IFRS 17 as BAU: A Question of Timing - Neil Bruce 25 September 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

IFRS 17 as BAU: A Question of Timing Neil Bruce 25 September 2019

Agenda

Iteration of assumptions:

• Introduction to IFRS 17

• BAU under IFRS 17

• Prioritising your effort

• Conclusion

06 September 2019 2

Introduction to IFRS 17 Application and Progress 04 September 2019

IFRS 17 – the basics

• Common (almost) global standard for reporting to investors, not regulators

What Who

§ Global* accounting standard covering § Any entity which issues insurance contracts and

insurance contracts with a consistent reports under IFRS

measurement basis § May be mandated by (inter)national legislation

§ General purpose financial reporting to (e.g. listed entities in EU or insurance entities in

meet needs of investors and creditors some jurisdictions)

§ Not designed to meet requirements of § Entities may opt to publish under IFRS alongside

supervisors/regulators national GAAP accounts

§ Subsidiaries of such entities will need to report

internally under IFRS (via reporting pack or similar

simplified mechanism)

§ Many large entities (particularly unlisted) will

continue to use local GAAP

§ US entities will report under US GAAP as now

4

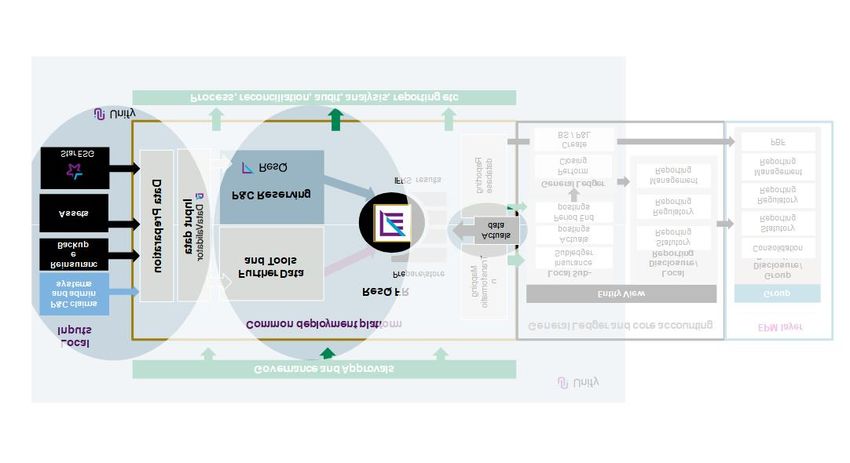

Potential IFRS 17 architecture

§ Usual focus on

Xxxxxx accounting end of the

process

§ Xxxxxx Governance and Approvals

Local § Xxxxxx § Many solutions require

Inputs ̵ Xxxxxx Common deployment platform General Ledger and core accounting EPM layer cashflows to enable

the calculation of the

Transformatio

P&C claims

Mapping

and adm in ResQ FR Entity View Group

systems Financials

n

Further Data Prepare/store Local Sub-Ledger Local Disclosure / Group

Data Preparation

Reporting Disclosure /

§

Reinsuranc Insurance

and Tools

e Subledger Reporting

Derivation of these

Input data

Backup Consolidation

Actuals Statutory

Actuals

data postings Reporting Statutory cashflows in non-trivial

Period End Reporting

Assets Regulatory

§

postings

Reporting

P&C Reserving

Regulatory

Actuarial assumptions

Reporting

database

Reporting

General Ledger

IFRS results

Perform

Management

Reporting Management will be critical in this

Closing Reporting

§

Star ESG

Create

BS / P&L

PBF Multiple other data

sources required

Process, reconciliation, audit, analysis, reporting etc including yield curves,

expenses etc.

5

IFRS 17 – Exposure Draft

• Consultation ends today, timetable indicates final version available mid 2020

One year delay

Presentation at portfolio

not group level

Challenge from Acquisition costs

multiple insurance

associations across

the globe (25 topics) Reinsurance

+1 from EU (mutuals)

CSM

Further issues will be addressed

after initial implementation

Most companies are using the delay to optimise their approach rather than slow down

implementation progress

6IFRS 17 – market progress

• Most that are directly affected are in the implementation stage, after completing a gap analysis

Dry runs:

Implementation:

Gap analysis:

§ No

§ Larger global companies

companies are at this

Monitoring § Smaller stage yet

progress: companies § Mostly driven by

Finance

§ Not directly § Companies

affected indirectly affected

anticipating

implementation

Companies are not consistent in their progress – depends on own situation

7BAU under IFRS 17 An actuary’s perspective

BAU – change in focus

• Focus will change when implementation is complete

Focus of current efforts will largely be Focus will move to more operational issues:

complete:

§ Hitting timetables

§ Feed into other processes (planning, investor

§ Accounting systems will be in place

metrics, M&A impacts, capital modelling)

§ Pipework tested and mappings in place

§ Interaction of Finance and Actuarial teams –

§ (Initial) accounting choices already defined controlling information flow and explaining

movements

Quarterly WD reporting timetable

Determine Extract Populate Extract Interpret Sign-off Post data to

assumptions q-end data tools results results results ledger

9BAU – pinch points

• Which areas are likely to cause particular problems

Main issues: = actuarial issue Particular issue:

§ Timeframes for production of Same as current GAAP

numbers and commentary

New sources and detail

§ Data capture

§ Investor comms Board responsibility

§ Planning/ business KPIs CFO responsibility, but need actuarial input

§ Managing effect of change

in assumptions Significant issue

§ Managing effect of change in standards Monitoring rather than pro-active approach

10BAU – pinch points

• Where will you be spending your time?

Main issues:

§ Timeframes for production of numbers Quarterly WD reporting timetable

and commentary

§ Data capture

Determine Extract q- Populate Extract Interpret Sign-off Post data to

§ Investor comms assumptions end data tools results results results ledger

§ Planning/ business KPIs

§ Managing effect of change in assumptions

§ Managing effect of change in standards

Governance and Approvals

Local

Inputs General Ledger and core EPM layer

Absolutely critical to spend time on P&C

claims

Com mon deployment platform

accounting

Mapping

Transfor

and Entity View Group

mation

admin ResQ FR

systems Further Data Prepare/store Local Sub- Local Group

getting the right assumptions into

Reinsur

Preparation

Insurance

and Tools Ledger Disclosure / Disclosure /

Input data

ance Subledger

Reporting Reporting

Consolid’n

Backup Actuals Statutory

Data

Actuals Reporting

data postings Statutory

Period End Regulator Reporting

the calculation, and providing

Assets

P&C postings y Regulator

Reporting y

Reporting

database

Reserving Managem Reporting

IFRS results General ent Managem

Perform

Ledger Reporting ent

Closing

credible and detailed commentary Star

ESG

Create

BS / P&L

Reporting

PBF

Process, reconciliation, audit, analysis, reporting etc

11BAU – level of granularity of setting assumptions

• Emphasis will be on ensuring consistent assumptions

§ Assumptions will be at a granular level

Group

§ Changes in consistency of assumptions

will show up in the reconciliations and hence

Financial Statements

Entity 1 Entity 2

§ Calculations of reserve adequacy on

IFRS 17 basis will need updating

IFRS 17 class 1 IFRS 17 class 2 IFRS 17 class 1

Group 1 Group 2

Exposure/ Actuals (claims,

Yield curves Past service expenses, Initial Current Future Risk

Coverage CSM premium and

(valuation, claims incurred, initial) claims and premium patterns recognition service service Adjustment

units expenses)

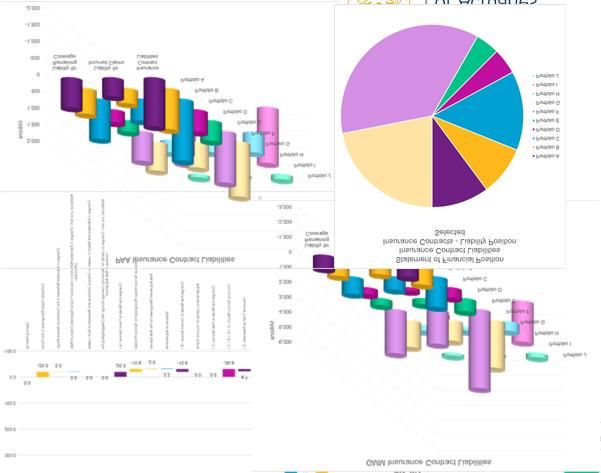

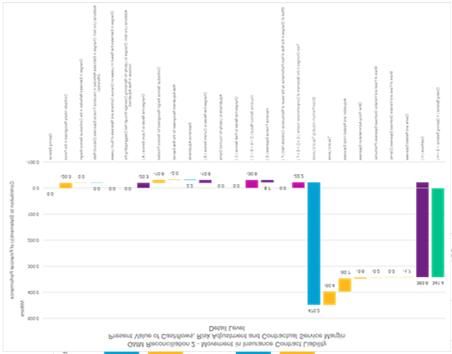

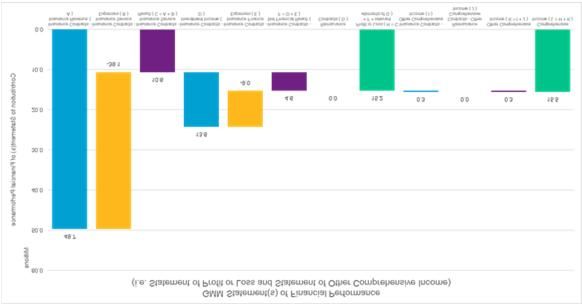

12BAU – interpretation of results

• Analysis of results will need to fit within the reporting timetable

§ Vast amount of detail – need to sift to explain all movements

§ Commentary needed for the financial statements

§ Approximations within the assumptions will result in

volatility in the reconciliations

§ Yield curve variation will be a major source of change

PAA rec

GMM recs

1-4

Group 1

IFRS 17 Portfolio

class 1 analysis

Entity 1 Group 2

IFRS 17 Reserve

Group class 2 adequacy

IFRS 17

Entity 2 class 1

13Prioritising your effort What’s going to be important?

Automate as much as possible

§ Data preparation and

population automatic

Xxxxxx

§ Xxxxxx § Automatic production of

Governance and Approvals assumptions based on

Local § Xxxxxx core reserving process

Inputs ̵ Xxxxxx Common deployment platform General Ledger and core accounting EPM layer

§ Population of IFRS 17

Transformatio

P&C claims

calculations

Mapping

and adm in ResQ FR Entity View Group

systems

n

Further Data Prepare/store Local Sub- Local Group

automatically

Data Preparation

Reinsuranc Ledger

Insurance Disclosure / Disclosure /

and Tools Reporting

e Subledger Reporting

Input data

§ Production of MI/

Backup Consolidation

Actuals Statutory

Actuals Reporting

data postings Statutory

Assets Period End

Regulatory

Reporting drillable results

postings

Reporting Regulatory

P&C Reserving

§ Allow quick review and

Reporting

database

Reporting

IFRS results General Ledger Management

Perform Reporting Management

Closing Reporting playback, with potential

Star ESG

Create PBF to adjust assumptions

BS / P&L

§ Build up story of the

Process, reconciliation, audit, analysis, reporting etc

quarter

15Areas of focus

• Some changes will be expected, others will not

Expected changes: Unexpected issue:

§ Change in level and shape of yield curves Split of impact if not produced as part of OCI

§ AvE on experience in the period e.g. inconsistent assumptions obvious

§ Unwind of CSM / LRC e.g. linear earning, not seasonal

§ New business adding to a cohort e.g. RI adjustments for gross new business

§ Unwind of discount Changes to initial discount rate over the year

§ Expense allocations and Risk Adjustment e.g. impact on expected future profit

§ Interpretation and reconciliations e.g. impact of appetite for reserve adequacy

16Focus area: AvE experience

As normal but

• Includes more detailed analyses due to moving between future/current/past

• Impact on future profits of changes in expectations of pricing strength

• Additional premiums (RP, AP) and allocation of the associated losses

• PAA revenue dependent on allocated expected (not actual) receipt of premium

AvE on

emerging

Future/ Expected

Premium

Current/ Past future

06 September 2019 17Focus area: Unwind of CSM/LRC

Compare

to

expected

Trend in

By Group/ remaining

cohort profit

PAA vs

GMM

Onerous/

Transfer

non-

to LIC

onerous

New

business

06 September 2019 18Focus area: New business

• Assign to a cohort

New • Reinsurance cohorts may have different timing of new

business business to gross

written • “Proportionate” reinsurance will need to include impact

of new gross business

Increase in • Split out from run-off of existing

CSM/LRC business

• Waterfall of effect of

Change in change in discount rate on

initial discount LRC as well as impact on

rate existing LRC

• Change in focus depending on

Interim seasonality

reporting • May have different seasonality for

RI and gross business

06 September 2019 19Focus area: Expenses and Risk Adjustment

These elements can impact not only past

but also future business profitability

CSM changes leading to changes in

expected profitability amount and timing

Changes in expectations of allocation of

RA will impact CSM/ unearned profit

06 September 2019 20Focus area: interpretation and iteration

Iteration of assumptions:

• Controls in setting, reviewing and signing off assumptions

• Reconciliations to core data and finance systems

• New/ different KPIs

• Reserve adequacy calculations and impact on message

• Bridging to other bases

06 September 2019 21Conclusion 18 September 2019

Conclusions

It’s not going to be easy:

• Efficient processes are critical

• Controls will need to be tighter than is usual at the moment

• Interpreting movements may require significant amounts of analysis

• Not all movements will be easy to explain, particularly if driven from

inconsistencies in assumptions

• Bridging to other bases may vastly increase workloads

06 September 2019 23Questions Comments The views expressed in this presentation are those of invited contributors and not necessarily those of the IFoA. The IFoA do not endorse any of the views stated, nor any claims or representations made in this [publication/presentation] and accept no responsibility or liability to any person for loss or damage suffered as a consequence of their placing reliance upon any view, claim or representation made in this presentation. The information and expressions of opinion contained in this publication are not intended to be a comprehensive study, nor to provide actuarial advice or advice of any nature and should not be treated as a substitute for specific advice concerning individual situations. On no account may any part of this presentation be reproduced without the written permission of the IFoA or authors. 18 September 2019 24

You can also read