Strengthening Agricultural and Market Value Chains - by Chuma Ezedinma UNIDO-Regional Office-Nigeria November 2015

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Strengthening Agricultural and Market

Value Chains

by

Chuma Ezedinma

UNIDO-Regional Office-Nigeria

November 2015

1

Agriculture/Market Value Chains

Agriculture value chains empowers farmers to

shift from subsistence farming to an

entrepreneurial business, it gives them the tools

they need to take ownership of the process and

build sustainable markets.

Market-oriented agriculture encourage farmers

to invest in their fields in order to increase yields

while decreasing production costs.

The input value chain encompasses those

involved in the steps leading up to the harvest.

These include agro-dealers, who sell farmers

agro-inputs and provide information on their use

or producer organizations that help farmers

learn more effective farming techniques.

The output value chain encompasses all the

steps that an agricultural product takes, from its

point of origin to the consumer.

2

Typical organizational Value Chain models

Model Driver of organization Rationale

Producer-driven • small-scale producers, especially when • access new markets;

(Association) formed into groups such as associations or • obtain higher market price;

cooperatives • stabilize and secure market position.

• large scale farmers.

Buyer-driven • processors; • assure supply;

• exporters; • increase supply volumes;

• retailers; • supply more discerning

• traders, wholesalers and other traditional customers – meeting market

market actors. niches and interests.

Facilitator-driven • NGOs and other support agencies; • ‘make markets work for the poor’;

MARKETS, IFAD, etc • regional and local development.

• national and local governments.

Integrated • lead firms; • new and higher value markets;

• supermarkets; • low prices for good quality;

• multi-nationals. • market monopolies

3

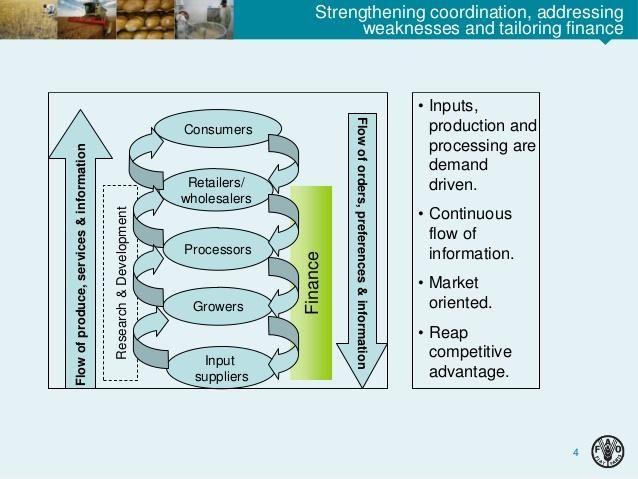

1. Value Chain: Improving Coordination, Cooperation and Efficiency

Farmer Cooperation in Agricultural Production

With too many small scale farmers at the agricultural production level,

cooperation is key to improve marketing power

5

2. Cost Reduction Strategies at the Farm Level:

Example in Cassava Production

35

100% 13.6% 11.6% 27.9% 40.5%

29.4

30 Use of Improved

25.4 26

25

21.2

inputs and

17.5

US$/ton

20 mechanization is

15 the key to

10 improve

5 efficiency at the

0 farm level

Traditional Improved Mechanized Mechanized Mechanized

system varieties planting planting and planting

harvesting &harvesting

&improved

varieties

3. Improving Value Chain Financing

Buyer Driven

Model

Commercial Banks /Financial institutions prefer to support small farmers where the

market risks can be controlled

9

Ware House Receipt Model

10

Regional Office Nigeria 2015 Retreat

4. Innovative Financing is key to growth in modern agro

food value chains

Significant gaps in financing systems

Financing working and investment capital for input supply,

non-farm assets, and industrial property has to be at core of

financing agenda for industrial development

Multiple financial products to meet emerging needs e.g.

timeliness, low cost (< 5%) and long term (15 – 20 year) loans

for internal and external infrastructure development in agro

industrial parks

Strengthen risk assessment and lending criteria

Adopt modern technological innovations to improve financing services

11Using ICT to improve Agricultural Financing

1 1. Abara Obodo 9. Nsukwa.

2. Abudu 10. Onicha Ugbo

3. Afor Ozoro 11. Onuobo

4. Edum Afor 12. Oyoko

5. Igbesi 13. Utenim

2 6. Iselle-Uku 14. Ebelleh

7. Koko Junction 15.Ogwashi-Uku

8. Nkwo Uromi 16. Ukokpo

3

4

Agbor

5

6 20% 40%

7 Asaba

Onitsha

10%

8

40%

70%

9

M-PESA, originally designed as a Umunede

system to allow microfinance-loan 10

repayments to be made by phone, 11 No. Market Name Agbor Asaba Umunede

reduces the costs associated with

1. Abara Obodo 25% 25% 50%

2. Abudu 20% 20% -

3. Afor Ozoro 50% - -

handling cash and making possible 12 4.

5.

6.

Edum Afor

Igbesi

Iselle-Uku

30%

30%

100%

10%

20%

-

40%

50%

50%

lower interest rates. 13

7.

8.

9.

Koko Junction

Nkwo Uromi

Nsukwa.

30%

30%

20%

20%

20%

30%

20%

50%

40%

10. Onicha Ugbo 20% - 40^

11. Onuobo 40% - -

It has been broadened to become a 14

12.

13.

14.

Oyoko

Utenim

Ebelleh

20%

20%

-

10%

20%

20%

30%

40%

30%

general money-transfer scheme in 15 16

15.

16.

Ogwashi-Uku

Ukokpo

-

-

10%

30%

60%

50%

Kenya.Marketing

Marketing is a business function that identifies consumer needs,

determines target markets and applies products and services to

serve these markets. It also involves promoting such products and

services within the marketplace.

Marketing is integral to the success of a business, large or small,

with its primary focus on quality, consumer value and customer

satisfaction. The "Marketing Mix" Strategy is a tool made up of four

variables known as the "Four P's" of marketing.

Products are the goods and services that your business provides

for sale to your target market. In developing a product consider

quality, design, features, packaging, customer service and any

subsequent after-sales service.

Place is in regards to distribution, location and methods of getting

the product to the customer. This includes the location of the

business, shop front, distributors, logistics and the potential use of

the internet to sell products directly to consumers.

Price concerns the amount of money that customers must pay in

order to purchase your products. There are a number of

considerations in relation to price including price setting,

discounting, credit and cash purchases as well as credit collection.

Promotion refers to the act of communicating the benefits and

value of your product to consumers. It then involves persuading

general consumers to become customers of your business using

methods such as advertising, direct marketing, personal selling

and sales promotion.

13Branding and Packaging are important

Market Information: Strengthening Value Chains with ICT

Using ICT to improve access to markets

15Impact of ICT – Mobile Phones Reduces logistics and transportation costs. Farmers obtain the latest information with a phone call instead of making a long trip to a market. Helps in collection, aggregation and delivery. Improves negotiation power. Farmers’ increase their power to negotiate, particularly with traders, based on their ability to understand pricing in multiple markets, to cut out intermediaries, and to sell directly to larger-scale buyers. More sophisticated marketing plans based on price information. For example, farmers can modify the date of marketing, product permitting, or switch to alternate markets, transport and regulation permitting. Broader and deeper networks. Farmers communicate by phone with traders and farmers outside of their immediate geography as opposed to making a physical trip. The ability to communicate more easily and to triangulate information creates deeper trust in key trading relationships. Innovative partnerships. partnerships are facilitated and built among groups of producers, or by virtue of direct communication with corporations and traders, or through the ability to supply product based on just-in-time and/or quality needs. Informed use of inputs. Farmers can identify sources of inputs, obtain them more cheaply, and are better able to buy and apply them at the optimal times. Need to improve the Growth Improves farm business management through better information Enhancement Support (GES) about which inputs to use, new knowledge about grades and standards for produce, and increased interaction with corporations, Scheme and the E-Wallet System traders, and other farmers.

The Challenge to Agribusiness Sector Development

Existing and intending Agro-

72%

industrialists blame poor access to

Infrastructure, Finance, Secure

Feedstock Supplies and exacting

56% 55% Operational Environment

53%

45%

39%

28%

24%

19%

5%

Infrastructure Financing Securing Policy & Regulatory Human Capital Governance Information & Land Government Competitive

Supplies Communication Coordination Environment

Environment

Note: Data from 75 investors; 1Respondents have cited all challenges that are applicable to them

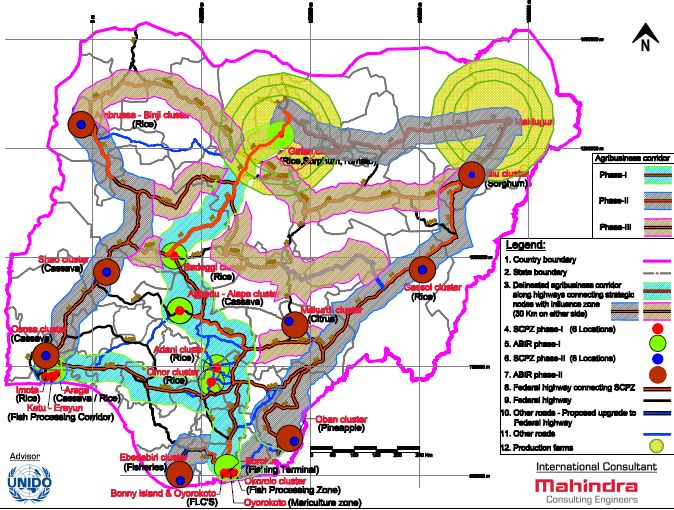

17Agro Industrial Clusters:

……. a new agricultural investment framework

Shift agriculture from

government

controlled to private

sector led

To stimulate

Transform the

private sector agricultural financial

investments to landscape

drive a market-led

agricultural Channel investments

in infrastructure and

transformation services

Strengthen the policy

and investment

climateSCPZ

Delineated area,

typically 250 ha.,

dedicated to driving the

facilitation of modern

processing capacity

ABIR

The immediate SCPZ

production neighborhood,

typically 30-50 km radius,

• constitutes the host

communities

• critical to ensuring

adequate feedstock

supplies

19Business Plan

Description

Focus crop Rice

Beans, Cassava, Cocoyam,

Additional crops Maize, Melon, Groundnut and

Yam

Raw materials required for the

638,424 MTPA

SCPZ

Growing area required 137,745 hectares

Total area of SCPZ 256.01 hectares

Combined SCPZ Development Investment Opportunity1

Site Management: Utilities, roads, and

agro-specific infrastructure

Investment

Power: Bioenergy and distribution

Opportunities

Water: Well and pump house, pumping

and treatment, and distribution

Initial Combined

$27.71 million

Investment

Combined

SCPZ Internal Infrastructure

Investment Over $48.81 million

Details

Length of road Four Years

13.72km

Total average water demand 5,626 cum/day Year 1: $11.8 million

Wastewater generation 3,957.92 cum/day Profit After Tax Year 2: $7.9 million

MSW generation

Year 3: $6.1 million

56.91TPD

Power demand 56.66MVA IRR 20.97%

Payback Period 4 yearsAgro Industrial Corridors: Transform the agricultural landscape

21Brings Additional Players into the Value Chain

Site/Estate/Infrastructure

1 Investors ?

Industrialist/Agro

2

Processors

•Finance

•Land Devt/Alloc 3 Farmer Coops/Companies

•Ease of Doing

Business 4 Service Providers

Ease of Doing Business indicators

Government (Federal, State,

Starting a Business

5 LG)

Dealing with Construction Permits

Getting Electricity

Registering Property

6 Development Partners

Getting Credit

Protecting Investors

Paying Taxes

Trading Across Borders

Enforcing Contracts

Resolving InsolvencyBuilding Trade Capacity

Three key problem areas that require specialized assistance to enable the expansion and competitiveness of

exports from Nigeria:

The lack of marketable products for exports;

The lack of capacity to conform to international standards;

The lack of information on rules of trade, markets and procedures to connect with export markets.

The 3 Cs that enables a country to Compete, Conform and Connect.

Products to Markets

Develop Competitive

Prove conformity with Connect to the

manufacturing

Market Requirements Market

capability

Compete Conform Connect

.........by upgrading supply capacities and standards infrastructure

Strategic partnerships with international standards measurement and accreditation bodies: International

Organization for Standardization (ISO), International Laboratory Accreditation Cooperation (ILAC),

International Accreditation Forum (IAF), International Bureau of Weights and Measures (BIPM),

International Organization of Legal Metrology (OIML).

23Regional Office Nigeria 2015 Retreat

NATIONAL QUALITY INFRASTRUCTURE & INTERNATIONAL LINKAGES

Metrology

Certification National Testing

Quality

Infrastructure

Standardization Accreditation

CODEX

24Regional Office Nigeria 2015 Retreat

5 Key Areas

1. Assistance for the promulgation of a National Quality Policy (NQP)

and improvements in ensuing legislation for the NQI

2. Establishment of a National Accreditation Body (NAB) and Capacity

development for accreditation auditors

3. Establishment of a National Metrology Institute (NMI)

4. Improved Private sector capacity to create and support conformity

assessment bodies (CAB) in the NQI Program

5. Extend the use of the NQI services through awareness activities and

better trained NQI’s workforce.

25Developing SPS Compliance

Developing SPS compliance infrastructure involves the following:

Help frame legislation and regulations for SPS compliance.

Introduce the new ISO 22000 for food safety management.

Creating a Competent Authority with enforcement power to monitor producers

and players in the value chain to ensure conformity to standards.

Develop traceability systems that enable authorities to trace problems in

exported products through the value chain.

Establish or upgrad microbiological/chemical and metrological laboratories

with international accreditation for SPS testing.

Set up support services with CODEX Alimentarius Committees and a SPS

Enquiry Point.

Set up national or regional technical support centres for expert assistance to

laboratories, government officials, producers and processors.

26Thank You

27You can also read