Santander Consumer Bank AS - Investor Presentation 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Santander

Consumer Bank AS

Investor Presentation 2017

1

Disclaimer

Important information

Santander Consumer Bank AS ("SCB") cautions that this presentation contains forward-looking statements. These forward-looking statements are found in various places throughout this presentation and include, without

limitation, statements concerning our future business development and economic performance. While these forward-looking statements represent our judgment and future expectations concerning the development of our

business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to: (1) general market,

macro-economic, governmental and regulatory trends; (2) movements in local and international securities markets, currency exchange rates and interest rates; (3) competitive pressures; (4) technological developments;

and (5) changes in the financial position or credit worthiness of our customers, obligors and counterparties. The risk factors that we have indicated in our past and future filings and reports, could adversely affect our

business and financial performance. Other unknown or unpredictable factors could cause actual results to differ materially from those in the forward-looking statements.

This document has been prepared by SCB for information purposes only and its contents are proprietary information and are strictly private and confidential. You agree that this document should not be reproduced (in

whole or in part), delivered or distributed to others or replicated without the prior written consent of SCB and is intended to be read by market professionals (eligible counterparties and professional clients) and should not

be disclosed to nor relied upon by retail clients and/or investors.

Forward-looking statements speak only as of the date on which they are made and are based on the knowledge, information available and views taken on the date on which they are made; such knowledge, information

and views may change at any time without notice. SCB does not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

Likewise, this document contains certain tables and other statistical analyses (the "Statistical Information") which may have not been audited. Numerous assumptions have been used in preparing the Statistical Information,

which may or may not be reflected in this document or be suitable for the circumstances of any particular recipient. As such, no assurance can be given as to the Statistical Information's accuracy, appropriateness or

completeness in any particular context, or as to whether the Statistical Information and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Statistical

Information should not be construed as either projections or predictions or as legal, tax, financial, investment or accounting advice.

Note: Statements as to historical performance or financial accretion are not intended to mean that future performance, share price or future earnings (including earnings per share) for any period will necessarily match or

exceed those of any prior year. Nothing in this presentation should be construed as a profit forecast.

The information contained in this presentation is subject to, and must be read in conjunction with, all other publicly available information, including, where relevant any fuller disclosure document published by SCB. Any

person at any time acquiring securities must do so only on the basis of such person's own judgment as to the merits or the suitability of the securities for its purpose and only on such information as is contained in such

public information having taken all such professional or other advice as it considers necessary or appropriate in the circumstances and not in reliance on the information contained in the presentation. In making this

presentation available, SCB gives no advice and makes no recommendation to buy, sell or otherwise deal in shares in SCB or in any other securities or investments whatsoever.

Neither this presentation nor any of the information contained therein constitutes an offer to sell or the solicitation of an offer to buy any securities. No offering of securities shall be made in the United States except

pursuant to registration under the U.S. Securities Act of 1933, as amended, or an exemption therefrom. Nothing contained in this presentation is intended to constitute an invitation or inducement to engage in investment

activity for the purposes of the prohibition on financial promotion in the U.K. Financial Services and Markets Act 2000. This document is not intended for distribution to, or use by, any person or entity in any jurisdiction or

country where such distribution or use would be contrary to law or regulation.

The businesses included in each of our geographic segments and the accounting principles under which their results are presented here may differ from the included businesses and local applicable accounting principles

of our public subsidiaries in such geographies. Accordingly, the results of operations and trends shown for our geographic segments may differ materially from those of such subsidiaries.

To the fullest extent permitted by law, SCB does not accept any liability whatsoever (including in negligence) for any direct or consequential loss arising from any use of or reliance on material contained in this document. In

addition neither SCB nor any of their affiliates makes any representation or warranty as to the fairness, accuracy, completeness, adequacy or comprehensiveness of the information contained in this document and

expressly waives any responsibility arising from any lack of accuracy, comprehensiveness and adequacy of the information contained in this document.

This document has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently neither

SCB nor any director, officer, employee or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the document distributed to you in electronic format and the hard

copy version available to you on request from SCB.

This presentation is provided on the basis of your acceptance of the terms of this disclaimer.

2

Table of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

3

Financial Highlights Q1-2017

NOK 868,7 MM in Profit before tax

P&L 4,9% Net Interest Income ratio

18,7% Return on Equity

NOK ~144 Bn in Total Assets

Assets 3,1% increase in Net Loans

2,8% Return on Assets

Affirmed ratings of A-/A3 by Fitch/Moody’s

Funding

Self funding ratio increased from 70,4% to 75,4%

Consolidated Liquidity Coverage Ratio of 113%

Risk

NPL ratio lowered to 2,01%

14,6% CET1 ratio

Capital

Dividend of NOK 1,2 billion paid to parent

4

SCB Nordic at a glance

Strong performance in a AAA region, Q1-2017 figures

Nordic

Gross Outstanding Auto Loans¹: 100,3 Bn (76%)

Gross Outstanding Unsecured Loans²: 31,6 Bn (24%)

Profit Before Tax: 869 MM

Norway Finland

Auto Loans: 42,4 Bn Auto Loans: 19,2 Bn

Unsecured Loans: 10,9 Bn Unsecured Loans: 2,4 Bn

Profit Before Tax: 374 MM Profit Before Tax: 148 MM

Total

Outstanding 40%

share Total

16% Outstanding

Denmark share Sweden

Auto Loans: 21,0 Bn Auto Loans: 17,7 Bn

Unsecured Loans: 5,1 Bn Unsecured Loans: 13,2 Bn

Profit Before Tax: 192 MM 53 % Profit Before Tax: 155 MM

Total

Total 24% Outstanding

Outstanding 20% share

share

Source: Q1 2017 Report

All figures in Norwegian Kroner (NOK)

1) Gross Outstanding Auto Loans (“Auto Loans”): Total loans before individual and group-wise write-downs, Operational leasing and Stock Finance.

5 2) Gross Outstanding Unsecured Loans (“Unsecured Loans”): Direct Loans, Credit Cards and Sales Finance (“Durables”)

3) Return on Assets: PBT (annualized) / ANEA

Strong asset growth

Robust business development and growth across all Nordic countries

Gross outstanding loans by geography

140 000

3%

8%

120 000 16%

16% 15%

15%

100 000 39%

20% 20% 20%

20%

80 000 16%

23% 24% 24%

21% 24%

60 000

40 000

41% 41% 40%

40%

20 000

0

2012 2013 2014 2015 2016 Q1 2017

Finland Denmark Sweden Norway

Source: SCB annual reports (2012 – 2016) and Q1 2017 report

6 Figures in NOK million

Solid financial performance

Increased earnings from strong asset growth, lower funding costs and merger synergies

Profit before tax (NOK MM)

3 500

3076

3 000

2 500

2 000

1942

1 500 1393 1321

1136

1 000 869

712

500

0

2012 2013 2014 2015 2016 Q1 2016 Q1 2017

Full-year 2016 development

2016 full year PBT contribution from the GE-portfolio compared to only half year in 2015

Net loans increased by 7,5%

Reduced funding costs in 2016

Opex in 2015 was significantly higher than 2016 due to restructuring costs related to the merger with GE.

LLR & write off alignment after the merger in 2015

Source: SCB annual reports (2012 – 2016) and Q1 2017 report

7

SCB achieved its stand-alone rating in 2016

Ratings are equalized with those of its direct and ultimate parent

Moody’s Fitch S&P

Banco Santander Long Term: A3 Long Term: A- Long Term: A-

S.A. Short Term: P-2 Short Term: F2 Short Term: A-2

(Stable Outlook) (Stable Outlook) (Positive Outlook)

Santander Consumer Long Term: A3 Long Term: A- Long Term: BBB+

Finance S.A. Short Term: P-2 Short Term: F2 Short Term: A-2

(Stable Outlook) (Stable Outlook) (Positive Outlook)

Santander Consumer Long Term: A3 Long Term: A-

Bank AS Short Term: P-2 Short Term: F2 -

(Stable Outlook) (Stable Outlook)

SCB AS ratings

affirmed by

Fitch & Moody’s

for 2017

8

Table of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

9

Core strengths of SCB Nordic

Market leader in the Sound financial Good asset quality Part of the Santander

Nordics performance group

• #1 position in auto finance in • Strong profitability history - • Internally developed risk • Strong, globally diversified

Norway, Finland and PBT of NOK 869 million models owner

Denmark, and #4 in Sweden • Total Assets of NOK ~144 • Pro-active portfolio • Sharing of risk management,

• Pan-Nordic market leader in billion management systems and knowledge

the unsecured segment • Solid capitalization. CET11 of • Retail customer base

14.6% • Low and stable NPL-ratio at

2.01%2

Source: Q1 2017 Report

1) CET1 = Common Equity Tier 1

10 2) NPL-ratio = Non-performing loans / Gross outstanding loansThe Nordic

Core Auto

strengths of Finance market

SCB Nordic

SCB’s market share and main competitors

Market leading position provides

Norwegian market economy of scale Finnish market

8% 13 % 6%

9%

25 % 21 %

11 % 24 %

19 % 27 %

36 %

Santander Consumer Bank DNB Finans Santander Consumer Bank OP Financial Group

VW Møller Bilfinans Nordea Finans Nordea Finans Danske Finance

Sparebank 1 Gruppen Others (incl captives) Others (incl captives)

Danish market Swedish market

12 % 36% 14 % 34 %

Market shares

and position 27%

14 % 18 % 20 % Market shares 10 %

36% 18 %

24 %

and position

#1

#1

Santander Consumer Bank Jyske Finans Santander Consumer Bank Volvo Finans

Nordea Finans

Others (incl captives)

Nordania

53 % Volkswagen Finans

Others (incl captives)

DNB Finans

#4

Partnerships with

Market shares 10% Market shares

and position 20%

#1

and position

19 brands &

3.900+

dealers

Source Norway: Internal calculations based on data from Finansieringsselskapenes Forening as per Q1 2017

Source Finland: Internal calculations based on data from Finnish Transportation Safety Agency (Trafi) as per Q1 2017

11 Source Denmark: Internal calculations based on data from Finans og Leasing as per year-end 2016

Source Sweden: Internal calculations based on data from Finansbolagens Förening as per year-end 2016Segments and customer types

SCB Auto’s main business area is car financing for private customers

Stock

Finance

Other Private

Persons

5%

6%

40%

13%

Auto SME

77% 23%

New Cars

6%

Wholesale

49% Other 4%

Used Cars

Segmentation based on Gross outstanding loans figures for Q1 2017

“Other” segments refers to leisure financing

12

“Other” customer type primarily consists of municipalitiesUnsecured product offering and segments

The Unsecured portfolio is divided into three main products

1%

Sales

20% Finance

Credit

Cards

79%

Direct

Loans

Segmentation based on Gross outstanding loans figures for Q1 2017

13Digitalisation at the core of consumer strategy

The journey has started and will continue during 2017

Santander Commerce Universe

Digital NORDIC

Building a Digital foundation - Core system replacement Plastic to Wallets

Transformation PSDII

CONSUMER

Digital application and

BUSINESS

Journey signature processes

HOW WHO

“Banking is no longer somewhere you go,

but something you do” (Brett King)

WHAT

“Banking is essential, Banks are

not” (Bill Gates)

CRM – a foundation for a real time engine to convert big data to customer value

14Table of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

15Group Balance Sheet summary

Robust balance sheet driven by growth in net loans

NOK Billion Q1 2017 Q4 2016 Δ Q/Q % FY 2016 FY 2015 Δ 16/15 %

Claims on Banks 3,0 4,0 -1,0 -26 % 4,0 5,8 -1,8 -31 %

Net Loans 125,5 121,7 3,8 3% 121,7 113,6 8,1 7%

Cash, Comm Paper, Bonds, Central Bank 9,2 10,9 -1,7 -16 % 10,9 9,2 1,7 18 %

Other Assets 6,5 6,1 0,4 7% 6,1 7,3 -1,2 -16 %

Total Assets 144,1 142,7 1,4 1% 142,7 135,9 6,8 5%

Liabilities to Banks 29,9 35,0 -5,1 -15 % 35,0 33,6 1,4 4%

Liabilities to Customers 43,9 41,0 2,9 7% 41,0 37,4 3,6 10 %

Bonds and other long term loan raising 47,3 42,6 4,7 11 % 42,6 41,5 1,1 3%

Other Liabilities 3,1 3,6 -0,5 -15 % 3,6 4,4 -0,8 -18 %

Subordinated loan capital 3,6 3,6 0,0 0% 3,6 3,8 -0,2 -5 %

Equity 16,5 17,0 -0,5 -3 % 17,0 15,3 1,7 11 %

Total Liabilities & Equity 144,1 142,7 1,4 1% 142,7 135,9 6,8 5%

Full-year 2016 development

Overall Balance Sheet growth driven by growth in net loans

Claims on banks reduced due to lower reserves on securitization transactions

Increase in deposits consistent with funding strategy

Dividend payment of NOK 500 MM in December 2016

Bonds purchased as part of liquidity portfolio of NOK 14,2 bn YTD

Issued bonds of NOK 18,3 bn in 2016 bn YTD (NOK 7,9 bn in Q4)

Source: Q1 2017 and 2016 Annual Report

16Group Income Statement summary

P&L showing steady growth with increasing PBT after legal merger

NOK MM Q1 2017 Q1 2016 Δ Q/Q % FY 2016 FY 2015 Δ 16/15 %

Interest Income 1 895 1 912 -17 -1 % 7 657 6 444 1 213 19 %

Interest Expenses -345 -375 30 -8 % -1 405 -1 525 120 -8 %

Net Interest Income 1 550 1 537 13 1% 6 252 4 919 1 333 27 %

Net fees, Commissions and Other 135 113 22 19 % 375 290 85 29 %

Other product related income & cost -23 -4 -19 475 % 70 29 41 141 %

Gross Margin 1 662 1 647 15 1% 6 697 5 238 1 459 28 %

Personnel Expenses -282 -296 14 -5 % -1 161 -1 014 -147 14 %

Administration Expenses -377 -340 -37 11 % -1 303 -1 418 115 -8 %

Depreciation -26 -27 1 -4 % -109 -79 -30 38 %

Net Operating Income 978 984 -6 -1 % 4 124 2 727 1 397 51 %

Other Operating Expenses -1 0 -1 - -70 12 -82 -

Loan Losses -108 -272 164 -60 % -977 -797 -180 23 %

Profit Before Tax 869 712 157 22 % 3 076 1 942 1 134 58 %

Taxes -205 -182 -23 13 % -765 -435 -330 76 %

Profit After Tax 663 530 133 25 % 2 311 1 507 804 53 %

Q1 2017 development Full-year 2016 development

Increase in net loans is higher than increase in net interest Legal merger with Santander Consumer Bank AB occurred on 1

income due to increase in Auto part of the product mix portfolio. July 2015 and therefore the first six months of AB performance

Lower funding cost contributes to a higher net interest income. are not included in statutory figures

Significantly lower losses, mainly driven by lower reserves. Write- A financial tax on wages of 5% of gross salaries paid to correct for

off and recoveries relatively stable. lack of VAT on financial services was introduced in Norway on 1

Jan 2017

Source: Q1 2017 and 2016 Annual Report

17Solid financial KPI development

Strengthening ratios due to merger effects

Return On Assets1 Return on Equity2

3,0 % 20,0 %

2,6 % 17,5 %

17,2 %

2,5 % 16,2 % 16,3 %

2,1 % 15,0 %

2,0 % 13,7 %

2,0 %

12,9 %

1,8 %

12,5 %

1,7 %

1,5 % 10,0 %

7,5 %

1,0 %

5,0 %

0,5 %

2,5 %

0,0 % 0,0 %

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

ROA: Increase due to higher portion in unsecured ROE: Increase due to strong PAT growth in 2016

financing and merger one-offs in 2014 and 2015. and despite higher regulatory requirements.

Source: SCB annual reports (2012 – 2016)

1) Return on Assets: PBT / ANEA

18

2) Return on Equity: PAT / Average Core Capital (CET1)Solid financial KPI development

Increased profits and stricter cost control

Net Interest Income Ratio1 NII Ratio: Development largely due to higher portion of

7,0 % unsecured loans from merger.

6,0 %

5,3 %

5,0 % 4,6 % 4,6 % 4,4 % 4,7 % C/I Ratio: Decrease due to strong cost control, synergies from

4,0 % merger and higher margins.

3,0 %

2,0 % Loan Loss/ANEA: Development driven by stable risk

1,0 % performance and more conservative LLR adjustment in 2014.

0,0 %

2012 2013 2014 2015 2016

Cost / Income Ratio2 Loan Loss / ANEA3

60% 1,25%

50% 1,1 %

50% 1,00%

42% 44% 0,9 %

42% 40% 0,8 %

40% 0,8 % 0,7 %

0,75%

30%

0,50%

20%

10% 0,25%

0% 0,00%

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Source: SCB annual reports (2012 – 2016)

1) Net Interest Income Ratio: NII / ANEA

19 2) Cost / Income ratio: OPEX / Gross Margin

3) Loan Loss / ANEAFunding

Steadily increasing self funding, with focus on deposits and senior unsecured issuances

Self-funding pillars1 Funding composition

120

100 17% 22% 27%

Senior

Securitization Deposits

Unsecured 80

NOK billion

33%

35% 36%

• 8 current • NOK 7,25 billion • In Norway 60

outstanding outstanding in deposits are 20%

13%

40 12%

transactions the Norwegian guaranteed up to

across Nordics bond market NOK 2 MM 20 30% 30% 25%

• Represents a • SEK 5,26 billion • In EU countries 0

2011 2012 2013 2014 2015 2016 Q1 2017

low-cost and outstanding in the guarantee is

stable funding the Swedish up to EUR Parent funding Securitization Deposits Unsecured Bonds

source bond market 100,000

Self-funding ratio

• EUR 2,25 billion • NOK 44 billion in

outstanding from total deposits 100%

four Benchmark across Norway, 75,4 %

transactions Sweden and 80% 70,1 % 70,4 %

62,4 %

issued under the Denmark

60% 49,6 %

SCB AS EMTN

Programme

40%

28,2 %

21,9 %

20%

0%

2011 2012 2013 2014 2015 2016 Q1 2017

Source: Q1 2017 Report

20 1) Outstanding amounts/transactions as per Q1 2017Unsecured Senior Funding

2016 summary and Q1 2017 developments

NOK SEK EUR

New Issuances 3,651 million 1,451 million 1,000 million

2016

Maturities 1,104 million - 500 million

Repurchases 401 million 90 million -

Net new funding 3,250 million 1,210 million 1,000 million

Total outstanding¹ 5,821 million 4,860 million 1,750 million

Preferred Format Floating Rate Note Floating Rate Note Fixed Rate Note

Preferred Tenor 2 – 3 year 2 – 3 year 3 year

New Issuances 2,200 million 400 million 500 million

2017

Maturities - - -

Repurchases 800 million - -

Net new funding 1,400 million 400 million 500 million

Total outstanding² 7,251 million 5,260 million 2,250 million

Preferred Format Floating Rate Note Floating Rate Note Fixed Rate Note

Preferred Tenor 3 – 5 year 3 – 5 year 3 year

Source: Q1 2017 Report, 2016 Annual Report, Bloomberg

1) Outstanding amounts as per year-end 2016

21

2) Outstanding amounts as per Q1 2017Unsecured Funding

Maturity profile 2017 - 2022

Total Maturity (EUR MM) EUR MM

1500 1200

1000

1000

1400 800 750

600 500

1300 400

200

1200

0

2017 2018 2019 2020 2021 2022

1100

1000

1000 SEK MM

900 3000

2410

2500

800 2000

1450

1500

1000

700 1000

750 500 400

600 0

2017 2018 2019 2020 2021 2022

500

152

400

500 NOK MM

4000 3451

300

3000

105

200 376

42 2000 1600

253 1300

100 175 1000

900

142

98

0 0

2017 2018 2019 2020 2021 2022 2017 2018 2019 2020 2021 2022

NOK SEK EUR

Source: Q1 2017 Report, 2016 Annual Report, Bloomberg

22 FX: SEK/NOK 0,9618 EUR/NOK 9,1683 EUR/SEK 9,5322Nordic Deposits

Online distribution of high-yield deposit products

Nordic Deposit

Consolidated Total Balance: NOK 44 Bn

• Retail customer base

• Highly competitive market with many small players

Norway

Deposit Balance: NOK 19,8 Bn

• Demand products with floating interest

rate

% of

Consolidated 45%

Denmark balance

Deposit Balance: NOK 11,5 Bn Sweden

• Demand and Notification product with Deposit Balance: NOK 12,7 Bn

floating interest rate • Demand and Notification product with

• Termed Deposit with fixed interest rate

53 % floating interest rate

% of

% of

26% 29% Consolidated

Consolidated

balance

balance

Source: Q1 2017 Report

23Strict capital requirements in Norway

Ensuring strong capitalization of the bank

CET1-ratio requirements per Q1 2017 and expected requirements per Q4 2017

Q1 2017 Q4 2017

2.2% 2.2%

Pillar 2 CET1- Pillar 2 CET1-

requirement requirement

Countercyclical Countercyclical

buffer ~1.03% buffer ~1.3%1

~0.27%

~13.23% Systemic risk ~13.5% Systemic risk

Increase in CET1

buffer 3% buffer 3%

requirements due to

~11.03% ~11.03% increase in ~11.3% ~11.3%

Pillar 1 CET1- countercyclical buffer Pillar 1 CET1-

requirement Conservation requirement Conservation

buffer 2.5% buffer 2.5%

Minimum CET1 Minimum CET1

requirement requirement

4.5% 4.5%

• Strict requirements in Norway with the inclusion of additional buffer requirements and a high countercyclical buffer requirement

• Pillar 2 requirement for SCB was set to 2.2% by the Norwegian FSA, applicable from January 2017

• From Q4 2016, the countercyclical buffer requirement is calculated as a weighted average of the risk weighted assets in the

countries where the bank operates

• Per end 2017, the bank expect a CET1 ratio requirement of about 13.5%

• From July 2017, SCB will have to comply with a leverage ratio requirement of 5%

1) Pillar 1 CET1 requirement here incorporates the increase in countercyclical buffer from 1.5% to 2% in Norway in December 2017. Total countercyclical buffer requirement is set to

1.3% since the countercyclical buffer requirement is calculated as a weighted average of the risk weighted assets in the countries where the bank operates . The countercyclical

24 buffer for SCB will vary with the share of risk weighted assets in each country and according to the buffer requirement determined by the respective countrySCB has strengthened its capital ratios

With a CET1 ratio ~15%

Capital ratios evolution SCB Group1

25%

20% 19,14% 18,66%

17,77% 17,41% 18,08%

16,89%

15,26% 15,09% 14,63%

15% 13,71% 13,86% 14,12%

13,06%

10,90%

9,69%

10% 10,78% 11,43% 11,53% 11,41%

10,27%

5%

0%

2013 2014 2015 2016 Q1 2017

CET1 Tier 1 Tier 2 Leverage ratio

High capital ratios attained through solid earnings and IRB

• SCB capital ratios are comfortably above regulatory requirements

• Adoption of advanced IRB approach in December 2015 provided capital relief of about NOK 1.3 billion

• Combined with solid earnings in 2016, SCB paid dividends of NOK 1.7 billion¹ for 2016

• SCB aims to pay annual dividend subject to ensuring adequate capitalization of the bank

• With a leverage ratio of 11.4%, the bank is well positioned to meet the coming leverage ratio requirement

1) NOK 500 million payed in December 2016 and NOK 1.2 billion payed in February 2017. Therefore, December 2016 capital ratios

25 include the dividend payment of NOK 1.2 billion in February 2017.Table of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

26Risk Management

Clear governance and management structures

Clear governance & key Seeking synergies to be efficient Making sure to have the

decision bodies best team in Risk

General Assembly

Independent entities Financial

GREAT PEOPLE

Supervisory

(Shareholder) Supervisory Board

Committee of Representatives

Authority

+

Board of Directors

Control Committee

OPPORTUNITY

=

Directors

Audit Committee

Remuneration

Committee

Internal Audit

SCB AS

Internal Audit Director RESULTS

Risk Committee

Internal Audit

Administration

Grupo Santander

Chief Executive Audit

Officer

Securitization

Senior Management AML

Team (SMT) Basel II

Credit Risk

Credit Committee Legal

(1. Auto 2. Non-

Auto) Finance

IT

Asset & Liability

Committee

Independent Credit Risk

Capital Committee

Control Unit

Nordic Internal

Control Committee External Audit Deloitte

Sourcing Board

Compliance

Committee

AML Committee

Branches lead by

Local Management

Teams

Local Credit

Committee

27Sound underwriting processes

Information is fed into PANDE1 Key components in underwriting

• Credit reports from • Minimum acceptance

external agencies criteria including:

• Internal payment history • Min. age

• Pay-slips, tax • Down payment

Credit requirements (LTV)

information declarations, etc.

• AML/Fraud

Credit info Credit policy

Credit

policy PANDE Scorecards

• Internally developed • Includes:

scorecards since 2010 • Age

• Enables high degree of • Mileage

automatization • Brand

• Models integrated into

management

Vehicle

information

Scorecards Vehicle info

28 1) Pan Nordic Decision EngineCreditor friendly legal environment

Good legal environment for automatic underwriting and collection in the Nordics

Underwriting: Underwriting: Underwriting: Underwriting:

• Public access to • Access to debt register • Negative payment • Negative payment

income history and income register register

• Negative payment information

register (Upplysningscentralen)

Collection: Collection: Collection: Collection:

Collateral can be Collateral can be Collateral can be Collateral can be

repossessed outside repossessed outside of repossessed outside of repossessed outside

of court court court of court

Withholding of salary Withholding of salary For both secured and For auto loans, the

can be arranged can be arranged unsecured loans, the Bank can claim

Sales-lien on car will For auto loans, the Bank will have a claim proceeds from sale of

expire after 5y Bank can claim on the Borrower for the car

For both secured and proceeds from sale of any outstanding For unsecured loans,

unsecured loans, the the car and payment of amount up to 15-20y the Bank will have a

Bank will have a outstanding invoices lifetime claim on any

Denmark

Sweden

lifetime claim on the For unsecured loans, outstanding loan

Norway

Finland

Borrower for any the Bank will have a

outstanding loan lifetime claim on any

outstanding loan

29Tight risk controls result in stable performance

Risk ratio breakdown

NPL Ratio 2012 2013 2014 2015 2016 Q1 2017 NPL Ratio3

Denmark 0,70 % 0,71 % 0,61 % 0,97 % 1,21 % 1,30 % 2,05% 2,01% 2,01%

1,76%

1,61% 1,48%

Finland 1,38 % 1,04 % 0,89 % 0,72 % 0,71 % 0,71 %

Norway 2,47 % 2,47 % 2,36 % 3,41 % 3,36 % 3,35 %

Sweden 0,74 % 0,48 % 0,61 % 1,52 % 1,22 % 1,22 %

Nordic 1,76 % 1,61 % 1,48 % 2,05 % 2,01 % 2,01 %

2012 2013 2014 2015 2016 Q1 2017

NPL Ratio 2012 2013 2014 2015 2016 Q1 2017

Auto¹ 1,30 % 1,20 % 1,09 % 1,01 % 1,08 % 1,07 % Coverage Ratio4

Unsecured² 6,24 % 5,32 % 4,77 % 4,95 % 4,88 % 4,94 %

126,9 %

113,5 %

Nordic 1,76 % 1,61 % 1,48 % 2,05 % 2,01 % 2,01 % 97,7 %

106,8 %

98,6 % 99,3 %

Coverage Ratio 2012 2013 2014 2015 2016 Q1 2017

Auto¹ 69,2 % 75,5 % 89,4 % 95,4 % 90,4 % 86,9 %

Unsecured² 138,6 % 136,4 % 148,1 % 111,8 % 113,1 % 107,7 %

Nordic 97,7 % 98,6 % 126,9 % 106,8 % 113,5 % 99,3 % 2012 2013 2014 2015 2016 Q1 2017

1) Auto includes Stock Finance

2) Unsecured includes Direct Loans, Credit Cards and Sales Finance (“Durables”)

30 3) NPL ratio = Non-performing loans / Gross outstanding loans

4) Coverage Ratio = Loan Loss Reserves (Write Downs) / NPLTable of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

31Part of the Santander Group

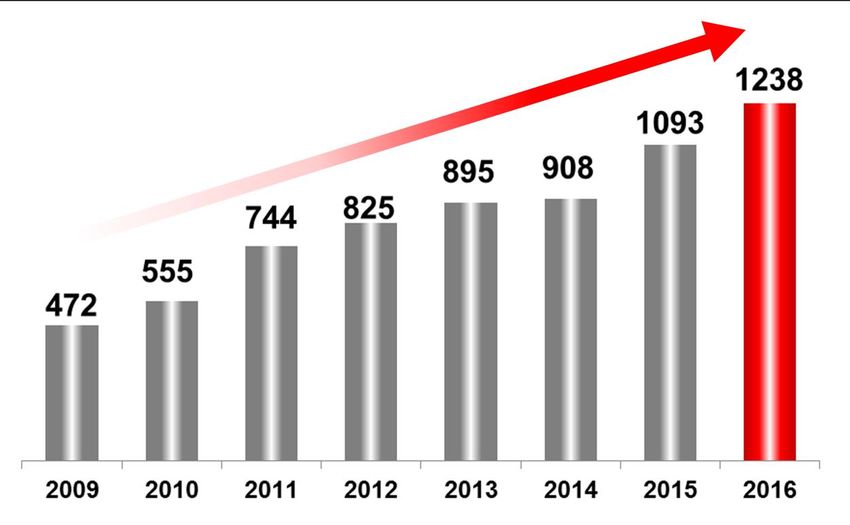

A leading financial group worldwide

1.35 TN

EUR total

assets 128 MM

customers

6.204 BN

EUR PAT

2016

95 BN

EUR total

assets

1.238 BN

EUR PAT

2016

SCF: Management perimeter (Includes Santander Consumer UK)

32Fully owned by Santander Consumer Finance

Santander Consumer Bank AS is regulated by the Norwegian FSA

Banco Santander S.A.

SCF accounts for 14% of

Banco Santander’s NAP1

Santander Consumer

Finance S.A.

SCB Nordic accounts

for 22% of SCF’s NAP

Santander Consumer

Bank AS

Norway

Santander Consumer Santander Consumer Santander Consumer

Bank AS Bank AS Finance OY

(Branch, Sweden) (Branch, Denmark) (Subsidiary, Finland)

1) Percentage over Banco Santander 2016 Profit after tax, excluding Corporate Centre and Real Estate Activity in Spain.

33Our Culture

“At the heart of our culture we believe that wherever we operate, everything we do

should be Simple, Personal and Fair.”

Ana Botín

Group executive chairman

34Key takeaways for continued growth

• Defend our position as a Nordic market leader

• Continue to deliver strong financial results

• Maintain focus on risk to ensure good asset quality

• Continue leveraging strength of a global banking franchise

35Table of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

36Grupo Santander & Santander Consumer Finance

Subjects Banco Santander Santander Consumer Finance

Santander, a leading financial group

Key Figures Mar’17

Total assets (trill. €) 1.35

Attributable Profit 1Q’17 (mill. €) 1,867

Headcount 188,182

Customers (millions) 128

Shareholders (millions) 3.96

Branches (units) 12,1171Q'17 Financial Highlights

Chg. 1Q’17 / 1Q’16

(1) % change in constant euros

FL CET1: Common Equity Tier 1 Fully Loaded RoTE: Return on Tangible Equity EPS: Earnings Per Share TNAV: Tangible Net Asset Value1Q'17 Business Highlights

Chg. Mar’17 / Mar’16

Note: Loans excluding repos. Customer funds: deposits excluding repos + marketed mutual funds. % change in constant eurosDelivering on our commitments with a story of profitable growth (1) % change (constant euros), (2) Dividends charged to 2017 profit to be submitted to the AGM for approval EPS: Earnings Per Share DPS: Dividends Per Share FL CET1: Common Equity Tier 1 Fully Loaded

Subjects Banco Santander Santander Consumer Finance

Santander Consumer Finance

Santander Consumer Finance is the European leader

in the consumer finance industry …

… fully owned by Santander, one of the largest

financial groups in the world

Its core businesses are car finance and consumer

finance (durables financing, personal loans and

credit cards) …

… distributed mainly through point-of-sales, and

direct-to-consumer channels such as internet,

telemarketing platforms and branches.European leader in the consumer finance industry

Key Figures Mar’17

Loans (bill. €) 95

Deposits (bill. €) 36

Attributable Profit 1Q’17 (mill. €) 344

European countries 15

TOP 3 position1 (countries) 14

Customers (million) 20

PoS partnerts (thousand) >130

SCF: Management Control Perimeter (includes SCUK).

(1) By Market share in New Business car loans or durablesWith recurrent profits through the cycle

Net Attributable Profit

€ Million

All-time record profit result in 2016

In 1Q17, profit of €344 million (+19% y-o-y)

SCF: Management Control Perimeter (includes SCUK).A differential and proven business model

A

High diversification and European leadership

B

Advanced car financing platform and strong foothold in consumer finance

C

SCF’s

Efficiency leadership with proven integration capabilities

business model

D

Best-in-class risk and collections capabilities

E

Sound funding structureA

Well spread across Europe and well balanced

between car and consumer loans

Geographic diversification Product diversification

Outstanding: €95 bn Outstanding: €95 bn Auto

(Mar’17) Other (Mar’17) Car Stock Consumer

Other

Poland Finance

7% Other

Italy 4% 10%

5%

Auto

7% Germany Mortgages -New

UK 36% 8%

35%

8% % loans % loans

by country Cards 3%

by product

4%

10%

France Durables 13%

13% 15% 22%

Auto-Used

Spain Direct

Nordic Countries

Well spread across 15 European countries Car financing represents the biggest share

Important foothold in the largest economies of the portfolio: 67%

74% portfolio in AAA & AA countries Consumer lending (durables financing, cash

loans and credit cards): 21%

SCF: Management perimeter (i.e. including SCUK)B

Advanced car financing platform and strong foothold

in consumer finance

Advanced car financing platform Strong foothold in consumer finance

• Presence in all European markets • TOP retail chain agreements throughout

Europe

• TOP positions in its geographies,

including the 5 biggest European auto • >55,000 POS partners

markets: Germany, France, UK, Italy and

Spain, that accounts for 75% of Europe’s • 4.3MM consumer loans per year

car registrations

• TOP 3 in core geographies

• >75.000 POS (captive and non-captive)

• Digital direct business platforms

• The longest European captive

agreements base: more than 100

agreements with 15 manufacturers Consumer Finance: Durable financing, Personal loans and Credit Cards

SCF: Management perimeter (i.e. including SCUK)C

One of the best efficiency ratios in the industry, with

proven capabilities to make the most of integrations

2008

Cost to Income • UK • Austria 2014 …

Pan-European peers • Germany • Finland

• Norway

• Sweden

2009 • Denmark

• German

• Benelux

2015 …

2010

• France

• Poland

• Germany

• UK

• Italy

2011 • Spain

• Poland

• Germany • Portugal

• Belgium

• Austria

• Netherlands

2014 • Switzerland

• Spain

SCF: Management perimeter (i.e. including SCUK)

Peers: CREDIT AGRICOLE Consumer Credit, BNP Personal FinanceD Sound risk metrics

Risk Premium (%) NPL Ratio (%)

Coverage Ratio (%)

SCF: Management perimeter (i.e. including SCUK). Risk Premium: Ratio (%) of average VMG (last 12 months variation in delinquency balance minus Net Write Offs for the

period) to average portfolio (for a period of twelve months). (12-month VMG / 12-month Average Managed Loans) * 100.E Funding diversification

SCF’s funding structure

Mar’17

• Capacity to do issuances

in all countries

• Diversification of deposits

in many countries

• Improvement of access

cost to markets

• Increase of long term

financing versus short

term

SCF: Management perimeter (i.e. including SCUK)All in all, SCF is a significant contributor to Santander’s

results, representing 14% of the Group’s profit* in 1Q17

SCF

represents

14%

of

SAN profit (*)

in 1Q17

SCF geographies in Europe

• Austria • Italy • Nordics

• Benelux • Portugal • Poland

• France • Spain • UK

• Germany • Switzerland

SCF: Management perimeter (i.e. including SCUK). Excluding SCUK, SCF represents 13% of SAN profit*

(*) Percentage over SAN underlying profit in 1Q17, excluding Corporate Centre and Real Estate Activity in Spain.Table of contents

1. Highlights

2. Company Overview

a) Business

b) Financials

c) Risk

d) Santander Group

3. Appendix: Banco Santander & Santander Consumer Finance

4. Appendix: Contacts

54Contacts

• Anders Bruun-Olsen, Nordic CFO • Thomas Andrén-Johansen, Capital Markets Manager, Nordic

• Mobile: +47 95 76 83 28 • Mobile: +47 91 82 42 44

• E-mail: anders.bruun.olsen@santanderconsumer.no • E-mail: thomas.andren.johansen@santanderconsumer.no

• Priscilla Halverson, Capital Markets Director, Nordic • Morten Christopher Freberg Holme, Capital Markets Manager, Nordic

• Mobile: +47 92 06 58 75 • Mobile: +47 92 82 38 33

• E-mail: thomas.andren.johansen@santanderconsumer.no

• E-mail: priscilla.halverson@santanderconsumer.no

• Anders Fuglsang, Capital Markets Manager, Nordic • Joachim Joveng Rogne, Capital Markets Analyst, Nordic

• Mobile: :+47 48 23 86 32

• Mobile: +47 95 04 21 28

• E-mail: joachim.joveng.rogne@santanderconsumer.no

• E-mail: anders.fuglsang@santanderconsumer.no

• For more information:

• Santander Consumer Bank AS: www.santanderconsumer.no

• Santander Consumer Finance SA: www.santanderconsumer.com

• Banco Santander: www.santander.com

55Thank you!

You can also read