Getting Started on the Road to Recovery and - Spring Flooding Tax Filing Deadlines - Schreiber & Schreiber - nescpa

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Schreiber & Schreiber

Certified Public Accountants

Getting Started on the Road to Recovery

and

Spring Flooding Tax Filing Deadlines

Nebraska CPA Society

April 11, 2019

© 2019 Gerard H. Schreiber, Jr., CPA

1

Jerry Schreiber

• Partner with Schreiber & Schreiber

• Author, “Documenting a Casualty Loss”,

Journal of Accountancy, November 2008

http://www.journalofaccountancy.com/Issues/2008/Nov/Documenting+a

+Casualty+Loss.htm

• Presentations include Hurricanes Katrina, Rita, Wilma, Gustav, Ike,

Isaac, Irene, Sandy, Matthew, Harvey, Maria, Irma, Florence, and

Michael, 2010 Nashville TN flooding, 2012 Colorado Springs Fires, 2014

Oklahoma Tornadoes, South Carolina 2015 Flooding, Spring 2016

Louisiana Flooding, August 2016 Louisiana Flooding

• Member, AICPA IRS Advocacy and Relations Committee

• Author, "An Overview of AICPA and IRS Rules of Practice”, The Tax

Adviser, February 2014

• Author, “Tax Practice Quality Control”, The Tax Adviser, November 2012

• Author, "Circular 230 Best Practices”, The Tax Adviser, April 2010

• Author, “Strengthening Tax Services' Foundation”, Journal of

Accountancy, May 2009

• Contact at: ghschreiber@bellsouth.net Phone 504-832-1819

2

Today’s Topics

• General Overview and Resources

• IRS Filing Dates

• IRS Examples

3

E Mail Future Questions to:

ghschreiber@bellsouth.net

4

5

6

7

8

The Most Important Thing About

A Disaster:

Your Comfort Zone Disappears

9

Resources

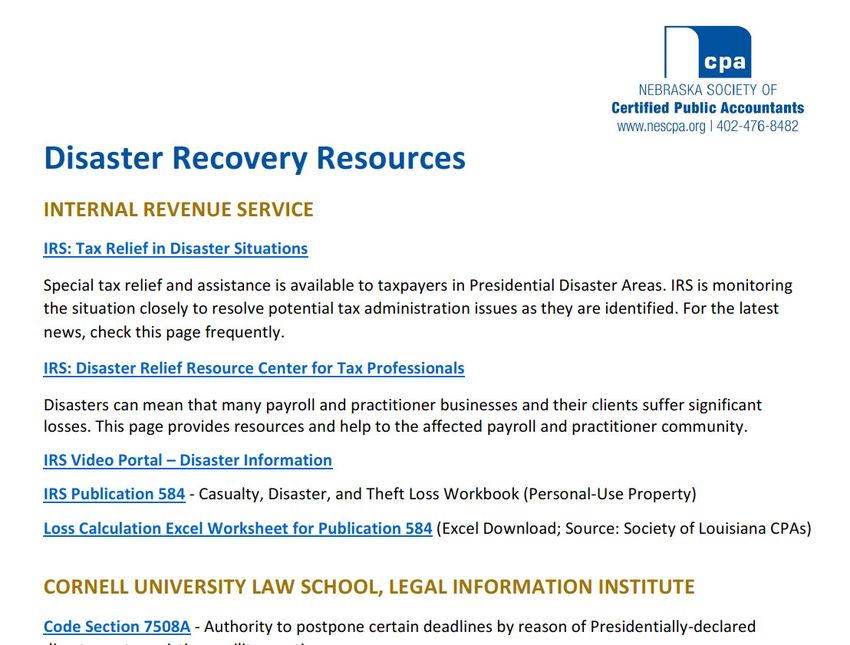

• AICPA Casualty Loss Guide

• IRS FAQ’s Disaster Victims http://www.irs.gov/Businesses/Small‐

Businesses‐&‐Self‐Employed/FAQs‐for‐Disaster‐Victims

• CPA Disaster Yahoo Group

http://finance.groups.yahoo.com/group/CPA_Disaster/

• Local Network Groups

• DisasterAssistance.gov

• FEMA

• Social Media

• Insurance Company List

http://www.iii.org/articles/insurance‐company‐claims‐

filing‐telephone‐numbers.html

• United Policyholders www.uphelp.org

1011

12

13

14

15

16

17

http://www.iii.org/articles/insurance-company-claims-filing-telephone-

numbers.html

Here is a list of claim contact numbers:

A

AAA Insurance (Auto Club Family Insurance Company) 800-222-7623 ext. 5000

Acadia Insurance Company 800-444-0049, ext. 2600

ACE Private Risk Services 800-945-7461

ACE USA Clients receive individual 800 numbers or call 800 945-7461 (ACE USA/ACE Recreational Marine

claims); 800 234-7354 (Disaster Mortgage Protection claims)

Acuity 800-242-7666

AGCS Marine 800-558-1606

Alabama Department of Insurance 334-269-3550

Alabama Municipal Insurance Corporation 866-239-AMIC

Alfa Insurance Group 888-964-2532

Allmerica 800-628-0250

Allstate 800-54-STORM (800-547-8676)

Allstate Floridian Insurance Company 800-54-STORM (800-547-8676)

America First Insurance 877-263-7890

America’s Health Insurance Plans (AHIP) 800-644-1818

American Bankers Insurance Company 800-245-1505

American Federation Insurance Company 800-527-3907

American General Property Insurance Company of Florida 800-321-2452

American International Group, Inc. (AIG) 877-244-0304

American National Property & Casualty Company & Affiliates 800-333-2860

American Reliable Insurance Company 800-245-1505

American Security Insurance Company 800-326-2845

American Skyline Insurance Company 888-298-5224

American States Insurance Company 888-557-5010

American Strategic Insurance 866-ASI-LOSS (274-5677)

American Superior Insurance 954-577-2202

Arch Insurance 800-817-3252

1920

Loss Diary/Workbook

2122

23

24

25

FEMA

Individual v. Public Assistance

26Individual Assistance

The Individuals and Households Program (IHP) can assist those affected

by the recent storms in Iowa by providing financial assistance for

housing or other needs. The program is available to all people who

qualify regardless of race, sex, religion, color or national origin. FEMA’s

IHP is available to both homeowners and renters.

The IHP has two provisions; Housing Assistance and Other Needs

Assistance.

Housing Assistance can provide funding for:

Referrals for rental housing

Financial assistance to rent a different place to live

Repairs to make the home safe, sanitary and functional

Replacement - financial assistance to replace destroyed homes

Other Needs Assistance may include funding for:

Medical, dental and funeral expenses

Essential personal property such as furniture, clothing and some

appliances

Repair or replacement of damaged vehicles

Other disaster-related expenses

27Individual Assistance(Continued)-

Individual assistance can also be in the form of federal low-interest

disaster loans from the U.S. Small Business Administration (SBA) for

homeowners, renters, businesses of all sizes, and private non-profit

organizations.

Homeowners may borrow up to $200,000 to repair or replace their

primary residence. Renters and homeowners may borrow up to $40,000

to replace personal property. Up to $2 million may be borrowed by

businesses for any combination of property damage or economic injury.

The SBA also offers working capital loans to small businesses and most

private, non-profit organizations of all sizes having difficulty meeting

obligations as a result of the disaster.

For information on SBA disaster loans, call (800) 659-2955 or visit

www.sba.gov. Hearing- or speech-impared individuals may call (800)

877-8339.

28Public Assistance

Under the Public Assistance Grant Program, FEMA awards grants

to assist state and local governments and certain private

nonprofit organizations with the response to and recovery from

disasters. The program provides funding for debris removal,

implementation of emergency protective measures and

permanent restoration of infrastructure. The program also

encourages protection from future damage by providing

assistance for hazard mitigation measures during the recovery

process. The program runs on a cost share with FEMA and the

applicant who may be the state or local governments.

Public assistance is based on a partnership between FEMA, state

and local officials. FEMA is responsible for managing the

program, approving grants and providing technical ...

29IRS Filing Issues and Dates

3031

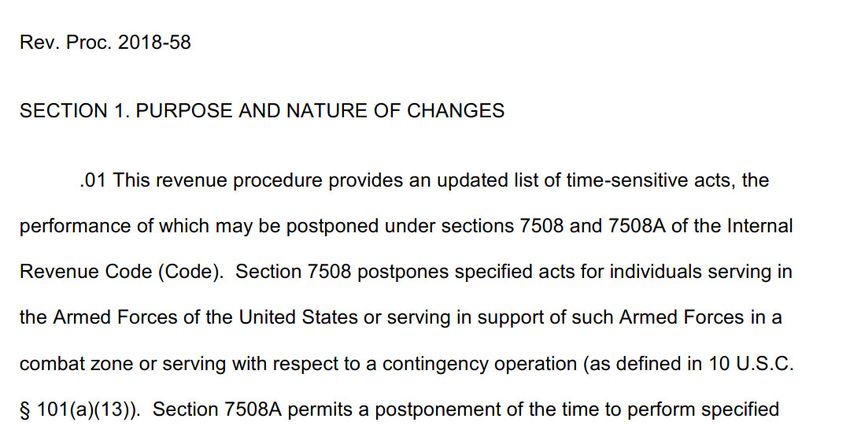

Unless an act is specifically listed in Rev. Proc.

2018-58, the postponement of time to file and

pay does not apply to information returns in

the W-2, 1094, 1095, 1097, 1098, or 1099 series;

to Forms 1042-S, 3921, 3922 or 8027; or to

employment and excise tax deposits.

32Form 5500

This relief also includes the filing of Form 5500 series

returns, (that were required to be filed on or after

March 9, 2019 and before July 31, 2019, in the manner

described in section 8 of Rev. Proc. 2018-58. The relief

described in section 17 of Rev. Proc. 2018-58,

pertaining to like-kind exchanges of property, also

applies to certain taxpayers who are not otherwise

affected taxpayers and may include acts required to be

performed before or after the period above.

33Schreiber & Schreiber

Certified Public Accountants

Tax Return Filings

34Code Section 7508A

•Section 7508A provides the Secretary of Treasury with

authority to postpone the time for performing certain

acts under the internal revenue laws for a taxpayer

affected by a federally declared disaster as defined in

section 165(h)(3)(C)(i), or

•A terrorist or military action ……..

•The Secretary may specify a period of up to one year

may be disregarded in determining, …., in respect of

any tax liability of such taxpayer whether the

performance of acts were performed within the time

prescribed without regard to extension….

•Special rules regarding pensions

35Taxpayer Acts Eligible for Relief

• Filing of returns • Bringing a

• Payment of tax lawsuit upon a

claim for

• Contributions to credit/refund of

retirement plan tax

• Filing of a Tax • All eligible acts

Court Petition listed in Rev.

• Filing of a claim Proc. 2018-58

for refund (https://www.irs.gov/pu

b/irs-drop/rp-18-58.pdf)

3637

Affected Taxpayers

Any individual, any business entity or sole proprietor:

• whose principal residence or principal place of

business, is located in the covered disaster area

• who is a relief worker affiliated with a recognized

government or philanthropic organization and who

is assisting in the covered disaster area

• whose principal residence or principal place of

business, is not located in the covered disaster

area, but whose records necessary to meet a filing

or paying deadline are maintained in the covered

disaster area

38Affected Taxpayers (cont’d)

• Any estate or trust that has tax records necessary to

meet a filing or paying deadline in a covered disaster

area

• The spouse of an affected taxpayer, solely with

regard to a joint return of the husband and wife

• Any individual visiting the covered disaster area who

was killed or injured as a result of the disaster

• Any other person determined by the IRS to be

affected by a federally declared disaster

39Government Acts Eligible for Relief

• Assessing tax

• Giving or making any notice or demand for

payment of tax, or… to any liability to the US

in respect of any tax

• Collecting, by levy or otherwise, of any

liability

• Bringing suit ……

• Allowing a credit or refund

• Any other acts specified in a revenue ruling,

revenue procedure, notice, or other

guidance

40What May Be Postponed

Under Code Sec. 7508A, IRS gives affected taxpayers until the extended

date (specified by county, below) to file most tax returns (including

individual, estate, trust, partnership, C corporation, and S corporation

income tax returns; estate, gift, and generation-skipping transfer tax

returns; and employment and certain excise tax returns), or to make tax

payments, including estimated tax payments, that have either an original

or extended due date falling on or after the onset date of the disaster

(specified by county, below), and on or before the extended date.

IRS also gives affected taxpayers until the extended date to perform

other time-sensitive actions described in Reg. § 301.7508A-1(c)(1) and

Rev Proc 2018-58, that are due to be performed on or after the onset date

of the disaster, and on or before the extended date. This relief also

includes the filing of Form 5500 series returns, in the way described in

Rev Proc 2018-58, Sec. 8. Additionally, the relief described in Rev Proc

2018-58, Sec. 17, relating to like-kind exchanges of property, also applies

to certain taxpayers who are not otherwise affected taxpayers and may

include acts required to be performed before or after the period above.

41Key Terms of §301.7508A-1

•Federally declared disaster area

•Relief from interest, penalties, additional

amounts, or additions to tax during

postponement period

•Acts eligible for relief

•Affected taxpayers

42

42Regulation 301.7508A-1

• Have a copy of the Regs

• Look at the eight examples in the

Regs

4344

From IRS:

The IRS automatically identifies taxpayers located

in the covered disaster area and applies automatic

filing and payment relief. But affected taxpayers

who reside or have a business located outside the

covered disaster area must call the IRS disaster

hotline at 1-866-562-5227 to request this tax relief.

45IRM 21.5.6.4.30 (10-01-2016)

-O Freeze

The -O (Disaster Indicator) freeze will only be input systemically by Information

Technology Services (IT) at the request of the Disaster Program Office or on a case-by-

case basis by Compliance personnel. Employees outside of Compliance will no longer

input the -O freeze.

Reminder:

Taxpayers will no longer self-identify for disaster relief by writing a disaster designation in

red at the top of their tax return.

The -O freeze allows for special penalty and interest calculations

The -O freeze suppresses some Master File and IDRS notices

The -O freeze does not freeze the module from refunding

The -O freeze may be systemically set on identified taxpayer accounts in presidentially

declared disaster areas

The -O freeze is released when the current date is beyond the secondary date (disaster

ending date) of the TC 971 AC 087

When performing account research the -O freeze is seen on CC ENMOD, CC IMFOLE

or CC BMFOLE.

If a Practitioner calls, is located in a covered disaster area and maintains records for

several taxpayers located outside the disaster area, inform the Practitioner to:

Call the Special Service line 1-866-562-5227

46IRM 21.5.6.4.30 (10-01-2016)

-O Freeze

Prepare an excel spreadsheet for 10 or more taxpayers and mail it to:

Internal Revenue Service

Special Services Section

1 Independent Drive Suite 500

Stop 6000

Jacksonville, FL 32202

Refer the practitioner to the IRS website for Tax-Professionals/Bulk-Requests-

from-Practitioners-for-Disaster-Relief, for additional information on completing

the spreadsheet.

For additional disaster related information refer to:

IRM 25.16.1.1, Overview, for disaster and emergency relief information on

administrative guidance and cross-functional operating procedures

IRM 20.1.2.1.2.2, Federal Disaster Area - IRC 7508A and IRM 20.2.7.11, IRC

7508A, Presidentially Declared Disaster or Terroristic or Military Actions

IRM 21.5.3.4, General Claims Procedures, for expedited processing of disaster

claims

A new -S freeze has been added to IMF and BMF Master File processing for

Presidentially declared disaster areas. Refer to IRM 21.5.6.4.37, -S Freeze, for

additional information.

47Bulk Requests from Practitioners for

Disaster Relief

Where the IRS has granted a postponement of time to file

returns and make payments in response to a federally

declared disaster, practitioners located in the covered

disaster area who maintain records necessary to meet a

filing or payment deadline for taxpayers located outside the

disaster area may elect to contact the IRS to identify such

clients. To identify the clients, the practitioner may contact

the IRS at 1-866-562-5227 or, alternatively, the practitioner

may use the following procedures if the practitioner

maintains the necessary records of a large number of

clients (ten or more):

48Bulk Requests from Practitioners for

Disaster Relief

Prepare a CD with info in an Excel Spreadsheet:

•Column A list their client's TINs

Note: List SSNs and EINs separately or indicate the TIN is

an SSN or EIN by placing dashes in their correct places

•Column B list the first four letters of the client’s last name

or the first four letters of the business name, using upper

case lettering. Do not use any periods, commas,

separators or any additional wording such as "the", etc.

Note: Use the first four letters of the taxpayer’s last name

on Trusts and Estates

49Bulk Requests from Practitioners for

Disaster Relief

•Do not include TINs of clients who live within the disaster

declared area. Click here for a zip code listing identifying

areas within the disaster area.

•Mail the CD to:

Internal Revenue Service

Special Services Section

1 Independent Drive, Suite 500;

Stop 6000

Jacksonville, FL 32202

•Be sure to include the Stop "6000" to ensure your request

is processed timely.

50Bulk Requests from Practitioners for

Disaster Relief

Include a cover letter with the CD requesting relief from

penalties and/or interest. The letter should also contain the

practitioner’s name and address and a statement that

identifies which disaster affected their clients. A copy of the

IRS news release may be helpful, but not necessary.

http://www.irs.gov/Tax-Professionals/Bulk-Requests-from-

Practitioners-for-Disaster-Relief

51Disaster Hotline Calls

•Document all calls for future reference

•Take down name and badge number

•Length of time of call

•Keep track of who you are transferred to

52Terms to be Used

• The later of the extended due date or the end of the

postponement period

• Original due date

• Postponed original due date per 7508A

• Extended due date

• Postponed extended due date per 7508A

537508A Information on Filing Returns

(Example-April 15th(original due date) or

XXXXXX(postponement original due date)

547508A Information on Filing Returns

“The later of the extended due

date or the end of the

postponement period”

(Example-October 15th(extended due date) or January

31st(end of postponement period)

557508A Information on Payments

Example 6. (i) A is an unmarried, calendar year taxpayer whose

principal residence is located in County W in State Q. A intends to

file a Form 1040 for the 2008 taxable year.

The return is due on April 15, 2009. A timely files Form 4868,

"Application for Automatic Extension of Time to File U.S.

Individual Income Tax Return.“

Due to A's timely filing of Form 4868, the extended filing deadline

for A's 2008 tax return is October 15, 2009.

Because A timely requested an extension of time to file, A will not

be subject to the failure to file penalty under section 6651(a)(1), if

A files the 2008 Form 1040 on or before October 15, 2009.

However, A failed to pay the tax due on the return by April 15,

2009, and did not receive an extension of time to pay under

section 6161. Absent reasonable cause, A is subject to the failure

to pay penalty under section 6651(a)(2) and accrual of interest.

56Example 6-There was a balance due on the original

due date of April 15th.

Important Terms:

• Extension of time to file-Yes

• Extension of time to pay-No(tax was due on 4/15)

• Interest accruing-Yes(balance due on 4/15-due date

for payment and filing)

57Extensions

http://www.irs.gov/businesses/small/article/0,,id=210

510,00.html

(06/09) Q: A taxpayer whose individual income tax return (Form

1040) is due to be filed on or before April 15, 2009, timely files an

extension of time to file the return under section 6081 thereby

extending the due date to October 15, 2009. If the county in which

the taxpayer resides is declared a federally declared disaster area

and, pursuant to section 7508A of the Internal Revenue Code, the

IRS postpones filing and payment obligations for the period

September 1, through November 2, 2009, when is the taxpayer’s

Form 1040 now due?

A: The due date for filing the individual income tax return

is the later of the end of the postponement period or the extended

due date. Here, the postponement period ends on November 2,

2009, which is later than the extended due date (October 15,

2009). Therefore, the taxpayer’s individual income tax return is

due November 2, 2009.

58Extensions-Continued

http://www.irs.gov/businesses/small/article/0,,id=210510,00.html

(06/09) Q: What is the effect of filing an extension of time to file under

section 6081, if, prior to the March 15, 2009, due date for filing a U.S.

Return of Partnership Income (Form 1065), an event in the state and

county in which the partnership was formed, results in the area being

declared a federally declared disaster area and, pursuant to section

7508A of the Internal Revenue Code, the IRS postpones filing and

payment obligations for the period March 1, 2009, through April 30, 2009?

A. The due date for filing the partnership return is the later of the

extended due date or the end of the postponement period. If the

partnership, which is an affected taxpayer with respect to the federally

declared disaster, filed an extension of time to file prior to the end of the

postponement period (April 30, 2009), the extension would relate back to

the original due date, March 15, 2009. The extension would run from

March 15, 2009, to September 15, 2009. Because the extended due date

(September 15, 2009) is later than the end of the postponement period

(April 30, 2009), the partnership’s Form 1065 is timely if filed on or before

September 15, 2009.(06/09)

59Extensions-Continued

http://www.irs.gov/businesses/small/article/0,,id=210510,00.html

(06/09) Q: A corporate taxpayer whose U.S. Corporation Income Tax Return (Form 1120) is due

to be filed on or before March 15, 2009, files an extension of time to file under section 6081

prior to the due date for filing the return thereby extending the due date to September 15, 2009.

If, as a result of a disaster, the county in which the corporate taxpayer’s principal place of

business is located is declared a federally declared disaster, and pursuant to section 7508A of

the Internal Revenue Code, the IRS postpones filing and payment obligations

for the period July 1, 2009, through August 30, 2009, when is the corporate

taxpayer’s Form 1120 now due?

A: The postponement period under section 7508A runs concurrently with any extensions of

time to file and pay under other sections of the Internal Revenue Code. The return is due the

later of the extended due date or the end of the postponement period. If the extended due date

occurs prior to the end of the postponement period, the return is due to be filed at the end of

the postponement period. If however, the postponement period ends prior to the extended due

date, the return is due to be filed on the extended due date. Here, the extended due

date (September 15, 2009) is later than the end of the postponement

period (August 30, 2009), therefore, the corporate taxpayer’s Form 1120

is due September 15, 2009. Unless the corporate taxpayer also filed an

extension of time to pay pursuant to section 6161, the corporate

taxpayer’s payment would be due on August 30, 2009, the last day of the

postponement period.

60Payment of Tax

7508A Regs-Example 2

Example 2. The facts are the same as in Example 1, except that because of the

severity of the hurricane, the IRS determines that postponement of government

acts is necessary. During 2009, Corporation X's 2005 Form 1120 is being examined

by the IRS. Pursuant to a timely filed request for extension of time to file,

Corporation X timely filed its 2005 Form 1120 on September 15, 2006. Without

application of this section, the statute of limitation on assessment for the 2005

income tax year will expire on September 15, 2009. However, pursuant to

paragraph (c) of this section, assessment of tax is one of the government acts for

which up to one year may be disregarded. Because September 15, 2009, falls

within the period in which government acts are postponed, the statute of limitation

on assessment for Corporation X's 2005 income tax will expire on November 30,

2009. Because Corporation X did not timely file an extension of time to pay,

payment of its 2005 income tax was due on March 15, 2006. As such, Corporation

X will be subject to the failure to pay penalty and related interest beginning on

March 15, 2006. The due date for payment of Corporation X's 2005 income tax

preceded the postponement period. Therefore, Corporation X is not entitled to the

suspension of interest or penalties during the disaster period with respect to its

2005 income tax liability.

61Fiscal Year Extensions

Returns due the 15th day of the third month following the year end(1065 and 1120S)

Year End Extension Due Date Extension Granted to Return/Extension would be due

1/31/2018 4/15/2018 10/15/2018 2/28/2019

2/28/2018 5/15/2018 11/15/2018 2/28/2019

3/31/2018 6/15/2018 12/15/2018 2/28/2019

4/31/2018 7/15/2018 1/15/2019 Extension and return would be

due 2/28/2019

5/31/2018 8/15/2018 2/15/2019 Return due on 2/28/2019

6/30/2018 9/15/2018 3/15/2019 Return due on 3/15/2019

7/31/2018 10/15/2018 4/15/2019 Extension would be due

2/28/2019

8/31/2018 11/15/2018 5/15/2019 Extension would be due

2/28/2019

9/30/2018 12/15/2018 6/15/2019 Extension would be due

2/28/2019

10/31/2018 1/15/2019 7/15/2019 Extension would be due

2/28/2019

11/30/2018 2/15/2019 8/15/2019 Extension would be due

2/28/2019

62Fiscal Year Extensions

Returns due the 15th day of the fourth month following the year end(1120 and 1041)

Year End Extension Due Date Extension Granted to Return/Extension would be due

1/31/2018 5/15/2018 11/15/2018 2/28/2019

2/28/2018 6/15/2018 12/15/2018 2/28/2019

3/31/2018 7/15/2018 1/15/2019 2/28/2019

4/31/2018 8/15/2018 2/15/2019 Return due 2/28/2019

5/31/2018 9/15/2018 3/15/2019 Extension would be due

1/31/2019

6/30/2018 10/15/2018 4/15/2019 Extension would be due

2/28/2019

7/31/2018 11/15/2018 5/15/2019 Extension would be duse

2/28/2019

8/31/2018 12/15/2018 6/15/2019 Extension would be due

2/28/2019

9/30/2018 1/15/2019 7/15/2019 Extension would be due

2/28/2019

10/31/2018 2/15/2019 8/15/2019 Extension would be due

2/28/2019

63Returns due the 15th day of the fourth month following the year end(1041)

(Extension is for 5 ½ months)

Year End Extension Due Date Extension Granted to Return/Extension would be due

1/31/2018 5/15/2018 10/31/2018 2/28/2019

2/28/2018 6/15/2018 11/30/2018 2/28/2019

3/31/2018 7/15/2018 12/31/2018 2/28/2019

4/31/2018 8/15/2018 1/31/2019 Return due 2/28/2019

5/31/2018 9/15/2018 2/28/2019 No Effect

6/30/2018 10/15/2018 3/31/2019 Extension would be due

2/28/2019

7/31/2018 11/15/2018 4/30/2019 Extension would be duse

2/28/2019

8/31/2018 12/15/2018 5/31/2019 Extension would be due

2/28/2019

9/30/2018 1/15/2019 6/30/2019 Extension would be due

2/28/2019

10/31/2018 2/15/2019 7/31/2019 Extension would be due

2/28/2019

64Fiscal Year Extensions

Returns due the 15th day of the fifth month following the year end(990)

Year End Extension Due Date Extension Granted to Return/Extension would be due

1/31/2018 6/15/2018 12/15/2018 2/28/2019

2/28/2018 7/15/2018 1/15/2019 2/28/2019

3/31/2018 8/15/2018 2/15/2019 Return due 2/28/2019

4/31/2018 9/15/2018 3/15/2019 No Effect

5/31/2018 10/15/2018 4/15/2019 Extension would be due 2/28/2019

6/30/2018 11/15/2018 5/15/2019 Extension would be due 2/28/2019

7/31/2018 12/15/2018 6/15/2018 Extension would be duse

2/28/2019

8/31/2018 1/15/2019 7/15/2019 Extension would be due 2/28/2019

9/30/2018 2/15/2019 8/15/2019 Extension would be due 2/28/2019

65Members Comment

My tax manager called the IRS number on the Isaac

notice. Very friendly agent, but in the course of 87

minutes, she was transferred to another person, who

transferred her to a third person, who transferred her to a

fourth person, who turned out to be the first person she

talked to! The person took our information, but, because

we had no power of attorney, could not confirm that they

took action on the account. However, our past experience

has been good in this regard.

I hear that someone from E&Y called the disaster hotline

and the answering agent asked “What is Hurricane Isaac?”

66IRS Notices

List in correspondence:

News release(be specific)(For Nebraska Spring

Flooding-NE-2019-02)

FEMA Declaration Number(FEMA-DR-4420)

Affected taxpayer

Affected area

Covered by 7508A

Relief from penalty and interest

OR

Contact Disaster Hot Line of Practitioner Hot Line

67IRS Notices

•Internal Revenue Manual •20.1.1.3.2 (12-11-2009)

•http://www.irs.gov/irm/part2 Reasonable Cause

0/irm_20-001-001r.html •20.1.1.3.2.2.2 (12-11-2009)

Fire, Casualty, Natural

Disaster, or Other

Disturbance

6869

Terms for Returns Impacted by Flooding

• “Original” due date

• “Postponed” original due date

• “Original extended” due date

• “Postponed extended” due date

• Extension of time to file (6651(a)(1))

• Due date for payment of tax (6161)

• Interest accrual date (6651(a)(2))

70Sample Practice Chart for 7508A Delays

Louisiana 2016 Flooding

(2-7508A Delays)

Original Postponed Original Extended Original Postponed

Due Due Date Due Date Extended Due Date

Date

August 4/15 4/15 10/17 1/17

Flooding

Spring 4/15 7/15 10/17 1/17

Flooding

St. Tammany 4/15 7/15 10/17 1/17

Tangipahoa

Livingston

71Sample Practice Chart for 7508A Delays

Hurricane Michael

Original Due Date Extended Original Due Date Postponed Extended

Due Date

4/15/2018 10/15/2018 2/28/2019

72Qualified Disaster Payments

Section 139(a) provides gross income does not include amounts

received by an individual for a qualified disaster payment.

Section 139(b) defines “qualified disaster payments” as amounts

paid for the benefit of an individual to:

1. Reimburse or pay reasonable and necessary personal, family,

living, or funeral expenses incurred as a result of a disaster

2. Reimburse or pay reasonable and necessary expenses to

repair or rehabilitate a personal residence or repair or

replacement of contents to the extent that the need for such is

due to a disaster

3. Payments by a Federal, State, or local government in

connection with a qualified disaster in order to promote the

general welfare.

73Qualified Disaster Payments-Continued

Section 139 (c) defines the term “qualified disaster” as:

1. A disaster resulting from terrorist or military action

2. A Federally declared disaster

3. A disaster resulting from any event the Secretary determines

to be of a catastrophic nature

4. A disaster determined by applicable Federal, State, or local

authority that warrants assistance from Federal, State, or local

authority governmental agencies.

74Qualified Disaster Payments-Continued

Revenue Ruling 2003-12 (https://www.irs.gov/pub/irs-drop/rr-03-

12.pdf) offers guidance indicating individuals who are disaster

victims will generally not to have to pay income tax on assistance

payments they receive. The revenue ruling provides taxpayers in

a Federally declared disaster area who receive grants from state

programs, charitable organizations or employers to cover

medical, transportation, or temporary housing expenses do not

include these grants in their income.

Prior to the issuance of this 2003 revenue ruling, there was only a

1953 revenue ruling on this subject (Rev.Rul. 131, 1953-2 C.B.

112). This revenue ruling concluded that payments made by an

employer to employees who were victims of a disaster do not

come “within the concept of gross income.”

75Qualified Disaster Payments-Continued

It is important to note the following terms in interpreting the relief

available to disaster victims:

• Qualified disaster payments

• Reasonable and necessary personal, family, living, or funeral

expenses

• Reasonable and necessary expenses for repairing a personal

residence or contents

• Other disaster payments for a Federal, State, or local

authority (FEMA payments).

This is a means of assisting disaster victims, not a blank check

for unlimited spending without tax consequences.

This 2003 revenue ruling and the applicable sections of Code

Section 139 provide a means for employers to be able to assist

their employees in restoring normality in their lives and also

provide assurance to disaster victims there will not be income tax

consequences on the qualified disaster payments they receive.

76E Mail Future Questions to:

ghschreiber@bellsouth.net

77Questions

78Thank You

Presented by:

Gerard H. Schreiber, Jr.

ghschreiber@bellsouth.net

504-832-1819

79You can also read