Voting and engagement policy - La Financière de l'Echiquier

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Voting and engagement

policy

La Financière de l’Echiquier

1

INTRODUCTION

Declaration of Commitment

In its capacity as a fund management company, La Financière de l'Echiquier, hereinafter referred to as

"LFDE", may hold shares in listed companies through the investments it makes on behalf of its clients.

Consequently, LFDE, a portfolio management company approved by the AMF and registered under number

GP 91 004, hereby presents its "Policy for Voting at Shareholders Meetings" and its Engagement Policy, which

comply with the following applicable regulations:

• Articles 319-21 to 319-25, 321-132 to 321-134, 321-158 and 321-159 of the AMF’s General Regulation

• The Shareholder Rights Directives II (SRD II) of 17 May 2017

• Article 198 of the PACTE law, which enacted the SRD II into French law

• The French monetary and financial code.

As a responsible investor, shareholder voting and engagement are central to our approach to improving

the Environmental, Social and Governance (ESG) practices of companies. The policy we set forth herein is intended

to support and further our convictions and ensure the overall consistency of our approach to responsible

investment and commitments. Our policy is consistent with:

• The United Nations’ Six Principles for Responsible Investment (PRI), to which we have been a signatory

since 2008

• Our Climate Strategy

• The regulatory framework of the French, German and Belgian sustainable finance labels for the relevant

funds

• The various collaborative engagement initiatives we participate in. 1

La Financière de l’Echiquier may update this document at any time.

To ensure transparency and in compliance with the applicable regulations, LFDE also issues the following

documents:

• A Voting and Engagement Report, which provides information on the exercise of LFDE’s voting rights at

the shareholder meetings of the issuers in its fund portfolios, and on the implementation of its

engagement approach, in accordance with its policy as presented in this document. This report is

published annually.

• Exhaustive inventories of the votes cast at the shareholder meetings of the issuers in SRI-labelled fund

portfolios over the past year.

These inventories are published annually for each fund.

Our policy and reports are available on our website in the "Responsible Investment" section, on the "To find out

more" page, under the "LFDE Documents – Shareholder dialogue” heading.

Complete voting records are also available for each labelled fund on its dedicated page, which is accessible from

the "Funds" section of our website.

1

The list of SRI-labelled funds and our collaborative engagements are available in our Transparency Code.

2

Managing conflicts of interests

To minimise the risk of conflicts of interests and deal with such conflicts if necessary, LFDE has set up an

appropriate organisation and laid down strict rules for its managers, employees and directors. For example:

- - The company’s staff are all subject to strict ethical rules, most notably on their personal financial market

transactions. Employees may not invest in directly-held securities. They must certify their situation with

the Compliance and Internal Control Officer when they join the company and renew this certification

annually. These rules apply to any securities accounts opened with a third party in their name or over

which they have power of attorney.

- LFDE exercises particular vigilance to prevent conflicts of interests which may result from a corporate

office held by an independent director of the management company or of its funds.

- Lastly, LFDE monitors all votes cast by its funds managers and analysts and exercises increased vigilance

on votes that are contrary to its voting policy.

This policy was updated in May 2021.

By: Valentin Vigier, Antoine Fabre and Sonia Pavot – La Financière de L’Echiquier

3SUMMARY

I. VOTING AT SHAREHOLDER MEETINGS

A. Decentralised exercise of voting rights

B. How votes may be cast

C. Shareholder engagement at shareholder meetings

II. VOTING PRINCIPLES AND GUIDELINES

A. General principles

B. Approval of annual accounts

C. Governance organisation and functioning

D. Minority shareholder rights

E. Corporate action and the appropriation of earnings

F. Executive compensation

G. Other

III. ENGAGEMENT PROCESS

A. Managing the engagement

B. Individual engagement with companies

C. Other forms of individual engagement

D. Collaborative engagement

E. Prioritisation of engagement

F. Insider information

IV. PRINCIPLES OF THE ENGAGEMENT POLICY

A. Engagement principles and objectives

B. The main engagement themes

C. Specific themes

V. ESCALATION PROCEDURE

4I. VOTING AT SHAREHOLDER MEETINGS

LFDE systematically exercises its voting rights at the shareholder meetings of the companies it invests in, while

observing a voting policy that aims for the highest standards of good governance and responsibility to its

employees, society and the environment, including the fight against climate change.

Exceptions to the exercise of voting rights: The voting policy at shareholder meetings does not apply to funds that

are managed using quantitative and macro-economic strategies, Africa theme funds, and funds of funds. On

31/12/2020, these funds represented about 7% of LFDE's assets under management.

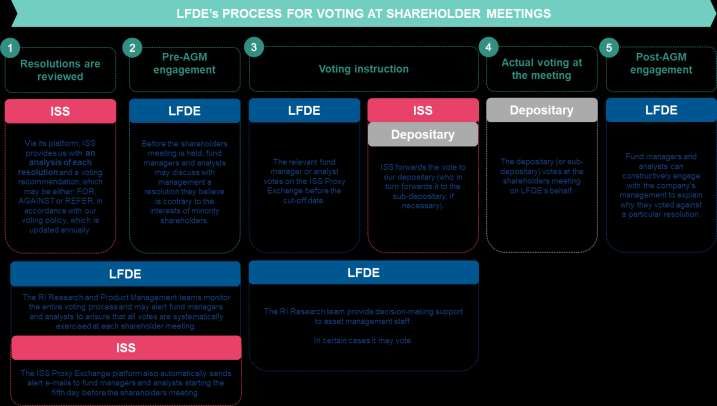

A. Decentralised exercise of voting rights

The exercise of voting rights has been decentralised. This means that each fund manager and analyst votes

for the companies whose financial and ESG performance he or she monitors. This person is then responsible for

the single vote for all of LFDE’s holdings in that company. We believe it is essential to have thorough knowledge

of companies and to follow them over time in order to understand what is at stake at annual shareholder meetings

and make the decisions we believe are good for both the company and our clients, as minority shareholders. This

decentralised approach ensures the participation of the entire asset management team, with the support of the

Responsible Investment (RI) research team.

The annual shareholders meeting also provides an opportunity to assess how a company is progressing,

particularly with respect to its corporate governance. Decentralising voting to the fund management team enables

fund managers and analysts to gain more in-depth knowledge of the companies in which they invest.

The RI Research team helps fund managers and analysts ensure that they understand the voting process and

resolutions. This team may be asked to vote at the shareholder meetings of companies that are deemed to be of

strategic importance (e.g. because they are controversial, one or more resolutions impacts the company's CSR

strategy, LFDE has a large stake in the company, or LFDE has an enhanced engagement process with the company).

5B. How votes may be cast

La Financière de l’Echiquier prefers postal voting but, depending on circumstances, reserves the right to vote

directly at shareholder meetings or to authorise the company’s Chair to vote on its behalf. Exceptionally, it may

also appoint a proxy.

Voting rights are exercised in partnership with ISS (Institutional Shareholder Services), the world leader in

corporate governance and responsible investment solutions. Each year, ISS informs LFDE of the most recent

developments in voting requirements and practices and of any changes it has made to its own voting policy. This

annual review enables us to improve our shareholder voting policy, maintain high standards and ensure that our

voting is consistent with our values.

Throughout the year, ISS handles the placing of LFDE’s orders with its depositaries. ISS also reviews the resolutions

to be voted on and provides specific recommendations, in accordance with the principles of our voting policy.

These recommendations provide fund managers and analysts with an initial analysis of the resolutions to assist

them in voting in accordance with our voting policy. The person who will exercise the vote is responsible for

reviewing these recommendations in light of the company’s specific situation and challenges. In some cases, this

person may decide to vote against the recommendation and therefore against the voting policy. Such cases are

very rare and when the fund manager or analyst votes he or she must systematically substantiate the exceptional

characteristic that justifies deviating from the voting rule.

In the effort to achieve its objective of voting at every shareholder meeting, LFDE has implemented a system for

closely monitoring voting activity. To ensure maximum vigilance, this monitoring is the collective responsibility of

the following stakeholders:

• The Asset Management Assistant: During the annual shareholder meeting season, fund managers and

analysts receive an email every Monday from the Asset Management Assistant (or if unavailable from the

Product Management team) that summarises all the meetings to be voted at over the next 10 days, to

enable them to identify the meetings where they are to vote.

• ISS: Fund managers and analysts are registered on the Proxy Exchange platform and are linked with the

funds for which they are responsible. For each shareholder meeting of a company that is monitored by a

fund manager or analyst, the latter will receive an e-mail alert every day starting five days before the

meeting and until votes have been exercised.

• The RI Research team: The RI Research team members monitor the voting schedule daily and directly

contact fund managers and analysts who are to vote at an upcoming shareholder meeting.

Due to the number of intermediaries involved (which include ISS, the centralising agent Broadridge, our

depositaries and sub-depositaries), in some very rare cases we may not be able to vote for technical reasons. LFDE

has adopted a best-effort approach and in such cases and shall not be held responsible.

Our service provider ISS keeps all voting data for each resolution. These data are aggregated by portfolio and for

LFDE in general. LFDE uses these data to inform its clients of the exercise of its shareholder votes each year with

full transparency. Two examples of this are the annual report on shareholder voting and engagement and annual

SRI reports available on our website.

6C. Shareholder engagement at shareholder meetings

Voting at shareholder meetings often provides an opportunity to meet with company management. The

resolutions voted on at shareholder meetings are central to the company’s operation and development. It is

therefore important that LFDE is able to engage with management at this time.

• This engagement may take place before the meeting, when we wish to talk with management to gain a

better understanding of the reasoning behind a specific proposed resolution and inform them of what

responsible investors expect in terms of best practice in formulating resolutions.

• This engagement may also occur after the meeting, to discuss why we voted "against" the management

team's recommendation on a proposed resolution. This enables us to confirm the importance of good

governance practices we expect.

7II. VOTING PRINCIPLES AND GUIDELINES

A. General principles

La Financière de l’Echiquier is an asset management company whose core competence is stock picking. This

approach consists in implementing a rigorous stock selection process that includes a fundamental analysis of each

investment case and face-to-face meetings with the companies in which the funds invest.

This means that when LFDE fund managers invest in a listed company they have complete confidence in its

management and agree with its strategy. LFDE invests in companies that create value for their shareholders and

all of their stakeholders. Accordingly, although there may be no fundamental reason to oppose a management

team's voting recommendations at a shareholder meeting, LFDE carefully examines all of the resolutions

proposed, and in particular those which may be contrary to the interests of the company or of its minority

shareholders.

Since its inception, LFDE has attached great importance to knowing and understanding the companies in which it

invests. For example, small and medium-sized listed companies often face different governance issues than do

large companies, where there is often a disconnect between the main shareholder, operational management and

risk management. We adapt the voting principles presented below to the various situations we may encounter

and are committed to exercising our voting rights with full knowledge and consideration. This desire to understand

the companies in which we invest is at the core of our ESG-integrated investment process for all our actively

managed funds. This is reflected in particular in the in-depth governance analysis that each fund manager and

analyst carries out internally, and which accounts for the majority of our ESG rating.

The following section presents La Financière de l'Echiquier's positions on various issues that are dealt with at

shareholder meetings. For greater transparency and clarification, we have provided actual examples of some

applications of our voting policy in the boxes below, using the following colour codes: FOR, , AGAINST and

REFER]

- How ISS applies our voting policy -

When a fund manager or analyst logs on to the ISS Proxy Exchange platform to vote at a shareholder meeting,

each resolution has been carefully reviewed by ISS and one of the following personalised voting recommendation

is provided:

- FOR when the resolution is consistent with LFDE’s voting policy

- AGAINST when the resolution goes against LFDE’s voting policy

- REFER when the task of reviewing the resolution is left up to the fund management team.

This option is reserved for resolutions that LFDE’s RI research team believes require more in-depth analysis on a

case-by-case basis, such as on compensation systems, the appointment and reappointment of a director, or of a

social or environmental nature.

8B. Approval of annual accounts

Approval of annual accounts

LFDE approves annual accounts when the auditors' report is included in the management report and the

auditor has made no reservations.

OUR VOTING POLICY AT WORK

LFDE's voting policy recommends voting FOR unless:

- REFER The preparatory documents (i.e. the annual report and the auditors' report) were not available when the

analysis was conducted,

- REFER ISS raises concerns about the board or executive compensation and there is no appropriate resolution on

the agenda for expressing our disagreement,

- AGAINST The auditors have expressed reservations, or the accounts or audit procedures are contested.

Related-party agreements

It is important that auditors inform shareholders of any transactions that may be subject to conflicts of

interests, and clearly explain the company’s interest in such transactions and their financial terms and conditions.

Past agreements that remain valid must appear in the auditors’ report and be approved by shareholders.

AGAINST LFDE could vote against the auditors’ report on related-party transactions if there is insufficient

information to judge the justification for the transactions presented or if a transaction is contrary to the interests

of minority shareholders.

Auditor appointment, rotation and compensation

In line with the European Directive 2014/56/EU amending Directive 2006/43/EC on statutory audits of annual

accounts and consolidated accounts and Regulation 537/2014 on specific requirements for the statutory auditing

of public interest entities, which came into force in June 2014, audit firms must be rotated at least every 10 years,

and at least every 24 years where there are joint audit firms.

La Financière de l’Echiquier also wants auditors to be mainly remunerated for their auditing work.

AGAINST If the fees received for non-auditing services exceed 70% of the fees received for auditing, or if the

company does not break down these fees, LFDE may vote against the approval of this compensation. This 70%

ratio excludes fees for services related to IPOs, key acquisitions and other exceptional services.

OUR VOTING POLICY AT WORK

Financière de l'Echiquier's voting policy recommends voting FOR unless:

- AGAINST The auditor’s term of office exceeds 10 years (or 24 years if the company has two joint auditors, which

is mainly the case in France). In other countries, we will observe this guideline to the best of our ability, as

information is not always available.

- AGAINST Fees paid to auditors for non-audit services exceed 70% of audit fees.

- AGAINST The company did not disclose the amount paid to the auditors.

9C. Governance organisation and functioning

Governance structure

LFDE has no automatic preference for a one-tier board structure (with an executive committee and a

board of directors) or a two-tier board structure (with a management board and a supervisory board).

OUR VOTING POLICY AT WORK

REFER When a company wishes to switch from one or the other governance structure, each case is reviewed

individually. This review process usually includes a discussion with the company’s management to determine the

reasons for the change and its impact on the company’s stakeholders.

Separation of powers

LFDE favours the separation of executive and supervisory functions. This separation can be achieved by:

▪ A two-tier board structure: a public limited company with a management board and a supervisory board

▪ A one-tier board structure with separation between the functions of CEO and chair of the board.

However, in many companies, and mainly those of small or medium size, the company’s founder or a descendant

runs the company and also chairs the board. This person is often the main shareholder and can legitimately lead

and represent the company.

When the same person is both the chief executive officer and the chair of the board, it is important that the board

has provided for independent checks and balances that can effectively limit the CEO’s actions. To this end, LFDE is

attentive to the following:

▪ The Board of Directors is composed of a majority of members who are independent

▪ There is a Deputy Chief Executive Officer

▪ There is an independent Vice-Chair, who is charged with the task of informing shareholders of

governance issues. In the absence of such a Vice-Chair, LFDE checks that there is appointed a lead

independent director, whose role is clearly defined in the company's articles of association, to fulfil the

Vice-Chair’s role and to assist the CEO and Chair with his or her duties. This person’s responsibilities could,

for example, include adding items to meeting agendas, convening meetings of independent directors and

conducting the Chair’s evaluation.

OUR VOTING POLICY AT WORK

REFER] Since the assessment of checks and balances within a company is a complex task, all resolutions dealing

with the following matters are reviewed by the LFDE fund manager or analyst on a case-by-case basis.

Board composition and appointment of directors

LFDE attaches great importance to the appointment and reappointment of directors, whose CVs it carefully

examines. This serves to ensure that the board will be able to operate more effectively, by being well-balanced,

with complementary experience and skills and sufficient geographical, gender and age diversity.

10Given the importance of the board’s composition, LFDE has adopted the following guidelines:

• To ensure that the board’s composition is regularly approved by shareholders, LFDE prefers to be able to vote

on each director’s reappointment in a separate resolution, at least every 4 years.

• LFDE has observed that in order to function effectively and optimally, boards generally must have a minimum

of 5 and a maximum of 15 members. This is therefore the ideal board size that LFDE has chosen.

• LFDE also looks at the availability and attendance of directors and expects any attendance rate below 75% to

be justified. LFDE therefore opposes the holding of more than four positions on corporate boards and more

than two if one of the positions is an executive position.

• LFDE generally disapproves of the appointment of alternate directors, as they are not in a position to ensure

the continuity of the decision-making process.

• In addition to the individual experience and skills of directors and the complementary nature of their profiles,

LFDE attaches great importance to their being at least one third independent directors on the board when

the company is controlled by another. If a company is not controlled by another, LFDE expects to see a

majority of independent directors on the board. The AFEP-MEDEF report provides the following definition of

an independent director: "a director is independent when he or she has no relationship of any kind with the

company, its group or its management that might compromise the exercise of his or her free judgment". To

promote employee representation on corporate boards, LFDE does not count employee representatives or

employee shareholder representatives as independent board members.

• For many companies, setting up specialised committees may prove to be extremely useful. In order to give

certain subjects the in-depth attention they deserve, these committees are made responsible for overseeing

audit processes, appointments, compensation and even the company’s strategy and corporate social

responsibility (CSR). LFDE pays particularly close attention to the presence of executive directors on audit and

compensation committees, and encourages audit committees to be made up of independent directors only.

It is preferable that these committees be composed of three to five members.

• LFDE only approves the presence of non-voting members on boards on a temporary basis (for example,

pending their election at the next shareholders meeting) and if properly justified by the company.

• To ensure gender diversity, LFDE requires that at least 30% of board members be women (or men as the case

may be). If a country's regulations require more than a 30% minimum, we align ourselves with this

requirement (as is the case in France, when the minimum ratio was increased to 40% under the COPE

ZIMMERMANN law).

OUR VOTING POLICY AT WORK

REFER] Resolutions on a board’s composition are mainly dealt with on a case-by-case basis, except in the

following situations:

- Gender diversity: AGAINST If the minimum ratio of women on the board (or of men as the case may be) is not

obtained, we will vote “against” in the following order: against the reappointment of the chair of the nomination

committee, or if irrelevant against the reappointment of the other members of the nomination committee, or if

irrelevant against the appointment or reappointment of a male director.

- Multiple directorships: AGAINST If a non-executive director holds more than four directorships in listed

companies, or holds more than one directorship in addition to an executive position.

- Attendance: AGAINST: If a director has attended fewer than 75% of board and committee meetings during the

year under review.

11D. Minority shareholder rights

Respect for the principle of "one share, one vote".

In accordance with the fundamental principle of shareholder democracy, LFDE wants the voting rights of

shareholders to be proportional to their economic interest in the company in which they invest, and wants the

companies in which it invests to observe the "one share, one vote" principle. LFDE also disapproves of restrictions

on voting rights, multiple classes of shares with different voting rights, and preference shares with more voting

rights than ordinary shares. LFDE pays close attention to companies that propose resolutions to allow double or

higher voting rights, particularly in countries where regulations on multiple voting rights have become laxer (such

as UK and Spain), as was the case in France with the Florange law.

Anti-takeover measures

LFDE opposes measures that could cause a takeover bid to fail unless these measures are first approved

by shareholders at a meeting held during the takeover bid period. LFDE will therefore speak out against any anti-

takeover measure, such as a share buyback or the granting of stock warrants exclusively to a category of

shareholders, which are not suspended during a takeover bid pending shareholder approval.

Change of legal form

A company’s legal form can have a considerable impact on the rights of minority shareholders. For

example, LFDE opposes a company’s conversion to limited partnership type partnership, which requires minority

shareholders to delegate nearly all of their powers to a general partner.

OUR VOTING POLICY AT WORK

AGAINST We are opposed to any measure that does not respect the "one share, one vote” principle, such as

issuing non-voting shares, issuing shares with double or multiple voting rights, and restricting voting rights.

E. Corporate action and the appropriation of earnings

Capital increases with pre-emptive subscription rights

LFDE votes in favour of capital increases with pre-emptive subscription rights (PSR) as long as the shares

issued do not represent more than 50% of share capital.

Capital increases without pre-emptive subscription rights

LFDE is generally against the issuance of shares without pre-emptive subscription rights (and without a

mandatory priority period) or through a private placement, unless this has first been discussed with shareholders.

Share buybacks

LFDE will vote in favour of plans to buy back shares representing up to 10% of share capital (and 15% in

the United Kingdom, Ireland and South Africa, where such share buybacks are commonly accepted) provided that

12the company’s treasury stock does not already exceed 10% (or 15% in the above-mentioned countries). However,

as stipulated above, LFDE will continue to vote against share buybacks that could be made during a takeover bid

period or which could compromise the company’s ability to continue as a going concern.

Dividends

LFDE believes that the dividend policy proposed to shareholders must be responsible, justified, and in

line with the company's strategy and prospects. The distribution of dividends must not jeopardise the company's

viability as a going concern. If the distribution of dividends to shareholders is to the detriment of investment,

which is the engine of future value creation, LFDE considers that this is contrary to the long-term interests of

shareholders.

LFDE also believes that it is important that companies share value with all of their stakeholders, and in particular

with their employees. The distribution of dividends must not come at the expense of their compensation. All

companies must make sure to achieve a proper balance between the two, since this promotes a sense of unity

and common purpose.

As a long-term shareholder, LFDE therefore understands and accepts why a company may decide not to pay

dividends when it has made a loss, when its debt is excessively high, or in the event of an exceptional crisis, such

as the COVID-19 pandemic. During the COVID-19 crisis, LFDE looked closely at the dividend policies of companies

that received state aid and/or resorted to short-time working.

OUR VOTING POLICY AT WORK

FOR We approve dividend distributions unless the company's payout ratio is negative or exceeds 80%, which

results in a REFER and a case-by-case assessment of the company's situation by the relevant fund manager or

analyst.

F. Executive compensation

The introduction of say-on-pay rules in France has intensified LFDE’s vigilance on the transparency, clarity and

quality of the criteria and objectives used to determine executive compensation, and ensure that the latter is

consistent with the interests of minority shareholders. If the compensation paid to a company’s executives does

not seem to be aligned with its long-term performance, LFDE will seek to arrange a meeting with the company’s

management before the shareholders meeting, to emphasise the importance of this alignment and inform the

company of how it will vote.

Transparency and clarity

Executive compensation must be reviewed annually and individual compensation explained in detail in the

annual report and/or compensation report, which must be provided prior to the shareholders meeting. LFDE

attaches particular importance to the transparency and clarity of compensation schemes, to ensure that

shareholders have sufficient information to approve compensation.

LFDE looks for clear information on the following:

13• The amounts attributed for each component of compensation (e.g. fixed salary, bonus, directors' fees,

benefits in kind, multi-year variable compensation, options, potential share rights and complementary

pension plans)

• The criteria and methodology used to assess performance

• The performance thresholds and targets and actual performance.

LFDE also believes that no executive should sit on the compensation committee.

Alignment with performance

So that a company’s progress can be measured over time, LFDE encourages management to define financial

and ESG indicators that are consistent with the company’s strategy and specific long-term objectives in accordance

with its strategic plan. To ensure that the interests of executives are aligned with those of shareholders, LFDE

believes that executive compensation schemes should be based on performance criteria that are coherent,

challenging and measurable.

Since LFDE is convinced that compensation should be performance-based, we oppose the granting of variable

compensation that is not subject to performance criteria, graduated thresholds or caps. We also disapprove of

any measures that enable compensation rights or vesting periods to be modified. However, LFDE strongly

recommends the use of specific and verifiable environmental and social performance criteria that are consistent

with the company's sustainable development objectives and strategy.

LFDE approves measures that encourage senior executives to own shares in their company, since this

naturally aligns their interests with those of shareholders.

Moderation

LFDE does not intend to express its opinion on the amount of compensation granted. However, we look

out for abusive compensation that could be detrimental to the company’s cohesion and performance. When a

company’s financial situation forces it to lay off employees, management’s compensation must be exemplary (e.g.

no increase in fixed salary, no annual bonus, etc.). During the COVID-19 crisis LFDE was particularly attentive to

the amount of annual variable compensation granted to management by companies that received financial

support from the government and/or implemented a lay-off plan.

As a general rule, LFDE approves the disclosure of compensation-equity ratios and monitors them closely. The

assessment of compensation-equity ratio must take each company’s specific business environment into account.

However, we generally recommend a ratio of 1%.

Compensation of non-executive Board members

LFDE believes that directors should be remunerated with fees that are based on their attendance of meetings

and not on the company's performance.

The compensation of non-executive chairs of boards of directors should be commensurate with their role and

responsibilities and should not deviate excessively from the fees paid to the other directors.

LFDE approves the direct holding of a company’s shares by its non-executive board members throughout their

term of office; once again to ensure that their interests are aligned with those of shareholders.

14Employee share ownership

LFDE approves the promotion of employee share ownership plans, to enable all employees to share in

their company’s success.

OUR VOTING POLICY AT WORK

REFER] Resolutions concerning executive compensation are mainly dealt with on a case-by-case basis. Their

review is left to the fund manager’s discretion, except in the following exceptional cases, for which LFDE's voting

policy recommends voting AGAINST:

- If the performance indicators for each component of compensation are not disclosed

- If long-term variable compensation vests in less than 3 years after the grant date

- If termination payments exceed 24 months of salary (i.e. fixed and variable short-term compensation)

- If there is no cap on short-term variable compensation

- If there are no performance criteria for long-term variable compensation

- If the terms of performance are reassessed after the end of the performance measurement period

- If the vesting period is progressive on an annual basis

- If the vesting period is accelerated due to beneficiary’s departure from the company.

G. Other

Amendments to articles of association

Resolutions involving changes to a company’s articles of association are examined on a case-by-case basis

and in accordance with the principles of good governance set out throughout this voting policy. Particular

attention is paid to resolutions to transfer a company's registered office to a country offering tax advantages.

Shareholder resolutions

Resolutions placed on the agenda by shareholders other than board members are carefully reviewed on

a case-by-case basis, in accordance with the principles of good governance set out in our voting policy.

Accordingly, in order to defend the interests of the minority shareholders who indirectly own units in LFDE’s funds,

LFDE reserves the right to vote against such resolutions or to abstain from voting.

15Resolutions of an environmental (including climate) and social nature

As a signatory to the United Nations Principles for Responsible Investment, LFDE considers that exercising

its voting rights gives it an opportunity to encourage companies to adopt environmental and social best practices.

Our voting guidelines therefore encourage companies to take these responsible investment considerations into

account.

Convinced that the use of environmental and social criteria enables risks to be assessed more effectively, we have

incorporated these criteria into our voting policy for all of the meetings at which we may vote.

LFDE’s Climate Strategy includes a commitment to make an active contribution to the transition to a low-carbon

economy. This commitment is reflected in the votes cast by fund managers and analysts, which take into account

the extent to which a company’s resolutions are consistent with this low-carbon economy objective. LFDE

approves pro-climate resolutions to:

• Set ambitious quantitative targets for the reduction of CO2 emissions for the company's business activity

and/or products

• Reduce the absolute volume of CO2 emissions

• Provide more transparency on the risks of climate change (regulatory, financial and physical), their

identification and mitigation.

LFDE systematically supports efforts to increase corporate transparency on climate-related actions and

approves efforts to promote the ‘Say on Climate’ and thus encourage company’s to submit their climate strategy

to the approval of their shareholders. However, LFDE closely monitors the objectives of the proposed strategies

and makes sure that they are relevant. LFDE also carefully examines shareholder resolutions to encourage

companies to adopt a climate strategy that is compatible with a viable climate trajectory, particularly if the

company is carbon-intensive.

Although human resources issues are less frequently dealt with at shareholder meetings, they are also a subject

of our concern.

We also carefully review resolutions that seek to define a corporate purpose and/or mission or which are related

to B-Corp certification.

OUR VOTING POLICY AT WORK

REFER] Resolutions proposed by external parties are reviewed on a case-by-case basis in accordance with our

responsible investment philosophy, as described above.

For resolutions of an environmental or social nature, LFDE has also set up an alert system on the ISS Proxy Exchange

platform to ensure that they are systematically detected and carefully reviewed.

16III. SHAREHOLDER ENGAGEMENT

As a responsible investor, shareholder engagement is an integral part of our business and has been central to

our relationship with companies since 2013. Through engagement and dialogue, LFDE seeks to make a positive

contribution to their governance and to their environmental and social practices.

A. The engagement process

Helping to improve the practices of companies and our stakeholders is a long-term process. To ensure the

most effective shareholder engagement, we have organised our efforts to make the greatest possible contribution

within the scope of our means. As with the exercise of its voting rights, LFDE has decentralised its engagement

process. All fund managers and analysts are responsible for engaging with the companies whose financial and ESG

performance they monitor. They are responsible for the engagement relationship for all of LFDE's holdings in that

company. We are convinced that the long-term monitoring of companies and the in-depth knowledge thus gained

are essential to understanding their challenges and to assessing their progress.

LFDE engages with investee companies in two distinct ways:

• Through individual engagement

• Through collaborative engagements.

All information gained from our individual and collaborative engagement actions is shared with our asset

management team via our Phoenix database, internal meetings and various information channels.

Since 2018, our annual report on the exercise of voting rights also provides an overview of our engagement

actions, while providing concrete examples. Our voting and engagement policy is available on our website in the

“Responsible Investment” section, on the ““To find out more” page, under the “LFDE Documents – Shareholder

dialogue” heading.

B. Individual engagement with companies

LFDE engages individually with companies throughout the life of its investment, mainly by determining areas of

improvement, formally defining these areas and presenting them to management.

LFDE conducts its individual engagement approach as follows:

• For SRI-labelled equity funds: When an ESG analysis is completed, the fund manager or analyst who

follows the company determines a certain number of areas of improvement. These areas of improvement

are the environmental (including climate change), social and governance practices of the company which

LFDE would like to see improve. We want the goals we share with the company to be realistic, measurable

and auditable. These areas of improvement are formalised in writing and sent to the company.

During the follow-up meeting, which takes place on average every two years, we assess with

management the progress achieved relative to the objectives set (i.e. the areas of improvement achieved,

partially achieved or not achieved), and together redefine new areas of improvement. In addition to this

formal biennial review, for our Impact funds in particular we make it a point to monitor their areas of

improvement more frequently.

• For SRI-labelled bond and diversified funds and ESG-integration funds: Unlike SRI-labelled equity funds,

engagement with companies is strongly recommended but not systematic. Areas of improvement are

systematically defined by the relevant fund manager or analyst when each ESG review is completed.

17These areas of improvement are also formalised in writing but are not systematically sent to the

company. They are, however frequently discussed during periodic meetings with management teams,

since ESG issues are increasingly discussed with investee companies.

In the following cases, companies are usually informed of their areas of improvement:

• LFDE holds a substantial stake in the company and the company is geographically proximate.

• The ESG issues identified are material: During the ESG review, if one or more areas of improvement

involve ESG issues that are particularly important to the company, the company will be informed of

these areas of improvement.

• Consultation with stakeholders: It is not uncommon for fund managers and analysts to interact with

other stakeholders in the company. If certain common concerns on material issues emerge, then it

is important that we as shareholders discuss these concerns with the company’s management.

• Post-AGM engagement: When engagement at the annual general meeting has already been made

on issues that were identified as ‘areas of improvement' during the ESG review, it is not uncommon

for these issues to be discussed with the company to emphasise their importance.

In its effort to continuously improve its responsible investment approach, LFED aims to strengthen its individual

engagement practices and systematically inform companies of their areas of improvement and thus manage all of

its funds in a consistent manner. To this end, the RI Research team monitors the percentage of areas of

improvement that are sent to companies out of the total number determined each year.

C. Other forms of individual engagement

Although its engagement actions are mainly intended for companies, LFDE also engages with other

stakeholders, such as regulatory authorities and ESG data providers, because we believe that all stakeholders in

our ecosystem have a role to play in the development of responsible finance.

• Engagement with companies (and their stakeholders) on a more discretionary basis

o In-depth discussions with companies on specific points that fall outside the scope of the areas

of improvement or with external consultants at the company’s request

o Training provided to corporate CSR officers and other financial market participants

o Submitting written or oral questions at shareholder meetings

• Engagement with stakeholders in the responsible investment ecosystem

o Engagement with ESG data providers (e.g. Trucost, MSCI ESG Research and ISS) to help them

improve the quality of the services and data they provide and develop their analytical

methodologies and services.

• Engagement with public authorities on sustainability issues

o Responding to consultations prior to the issuance of new regulations, participating in

sustainability working groups and advocacy activities (e.g. European Taxonomy and AMF’s

doctrine on the use of ESG criteria).

• Engagement with other fund management companies on their approach to responsible investment

o In-depth discussions with fund management companies on their SRI approach when selecting

funds for our Allocation strategy, using our “LFDE SRI maturity" methodology

o Exchanging ideas on areas of improvement.

18D. Collaborative engagement

In addition to its individual engagement with companies, in 2019 LFDE strengthened its collaborative

engagement efforts with other investors.

This approach, which is complementary to individual engagement, enables LFDE to:

• Engage on issues that are difficult to address individually

• Target several companies in the same sector simultaneously

• Make its voice heard with companies with which individual engagement would not be effective (see the

escalation procedure described in section V.2)

• Engage with companies excluded from its investment universe to support them in their transition (e.g.

thermal coal companies).

We select the collaborative engagement initiatives in which we wish to participate in accordance with our

responsible investor policy and approach. The collaborative engagements in which La Financière de l’Echiquier

participates are described in its Transparency Code, which is available in the "Responsible Investment" section, on

the “To find out more“ page, under the “LFDE documents – General approach” heading.

E. Prioritisation of engagement

Engaging with companies is a long-term and time-consuming process. To optimise its effectiveness, LFDE

prioritises the allocation of its resources on a case-by-case basis and in accordance with the following criteria:

• Geographic region and proximity: LFDE is a long-term investor that has historically - and still today - been

mainly exposed to European companies. This proximity with European issuers of securities plays a key

role in our engagement decisions, since it ensures a higher probability of success. We therefore favour

engagement with European companies which offer this proximity.

• The materiality of ESG events that require an urgent need for progress on ESG issues, such as

controversies, violations of international standards, etc.

• The size of the investment in the company

• Alignment with our responsible investor commitments (see section IV.C for more information)

• The most carbon-intensive companies.

F. Insider information

LFDE may, in some exceptional cases, obtain insider information in the course of its engagement process. In

such cases, Internal Control staff will implement market abuse controls to minimise this risk.

19IV. THE ENGAGEMENT POLICY

A. Engagement principles and objectives

The objectives of LFDE’s individual and collaborative engagement efforts are to:

• Get companies to adopt best practices in terms of their governance, compliance with international

standards, and responsibility towards their employees, society and the environment, including the fight

against climate change and the loss of biodiversity.

• Encourage companies to be more transparent, to enable us to gain a better understanding of their

governance and CSR strategy.

• Help companies improve the measurement of their impacts.

In its effort to establish a quality shareholder engagement relationship, LFDE strives to comply with the following

best practices:

• Define objectives that are measurable, verifiable and time-bound (with intermediate and final deadlines)

to enable more accurate monitoring of performance and ensure that the impact of our engagement is as

measurable as possible.

• Monitor, whenever possible, the progress that companies have made toward their objectives. If we feel

that the company's trajectory is insufficient in some areas, we will re-engage with the company on these

issues.

B. The main engagement themes

The engagement of LFDE’s fund management team focuses above all on the issues that are most important

for each company. It is therefore difficult to draw up an exhaustive list of our engagement themes. In addition to

the issues listed in the section dealing with our voting policy guidelines, we engage with companies in the following

areas:

Governance:

o Transparency of the company's governance and internal procedures

o Chief executive succession planning

o Executive compensation

o Composition of governance bodies (proportion of independent members, gender and ethnic

diversity, director profiles, etc.)

o Checks and balances

o Respect for minority shareholders

o Evaluation of ESG risks.

Environment:

o Environmental roadmap objectives and their milestones

o Transparency (disclosure of environmental performance, supplier audit findings, information on

the supply chain, etc.)

o Alignment of environmental targets with best practice and industry standards, such as the

Science Based Targets.

20Human resources:

o Transparency (disclosure of HR performance indicators: employee turnover rate, occupational

accidents, satisfaction surveys, etc…),

o Protection of employees and contractors (safety, social protection, freedom of association, etc.)

o Employee loyalty and support (additional training efforts, reduction of the turnover rate, etc.),

o Responsible management of corporate restructuring.

Controversies and Compliance with International Standards:

o The handling of environmental, social and governance controversies

o Human rights violations

o Forced labour and child labour

o Money laundering and corruption.

C. Specific themes

In its approach to shareholder engagement, LFDE pays particular attention to issues related to its broader

policies and commitments, and to those which must be addressed by its SRI-labelled funds.

• Climate Strategy

LFDE has strengthened its commitment to fight climate change and to meet the objectives of the Paris

Agreement in early 2021, by publishing its Climate Strategy, which contains a policy to regulate the financing of

thermal coal. Engagement with companies is a key component of this strategy.

A specific engagement procedure has been defined for the companies in the thermal coal industry, to support

them in their total withdrawal from thermal coal activities by 2030. In addition to this, companies that are

considered to play an important role in the environmental transition are also subject to an enhanced engagement

procedure. In both of these cases, our engagement will be based on a detailed analysis using our proprietary

"Climate Maturity" methodology.

LFDE’s Climate Strategy and Coal Policy are available on our website in the "Responsible Investment" section, on

the “To find out more“ page, under the "LFDE Documents - General Approach” heading.

• Signing of the Finance for Biodiversity Pledge

In December 2020, LFDE joined the Finance for Biodiversity Foundation initiative, the objective of which is to

get financial institutions to promote biodiversity. This initiative enables LFDE to focus on biodiversity issues, for

which there is a specific engagement process for companies that are particularly exposed to and dependent on

biodiversity.

• The French government’s SRI label

The French SRI label requires certified funds to outperform their benchmark on at least two ESG performance

indicators, to ensure that these issues are taken into account in investment decisions and that fund managers are

committed to improving the profile of their portfolios in respect of these indicators.

LFDE has selected a climate indicator: the carbon footprint per million euros of revenue. We will therefore be

particularly vigilant about the carbon footprint of companies, an SRI theme that will also be at the core of our

engagement efforts. The second ESG performance indicator will be selected some time in 2021.

• Impact Doctrine

Engagement is a key component of additionality, which is an essential criterion of impact funds. Additionality

is an investor’s direct and specific action or contribution which enables an investee company or a financed project

21to increase its net positive impact. This is why LFDE is strengthening its engagement with companies on their

impacts and the measurement of these impacts.

In 2021, LFDE will also implement a new type of engagement in the form of a multi-stakeholder seminar for clients,

companies, partner organisations and employees, with the objective of sharing information and best practices and

discussing impact-related topics in conferences and workshops.

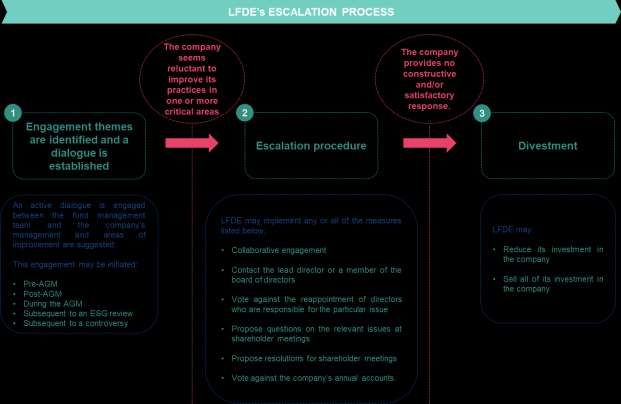

V. ESCALATION PROCEDURE

Despite our engagement efforts, some companies may not make a constructive effort to progress in an area

which our fund management team considers to be critical. In such cases, LFDE will observe the escalation

procedure described below.

The escalation procedure sets forth the various engagement actions which fund managers and analysts may

undertake, and which go so far as divestment if unsuccessful.

LFDE's escalation procedure:

1. Identifying engagement themes and establishing a dialogue.

Fund managers and analysts begin by initiating an active dialogue with the company's management and

providing areas of improvement on the SRI themes on which the company is expected to make progress over the

short or medium term. This dialogue may occur during dedicated ESG meetings, and also before shareholder

meetings (Pre-AGM), during (in AGM) or afterwards (Post AGM). During this initial phase, fund managers and

analysts define measurable objectives that will be used to assess the company’s progress. These areas of

improvement are monitored over an extended period and are the subject of numerous interactions between our

investee companies and LFDE fund management teams.

2. Escalation

If the company is reluctant to change its practices on the most critical issues, the fund manager or analyst can

insist on the importance of these issues by adopting a more "activist" approach. However, LFDE's objective is to

be constructive and co-operate closely with the company by maintaining an open dialogue to preserve the

relationship of trust that has always characterised LFDE’s approach to shareholder engagement.

For this purpose, LFDE may implement any or all of the measures listed below:

• Undertake a collaborative engagement with other like-minded investors

• Contact the lead director or a member of the board of directors to express its expectations

• Vote against the reappointment of a director who is responsible for the particular issue (e.g. a member

of the audit or risk committee)

• Propose questions on our engagement themes at shareholder meetings

• Propose resolutions at shareholder meetings

• Vote against the company's annual financial reports.

3. Divestment

If the escalation measures fail to bring about a positive change in the company's practices and we consider

that we have not obtained a constructive and satisfactory response, as a responsible investor we may partially or

even completely divest our investment in the company, in the best interests of our clients.

Companies will be informed of this to raise their awareness of the importance of engagement with their investors.

22Furthermore, LFDE does not exclude the possibility of continuing its engagement actions after divestment, which

may, for example, be the case when the company is involved in a controversy.

2324

You can also read