Short Energizer Holdings, Inc - NYSE:ENR Sohn Conference - May 2017 - SOHN - Conference Foundation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Short Energizer Holdings, Inc.

NYSE:ENR

Sohn Conference – May 2017

Company Overview

Core Battery (~90% of Sales)

2000 – Spun off by Ralston Purina

2015 – Spun off by Edgewell

Personal Care

May 2016 – Acquired HandStands

(Auto Care)

Batteries (Alkaline): #1 or #2 HandStands (~10% of Sales)

player in most/all markets, #2 in

US with 30% share

Lighting (flashlights – ~15% US

share, headlights, and lanterns)

Auto Care (fragrance – ~20% US

share, appearance)

Page 2

When Did You Last Buy Batteries?

Page 3

Alkaline Batteries Are In Long-Term Secular Decline Source: Deutsche Bank Page 4

Secular Decline Of Alkaline Batteries Likely To Continue

European Battery Sales (Y/Y)

Global Alkaline Battery Market

expected to decline at 0.16%

CAGR from 2015 to 2019

In the US and Europe, battery

sales have been declining in the

~3-4% range over the last

several years

Products, like mobile phones and

smart watches, now featuring

lithium-ion batteries

Lithium-Ion Market forecast to

grow at 11.6% CAGR from 2016

to 2024

OEMs and their suppliers

provide lithium-ion batteries, not

Duracell or Energizer

Source: Research and Markets, Transparency Market Research, Deutsche Bank Page 5

High Customer Concentration With Major Retailers

Some argue that, with Berkshire’s Battery Retailers

acquisition of Duracell, the players in

the space will act more rationally

The Problem: All of the power lies in

the hands of retailers

In the US, ~90% of battery sales are

concentrated among only 8 or 9

retailers

Retailers have all the leverage over

their suppliers, forcing them to drop

their margins, threatening to give

preference to other branded players

or private players

Retailers will continue to beat up the branded players, resulting

in declining prices and margins for battery suppliers.

Page 6

Costco Case Study

Costco beat up their suppliers so much that the

winner in the competition to be their exclusive

supplier, Duracell, was forced to also make a

private label battery for them. The kicker is that

the private label lasts longer as well.

Discharge Duration

[Gray = Kirkland Signature, Orange = Duracell]

The identical

bottoms of the

batteries reveal

that they were

made by the same

company (Duracell)

Source: http://www.paulallenengineering.com/blog/kirkland-signature-alkaline-batteries Page 7

Private Label Vs. Branded Batteries: Value Proposition

Private Label Branded

Basic Technology Patent Date 1960 1960

Pricing Lower (25-40%) Higher

Cost Per Unit Energy Lower Higher

Variable Production Costs Same Same

Overhead Bare Bones Sizable Offices and Sales & Marketing Teams

Advertising Budgets Virtually Non-Existent Sizable

Private Labels have 10-15% share Brand doesn’t carry the same

in the US and ~30% share in weight for batteries as it does for

Europe other products, like detergent or

shaving razors

Private Labels have turned

batteries into commodities. With The products are not

little overhead and no advertising, differentiated, and consumers,

they offer essentially the same given the availability of

product at a much lower price information, have begun

This low-priced alternative should realizing it

lead to declining share, pricing, and

margins for branded players, Energizer and Duracell have cut

regardless of what they do their advertising budgets

accordingly

Source: Clark.com, Batteryshowdown.com Page 8

Private Label Vs. Branded Batteries: Performance Even in the European market, which has Private Label share in the ~30% range, which reflects the increased competition there, Private Labels like Ikea Alkalisk and Costco Kirkland Signature are still the best deals Source: Batteryshowdown.com, Deutsche Bank Page 9

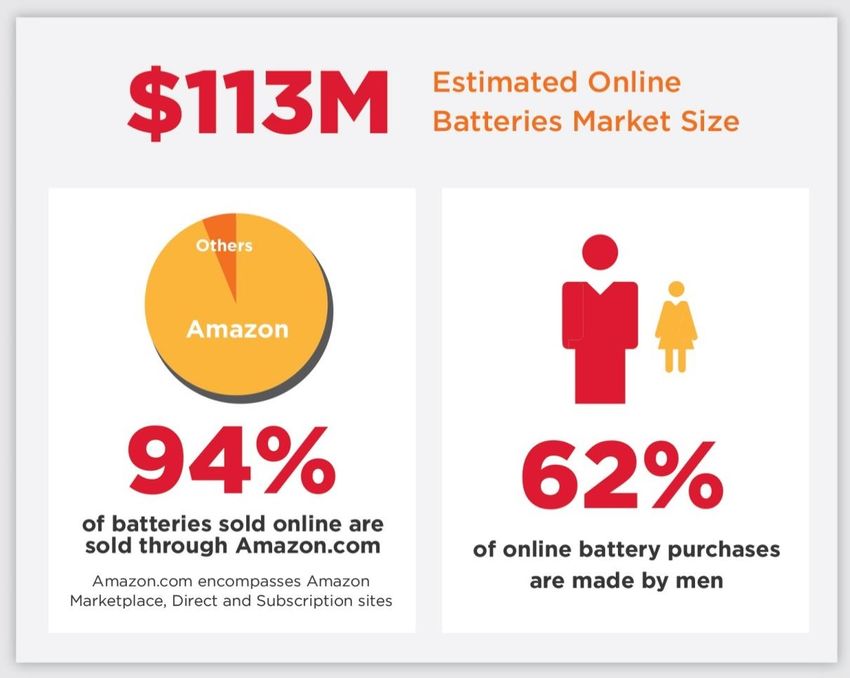

Private Label vs. Branded Batteries: E-Commerce Source: Amazon.com Page 10

Retail And The Amazon Effect

“The times they are a changin’.” – Bob Dylan

E-Commerce currently

makes up about 2-4% of

total battery sales

E-Commerce has grown

75% in the past year, and

will likely continue to

grow at a very fast pace

Private Labels can now

circumvent the

distribution and

relationship advantages

of the branded players

Source: 1010data Page 11Retail And The Amazon Effect (Continued)

In addition to declining pricing and margins, the ascendancy of E-

Commerce should also result in share loss for branded players

Source: 1010data Page 12Energizer’s Cost-Cutting Prospects Are Minimal

Some sell-side analysts indicate

that there is room to cut costs

By all accounts, Energizer has

been a well-run business over

the last several years

As indicated to the left,

Energizer’s 2013 restructuring

recently streamlined their

business

Speaking with Energizer’s IR,

they indicate that there is no real

cost-cutting opportunity

Source: Energizer Investor Presentation Page 13Energizer Hyped As An Acquisition Platform . . .

After 2000 Ralston Purina Spin After 2015 Edgewell Spin

Leveraging their distribution The battery business has

platform, Energizer acquired a declined, reducing Energizer’s

great set of brands leverage to introduce new

products

Shaving: Edge, Schick, Skintimate

The good brands are spoken for

Sun Care: Banana Boat, Hawaiian

Tropic Energizer now has to bid against

the likes of P&G, Unilever,

Feminine Care: Playtex, Stayfree, Nestlé, and Edgewell for deals

Carefree, and O. B.

Energizer is not as well

capitalized as these other

businesses

Energizer plans to make more acquisitions, and this should result in a

squandering of shareholder value

Page 14. . . But Energizer Is Now A Fundamentally Worse Platform

After 2000 Ralston Purina Spin After 2015 Edgewell Spin

Highly

Do you know

Recognizable

these brands?

Brands

Page 15Energizer’s First Acquisition Was Unimpressive

HandStands Shrinking Market Share

ENR paid 10x EBITDA (not cheap),

with HandStands growing at low-

to-mid single digits, although even

this is questionable

Auto care is highly competitive,

with HandStands losing share

(going from 26% to 18% in HandStands’

fragrance) and sales recently share

dropped from

HandStands is already in ~70% of 26% to 18%

the retailers where Energizer is in fragrance

already featured, leaving minimal in just one

room for growth year

The Energizer retailers which don’t

carry HandStands likely don’t really

sell automotive products

Source: Energizer Investor Presentation, Deutsche Bank Page 16Energizer’s Recent Results Confirm Weakness

1st Quarter – 2017 2nd Quarter – 2017

Stock traded up due to 7% On May 3rd, 2017, ENR reported

organic growth, whose primary NO ORGANIC GROWTH

drivers were temporary

“Inventory Deload”: This sounds

3%: shelf space gains, to be a lot like channel stuffing

lapped in the 2nd quarter

“Price Increases”: With the rise

3%: incremental holiday activity of Private Labels, especially

Amazon, this isn’t sustainable

Margin improvements due to

favorable commodity prices and

holiday sales improvements

Temporary factors (shelf space gains, commodity prices, hurricane sales)

have enabled Energizer to beat street estimates on poor quality earnings

Source: Energizer Earnings Transcripts Page 17Several Near-Term Headwinds For Energizer “Inventory Deloading” Lapping of shelf space gains in 2017 should result in little or no organic growth Commodity prices, recently at historic lows, are rising and are expected to rise much more Rising interest rates (which are US Treasury Yield Curve expected) would make yield companies like Energizer less attractive Source: IMF, US Treasury Page 18

Channel Stuffing, Anybody? Energizer’s Distribution Gains Energizer Added New Displays In Stores Some of this involves increasing the number of displays at some of their retailers Though slightly beneficial, this artificially improves sales by saddling retailers with more inventory With their aggressive revenue Energizer’s Organic Growth recognition, this is de facto channel stuffing In the most recent quarter, “inventory deload” (-4%) rendered their organic growth flat Source: Energizer Investor Presentation and Earnings Transcripts Page 19

Energizer’s Private Market Value

Warren Buffett, Berkshire Acquires Duracell

Berkshire Hathaway CEO

February 2016: Berkshire

Hathaway acquired Duracell, the

#1 alkaline battery player, paying

7x EBITDA

Buffett traded his $4.7 billion

worth of Procter & Gamble shares

($336 million cost basis) for

Duracell and $1.8 billion in cash

Doesn’t include Berkshire’s ~$1.5

billion in tax savings from avoiding

capital gains on the P&G shares.

Including this, Berkshire actually

paid more like 3.4x EBITDA

Given that Energizer is the #2 player in the space, an 8x forward

EV/EBITDA multiple is very conservative

Page 20Energizer Is Exceedingly Overvalued

FY 2017E FY 2018E FY 2019E FY 2020E

Revenues 1,686 1,678 1,670 1,663

Growth % 3.2% (0.5%) (0.5%) (0.4%)

EBITDA 326 323 320 317

EBITDA Margin % 19.4% 19.2% 19.2% 19.1%

Market Capitalization 3,693 3,702 3,711 3,720

Net Debt 570 478 388 301

Enterprise Value 4,263 4,180 4,099 4,021

Forward EV/EBITDA Multiple 13.1x 12.9x 12.8x 12.7x

Assumed Forward EV/EBITDA Multiple 8.0x 8.0x 8.0x 8.0x

Implied Share Price $33.02 $33.98 $34.96 $35.95

Implied Return 44.7%

This is assuming that multiples don’t compress below 8x

Page 21Several Catalysts Can Lead To Energizer Shares Declining

Energizer’s investor appeal is its

2% dividend yield

Rising interest rates (which are

expected) would make yield

companies less attractive

Continued secular decline in the

alkaline battery space

Disappointing earnings as a

result of temporary factors

reversing

Poor acquisitions, which could

lead to debt or equity offerings

that could harm stock price

Page 22Thank You!

DISCLAIMER: THIS PRESENTATION IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES. PLEASE DO YOUR OWN RESEARCH.

DISCLOSURE: WE ARE SHORT SHARES OF ENERGIZER.You can also read