SAMSUNG Electronics A contrarian's perspective on a top 10 global brand with above average growth potential and a wide margin of safety - ValueWalk

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SAMSUNG Electronics

A contrarian’s perspective on a top 10 global

brand with above average growth potential

and a wide margin of safety.

By: Michael Wood www.evansic.com

Contest Qualification

Source: Samsung Investor Day Presentation 2013

How to buy Samsung Electronics 1. Samsung Electronics (005930 KS Equity) Price: KRW 1,367,000 Prices as of 06/13/14 Shares: 150,777,000 FX rate: 0.0009 USD/KRW Market Cap USD: $185 Billion 2. Samsung Electronics GDR (SMSN LI Equity) Price: USD 672.50 Prices as of 06/13/14 Equiv. GDRs: 276,431,000 Market Cap: USD 185.9 Billion

Disclosure • All values from here on out are reported in USD • All prices and market caps are as of 06/13/14 • This report contains forward-looking numbers that could differ from actual results • Samsung Electronics is not a suitable investment for all investors and individual circumstances should be taken into consideration • This report is intended to provide the investor with research relating to Samsung Electronics and is not a solicitation to buy the stock

Proven Investment Process Cheap price Management: honest & skillful capital allocators Dominant and strengthening competitive advantage (low-cost & high-quality manufacturing) Globally recognized brand that is well taken care of (broad and strong associations) Excellent balance sheet protection

Samsung Quick Stats • Market Cap = $ US 186 Billion • Non-operating assets (net) = $ US 60.4 Billion • Enterprise Value = $ US 125.6 Billion • Q1-2014 Book value = $ US 145.5 Billion • 2014E Net Income = $ US 24.0 Billion • 2014E Free-cash-flow = $ US 24.0 Billion EV/FCF2014 = 5.2x (prices as of 06/13/14)

Thesis 1. Samsung’s businesses are not well understood, as the market is assuming Samsung is only a smartphone company 2. Samsung Semiconductor is worth the enterprise value itself (the market price implicitly assumes mobile is worth -$33B) 3. Samsung trades at more than a 50% discount to peers and intrinsic value 4. Samsung is manufacturing 13 products with global #1 market share that have very defensible market positions 5. Several catalysts are in motion to unlock the trapped value, including IPOing non-core businesses, corporate restructuring and massive share buybacks ($60B net cash) 6. Management has an astounding track record of successfully creating shareholder value

Dispelling the Myths

1. Success of Samsung hinges on the success of the

Galaxy S franchise

2. There is no growth left in the smartphone

industry (the market is fully saturated)

3. Lenovo will drive Samsung’s mobile operating

margins to 3% (while Apple will continue to

operate in a vacuum)

4. Samsung is a copy-cat and is only successful

because they infringe on others’ patents

5. Samsung is not shareholder friendly and will

never return capital to shareholders

This presentation seeks to rectify the myths that cloud

the investor’s mindset on Samsung Electronics

Myth 1 Debunked: Sales by Product (2013)

• Apple’s Portfolio: • Samsung’s Portfolio:

• DRAM 5%

• iPhone 53% • NAND 4%

• iPad 19% • Logic Chipset 5%

• Mac 13% • Mobile Display 5%

• iPod 3% • Large Panel Display 6%

• Tablets 4%

• iTunes 9% • Low-end Smartphones 14%

• Accessories 3% • Premium Smartphones 28%

• Feature phones 3%

• Networking Equipment 2%

• Laptop/PC 4%

• TV/Screen 13%

• Home Appliances 6%

Samsung has a diverse product offering that can withstand the failure of

any single product. Even if iPhone wipes out Galaxy S, Apple will still need

to buy Samsung’s DRAM and NAND memory chips (in larger quantities).

Cheap Price: Samsung SOTP Value 1. Non-core Assets (net) are worth $US 60.4 Billion 2. Samsung Semiconductor is worth $US 125 Billion 3. Samsung Display is worth $US 29.7 Billion 4. Samsung Home Appliance is worth $ US 11.2 Billion 5. Samsung IT & Mobile is worth $ US 208 Billion Total Equity Value $ US 433B Upside to current price: 134%

1. Non-core Assets (net) – $60.4B

• Cash and Cash Equivalents: $17.0 billion

• ST Financial Instruments: $38.6 billion

• ST Available-for-sale FA: $1.9 billion

• LT Available-for-sale FA: a $7.3 billion

• Investment in Associates: b $6.1 billion

• ST Borrowings: -$6.8 billion

• Debentures: -$1.2 billion

• LT Borrowings: -$2.5 billion

Non-Operating Assets (Net) $US 60.4 billion

As of Q1 20141. a. LT Assets Available for Sale

(In millions of US Dollar) Mar-14 Dec-13

Equity securities - Listed $ 3,680 ** $ 3,959

Equity securities - Non-Listed 3,088 704

Debt Securities 558 951

Total $ 7,326 $ 5,615

** Listed Equity Securities:

Number of S hares Percentage of Acquisition Book Value

All values in millions of US Dollars

Owned Ownership Cost March 2014

Samsung Heavy Industries 40,675,641 17.6% $ 195 $ 1,166

Samsung Fine Chemicals 2,164,970 8.4% 41 87

Hotel Shilla 2,004,717 5.1% 13 120

Cheil Worldwide 2,998,725 2.6% 2.6 74

iMarket Korea 647,320 1.8% 0.3 15

SFA 1,822,000 10.2% 34 67

Wonik IPS 7,220,216 9.0% 57 56

ASML 12,595,575 2.8% 653 1,123

CSR - 0.0% - 99

Rambus 4,788,125 4.3% 83 43

Seagate Technology 12,539,490 3.8% 197 669

Wacom 8,398,400 5.0% 56 56

Sharp 35,804,000 3.0% 110 108

Other - 42 49

Total $ 1,484 $ 3,6801. b. Investment in Associates

• Samsung SDS to be spun-off in Q4-2014

All values in millions of US Dollars

Book Value Net Asset

Investee Acquisition Cost

March 2014 Value

Samsung Card $ 1,384.69 $ 2,092 $ 2,077

Samsung Electro-Mechanics 323.82 841 840

Samsung SDI 309.02 1,067 1,316

Samsung SDS 136.54 803 783

Samsung Techwin 144.26 363 395

Samsung Corning Advanced Glass 193.41 186 186

Other 766 766

Total $ 6,117 $ 6,3622. Samsung Semiconductor

• Samsung Semiconductors is worth 9.5x 2015 operating profit

• This equates to a value of $US 125 Billion

• Consistent with Micron (@7.8x 2015 OP) and SanDisk (@ 10x

2015 OP)

• Samsung Semiconductors is worth the enterprise value of

the entire company by itself!!!!

All values are in $US Billion

Samsung Semiconductor 2009 2010 2011 2012 2013 2014E 2015E

Total Revenue 21.4 32.0 33.3 30.7 33.5 41.6 44.9

DRAM 7.5 14.8 12.1 10.6 12.3 16.3 17.5

NAND 5.2 6.7 8.1 7.4 9.1 11.1 12.4

System LSI 3.5 5.9 9.9 11.7 11.4 13.5 14.2

Operating Profit 1.7 8.6 5.8 3.7 6.4 11.4 13.0

Operating Margin 8% 27% 17% 12% 19% 27% 29%

Source: Bloomberg, Company filings, AllianceBernstein2. a. Samsung Memory

• #1 global market share in overall memory

• #1 global market share in Mobile DRAM (49%)

• #1 global market share in PC DRAM (33%)

• #1 global market share in NAND (32%)

Source: DRAMeXchange2. Samsung Semiconductor – Peers

• Samsung trades at half the valuation of sector

• Samsung Semiconductor will earn $11.4 billion operating

profit in 2014, on par with Intel and Qualcomm

• Samsung Semiconductor by itself deserves $125 billion

valuation, on par with Intel and Qualcomm’s enterprise values

All values are in millions of US Dollars

Semiconductor Market Cap Enterprise Gross P/E ex. net cash P/B 5-Year

Value Revenue 2014 2015 2016 Q1 2014 ROE

Intel $148,500 $136,577 $53,100 14.8 14.2 12.2 2.6 20.7%

Qualcomm $134,170 $102,117 $27,470 14.6 13.5 10.1 3.5 16.4%

Micron Tech. $33,360 $26,992 $16,300 9.6 8.8 8.5 3.3 12.7%

SK Hynix $32,085 $34,168 $13,238 7.7 6.4 6.8 2.8 10.8%

SanDisk $22,280 $19,560 $6,660 15.3 14.7 13.0 3.4 13.4%

Sector Average 12.4 11.5 10.1 3.1 15%

Samsung Electronics $185,531 $125,110 $232,715 5.2 4.9 4.7 1.4 20.1%

Source: Bloomberg, Company filingsDRAM Recovery leaves SMSN behind • Consolidation in the DRAM space to 3 competitors has caused DRAM prices to soar and margins to expand • Since 2013, Micron is up 410%, SK Hynix +83% and Samsung -10%

Semiconductor Industry by Revenue

• Does a company that is consistently taking share in the

semiconductor industry deserve a 50%+ discount to its peers?

Source: Gartner3. Samsung Display

• Samsung Display is worth at least 9x 2014 op.

profit, given that their main competitor LG

Display trades at 13.7x 2014 operating profit

• Samsung Display is worth $29.7 billion

All values are in $US Billion

Samsung Display 2009 2010 2011 2012 2013 2014E 2015E

Total Revenue 20.7 25.4 26.3 29.0 27.8 29.5 31.1

Large Panel 9.8 21.6 20.4 19.5 14.7 13.6 14.3

Small & Medium Panel - 2.3 2.4 2.3 0.6 0.5 0.5

AMOLED (aka OLED) - 1.5 3.4 7.2 12.6 15.3 16.3

Operating Profit 1.4 1.7 (0.3) 2.8 2.9 3.3 3.6

Operating Margin 7% 7% -1% 10% 10% 11% 12%

Source: Bloomberg, Company filings, AllianceBernstein3. Samsung Display – #1 Position • Samsung is the dominant player in display with 99% market share in AMOLED • Samsung has already announced Super AMOLED, securing a two-stage technology lead on peers • Despite the technological edge, Samsung trades at a steep discount to its most comparable peer LG Display

3. Samsung Display – Peers

• Samsung Display trades at a 50% discount to

its inferior South Korean competitor LG

Display

• Samsung Display deserves a premium to LG

Display (7% assumed)

• This is the basis of the $29.7 Billion valuation

All values are in millions of US Dollars

Display Market Cap Enterprise Gross P/E ex. net cash P/B 5-Year

Value Revenue 2014 2015 2016 Q1 2014 ROE

LG Display $9,591 $12,712 $27,370 16.1 10.2 9.1 1.0 8.6%

Samsung Electronics $185,531 $125,110 $232,715 5.2 4.9 4.7 1.4 20.1%

Source: Bloomberg, Company filings4. Samsung Home Appliance

• Samsung Home Appliance is worth 7x 2013

operating profit

• Whirlpool trades at 7.8x 2014 operating profit

• This is the basis of the $11.2 Billion valuation

All values are in $US Billion

Samsung Home Appliance 2009 2010 2011 2012 2013 2014E 2015E

Total Revenue 41.0 48.7 42.3 45.0 45.0 52.7 53.4

Visual Display (TV, Monitors) 26.3 28.9 31.3 30.8 29.0 34.0 33.9

Appliance 7.7 10.0 11.0 11.8 13.7 16.1 17.0

Other 7.0 9.8 - 2.3 2.3 2.6 2.6

Operating Profit 2.5 0.4 1.1 2.1 1.3 1.6 1.6

Operating Margin 6% 1% 3% 5% 3% 3% 3%

Source: Bloomberg, Company filings, AllianceBernstein4. Samsung Home Appliance • Samsung has been the fastest growing company in the Home Appliance arena • Samsung is strategically well positioned to take advantage of the smart-home revolution and the convergence between technology and home appliances

4. Samsung Home Appliance • Samsung has been making refrigerators since the 1960’s • Consistently ranked the highest performance product by Consumer Reports • Continues to innovate in the space (Partnership with SodaStream brings carbonated water to the fridge)

4. Samsung Home Appliance • Samsung is expecting 5.1% CAGR out to 2017

4. Samsung Home Appliance – TV • Samsung has had the best selling TVs for the last 8 years • Samsung has the #1 brand awareness globally for TVs

4. Samsung Home Appliance – Peers

• $11.2 Billion valuation for Samsung Home Appliance

is a discount to Whirlpool’s valuation

• Samsung ought to have a premium valuation due to

the disruptive/innovative products and the outsized

growth

All values are in millions of US Dollars

Home Appliance Market Cap Enterprise Gross P/E ex. net cash P/B 5-Year

Value Revenue 2014 2015 2016 Q1 2014 ROE

Whirlpool $10,680 $12,280 $19,410 10.9 9.5 10.1 2.3 13.9%

General Electric $270,050 $434,451 $149,580 16.0 15.8 14.9 2.0 10.4%

Sector Average 13.4 12.7 12.5 2.2 12%

Samsung Electronics $185,531 $125,110 $232,715 5.2 4.9 4.7 1.4 20.1%Samsung valuation so far… Non-core Assets = $60.4 billion Samsung Semiconductor = $117 billion Samsung Display = $ 29.7 Billion Samsung Home Appliance = $11.2 Billion Net Asset Value = $ 218.3 Billion Market Cap = $ 185 Billion Implied value Samsung Mobile = -$ 33.3 Billion

5. Samsung IT & Mobile • Is the world’s largest manufacturer of cell phones really worth -$33 Billion? • Are the risks so high that a business generating $25 Billion operating profit is worth less than nothing!? • Contrarian View: The fear of a mobile implosion has created a wide margin of safety for the contrarian investor, not to mention a potentially lucrative investment opportunity!

5. Samsung IT & Mobile

• Consensus view:

– Samsung Mobile generates all of their profit from

Galaxy S franchise

– Lenovo will drive Samsung’s operating margins to

3%

– Apple will be unaffected by this inevitable industry

paradigm shift

– Growth in smartphones has stagnated and will

likely remain so for the foreseeable future5. IT & Mobile – What is in the group?

• Samsung IT & Mobile is comprised of:

– Premium smartphones

– Low-end smartphones

– Feature phones

– Tablets

– Premium PCs and laptops

– Networking equipment

All values are in $US Billion

Samsung IT & Mobile 2009 2010 2011 2012 2013 2014E 2015E

Total Revenue 30.1 35.0 60.7 93.1 125.2 143.2 149.7

Mobile/Tablet 27.8 32.4 48.1 81.8 112.7 127.5 132.3

PC/Laptop - - 10.7 7.7 8.1 10.1 11.4

Networking Equipment 2.3 2.6 1.9 3.7 4.3 5.6 6.0

Operating Profit 3.3 3.7 7.3 17.1 22.5 25.8 26.0

Operating Margin 11% 10% 12% 18% 18% 18% 17%

Source: Bloomberg, Company filings, AllianceBernstein5. Samsung Smartphone Strategy • Bifurcated strategy: Focused on the (1) high- end and (2) low-end • Success in the low-end will continue to drive manufacturing costs lower and bargaining power with suppliers higher • Success in the high end will be predicated on high quality products and a strong brand image

5. Samsung Premium Smartphones • Two dominant premium smartphone franchises: (1) Galaxy Note (2) Galaxy S • With the Galaxy Note, Samsung pioneered the ‘Phablet’ space

5. Samsung Galaxy S5 Selling Well • Launched in Q2-2014 • Sold 10 million units 10% faster than Samsung Galaxy S4 • This successful launch should help dampen the consensus view that the smartphone business is about to implode

5. Samsung Low-end Smartphones

• Samsung offers a broad array of low-end phones that

each focus on one different main performance

feature

• First phone released with Tizen OS – Samsung Z

Samsung Z Samsung Galaxy Ace 3 Samsung Galaxy Star

Samsung Galaxy Young Samsung Galaxy Active Samsung Galaxy GrandMyth 2 Debunked: Smartphone Growth • Growth in smartphone units – Ericsson • 16.5% unit growth CAGR over 5 years • Pricing would have to fall by 16.5% annually for the next 5 years for sales and earnings to remain flat

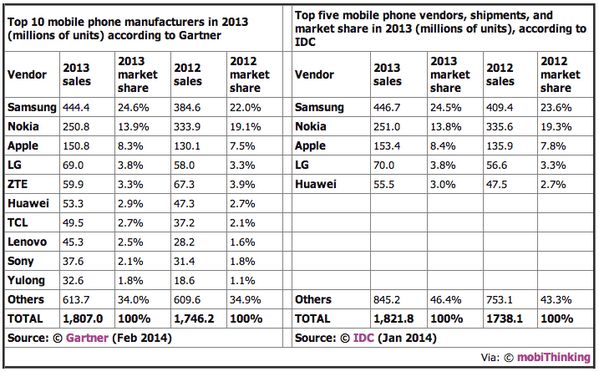

5. Global Smartphone Market Share • Samsung is the dominant supplier of smartphones, with 31.2% market share as of Q1-2014

5. Global Cell Phone Market Share When one includes premium smartphones, low-end smart phones and feature phones, Samsung still stands out as the dominant supplier for mobile devices to the world:

5. Samsung Tablets • Samsung has a solid line up of premium tablets • Samsung recently announced the launch of new tablets with 2K resolution (best on market)

5. Samsung Tablets Taking Share from Apple • According to IDC Samsung took 5% market share directly from Apple in 2013 • Samsung now has 22.3% market share in tablets • Samsung is the only tablet to gain an real traction against Apple

5. IT & Mobile – What’s it worth?

• Apple’s enterprise value trades at 8.9x 2014

operating profit

• Samsung’s IT & Mobile business is worth at least 8x

2014 (10% discount to Apple)

• Therefore, Samsung IT & Mobile is worth $208B

All values are in millions of US Dollars

IT & Mobile Market Cap Net Cash Enterprise Gross P/E ex. net cash P/B 5-Year

(debt) Value Revenue 2014 2015 2016 Q1 2014 ROE

Apple $550,930 $133,627 $417,303 $181,382 10.6 10.2 10.0 4.6 27.6%

Google $371,340 $53,472 $317,868 $52,280 17.3 14.5 12.3 4.3 18.5%

Lenovo $13,271 -$1,500 $14,771 $33,873 16.9 15.2 10.8 4.7 20.3%

Microsoft $339,710 $81,100 $258,610 $88,380 11.3 10.5 9.9 4.0 36.3%

IT & Mobile Average 14.0 12.6 10.7 4.4 26%

Samsung Electronics $185,531 $60,721 $124,810 $232,715 5.2 4.8 4.7 1.4 20.1%Myth 3 Debunked: Lenovo drives margins to 3% • If the consensus is correct and Lenovo is successful in driving down Samsung’s operating margins to 3%, then Samsung will still generate $4.3 billion in operating profit for 2014 • Using a 15x multiple this business is worth $64 billion in a worst case scenario (Lenovo trades at 18x operating profit) • In this scenario Samsung Electronics’ intrinsic value is $283 Billion • Upside to Samsung Electronics in this scenario is still 52% The worst case is more than priced into the stock. Samsung provides a margin of safety for the prudent investor even in a (highly unlikely) worst case scenario.

Except: Brand Matters to Customers!

• Samsung’s brand ranked #8th in the world according to Interband’s Top 100 Global

Brands

• Samsung has a premium product and scale like just like its peers on this list

• Samsung’s brand power will help protect against Lenovo’s aggressive pricing

• This will mitigate the downside scenario that IT & Mobile is only worth $64BSamsung is a premium brand

• Samsung pioneered one of the great rebranding efforts of the modern era

• #1 brand awareness for Smartphones around the world

• #1 brand awareness for TVs around the world

• Lenovo is competing against a lower cost operator that is more widely recognized

in the global market place – they have a tall order ahead of them to try and knock

down SamsungSamsung takes good care of their brand

• Samsung advertises more aggressively than Coca-Cola (the most prolific

advertiser)

• Samsung advertises 4 times more than Apple

• Despite this focus on the customer, the consensus believes that Apple is far more

immune to competitive pressure on its margins

• Even if Lenovo or Apple forces Samsung to compete as a low-end player, they will

not need to advertise as aggressively (mitigating the impact on operating margins)Samsung takes good care of their people

• Samsung is able to advertise more aggressively than Apple because of their

commitment to human capital

• Samsung employs over 325,000 people, more than 4 times what Apple employs

• To commemorate the chairman's 25th anniversary, the employees were paid a $2

billion bonus

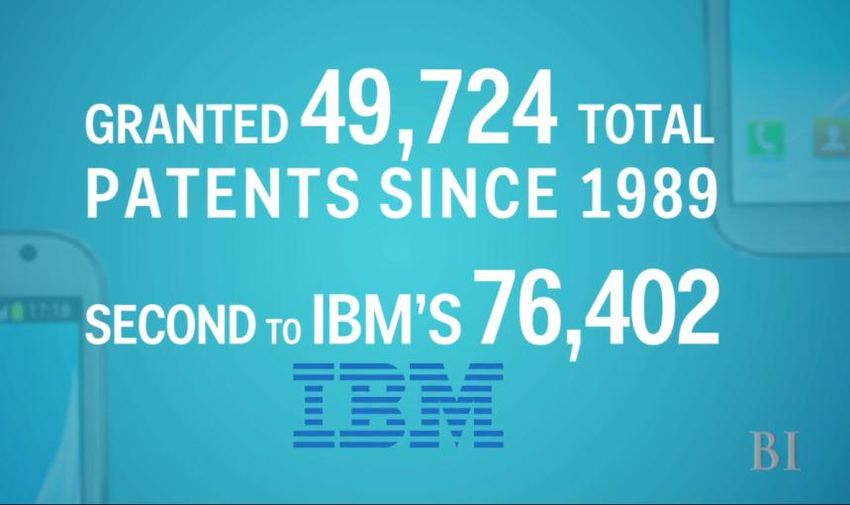

Source: Investor Presentation 2013Myth 4 Debunked: Samsung’s Patent Portfolio is Strong • Since their venture into the cell phones business in 1992, Samsung has amassed a mobile patent portfolio that consists of 16,000 patents • Samsung couldn’t possible be a copy-cat if they have amassed nearly 50,000 patents since 1989 (second only to IBM) • Despite Apple’s patent victories in the US, no major victories have been awarded off home-turf • The most recent patent ruling found that Apple also infringed on Samsung’s patents

‘Three Stars’ of Samsung • Samsung was founded by Lee Byung-Chul (top), is currently chaired by Lee Kun Hee (left), and will be succeeded by Lee Jae-Yong (right) • Samsung is a family owned business with the current chairman controlling 49.7% of voting control • The Lee family has an impeccable record for allocating capital to growing sectors of technology • Each generation has left their unique mark on the company

Proven Track Record

Source: Bloomberg, Company FilingsExcellent Capital Allocation – Return on Capx

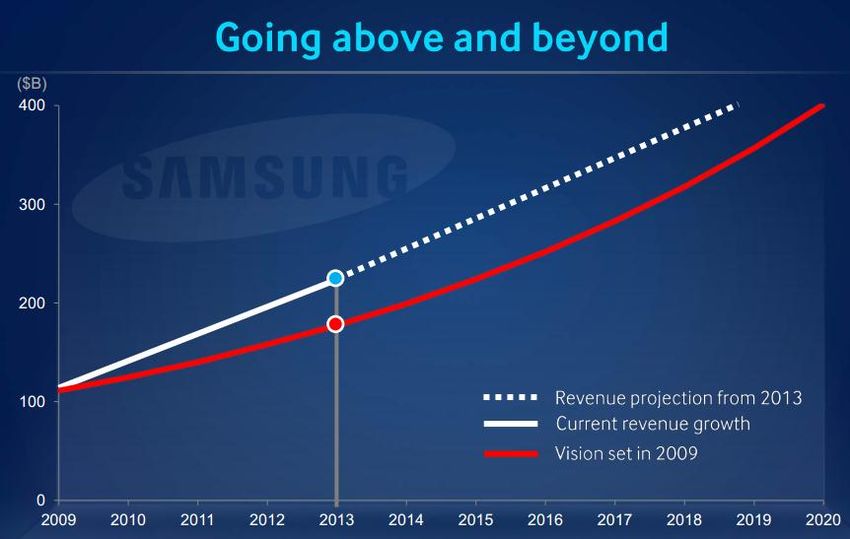

Source: Investor Presentation 2013Management expects more of the same • While most struggled to keep their heads above water in 2009, Samsung set the goal to reach $400 billion sales by 2020 • So far so good:

Founder: Lee Byung-Chul

• Born: 1910

• Died: 1987 (at age 77)

• Founded Samsung in 1969

• Started as a rice-trading operation

• Transitioned into manufacturing TV

sets, electric fans and refrigerators

• Extended the business in the 1950s to

include banking, insurance, real estate

and tungsten exporting

• Invested in microprocessor

manufacturing in 1974 by purchasing

Korean Semiconductor Company out

of bankruptcy

Lee Byung-Chul’s philosophy for establishing new businesses:

“Pounce on them when the market is at rock bottom.”Ahead of their time: Samsung’s 1980 Sahoon

The company’s philosophy promotes the idea that

the individual will grow to be a Samsung man by:

1. Acquiring the capability and the courage for

empowerment

2. Growing an internationally oriented mind

3. Making use of team spirit and solidarity

4. Reminding the employee of the sovereignty of his

existence as the leader, making history for his time

5. Thinking in terms of effectiveness, not to be

inhibited by past practices and attitudes

6. Cultivating the pioneering attitudeCurrent Chairman: Lee Kun-Hee

• Age: 72

• Chairman since: 1987

• Son of Lee Byung-Chul

• Most notable accomplishment is the

64MB DRAM memory chip, transforming

the formerly bankrupt company into the

worldwide memory leader

• Chairman Lee wanted to build a brand,

not just a product

• Today, Samsung has 13 products with #1

global market share all under the

Samsung brand

• Diagnosed with lung cancer in 2000

• Suffered a severe stroke in 2014Catalyst: Corporate Restructuring • The fabric of the circular holding structure is unraveling • 2013: Gov’t bans cross holding structures, provides tax break for unwinding of circular holding structures • 2014: Chairman Lee tragically suffers a severe stroke • 2014: Samsung announced IPO of Samsung SDS, Samsung Everland

Catalyst: Gov’t Bans Cross Shareholdings • President Park Geun Hye’s government introduced in 2013 legislation banning family-run chaebol businesses from creating new cross shareholdings, which were blamed by the Intarnational Monetary fund for contributing to the nation’s 1997-1999 financial crisis • The government is also offering tax breaks to encourage the chaebol to unwind existing structures to form more transparent holding companies Could Jay Lee use this tax break as an opportunity to transfer his father’s assets in exchange for a conversion of Samsung Electronics into a holding company structure?

Catalyst: New Chairman Jay Y Lee • Age: 42 • Son of Lee Kun-Hee • Graduated from Seoul National University • Graduated from Keio University (Japan) • PhD from Hardvard University • Fluent in Korean, Japanese and English • Brokered the licensing deal with Android that enabled Samsung’s Mobile division to grow from $35 billion to $135 billion in 5 years • Main point of contact for key suppliers and partners (Google, Apple, Sony, HP)

Catalyst: Samsung SDS IPO • Announced May 8, 2014 • Expected to IPO in Q4 2014 • Established in 1985 as a data system and technology consulting company • Provides IT and Networking consulting, customized application integration, IT infrastructure outsourcing

Catalyst: Samsung Everland IPO • Announced on May 15, 2014 • Expected to happen Q1-2015 • Everland is a holding company with influential ownership in Samsung Life (the largest shareholder of Samsung Electronics) • This IPO marks the unraveling of Samsung’s circular holding structure • Proceeds are expected to cover estate taxes for Jay Lee and family

Myth 5 Debunked: History of Share Buybacks

• Preserving capital became the priority in 2008

as the Lee family planned for succession.

Lee Kun Hee began

succession planning

for Jay Lee

Lee Kun Hee suffers

severe strokeCatalyst: Inevitable Share Buyback • Chairman Lee Kun-Hee currently has 49.7% voting control of Samsung Electronics • Presumed tax bill is $US 6 billion • IPO of SDS and Everland are expected to yield $3 billion for the family • Jay Lee will need to repurchase up to $US 20 billion worth of shares within Samsung Electronics to retain his father’s current voting control

Management recognizes valuation disparity

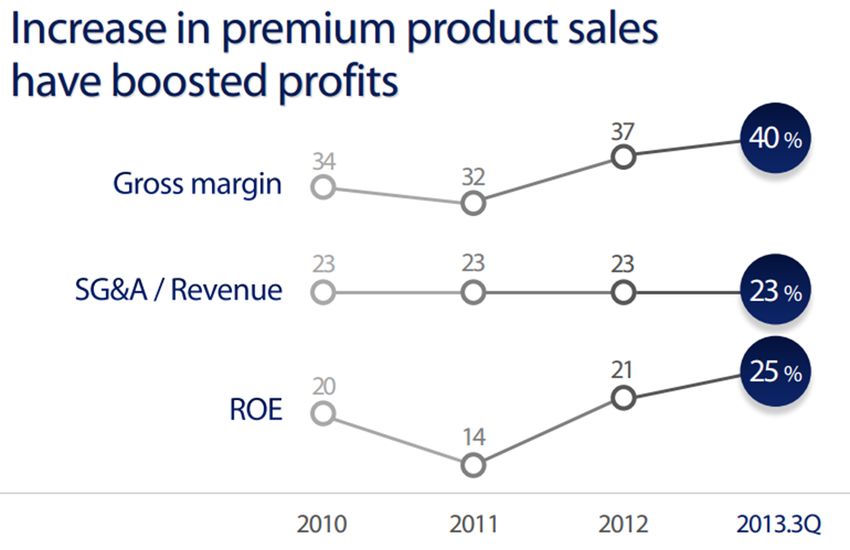

Source: Investor Presentation 2013Samsung is firing on all cylinders

Source: Investor Presentation 2013Conclusion • Samsung Semiconductor is worth enterprise value • Market is ascribing no value to IT & Mobile, Display and Home Appliances • #8 Global Brand Value in the world • #1 Brand awareness in Smartphones and TVs • 13 Products with #1 market share • Improving corporate governance • Realigned interests with Lee family • Massive share buybacks on the horizon • Limited downside given $60.4 billion Non-core Assets

Valuation Extremes… 14’ Rev: $232B 14’ Rev: $11.9B 14’ FCF: $24B 14’ FCF: $3.1B EV: $129B EV: $159B Samsung’s enterprise value is $30 billion cheaper than Facebook yet 8x more profitable!!

What’s in your portfolio? By: Michael Wood www.evansic.com

You can also read