

opinion of the already expressed.Amount of payments made to foreign residents due to financing

Payable balance

*Country of origin of the loan Select

*Balance to December 31 of the fiscal year stated

*Type of financing Select

*Name of beneficial owner of the interest

*Currency

*Appliable interest rate %

*Maturity date of principal and incidental amounts

SAVE CANCEL

IMAGE 8

Shortly

As mentioned before, the incorporation of this new platform to file annual statements implies both a

complexity derived from its newness and also certain aspects generated by the parameters that have been

preestablished at its creation.

There are further observations, such as the income to taxpayers located at the norther border zone in

connection to the income for interim payments and the annual income, the profit coefficient for

partnerships as advanced payments or yielding to partners are not being considered, as well as in the case

of a loss, the system does not enable negative amounts and shows zero, thus the aspects discussed

hereinabove are not the only aspects to be considered.

Undoubtedly, it is recommendable perform a review and detailed match between preloaded information

and the information contained in the accounting records of taxpayers.

We will follow-up this situation in order to be updated in regard to the declarations of tax authorities and

possible adjustments to the inconsistencies detected in the Tool. In any case, our professionals will be at

your service to clarify any doubt you may have.

© 2020 Andersen Tax & Legal, México. All rights reserved.

This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a

professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information

expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different

opinion of the already expressed.Contacts: Jose Luis Montes Muñoz Cano Country Managing Director jose.montes@AndersenTaxLegal.mx Eduardo Arizmendi Managing Director CDMX eduardo.arizmendi@andersentaxlegal.mx Marco Antonio Ruiz Managing Director Guadalajara marco.ruiz@andersentaxlegal.mx © 2020 Andersen Tax & Legal, México. All rights reserved. This newsletter has been prepared with the intention to provide general comments about the application of legal and tax norms. This document should not be considered at any time a professional advice and/or definite opinion about the specific case. Andersen Tax & Legal is not responsible for the incorrect interpretation or misuse that could be given to the information expressed in this document. Also, we do not take any responsibility for changes in the legislation and/or normativity after the issuance of this document and that could result in a different opinion of the already expressed.

You can also read