Adaption of Management Control Mechanisms for Swedish companies operating in Australia

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Adaption of Management Control Mechanisms

for Swedish companies operating in Australia

Bachelor’s Thesis 15 hp

Specialization: MC

Department of Business Studies

Uppsala University

Fall Semester of 2021

Date of Submission: 2022-01-12

Julia Bergling

Erica Tranefalk

1

Supervisor: Tina Hedmo

Abstract Successful companies that are founded and established in Sweden are likely to at some point look to expand outside of Sweden. When they do so they will need to adapt the company to the environment and circumstances that are present in the local market they are expanding to. The main purpose of this thesis is to investigate Swedish companies’ use of control mechanisms when running a subsidiary in Australia. Applying the theoretical framework by Malmi and Brown (2008), four Swedish companies operating in the Australian market were selected. Ikea using culture as an asset make them an interesting comparison to three highly reputable tech-companies that both differ from Ikea in age and size. It was found that cultural control mechanisms were heavily featured among the respondents' respective companies, and reward and compensation control mechanisms were altered the most when operating in Australia compared to Sweden. Sammandrag Framgångsrika bolag grundade och etablerade i Sverige kommer sannolikt att någon gång expandera utanför Sverige. När de gör det kommer de att behöva anpassa företaget till den miljö och de omständigheter som råder på den lokala marknaden de expanderar till. Huvudsyftet med denna uppsats är att undersöka hur svenska bolag styr sina kontrollmekanismer när de driver en filial i Australien. Fyra svenska företag på den australienska marknaden har valts att studeras utifrån det teoretiska ramverket av Malmi and Brown (2008). Ikeas användning av svensk kultur som en tillgång gör det till en intressant jämförelse med tre välrenommerade teknikföretag, som både skiljer sig från Ikea när det gäller ålder och storlek. Det visade sig att kulturella kontrollmekanismer var flitigt förekommande bland respondenternas respektive företag, och belönings- och kompensations- kontrollmekanismerna förändrades mest när man verkade i Australien i jämförelse med Sverige. Keywords: Management Control Systems, Management, Control, Control Mechanisms, Multinational Firm, Sweden, Australia, Expansion

Acknowledgements We would like to thank our supervisor Tina Hedmo and our fellow students whom we have shared this journey with, through seminars with mutual exchange of feedback and constructive criticism. We would also like to thank and acknowledge the contributions made by our four respondees who took the time out of their busy schedules to help us in our work. Without their contribution there would have been no thesis to be written on the subject.

Table of Contents 1. Introduction .............................................................................................................. 1 1.1. Globalisation ................................................................................................................. 1 1.2. Challenges for the multinational corporation ............................................................... 1 1.3. Control Mechanisms ..................................................................................................... 2 1.4. Swedish companies operating in Australia ................................................................... 2 1.5. Purpose of study and research question ....................................................................... 3 1.6. Disposition..................................................................................................................... 3 2. Theoretical Framework ............................................................................................. 4 2.1. Management Control System ....................................................................................... 4 2.1.1. Definition.......................................................................................................................... 4 2.1.2. Formal and Informal Control Mechanisms ....................................................................... 4 2.1.3. Factors that affect the choice of MCS .............................................................................. 5 2.1.4. MCS as a Package ............................................................................................................. 6 2.2. The relationship between MCS and environmental factors ........................................... 9 3. Methodology .......................................................................................................... 10 3.1. Research approach ...................................................................................................... 10 3.2. Data collection ............................................................................................................ 10 3.2.1. Sampling ......................................................................................................................... 10 3.2.2. Interviews ....................................................................................................................... 11 3.2.3. Anonymity ...................................................................................................................... 12 3.3. Data analysis method .................................................................................................. 12 3.4. Research ethics ........................................................................................................... 12 3.5. Quality of research ...................................................................................................... 13 4. Result ...................................................................................................................... 14 4.1. Ikea .............................................................................................................................. 14 4.1.1. Cultural controls ............................................................................................................. 14 4.1.2. Planning controls ............................................................................................................ 14 4.1.3. Cybernetic controls ........................................................................................................ 15 4.1.4. Reward and Compensation ............................................................................................ 15 4.1.5. Administrative Controls.................................................................................................. 16 4.2. The Adam Company .................................................................................................... 16 4.2.1. Cultural controls ............................................................................................................. 16 4.2.2. Planning controls ............................................................................................................ 17 4.2.3. Cybernetics controls ....................................................................................................... 17

4.2.4. Reward and Compensation ............................................................................................ 17 4.2.5. Administrative Controls.................................................................................................. 18 4.3. The Bertil Company ..................................................................................................... 18 4.3.1. Cultural controls ............................................................................................................. 18 4.3.2. Planning controls ............................................................................................................ 19 4.3.3. Cybernetics controls ....................................................................................................... 19 4.3.4. Reward and Compensation ............................................................................................ 20 4.3.5. Administrative Controls.................................................................................................. 20 4.4. The Cesar Company ..................................................................................................... 20 4.4.1. Cultural Controls ............................................................................................................ 20 4.4.2. Planning Controls ........................................................................................................... 21 4.4.3. Cybernetic Controls ........................................................................................................ 21 4.4.4. Reward and Compensation ............................................................................................ 22 4.4.5. Administrative Controls.................................................................................................. 22 5. Analysis ................................................................................................................... 23 5.1. Environmental factors - Sweden vs Australia .............................................................. 23 5.2. Cultural Control Effects ............................................................................................... 23 5.3. Planning Control Effects .............................................................................................. 24 5.4. Cybernetic Control Effects........................................................................................... 25 5.5. Reward and Compensation Effects ............................................................................. 25 5.6. Administrative Control Effects .................................................................................... 25 6. Conclusion............................................................................................................... 27 6.1. Suggestion for future studies ...................................................................................... 28 7. References .............................................................................................................. 29 Appendix ........................................................................................................................ 32

1. Introduction This chapter describes the background of the study as well as a statement of the problem. It also presents the purpose and research question of the study, along with the intended contribution of the research. 1.1. Globalisation As the world economy becomes increasingly globalised, companies naturally seek new markets to expand their business to. There are several different reasons for a company to expand such as entering new markets, increasing revenue, and gaining a competitive advantage. Almost half of Sweden’s GDP comes from exports which highlights that Swedish companies strategically explore business expansion abroad (The World Bank, 2020). Furthermore, Sweden’s relatively small population size is perhaps an explanation for the need to enter a foreign market as it can contribute and open opportunities that do not exist within the Swedish borders. In 2019, there were 3 813 Swedish companies operating a subsidiary abroad, which was an increase of 710 subsidiaries since 2018 (Peter Frykblom, 2021) and 200 of these companies are operating in Australia (Business Sweden, 2020). Australia, with its British roots and partnerships within the Commonwealth, has a business culture with many similarities to European companies. This could also be the reason why Australia sometimes is called “Sweden’s most remote neighbour”. Furthermore, Australia has a market size twice the size of Sweden’s and offers great opportunities in several industries such as mining, construction, medical technology, and agriculture (Business Sweden, 2020). There is currently a negotiation going on between the EU and Australia concerning a free trade agreement (FTA) which aims to increase trade in goods and services between the two partners (European Commission, 2017). The EU having a trade agreement with Australia could simplify the arrangement for Swedish companies wanting to expand to the Australian business market. Australia being an attractive market for Swedish business expansion highlights the question of how Swedish companies decide to govern their subsidiaries in Australia. 1.2. Challenges for the multinational corporation Previous research has introduced two possible directions for a multinational corporation (MNC) when expanding abroad (Forsgren, 2017). Either the expansion puts its focus on the product itself - a new target market with different needs and values, or the expansion is to the greatest extent geographical, and focus will be to correspond to the new local area with the original product. In either way, competing successfully in a global world requires companies to respond to local demands while also establishing a high level of integration between the business units across borders. Seifzadeh, Rowe and Moghaddam (2021) argue that in order to become a successful company, which can be defined as attaining organisational goals, it is the headquarters’ (HQ) responsibility to ensure that each subsidiary is effectively managed in a way so actions and decisions that are taken contribute to the overall performance of the corporation. Lawrence and Lorsch (1967) emphasize the importance for both integration and 1

differentiation to meet the environmental demands. Integration is needed for effective performance and differentiation is needed for a company to adapt to the external environment. Another study shows that the key factor for a MNC’s performance is its capability to respond to differences between countries, such as local competitors and financial distortions (Forsgren, 1992). This puts pressure on the HQ to analyse the environment of each subsidiary and adapt to the environment they operate in (Forsgren, 1992; Pehrsson 1992; Schlegel, 2011). The main idea behind the contingency theory is that there is no best way to structure and control a company (Morgan, 2006, p.42). Instead, the environment and the company itself needs to be analysed in order to choose the strategy that is believed to best suit the corporation’s goals, values and plans (Alpander, 1977; Ambos and Schlegelmilch, 2007). Different units of a MNC might face different contingencies and these can in turn be managed through a variety of control mechanisms. The differences in contingencies can also put the subsidiary in a conflicting position, as they both face pressure from the HQ to operate according to the MNC’s strategy as well as from the local suppliers, customers and stakeholders to gain legitimacy on the local market. The environment that a subsidiary operates in could have a higher degree of complexity which requires them to have more autonomy and flexibility (Nohria and Ghoshal, 1994). Hamilton and Kasklak (1999) bring up country restrictions and cultural distance as two factors for what type of management is suitable. Furthermore, size, level of employee education or the subsidiary’s dependence on resources can also have an impact on what control mechanisms to apply (Gomez and Sanchez, 2005). 1.3. Control Mechanisms Andersson and Funck (2005) explains governance as actions the company’s management takes to achieve their desired goals. Malmi and Brown (2008) define management control as controlling activities management put in place to direct employee behaviour. Another phrase for these activities is control mechanisms. The control mechanisms are parts of the management control system (MCS) set out by management to govern the employee towards the organisational goals. In other words, how the control mechanisms are used to influence behaviour, so the company’s goals are achieved. 1.4. Swedish companies operating in Australia One of the first organisations that non-swedes think about when they think of Swedish companies is conceivably Ikea. Ikea was founded in Sweden in 1943, opened up their first subsidiary outside Scandinavia in Switzerland 1973 and expanded to Australia in 1975 (Ikea, n.d.). Ikea is one of the largest furniture retailers in Australia and holds around 16% of Australia's furniture market (Powell, 2019; IBISWorld, 2021). Ikea’s business concept is “to offer a wide range of form-fitting and functional home furnishing products at such low prices that as many people as possible can buy them” (Ikea, n.d.). Ikea can be seen as unique as it is one of the world’s most known and successful retail-companies in the world. Since 1943, it has built up a strong brand value, with a low-cost strategy and a strong emphasis on Swedish culture. Ikea is constantly looking for ways to grow its business and is today operating in more than 50 countries, which makes it a compelling company to study. 2

The European Trade Commission has ranked Sweden as the leading nation of innovation

within Europe (European Commission, 2021). The tech-industry is generally on the front

foot when it comes to continuous development and innovation and is therefore an interesting

industry for a case study of this nature. For this study, three highly reputable tech-companies

that are each a leader in their respective niche markets have been selected to further

investigate how companies need to adapt their control mechanisms when expanding across

borders. Of particular interest is to see how these, rather young, subsidiaries are controlled

by their HQ compared to the well-established company Ikea.

1.5. Purpose of study and research question

Based on the discussion above it is of great importance to understand the local environment

when expanding across borders. Previous research has shown a relationship between factors

such as size and market complexity and the choice of control mechanisms. However, even

though there are many studies on MCS, there is little agreement on which components that

are necessary to complete the whole system and according to Malmi and Brown (2008),

there is a lack of research on MCS as a package (O’Grady, Morlidge and Rouse, 2016).

The aim of this study is to investigate the choices of control mechanisms when a company

runs a subsidiary on a different market than the market of origin. The purpose has been

further refined to investigate Swedish companies that have an established subsidiary in

Australia. This study’s contribution derives from the stated need of more empirical studies

that view MCS as a package.

The research question of this thesis will therefore be;

How do Swedish companies adapt their management control system when

operating an Australian subsidiary?

1.6. Disposition

The remaining chapters for this thesis will be presented in the order as presented in the

figure below:

THEORY METHOD RESULTS ANALYSIS CONCLUSIONS

32. Theoretical Framework The following chapter presents the key concept and previous research within MCS. It begins with an explanation of MCS and factors that potentially can affect the choice of MCS. It then moves to describing MCS as a package and finally describing the relationship between the environmental effects and MCS. 2.1. Management Control System 2.1.1. Definition Defining MCS is challenging as there are several definitions and descriptions of the concept (Malmi and Brown, 2008). For example, Ouchi (1979) defines it as “mechanisms through which an organization can be managed so that it moves towards its objectives'”. Merchant and Van der Stede (2007) describe management control as “dealing with employees’ behaviour”. Malmi and Brown (2008) define management controls as “systems, rules, practices, values and other activities that the management uses to direct employee behaviour”. Furthermore, if these activities are complete systems or are unmonitored, they should be called decision-support systems rather than MCSs. The model from Malmi and Brown has been criticised for example by O’Grady et al. (2016, p.3) because the model is supposed to work as a “collective whole”, however, the framework does not account for how this would or should be accomplished. Furthermore, Siska (2015, p.145) criticise Malmi and Brown’s model for having limited potential as it does not give enough information. Siska further reasons that this might be a reason why Tessier and Otley (2012) go back to previous research. Notwithstanding the critique noted above, this study will use the definition presented by Malmi and Brown (2008) as this model has been identified as the standard model that most considers seeing MCS as a complete package. It is recognised that this study is only looking at subsidiaries’ MCS from a high-level perspective and therefore Malmi and Brown’s (2008) holistic approach is considered to be the most applicable. 2.1.2. Formal and Informal Control Mechanisms As well as there are several ways to define MCS, researchers have also categorised the different types of control mechanisms in numerous ways. One way is to categorise them as formal and informal control mechanisms. As there are several studies that use these two terms when analysing factors that affect the choice of MCS, these terms will be used in combination with the framework presented by Malmi and Brown (2008) to further understand how the HQ of the selected companies for this study have chosen to control their subsidiaries in the Australian business market. Formal control mechanisms are the use of centralisation, formalisation, standardisation, planning, behavioural control and output control. Informal control mechanisms relate to lateral relations, informal communication and the organisational culture (Martinez and Jarillo, 1991; Gomez and Sanchez, 2005). 4

2.1.3. Factors that affect the choice of MCS As mentioned earlier, the environment and its contingencies have to be analysed in order to choose what strategy best suits the company and its goals and values. There are several factors that play a role when choosing control mechanisms and it is important to understand the impact of these factors (Seifzadeh et al., 2021). One internal factor that has proved to influence the choice of control mechanisms is size. When a MNC contains a larger number of business units, it will more likely use output controls (Seifzadeh, et al.., 2021). Furthermore, when the size of the HQ is larger, they have a better ability to use behavioural controls as a larger HQ presumably has more resources and therefore also has a better ability to process information (Seifzadeh, et al.., 2021). When the size of the subsidiary, and the size of the MNC as a whole, is larger, formal mechanisms, such as standard operating procedures and manuals, may be of better use than informal control mechanisms (Gomez and Sanchez, 2005). One external factor refers to the degree of a subsidiary’s dependency on resources. If the subsidiary is dependent on the HQ for resources, the HQ can to a higher degree influence the subsidiary. In contrast, if the subsidiary is more self-sufficient and has autonomy, the HQ’s influence on the subsidiary is limited (Doz and Prahalad, 1981). Furthermore, if the local environment that the subsidiary is operating in is complex, previous studies have shown a negative relation to centralisation but a positive relation to formalisation and normative integration. This means that in a complex environment a MNC tends to be more decentralised, decisions will to a higher extent be made accordingly to impersonal rules, routines and procedures and the different units of the MNC share to a higher degree the same values and goals (Nohria and Ghoshal, 1994). When expanding abroad, a MNC might face differences in regulations and restrictions affecting the business. If the MNC is affected by government regulations or restrictions, either in the host country or the country that each subsidiary operates in, it could potentially be harder for the HQ to influence processes within each subsidiary. In a case with more strict regulations and restrictions, behavioural and output controls are less effective whereas input controls, such as training and socialisation, are more effective (Hamilton and Kasklak, 1999). Hofstede’s theory (Hofstede Insights, n.d.) of cultural dimensions has been widely used in studies when analysing differences between nations and its culture. Hofstede presents six dimensions, which allows one to analyse a nation from different aspects, are power distance, individualism, masculinity, uncertainty avoidance, long-term orientation and indulgence (Hofstede Insights, n.d). Hamilton and Kasklak (1999) discuss cultural distance and suggest the benefits of using local expertise when the cultural distance is large. Furthermore, they also state that the performance of the subsidiary could be hard to monitor when the cultural distance is large, and instead of using behavioural and output controls, which have shown to be ineffective in such situations, the HQ should rather use input controls. In figure 1 below, Hofstede’s study (Hofstede Insights, n.d.) of cultural dimensions presents a ranking of the Australian and Swedish cultures. The largest difference is in regards to 5

Masculinity. According to the model, Swedish culture is more “feminine” and instead of

strong emphasis on achievements and material rewards for success there is a focus on

reaching high levels of cooperation and quality of life.

Figure 1. Cultural differences, Australia vs Sweden. Source: Hofstede Insights, n.d.

Another factor that has been found to influence the choice of control mechanisms when

operating a subsidiary abroad is the level of education. If the employees at the subsidiary

hold a higher level of education, the control mechanisms tend to be informal rather than

formal (Gomez and Sanchez, 2005). As seen in figure 2 below, the educational level is

similar in Australia and Sweden. Between 1970 and 2010, Australia has in general had a

higher rate of completed tertiary educational level.

Figure 2. Share of the population with completed tertiary education. Source: OECD Data,

2020

2.1.4. MCS as a Package

Malmi and Brown’s (2008) study accentuates the importance that MCS' should be used as a

package rather than using separate control mechanisms in isolation from each other. In their

study, they present a framework that identifies five types of control mechanisms: planning,

cybernetic, reward and compensation, administrative and cultural. Figure 3 below illustrates

the roles of the different types of control in Malmi and Brown’s (2008) model. At the top

sits cultural control covering the whole control system and providing context to the other

types of controls. At the middle of the figure are the planning, cybernetics and reward and

compensation controls usually tightly linked and they are presented in the figure in the order

they usually occur. At the bottom of the figure are the administrative controls that provide

6the fundamental groundwork for planning, cybernetic and reward and compensation

controls.

Figure 3. T. Malmi and D.A. Brown 2008, p.291

Cultural Controls

There are three aspects of cultural controls; clan controls (Ouchi, 1979), value-based

controls (Simons, 1995) and symbol-based controls (Shein, 1997).

Clan control is the creation of subcultures or micro cultures within a company. These are

characterised by like-minded individuals that influence others with a certain set of skills and

values.

Value-based controls is a belief system that can be divided into three levels;

1) Certain types of values in applicants are sought out to match the values of the company during

the recruitment process.

2) Values of individuals are adjusted to fit the company by socialising.

3) The values of the company are clearly illustrated and employees behave in unity with them

even if they do not hold on to them personally.

The senior managers formally communicate basic values, purpose, and direction of the

company. Mission statements, visions and statements of purpose are all examples of value-

based control.

Symbol based controls develop a culture by visible expressions, for example a building

layout, a workplace design or dress codes. An open office plan can initiate communication

and create culture, and compelling employees to wear a uniform can create a culture of

professionalism (Malmi and Brown, 2008).

Planning Controls

Planning is a forecast-type of control directing employee behaviour through goal setting,

clarifying the level of effort and behaviour expected from the employee as well as facilitating

7coordination between the activities of groups and individuals. Planning can be split into two

subtypes; action planning with a more tactical focus to set the activities for the company’s

goals usually within a year and long-range planning with the goals and activities for the

medium or long-term with a more strategic nature. According to Malmi and Brown (2008),

planning can be done with little reference to budgeting and operational planning often forms

a task list which provides guidance on what to do.

1. Standards of performance

2. Measuring system performance

3. Comparing performance to standards

4. Feeding back information about unwanted

variance in the system and modifying the

system accordingly.

Figure 4. Cybernetic clarified as a feedback loop. Based on Malmi and Brown’s (2008)

model

Cybernetic systems can either be an information system or a control system. It is important

to make a distinction between cybernetic control systems used for information and decision

making and those that are used to direct and control behaviour. It is only when linking

behaviour to targets and getting accountability for variations in performance that cybernetic

systems go from being an information system to support decisions to an MCS. Four basic

cybernetic systems are budgets, financial measures such as cost/income ratio, return on

equity and economic value added and non-financial measures. Hybrids including both

financial and non-financial measures are common such as the balanced scorecard (Malmi

and Brown, 2008).

Reward and Compensation Controls

Reward and compensation systems are used to motivate and increase performance of

individuals and groups to achieve goals and set out activities. Reward and compensation are

believed to lead to increased effort by the employees. Linking effort and employees' tasks

can impact performance in three ways; effort direction (tasks individuals focus on), effort

duration (how long individuals devote themselves to the task) and effort intensity (the

amount of attention devoted to the task). Rewards are often connected to the achievement of

goals defined by the cybernetic controls but there could also be other reasons such as

providing rewards and compensation to retain employees and encouraging cultural control

(Malmi and Brown, 2008).

8Administrative Controls

Administrative control systems are used to direct employee behaviour by organising

individuals and groups. Monitoring of behaviour, clarification of who is accountable for

employees’ behaviour and specifying the process of how task and behaviour should or

should not be performed are examples of ways to do it

Three different groups of administrative control exist:

1) Organisation design and structure – The way the company is structured can encourage

certain types of contact and relationships. Control that works through functional

specialisation and influences control through reducing the variability of behaviour and, in

turn, increasing its predictability.

2) Governance structures – Establishing formal authority and accountability to direct employee

behaviour. This includes systems that make sure representatives of various functions and

organisational units meet to coordinate their activities both vertically and horizontally.

3) The procedures and policies – Bureaucratic approach by specifying the process and

behaviour within the company by using standard operating procedures, rules, and policies.

Training can be included in administrative control as an individual can be trained to follow

the set-out policies and procedures (Malmi and Brown 2008).

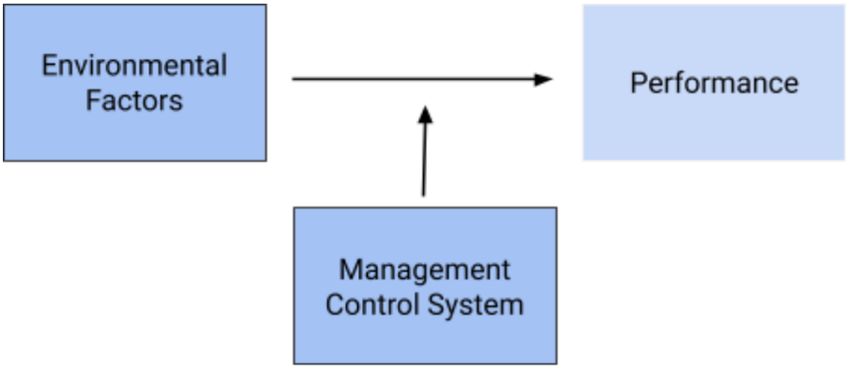

2.2. The relationship between MCS and environmental factors

Figure 5 below illustrates the relationship between MCSs, the environmental factors and the

performance of the subsidiary. The environmental factors, consisting of internal and external

factors, have in previous research proved to have an impact on the choice of control

mechanisms and should therefore be considered to understand how the HQ choose to control

their subsidiaries. Each company’s MCS package is somewhat unique to their corporation

as well as the environmental factors they might face. However, how a MNC chooses to

control their subsidiaries will have an impact on its performance (Alpander, 1977). If the

parent corporation does not understand the local environment of the subsidiary and does not

let the subsidiary have autonomy to be able to adapt to the local environment, it might lead

to a weak performance. In contrast, if the subsidiary has autonomy so it can adapt to the local

environment, it could potentially lead to a better performance.

Figure 5. The relationship between internal factors, external factors, MCS and

performance.

93. Methodology In the following chapter the choice of research approach will be presented. This will be followed by a motivation for the study’s choice of data collection as well as the method used to analyse the data. Lastly, there will be a discussion concerning the research’s ethics and quality. 3.1. Research approach This study aims to answer how a Swedish subsidiary in Australia adapt their MCS which can be seen as a comparative research design. When deciding the approach to conduct a study, one can decide between qualitative and quantitative research. According to Bryman and Bell (2019, p.356) qualitative research is preferable when research material mainly emphasizes words and individuals rather than numeric data. MCS is a reflection on the governance the company’s management team decides to take. The governance is set by the managers in the organisation and therefore it is believed that the managers concepts, opinions, and experiences will best be answered in qualitative research. Consequently, MCSs are best captured in interviews with responsible individuals. This, combined with the complex nature of MCS, led to a qualitative study being chosen for this study. When conducting a study, a deductive or inductive approach can be chosen (Bryman and Bell, 2019, p. 64). For this study, a deductive approach was selected as the theory is used to guide the research rather than being the outcome of it. 3.2. Data collection 3.2.1. Sampling A common type of sampling is purposive sampling (Bryman and Bell, 2019, p.388). For this study, it was important to ensure that the sample was relevant to the research question which is why purposive sampling was chosen. However, it should be noted that this type of sampling does not show to what extent it is possible to generalise the findings to a broader population. When selecting companies that were relevant to the research question, there were three criteria’s that had to be fulfilled. Firstly, the companies needed to be founded in Sweden. Secondly, they needed to still be operating parts of their business in Sweden. Finally, at the time when this study took place, they had to be operating a subsidiary in Australia. It should however be mentioned that the location of each company’s HQ is not all placed in Sweden. Four companies were identified to make out the population. One of the companies is operating within the retail industry and three of the companies are operating within the tech- industry. The retail company is, as mentioned in the introduction, Ikea. Ikea has been selected to this study as it is unique in being one of the world’s most known and successful retail-companies in the world. The reasoning for choosing to study companies within the tech-industry is because Sweden is a leading nation of innovation within Europe and could perhaps give a more complete picture since tech-companies might face different contingencies than Ikea (European Commission, 2021. Ikea employs more than 200 000 persons worldwide, more than 10 000 persons in Sweden and more than 4 500 persons in 10

Australia. The tech-companies on the other hand are each less than 1 000 employees

worldwide. Ikea has been doing business in Australia for more than 46 years while the tech-

companies have expanded to Australia in the last seven years. Furthermore, other presumed

differences in regards to the contingencies could be the technology, the environment and the

strategy of the companies. Ikea is well known for its large scale of mass producing and their

market could be described as stable. They have, as mentioned earlier, a low-cost strategy as

their aim is to offer affordable products. In contrast, the tech-companies are operating in a

more dynamic environment and their focus is on customisation rather than large scales of

mass production. The tech-companies have a different strategy than Ikea as they focus more

on innovation and product development. Moreover, the tech-companies are not known for

being Swedish in the same sense as Ikea. This makes the reflection between these two

industries interesting, as it will shed light on to what extent the Swedish heritage matters for

a company when operating a subsidiary abroad.

Persons within the management team from each firm were contacted through email or

LinkedIn. They were provided with information about this study, its purpose and research

question and asked if they would be interested in participating in an interview.

The interviewees chosen were:

• IKEA

Participant’s role: Chief Executive Officer AU / NZ

• The Adam Company

Participant’s role: Chief Operating Officer (Global)

• The Bertil Company

Participant’s role: Managing Director AU / NZ

• The Cesar Company

Participant’s role: Country Manager AU

3.2.2. Interviews

Through semi-structured interviews, data was collected for each variable in the model

presented by Malmi and Brown (2008). The interviews each lasted approximately 40-50

minutes. This form of data collection made it possible to vary the order of the questions

depending on how the interviewee answered as well as ask follow-up questions. The

interview questionnaire is attached below in the appendix.

A representative from the management level in each organisation was selected for the

interviews as they are responsible for the MCS and have great insight in what control

mechanisms are used in their company. The conceptual model of Malmi and Brown (2008)

was used as an interview guide. The model was slightly adjusted to make concepts

understandable for persons who have not studied the model and some words were translated

to Swedish as the interviews were held in Swedish.

11Bryman and Bell (2019, p.212) state that there are two types of interviews: in person and by telephone. As the respondents are located in Australia while the authors are located in Sweden during the time of this study, telephone interviewing was the most fitting option. In consideration of the limitations to read and observe body language during a phone interview, virtual interviews were held via Zoom and Teams when possible. One of the interviews with one of the tech-companies was held via a phone call via WhatsApp. The choice of using Zoom or Teams was dependent on the respondent’s preference. 3.2.3. Anonymity When conducting the interviews, the respondents were asked if they wanted to be anonymous. Ikea did not want to be anonymous whilst the tech-companies chose to be anonymous in this study. This means that background information will be presented about Ikea, but not about the tech-companies. As the tech-companies have a more niche market focus, there will be less transparency in regard to their products and services. 3.3. Data analysis method The method used to analyse the collected data was the thematic method as it is argued to be well suited when handling qualitative data (Bryman and Bell, 2019, p.519). When analysing the data, the authors could find patterns that matched Malmi and Brown’s (2008) framework. As the findings were organised in the same systematic way it was possible to further discuss the similarities and differences between the four companies. Moreover, the findings were discussed together with potential environmental factors that may have influenced the chosen control mechanisms. When analysing the differences in national culture this study focuses only on masculinity as it is the dimension with a noteworthy difference between Australia and Sweden. This choice does not deny the importance of the other dimensions as they indeed play a part in a nation's culture. However, the limitation is explained by the wish to create a balance between the control mechanisms in the model presented by Malmi and Brown (2008). 3.4. Research ethics When conducting research, it is important to be aware of ethical issues that can arise throughout the research process (Swedish Research Council, 2017). These can be divided into four main areas; whether there is harm to participants, whether there is a lack of informed consent, whether there is an invasion of privacy and whether deception is involved (Bryman and Bell, 2019, p.114). To handle these issues the respondents were ensured that neither their integrity nor anonymity would be endangered. The data was not used for other research purposes and the data was kept safe and only accessible to the authors. The respondents were asked if they wanted to be anonymous in this study and, to ensure that the data was not misunderstood, all respondents were given access to the compiled data before finalising the study. 12

3.5. Quality of research There are mainly three quality criteria that one should be aware of when conducting a study: reliability, replication and validity (Bryman and Bell, 2019, p.46). Reliability is used to evaluate to what extent it is possible to produce the same results if the research would be repeated. Replication is about how well other researchers can repeat the same research and this is best handled by giving detailed information about the procedures of the study. Lastly, validity measures how well the research captures the phenomenon that it is intended to study and to what extent the conclusions are true. In this thesis, discussions around the reliability and replication criteria will be heavily dependent on the data collection described in section 3.2. To increase the quality of the study’s reliability and replication, the interviewees were asked to validate their contribution by proofreading the final draft of the thesis. The adoption and design of the MCS can vary depending on the industries the subsidiaries operate in, size of the subsidiaries, individuals in the organisation as well as what time they integrated in Australia. To address this issue, the model Malmi and Brown (2008) present is used as it emphasizes the importance of how different components (control mechanisms) in the model are linked and need to be looked at as a whole system. A company’s MCS package is shaped from the interactions of different factors, external and internal, and are under continual development (Otley, 2016). Because of the continual development, it can be said that the timing of the establishment of the subsidiaries can be considered of less importance. The size, individuals of organisation and design is indeed of consequence, however, the scope of this study does not allow to interview all possible permutations of companies. As this study aims to study control mechanisms as a package, it can reduce the sense of depth in the analysis compared to studies that solely focus on one control mechanism or one factor. This is acknowledged as a limitation by the authors. Furthermore, the interview format has some inherent risks. An interviewee may modify his or her answer in order not to appear disloyal to the company, and the interviewer may unintentionally influence the interviewee. There is also the issue of the interviewee’s subjective interpretation of the interview questions where the interviewee may have misjudged, misunderstood, or excluded information. Regarding the risks of a semi- structured interview, the benefits of this interview-style were considered to outweigh the disadvantages. The benefits include things such as us being able to ask follow-up questions and to try to minimise the risk of misjudged or misunderstood answers. 13

4. Result

In the following chapter the results from Ikea will be presented and thereafter the results

from the tech-companies.

4.1. Ikea

4.1.1. Cultural controls

Cultural controls are heavily featured in Ikea. The Swedish heritage is important for Ikea

and it gives the company uniqueness to build brand value. Christmas celebration,

Midsummer party, Lucia and a yearly kick-off are some traditions that are the same in

Australia and Sweden. The stores are nearly identical, the design of the offices is open and

everyone is wearing a blue and yellow uniform.

“For some roles, it is necessary to have the right experience or qualifications,

such as program developing skills. However, in most cases, the ‘right’

degrees or grades are not necessary.”

For Ikea, the focus is on finding the right person that fits with Ikea's values. All recruitment

processes are based on global competence profiles. The competence profiles are developed

and designed by INGKA Retail Services in Malmö, Sweden and is a universal system with

job titles, job descriptions, specific functions of units and so on. To find the right person,

there is usually a minimum of three people involved for each recruiting process: the

recruiting manager, the recruiting manager’s manager and appointed HR resource. The

manager in charge holds interviews individually but also together with an upper manager,

which is called “grandparent” interviewing. The process is designed to help secure the best

candidate for the job with a good company value fit.

“The focus is on finding the right person”

An employee at Ikea must have the capability to work in a team. “Creating engagement and

being together” is a cultural value at Ikea. The employees are encouraged to come up with

new ideas and to be intrapreneurs. They would like to be able to call themselves “The

world’s biggest small company”. Acting like a small company with an entrepreneurial

mindset, Ikea has globally implemented a survey system where all employed persons can

participate and share their current Ikea work experience. The survey is conducted annually

and focusses on co-worker engagement, culture, values and leadership. The survey topics

and questions are the same across every Ikea retail country. The surveys give a good view

of how all the co-workers experience and rate the total organisation’s people and culture

performance. The results of each survey period are openly shared and also form the base for

each unit or team’s yearly people and culture action plan.

4.1.2. Planning controls

The business planning process starts in January every year. where there is a dialogue between

each subsidiary and the board. Different ideas and plans are presented for the board and the

board meets these plans with inputs and how much money that will be invested. The board

also compares each subsidiary’s plan with the ambition for the whole corporation.

14The short-term planning in the form of an operational plan at Ikea is two-folded where it has its focus on keeping the prices low without having an impact on quality. This is closely related to one of the famous strategies that Ikea has, cost reduction. The second leg is sales targets for each unit and are based on the estimated overall budget set by the board. However, each subsidiary may have some input for how to reach the sales target. The employee’s performance is broken down locally by managers. The long-term planning is firstly focusing on expansion and how to increase their market shares in their 5-year market development plan (MDP). The MDP in Australia has been focusing on increasing customer accessibility and the planning involves several workshop processes (market potential development planning) that focuses on different geographical areas in Australia. Prior to Covid19, the online sales in Australia were 10% of the overall sales, where now it is more than 20 %. Therefore, the latest plans involve more emphasis on “omnichannel retailing” through digital solutions, online warehouse fulfilment capacities and related services. Furthermore, there is a continuous planning horizon which attempts to predict what the business will look like at a 10-year perspective. The Australian subsidiary presents a road map of development to the board and the planning involves financial and profitability goals, cost structure and sustainability. Going circular and carbon neutral is one example of Ikeas 10-year plan. 4.1.3. Cybernetic controls Ikea Pty Ltd in Australia and Ikea of Sweden AB are similar in their composition and function. Ikea is a franchise model with a central office in Holland that implements standards throughout the group. To measure employees' performances, Ikea has implemented a global system called business operations transformation that is monitored and constantly developed by a service provider. This service provider sits within the Ikea group and the framework is designed globally, by specialists in each field. Both financial and non-financial measurements are connected to this system. Furthermore, Ikea has a ‘Talent for all’ system where each employee has a meeting with a manager at the beginning of the year and midterm performance review where they discuss goals of personal development. These are later reviewed at the end of financial year and can be used in salary negotiations. 4.1.4. Reward and Compensation Each year the employees at Ikea receive a salary increase based on Consumer Price Index (CPI) and individual performance. For the base increase, all units follow the same principles as they use a Predictive Index (PI). Local management rates performance – as described in the previous section – and if the performance exceeds expectations the manager may decide to give an additional salary increase. 15

4.1.5. Administrative Controls

The organisational structure is described as hierarchical, with little communication between

franchises. In general, each franchise has the same organisational and competence setup and

is run by a CEO that is solely responsible for the franchise.

INGKA Group Retail, has developed competency profiles for all different jobs within Ikea.

Comparing Australia and Sweden, the units look very similar. By implementing a global

competency profile, it has improved the communication between franchises.

Furthermore, all systems (sales, stock take, accounting system) are centrally monitored by

specialised staff. These functions are shared globally and therefore not present in every

country.

Ikea has globally embraced omnichannel, such as customer support online and activity on

social media, as a strategy to get a higher exposure online. This tool gives the company

access to valuable data with customer information, which must be saved on a server to further

analyse it. Some countries have laws against collecting customer information, however,

Swedish and Australian law is quite similar and therefore there is no significant difference

between the two franchises.

4.2. The Adam Company

4.2.1. Cultural controls

When expanding to Australia there was a manager from Sweden in charge. Being “the first

person on the ground and setting everything up”, the manager had extensive knowledge of

the company's core values which was important in the expansion process when settling down

and hiring the right people. The Adam Company’s vision is the same for the entire enterprise

including its subsidiaries around the world.

Even though there was a Swedish manager setting everything up there are no other Swedish

people working in the Australian subsidiary today. The Adam Company has from the

beginning of the expansion hired local people with no connection to Sweden and its culture.

“Not actively going out looking for Swedes”

The recruiting processes are quite similar between the units in Australia and Sweden. The

Adam Company uses their core values when finding new employees and the questions are

the same during the interviews. There is a stronger focus on the cultural values and how well

the person fits within the team rather than what qualifications the new employee has. To be

able to find the right person the company has multiple interviews, including “grandparent”

interviews. In Sweden they might have one or two extra interviews with each applicant as it

is harder to terminate an employment if it emerges that the person was not a fit with the

company.

Within the company there are traditions and ceremonies such as the two very Swedish ones

Lucia and Midsummer, a kick-off, a sporting tournament, and a system where employees

anonymously can be complimented. However, traditions and ceremonies are not all put in

16place by the management team. Instead, employees are encouraged to come up with new

ideas for future traditions to have a company culture that is created by all. It is also extremely

important that the traditions and ceremonies do not create a “we against them” feeling.

4.2.2. Planning controls

“The matrix model makes it possible to create smaller groups within the company”

Having a matrix model in The Adam Company enables them to create smaller groups within

the company. This makes it easier for the company to have weekly meetings and to make

decisions and planning on a lower level. Otherwise, everything, even less important matters,

would come up to the board level and time would be spent on things that should have been

resolved in the lower levels.

The Adam Company has divided their planning into 5 years, 3 years, 1 year and quarterly.

The decisions regarding the planning are centralised to the management team.

Their short-term planning (≤ 1 year) focuses more on sales and are called performance

development plans (PDP). The PDPs both include goals for the whole corporation, but also

individual goals for each employee. The PDPs for e.g., the salespersons include for instance

their sales budget and to develop an account management plan.

Their long-term plans (3-5 years) are for instance a revenue growth plan, expansion overseas

or launching a new project.

4.2.3. Cybernetics controls

The Adam Company has two budgets, one main budget that is set by the management team

and the board and one that each local entity is given. The main budget is based on trends

over the last 12 months; “where is the company, Sweden, or Australia heading?”. The sales

plan for each entity is 5-12% higher than in the main budget, which gives room for bonuses

or if something unexpected would happen.

The existing roles and tasks within the company in Australia and Sweden are similar and

consist of salespersons and suppliers. There is one universal measurement system which

measures both financial and non-financial performances. It is based on a business

intelligence system that connects to the company’s financial, production, sales activity, and

administration system. The system is very precise where the management team as well as

each employee can see their performance in relation to their target in real time. Since it is

available for all employees, it creates a constant feedback-loop where employees at all levels

can use the system in different ways to improve the way the company is run.

4.2.4. Reward and Compensation

The Adam Company uses monthly bonuses, which is industry standard, but are actively

trying to move away from this. Salary adjustment, promotion, training, and conferences are

tools that instead would be used to reward good behaviour and termination of employment

can be used for the opposite reason.

17You can also read