Globalization of China A-shares - Are You Ready? November 2020 - Asia-Pacific Research ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Globalization of China A-shares

Are You Ready?

November 2020

(11th Edition)

1

About the Author

Qi Wang, CFA qi.wang@megatrust.com.hk

Qi is the co-founder and CEO of MegaTrust Investment (HK), part of a research-

driven, boutique manager specializing in China A-shares. MegaTrust Investments was

founded in Shanghai in 2007 and has around US$700 million of AUM as of November

2020, with over 12 years of historical Alpha generation.

Prior to joining MegaTrust, Qi was the Head of China Index Research at MSCI, a

global index and analytics solutions provider. He advised the world’s leading asset

owners on global investing, asset allocation, portfolio construction, and risk analysis.

He also led the research and consultation on China A-share index inclusion.

Qi has over 23 years of research and investment experience, starting as a Financial Analyst in the Global

Investment Research Department of Goldman Sachs in New York. He later joined UBS and co-founded the

firm’s Global Tech Strategy Group. He was then hired by global hedge fund manager Elliott Advisors to run its

fundamental long-short strategy in Asia. Following Elliott, Qi became the CIO for China Everbright Limited, a

Chinese financial conglomerate in Hong Kong. Qi graduated from Dartmouth College with a degree in

electrical engineering in 1997, and Colby College with a double major in Mathematics and Computer Science

in 1996.

2

What is China A-share?

“Chinese stocks” are traded everywhere from China to Hong Kong to the U.S.

A-shares refer to stocks listed in China on the Shanghai and the Shenzhen Stock Exchanges

Share Class Description Place of Listing Currency Sample Securities Foreign Access

A-shares Chinese stocks listed in China, Shanghai, RMB Kweichow Moutai (600519.SH) Limited

denominated in RMB Shenzhen Pingan Insurance (601318.SH)

B-shares Chinese stocks listed in China, Shanghai, USD Lujiazui B (900932.SH) Unlimited

denominated in USD or HKD Shenzhen HKD Changyu B (200869.SZ)

H-shares Chinese stocks listed in Hong Hong Kong HKD Pingan Insurance (2318.HK) Unlimited

Kong under the CSRC approval China Telecom (0728.HK)

Red Chips Chinese companies Hong Kong HKD China Mobile (0941.HK) Unlimited

incorporated abroad Tencent (0700.HK)

Overseas Chinese stocks listed abroad via New York, USD Baidu (BIDU) Unlimited

Listed ADR or ADS London etc. Alibaba (BABA)

Excluding the 128 dual-listed A/H shares, there are still nearly 4000 Chinese companies that can only

be accessed through A-shares

3Second Largest Market Globally

Total Market Cap and Annual Turnover

Total Market Cap Annualized Trading Annualized

Country / Region Exchanges (USD billion) Volume (USD bilion) Turnover

U.S. NYSE + NASDAQ 35,682 46,863 131%

China A-shares Shanghai + Shenzhen Stock Exchange 9,182 25,189 274%

Japan Japan Exchange Group 5,664 6,226 110%

Europe Euronext 4,286 2,743 64%

Hong Kong Hong Kong Stock Exchange 4,890 2,737 56%

India Bombay Stock Exchange 1,827 1,565 86%

Free Float Market Caps

A-shares B-Shares H-Shares Red Chips

USD 4,170 billion USD 17 billion USD 529 billion USD 195 billion

Source: World Federation of Exchanges, Wind and MegaTrust.

Note: As of June 30, 2020. USD/RMB exchange rate = 6.607. The free float market cap of A-share companies is estimated at 40% of the total market cap. The true market turnover of

A-shares would be much higher if based on the free float market cap (as opposed to the total market cap).

4Rapid Expansion Through IPOs

328 A-share IPOs so far in 2020, raising a total of RMB 412 billion (USD 62 billion)

Majority of the newly listed companies are in advanced industries like Healthcare and Tech

Number of A-share IPOs by Sector

140

124

120

100 89 90

86 85

80

64 64

60 51

46

41 40

40 33 32

27 23

1713 19 20

20 1114 1113 8 11

5 4 0 1 3 5 6 6 3 2 5

1 0 1 0

0

Consumer Consumer Energy Financials Healthcare Industrials Technology Materials Telecom Utilities

Disc. Staples

2017 2018 2019 2020 YTD

Source: Wind. As of November 10, 2020.

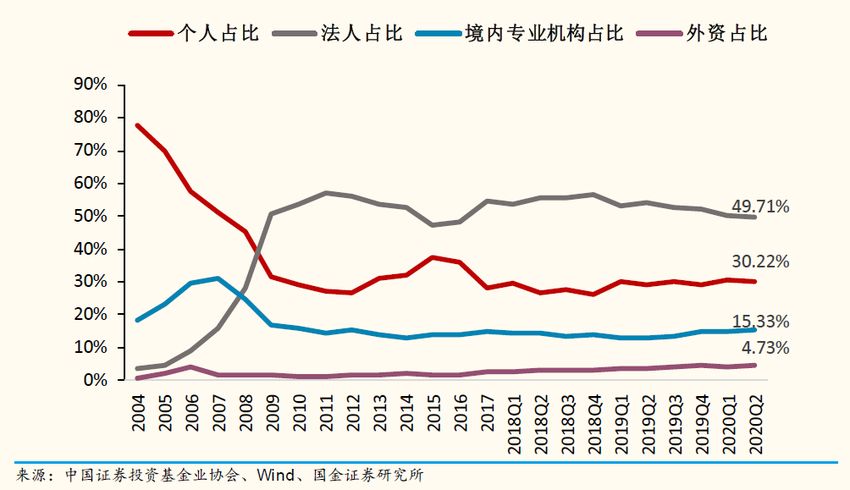

5Predominantly Retail Market

Over 130 million individual investors in China

“Retail investors” account for 30-40% of the stock ownership

yet they contribute to more than 80% of the trading volume

A-share Investor Composition

As % of Float Market Cap

Promoters / Insiders 50%

Retail Investors 30%

Domestic Institutions 15%

Foreign Institutions 5%

Source: AMAC and Sinolink, as of June 2020.

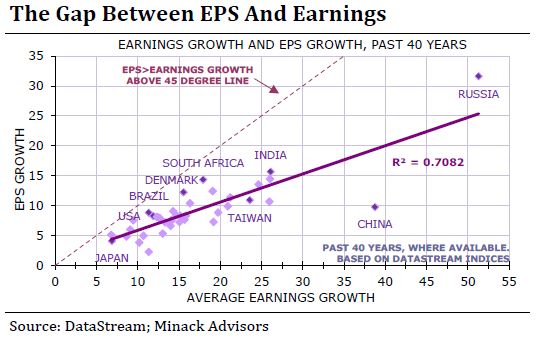

6Passive Investing: A Zero-Sum Game?

The long-term* index return of A-shares is near

zero, despite China’s high GDP growth historically

The high volatility and large drawdowns make the Some argued that the high earnings growth in

market extremely difficult to time China did not necessarily translate into high EPS

* “Long-term” refers to the last 10-15 years. Please refer to the Disclosures page growth, mainly due to share dilution

regarding the use of indices.

We call this the “growth trap”

7Low Foreign Ownership

Extremely low foreign ownership of China A-shares compared to other markets

Foreign Ownership of Domestic Stock Markets

50%

44%

40% 36%

30%

24%

20%

20% 16%

10%

3.6%

0%

Taiwan Korea Japan India U.S. China A-share

Source: Various stock exchanges and MegaTrust estimates. As of September 30, 2020. Data available upon request.

8Market Opening and Reform

Perhaps the only “good news” out of the Trade War is more financial opening by China

Date Event

January 2019 Proposed a new round of QFII/RQFII reforms by merging the two systems and broadening the investment scope

March 2019 Passed the new Foreign Investment Law which protects the intellectual property rights of foreign investments,

and prohibits forced technology transfers

June 2019 Launched the Shanghai-London Stock Connect with the listing of Huatai Securities on the London Stock

Exchange

August 2019 Introduced Loan Prime Rate (LPR) for the banking sector in order to develop a more efficient, market-based

system for pricing loans. Foreign banks were invited to participate the rate initiation group for the first time.

July 2019 Announced “11 Measures” to further open up the country’s financial sector, lifting / removing foreign

ownership limits for various financial services

September 2019 Lifted the investment quota limit for QFII and RQFII, which had been existent for 16 years

October 2019 Announced plans to scrap the foreign ownership limits on banks, insurance, securities brokerage and asset

management firms by 2020

October 2019 Simplified the regulations of foreign banks and insurance companies to set up and conduct business in China

May 2020 Introduced another round of QFII/RQFII reforms by removing the quota limits, among other major changes

September 2020 Announced more QFII rule changes, including the expansion of the investment scope to more financial products

Source: Chinese government websites.

9Global Index Inclusion

Even without the A-shares, China is already the single largest country in Emerging Markets

MSCI and FTSE have both started the “initial inclusion” of A-shares in their EM indices

MSCI Emerging Markets Index FTSE Russell Emerging Index

Others 11% Others 14%

Mexico 2%

Russia 2%

Malaysia 2% China

S. Africa 4% Thailand 2% Offshore

China Mexico 2%

Brazil 4% 38%

All China Offshore Russia 3% All China

38% South Africa

43% 3%

44%

India 8%

Brazil 5%

Taiwan 13% India 10%

China A

China A 5%

Korea 12% Taiwan 14% 6.8%

Note: As of November 10, 2020.

10Full Inclusion Simulation

If fully included, A-shares would account for over 20% of emerging markets

We expect $640 billion of foreign capital inflows to A-shares as a result of the full inclusion

Assuming full

MSCI Emerging Markets Index FTSE Russell Emerging Index

inclusions of

A-shares

Others 9%

Others 11%

Mexico 2% China

Russia 2% China Malaysia 2%

Offshore Thailand 2% Offshore

Brazil 3% Mexico 2%

32% 30%

S. Africa 4% Russia 2%

Brazil 2%

South Africa

India 7% 4%

All China All China

53% India 8%

56%

Taiwan 11%

Taiwan 11%

Korea 10% China A China A

21% 27%

Note: Based on the pro-forma full inclusion of China A-hares as of November 10, 2020.

11Fast and Furious

From initial to full inclusion

Market Initial Inclusion Year Full Inclusion Year Time

Korea 1992 1998 6 years

Taiwan 1996 2005 9 years

China A-share 2018 TBD 3-5 years?

Technical reasons why A-share’s final weight will be higher than expected

• A large number of IPOs each year

• Increase in free float market cap

• Possible relaxation of the foreign ownership limit (currently 30%)

• Potential outperformance of A-shares (vs. other emerging markets)

• Currency appreciation (vs. other emerging markets)

Should China still be considered an “Emerging Market”?

Will China become a standalone classification in the future?

• Emerging Market ex. China

• Asia ex. Japan ex. China

12Inflows Driven by Active Allocation

Global index inclusion is essential to but not necessary for the Globalization of A-shares

Though MSCI/FTSE has postponed the further inclusion of A-shares, we still expect significant inflows

in the near-term, as active managers move from under-weight to equal-weight China

Non-Indexing Active Allocation of A-shares in Emerging Markets (US billions)

Percent in NB* 0% 3% 5% 7% 10%

0% 0 0 47 98 175

20% 0 16 67 118 194

40% 0 36 87 138 214

60% 0 55 106 157 234

80% 0 75 126 177 253

Source: Based on the simulation by MegaTrust as of November 10, 2020. The assumptions and additional notes are as follows:

(1) Total assets tracking the MSCI, FTSE and other emerging market indices are estimated at USD 3 trillion, of which A-share accounts for 5-7%.

(2) The active money tracking the index is estimated at 85% of the total assets, with passive allocations accounting for the remaining 15%.

(3) The “Non-indexing Percent in NB” refers to the percent of inflows through Stock Connect Northbound that are unrelated to indices, e.g. retail money and hedge funds etc.

(4) Total inflows through Stock Connect North Bound since the initial inclusion is around RMB 650 billion.

(5) USD/RMB exchange = 6.607

13Are You Underinvesting in China?

China will account for 18% of the world GDP in 2021 by IMF estimate

Yet China accounts for just 6% of global equities according to MSCI

World GDP World Stock Market (ACWI)

Other, 38% Other, 19%

France, 3%

U.K., 3%

Germany,

France, 3% 3%

U.K., 3% Japan, 7%

Germany,

5% India, 1%

Japan, 6% U.S., 24%

China, 6%

India, 3%

U.S., 58%

China, 18%

Source: IMF estimates (GDP based on PPP) and MSCI. As of November 10, 2020.

14Impact on the Emerging Markets Universe

A-shares outnumber non-A-shares by 2 to 1 in the All China universe

There are more A-shares than all other BRICS stocks combined

A-share inclusion has increased the number of EM stocks by 50%

Standard Index EM without

Number of Stocks Large + Mid Caps A-shares Additions from A-share Inclusion

China A-shares 475 # of stocks # of stocks % change

China Offshore 239 Communication 84 18 21%

China Total 714 Consumer Discretionary 120 33 28%

Korea 107 Consumer Staples 104 39 38%

Taiwan 87

Energy 71 13 18%

India 86

Financials 206 67 33%

Brazil 56

Health Care 24 58 242%

South Africa 39

Russia 23 Industrials 87 74 85%

USA 618 Information Technology 29 85 293%

Japan 320 Materials 87 53 61%

Asia Pac ex.Japan 1,255 Real Estate 53 21 40%

Frontier Markets 90 Utilities 62 14 23%

Emerging Markets 1,392 Total 927 475 51%

Developed Markets 1,603 Source: MSCI. As of October 2020.

15Declining Market Volatility

South Korea (60-Day Vol) Taiwan (60-Day Vol)

China A-shares (60-Day Vol)

Global index inclusion rising foreign

ownership and institutional holdings

lower market volatility

Source: Wind. Based on the Kospi Index (South Korea), the TWSE Index (Taiwan),

and the CSI 300 Index (China A-shares). Please refer to the Disclosure page

regarding the use of indices.

16Correlations of A-shares vs. Global Markets

Monthly Return Correlations (Dec 2014 - Oct 2020)

ACWI EAFE WORLD EM FM China A

ACWI 1.00

EAFE 0.97 1.00

WORLD 0.89 0.87 1.00

Emerging Markets (EM) 0.65 0.66 0.62 1.00

Frontier Markets (FM) 1.00 0.96 0.85 0.64 1.00

China A 0.45 0.42 0.52 0.28 0.42 1.00

Weekly Return Correlations of A-shares and Nasdaq (Dec 2009 - Oct 2020)

Shanghai Shenzhen

Composite Composite SSE 50 CSI 1000 ChiNext

Correlation 0.34 0.32 0.34 0.26 0.24

Downside Correlation 0.36 0.32 0.33 0.29 0.29

Source: Wind and MSCI. Please refer to the Disclosures page regarding the use of indices.

17Long-term Sector Rotation

In Korea and Taiwan, Consumer Discretionary and Financials saw the greatest reversals in relative

performance, before and after the global index inclusion

South Korea Taiwan

Annualized Excess 3 Years Before 3 Years After Annualized Excess 3 Years Before 3 Years After

Return Over Market Inclusion Inclusion Return Over Market Inclusion Inclusion

Consumer Discretionary 0.1% 27.1% Consumer Discretionary -7.4% 15.8%

Consumer Staples 8.7% -1.8% Consumer Staples -15.3% -10.0%

Energy -2.5% NA Energy NA NA

Financials -15.1% 20.3% Financials -14.2% 5.3%

Health Care 9.7% -53.1% Health Care NA NA

Industrials -8.0% -44.5% Industrials -6.0% -7.3%

Information Technology -4.1% -0.3% Information Technology 14.6% -3.6%

Materials 1.3% -10.5% Materials 4.2% 12.9%

Telco Service 26.7% 50.7% Telco Service NA NA

Utilities 11.0% -18.7% Utilities NA NA

Source: MSCI. Based on the MSCI Korea Index, the MSCI Taiwan Index and the respective sector indices. For South Korea, the analysis is for the three years prior to 100% index inclusion on

September 1, 1998, and the three years thereafter. For Taiwan, the analysis is for the three years prior to 80% index inclusion on December 1, 2000, and the three years thereafter. The

excess return equals the annualized sector return minus the market return. Please refer to the Disclosures page regarding the use of indices.

180.4

0.6

0.8

1

1.2

1.4

1.6

1.8

12/1/1996

7/1/1997

2/1/1998

9/1/1998

4/1/1999

11/1/1999

6/1/2000

1/1/2001

8/1/2001

3/1/2002

10/1/2002

5/1/2003

12/1/2003

7/1/2004

2/1/2005

inclusions in global indices

9/1/2005

4/1/2006

refer to the Disclosures page regarding the use of indices.

11/1/2006

Value / Growth Relative: Korea

6/1/2007

1/1/2008

Style Shift Already Underway

similar structural change since 2014

8/1/2008

3/1/2009

10/1/2009

5/1/2010

Both Korea and Taiwan had a notable style

The China A-share market is experiencing a

switch from growth to value following their

12/1/2010

Source: MSCI. Based on the MSCI Korea Index, the MSCI Taiwan Index, the MSCI

China A Onshore Index, and the respective Value and Growth sub-indices. Please

7/1/2011

0.0

0.5

1.0

2.0

2.5

3.0

1.5

0.6

0.8

1

1.4

1.6

1.2

12/29/2000

12/1/1996

12/29/2001 7/1/1997

12/29/2002 2/1/1998

9/1/1998

12/29/2003

4/1/1999

12/29/2004 11/1/1999

12/29/2005 6/1/2000

1/1/2001

12/29/2006

8/1/2001

12/29/2007 3/1/2002

12/29/2008 10/1/2002

5/1/2003

12/29/2009

12/1/2003

12/29/2010 7/1/2004

12/29/2011 2/1/2005

9/1/2005

12/29/2012

4/1/2006

12/29/2013 11/1/2006

6/1/2007

12/29/2014

Value / Growth Relative: A-share

1/1/2008

12/29/2015 8/1/2008

12/29/2016 3/1/2009

10/1/2009

12/29/2017

5/1/2010

12/29/2018 12/1/2010

12/29/2019 7/1/2011

Value / Growth Relative: Taiwan

19A Paradigm Shift in China A-shares

300

China A-share Factor Index Performance

260

220

Quality has the best performing factor in the last five years

180

140

100

60

20

Market Large Cap Mid Cap Small Cap Value Growth High Dividend Yield Min Vol Momentum Quality

Return Market Large Cap Mid Cap Small Cap Value Growth HDY Min Vol Momentum Quality

Since Dec 2015 14.1% 38.4% -27.5% -38.7% 15.9% 9.0% 62.1% 17.6% 45.5% 144.5%

Source: MSCI. Based on the MSCI China A Onshore Index (“Market”) and the respective sub-indices (all other). June 2015 to October 2020.

20Small is Ugly?

We think small caps overall will continue to underperform the market, as part of a long-term,

secular shift towards more fundamentals and value-based investing

Large Caps (CSI 300) vs. Small Caps (CSI 1000)

CSI 300

CSI 1000

Source: Wind. As of November 10, 2019. Please refer to the Disclosures page regarding the use of indices.

21Quality of Growth Issue

We believe questionable M&As funded by dilutive share placements are commonly used by small-

mid cap companies to produce superficially high growth… but low quality earnings

(RMB millions except for EPS) 2013 2014 2015 2016 2017 2018 2019 2020E CAGR

Sales 3,584 5,979 8,347 12,319 15,231 23,104 28,106 36,462

Sales Growth YoY 67% 40% 48% 24% 52% 22% 30% 39%

Net Profit 439 712 68 640 222 389 710 689

Profit Growth YoY 62% -90% 845% -65% 75% 83% -3% 7%

Diluted EPS 1.02 0.74 0.04 0.32 0.10 0.18 0.28 0.35

EPS Growth YoY -27% -95% 700% -69% 80% 56% 25% -14%

Source: Wind. Based on the reported financials and stock price of an A-share small cap company.

22Our Investment Philosophy

Invest in high quality companies at reasonable valuation with high conviction

Quality is essentially about Sustainability

Sound

Business

Model

Steady

Reasonable

Earnings

Valuation

Growth

Quality is about

Sustainability

Good Strong Cash

Corporate Flow & Balance

Governance Sheet

Sustainable

ROE

23Summary of Our Views

The China A-share market is big and expanding

The market is rapidly opening up to foreign investors

We expect global index inclusion to trigger over US$640 billion of capital inflows

Globalization of China A-shares should have a major impact on global investing

…and also cause a paradigm shift in the local Chinese market

Passive investing in A-shares can be a trap, a “growth trap”

We believe in active management through fundamental research & stock picking

Our unique Quality framework for China A-shares is key to Alpha generation

Please contact us if you’d like to learn more about our award-winning A-share strategy

24Disclosures

MTI Management (HK) Limited (“the Company”), trading as MegaTrust Investment (HK), is a company incorporated in Hong Kong with limited liability. The Company

is licensed by the Hong Kong Securities and Future Commission (SFC) to conduct Type 4 and Type 9 regulated activities, namely “Advising on Securities” and “Asset

Management”. The Company’s licenses are subject to the following conditions: (1) The Company shall not hold client assets. The term “hold” and “client assets” are

as defined under the Securities and Futures Ordinance (SFO). (2) The Company should only provide services to professional investors. The term “professional

investor” is as defined by the SFO and its subsidiary legislations. This document (“the Document”) is prepared by the Company for information purpose only. It does

not form the basis of, nor should it be relied upon in connection with any subsequent contract, agreement, transaction or trade. None of the information here

constitutes a recommendation, offer, or a solicitation of an offer to buy/sell any securities, portfolios of securities, financial products, investment schemes or trading

strategies. This Document should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors

and/or clients when making investment decisions. To the extent that any of the information contained in this Document may be deemed investment advice, such

advice is impersonal and not tailored to the investment needs of any specific entity, person, or group of persons. From time to time, the Company may act on the

information in this Document by holding positions or other interests in securities mentioned in this Document, and may trade such securities for its own account or

an account/scheme managed on behalf of its clients, in manners that may or may not be consistent with the views expressed in this Document. All market indices

mentioned in this Document, including but not limited to the MSCI China A Index ("the Index") are unmanaged. The Index is being utilized for illustrative purposes

only and an investor cannot invest directly the Index. The timing of transactions in a portfolio, advisory fees, transaction fees, and other management activities can

create significant differences between the performance of the Index and an investment seeking similar or superior performance results relative to the Index.

Investors are cautioned that no Index is directly comparable to the performance of a specific fund, since each Index has its own unique returns and volatility, and the

Index should not be relied upon as an accurate comparison. This Document is provided to you incidentally, and any opinions expressed here are subject to change

without notice. The information contained in this Document has been compiled with considerable care to ensure its accuracy and validity. However, no presentation

or warranty, express or implied, is made to its accuracy or completeness. The Company accepts no liability for any direct or consequential financial losses or

damages, including for any loss of capital arising from your use of the Document. Investing in Chinese securities involves a high degree of risk. The possibility of

partial or total loss of capital exists. Prospective investors should carefully consider the relevant risk factors of their investments, including but not limited to the risks

explained in this Document. The risks from political, economic and market factors are particularly relevant in China. Such risks include various forms of punitive or

confiscatory government interventions, inadequate financial regulations, high brokerage fees and transaction costs, less reliable settlement and custody practices,

loss of registration of securities, low market liquidity, high market volatility, and poor reporting standards. Prospective investors are advised to ensure that they

obtain appropriate independent professional advice before making any investment decisions. This Document is non-public, the recipient of this Document agrees to

treat all information contained herein with reasonable care and confidentiality.

25Contact Info

Qi Wang 王崎

MegaTrust Investment (HK) 世誠投資(香港)

Suite 719, Grand Millennium Plaza 香港中環皇后大道中181號

181 Queen’s Road Central 新紀元廣場低座7樓719室

Central, Hong Kong 傳真: (852) 3511 6111

Tel: (852) 3511 6023 電話: (852) 3511 6025

Email: qi.wang@megatrust.com.hk 電郵:qi.wang@megatrust.com.hk

Jun Xiong 熊俊

MegaTrust Investments 上海世诚投资管理有限公司

Suite 715, Citigroup Tower 中国上海陆家嘴金融贸易区

Lujiazui Finance and Trade Zone 花园石桥路33号花旗集团大厦715室

Shanghai, China 200120 传真:(86) 21 6887 8560

Tel: (86) 21 6887 8556 电话:(86) 21 6887 8556

Email: wei.zhang@shmti.com 电邮:jun.xiong@shmti.com

26You can also read