CACI - Derby City Council

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CACI Property Consulting

Derby City Centre

Retail Circuit Strategy 2008-2012

Full Report – Final

Simon Ho,

Managing Consultant

Colette Shields,

Account Manager

Property Consultancy Group

Date: November 2008

Tel: 0207 605 6226

Email: sho@caci.co.uk

Page 1

CACI Property Consulting

Report Structure

1. Project Scope and Methodology

2. Derby’s Current Catchment and Competition

3. Centre Benchmarking & Potential to change Market

Positioning

4. Current Retail Provision and Pitch Performance

5. Future Retail Circuit and Zone Strategy

6. Future Option Testing

7. Conclusions & Recommendations

Page 2

CACI Property Consulting

Derby City Retail Circuit

1. Project Scope and Methodology

Page 3

CACI Property Consulting

Project Scope

CACI have been instructed by Derby City Council to examine the current retail market for the Derby

City’s Retail Circuit and to assess the strengths, weaknesses, opportunities and threats for a

strategy to maximise the future performance of the city’s retail.

This project has been commissioned shortly following the opening of the new Westfield Derby

scheme. This means that it has been able to review the year 1 performance of the new scheme, and

what the short-term consequences have been for Derby City as a whole.

CACI have been able to review the subsequent implications for Derby’s retail ranking and

attractiveness as a location for retail and leisure operators.

A major part of the project has been to review the potential for new operators to take existing space

within the city, and what part the new Cathedral Quarter BID can play in making this a commercial

reality.

Page 4

CACI Property Consulting

Project Scope

Provide a strategy for the city centre that includes:

A short term solution to capitalise on new visitors to Derby attracted by the

opening of Westfield Derby.

A longer term strategy for Derby City Centre ensuring that the centre’s regional

position is consolidated.

A qualification of the fit between Derby Cathedral Quarter BID aims and an

optimal strategy for the city centre as a whole.

Address the following issues:

Help to understand target consumers and identify missing shoppers & visitors to

the City.

Identify and analyse distinct trading zones / pitches in the City Centre.

Identify gaps for new complementary food and drink, leisure and retail

requirements in the city centre.

Define areas undergoing change and advise on strategy to revitalise these areas.

Advise on new uses for vacant and underperforming sites/premises.

Page 5

CACI Property Consulting

Methodology – Shopper Flows

Stratford-upon-

Retail Footprint predicts the flow of shoppers

Leamington Avon

at postcode sector level to competing retail

destinations. It is a consumer driven model Spa

that reflects the choices available to shoppers

for comparison goods shopping trips.

For each postcode sector, the market is

allocated out to centres as a function of the

size (or attraction) of the centre versus the

accessibility (cost) of travelling there.

The Retail Footprint Score (RF Score) CV37 6

measures the size of each centre. It is

weighted by the national average turnover per

outlet for each retailer within the centre.

Ultimately, Retail Footprint defines overlapping

catchments for over 3,000 retail centres within

the United Kingdom. This enables assessment

of market potential, competition levels, and

consumer groups.

Retail Footprint catchments are defined by the Birmingham

sub catchments: Primary (first 50% of

shoppers), Secondary (next 25% of shoppers),

Oxford

Tertiary (next 15% of shoppers), and

Quaternary (final 10% of shoppers).

Page 6

CACI Property Consulting

Methodology – Retail Centre Class

In Retail Footprint, centres are further described by their Class, which defines the role or function of centres within the

retail hierarchy and the consequent characteristics of shopping trips. For instance, Classes such as ‘Primary Centres’ see

strong shopper flows over large distances, and very strong flows from local customers. At the other end of the hierarchy

customers will only travel to ‘Small Rural Centres’ or ‘Small Local Centres’ if they live very close.

CACI recalibrate Retail Footprint on an annual basis using new data on shopper flows received from a combination of

credit and debit card transactions, client’s own in-house exit surveys and loyalty cards.

30

Average Drive Time (minutes)

25

20

15

10

5

0

es

s

es

s

s

ns

es

ns

es

s

tre

n

tre

tre

ls

rk

tr

tr

io

w

tr

tr

w

al

en

en

en

Pa

en

en

To

sh

en

en

To

lM

lC

C

lC

C

C

Fa

tC

tC

ng

al

na

an

n

or

y

ra

ca

on

le

ba

pi

ar

ic

ith

io

li t

aj

Ru

Lo

ut

tr

op

im

gi

Ur

eg

po

M

w

is

O

Re

Pr

Sh

s

R

D

ro

y

rk

n

or

et

ilt

or

Pa

w

M

Bu

ct

aj

To

Fa

il

M

e

ta

of

os

Re

ut

rp

O

Pu

Page 7

CACI Property Consulting

Methodology – Market Positioning

Retailers have also been divided into Premium, Mass and Value categories in order to provide greater understanding of the

market position and role of centres. Value retailers include Poundstretcher, TK Maxx, Argos, Woolworths, New Look, and

Peacocks. Mass retailers include WHSmith, Top Shop, Clinton Cards, Next, and Dixons. Premium retailers include House of

Fraser, Selfridges, French Connection, Zara, LK Bennett, and Joseph.

The proportion of Value, Mass and Premium retailers present in a major centre will have an effect on the distances people will

travel to get to a centre. Value orientated major centres have smaller more localised catchments, while shoppers will be willing

to travel further to reach a Premium offer.

In the case of regional centres, people are more willing to drive longer distances for the larger scale retail offer, amongst which a

good provision of premium shops can be found.

Regional Centre Quality Major Centre

Average Major Centre Value Major Centre

100%

90%

80%

70%

% Shoppers

60%

50%

40%

30%

20%

10%

0%

0

5

10

15

20

25

30

35

40

45

50

55

60

Drivetime Band (minutes)

Page 8

CACI Property Consulting

ACORN: An Overview

ACORN combines geography with demographics and lifestyle information, grouping the entire population into 5

categories, 17 groups and 56 types. By analysing significant social factors and consumer behaviour, it provides precise

information and an in-depth understanding of the different types of consumers in every part of the country.

ACORN can be used proactively as part of a shopper-focused tenant mix strategy, to facilitate ongoing asset

management, for effective catchment zoning and ‘battleground’ analysis, and to drive marketing and shopper

communication strategies.

ACORN

Wealthy Achievers Urban Prosperity Comfortably Off Moderate Means Hard Pressed

Category 1 Category 2 Category 3 Category 4 Category 5

Groups A - C Groups D - F Groups G - J Groups K - M Groups N - Q

Types 1 - 12 Types 13 - 23 Types 24 - 36 Types 37 - 43 Types 44 - 56

Most Affluent Most Deprived

Page 9

CACI Property Consulting

Derby City Retail Circuit

2. Derby’s Current Catchment and

Competition

Page 10CACI Property Consulting

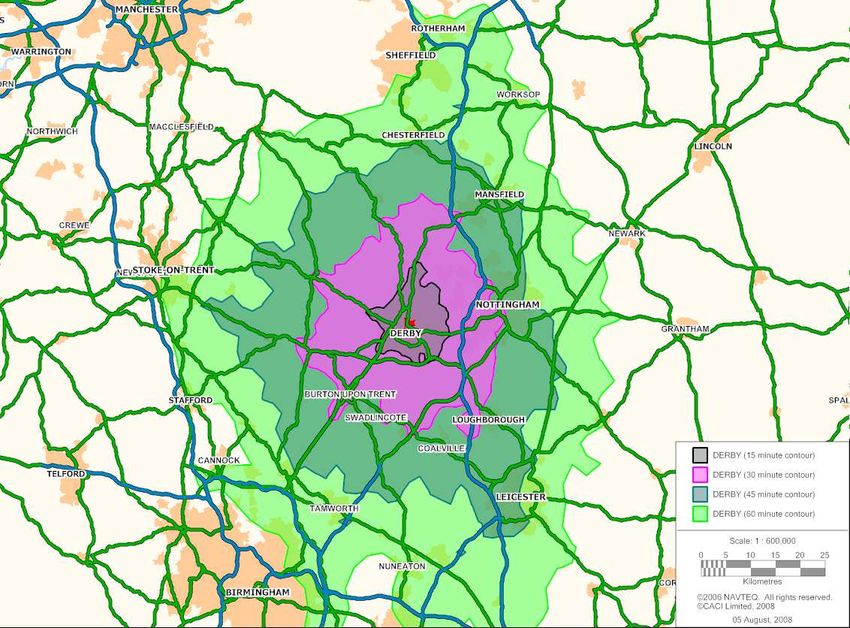

Study Area – Drivetimes from Derby City Centre

Derby City is located to the west

of the M1, from which it gains

strategic access to the north and

south.

Nottingham to the east,

Loughborough to the south-east

and Burton-Upon Trent to the

south-west are located 30

minutes drivetime from Derby.

Chesterfiield to the north,

Mansfield to the north-east and

Leicester to the south-east are

located 45 minutes drivetime

from Derby.

Stoke-On-Trent to the west,

Birmingham to the south-west

and Sheffield to the north all lie

60 minutes drivetime from

Derby.

Derby benefits from a number of

radial A-Roads providing access

north-west, north, east, south-

east, south-west and west.

Access directly south is the least

convenient.

Page 11CACI Property Consulting

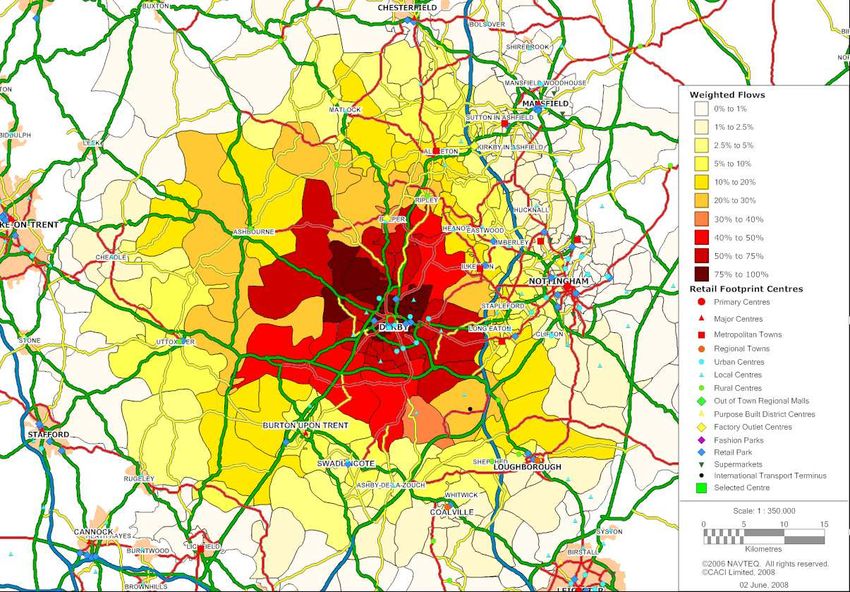

Derby 2007 catchment*

2007 Retail Catchment Map Centre Class Average Major Centre

Retail Footprint Score 543 Centres competing

Ranking 53 locally within Derby’s

catchment shoppers

Comparison goods exp £429.7m include Burton-On-

Share of 15 minute catchment 63.8% Trent, McArthur-Glen

Outlet Centre at

Share of 15-30 min catchment 14.8% Mansfield, the

Share of 30-45 min catchment 1.0% metropolitan towns of

Long Eaton and

Ilkeston.

Belper local centre and

the Wyvern and

Kingsway retail parks

trade within Derby’s

core market area.

Derby’s main

competitor is

Nottingham, located

over 30 minutes

drivetime away.

Despite relative low

levels of local

competition, Derby’s

catchment in 2007

was not filling its full

potential – in

particular with respect

to it not extending

further into the 30

minute drivetime of

the city.

* This scenario was prior to the opening of the Westfield Extension in Derby

Page 12CACI Property Consulting

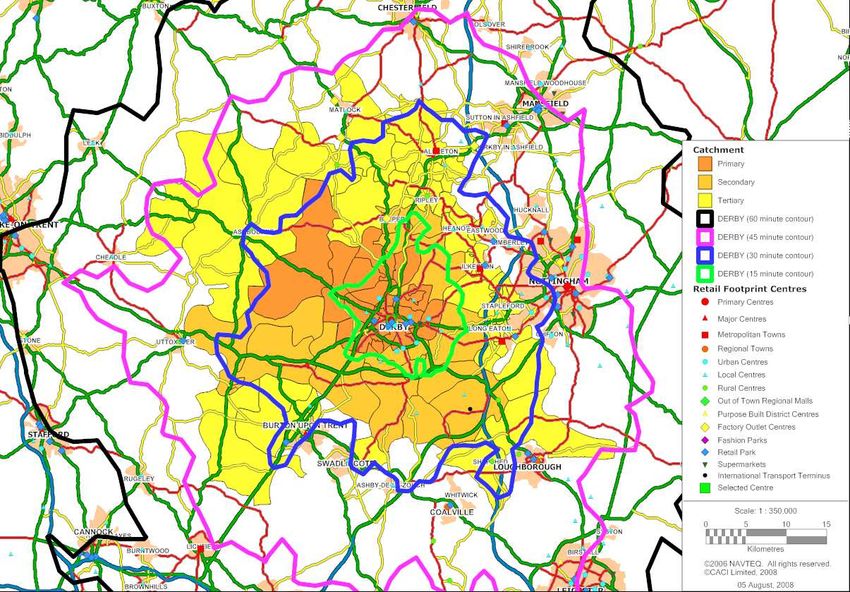

Derby 2008 catchment*

2008 Retail Catchment Map Centre Class Average Regional Centre

Retail Footprint Score 716 Derby’s new Major

Ranking 38 Catchment, where

90% of spend comes

Comparison goods exp £682.9m from, has substantially

Share of 15 minute catchment 76.1% expanded following

the opening of the

Share of 15-30 min catchment 29.9% Westfield extension. It

Share of 30-45 min catchment 4.0% is now contained

within a 45 minute

drivetime of Derby.

The Core Catchment

(Primary & Secondary)

is contained within a

30 minute drivetime.

To the south and

south-east of Derby,

the major catchment

is contained within 30

minutes, due to the

influences of Burton-

On-Trent and

Loughborough.

To the east and north-

east the catchment is

similarly contained,

due to Nottingham,

just 30 minutes away.

There is less

competition to the

west, meaning the

catchment extends

further.

* This scenario is prior to the opening of Leicester’s Highcross extension and Nottingham Trinity Square scheme due to open later in 2008.

Page 13CACI Property Consulting

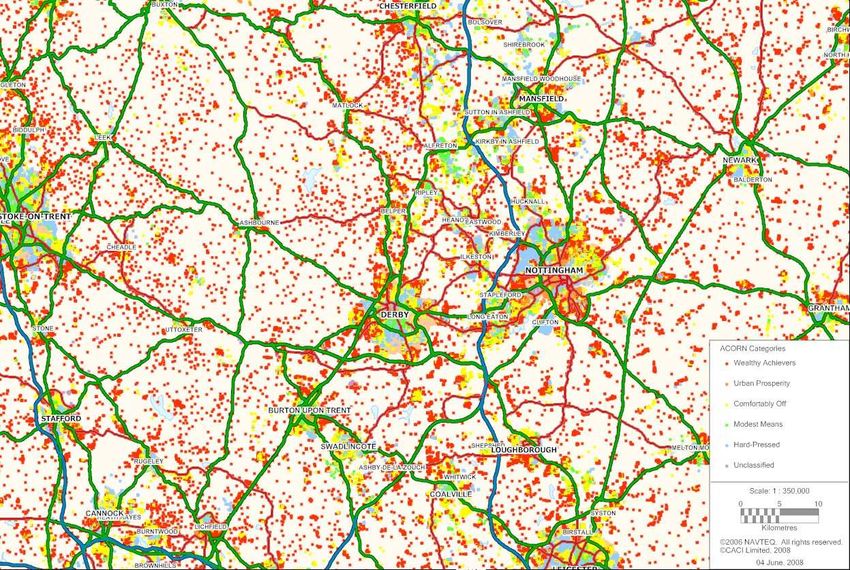

Derby Catchment Area: ACORN Spatial Distribution

The ACORN Category

of each postcode in

the catchment area of

Derby has been

plotted, providing a

visual clue to the

spatial distribution of

Derby’s varying

demographic groups.

The higher

concentration of

‘ACORN dots’ reflects a

larger concentration of

postcodes, and hence

population.

A number of

residential areas

within Derby’s

catchment have been

identified on the map,

which represent

important areas from

which Derby needs to

attract trade. These

areas are used on the

next page to

understand what

market share Derby is

taking from these

areas.

Page 14CACI Property Consulting

Current Shopper Flows Map

The better north-south connections

compared with east-west is a benefit

to Derby’s ability to attract market

shares.

The areas to the north and west

access Nottingham via Derby, which

means Derby achieves higher market Competition

shares from these residents. here with

Nottingham is

intense.

Market shares

extend further west

due to less

competition.

Derby is in direct competition with

Nottingham in this area, with Derby

benefiting from the residents living

west of the M1. The Westfield

extension has succeeded in turning

customers back towards Derby.

Wealthier residents living to the

This area is good territory for Derby,

north of Burton-On-Trent now have

with Nottingham further away and a

an alternative to shopping in their

weaker retail offer in Burton-On-

more local Average Centre. These are

Trent & Loughborough.

newly won customers, due to the

improved offer from the Westfield

extension.

Page 15CACI Property Consulting

Derby’s Catchment Residents: ACORN Group Profile

Derby Shopper Profile 07 Derby Shopper Profile 08 UK average 30 minutes of Derby

20%

18%

16%

14%

% Shoppers

12%

10%

8%

6%

4%

2%

0%

es

es

s

ip

es

es

es

ys

t

ts

a

s

es

ls

ty

le

es

s

u

er

bi

sh

te

oo

iti

ili

ili

na

i li

gl

O

re

si

ng

il i

iv

ur

n

m

m

ni

m

un

d

in

er

am

G

R

io

g

io

ut

ar

Si

ub

Fa

ba

Fa

t in

a

S

dv

ss

m

ns

r

t

ec

F

H

lla

n

lF

g

d

S

Ur

m

fe

ar

A

g

ue

ng

Pe

re

Ex

in

ne

e

Co

ia

in

d

Co

o

St

s

y

ir

cu

ed

ffl

hi

tle

Pr

i

de

gl

tr

it

t

-R

sp

e-

hy

en

s

A

C

Se

us

ug

at

an

et

ri

ur

s

lu

A

h

lt

ud

r

u

uc

ou

nd

S

ig

ea

si

tr

B

B

ne

ro

H

Pr

A

S

Ed

Fl

-I

W

In

pe

st

os

Po

Pr

Derby’s catchment shopper demographic profile provides strong market opportunities, with an above average presence of

Wealthy Achievers and a particularly high level of Secure Families (15.9% of shoppers, index of 111 against UK average).

There are indices of Wealthy Executives, Affluent Greys, Flourishing Families and Settled Suburbia are 8.7%, index of 114,

13.3%, index of 166, 9.2%, index of 115 and 10.4%, index of 159 respectively. This means Derby will be more resilient to an

economic turn-down and has a large population of family groups – who have particularly strong shopping patterns, supporting

a wide-range of retail categories.

Derby’s catchment is generally older and more suburban and rural than those of larger cities, with less Professionals, Educated

Urbanites and Aspiring Singles than the UK average. The impact of improving the retail offer in Derby has been to draw in

more people from all groups, but in particular the relative proportion of Affluent Greys and Flourishing Families has increased.

NB Derby Shopper Catchment Profiles ’07 and ’08 derived from respective Retail Footprint catchments. The difference in profiles is the result of the

Page 16 change in shopper catchment between 2007 and 2008 due to the improved shopping offer brought about by the Westfield Extension. It should

be noted that this profile shows the POTENTIAL to draw spend from each group, as opposed to actual spend attainment.CACI Property Consulting

Derby’s Catchment Residents: ACORN Group Profile

Derby Nottingham

20%

18%

16%

14%

% Shoppers

12%

10%

8%

6%

4%

2%

0%

s

ut

ys

ip

es

ia

es

es

ty

es

rs

s

es

es

ls

s

s

le

ot

ie

ve

rb

sh

na

O

ne

re

si

gl

ili

ili

ili

it

ili

ng

o

it

er

ti

n

u

m

g

n

m

G

rd

am

m

io

R

io

n

ba

ub

Si

in

Si

u

dv

u

Fa

Fa

Fa

ss

t

a

ns

r

ec

en

m

rt

a

F

H

r

g

S

ed

A

fe

U

ll

Pe

in

Ex

a

g

m

g

al

re

u

d

e

co

St

in

y

ro

en

in

d

is

fl

ri

ir

le

o

cu

it

nt

y

te

e-

gl

C

f

sh

sp

st

P

R

tt

rd

C

A

h

Se

ca

g

de

an

lu

du

s

Se

lt

h

ri

A

er

u

ru

ou

ig

ea

B

u

u

B

ru

si

In

n

Ed

o

St

H

er

W

In

A

P

Fl

t

sp

os

ro

P

P

Derby’s profile of Wealthy Executives, Affluent Greys and Flourishing Families is as strong as that of Nottingham, and actually

has higher relative proportions of Secure Families and Settled Suburbia.

Whilst difficult to compete against Nottingham for the younger and more urban lifestyle groupings, Derby’s profile enables

Derby to compete for custom from all other shopping groups. The main exception here would be the Starting Out group,

where there is the same relative proportion of this group in Derby’s catchment as there is in Nottingham.

There is an opportunity for Derby to differentiate from Nottingham by focusing on its profile strengths, to appeal to family

groups and older groups.

Page 17CACI Property Consulting

ACORN Groups – Typical Retailers

Wealthy Affluent Flourishing Prosperous Educated Aspiring Starting Secure Settled

Executives Greys Families Professionals Urbanites Singles Out Families Suburbia

John Lewis Jacques Vert Polo Ralph Lauren Karen Millen Diesel Mango Warehouse Debenhams Marks & Spencer

Russell & Bromley Country Casuals Fiorelli L K Bennett Whistles Zara Oasis Next Hawkshead

Mulberry Church's Lacoste Reiss Jigsaw Office Schuh Dorothy Perkins Clarks

Mappin & Webb Viyella Petit Bateau Hobbs Ted Baker GAP Sole Trader Top Shop Wallis

DAKS Windsmoor Ecco Hugo Boss Dune Elle Bank Mothercare Principles

Austin Reed Marks & Spencer Daisy & Tom Gieves & Hawkes Crew Clothing Adams HoF

Molton Brown EWM Fat Face Pink T M Lewin Miss Selfridge H&M

Bally Monsoon Jo Malone River Island

Prudent Asian Post Industrial Blue-collar Struggling Burdened High Rise Inner City

Pensioners Communities Families Roots Families Singles Hardship Adversity

Damart Littlewoods New Look Barratts Woolworths Aldi Internacionale Bon Marche

Scholl Morrisons Bay Trading Co Burton M K One Shoe Express Bacons Shoes QS

Littlewoods Matalan H Samuel Peacocks Stead & Simpson Primark Bewise Shoefayre

BHS Argos T K Maxx George Ciro Citterio Cromwell's Madhouse The Officers Club

Claire's Slater Menswear BHS Shoe Zone

Ethel Austin TJ Hughes

Wealthy Executives are some of the most affluent people in the UK. They live in wealthy, high status suburban, rural and

semi-rural areas of the country. Since incomes in this group are high, the shoppers favour upmarket, quality retailers such as

Jigsaw, Austin Reed, Jaeger, Ted Baker, John Lewis, Jones the Bootmaker, Karen Millen and Monsoon.

Flourishing Families are wealthy families with mortgages. The live in established suburbs, new housing developments around

commuter towns and villages and rural areas. These are high income achievers, successfully juggling both jobs and families.

Preferred shops range from the upmarket traditional House of Fraser & John Lewis to the mass brands of Debenhams. H&M,

Fat Face, Coast and The Body Shop.

Secure Families comprises of home owning families living comfortably in stable areas in suburban and semi-rural locations.

People are employed in a range of occupations, including middle management and clerical roles. The retail choices of Secure

Families demonstrate lower spending patterns with many mass and value retailers featuring. Dorothy Perkins, New Look,

River Island and Miss Selfridge for womenswear and Next for men.

Page 18CACI Property Consulting

Current Catchment Summary – RF Catchment Areas

Total comparison Weighted

Total Total Market

Catchment goods expenditure Market

population households Share

(£m) Potential (£m)

Primary 209,187 89,912 £457.6 £345.5 75.5%

Secondary 150,852 64,183 £346.9 £167.1 48.2%

Tertiary 323,293 140,523 £731.9 £102.8 14.0%

Outside £67.5

Core 360,039 154,095 £804.5 £512.6 63.7%

Major 683,332 294,618 £1,536.3 £615.4 40.1%

Total £682.9

Derby currently attracts Comparison goods market potential of £682.9m per annum.

The major catchment area (Primary, Secondary and Tertiary) is where 90% of Derby’s comparison goods spend is

estimated to come from. Comparison goods expenditure from this area is £615.4m. This is generated from a major

catchment area of 663 thousand households with an annual Comparison goods spend of £1.5 billion.

Derby captures a 75.5% market share from the Primary catchment and 48.2% from the secondary catchment, together

generating Comparison goods expenditure of £512.6m from this core catchment area, where 75% of Derby’s comparison

goods spend is estimated to come from.

The market share achieved from the core catchment is 63.7%, whilst the market share achieved across the major

catchment is 40.1%.

Page 19CACI Property Consulting

Current Catchment Summary – Drivetime Catchment Areas

Total comparison Weighted

Total Total Market

Catchment goods expenditure Market

population households Share

(£m) Potential (£m)

0-15 Mins 156,495 68,329 £335.5 £255.4 76.1%

15-30 Mins 500,395 214,795 £1,121.4 £335.6 29.9%

30-45 Mins 940,374 403,778 £2,111.3 £85.2 4.0%

45-60 Mins 517,195 225,466 £1,185.7 £6.7 0.6%

0-30 Mins 656,890 283,124 £1,456.9 £591.0 40.6%

0-45 Mins 1,597,264 686,902 £3,568.2 £676.1 18.9%

0-60 Mins 2,114,459 912,368 £4,753.9 £682.8 14.4%

Derby currently attracts Comparison goods market potential of £682.8m per annum from within a 60 minute drivetime

catchment. This is generated from a catchment area of 912 thousand households with an annual Comparison goods

spend of £4.7 billion.

Derby captures a 76.1% market share from the 15 minute catchment and 29.9% from the 15-30 minute catchment,

together generating Comparison goods expenditure of £591.0m from this 30 minute catchment area, where 87% of

Derby’s comparison goods spend is estimated to come from.

The market share achieved from the 30 minute catchment is 40.6%, whilst the market share achieved across the 45

minute catchment is 18.9% and across the 60 minute catchment area is 14.4%.

Page 20CACI Property Consulting

Leakage to Competing Centres

Derby's current market penetration of its major catchment is 40.2% and 63.5% of its core catchment, making it the dominant

retail centre within its catchment.

The list of centres taking market share from Derby’s catchment has been ranked by the share of its major catchment. Other

than Derby, only Nottingham and Burton-on-Trent takes more than 5% market share of this catchment area, where 90% of

Derby’s current shoppers are estimated to come from.

In relation to the core catchment, other than Derby only Nottingham takes more than 5% market share. Burton-on-Trent

takes 3.9% whilst Wyvern and Kingsway Retail Parks take 2.5% and 2.4%, and Belper 2.0%.

This means that Derby has very little in the way of significant local competition, with its only main competitor being

Nottingham.

Centre Name Retail Classification Retail Ranking Market Market Share

(2008) Share (Core)

(Major)

Derby Average Regional Centres 38 40.2% 63.5%

Nottingham Principal Centres 7 16.0% 10.3%

Burton-on-Trent Lower Average Centres 125 8.5% 3.9%

Mansfield - McArthurGlen Outlet Centre Major FOCs Mass Market 217 2.8% 1.7%

Long Eaton Lower Average Metropolitan Towns 538 2.6% 0.8%

Ilkeston Value Metropolitan Towns 615 2.4% 0.6%

Heanor Average Local Centres 740 2.0% 0.6%

Ashbourne Rural Centres 886 1.8% 0.2%

Ripley Rural Centres 836 1.8% 0.7%

Alfreton Value Metropolitan Towns 669 1.7% 0.1%

Belper Average Local Centres 972 1.6% 2.0%

Derby - Wyvern Retail Park Retail Parks Minority Fashion 1041 1.5% 2.5%

Derby - Kingsway Retail Park Retail Parks Minority Fashion 1087 1.3% 2.4%

Spondon - Asda Wal-Mart Supermarkets 1304 1.0% 1.5%

Leicester Quality Regional Centres 14 0.9% 0.9%

Page 21CACI Property Consulting

Section Summary – Derby’s Current Catchment

Since last year, following the opening of the 36,897 sqm gla Westfield Extension in October 2007,

Derby has seen substantial growth in its trading catchment area and market penetration of existing

trading areas.

Market Potential has increased by 65%, from £414.2m to £682.9m per annum – increasing Derby’s

UK ranking from 63rd to 38th.

Derby’s catchment area contains strong concentrations of Wealthy Executives, Affluent Greys,

Flourishing Families and Secure Families. This means that there are particularly strong retailing

opportunities for the centre, and that engaging with these groups will be critical to maximising

Derby’s potential as a retail destination.

Derby’s catchment is generally older and more suburban and rural than those of larger cities, with

less Professionals, Educated Urbanites and Aspiring Singles than the UK average.

The impact of improving the retail offer in Derby has been to draw in more people from all groups, but

in particular the relative proportion of Affluent Greys and Flourishing Families has increased.

Derby has very little in the way of significant local competition, with its only main competitor being

Nottingham.

There is an opportunity for Derby to differentiate from Nottingham by focusing on its profile strengths,

to appeal to family groups and older groups.

Page 22CACI Property Consulting

Derby City Retail Circuit

3. Centre Benchmarking & Potential to change

Market Positioning

Page 23CACI Property Consulting

Derby 2008 – Current Benchmarks

CACI have used ACORN and expenditure data to identify towns with a similar market potential size (in terms of Comparison

Goods expenditure) and shopper lifestyle profile to Derby, that share a post-industrial heritage. The similarity of the ACORN

profile is measured by the degree of correlation. A correlation of 1 is a perfect match with Derby. A correlation greater than

0.70 is considered to be a strong fit.

Southampton is classed as a ‘Quality Regional Centre’, whilst Leicester and Sheffield are classed as an ‘Average Regional

Centre’ in Retail Footprint; the same as Derby. Bradford and Coventry are classed as ‘Major Centres’; one classification

beneath the ‘Regional Centre’ classification, and have much lower market potential sizes; more similar to Derby pre Westfield

extension. Furthermore, the profiles of these city’s do not correlate so well with that of Derby.

The performance of Leicester shown here is prior to the opening of the Highcross Extension, which will take Leicester from

‘Average’ to ‘Quality’ Regional Centre. Alongside the benchmarks, Nottingham is included in the analysis, as Derby’s main

competitor. Nottingham is classified as a ‘Principal Centre’ – a classification above ‘Regional Centre’.

Annual Comparison Expenditure

£1,600 1.00

£1,400

0.90

£1,200

Correlation

£1,000 0.80

(£m)

£800

£600 0.70

£400

0.60

£200

£0 0.50

by

ry

d

ld

r

on

am

or

te

nt

er

fie

pt

es

f

gh

ad

ve

D

ef

m

ic

tin

Sh

Co

Br

ha

Le

ot

ut

N

So

Comparison Expenditure (£Millions) Correlation

Page 24CACI Property Consulting

Derby’s Current Benchmarks – ACORN profile

The individual profiles of Leicester, Southampton and Sheffield each vary from the profile of Derby in different ways, but

generally fit well to Derby’s profile, although in both Southampton and Sheffield the proportions of Prosperous

Professionals, Educated Urbanites and Aspiring Singles are higher, where Derby’s profile is weaker.

Leicester has the closest overall fit to Derby, albeit with lower relative levels of Affluent Greys and higher relative levels

of Secure Families, but sharing the characteristic of lower levels of Prosperous Professionals, Educated Urbanites and

Aspiring Singles. Both Bradford and Coventry are most dissimilar to Derby, due to much lower levels of Wealthy

Executives, Affluent Greys and Flourishing Families, against much higher levels of Asian Communities in Bradford and

Post-Industrial Families and Blue-collar Roots in Coventry.

Derby Leicester Southampton Sheffield Bradford Coventry

25%

20%

% Shoppers

15%

10%

5%

0%

s

es

es

p

es

es

ut

s

ys

a

s

es

s

ls

ity

le

es

s

le

hi

ot

er

bi

te

iti

ili

ili

ili

O

na

re

ng

ili

ng

ds

iv

rs

ur

Ro

on

m

am

ni

m

un

m

G

g

io

ut

ve

ar

Si

Si

ub

Fa

ba

t in

Fa

si

Fa

m

s

r

nt

ec

F

H

Ad

lla

en

es

g

d

S

Ur

ar

m

e

g

ng

re

rin

Ex

e

l

se

of

o

flu

ria

lin

d

tP

en

Co

St

ty

cu

-c

ed

le

hi

pi

Pr

Ri

y

gg

Af

st

en

Ci

rd

tt

ue

r is

Se

As

lth

at

n

du

h

us

Se

ru

Bu

ia

ud

r

Bl

uc

ou

ig

ea

ne

As

In

ro

St

H

Pr

Ed

Fl

W

In

pe

st

os

Po

Pr

Page 25CACI Property Consulting

Derby’s Current Benchmarks – average ACORN profile

The overall fit with the benchmark average provides a reasonable good fit with Derby. However, Derby has higher

relative levels of Wealthy Executives, Affluent Greys, Flourishing Families, Secure Families, Settled Suburbia and

Struggling Families than the benchmark average. This is counter-balanced with lower relative levels of Prosperous

Professionals, Educated Urbanites, Aspiring Singles, Post-Industrial Families, Burdened Singles and High Rise Hardship.

Derby Current Benchmark Average

20%

18%

16%

% Shoppers

14%

12%

10%

8%

6%

4%

2%

0%

s

es

es

p

es

es

es

ut

ys

a

s

s

es

ls

ity

le

es

s

hi

ot

bi

er

te

iti

ili

ili

il i

O

gl

na

re

ng

ili

ds

iv

rs

ur

Ro

on

m

m

ni

m

un

in

m

G

g

io

ut

ve

ar

Si

ub

Fa

ba

Fa

t in

Fa

S

i

Fa

s

m

s

nt

r

ec

H

Ad

lla

en

es

g

d

S

Ur

ar

m

e

g

ng

re

rin

Ex

e

l

se

o

of

flu

ria

lin

d

tP

en

Co

St

ty

cu

-c

ed

le

hi

pi

Pr

Ri

y

gg

Af

st

en

Ci

rd

ue

tt

ris

Se

As

lth

at

n

du

h

us

Se

ru

Bu

ia

ud

r

Bl

uc

ou

ig

ea

ne

As

In

ro

St

H

Pr

Ed

Fl

W

In

pe

st

os

Po

Pr

Page 26CACI Property Consulting

Benchmarks: Market Positioning

Comparing the current market positioning of Derby’s multiple comparison goods stores with the market

positioning of its benchmarks demonstrates that Derby has a stronger mass-bias than the average, with a

lower level of value stores.

Both Leicester and Southampton have higher overall RF Scores (reflecting a higher overall presence of

multiple comparison goods stores) and a higher level of Premium. Derby’s current retail positioning is most

similar to Plymouth, which also has a strong mass-bias. Sheffield, Coventry and Bradford all have much

higher relative levels of value retailers and a lower level of Premium.

The healthy presence of premium independents in Derby, and its demographic profile, that contains more

Wealthy Achievers and Secure Families than across its current benchmarks would all suggest that Derby

should be performing better than these centres, with an opportunity to develop a premium multiple market.

This opportunity is particularly pertinent to retaining spend from Nottingham, whose overall multiple

comparison goods retail offer is not only 70% larger (based on RF Score) but has a higher relative mix of

premium stores.

The strong premium multiple market in Nottingham can be viewed as a threat to developing one in Derby. To

qualify the opportunity, more evidence is needed on other centres which have achieved a strong multiple

premium market despite a larger, dominant neighbour.

Centre Name RF Score Premium % Mass % Value %

Derby 716 15.6% 62.8% 21.7%

Nottingham 1202 22.9% 56.7% 20.4%

Leicester 782 18.4% 56.5% 25.2%

Southampton 785 18.6% 57.6% 23.7%

Sheffield 753 11.6% 54.5% 33.9%

Bradford 699 7.1% 58.2% 34.7%

Coventry 730 9.9% 55.0% 35.1%

Benchmark Average 750 13.1% 56.4% 30.5%

*Based on count of multiple fascias only, Derby data updated from audit

Page 27CACI Property Consulting

Main Competing Centres on catchment: Market Positioning

The table below shows the current top six competing centres on Derby’s catchment, detailing their size (in

terms of Retail Footprint score) and market positioning in comparison to Derby.

Nottingham is Derby’s key competitor. It has a larger Retail Footprint score and has a much higher level of

premium outlets. This means that not only does Nottingham have a larger retail offer, it better caters for the

more affluent groups in Derby’s catchment – meaning that currently more of their spend will leak from the

Derby catchment to Nottingham.

Other than Nottingham, all other centres competing within Derby’s catchment have a higher mix of value

retailing than Derby (where the mix is already high), and therefore are more effective at competing for spend

from lower income groups and bargain hunters.

This highlights a key opportunity for Derby to improve its performance against its dominant competitor, by

growing a niche premium offer within the city centre, that will retain and attain greater patronage and spend

from the wealthier groups in Derby’s catchment.

Centre Name RF Score Premium % Mass % Value %

Derby 716 15.6% 62.8% 21.7%

Nottingham 1299 22.9% 56.7% 20.4%

Burton-on-Trent 429 5.6% 54.4% 40.0%

Mansfield - McArthurGlen Outlet Centre 61 10.8% 51.4% 37.8%

Long Eaton 173 0.0% 56.3% 43.8%

Ilkeston 130 4.0% 48.0% 48.0%

Page 28CACI Property Consulting

Derby 2008 –Aspirational Benchmarks

CACI have used ACORN and expenditure data to identify towns with a similar market potential size (in terms of Comparison

Goods expenditure) and shopper lifestyle profile to Derby, that can help qualify the opportunities for Derby to develop a

premium market. The similarity of the ACORN profile is measured by the degree of correlation. A correlation of 1 is a perfect

match with Derby. A correlation greater than 0.70 is considered to be a strong fit.

All of the selected benchmarks, excluding Sheffield, are classed as ‘Quality Regional Centres’ in Retail Footprint.

Bath, Chester and York are all particularly relevant benchmarks, due to their competitive position with the larger cities of

Bristol, Liverpool and Leeds respectively.

Annual Comparison Expenditure

£900 1.00

£800

£700 0.90

£600

Correlation

0.80

£500

(£m)

£400

0.70

£300

£200 0.60

£100

£0 0.50

by

rk

er

th

r

ld

m

te

Yo

et

Ba

er

fie

a

es

nh

Ex

D

ef

Ch

te

Sh

el

Ch

Comparison Expenditure (£Millions) Correlation

Page 29CACI Property Consulting

Derby’s Aspirational Benchmarks – ACORN profile

The individual profiles of the benchmarks each vary from the profile of Derby in different ways, but generally

fit well to Derby’s profile, with exception of the proportion of Prosperous Professionals and Educated

Urbanites, where Derby’s profile is weaker.

Chester has the closest fit to Derby, similar with respect to lower levels of Prosperous Professionals and

Educated Urbanites.

Derby Chester York Cheltenham Sheffield Bath Exeter

25%

20%

% Shoppers

15%

10%

5%

0%

s

es

es

p

es

es

ut

s

ys

a

s

es

s

ls

ity

le

es

s

le

hi

ot

er

bi

te

iti

ili

ili

ili

O

na

re

ng

ili

ng

ds

iv

rs

ur

Ro

on

m

am

ni

m

un

m

G

g

io

ut

ve

ar

Si

Si

ub

Fa

ba

t in

Fa

si

Fa

m

s

r

nt

ec

F

H

Ad

lla

en

es

g

d

S

Ur

ar

m

e

g

ng

re

rin

Ex

e

l

se

of

o

flu

ria

lin

d

tP

en

Co

St

ty

cu

-c

ed

le

hi

pi

Pr

Ri

y

gg

Af

st

en

Ci

rd

tt

ue

r is

Se

As

lth

at

n

du

h

us

Se

ru

Bu

ia

ud

r

Bl

uc

ou

ig

ea

ne

As

In

ro

St

H

Pr

Ed

Fl

W

In

pe

st

os

Po

Pr

Page 30CACI Property Consulting

Derby’s Aspirational Benchmarks – average ACORN profile

The overall fit with the benchmark average provides a particularly good fit with Wealthy Executives, Affluent Greys and

Flourishing Families. However, Derby has lower proportions of Prosperous Professionals and Educated Urbanites, and

higher proportions of Secure Families and Settled Suburbia – presenting stronger opportunities amongst older

consumer groups and family groups.

Derby Aspirational Benchmark Average

20%

18%

16%

% Shoppers

14%

12%

10%

8%

6%

4%

2%

0%

s

es

es

p

es

es

es

ut

ys

a

s

s

es

ls

ity

le

es

s

hi

ot

bi

er

te

iti

ili

ili

il i

O

gl

na

re

ng

ili

ds

iv

rs

ur

Ro

on

m

m

ni

m

un

in

m

G

g

io

ut

ve

ar

Si

ub

Fa

ba

Fa

t in

Fa

S

i

Fa

s

m

s

nt

r

ec

H

Ad

lla

en

es

g

d

S

Ur

ar

m

e

g

ng

re

rin

Ex

e

l

se

o

of

flu

ria

lin

d

tP

en

Co

St

ty

cu

-c

ed

le

hi

pi

Pr

Ri

y

gg

Af

st

en

Ci

rd

ue

tt

ris

Se

As

lth

at

n

du

h

us

Se

ru

Bu

ia

ud

r

Bl

uc

ou

ig

ea

ne

As

In

ro

St

H

Pr

Ed

Fl

W

In

pe

st

os

Po

Pr

Page 31CACI Property Consulting

Anchor Department Stores @ Benchmarks & Competing Centres

Derby: Debenhams, Co-Op, Bennetts

Nottingham:Debenhams, House of Fraser, John Lewis

Leicester: Fenwick, House of Fraser, John Lewis

Chester:Debenhams (Browns of Chester), TJ Hughes

Liverpool: John Lewis, Lewis’s, TJ Hughes, Debenhams*

York: Boyes, Browns of York, Debenhams, Fenwick Chester

Leeds: Debenhams, Harvey Nichols, House of Fraser

Cheltenham:Debenhams, House of Fraser

Bath:House of Fraser, Debenhams

Bristol: House of Fraser, Debenhams

Sheffield: Atkinsons, Debenhams, TJ Hughes, John Lewis

Meadowhall:House of Fraser, Debenhams

Exeter: Debenhams, House of Fraser

Bath

Source: EGI, CACI Retail Locations

Page 32CACI Property Consulting

Existing Malls & A1 Development Pipeline @ Benchmarks

Derby:

Westfield Derby – 90,897 sqm gla: (just completed 36,897 sqm gla extension)

Nottingham:

Victoria Shopping Centre – 91,137 sqm gla

The Pod – 9,290 sqm gla (opened 2007, mixed retail and hotel)

Trinity Square – 16,258 sqm gla: under construction

Westfield’s Broadmarsh – 44,227 sqm, gla: planned 76,073 sqm gla extension

The Pod - Nottingham

Chester:

The Mall – 20,903 sqm gla: Just sold to Carlyle, potential for 10,000 sqm ext.

Northgate Centre – 9,290 sqm gla

York:

Coppergate Shopping Centre – 13,935 sqm gla, Lasalle have just bought from Landsec and

appointed Centros to deliver circa 26,942 sqm gla extension.

Cheltenham:

Beechwood SC – 11,799 sqm gla Princesshay -

Regent Arcade – 17,837 sqm gla Exeter

Bath:

The Podium SC – 6,596 sqm gla

Multi’s Southgate Shopping Centre – 35,220 sqm gla (just completed 19,148 extension)

Exeter:

Henderson’s Princesshay Shopping Centre, opened Sep 07 – 36,308 sqm gla

Source: EGI, CACI Centre Futures

Page 33CACI Property Consulting

Existing Malls & Development Pipeline @ Sheffield

Existing Malls:

Orchard Square – 14,864 sqm gla (1987)

Moor Shopping Centre – 30,000 sqm gla (1997)

New A1 Retail Development

New Retail Quarter: Sevenstone, Hammerson – 79,896 sqm

gla under construction, to include John Lewis – due to open

New Commercial Office Development

Sevenstone - Sheffield

St Pauls Place (Norfolk Street), Heart of The City – 18,580

sqm gla – under development

Riverside Exchange – 12,820 sqm gla – under construction

Sheffield Digital Campus, Sheaf Street:–15,000 sqm gla in

phase 1 alongside ‘Electric Works’ creative space

The Square, Castlegate; 8,000 sqm gla 1st and 2nd phases,

full potential up to 15,000 sqm gla. Phase 1 complete.

St Pauls Place - Sheffield

Source: EGI, CACI Centre Futures

Page 34CACI Property Consulting

Aspirational Benchmarks: Market Positioning

Comparing the current market positioning of Derby with the market positioning of its benchmarks, shows

that the benchmarks have a higher representation of premium retailers than Derby, with exception of

Sheffield.

This demonstrates that whilst the recent extension of the Eagle Centre significantly improved market shares,

the size of its catchment and its UK ranking, Derby City Centre has further opportunities to capitalise on this

investment.

There is an unmissable opportunity to optimise its retail mix throughout the rest of the centre to alter the

overall market positioning of the centre. This change in market positioning should in turn maximise

conversion of the spend available within its catchment, in particular from the wealthier groups.

This opportunity is based on the current market potential of the centre, and is therefore is an opportunity for

immediate action – relating to improving the leasing of existing units throughout the city centre; drawing

footfall out of the Eagle Centre through a stronger city centre retail circuit.

Since the requirements of premium retailers are less dependent upon the size of retail floorplates, but rather

the quality of the high street environment, there exists a timely opportunity for the Derby BID to initiate this

new leasing scenario through investment in the public realm and partnership work with local landlords and

agents.

Centre Name RF Score Premium % Mass % Value %

Derby 716 15.6% 62.8% 21.7%

Chester 756 21.2% 62.4% 16.4%

York 755 22.9% 60.8% 16.3%

Cheltenham 728 26.9% 56.9% 16.3%

Sheffield 699 11.6% 54.5% 33.9%

Bath 611 31.4% 57.7% 10.9%

Exeter 665 17.4% 61.7% 20.9%

Average 702 21.9% 59.0% 19.1%

*Based on count of multiple fascias only, Derby data updated from audit

Page 35CACI Property Consulting

Market Positioning of Clothing & Accessories – Benchmark Targets

Comparing Derby’s clothing & accessories mix by market positioning against Derby’s aspirational

benchmarks, we confirm that the opportunity for improving the premium mix of Derby lies with the

opportunity to improve upon the representation of ‘Upper’ and ‘Upper Middle’ retailers in the centre.

These premium fashion retailers trade well in areas with good quality public realm, mixed in with strong

independent fashion and specialist stores.

There is an opportunity to build a cluster of such stores in the city centre, catalysing the development of a

strong, complementary area of retail pitch to the Eagle Centre, creating a point-of-difference for Derby

compared to out-of-town style shopping provision, and develop a city centre environment convivial to

attracting more of the Wealthy Executives, Affluent Greys and Flourishing Family groups.

Derby Aspirational Benchmarks

60%

50%

% Multiple Clothing Retailers

40%

30%

20%

10%

0%

Upper Upper Middle Middle Lower Middle Lower

*Based on count of multiple fascias only, Derby data updated from audit

Page 36CACI Property Consulting

Premium Retailer Model – sustainable levels of demand

To determine a sustainable level of premium shopping for Derby City Centre, post-development, CACI have

built a regression model to predict the average premium RF score supportable in centres across the UK,

based upon the ‘premium shopper population’ of each centre, defined by the estimated number of shoppers

in the following ACORN group categories: Wealthy Executives, Flourishing Families, Prosperous Professionals,

Educated Urbanites and Secure Families.

500

450

400

Premium RF Score

350

300

250

200

150

100

50

0

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000

Premium Shopper Population

Predicted Actual

Page 37CACI Property Consulting

Premium Retailer Model – sustainable levels of demand

The extended Westfield Derby has had the effect of significantly increasing the market potential of Derby to

support a strong cluster of premium retailers. However at current this opportunity has only been taken up as

far as what the Average Trend across the UK would predict.

Derby’s affluent catchment and BID improvements to the public realm in the Cathedral Quarter means that

there is potential to outperform this Average Trend, and work at the Upper Trend, performing closely to

benchmark towns of Cheltenham, Chester and Bath.

250 London -

Knightsbridge Norwich Upper Trend

Cheltenham Newcastle-

200 Tunbridge Upon-Tyne

Merry Wells Bath Southampton/

Meadowhall

Premium RF Score

Hill

Oxford Cardiff/Aberdeen

Chester

150 Solihull Bromley

Average Trend

Croydon

100 Watford

Sheffield

Thurrock

50

Derby 2008

Derby 2007

0

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000 55,000 60,000 65,000

Premium Shopper Population

Predicted Actual

Page 38CACI Property Consulting

Section Summary – Centre Benchmarking & Market Positioning

Comparisons with other post-industrial cities such as Leicester, Southampton, Plymouth, Sheffield and Hull

reveals that Derby has a stronger mass-bias than the benchmark average, with a lower level of value stores,

associated with a stronger level of Wealthy Executives, Affluent Greys, Flourishing Families, Secure Families

and Settled Suburbia compared with the average market these benchmark towns operate in.

In terms of demographic profile, Derby is closest to Leicester. Both Leicester and Southampton have a stronger

premium presence than Derby. Considering the healthy presence of premium independents in Derby, and its

strong demographic profile, Derby should be performing better with respect to its market positioning balance,

with a clear opportunity to develop a premium multiple market.

The strong premium multiple market in Nottingham can be viewed as a threat to developing one in Derby. To

qualify the opportunity, more evidence is needed on other centres which have achieved a strong multiple

premium market despite a larger, dominant neighbour.

Chester, York and Bath have all developed strong premium multiple markets in the shadow of a more dominant

neighbour. Other relevant benchmarks, which have similar market potential size and demographic profile

include Cheltenham and Exeter. Sheffield has also been selected as a particularly relevant benchmark – a city

which needs to compete against Meadowhall and which has a strong set of office developments in the pipeline,

despite strong competition with Manchester, Leeds and Nottingham in terms of office markets.

Comparisons with these cities/towns qualifies that there is an economically sound argument for Derby to

strengthen its premium market, with opportunities to attract a significant number of additional ‘upper’ and

‘upper-middle’ clothing and premium home, jewellery and toiletry retailers.

In order to achieve this, Derby will need to create a step-change in the way that it is perceived, by both the

retail community as well as consumers, to achieve a premium market, supportable along the lines of an ‘Upper

Trend’ established by a number of successful towns and cities across the UK.

Chester, York and Bath benefit from heritage and a strong tourism strategy. Sheffield does not operate under

the shadow of a nearby dominant centre. Therefore, despite the comparisons, ultimately Derby’s situation and

future development strategy will be unique to Derby. The key lessons to draw is that Derby needs to have a

wider point of interest than retailing alone, and like Sheffield, will need to develop a much stronger city-based

employment sector to support the city retail economy, in the absence of such a strong tourism market as other

benchmarks enjoy.

Page 39CACI Property Consulting

Derby City Retail Circuit

4. Current Retail Provision & Pitch

Performance

Page 40CACI Property Consulting

Derby City Centre– Identified Areas

The city centre and

North Area the adjoining

riverside and North

Castleward areas has

been divided into 4

distinct areas.

The Retail Core is

where the core city

centre retailing

occurs, and broadly

fits with DCC’s

current planning

boundaries.

West Area East Area The limits of the new

Cathedral Quarter

BID (red) are also

Retail Core shown which broadly

encompasses the

identified north-west

business area.

© Crown Copyright. All rights reserved. (100024913) (2008)

Page 41CACI Property Consulting

Derby City Centre– Places of Note

Joseph Wright College

Derby Cathedral

Fountain – Market Place

Ark –Sadler Gate

Friar Gate Sadler Gate

Market Place

Victoria Street

Pedestrianised Street

St Peters Street – St Peters Street

La Tasca –Friar Gate

Westfield Derby

Westfield Shopping Mall

Buses – Victoria Street

© Crown Copyright. All rights reserved. (100024913) (2008)

Page 42CACI Property Consulting

Derby City Centre – Audit June ‘08

On the 23rd June 2008 CACI conducted a detailed retail floorspace audit of all retailers currently trading in the

Retail Core of Derby to determine:

Derby’s current retail provision by fascia category (Clothing, Health & Beauty, Leisure Goods etc.)

Current Operator Configuration (Department Store, Variety Store, MSU, Multiple and Independent)

Floorspace provision by Retail Pitch (Westfield Derby, St Peters Street, Sadler Gate etc.)

This critical appraisal of current retail supply has enabled CACI to draw conclusions on the relative strength of

competing areas of retail pitch and operator configuration and market positioning relative to catchment

potential and demand.

In order that this report remains relevant at point of publication, the old M&S store in the Cornmarket has been

entered into the audit as the new Primark, and the old M&S food hall a new Tesco-Metro.

To estimate net internal trading areas, CACI auditors have paced the size of every retail unit open for trade.

For vacant premises, CACI have used either OS mapping or estimated the available net trading space from

taking external measurements of the unit.

Page 43CACI Property Consulting

Retail & Services Provision – Floorspace Breakdown

Retail / Service Provider Net Sq. M % of RCG % of Total Derby city centre’s Retail Core

Category currently provides 79,056 net

sq.m. in the core ‘Retail

Centre Goods’ (RCG)

Department Stores 20,544 26.0% 17.1% categories, with the

Variety Stores 7,020 8.9% 5.8% department stores and

Clothing & Accessories 34,458 43.6% 28.6% clothing & accessories sector

representing 69.6% of this

Leisure Goods 7,186 9.1% 6.0% space.

Household Goods 3,047 3.9% 2.5% The Leisure Goods category

Health & Beauty 3,704 4.7% 3.1% has 9.1% of RCG floorspace,

Electrical Goods 3,098 3.9% 2.6% Household Goods has 3.9%

whilst Health & Beauty

Retail Centre Goods Sub-Total 79,056 100.0% 65.7% account for 4.7% and

Catering 9,495 7.9% Electricals 3.9%.

Markets 6,222 5.2% Amongst the 23.1% of retail

Supermarkets 3,144 2.6% floorspace categorised as Non-

RCG, Catering takes 7.9%, the

Convenience 588 0.5% markets take 5.2% of all

Other Sales of Goods* 1,034 0.9% space, Supermarkets

Banks and Building Societies 2,075 1.7% (Sainsbury’s and Tesco Metro)

2.6%, Banks & Building

Other Services** 4,030 3.3% Societies 1.7% and Other

Amusements/Betting Shops 1,263 1.0% Services 3.3%.

Non RCG Sub-Total 27,851 23.1% Total floorspace in Derby city

Non-Vacant Sub-Total 106,907 88.8% centre’s Retail Core available

for retail and services is

Vacant 13,501 11.2% 120,408 net sq.m. 13,501 net

Grand Total 120,408 sq.m. is vacant (11.2%).

NB. Retail Centre Goods are those retail categories which represent the majority of shopping centre trading activity

*Other Sales of Goods include antique shops, charity, florists and DIY.

Page 44 **Other Services include surgeries, dentists, estate agents, hairdressers, insurance, laundry, pawnbrokers, photo-processing, piercing and tattoo

studios, post office, recruitment, repairs, salon, travelCACI Property Consulting

RCG Operator Configuration (proportion of floorspace)

Other MSU's Other Variety Stores

Coop Bennetts 9% 2%

Primark

4% 2%

MAXX (T K) 4% Multiples - Units

2% 30%

BHS

2%

Wilkinson

2%

Matalan

3%

Woolworths

2%

Next Boots Independents

3% 2% Debenhams Marks & Spencer 15%

10% 8%

The town is anchored by a number of Department Stores, Variety Stores and major space users (MSUs) accounting for 55.7%

of net space. There are currently five department stores, of which just Debenhams and M&S occupy a significant floorplate. The

circa 8,500 sq m net Debenhams is located in the new Westfield Derby centre, on the southern end of the centre – meaning it

is located right on the edge of the city centre. Debenhams was previously located on Victoria Street. The Marks & Spencer is a

circa 7,000 sq m net store that joins the new Debenhams in anchoring the southern end of the new Westfield Derby centre.

M&S was previously located in two units; one on the top end of St Peters Street and the other on Cornmarket. Together they

take 19% of floorspace.

Derby’s other Department, Variety and MSU stores together take up 35% of space respectively and include Westfield Derby

centre –Boots, Woolworths, SportDirect.Com, New Look, Next, Zara, Top Shop, H&M,; St Peters Street– BHS, JJB Sports, ;

London Road – Woolworths, WH Smith, Matalan, Argos, Wilkinson; East Street – Co-Op, TK Maxx; Irongate – Bennetts and the

new Primark on Cornmarket.

Multiples (national retailers operating out of non-MSU units) currently account for the largest percentage of sales space in

Derby city centre, 32%. These are most highly concentrated in Westfield Derby, St Peters Street, East Street, Albion Street and

London Road.

There is also high concentration of independents in Derby, taking 15% of utilised retail space. These are most highly

concentrated in Babington Lane, Sadler Gate and Irongate. There is also strong independent presence in Green Lane,

Osmanton Road and The Strand.

Page 45CACI Property Consulting

Derby City Centre– Core Retail

North Side

Sadler Iron Gate

Wardwick Friar Gate

Gate

Cornmarket

East Side

Market Place

East

Curzon Street

St Peters Street

Street

Green Eagle

Lane

Westfield

The Spot

Extension

Green Lane

East Street

Babington Lane © Crown Copyright. All rights reserved. (100024913) (2008)

Page 46CACI Property Consulting

Retail Category – Floorspace (Net Sq M) by Primary Areas of Pitch

Retail / Service Provider Westfield East St Peters Corn Sadler Green

Category Extension The Spot Eagle Street Street market Gate Lane Total

Department Stores 14,199 0 0 2,835 1,839 0 1,671 0 20,544

Variety Stores 0 6,258 284 312 166 0 0 0 7,020

Clothing & Accessories 17,175 879 1,914 3,751 2,843 4,051 2,662 1,182 34,458

Leisure Goods 3,001 1,079 481 1,536 229 116 368 377 7,186

Household Goods 417 1,311 294 0 0 0 96 929 3,047

Health & Beauty 425 266 2,665 50 99 71 0 128 3,704

Electrical Goods 980 74 334 641 135 74 480 381 3,098

Retail Centre Goods Sub-Total 36,197 9,866 5,972 9,125 5,310 4,312 5,276 2,997 79,056

Catering 2,817 839 391 436 441 1,055 2,620 896 9,495

Market 0 0 4,405 0 0 1,818 0 0 6,222

Supermarket 0 0 1,555 0 1,589 0 0 0 3,144

Convenience 0 161 38 131 23 12 95 128 588

Other Sales of Goods 0 212 0 20 100 267 77 359 1,034

Banks and Building Societies 0 222 0 684 358 632 146 33 2,075

Other Services 295 672 197 124 186 814 1,087 655 4,030

Amusements/Betting Shops 0 164 0 205 133 139 308 315 1,263

Non RCG Sub-Total 3,112 2,270 6,585 1,599 2,829 4,738 4,332 2,386 27,851

Non-Vacant Sub-Total 39,309 12,136 12,558 10,724 8,139 9,050 9,608 5,383 106,907

Vacant 881 200 1,756 445 1,018 515 1,363 7,324 13,501

Grand Total 40,190 12,336 14,314 11,169 9,157 9,565 10,971 12,707 120,408

NB. Retail Centre Goods are those retail categories which represent the majority of shopping centre trading activity

*Other Sales of Goods include antique shops, charity, florists and DIY.

Page 47 **Other Services include surgeries, dentists, estate agents, hairdressers, insurance, laundry, pawnbrokers, photo-processing, piercing and tattoo

studios, post office, recruitment, repairs, salon, travelYou can also read