Shriram Housing Finance - pg 5 - Banking Frontiers

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Vol. 19 No. 10 February 2021 `75

Pages 52

Shriram Housing Finance pg 5

UCO Bank pg 6

Max Life Insurance pg 15

Online AGMs pg 30

www.bankingfrontiers.com

www.bankingfrontiers.live

Dimensions

o f T r a n s f o r m at i o n

LAV ANUP GOVIND JAIDEEP K PAUL RAJEEV

CHATURVEDI RAU SINGH HANSRAJ THOMAS YADAV

Presents

AWARDS 2021

World of

Virtual Summit l 6th March 2021

The World has undergone a shift in recent times. Most of the organisations

World of NEXT

have seen their plans dwindle. A World where digital is no longer a thing

that is difficult to learn, A World where Digital is the new normal. Digital

work has but the entire financial inclusion and payments space into a full

throttle. The payment industry is also exploring newer capabilities with

new payment umbrellas and newer regulations coming up to achieve

the payment targets. Security is consistently the only factor which has

Welcome to the

maintained its highest relevance in the world Next.

Finnoviti for the BFSI sector and Technoviti

for the FIntech and Big Tech Sector will

CONTACT US

ASHISH VERMA

explore what is going to be shaping the

+91 - 98332 36943

NEXT in Financial Services. The conference ashishverma@glocalinfomart.com

content would be carefully designed around STALIN SALDHANA

the following areas to ensure a strategic +91 - 91677 94513

stalinsaldhana@glocalinfomart.com

input for leaders when they plan their NEXT.

Call for Nominations!

Editor’s Blog

N. Mohan

Mobile : 9322895820

Email : mohan@bankingfrontiers.com

February 2021 - Vol. 19 No. 10

Bad bank for healthier banks

T

Group Publisher : Babu Nair he Government in the Budget 2021

has mooted the setting up of an asset

Group Editor : Manoj Agrawal management company and an asset

reconstruction company to manage the

Editor : N. Mohan

mounting NPAs in the banking system in

the country. The country’s banks together

Editorial are expected to put initial capital for the

Mehul Dani, Ravi Lalwani, V. Raghuraman framework. With this proposal comes back

the idea of setting up of a bad bank and it is

Research Editors evident that the Government is worried about

V. Babu, Ratnakar Deole, the possible spike in the already worsened

W.A. Wijewardena, Sanchit Gogia, NPAs situation as the pandemic has directly contributed to increasing number of

K.C. Shashidhar, Dr L.S. Subramanian, defaults among borrowers as well as loan write-offs and restructuring among the

Ajay Kumar measures initiated to soften the impact.

The concept of bad bank has been tried and tested with mixed results in countries

Advisor-Alliances like the US, Sweden, Finland, France and Germany. The idea came up in India

Ateeq Siddique during the tenure of Dr Raghuram Rajan as the governor of the Reserve Bank of

Marketing India. The proposal was in fact made after an asset quality review of banks revealed

that several banks had suppressed bad loans to show a healthy balance sheet.

Kailash Purohit, Dhiraj Mestry,

Many experts believe that a professionally-run bad bank, funded by the private

Dhara Thobani, Rohit Kahar, Aditya Arya

lenders and supported by the government, can be an effective mechanism to deal

Events & Operations with NPAs. The government must indeed be a stakeholder in the set-up, which only

Shirish Joshi, Stalin Saldhana, will help getting the desired result, they aver. In fact, the IBA had supported such

Pramod Jadhav, Ashish Verma, a proposal and suggested equity contribution from the government and banks.

Wilhelm Singh, Sneha Agrawal, However, the government has not responded to this proposal as it seems to be

looking at a market-led resolution process.

Samata Mestry, Ramesh Vishwakarma

There are opponents too. They feel that this will be an easier way out for banks

Design having substantial NPAs to park all their bad assets and then do nothing to resolve

Somnath Roy Choudhury them. They point out to the ineffective legislation of Insolvency and Bankruptcy

Code, which has shown very limited results.

Published By There has been an instance in 2004 of bad loans getting transferred from a

Glocal Strategies & Services bank to a special purpose vehicle, when IDBI Bank put nearly Rs 90 billion of bad

D-312, Twin Arcade, Military Road, Marol, loans into a wholly owned special purpose vehicle. It remains a fact that neither

Andheri (E), Mumbai 400059, India. did the bank recover substantial amounts via this special purpose vehicle nor could

Tel: +91-22-29250166 / 29255569 it improve its NPA situation.

Fax: +91-22-29207563 A bad bank is essentially an ARC, and India has ARCs that operate in the

private sector. In allowing their operations, the Reserve Bank of India hoped

that these ARCs would buy bad loans of commercial banks and using their own

mechanism to resolve them. Unfortunately details show that these ARCs could not

Printed & Published by Babu Nair on

even touch the peripheral layer.

behalf of Glocal Strategies & Services and

What the country needs today are comprehensive structural reforms to manage

Printed at Indigo Presss (India) Pvt Ltd., the NPAs of banks rather than experimental schemes and legislations often coming

Plot No. 1C/716, Off Dadoji Konddeo Cross in as knee-jerk reactions. The examples are the Strategic Debt Restructuring and the

Road, Between Sussex and Retiwala Indl. Scheme for Sustainable Structuring of Stressed Assets (S4A) and more recently the

Estate, Byculla (E), Mumbai 400027. IBC. For any effort to be meaningful and result-yielding, there has to be a realistic

identification of the problem and its magnitude, an understanding of the conditions

Editor: Manoj Agrawal (Responsible for that led to the problem and then evolving practical methods in resolving the problem.

selection of news under PRB Act) And of course, there must be a will on the part of the banks and the government to

resolve the issue by strictly prohibiting extraneous considerations. Otherwise, bad

bank or ARCs, unrealistic NPAs will continue to haunt our banking system.

Banking Frontiers February 2021 3

N E W S Regulator

Chinese central bank sets up JV with SWIFT

Global financial

Bahrain grants license

messaging and cross- for CoinMENA

border payments system The Central Bank of Bahrain has

SWIFT has set up a joint granted permission to Middle Eastern

venture with a unit of the digital assets exchange CoinMENA to

People’s Bank of China launch its operations in the country. The

possibly an indication certified Sharia-compliant exchange said

of how China wants it has now been awarded a Crypto Asset

to explore global use Services Company license (category 2)

of its proposed digital by the central bank. The platform will

currency. The unit that become one of relatively few fully licensed

the central bank of China and operating digital assets exchanges

that will be involved in for retail and institutional investors in

the joint venture is its the Kingdom of Bahrain, the United

digital currency research institute and clearing center. Other participants in the Arab Emirates, Saudi Arabia, Kuwait

joint venture are China’s Cross-border Interbank Payment System (CIPS) and the and Oman. Once launched, it will offer

Payment & Clearing Association of China, both supervised by the central bank. The spot trading in 5 major cryptocurrencies

joint venture is being named as Finance Gateway Information Services Co. It is - bitcoin, ether, XRP, litecoin and bitcoin

having its head office at Beijing and the purported business it will handle has been cash. It also plans an over-the-counter

described as information system integration, data processing and technological desk for larger trades.

consultancy. There are 2 other Chinese payments market participants and

infrastructure providers as partners in the venture. SWIFT said the joint venture

will be able to obtain necessary licences for local network management activities

SAMA changes

and its services will be limited in scope and entirely focused on maintaining Governor

compliance with applicable regulations in China.

Kenya’s central bank to modernize payment system

The Central Bank of Kenya has come out with a draft document outlining a 5-year

digitization plan to modernize the country’s domestic payment landscape. The

document, titled Kenya National Payments System Vision and Strategy 2021-2025

and released in December 2020, stresses the regulator’s commitment to establishing

a regulatory landscape that is conducive to innovation, as well as embracing open

banking and APIs, among other key areas of focus. The central bank said it will

work to define standards for API development and mandate data portability with

hopes that more options and innovative solutions will be made available for Kenya-

based users to choose from. The proposed standards will include API specifications

for identification, verification, and authentication; customer account information/ Saudi Arabia’s ruler has removed

data access; transaction initiation; and formats and coding languages for APIs. the central bank’s governor Ahmed

Al-Kholifey and appointed Fahad

Dubai central bank fine on BoB Al-Mubarak as the new governor. This

The Central Bank of the United Arab Emirates has imposed financial sanctions would be Al-Mubarak’s second stint

on 11 banks operating in the country for their failure to reach appropriate levels as governor of Saudi Central Bank,

of compliance on anti-money laundering and sanctions. Among the 11 banks is or SAMA. A decree by the king said

Bank of Baroda, GCC operations, Dubai. A statement said the sanctions imposed at-Kholifey, who had held the post since

amounted to a total of AED45.76 million ($12.5 million). A statement from the 2016, would become an adviser at the

central bank said the financial sanctions take into account the banks’ failures royal court. Al-Mubarak was central

to achieve appropriate levels of compliance regarding their AML & Sanctions bank governor from 2011 to 2016. He

Compliance Frameworks as at the end of 2019. All banks operating in the UAE was most recently a minister of state and

have been allowed ample time by the CBUAE to remedy any shortcomings and served as the kingdom’s Sherpa during

were instructed in the middle of 2019 to ensure compliance by the end of that year, its presidency last year of meetings of the

informing them that further shortcomings would result in penalties under the Group of 20 industrialized economies. He

Federal Decree Law No. (20) of 2018 and its executive regulation. The sanctions was also previously chairman of Morgan

imposed on Bank of Baroda were of AED 6,833,333. The bank said it been taking Stanley’s Saudi Arabia unit. Saudi Arabia

steps to ensure compliance with the Federal Decree and has been communicating now intends to more than double the size

with the Central Bank. of its sovereign wealth fund by 2025.

4 Banking Frontiers February 2021

Future Lending

App & API drive transformation at SHF

App engages customers and API engages partners:

S

hriram Housing Finance feels that we would target having an interactive

the consumer acceptance of digital kiosk at our key branches that would assist

interaction has evolved considerably the customers,” says Subramanian.

as the pandemic has forced everyone to

fasten the pace of digital engagement with MORE SERVICES VIA CLICK

the consumer. The company’s MD and Shriram Housing Finance is now working

CEO Subramanian Jambunathan says towards offering more services via click

the company was already on the path to of a button, and this is not just limited

evolve as a tech-driven mortgage company, to service. Subramanian says: “We are

where moving away from human interface looking to offer pre-approved loans to

was considered inevitable. “The pandemic our customers for home renovation or

perhaps forced us move faster as consumer purchase of new house which would be

behavior changes were brought in by in a seamless and paperless format.”

environmental factors rather than we

driving those changes. We always believed MULTIPLE DIGITAL TOOLS

that a digital journey would become the Technology is not just limited to

forefront of customer interaction over the customer engagement; it has also

next 3-5 years,” says he. become a critical part of the company’s

customer onboarding process as some

CALL, EMAIL, SMS, WA

Subramanian Jambunathan is of its processes have moved completely

A customer wanting to reach SHF can looking to offer pre-approved digital. Subramanian lists them: “We

do so via a branch visit or writing/calling loans to his customers for home have deployed multiple digital tools for

its contact centre. Branch visit was the renovation or new house doing credit checks to facilitate a quicker

most prevalent mode in pre-pandemic turnaround for our customers. We have

era and Subramanian says more than launched our mobile app amidst the facilitated an online application process

80% of the queries were raised by lockdown in July 2020, and the same for our potential customers. The same can

customers with service representatives has become our go to mode to share be done via our website or our mobile app

at the branches. While the company information with customers. Over the which can be downloaded from Google

facilitated its customers to reach it via last 6 months, we have seen almost 40% Playstore. The KYC checks supporting the

call/email/message, the dominant mode of our customers downloading our app. application and the required documents

continued to be branch visits. “We were Today we have over 7000 of our customers for financial assessment of the applicant

already having a one-way communication using our app, while 2500+ have sent are also carried out online. Add to this,

via SMS/WhatsApp, business with our us at least 1 query over this period. This the fact that a lot of our credit checks are

customers over the last few years where we percentage increases to 50%+ if we look done via API integrations across multiple

would keep them posted on the updates at our customers based in metro cities and service providers, who help us validate

about the company, as well as specific state capitals. However, the big positive authenticity of documents, carry out

updates on the industry news, which for us here is that our customers in non- address checks and property geo-tagging

could impact our customers, such as metro locations have also accepted our for better risk management. There are

interest rate movement, basic updates on mobile app as a new communication multiple other legs of the process as well

house maintenance and upkeep and news mode with us. This is a significant win for which would move digital in the course of

articles on real estate,” he says. us as it helps us build a long-term digital next few months.”

engagement journey with the customer.” All in all, Shriram Housing Finance’s

NON-METRO APP USERS Today, the company can offer similar endeavour is to move as many processes

To make the system more efficient, the services over the app what its contact center and customer interactions to a digital

company worked on launching its mobile offers. Any query raised is responded to format which is the new normal.

app and offer a customer portal on its and addressed within 2 working days. Subramanian adds: “We have made

website. The app launch was planned “This helps us reduce the wait time for significant progress on this over the last

in April 2020, but got delayed due to our customers if they reach out to our call few months, and you would definitely see

the lockdown. center for any query. Since we have also more of it in due course.”

Subramanian updates: “We finally enabled a customer portal on our website, mehul@bankingfrontiers.com

Banking Frontiers February 2021 5

Towards Customer Convenience

Technology helps UCO Bank

regain & retain its brand

Saroj Nayak, GM - IT, speaks about the direction and velocity of digital

initiatives at the Kolkata headquartered PSU bank:

Mehul Dani: How has the digital strategy (DFS), Government of India.

of the bank been implemented in the Percentage of digital (home & mobile

current FY? channel) transactions to total transactions

Saroj Nayak: During the has increased to 69% as of third quarter

unprecedented era of the pandemic, which from 47% as of the first quarter of the

took almost the entire 2020 from us, we current FY. Adoption percentage of mobile

have been able to experience the strength and internet banking among operative non-

of technology. It is established now, BSBD SB account customers in the bank

undoubtedly, that technology is the tool has increased to 20% from 15% during the

which can bridge the gap between demand same duration. Adoption percentage of

and supply or to say between business and mobile / internet banking among operative

consumer. This is more pertinent in the non-BSBD SB account customers in

case of service industry like banks. transaction intensive branches the

We have strengthened our call center bank customers in transaction intensive

so that customers can reach us for any branches of the bank is up from 12% in the

clarification/ enquiry. ‘UCO Sampark’ is first 3 months to 16% in the first 9 months

the IVR based phone banking solution of the current FY.

which provides automated banking facility

to the customers. For walk-in customers, How much business has been garnered

we have introduced lead generation facility Saroj Nayak reveals that UCO online by the bank in the current

through miss call/ SMS / website during Bank aims to provide channel- FY? How have you brought business

pandemic so that customers can submit platform-device agnostic correspondents and agents into the fold

their requests. Our call center executives banking experience to its of your digital strategy?

in turn contact them and help them in customers Digital banking has both tangible and

onboarding. intangible benefits in terms of reduction

We are proud to anchor the ‘PSB cardless withdrawal facility using mobile of cost of delivery of service, improvement

Alliance – Door Step Banking Project’, banking U-Cash. Payments using QR code in customer satisfaction, improvised

which was launched by the Finance scan are also introduced for contactless compliance, etc. We have deployed more

Minister on 9 September. Through this shopping experience. Customers can than 3000 ATMs, cash recyclers and

we are providing array of banking services generate virtual cards using same mobile self-service banking kiosks in addition to

right at the doorstep of the customers, who banking app and use that for e-commerce 10,000 PoS devices and 3500 business

can book it using mobile app/ DSB portal transactions. correspondents with micro-ATM devices

or call centre. In a nutshell, using a single app, a for providing real time transaction facility

retail customer can manage his entire in the remotest villages of the country. With

How have been usage patterns of banking needs right from payment/ fund an active card base of around 10 million

apps, mobile & internet banking, digital transfer to investment, loans, UPI, etc. and 3.2 million m-banking customers,

payments at the bank? Non-customers can use our UCO Pay our customer induced digital transaction

We have taken a number of initiatives Plus app to their saving accounts in real share is approximately 70%. There is a

to offer banking facility to the customers time and also do video KYC. During the visible shift of customers from using the

without requiring them to come to the pandemic, we have introduced ‘Video Life digital platform for business transaction

branch. We have strengthened our mobile Certificate’ facility for pensioners through to gradually shifting towards non-financial

banking application (UCO m-Banking which they were able to submit their life banking services like opening of account,

Plus) by providing additional features certificate online from the convenience of investment in fixed deposit, recurring

like facility to open PPF account, Sukanya their homes. This was a big relief for all of deposit, PPF account, application for

Samridhi account, to apply for loans – them and it was appreciated by all corners advances, etc, through online mode.

home, car, etc. We have already introduced including department of financial services In the payment acquiring ecosystem,

6 Banking Frontiers February 2021

we have more than 150 merchants live UPI & Wallet USERS

600,000 552,346

on our fee collection module. The bank is 535,678

501,279

not only garnering business in the form 500,000

of interchange income and commission 415,333 406,339 415,385

but also through expanding its float in 389,099

400,000

334,476

the business accounts. Online and digital

initiatives have also helped us to retain 300,000

our existing customers who were in

requirement of different digital solutions 200,000

for their business to survive during the

100,000

covid situation and also acquired new

customers on basis of the merchant 0

on-boarding digital products. Mar-20 Sep-20 Nov-20 Dec-20

Who are your main tech vendors and what link to have redundancy of network link at IIM, etc. At the same time our e-learning

are their services? Give details about data every level, covering all the branches and platform is providing on-the-go training to

centre, networking hardware, size of your offices (more than 3300) on pan India basis. our staff members.

IT team and training provided to upgrade The core network is built with devices from

the skill set of staff members. What is the all leading network and security hardware How strong is the bank’s presence on social

capex and opex for digital initiatives by OEMs - Cisco, HP, Checkpoint, Imperva, media? What online marketing efforts have

your bank? Fire-eye, Cyber Ark, etc. been undertaken for the current FY?

Our core banking solution is Finacle The deployment of solutions is both on We have been active on social media

from Infosys. We have engaged leading capex and opex models subject to criticality platforms through our official handles in

technology service providers to deploy of the solution and business model. Recently, Facebook, Instagram, Twitter & LinkedIn.

state of the art, safe and secure technology we have changed our CTS solution from We are engaging social media users with

solutions. It would not be prudent to discuss capex to opex. Thus, it is a constant process different types of awareness posts like

details of our data center, networking and which depends on various factors. We are interest rate updation, digital product

hardware sizing, but at the same time I now even going for a cloud-based solution initiatives for merchants & retail customers,

can tell you that bank has 4 data centers, 2 deployment for non-critical projects. asset & liability product features and cyber

at Bangalore in hosted model for primary We have been managing our CBS and security measures, covid protocol/ best

and near site and 2 at Kolkata in our own DC maintenance through an in-house practices, etc on a regular basis. We are

building working as primary and DR site. team. Our internal software development interacting with more than 50 social media

Our hardware sizing and networking team is continuously developing new users on daily basis on queries, feedbacks or

solution is scalable enough to take care of our software solutions and modules. As part grievances. As of now, we have a Facebook

expansion plan in the next decade. We have of capacity building, we are imparting customer review rating of 4.2/5.

a robust wide area network setup on MPLS training to our staff through premier We have a lead management system

platform with multiple service providers’ institutes like IDRBT, NIBM, BIRD, in place. In the current FY, we have

mainly focused on organic posts and lead

generation from social media. The link for

garnering leads is posted in social media

for interested or prospective customers.

The bank reaches the customers who fill

up the details and converts the leads into

prospects.

Banking has seen a major shift from

manual to digital channels in the last few

years. Now people are more aware of the

uses and advantages of using debit cards

and mobile banking. These initiatives have

also helped our economy to march towards

a less cash mode.

What kind of promotional initiatives are

planned for the next FY? To what extent

Banking Frontiers February 2021 7

Towards Customer Convenience

technology will be an enabler in the Mobile Banking MPASSBOOK USERS

foreseeable future for your bank?

3,500,000 3,205,992

We are also going to enter the virtual 3,048,707

market with our products and offer 2,800,602

3,000,000

better convenience and experience to our 2,322,608

2,500,000 2,165,330 2,257,036

prospective customers. In the next FY, we 2,084,959

will extensively work towards brand and 2,000,000 1,673,266

performance campaigns. Covid and post

covid situation has also added up towards 1,500,000

digital banking like introduction of video 1,000,000

KYC, applying of virtual debit cards through

mobile banking. We have always been a 500,000

pioneer in digital banking initiatives in the 0

banking industry with our award-winning Mar-20 Sep-20 Nov-20 Dec-20

mobile applications. Hence, technology has

enabled us to regain and retain our brand as predictive analytics to identify the products Finacle 10.x. This will help us to strengthen

a digital friendly bank and with the further or services that customers are most likely our core capabilities and technical platform.

advancement and adoption of technology, to be interested in for their next purchase) Finacle 10.x is built around API support

we will definitely work towards more and locational intelligence already provide system which opens up the door to limitless

digitization. the said data. API based integration. At the same time,

we are upgrading our e-banking solution

How have you gained by deploying How is your bank involved in partnering, platform, which shall be our step towards

analytics to increase business? How investing and supporting fintechs and creating a digital hub. We target to provide

is technology put to use for customer startups? channel agnostic, platform agnostic and

relationship management (CRM)? What We have tie-ups with some of the device agnostic banking experience to our

are you doing to enhance customer leading fintechs for introducing best of customers. In seriatim, our endeavour is

experience? technology solutions, innovative business to introduce new loan originating system,

Data analytics is a very important tool reengineering ideas and last mile delivery which will ultimately provide an end-to-

in banking industry, with vast structured products; with an overall target of enhanced end solution to the customers to apply,

and unstructured data generated by many customer convenience, improving business track and avail credit within defined

devices in various platforms can provide processes, proper compliance and of course turn around time as per their needs from

stupendous insight. With banking products optimization of cost of delivery. Services being anywhere, anytime. We understand that

becoming increasingly commoditized, availed through these fintechs are primarily in the current era of generation Y, where

analytics can help banks differentiate related to fetching outside world reports millennials are the largest customer

themselves and gain a competitive edge. on topics like GST, financial statements, base, banking anywhere and anytime

Banks in the past have been reluctant analysis of balance sheets, analysis of bank is the key towards successful customer

to employ analytical tools due to legacy statements, CIBIL report, PAN verification, engagement. In this direction, we are

data and its accuracy. In line with other business correspondent services etc. going to bring ‘banking on the go’ through

public sector banks, we use analytics In order to manage this journey of our innovative kiosk solution. Recently,

at a very limited level. But with regular onboarding fintech companies and to we have launched ‘Green Channel Kiosk

data cleaning and advanced tools in data choose the worthy projects out of number Banking Solution’, wherein customers can

analytics, we may employ analytical tools of startups, we have adopted a board avail self-service within the branch premise

in full use in the near future. approved fintech policy, which covers the as well. Further, we have to integrate with

Analytics can provide banks like ours entire gamut. We are quite optimistic that social media platforms and increase our

with more marketing muscle. Functional our tie-ups with suitable partners will help footprint on these growing channels to tap

areas like risk, compliance, fraud, NPA us to achieve both economy of scale and the customers and also to provide banking

monitoring, and calculating value at risk economy of scope at the same time. wherever they want. Artificial Intelligence

can benefit greatly from analytics to ensure and Machine Learning are the technologies

optimal performance, and in order to take In the post covid- scenario, what are your which are going to be the driving force for

crucial decisions where timing is very targets and plans for IT, digital initiatives change of face of banking in coming years.

important. The use of analytics can help in the current FY and what is planned for While the list is endless, our vision is

banks like ours differentiate themselves the next FY? clear. To offer convenient, cost effective,

and remain competitive in the future. We are in the process of upgrading our consumer friendly technology solutions.

Solutions like ‘Next Best Offer’ (the use of core banking solution from Finacle 7.x to mehul@bankingfrontiers.com

8 Banking Frontiers February 2021

Cartoon

Engaging Regulators & The Dependable App Shielding Strategy

Enhancing Possibilities

Joseph Cleetus

Head of Business

Transformation Mathan Babu

Lulu International

Exchange Pinakin Dave Kashilingam

Country Manager, India CISO & Data Privacy

Summary: Joseph Cleetus & SAARC, Onespan Inc Officer, NPCI

cites the strong support

from regulators and their

Summary: App-based payments have

changing outlook in being

revolutionised digital payments but at the same

more supportive, business

time frauds too have equally shown a high growth

savvy and based on an in-depth

trajectory.

understanding of technology.

Banking Frontiers February 2021 9

Agriculture

`1.76 tn sanctioned to farmers via 18.7mn KCCs

1 8.70 million Kisan Credit Cards (KCCs)

with credit limit of `1.76 trillion have

been sanctioned to farmers across the

documentation, built-in cost escalation

in the limit, any number of withdrawals

within the limit, etc. In order to ensure

country up to 29 January 2021 during that all eligible farmers are provided

the special drive going on since February with hassle-free and timely credit

2020, as per information furnished by for their agricultural operations, the

public sector banks and NABARD. Government runs the KCC Scheme,

Anurag Singh Thakur, Minister of which specifically enables the farmers

State for Finance & Corporate Affairs, to purchase agricultural inputs such as

states that the KCC Scheme has been seeds, fertilizers, pesticides, etc. The total

simplified further, which has the coverage numbers of KCCs issued in the

provision of ATM enabled debit card country are 18.08 million with credit limit

with, inter alia, facilities of one-time of `1.68 trillion as of 8 January 2021.

One District, One Product cluster for better processing, export

T he concept of ‘ ‘One District

One Product’ cluster is aimed at

promoting specialization and better

Corporation Limited (NERAMAC), Tamil

Nadu-Small Farmers Agri-Business

Consortium (TN-SFAC), Small Farmers

current year for formation in 115

aspirational districts in the country.

NAFED will provide market and

processing, marketing, branding and Agri-Business Consortium Haryana value chain linkages to the FPOs formed

export of agri products. Agriculture value (SFACH), Watershed Development by other implementing agencies. NAFED

chain organizations are forming FPOs Department (WDD)- Karnataka & has formed and registered 5 honey FPOs

and facilitating 60% of market linkages Foundation for Development of Rural during the current year in Uttar Pradesh,

for members’ produce. Value Chains (FDRVC)- Ministry of Madhya Pradesh, Rajasthan, Bihar and

Under this central sector scheme Rural Development. West Bengal.

with funding from Government of India, The implementing agencies will engage FPOs will be provided financial

9 implementing agencies have been Cluster Based Business Organizations assistance up to `1.8 million per FPO for

finalized for formation and promotion (CBBOs) to aggregate, register and a period of 3 years. In addition to this,

of FPOs - Small Farmers Agri-Business provide professional handholding support provision has been made for matching

Consortium (SFAC), National Cooperative to each FPO for a period of 5 years. equity grant up to `2,000 per farmer

Development Corporation (NCDC), During 2020-21, a total of 2200 FPO member of FPO with a limit of `1.5

National Bank for Agriculture and Rural produce clusters have been allocated, million per FPO and a credit guarantee

Development (NABARD), National which also include specialized FPO facility up to `20 million of project loan

Agricultural Cooperative Marketing produce clusters such as100 FPOs for per FPO from eligible lending institutions

Federation of India (NAFED), North organic, 100 FPOs for oil seeds etc. Of to ensure institutional credit accessibility

Eastern Regional Agricultural Marketing these, 369 FPOs are targeted during to FPOs.

World Bank’s SMART Project to transform 10,000 villages

M aharashtra Government has

launched the World Bank assisted

State of Maharashtra’s Agribusiness and

access to new and organized markets for

producers and enhance private sector

participation in the agribusiness. The

to channelize farm produce.

The project is a giant step towards

transformation of rural economy and

Rural Transformation (SMART) Project to project will be implemented in 10,000 empowerment of farmers and also

transform rural Maharashtra. This project villages in the state with an objective sustainable agriculture through public-

aims to revamp agricultural value chains to achieve sustainable farming within private partnership. It seeks to ensure

in post-harvest segments of agriculture, next 3 years. It will cover almost one- higher production of crops and create

facilitate agribusiness investment and fourth of Maharashtra. Its focus is on robust market mechanism to enable

stimulate SMEs within the value chain. villages which are reeling under worst farmers to reap higher remuneration for

It will also support resilient agriculture crisis compounded by lack of the yield.

agriculture production systems, expand infrastructure and assured value chains mehul@bankingfrontiers.com

10 Banking Frontiers February 2021Future Banking

2021: Cloud Trends for the BFSI Sector

Cloud is going to be a crucial factor in BFSI operations of the future:

A

s we graduate to a world shaped placate regulators. In India, there are

by physical distancing, banks and ways that the cloud can resolve regulatory

financial institutions are adapting compliance. For example, in 2020, NPCI

and innovating too. For firms looking to rolled out more than 20 circulars relating to

recover in the short-term and accelerate UPI, requiring bank compliance. Keeping

their growth trajectory in the longer term, up to these circulars is a significant task for

technology-fuelled experiences can help all the banks and the cloud can help keep

them compete, ramping up services and up with the regulatory mandates.

profitability while reshaping customer While it will be a gradual shift over the

experiences. In this scenario, banks must next 5 years, I would hope banks can reduce

focus on internal IT operations and systems overheads, which restricts their ability to

to ensure operational integrity. innovate, by working with cloud providers

This is where the power of the cloud and regulators to automate and simplify

will come in. Core legacy systems can pose activity through increased transparency.

challenges to Indian banks due to lack of

flexibility, agility and ease of integrating Long live the marketplace

with external systems. Coupled with the Ciaran Chu platform

plethora of changes in the UPI space, banks One of the greatest drivers of cloud within

are constantly looking at new partnerships became the norm. As a result, in 2021 we India’s BFSI sector will be the need for banks

with emerging fintechs. In doing this, banks will see banks increase expenditure on to diversify their revenue models from fee-

today incur heavy operational overheads process simplification and improvements – based transactions (where it is a race to zero)

to continue to run and maintain legacy something that the cloud can deliver. to new client-based services. India’s banks

systems. Future-proofing of core systems is face eroding revenue as Merchant Discount

definitely the need of the hour. Changing relationship Rate (MDR), Merchant Service Fee (MSF)

In 2021, cloud will command vital between data regulation and other charges such as interchange are

infrastructure for India’s banking and and innovation highly regulated – highlighting the need

payments sector, enabling agility, improved With changing geopolitical dynamics, to diversify. For example, with Google

remote collaboration and faster application we will see increased focus around Pay or WhatsApp Pay, banks acquire new

development and deployment. data sovereignty and consumer safety, customers on channels outside of their own

Outlined below are the 3 big cloud as consumers seek to understand how at a much lower cost to what they would

trends that ACI Worldwide sees having precisely their data is being used and have incurred the traditional way. Once

the biggest impact on India’s BFSI sector governed. Big cloud providers will continue they have these new customers, it opens

in 2021: to canvas and work with regulators to find up new cross-sell and up-sell opportunities

common ground on the best way to run for the bank; they could sell a loan product

Revaluation of operational their infrastructure long term. WhatsApp or a credit card. In fact, Indian banks are

control processes is a good example on how not only banks partnering with fintechs to provide instant

One of the big challenges of cloud adoption but fintechs and bigtechs are also striving credit, so it does open up new avenues of

pre-covid was the amount of operational hard to comply with regulatory norms in income for the banks, and it is instrumental

overhead and risk acceptance knowledge India. WhatsApp had to put its UPI launch to their overall payment strategy.

required to migrate workloads from on hold for over a year to comply with RBI’s While some Indian banks are still ‘on

on-premises to the cloud. Alongside was the data localization requirements. Banks on the fence’ when it comes to shifting to the

fact that many banks had in place arduous the other hand invested in upgrading their cloud – whether in a pure cloud, hybrid

control processes that were difficult to systems to support the massive transaction or multi-cloud model – the benefits are

overcome. Due to the pandemic, banks have volumes that WhatsApp was expected to making it increasingly attractive. It is only

realized that many offshore resources that bring in. a matter of time before the cloud will be

were maintaining systems could not log in Regulators in the past have stood in viewed less as an option and more as a

from home, causing a risk issue. Banks were the way of innovation, in part due to a business imperative by the banking and

forced to re-evaluate these processes to lack of understanding of the competitive payments industry.

ensure they were fit for purpose in this new landscape. Banks would end up spending Ciaran Chu, Practice Leader - Public Cloud,

world, where physical distancing quickly more on maintaining the status quo to ACI Worldwide

Banking Frontiers February 2021 11Digital Transformation

Powered by E.T.C.

StashFin has adopted Engineering, Technology and Culture practices

from bigtechs to fuel its digital acceleration:

S

tashFin, being a digital lending incorporating into its products or for

venture, has since 2016 been enhancing the work environment at the

dedicated to transforming the organization. Parikshit says a perfect

traditional lending system by providing example of this approach was seen during

customers with a flexible credit line card, the lockdown period where the company

using a fully digital journey. Parikshit successfully deployed a state-of-the-art

Chitalkar, Co-founder, says this has work from home (WFH) infrastructure

been made possible by the company’s based on a cutting-edge technology like

relentless drive towards digitization DNS/Layer 7 VPNs and achieved 100%

of traditionally manual processes and work efficiency for all employees in record

employing advanced technology-based time. “We are elated with what our team

strategies to offer an unmatched level of of passionate Stashers has achieved and

convenience as well as financial freedom we are completely focused and invested

to the customers.” in our human capital for the long run.”

CASH ON CARD BY APP ANALYTICS SOLUTIONS

When covid struck, StashFin accelerated StashFin has deployed analytics to

the pace of adoption of digital technologies either increase revenues or improve the

in its internal processes. When faced with Parikshit Chitalkar intends to customer experience. Parikshit explains:

the constraints of the lockdown, its teams make lot of capital investment “Given our size, the fact that we have

were forced to look at each process, find in Artificial Intelligence built, deployed and now manage over

fully digital alternatives and develop a 70 applications in production is pretty

solutions

completely online WFH suite for every commendable. People are often taken

employee. Parikshit pats his team for is part of our engineering, technology by surprise by the extent of our builds,

having risen to the challenges of a post- infrastructure and data science teams, especially coming from such a small

pandemic world and posting growth who in turn work on AI, machine learning team. We are big proponents of adopting

in all aspects of the business. “Today, and cloud technologies dedicatedly.” not only the latest technology trends but

our systems handle disbursal volumes Early on, StashFin made the decision also nuggets of engineering culture from

of 100+ loans an hour. Our credit line to keep all its technology buildouts the likes of Facebook and Amazon, which

card customers can load cash on their in-house and that has paid dividends we have been able to learn through our

cards in a matter of 90 seconds from the over time. “This provides us with a key investor network.”

StashFin app, with the freedom to use it competitive advantage in terms of agility StashFin starts with the 3 aspects of

24x7 whenever and wherever they please and the ability to innovate. ‘Stashers’ analytics it builds on - credit risk, process

to,” says he. (as we call ourselves internally) love optimization and data visualization.

it because they get to work on novel “Underlying is a strong data pipeline, and

OUTPACING THE VENDOR technologies, in sync with the business, we try to drive a full data democracy where

StashFin has managed to embed various and witnessing tangible results almost people and models alike can get all the

technologies into its app and website. It instantly. It has helped us build a culture data they want, real time,” says Parikshit,

has preferred to have a dedicated team, that is unheard-of in traditional software adding: “We are now working on building

rather than outsourced vendors. Reveals development teams,” he says. self-reinforcing models. We are in the

Parikshit: “We have a 100% in-house business of ingressing large volumes of

technology and data science team DEEP TECH PARTNERSHIPS data and use it to make decisions, which

that gives us the flexibility to integrate StashFin does have deep technical results in value for our customers and

solutions into our products and services partnerships with the likes of AWS, teams alike. To facilitate this paradigm,

within a fraction of the time it would Google, Cloudflare and NewRelic we look at data in 4 distinct categories -

take a vendor to do so. In fact, of the wherein it uses their resources to data infrastructure, credit risk analytics,

200+ employees we have today, 40% develop proprietary solutions either for process analytics and data visualization.

12 Banking Frontiers February 2021Each has a separate team with a clear in India, it is still in uncharted waters,

mandate.” as a country that is far ahead in many

Considering that all its products are dimensions. For example, the payments

exclusively digital, analytics has played revolution brought by UPI. There

a key role in rapid growth and success. is nothing similar in terms of user

The company has developed custom experience, technological complexity

analytics solutions, data pipelines, model and scale exists anywhere in the world,

pipelines and data visualization systems he says.

to understand its customer base and the It is imperative that StashFin remains

credit requirements and utilize those on the cutting edge of technology and data

insights to drive business volume growth sciences while employing best business

vide a superlative customer experience, practices. It stays committed to its goal

all the while minimizing credit and of introducing India to a new paradigm

default risk. The teams depend on hard of financial services, rapidly progressing

data to make day to day decisions, thus towards digitization of services with

equipping them with real insights into financial inclusion as the ultimate goal.

customers’ concerns and the ability to “This makes it imperative that a bulk

offer them practical solutions to resolve of our learnings must come from within

these concerns. All in all, it looks at both - via experimentation and continuous

internal and external customers in the customer feedback,” says Parikshit,

same light and hopes to add value to their explaining further: “A lot of our capital

lives at every step of the way. investment will primarily be in Artificial

Intelligence (AI) this year, especially on

LOW ATTRITION, WANT TALENT developing solutions using computer

It’s a very satisfying experience for a young vision technologies and building neural

engineer to build a feature in a couple networks for advanced fraud detection.

of days, deploy it in production, watch We have been fine-tuning our Machine

how customers interact with the feature want to participate in our growth journey Learning (ML) models for credit risk

live sitting with the sales and customer by living the values and ideals that are the assessment over the last year and will

support teams. Parikshit elaborates: bedrock of our organization’s success over now deploy these on a larger scale to serve

“This kind of exposure unearths their the past 5 years,” he adds. a broader segment of customers. We will

true potential transforming them from also be expanding our mobile footprint

just being coders to technologists who TECH-LED GROWTH to provide a larger bouquet of services to

can solve real business problems with StashFin offers loans in the range from our customers.”

code, one of the many reasons why we `500 to `500,000 with repayment mehul@bankingfrontiers.com

have very low attrition. We are open to periods ranging from 3 months to 36

new talent who share a similar zeal, thirst months. Its interest rates are from

for learning and want to participate in 11.99% APR (Annual Percentage Rate).

In Pursuit of

our growth journey.” But the rates may vary from case to case. Business Niche

StashFin likes to celebrate wins and All loans are repaid through EMIs via

pay credit where it is due, and high electronic payment system. Parikshit

performing individuals are rewarded adds: Over the last financial year, we had

and recognized. “Every Stasher or recorded rapid growth. This growth has

potential employee is egged on to find been brought about by the unrelenting

their fit in our lithe organization - be it focus on technological innovation, Ashutosh Singh

sales, tech, operations, customer service unmatched customer experience and CEO,

NSDL Payments Bank

or field executions and collections,” risk management. It required us to scale

says Parikshit. “We realize that tacit our systems and we are now looking to Summary: Ashutosh

knowledge and the right attitude is scale our teams in sync with the growth Singh mentions that

critical to a Stasher’s success, hence we opportunities ahead.” despite the constraints of

a payments bank, NSDL

promote a lot of lateral movement within

Payments Bank uses the

the organization. However, we are always IT, DIGITAL PLANS opportunities that it has and the USPs

open to new talent who share a similar Parikshit is of the view that when it of its offerings.

zeal, thirst for learning and who would comes to financial technology revolution

Banking Frontiers February 2021 13Efficient Controls

Minimizing Risks with Gig Workers

Sonal Patni, CTO at SMEcorner, a new age fintech lender, discusses the

security risks when working with gig workers:

Mehul Dani: What kind of risks can have access to those areas, and no more.

originate from gig workers? Assign only those roles to gig workers.

S o n a l Pat n i : C o m p a n i e s a r e

increasingly hiring gig workers to address What should be the correlation between

the evolving needs of their business. Gig regular employees and gig workers?

economy workers often need extensive Educate regular employees of the

access to the company’s systems and as a need to protect sensitive data. Your

result, can open up a number of cyberattack regular employees will provide guidance

vectors. This needs to be handled carefully. and mentorship to gig workers. Let your

Unlike a controlled network and in-house employees know about the restrictions on

employees, gig economy workers can’t be systems and data access. Inform them how

subjected to strict security oversight and the they can help out gig workers and the type of

security needs to adapt to the new threats data that is appropriate to share with them.

posed by the gig economy workers. Internal Put regular employees in place who

threats are a rising security concern among can guide, train and mentor gig workers.

enterprises, malicious insiders are viewed In addition to answering questions

as one of the top cyber threats across the Sonal Patni

and assisting with workplace tasks and

enterprise today. practices, they can also keep an eye on

how gig workers access and use data. Get

How can one mitigate the elevated risk measured to ensure there are no untoward them to gently guide gig workers in best

that gig economy workers bring in? incidents which can compromise security. practice for accessing and using business

Organizations need to have strict Your data needs to be properly segmented, and customer information.

security protocols in place to properly so that gig workers do not have access to

mitigate the elevated risk that this entails. your entire dataset but only to what they How can one restrict access to gig workers

Managing sensitive business data when need to carry out necessary tasks. Also, it to sensitive locations in the business?

you’re using gig workers can be a delicate is necessary to audit the data your business Make sure that you have proper access

balance. While you need to protect holds and assign it a sensitivity. controls in place for various parts of your

confidential business and customer business. For example, restrict access

information, workers need access to the What can an enterprise do to protect into server rooms or data centers. Use

right data and systems so they can do their customer, user and business information biometrics and other access devices to limit

job properly. Even with a strong security while making gig workers a useful and gig workers to where they need to be, and

framework in place to help safeguard data flexible part of its workforce? nowhere else.

from external hackers and threats, an influx When you onboard gig workers, make

of gig workers can open the door to new sure you educate them and share policies What should be done to know how gig

vulnerabilities right within the walls of an around data management and data workers are accessing data and systems?

organization. handling with them and have them sign up You can put auditing in place to check

to receiving this information. Make your what gig workers are doing on company

To what extent should access to company’s policies available to all your gig workers at systems. Your policies should state that you

systems be granted to gig workers? all times. Access to policies and guidelines may audit computer and data usage. Each

A gig economy worker should be around data handling is a must. access to the system should be logged and

provided with controlled access to only what every asset accessed must be measured to

he needs as opposed to a sweeping access How should one create roles for gig ensure there are no untoward incidents

to everything. Companies should employ workers with limited access rights? which can compromise the security of the

biometrics, multi factor authentication Every gig worker you take on will be organization. You can incorporate these

and just-in-time provisioning to reliably performing a specific role. Look at the suggestions one by one into your cyber

authenticate gig economy worker and responsibilities and tasks that role will security policies to gainfully employ gig

provide controlled access to the corporate carry out and decide what data, systems and workers and secure your business against

network. Each access to the system should software they need to access. Create only unwanted data issues.

be logged and every asset accessed must be those specific ‘roles’ in the network that mehul@bankingfrontiers.com

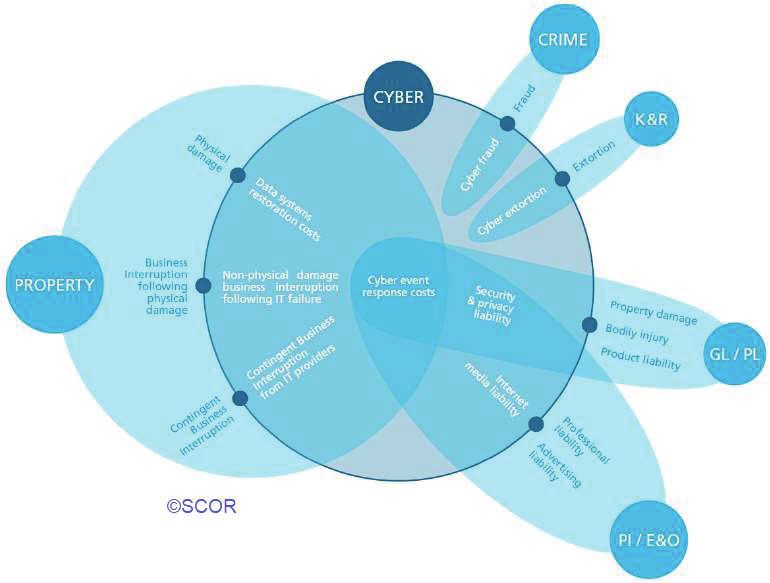

14 Banking Frontiers February 2021Cyber Insurance coverage. This is also known as “unintended” or “non-affirmative” cyber cove

Cyber exposure is a concern for all underwriters. Cyber affirmative and silent co

Detailed regulations in cyber insurance mooted are scattered in many different products beyond Standalone ones. Cyber

permeates all classes of insurance without boundaries of industries. A cyber even

trigger losses across various lines of insurance – property damage and bus

interruption resulting from computer systems failure / virus under property insura

siphoning money through phishing under crime insurance, product liability / recalls

The Working Group constituted by IRDAI suggest several steps to security vulnerabilities under product liability / recall insurance, breach of cont

enhance coverage under cyber insurance: negligence claims under E&O insurance and for managerial negligence under

insurance (FedEx case).

T

he Working Group set up by and every year new cyber incidents are

the Insurance Regulatory and carried out on specific targeted industries.

Development Authority of India During NotPetya and WannaCr y,

(IRDAI) to study cyber liability insurance healthcare, logistics, and manufacturing

has suggested that with unknown cyber risks establishments were targeted; during

on the rise, there must be detailed regulations covid, pharma companies and schools were

to address the issue. It says in its report: targeted. Coverages are evolving, more and

“Insurers may place this matter (silent cyber more demands would evolve in medium

issue) high on the agenda and address this term based on new discoveries about these

problem sooner than later. Silent cyber refers incidents. All these demand that cyber

to the unknown exposure in an insurer’s insurance underwriting teams invest more

portfolio created by a cyber peril, which has in cyber knowledge to build expertise The report specifically states that since

not been explicitly excluded or included.” to properly develop and manage their Affirmativeis

the attack usually targeted at multiple web

cover:

Covered through cyber specific policies for the coverage as mentioned ab

The report further elaborates: “Cyber portfolio,” observes the report. users/content users and the said condition

exposure is a concern for all underwriters. Non-affirmative cover:in the coverage, insurers

again leaves a gap

Policy explicitly does not exclude or include coverage. This is also know

Cyber affirmative and silent covers are SOME RECOMMENDATIONS may remove reference to targeted intrusion

“unintended” or “non-affirmative” cyber coverage.

scattered in many different products beyond The report states that cyber risks are not and extend cover as long as it is unauthorized.

When cyber insurance was introduced in the 1990s, the focus was on covering

standalone ones. Cyber risk permeates all static and therefore cyber insurance covers Besides, cyber insurance policies exclude

breach exposures in response to regulations framed by authorities in USA and Eu

classes of insurance without boundaries cannot be static. It is necessary therefore anybusiness

Later, with actualoperations

or alleged bodily

getting injury,

more digital and sickness,

owing to spread of all-perv

influence of information technology, insurers started offering wider coverage. But

of industries,” it says, adding: “With that as the market evolves in response to disease or death of any person howsoever

Report of the Working Group to study Cyber Liability Insurance

technology improving and digital business the emerging needs, the scope of the cyber caused Property Damage and any damage

expanding, silent cyber risks, especially in policy needs to be enhanced. The working to or destruction of any tangible property,

the banking sector, have also increased.” group therefore recommends several steps including loss of use thereof. “With absolute

and covers to facilitate the development cyber exclusions under other policies

GAPS NEED TO BE BRIDGED of a resilient and robust cyber space, becoming increasingly common, there is a

The working group feels that while the both in the short and medium term. Key need to cover cyber incident triggered bodily

current offerings are addressing the recommendations among these are: injury and property losses, so that they do

requirements of individuals reasonably Insurers may place the topic of Silent not fall in a no man’s land,” it says.

well, there are a few gaps, some of them Cyber high on the agenda and address this

relating to product features and the others sooner than later. In simple words, it is QUESTION OF STANDARDIZATION

to processes involved. It says while it may when the policy explicitly does not exclude The working group believes it is neither

not be possible to address all these gaps, or include coverage. desirable nor possible to standardize the

attempts can be made, in respect of some Insurance cover may respond either cover at this juncture. “Nevertheless, insurers

gaps, either to respond fully or partially. by affirmative cover, which means covered can build in certain minimum covers as a part

The report says coverage for losses through cyber specific policies for the coverage of individual cyber insurance. The attached

due to cyber incidents can be categorized or through non-affirmative cover where the model policy wording can be considered by

by differentiating between losses borne as policy explicitly does not exclude or include the insurance industry as a reference point

a direct result of the incident (First party coverage. This is also known as ‘unintended’ to provide minimum basic coverage,” it said.

coverage), and losses incurred as a result of or ‘non-affirmative’ cyber coverage. Cyber insurance product is in a

litigation by alleged injured parties (Third development phase, and standardization of

party coverage). It also provides coverage COMPREHENSIVE COVER the cyber policy wordings for individuals may

for other services. The working group emphasizes that insurers hamper the developments of this product

must work towards offering comprehensive in Indian market. It is important now to

UNCERTAINTY ON COVERS solutions rather than mere loss mitigation focus on popularising the cyber insurance

The working group finds that there is products, not only as a customer friendly product, make it easier for insurer to adapt

significant uncertainty in the market on initiative but also as a good risk mitigation the product as per the customer requirements

covers to be bought, appropriate limit measure. Insurers should strive to bring and continue to enrich customer’s experience

purchase, and taking right deductible. clarity to coverage on fines and penalties and protection, the working group said.

“Attacks on establishments are increasing which remains unclear at this moment. mohan@bankingfrontiers.com

Banking Frontiers February 2021 15You can also read