REPORT GERMANY MARKET - INDUSTRIAL AND LOGISTICS MARKETS OVERVIEW - COLLIERS INTERNATIONAL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GERMANY MARKET REPORT INDUSTRIAL AND LOGISTICS MARKETS OVERVIEW 2019 / 2020

NO LAND IN SIGHT

Fueled by ongoing high demand on the Suitable land sites for new-build con-

German commercial real estate invest- struction are a rare find in Germany’s

ment market and the low interest rate en- core markets and are likely to remain

vironment, industrial and logistics assets scarce going forward.

continued to perform very well in 2019,

once again ranking as the third strongest As a result, developers are looking to snap

asset class in Germany after office and up sites as quickly as possible and turning

retail. Investors poured a total of €6.6bn to speculative development and renova-

into German industrial and logistics as- tion of stock industrial sites. Companies

Peter Kunz FRICS sets over the course year. Although this and property developers are also becom-

HEAD OF INDUSTRIAL marks a yoy decrease, the drop can be ing more flexible when it comes to their

& LOGISTICS EMEA contributed to the current scarcity of search criteria, which puts other logistics

peter.kunz@colliers.com product. Foreign investors again showed regions where supply is more extensive

their enthusiasm for German logistics as- and affordable in the running.

sets, generating roughly 60% of annual

transaction volume. The largest logistics Demand for logistics assets will remain

deal of the year, the Maximus portfolio, in- high thanks the continued stability of the

volved a foreign investor. Singapore’s German economy and ongoing e-com-

sovereign wealth fund (GIC) acquired the merce boom. With land and construction

28-asset pan-European portfolio at the costs on the rise, property developers will

end of the year. German investors contin- need to secure suitable land at an early

ued to target their investment at light in- stage in order to fill their project pipeline.

dustrial properties in 2019, with the asset The smaller logistics regions around Ger-

class accounting for about one third of many’s secondary and tertiary cities in

their total transaction volume. the greater vicinity of the country’s major

logistics regions will also benefit from the

Despite the fact that investment activity current market situation and see growing

remains high, we are still seeing a short- demand going forward.

age of first-rate core assets. With land

hard to come by in Germany’s 8 major in-

dustrial and logistics markets, new-build

development activity is likely to remain

subdued, putting a cap on additional sup-

ply. This trend was particularly evident in

2019 take-up results, which were down

18% yoy in the country’s top 8 regions.

Berlin (+12%), Munich (+13%) and Leipzig

(+1%) were the only markets to post yoy

increases in take-up. Other markets such

as Hamburg (– 31%), Düsseldorf (– 31%)

and Stuttgart (– 43%) experienced steep

drops due to a lack of large-scale leases.

3

CONTENTS

Industrial and Logistics Markets Overview | Colliers International

CONTENTS | 2019 / 2020

Logistics in Germany 4

Logistics Regions in Germany 5

Market Data 6

Leasing Market

Germany 8

Berlin / Brandenburg 11

Düsseldorf 14

Frankfurt/Rhine-Main 17

Hamburg 20

Cologne 23

Leipzig 26

Munich 29

Stuttgart 32

Investment 35

Glossary 38

Contacts /Locations 39

4

Industrial and Logistics Markets Overview | Colliers International

Logistics in Germany | 2019 / 2020

LOGISTICS IN GERMANY

Germany is one of the most attractive demand for logistics space. As a result,

logistics markets worldwide thanks to its developers and tenants are being forced

central location in Europe, excellent to turn to the peripheral areas surround-

infrastructure, high technological stand- ing major conurbations.

ards and excellent building quality. Logis-

tics is Germany’s third-largest economic Germany’s ongoing economic growth and

sector after the automotive industry high consumer activity will continue to

and retail. The market recorded roughly boost demand for suitable logistics space.

€279bn in transaction volume in 2019. Investors remain under considerable

Logistics properties have also become pressure to invest and are showing in-

the third strongest-performing asset creasing interest in logistics assets in the

class on the German real estate invest- current low interest rate environment.

ment market. The logistics sector The smaller logistics regions will benefit

employs just over 3 million people but, from shortage of space combined with

despite favorable performance, still fac- rising land and construction costs in the

es significant challenges. country’s top markets going forward as

they enjoy comparatively moderate price

Limited supply and a lack of skilled work- levels and offer more opportunities for

ers are putting the brakes on the sector’s company expansion.

growth. Companies on the lookout for

space are increasingly taking the availa-

bility of labor and local business tax

policies into consideration in their deci-

sions. Megatrends like e-commerce and

same-day delivery are boosting demand

for suitable core products in conurba-

tions. Despite the fact that new-build

construction activity is on the rise, it will

not be enough to meet the anticipated

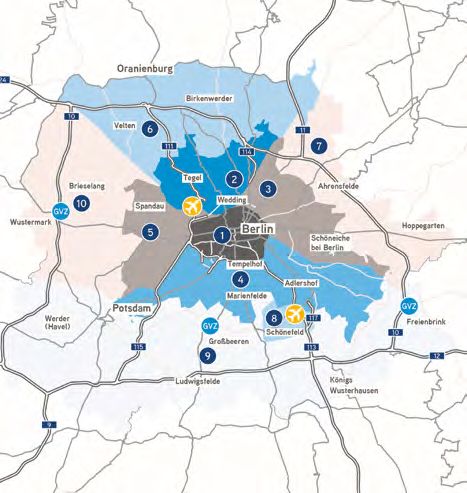

LOGISTICS REGIONS IN GERMANY 5

Industrial and Logistics Markets Overview | Colliers International

Logistics regions in Germany | 2019 / 2020

23 21

Rostock

20

19

Hamburg

Bremerhaven

6.30

28

Bremen 4.95

24

39 300

11

4.70 27

3.60

Berlin

60

Hanover Wolfsburg

1 6.10

Braunschweig

4.70 30 2

5.10 5.10

5.50 31 Osnabrück Magdeburg 13

4.15 4.20 220

4.30 Münster 395

43 100 95 14

110 15

33

Dortmund

Duisburg

38 Leipzig

Mönchen- 52 Düsseldorf Kassel / Bad Hersfeld

gladbach 4.60

Dresden

5.75

4.50 Erfurt 3.70 72

4.50

Cologne 4.75

49

45 3.70 4

80

17

4.30

6.50

3.60 5.80 220

75

Gießen485 5.40

3.10

Zwickau

80 4.50

60 Prime rent in € / sqm/month

4.20 330

180

71 ∅ rent in €/sqm/month

66 9

60

48

5.40 3.50 Frankfurt 73

Land price in €/sqm

4.50 75 70

Trier Aschaffenburg D E F I N I T IO N

160 67 Würzburg

3 93 Prime headline rents for logistics

63

Mannheim Nuremberg

and distribution space:

> 3.000 sqm Class-A properties

( > 10 m under beam height, 2–3 docking

Saarbrücken 62

65 5.00

gates/1.000 sqm, sprinkler system, share

6 of office space < 10 %) in a prime location

Regensburg

4.35 Karlsruhe 4.50 Average rents for logistics

7 and distribution space:

3.30 230

5.70 8

Stuttgart > 3.000 sqm with multifunctional usage

92 ( > 7 m under beam height, 1–2 docking

85

4.80

Ingolstadt gates / 1.000 sqm, limited share of office

6.50 space) in a traffic-favorable location

200 Ulm / Neu-Ulm

81

5.20 Land price:

94 Undeveloped commercial/industrial areas,

4.75

5 300 Munich ( > 20.000 sqm, mainly flat and rectangular,

no / limited usage restrictions)

3.90

7.15 Status January 2020

130 95

96 6.70

Airport

Augsburg 400

Freight transport centre

5.70

Harbour

4.50

125

6

Industrial and Logistics Markets Overview | Colliers International

Market Data | 2019 / 2020

MARKET DATA

Location Information

Germany Berlin Düsseldorf Frankfurt Hamburg Cologne Leipzig Munich Stuttgart

Population in 1.000 83,019 3,645 619 753 1,841 1,086 588 1,472 635

Employees Paying Social Security 33,407 1,528 424 602 996 583 273 897 426

Contributions in 1.000

Unemployment Rate in % 4.9 7.6 6.5 4.9 5.9 7.4 6.1 3.4 3.9

Per Capita Disposable Income in € 24,000 22,220 28,742 27,138 25,720 25,806 21,545 30,478 27,314

Sources: Federal Statistical Office, Land Statistical Offices, Federal Employment Agency, Nexiga GmbH

Industrial & Logistics Leasing

TOP 8 Berlin / Düsseldorf Frankfurt / Hamburg Cologne Leipzig Munich Stuttgart

Brandenburg Rhine-Main

Take-up 2019 in sqm 2,429,900 474,900 217,900 467,200 332,500 192,300 346,700 227,000 171,400

Change year-on-year in % – 18% 12% – 31% – 28% – 31% – 22% 1% 13% – 43%

Leasing performance 2019 in sqm 1,931,600 451,800 117,100 414,400 268,300 181,000 166,000 202,500 130,500

Change year-on-year in % – 24% 40% – 60% – 26% – 32% – 23% – 40% 1% – 49%

Forecast for 2020

Number of Deals 620 151 70 72 70 47 32 95 83

Average Area Size in sqm 4,730 3,145 3,112 6,580 4,750 3,738 11,005 2,389 3,117

Strongest Branch

Prime Rent in € / sqm / month 6.10 5.75 6.50 6.30 5.80 4.60 7.15 6.50

Forecast for 2020

Average Rent in € / sqm / month 5.10 4.75 5.40 5.00 4.50 3.70 6.70 5.20

Forecast for 2020

Trade Production & Manufacturing Transport & Logistics

7

Industrial and Logistics Markets Overview | Colliers International

Market Data | 2019 / 2020

Industrial & Logistics Investment – TOP 8*

TOP 8 Berlin Düsseldorf Frankfurt Hamburg Cologne Leipzig Munich Stuttgart

Transaction Volume 2019 in m € 2,518 414 413 493 267 129 190 493 119

Change year-on-year in % 1% – 36% 0% – 2% 6% – 37% 692% 114% – 45%

Forecast for 2020

* Refers to the defined logistics market areas

Industrial & Logistics Investment – Germany

2014 2015 2016 2017 2018 2019

Transaction Volume 2019 in m € 3,592 3,972 4,579 8,662 6,814 6,566

Change year-on-year in % 57 11 15 89 – 21 –4

Industrial Properties Share in % 27 32 31 12 42 28

Logistics Properties Share in % 73 68 69 88 58 72

Share in the Commercial 9 7 9 15 11 9

Real Estate Market in %

Share by International Investors in % 62 53 38 65 47 60

Portfolio Transactions in % 50 47 40 71 56 40

Largest Buyer Group in % Open-ended Opportunity Asset Open-ended Asset Asset

real estate funds / managers / real estate managers / managers /

funds / Private Fund funds / Fund Fund

Special funds equity funds managers Special funds managers managers

33 22 30 33 45 40

Largest Seller Group in % Property Property Property Asset Property Asset

developers developers developers managers / developers managers /

Fund managers Fund managers

31 20 26 46 30 26

Gross Initial Yield in % for 6.40 5.97 5.50 4.65 4.50 4.20

Class-A properties

8

LEASING MARKET GERMANY

Take-up Deals of similar scale were absent in Ger-

many’s other logistics hubs. More leases

Leasing Market Germany | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Just over 2.4 million sqm was let to tenants

were recorded in 2019 than in the previous

or built/purchased by owner-occupiers in

year, however (620 in total, +9%), reflect-

Germany’s 8 largest logistics hubs in 2019.

ing the fact that demand for industrial and

That reflects a yoy drop of roughly 18% for

logistics space remains high. Smaller units

the overall market. If we exclude owner-

of under 3,000 sqm were even more

occupier activity, which puts results at

popular than in the previous year. The

1.9 million sqm, take-up was down 24%

year’s largest-scale leases were signed by

yoy. Results, however, varied from region

online furniture retailer Wayfair for

to region. The Düsseldorf (– 31%), Rhine-

90,500 sqm in Lich in the northern Rhine-

Main (– 28%), Hamburg (– 31%), Cologne

Main area, Amazon for 31,000 sqm in

(– 22%) and Stuttgart (– 43%) regions

Schönefeld south of Berlin and automotive

posted steep drops in take-up with consid-

group BMW for around 32,000 sqm in

erably less availability while Berlin (+12%),

Vaterstetten (Munich).

Munich (+13%) and Leipzig (+1%) contin-

ued to experience ongoing momentum

thanks to a number of major leases signed.

FAST FACTS TOP 8

2019 2018 Change

Take-up in sqm 2,429,900 2,968,200 – 18%

Leasing Performance in sqm 1,931,600 2,544,900 – 24%

Owner-Occupiers in % 21% 14% – 18%

Number of Deals 620 571 9%

Average Area Size in sqm 4,730 4,862 – 3%

Figure 1: Take-up in 1,000 sqm Figure 2: Take-up by Size Category in %

500 up to 500 0%

452

414 501–1,000 4%

400 1,001–3,000 16%

300 268

3,001–5,000 14%

202

200 181 181

166

130 5,001–10,000 23%

117

101

100 above 10,000 43%

53 64

41

23 25

11

0

Berlin Frankfurt Cologne Munich

Düsseldorf Hamburg Leipzig Stuttgart

Leasing Performance Owner-Occupiers

9

Supply and Demand Rents

Industrial and Logistics Markets Overview | Colliers International

Leasing Market Germany | 2019 / 2020

Although demand for industrial and logis- With a few exceptions, prime and average

tics properties remains high, the scarcity rents in top locations continued to climb

of development sites and rising land pric- due to low supply and ongoing high

es, particularly in the large-scale segment demand. Prime rents in Frankfurt am Main

of over 10,000 sqm, is putting a damper on remained stable at €6.50 per sqm. High-

take-up (– 39%). Take-up results in this priced leases signed for new-build space

segment were down in markets such as continue to boost prime rent levels yoy

Hamburg and Frankfurt, although results despite lower take-up results. Prime rents

in those markets were bolstered by de- in Munich rose 2% yoy to a current €7.15

mand for units of up to 5,000 sqm (+27%). per sqm while Berlin (€6.10 per sqm, +7%),

Property developers are also beginning to Hamburg (€6.30 per sqm, +5%) and

focus their activities on locations outside Cologne (€5.80 per sqm, +5%) saw even

Germany’s 8 top markets, as these offer more significant increases.

more attractive prices and greater availa-

bility of land. Pre-leasing rates are quite

high in the top 8 markets, a factor that

continues to encourage speculative devel-

opment. More and more developers are

also looking into brownfield development

as a way to bring space to market.

Figure 3: Take-up by Branch Share in % Figure 4: Prime Rents in the TOP 8 in € / sqm

8

Others 18%

Logistics Service 7

Providers 28%

Production &

Manufacturing

Companies 28% 6

Trading

Companies 26% 5

4

2015 2016 2017 2018 2019

Berlin Düsseldorf Frankfurt Hamburg

Cologne Leipzig Munich Stuttgart

10

Summary and Outlook

Leasing Market Germany | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

In view of the current uncertainties around

automotive production and the ongoing

scarcity of development sites in Germany’s

top 8 regions combined with growing

demand for city logistics driven by the on-

going boom in e-commerce, 2020 is likely

to be another average year on Germany’s

top 8 industrial and logistics real estate

markets. Based on these general condi-

tions, we can expect brownfield sites to

become increasingly popular in prime

locations. At the same time, a number of

companies flexible enough to do so are

likely to turn to nearby markets that boast

greater availability. Such markets include

centrally located regions with good infra-

structure such as Kassel/Bad Hersfeld,

the eastern Ruhr region (especially Dort-

mund), Hanover, the Rhine-Neckar region

and cities such as Augsburg in southern

Germany.

Figure 5: Average Rents in the TOP 8 in € / sqm

7

6

5

4

3

2015 2016 2017 2018 2019

Berlin Düsseldorf Frankfurt Hamburg

Cologne Leipzig Munich StuttgartBERLIN / BRANDENBURG 11

Industrial and Logistics Markets Overview | Colliers International

Berlin / Brandenburg | 2019 / 2020

FAST FACTS

2019 2018 Change

Take-up in sqm 474,900 422,500 12%

Leasing Performance in sqm 451,800 322,300 40%

Number of Deals 151 102 48%

Prime Rent* in €/sqm/month 6.10 5.70 7%

Average Rent in €/sqm/month 5.10 5.00 2%

*achievable top rent in new buildings

Take-up according to Location

Submarket Take-up in sqm Share

1 Center 15,100 3%

2 City North 39,800 8%

3 City East 35,200 8%

4 City South 73,000 15%

5 City West 25,600 6%

6 Periphery North 45,300 10%

7 Periphery East 14,200 3%

8 Airport Area BER 20,300 3%

9 Periphery South 164,000 35%

10 Periphery West 42,400 9%

Total 474,900 10012

LEASING

Berlin / Brandenburg | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Take-up Supply and Demand

The Berlin industrial and logistics market While leases signed for units of over

registered total take-up of roughly 10,000 sqm accounted for around 50% of

474,900 sqm, up 12% yoy and exceeding take-up in the previous year, the share

2015’s record result of 451,400 sqm. claimed by this segment dropped by

Take-up results excluding owner-occupi- almost half in 2019 (122,400 sqm, or

ers were particularly strong. 145 leases 26%). The Amazon deal was the only one

were signed for a total of 451,800 sqm to exceed the 20,000 sqm mark compared

in 2019, reflecting a significant 40% yoy to five such deals recorded in the segment

increase and marking a new record result. in 2018. With the availability of units of

Markets such as Stuttgart (– 43%), this size continuing to drop and develop-

Frankfurt (– 28%) and Hamburg (– 31%) ment potential already exhausted in some

experienced a sharp downward trend in hot spots, we do not expect the situation

annual take-up in contrast, putting Berlin to relax any time soon. Small-scale units

and the Leipzig region at the fore of (up to 3,000 sqm), however, recorded an

Germany’s logistics hubs. Notable deals increase in take-up compared to the pre-

included leases signed by Amazon for vious year. A total of 99 leases were

roughly 31,000 sqm in Schönefeld and signed in this segment, reflecting a mar-

Microvast for around 16,000 sqm in ket share of 28% (around 130,700 sqm).

Ludwigsfelde as well as Kühne & Nagel’s As such, the segment accounted for

lease of 15,500 sqm in Oberkrämer near around two thirds of all leases signed in

Oranienburg. 2019.

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

500 474.9

451.4 up to 500 1,000 0%

424.8 422.5

501 – 1,000 27,900 6%

400

352.7 1,001 – 3,000 101,800 21%

3,001 – 5,000 94,600 20%

300

5,001 – 10,000 127,200 27%

above 10,000 122,400 26%

200

Total 474,900 100%

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201913

In terms of tenant breakdown, retailers Outlook

contributed slightly less to overall take-up

Industrial and Logistics Markets Overview | Colliers International

Berlin / Brandenburg | 2019 / 2020

Fresh supply will be hitting the market in

in 2019, a result that can be attributed to

2020 thanks to a number of ongoing prop-

the lack of high-volume deals in the pe-

erty developments in the periphery.

riphery. Retailers accounted for a total of

However, the supply bottleneck in the

142,500 sqm in take-up, down 30% yoy.

municipal area may push prices up even

This decrease, however, is mainly the

further and prevent them from leveling

result of the limited availability of units

off. Demand for small-scale light industri-

over 10,000 sqm as demand in the region

al space is also going to pick up in 2020

remains high.

with prices increasing as a result as prac-

tically no space is currently available for

Rents immediate tenancy. In light of the current

supply situation, we expect 2020 take-up

Ongoing high demand is also evident in

to reach levels similar to those recorded

the current rent trend. No other region

in the previous year.

has seen a comparable increase in prime

rents in the past two years. Some of the

logistics space over 3,000 sqm in the

municipal area is currently going for

€6.90 per sqm. And, as availability within

city limits grows increasingly scarce, we

could see prime rents continue to rise.

On the overall market (including the

periphery), prime rents currently come

to €6.10 per sqm, up 40 cents yoy.

Average rents rose by 10 cents to €5.10

per sqm at year-end 2019.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

Production & Manufacturing 7

Companies 23%

6.10

6 5.70

Logistics Service

Providers 28%

5.00 5.00 5.00

Trading 5

5.10

5.00

Companies 31%

4.50

4 4.25

Others 18%

4.00

3

2015 2016 2017 2018 2019

Prime Rent Average Rent14

Industrial and Logistics Markets Overview | Colliers International

Düsseldorf | 2019 / 2020

DÜSSELDORF

FAST FACTS

2019 2018 Change

Take-up in sqm 217,900 317,600 – 31%

Leasing Performance in sqm 117,100 295,600 – 60%

Number of Deals 70 66 6%

Prime Rent* in €/sqm/month 5.75 5.75 0%

Average Rent in €/sqm/month 4.75 4.75 0%

*achievable top rent in new buildings

40

Mühlheim

40

Take-up according to Location

57

59

an der Ruhr

Submarket Take-up in sqm Share

1 Düsseldorf 40,000 21%

5 524

Krefeld 44 2 Neuss 15,700 22%

Meerbusch

7 3 Kaarst 1,200 1%

44

6

Ratingen

4 Willich 0 8%

Willich

52

4

Viersen

Mettmann

5 Krefeld 16,900 20%

52 1

Düsseldorf 6 Meerbusch 0 0%

3 8

Mönchengladbach Kaarst Erkrath

13 Neuss 7 Ratingen 13,000 12%

Korschenbroich

46

14

2

Hilden 8 Erkrath 500 0%

9

9 Hilden 10,800 0%

61 59

11 10 10 Langenfeld 5,000 3%

540 Dormagen

12 Langenfeld

46

Rheinland 11 Dormagen 53,900 9%

Grevenbroich

57 12 Grevenbroich 15,100 3%

Leverkusen 13 Korschenbroich 0 0%

3

44

14 Mönchengladbach 45,800 1%

61

1 Total 217,900 100%15

LEASING

Industrial and Logistics Markets Overview | Colliers International

Düsseldorf | 2019 / 2020

Take-up continues to dwindle along with the

amount of available space able to meet

The Düsseldorf industrial and logistics

modern standards in terms of equipment,

market recorded 217,900 sqm in take-up in

location and size.

2019, around 100,000 sqm less than in the

previous year (– 31%). Annual results came

in well below expectations (– 36%) com- Supply and Demand

pared to the 5-year average (342,500 sqm).

Take-up of units ranging from 5,001 sqm

The bottleneck in the region becomes

to 10,000 sqm saw the steepest drop,

particularly obvious if we look at take-up

down yoy from 24% to 9%. Units featuring

excluding owner-occupiers, with only

less than 5,000 sqm accounted for rough-

117,100 sqm taken up by tenants in 2019.

ly 40% of total take-up (about 87,500 sqm,

This reflects a yoy decrease of 60%.

+41%). This increase shows that the

Only 4 deals were signed for units over

Düsseldorf market continues to be

10,000 sqm compared to more than twice

characterized by exceptionally high de-

as many in 2018. The largest deals posted

mand combined with limited availability,

in 2019 included the Hoyer GmbH owner-

particularly in prime locations. That

occupier development in Dormagen

means there is a very good chance that

encompassing roughly 50,000 sqm of

any space to come available will be

new-build space and the ABC-Logistik

quickly absorbed by the market. The trend

development on a brownfield site near the

towards speculative property develop-

Port of Düsseldorf (around 11,600 sqm

ment also reflects current excess de-

hall space). Demand for units starting at

mand. Supply in the large-scale segment

5,000 sqm remains high, driven by the

is not sufficient to meet that demand due

prevailing tenant structure. However, the

to a lack of space available for immediate

supply of suitable development sites

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

500 up to 500 4,400 2%

435.7

501 – 1,000 15,000 7%

400

346.7 343.8 1,001 – 3,000 40,100 18%

317.6

3,001 – 5,000 28,000 13%

300

5,001 – 10,000 19,500 9%

217.9

above 10,000 110,900 51%

200

Total 217,900 100%

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201916

tenancy at stock properties, which means Outlook

demand is primarily being met with

Düsseldorf | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

The lack of development sites is currently

new-build developments. However, land

being further exacerbated by the city’s

sites zoned for new-builds in prime

high requirements on companies in terms

locations are in limited supply, which is

of jobs, taxes and volume. Companies and

increasing tenant willingness to turn to

property developers are therefore likely to

peripheral locations within the region.

intensify their interest in locations out-

The high pre-leasing rate at new-build

side currently coveted submarkets such

developments is also an indication

as Neuss, Krefeld and Mönchengladbach.

that there just is not enough space

Chances are also good that companies

available on the market at the moment

will continue to build their own logistics

to adequately meet demand.

properties in light of the new-build supply

bottleneck in the Düsseldorf core area.

Rents

Prime and average rents are currently

stable with no significant increases likely

despite excess demand. We can also ex-

pect prime rents for units over 3,000 sqm

to remain stable over the course of the

year. We may see an increase in prices

for modern space (light industrial)

at business parks within city limits, as

companies are willing to pay more for

location and equipment in some cases.

Prime rents for this quality of space

within city limits currently come to €7.00

per sqm.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

6 5.75 5.75

Production & Manufacturing

Companies 23%

5.40 5.40 5.40

Trading

Companies 18% 5

Logistics Service 4.75 4.75

Providers 33% 4.50 4.50 4.50

4

Others 26%

3

2015 2016 2017 2018 2019

Prime Rent Average RentFRANKFURT/ RHINE-MAIN 17

Industrial and Logistics Markets Overview | Colliers International

FRANKFURT / RHINE-MAIN | 2019 / 2020

FAST FACTS

2019 2018 Change

Take-up in sqm 467,200 650,200 – 28%

Leasing Performance in sqm 414,400 563,600 – 26%

Number of Deals 72 83 – 13%

Prime Rent* in €/sqm/month 6.50 6.50 0%

Average Rent in €/sqm/month 5.40 5.20 4%

*achievable top rent in new buildings

Take-up according to Location

Submarket Take-up in sqm Share

480 Lauterbach

(Hessen)

Gießen

Fulda

1 Frankfurt am Main 25,200 5%

Wetzlar

485 8

5

7

2 Offenbach 15,500 3%

Butzbach 3 Darmstadt 27,100 6%

Limburg an der Lahn

Friedberg

(Hessen) 9

66 4 Groß-Gerau 131,300 28%

7 5 Mainz + Wiesbaden 27,400 6%

Bad Homburg

45

10

vor der Höhe

Gelnhausen

6 Main-Taunus-District 20,800 5%

Frankfurt

Hofheim am Taunus am Main Hanau 7 Hochtaunus-District 5,000 1%

Wiesbaden 1 Offenbach am Main

66 6 66

8 Gießen 117,200 25%

671 661 2 11

5 Dietzenbach

Mainz 9 Wetteraukreis 4,600 1%

Karlstadt

Ingelheim am Rhein 4 Aschaffenburg

Groß-Gerau 3

Darmstadt 10 Main-Kinzig-District 85,800 18%

67

3

63 11 Aschaffenburg 7,300 2%

Gernsheim

Alzey

Total 467,200 100%

Miltenberg

61 Heppenheim

(Bergstraße) Erbach 8118

LEASING

FRANKFURT / RHINE-MAIN | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Take-up Supply and Demand

The Frankfurt industrial and logistics Leases signed for over 10,000 sqm once

market generated 467,200 sqm in total again contributed the lion’s share to total

take-up in 2019, reflecting the weakest results, generating more than half of total

result ever recorded and coming in take-up (59%, or 278,900 sqm). However,

around 24% shy of the 5-year average this reflects a significant drop from the

(619,000 sqm). This drop in take-up previous year’s 75%, or 488,100 sqm.

can be primarily attributed to a lack of Although demand for units of over

large-scale transactions in the space 10,000 sqm remains stable, the supply

segment of over 20,000 sqm and to of developable sites is dwindling and

the increasing shortage of logistics increasingly less space in this segment is

development sites, which tend to involve being added to the market or becoming

long lead times. available for immediate tenancy. As such,

more and more companies are turning to

The most notable transactions recorded peripheral locations in the Rhine-Main

in the region in 2019 include the leases region, including Gießen, Mainz and

signed by online furniture retailer Wayfair Aschaffenburg, and are expanding their

for 90,500 sqm in the Lich submarket of search radius to the edges of the Frank-

Gießen, logistics service provider Zufall furt core area. Several property develop-

for 35,000 sqm in Flieden in the Main- ments are in planning for the new year

Kinzig-Kreis district and Geis Industrie- or are already under construction, and

Service GmbH in Rodenbach (32,000 sqm) we can expect these developments to

as well as two new-build developments in address the continued shortage of space

Gernsheim for Amazon (20,000 sqm) and to some extent. Current developments

Sonepar (26,000 sqm). include the Hillwood and Nvelop business

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

800 up to 500 2,500 1%

720.2

700 650.2 501 – 1,000 8,800 2%

584.0

600 1,001 – 3,000 32,800 7%

463.0 467.2 3,001 – 5,000 36,700 8%

500

5,001 – 10,000 107,500 23%

400

above 10,000 278,900 59%

300

Total 467,200 100%

200

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201919

park development in Erlensee, which will Outlook

comprise 4 construction phases encom-

Industrial and Logistics Markets Overview | Colliers International

FRANKFURT / RHINE-MAIN | 2019 / 2020

New space will be added to the market in

passing a total area of 60,000 sqm. Start

2020 thanks to several property develop-

of construction on phase 1 is scheduled

ments currently underway. Demand is

for spring 2020.

set to remain stable and we can expect

several major deals to be signed over the

Rents course of the year. We can also look for

the trend towards shorter lease terms

The excess demand we are currently

to continue in 2020, as a number of ten-

seeing on the market is pushing up prices

ants signed leases with terms of under

for stock space, in some cases to rent

5 years in 2019.

levels typically paid for new-build proper-

ties. Average rents experienced another

increase as a result to a current €5.40

per sqm with prime rents stable at €6.50

per sqm in the core locations around

Frankfurt Airport. That puts Frankfurt and

Stuttgart (€6.50 per sqm) in second place

following Munich (€7.15 per sqm) in a

national comparison.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

7

Production & Manufacturing

Companies 13% 6.50 6.50

6.40

6.30 6.30

Logistics Service

Providers 28% 6

Trading

Companies 48%

5.40

5 5.20 5.20 5.20

5.10

Others 11%

4

2015 2016 2017 2018 2019

Prime Rent Average Rent20

Industrial and Logistics Markets Overview | Colliers International

Hamburg | 2019 / 2020

HAMBURG

FAST FACTS

2019 2018 %

Take-up in sqm 332,500 484,600 – 31%

Leasing Performance in sqm 268,300 393,400 – 32%

Number of Deals 70 78 – 10%

Prime Rent* in €/sqm/month 6.30 6.00 5%

Average Rent in €/sqm/month 5.00 4.85 3%

*achievable top rent in new buildings

23 Quickborn Bargteheide 21

Take-up according to Location

7 Norderstedt Submarket Take-up in sqm Share

Tornesch

6 Tangstedt Ahrensburg

1 City West 12,200 4%

Langenhorn

Pinneberg 7

Ellerbek Schnelsen

Rellingen

2 City North-West 4,800 1%

2 3 Siek

Halstenbek

Niendorf Ohlsdorf 3 City North-East 6,300 2%

Rahlstedt Braak

Schenefeld Eidelstedt Stapelfeld

Wedel

Lurup

4 City East 52,000 16%

Stellingen

Rissen Barmbek Barsbüttel Witzhave

1

24

5 City South 124,000 37%

Glinde

Hamburg

Billbrook

Oststeinbek 6 Periphery North-West 25,700 8%

Waltershof Steinwerder 8 Aumühle

Moorfleet

GVZ

Willhelmsburg

255

25

7 Periphery North-East 69,400 21%

Billwerder

Moorburg

5

Buxtehude

253 Allermöhe

8 Periphery East 26,600 8%

Hausbruch Harburg

Neu Wulmstorf 4

9 Periphery South-East 5,900 2%

1 Geesthacht

261 10 Periphery South-West 5,600 1%

10

Hittfeld

Total 332,500 100%

Stelle 9 Winsen (Luhe)

Hollenstedt 39

Wenzendorf

7

Buchholz in

der Nordheide21

LEASING

Industrial and Logistics Markets Overview | Colliers International

Hamburg | 2019 / 2020

Take-up of construction on Wiska headquarters in

Kaltenkirchen in northern Hamburg was

Hamburg’s industrial and logistics real

one of the few owner-occupier deals to

estate market closed out 2019 with total

have a significant impact on the market.

take-up of 332,500 sqm, the weakest

The first construction phase (around

result posted in the past seven years.

10,000 sqm) will primarily focus on the

Although tenant and owner-occupier

logistics and production areas. The

activity have generated take-up results

facility is scheduled to be up and running

of over 450,000 sqm in the past several

by early 2021.

years, even posting more than

668,800 sqm in 2016, 2019’s year-end

result came in at just half. This considera- Supply and Demand

ble drop in take-up can primarily be

The Hamburg market is currently unable

attributed to the absence of large-scale

to meet demand due to a current lack of

deals signed for over 10,000 sqm.

space suitable for large-scale logistics

Although units of this size accounted for

development. Industrial and logistics

almost 60% of total take-up in the previ-

space is particularly hard to come by in

ous year, 2019 results put their share

the logistics hotspots located in the south

at just one third (roughly 109,100 sqm).

of the city as well as in the commercial

Large-scale leases recorded in 2019

district of Billbrook to the east. The num-

include those signed by logistics service

ber of new-builds available for immediate

provider ULD United Logistics & Distribu-

tenancy dropped drastically in 2019. As a

tion for around 30,000 sqm on Dradenau

result, companies will have to wait for

straße in Waltershof (port area) and by

property developments to be completed

Nutwork for almost 12,000 sqm of logis-

or stock space to come available. Only a

tics space in Völlhöfner Weiden. The start

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

800 up to 500 0 0%

700 668,8 501 – 1,000 1,600 0%

593,4

600 1,001 – 3,000 49,900 15%

484,6 3,001 – 5,000 69,400 21%

500 460,9

5,001 – 10,000 102,500 31%

400 332,5

above 10,000 109,100 33%

300

Total 332,500 100%

200

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201922

handful of new-build developments are Outlook

scheduled for completion in the foreseea-

Hamburg | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Demand is set to remain high in 2020 with

ble future. The Mach 2 speculative

competition for available units intensify-

development in Hamburg-Wilhelmsburg

ing as a result. Large-scale leases are

is expected to add space to the market

again on the horizon with the listing of the

in the coming 12 months. Developer

Mach 2 development, which is scheduled

Fourparx and investor AEW Europe are

for completion in August 2021. However,

planning to build a new type of logistics

2020 take-up results are unlikely to match

property with two levels and a total of

the average of the past 5 years (around

over 100,000 sqm of modern hall space.

531,500 sqm).

Rents

Rent trends reflect the tense relationship

between supply and demand that current-

ly dominates the market with prime and

average rents posting another yoy in-

crease in 2019. Prime rent for modern

logistics space of over 3,000 sqm came

to €6.30 per sqm at year-end, up consid-

erably by 30 cents yoy. That puts Ham-

burg along with Berlin among the markets

to post the highest rent increases last

year.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

7

Production & Manufacturing

Companies 14%

6.30

6.00

Trading 5.80 5.80 5.80

Companies 28% 6

Logistics Service

Providers 51%

5

5.00

Others 7% 4.85 4.85

4.75

4.60

4

2015 2016 2017 2018 2019

Prime Rent Average RentCOLOGNE 23

Industrial and Logistics Markets Overview | Colliers International

Cologne | 2019 / 2020

FAST FACTS

2019 2018 Change

Take-up in sqm 192,300 248,100 – 22%

Leasing Performance in sqm 181,000 236,100 – 23%

Number of Deals 47 37 27%

Prime Rent* in €/sqm/month 5.80 5.50 5%

Average Rent in €/sqm/month 4.50 4.50 0%

*achievable top rent in new buildings

46 Take-up according to Location

Submarket Take-up in sqm Share

46

59

540

57

1 Cologne 36,800 19%

542

3 2 Leverkusen 0 0%

2

3 Bergisch Gladbach 0 0%

44

15

12 Leverkusen 4 Rösrath 0 0%

Bedburg Pulheim Bergisch

61

Gladbach 5 Airport Area Cologne/Bonn 0 0%

14 3

Bergheim

1 6 Troisdorf 34,100 18%

1 4

Köln 7 Niederkassel 0 0%

11

Frechen 559

4 8 Wesseling 1,000 1%

4

Rösrath

13 Kerpen

10

GVZ 9 Brühl 0 0%

Hürth

Flughafen Köln/Bonn

555

10 Hürth 0 0%

Brühl 5

Düren

9 8 Niederkassel

6

11 Frechen 17,100 9%

535 Wesseling 7 Troisdorf

12 Pulheim 27,600 14%

560

13 Kerpen 46,400 24%

59

14 Bergheim 11,300 6%

Bonn

61

562 3 15 Bedburg 18,000 9%

Euskirchen 565 Total 192,300 100%24

LEASING

Cologne | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Take-up signed by logistics service provider Log-

win (17,000 sqm) in Kerpen, the expansion

Cologne’s industrial and logistics real

of industrial company Gerflor involving

estate market finished out 2019 with total

just under 9,000 sqm in Troisdorf and

take-up (including owner-occupiers) of

completion of the renovation of Cologne’s

192,300 sqm, down 22% yoy (2018:

theaters (roughly 8,100 sqm).

248,100 sqm). The market was also una-

ble to match the previous year’s result

excluding owner-occupiers (– 23%). Supply and Demand

Similar to Germany’s other top 8 industri-

New-build activity in Cologne was quite

al and logistics markets, this drop in

solid compared to Germany’s other mar-

take-up can be primarily attributed to the

kets. A handful of speculative new-build

absence of large-scale leases. This trend

developments are currently underway in

can also be seen in the number of deals

the city’s sought-after locations, includ-

signed. Although more leases were

ing construction of LogPlaza Frechen en-

signed in 2019 than in the previous year

compassing 18,000 sqm of new-build

(+27%), many of them involved small and

space west of the Rhine River. These

medium-sized units. Leases signed for

developments will boost supply in the city

between 5,001 – 10,000 sqm accounted for

as we continue into the new year. As

almost one third of total take-up, twice as

such, leases signed for new-build space

much as in 2018. Units of over 10,000 sqm

as well as pre-leasing activity also ac-

also generated roughly one third of total

counted for roughly 50% of take-up in

take-up (60,200 sqm). The share claimed

2019. Developers continue to focus on

by this segment, however, was considera-

speculative projects as demand for indus-

bly higher in the previous year at 44%

trial and logistics space remains high and

(2018: 108,200 sqm). The largest-scale

tenants looking for units over 5,000 sqm

leases of the year included the lease

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

300 up to 500 400 0%

248,1 501 – 1,000 7,600 4%

250

1,001 – 3,000 41,600 22%

199,4 198,2 192,3

200 3,001 – 5,000 20,400 11%

167,4

5,001 – 10,000 62,100 32%

150

above 10,000 60,200 31%

100 Total 192,300 100%

50

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201925

are still coming up short-handed. Kerpen Outlook

recorded the highest demand in 2019 with

Industrial and Logistics Markets Overview | Colliers International

Cologne | 2019 / 2020

In light of upcoming property develop-

take-up at 46,400 sqm, up 30% yoy,

ments planned in the Cologne periphery

thanks in part to the large-scale lease

and current land reserves, we expect

signed by Logwin mentioned above. The

tension on the market to ease slightly in

Pulheim submarket managed to double

terms of units starting at 5,000 sqm.

its take-up results yoy with roughly

As such, we may see 2020 take-up

27,600 sqm. Take-up within Cologne city

results not only match previous-year

limits came to around 36,800 sqm. Al-

levels but even exceed them.

though this reflects a yoy increase of 23%,

these results are significantly down from

2016 (77,700 sqm) and 2017 (97,100 sqm).

The Prologis and Alcaro developments

in Cologne-Niehl and Cologne-Kalk could

potentially increase the supply of space

within Cologne city limits.

Rents

Rents continued to rise over the course of

the year due to ongoing limited availability

and high construction costs, with modern

logistics space currently going for €5.80

per sqm in some cases. These prices,

however, are only being paid in locations

west of the Rhine within Cologne city

limits. Following the increase recorded in

Q4 2018, average rents remained stable at

€4.50 per sqm.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

6 5.80

Trading

Companies 16% 5.50

Production & 5.20 5.20

Manufacturing 5.00

Companies 20% 5

Logistics Service

Providers 32%

4.50 4.50

4 4.20 4.20

Others 32% 4.00

3

2015 2016 2017 2018 2019

Prime Rent Average Rent26

Industrial and Logistics Markets Overview | Colliers International

Leipzig | 2019 / 2020

LEIPZIG

FAST FACTS

2019 2018 Change

Take-up in sqm 346,700 343,700 1%

Leasing Performance in sqm 166,000 275,800 – 40%

Number of Deals 32 25 28%

Prime Rent* in €/sqm/month 4.60 4.60 0%

Average Rent in €/sqm/month 3.70 3.70 0%

*achievable top rent in new buildings

Magdeburg

Take-up according to Location

Submarket Take-up in sqm Share

1 Leipzig 114,600 33%

5

Dessau-Roßlau

2 District Leipzig 38,400 11%

Stadt Wittenberg

4 3 Nordsachsen 6,300 2%

6

Anhalt-Bitterfeld 4 Wittenberg 12,600 4%

9

5 Dessau-Roßlau 0 0%

14

3

Nordsachsen

6 Anhalt-Bitterfeld 116,000 33%

Halle (Saale)

7 Stadt

7 Halle (Saale) 22,600 7%

143

GVZ

Saalekreis 1 8 Saalekreis 36,200 10%

38 Leipzig

8 9

14

Total 346,700 100%

38

Landkreis Leipzig

2

7227

LEASING

Industrial and Logistics Markets Overview | Colliers International

Leipzig | 2019 / 2020

Take-up Supply and Demand

The Leipzig industrial and logistics mar- Leases signed for units of over 10,000 sqm

ket recorded total take-up of roughly accounted for roughly three quarters of

346,700 sqm in 2019, topping 2018’s re- total take-up, including the lease signed

cord results by a few thousand square by an automotive company for around

meters (2018: 343,700 sqm). This increase 23,300 sqm of new-build space at Segro

is even more impressive if we look at Logistics Park near Leipzig Airport and

long-term performance, with 2019 results the lease signed by intralogistics provider

exceeding the 5-year average by an im- Dematic for 18,000 sqm in Leipzig.

pressive 43%. This increase can in part

be attributed to several large-scale Despite the shortage of supply, particu-

owner-occupier developments, including larly for units over 5,000 sqm, there is

retailer Rossman’s project (26,000 sqm) some stock space that is still available.

in Landsberg (Saxony-Anhalt) and the These properties, however, are not up to

expansion of the site occupied by tech current standards and are therefore

manufacturer Tesvolt in Wittenberg having a difficult time finding tenants

(around 12,000 sqm). The completion of despite the high demand in the Leipzig

a paper factory in Sandersdorf-Brehna region, primarily due to high ancillary

(Anhalt-Bitterfeld district) for manufac- costs and outdated building technology.

turer Progroup AG deserves particular

mention. With a volume of over €460m, The production and manufacturing sector

the development was the largest invest- continues to be the source of highest

ment project in Saxony-Anhalt in 2019. demand in the Leipzig region, accounting

for almost 200,000 sqm, or 58% of total

take-up. Logistics service providers

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

400 up to 500 0 0%

343.7 346.7

501 – 1,000 0 0%

300 279.0 1,001 – 3,000 14,300 4%

258.0

3,001 – 5,000 9,900 3%

5,001 – 10,000 67,800 20%

200

above 10,000 254,700 73%

116.0 Total 346,700 100%

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201928

(19%) and retailers (16%) trailed at some Outlook

distance. Retailers saw take-up cut in half

Leipzig | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Availability is more important than

yoy due to the absence of leases signed by

location at the moment, as suppliers in

major retailers.

particular are currently under pressure to

find space with a set completion date.

Rents Around 100,000 sqm of speculative

logistics space is currently under con-

Prime rents (€4.60 per sqm) and average

struction, only about 10,000 sqm of

rents (€3.70 per sqm) for logistics space

which is scheduled for completion by

starting at 3,000 sqm remained stable

mid-2020. The remaining space will not

over the course of 2019. However, there is

hit the market until late 2020 or early

a chance that we may see a slight drop in

2021. As a result, companies will have to

new-build rents going forward, particu-

manage with rather limited supply in

larly in the Halle/Saale and Großkugel

2020.

area, i.e. primarily around Leipzig-Halle

Airport, as a number of property develop-

ers are currently active there within a

relatively small radius.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

5

Trading 4.60 4.60

Companies 16% 4.50 4.50

4.30

Logistics Service

Providers 19%

4

Production &

Manufacturing

Companies 58% 3.70 3.70

3.50 3.50

3 3.20

Others 7%

2

2015 2016 2017 2018 2019

Prime Rent Average RentMUNICH 29

Industrial and Logistics Markets Overview | Colliers International

Munich | 2019 / 2020

FAST FACTS

2019 2018 Change

Take-up in sqm 227,000 201,100 13%

Leasing Performance in sqm 202,500 201,100 1%

Number of Deals 95 97 – 2%

Prime Rent* in €/sqm/month 7.15 7.00 2%

Average Rent in €/sqm/month 6.70 6.60 2%

*achievable top rent in new buildings

Freising Take-up according to Location

Submarket Take-up in sqm Share

Hallbergmoos 1 Center 0 0%

Erding

11 Eching

Neufahrn

2 Center North-West 0 0%

Sulzemoos 92

Unterschleißheim

3 Center North-East 0 0%

88 Dachau Oberschleißheim

Garching 12

Bergkirchen

9 4 Center South-East 0 0%

99

Maisach

Olching

Allach

5 Center South-West 0 0%

Milbertshofen Kirchheim bei

Unterföhring München

Fürstenfeldbruck

Moosach Poing

6 City North-West 20,000 9%

6 2 7

München 3

7 City North-East 5,300 2%

99 94

1 Feldkirchen

96

Gilching Gräfelfing 5

Sendling

4

Vaterstetten 8 City South-East 5,900 3%

8 8

9

995

9 City South-West 5,400 2%

10 Unterhaching 10 Periphery South-West 36,000 16%

Baierbrunn 13 11 Periphery North-West 35,200 16%

Brunnthal

952

12 Periphery North-East 102,200 45%

95

13 Periphery South-East 17,000 7%

Total 227,000 100%30

LEASING

Munich | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Take-up Supply and Demand

The Munich industrial and logistics mar- Only three leases were signed for over

ket r ecorded roughly 202,500 sqm in 10,000 sqm in the Munich region, includ-

take-up (excluding office and common ing technology company Hönle’s own-

areas) in 2019, matching previous-year er-occupier development in Gilching

results (2018: 201,100 sqm). However, (roughly 14,500 sqm). Thanks to the deal

results did fall short of the five-year aver- signed by BMW, deals for over 5,000 sqm

age by 13%. If we include owner-occupier accounted for 35% of total take-up, or

activity, take-up for 2019 totaled roughly 79,700 sqm (9 deals signed). The space

227,000 sqm. The largest deal of the year segment of between 1,000 sqm and

was signed by automobile manufacturer 3,000 sqm again proved the most popular,

BMW for a property in Vaterstetten to the generating a total of 68,900 sqm with

east of Munich. The new site will feature about 42 deals signed. The segment also

around 32,000 sqm of hall space and is recorded a yoy increase of 27%.

located in the new VGP Park Parsdorf.

BMW is planning to move into the property Demand continues to be driven by

in 2020. Construction on the large-scale companies from the production and

property development began last October manufacturing sector, which claimed

and the development will feature total a 47% share, or 106,200 sqm, in line

rental space of 250,000 sqm. Machine with previous-year results.

building company Kraus-Maffei is

planning to relocate its premises from Munich continues to lag behind in terms

Allach to VGP Park Parsdorf by 2022. of new-build activity, falling short of

Germany’s other top locations such as

Berlin, Hamburg and Frankfurt. Aside

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

400 up to 500 4,100 2%

342.4

501 – 1,000 20,100 9%

300 1,001 – 3,000 68,900 30%

250.7 3,001 – 5,000 54,200 24%

221.7 227.0

201.1 5,001 – 10,000 34,200 15%

200

above 10,000 45,500 20%

Total 227,000 100%

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201931

from the first construction phase at VGP Outlook

Park Parsdorf, there are currently no

Industrial and Logistics Markets Overview | Colliers International

Munich | 2019 / 2020

Rents are likely to continue to rise, leading

significant new-build developments

many occupiers to turn to surrounding

underway to add space to the market. As

regions such as Augsburg, Ingolstadt and

a result, the majority of leases are still

Moosburg. We expect this year’s annual

being signed for space at stock proper-

take-up to match previous-year results

ties. This trend can be seen in current

thanks to the VGP Park development.

price levels with space at stock proper-

ties in some cases even going for new-

build prices. Supply on the market contin-

ues to be severely limited and available

space is often being re-let off-market.

Rents

Prime rents for warehouses exceeding

3,000 sqm rose 2% yoy to €7.15 per sqm.

Average rents also experienced a slight

increase to a current €6.70 per sqm.

Warehouse rents at the moment are

higher in Munich than in any other Ger-

man city.

Figure 2: Take-up by Branch Share in % Figure 3: Prime and Average Rents in ¤/sqm

8

Logistics Service

Providers 11%

7.15

Trading 7.00

6.85 6.85

Companies 19% 7 6.75

Production &

Manufacturing 6.70

Companies 47% 6.60

6.50

6 6.10

Others 23% 6.00

5

2015 2016 2017 2018 2019

Prime Rent Average Rent32

Industrial and Logistics Markets Overview | Colliers International

Stuttgart | 2019 / 2020

STUTTGART

FAST FACTS

2019 2018 Change

Take-up in sqm 171,400 300,400 – 43%

Leasing Performance in sqm 130,500 257,000 – 49%

Number of Deals 83 83 0%

Prime Rent* in €/sqm/month 6.50 6.50 0%

Average Rent in €/sqm/month 5.20 5.20 0%

*achievable top rent in new buildings

6

Take-up according to Location

Submarket Take-up in sqm Share

Heilbronn Schwäbisch Hall

1 Stuttgart 9,900 6%

2 Ludwigsburg 68,400 40%

81

3 Rems-Murr-District 60,200 35%

2

3

Pforzheim

Ludwigsburg 4 Göppingen 1,100 1%

Waiblingen 5 Esslingen 24,100 14%

Stuttgart 6 Böblingen 7,700 4%

Esslingen

1

Calw

am Neckar

Göppingen Total 171,400 100%

Böblingen

8

6 4

5

Tübingen

81

Reutlingen

Neu-Ulm33

LEASING

Industrial and Logistics Markets Overview | Colliers International

Stuttgart | 2019 / 2020

Take-up Supply and Demand

The Stuttgart industrial and logistics This dramatic drop in take-up can primar-

market finished out 2019 with roughly ily be attributed to the absence of deals

171,400 sqm in take-up, down a consider- for units of over 10,000 sqm, which have

able 43% yoy (300,400 sqm). This is the contributed significantly to take-up

second-lowest result recorded after results in the past. Only 2 leases were

2014’s dip and reflects a 37% drop com- signed in this segment in 2019 (30%, or

pared to the 5-year average. Take-up 52,200 sqm) compared to a total of 8 deals

excluding owner-occupiers came to in the previous year. The small-scale

130,500 sqm, roughly half of the result segment of under 3,000 sqm also posted

posted in 2018 (257,000 sqm). The largest a drop in take-up at 23%. Availability is

deals signed included the Greenfield scarce at the moment and the limited

property development for Daimler in new-build construction activity is unable

Waiblingen (42,000 sqm, Rems-Murr- to provide much relief. Demand from the

Kreis submarket) and the lease signed by automotive sector and automotive suppli-

Daimler subsidiary AMG for roughly ers is also subdued, primarily in response

10,200 sqm in Marbach (Ludwigsburg to uncertainties in the production indus-

submarket). try. Take-up generated by the production

and manufacturing sector fell from 44%

in 2018 to a current 35%. In addition to the

development site bottleneck in all sub-

markets of the Stuttgart logistics region,

building permits are subject to extremely

long lead times and the lack of skilled

workers is tangible. Developers are

Figure 1: Take-up in 1.000 sqm Take-up according to Size Category

Size in sqm Take-up in sqm Share

393.9

400 up to 500 1,200 1%

501 – 1,000 13,300 8%

300.4

300 1,001 – 3,000 37,300 22%

267.6

235.0 3,001 – 5,000 22,300 13%

5,001 – 10,000 45,100 26%

200 171.4

above 10,000 52,200 30%

Total 171,400 100%

100

0

2015 2016 2017 2018 2019

Whole year Average 2015 – 201934

beginning to turn to surrounding regions Outlook

as a result and are increasingly looking to

Stuttgart | 2019 / 2020

Industrial and Logistics Markets Overview | Colliers International

Despite current fluctuations in automo-

the Rhine-Neckar region and the areas

tive production, demand is expected to

along the A8 motorway towards Ulm and

remain high in 2020 with no dramatic

the A81 south of Herrenberg. We are also

impact on the logistics market. We can

likely to see more new-build construction

also expect demand to continue to be

activity along the A7 between the Feucht-

confronted with extremely limited space

wangen junction and Ulm. A few land

available for immediate tenancy, a

sites zoned for logistics are still available

situation that is unlikely to change in 2020

in these areas.

as the new-build pipeline is practically

non-existent at the moment. One of the

Rents few developments for the year involves

30,000 sqm east of Stuttgart along

Prime rents remained stable both within

highway B10 in Plochingen. Due to these

Stuttgart city limits and in surrounding

limiting conditions, we can expect market

districts such as Ludwigsburg, Böblingen

activity to keep a pace similar to that

and Rems-Murr-Kreis. Prime rents for

seen in 2019 and again fall short of the

warehouse space larger than 3,000 sqm

average posted in recent years.

still come to €6.50 per sqm. Average rents

have also stabilized at €5.20 per sqm.

FIGURE 2: Take-up by Branch Share in % FIGURE 3: Prime and Average Rents in ¤/sqm

7

Trading Companies 10% 6.50 6.50 6.50

Logistics Service 6.20 6.20

Providers 11%

6

Production &

Manufacturing

Companies 35%

Others 44% 5 5.20 5.20 5.20

4.80

4.70

4

2015 2016 2017 2018 2019

Prime Rent Average RentINVESTMENT 35

Transaction Volume Supply and Demand

Industrial and Logistics Markets Overview | Colliers International

Investment | 2019 / 2020

The German industrial and logistics real Portfolio deals accounted for €2.6bn in

estate market finished out 2019 with a transaction volume in 2019, or 40% of

satisfactory annual result. Investors annual transaction volume, down 32% yoy.

poured roughly €6.6bn into this asset Apollo Global Management and Palmira

class, bringing in the third-strongest Capital Partners sold the Maximus port

annual result to date since record year folio in Q4, the largest logistics portfolio

2017 (€8.7bn) and 2018 (€6.8bn) despite deal in 2019. Singapore’s sovereign wealth

ongoing limited supply. This result also fund (GIC) acquired the pan-European

managed to top the 5-year average by logistics portfolio comprising 28 assets

roughly 19%. Industrial and logistics once before the end of the year. The portfolio

again proved to be the third strongest as- changed hands for around €950m, €540m

set class on the overall commercial real of which was generated by the portfolio’s

estate market with a market share of over German assets. Other deals included the

9%. This excellent result can largely be sale of the Blue Chip portfolio comprised

attributed to exceptionally lively activity of 3 large distribution centers to GreenOak

during the end-of-year rally. Almost the and Apeiron (roughly €350m) as well as

same amount of capital was invested the sale of 9 logistics assets to the REIT

in Q4 as in Q1 and Q2 combined. And managed by Asian investor Frasers

results would have been even higher if (roughly €320m). The deal involving the

more product had been available. sale of the Amazon Logistics Center

(75,000 sqm) in Dortmund was one of the

year’s major and most expensive single-

asset deals with a gross yield of just above

4%. Arabian investors sold the asset to

Savills Investment Managers for roughly

€140m just two years after initial acquisi-

tion. Another notable single-asset deal

Figure 1: Transaction Volume Industrial & Logistics Figure 2: Transaction Volume by Property Type

in bn € in bn €

8,000 0 10 20 30 40 50

7,000 Office

6,000

Retail

5,000

Industrial &

4,000 Logistics

3,000 Hotel

2,000 Building Site

Commercial

1,000

3,972 4,579 8,662 6,814 6,566 Mixed use

0

Other properties

2015 2016 2017 2018 2019

Industrial Logistics TAV in total Transaction Volume GermanyYou can also read