New Challenges for the New Year - U.S.ECONOMIC OUTLOOK JANUARY 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

U.S. ECONOMIC OUTLOOK

New Challenges for

the New Year

JANUARY 2022

© 2022 Morning Consult, All Rights Reserved.

ABOUT THIS REPORT

Morning Consult’s monthly U.S Economic Outlook report provides an integrated

assessment of the strength of U.S. consumers, workers and households.

Businesses and investors rely on this report to understand emerging trends in

consumer demand, employment and personal finances.

The report draws on Morning Consult Economic Intelligence, a high-frequency,

global economic dataset, reflecting more than 11,000 daily economic surveys across

the 15 largest global economies.

2

IN THIS REPORT

4 U.S. Economic Outlook: January 2022

7 Consumer Confidence

14 Employment

27 Spending

30 Price Expectations

35 Personal Finances, Consumer Credit and Housing

43 Methodology

3

SECTION 1 U.S. ECONOMIC OUTLOOK: JANUARY 2022

SUMMARY

Confidence Employment Personal finances

Despite a rapid increase in cases, U.S. Rising COVID-19 cases negatively affected Financial vulnerability increased in

consumer confidence fell moderately in workers and job seekers in December. The December, with 22.3% of American adults

December. Morning Consult’s Index of incidence rate of pay or income losses spiked unable to pay their bills for a full month

Consumer Sentiment has fallen 0.9% since the week ending Dec. 18 before falling the last using just their savings. Increases in the

the onset of the omicron-driven surge in full week of the month. This moderate but costs of basic monthly necessities relative

COVID-19 cases, significantly below the 7% temporary increase in lost pay provides yet to wages are eating into Americans’

drop experienced during the delta-driven another signal of the growing resilience of the savings. If financially vulnerable adults were

surge in cases. While U.S. consumers have U.S. economy to the pandemic. Companies to lose their sources of income, they would

grown more resilient to COVID surges, are holding onto workers even as cases rise rapidly fall behind on their payments,

they are not yet in the clear, particularly as since they expect future demand to hold up. setting off a series of negative economic

the global economic recovery suffers due Given ongoing worker shortages, it makes and financial outcomes that the United

to omicron. more financial sense for companies to retain States has thus far avoided.

workers instead of laying them off and then

trying to rehire them.

U.S. Economic Outlook | New Challenges for the New Year 5

ECONOMIC INDICATORS DASHBOARD

CURRENT PERIOD PRIOR PERIOD CHANGE IMPACT

Consumer Confidence

ICS 89.4 89.9 0.5 pts ▼ NEGATIVE

Employment

Lost pay/income 12.6% 11.6% 1.0% ▲ NEGATIVE

Unemployment rate 13.6% 13.7% -0.1% ▼ POSITIVE

Labor force participation rate 55.0% 55.3% -0.3% ▼ NEGATIVE

Employment to population ratio 47.5% 47.7% -0.2% ▼ NEGATIVE

Personal Finances

Expenses were more than income* 13.8% 16.4% -2.6% ▼ POSITIVE

Financial vulnerability (unable

to pay basic expenses for a full 22.3% 21.5% 0.8% ▲ NEGATIVE

month using just savings)

*Current period for this series reflects survey data collected the first week of the month asking about personal finances during the prior month;

all other series compare the most recent data from the current month to the prior month

U.S. Economic Outlook | New Challenges for the New Year 6

SECTION 2 CONSUMER CONFIDENCE

CONSUMER CONFIDENCE REMAINS LARGELY STABLE DESPITE CASE SURGE

Morning Consult Daily U.S. Index of Consumer Sentiment

120 July 2021:

March 11, 2020: Dec. 27, 2020: Jan. 20, 2021:

WHO declares COVID- Trump signs second President Consumer confidence

115 begins to fall amid

19 a pandemic coronavirus relief Joe Biden’s

package into law inauguration COVID surge

110 March 13, 2020:

March 9, December

White House declares national

105 2020: 2021:

emergency over coronavirus pandemic

Dow Jones Consumer

100 Industrial Nov. 3, 2020: confidence

Average March 27, 2020: Election Day unfazed by

95 drops more President Donald Trump signs omicron

than 2,000 CARES Act into law

90 points March 6, 2021:

Senate passes

October 2021:

85 $1.9 trillion Supply issues

economic relief bill

and rising prices

80 Sept. 15, 2020: undermine

Average daily COVID-19 confidence

75 cases begin rising again

70

1

0

20

21

1

1

21

20

0

0

1

0

21

21

1

20

1

1

20

0

20

0

0

21

-2

-2

-2

l -2

r-2

-2

-2

-2

-2

-2

l -2

r-2

-2

-2

b-

g-

n-

p-

n-

b-

g-

p-

ay

ar

n-

ct

ec

ov

n-

Ju

ay

ar

ct

ec

ov

Ap

Ju

Fe

Ja

Ju

Au

Ap

Se

O

Fe

Ja

Ju

Au

M

Se

M

N

O

D

M

M

N

D

U.S. Economic Outlook | New Challenges for the New Year 8

SPIKE IN CASES HARDLY DENTED CONFIDENCE IN DECEMBER

New cases, 7-day moving average • Morning Consult’s Index of Consumer Sentiment (ICS) fell

300,000 by 0.5 points in December, giving up some of the gains

250,000 experienced in November.

200,000

• Possibly the most remarkable aspect of the decline in the

150,000 ICS last month was that it was not worse, given the nearly

100,000 unprecedented spike in cases in many parts of the

50,000 country. Overall, the 7-day moving average for new daily

0 COVID-19 cases in the United States rose from 73,000

near the end of November to 237,000 as of Dec. 27.

ICS, 7-day average • On the positive side — and likely a key factor in the

130 limited impact on confidence — hospitalizations and

120 deaths have been slower to rise compared to other

110

waves. Vaccinated adults especially are feeling more

100

protected, which is critical in supporting confidence as

90

adults inclined to receive the vaccine are also typically

80

70 more likely to have their confidence disrupted by rising

case counts.

Au 2 0

Au 2 1

Fe 2 1

N 21

O 21

Fe 2 0

M 20

N 20

Ju 2 1

O 20

Ju 0

M 21

Ju 1

Ap 21

D 21

1

Ap 20

D 20

Ja 0

M 21

Se 21

M 20

Se 20

2

-2

-2

-2

b-

g-

l-

n-

-

p-

-

r-

n-

-

-

l-

b-

g-

ay

ar

n-

r-

-

ct

p-

ec

ov

-

-

ay

ar

ct

ec

ov

Ja

Source: Morning Consult Economic Intelligence, Our World in Data, Johns Hopkins University CSSE COVID-19 Data

U.S. Economic Outlook | New Challenges for the New Year 9

OMICRON TESTING NEWFOUND RESILIENCE

Morning Consult U.S. Index of Consumer Sentiment, by annual household income • As previously reported, the U.S. economy

Rolling 30-day % change has becoming increasingly resilient to

COVID-19 surges over the course of the

Adults Less than $50,000 $50,000-$99,999 $100,000 or more pandemic, with each major COVID-19

15%

wave having a less severe impact on

10% consumer confidence.

5% • While the current wave of COVID-19 has yet

0% to peak, its impact on confidence has been

the most limited yet, with the 30-day rolling

-5% -0.9%

% change in the ICS reaching only -0.9% as

Omicron-driven

-10% -7.0% COVID surge of Dec. 28.

-15% -7.6% Delta-driven

• Despite increasing resilience, the U.S.

COVID surge

Second

-20% widespread economic recovery is looking increasingly

COVID outbreak fragile amid the rapid increase in new

-25% -27.6% COVID-19 cases. Historical data suggests

Initial U.S.

-30% COVID wave

that confidence could fall further as offices

shutter, airlines cancel flights and plans are

-35%

0 20 0 0 20 0 20 0 0 0 20 20 2 1 21 21 2 1 2 1 21 2 1 -21 2 1 2 1 21 21 widely disrupted, with the pandemic

eb -2 ar- p r-2 ay-2 un- Jul -2 ug - e p-2 c t-2 c t-2 ov- ec- Jan- Feb - Mar- Ap r- ay- Jun- Jul - Aug Se p- Oc t- Nov- Dec- remaining the primary risk to economic

F M A M J A S O O N D M

activity moving into 2022.

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 10WORRYING DECLINE IN PERCEPTIONS OF PERSONAL FINANCES

• Like November, an improving outlook for business Change in ICS and each of its components (Nov. 30 to Dec. 28)

conditions in the near term helped buoy the overall index,

with 12-month expectations rising 1 point in December.

Business Business Personal Personal

• However, the overall ICS declined 0.5 points in Conditions: Current Conditions: Finances: Finances: ICS

December, while the four remaining components of the 12-month Buying 5-year Current 12-month (Consumer

expectations Conditions expectations conditions expectations Sentiment)

index fell into the red, including expectations for longer-

term business conditions.

• Most alarming is the continued decline in perceptions of

1.0

current and future personal finances. Rising prices and

the omicron surge are having a real impact on

pocketbooks. As households begin to feel less certain

about their own finances, consumers may begin to pull -0.5

-0.2

back on spending, undermining the engine of the current -0.8

economic recovery. -1.0

-1.6

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 11OLDER CONSUMERS SLOWER TO REGAIN CONFIDENCE

• Older adults face much higher health risks Morning Consult Daily Index of Consumer Sentiment

from COVID-19, so it is no surprise that (% change from Jan. 1, 2020)

consumer confidence among baby boomers

Baby boomers Gen Xers Millennials Gen Zers

and Gen Xers fell further and has remained 5%

lower over the course of the pandemic.

0%

• In addition to public health risks, disparate

concerns over rising prices have also -5%

helped to widen the gap in recent months. -10%

Retired adults on fixed incomes face the

prospect of having their purchasing power -15%

eroded by inflation. Additionally, older -20%

Americans lived through the high inflation

period of the 1970s and 1980s and -25%

experienced the economic troubles that -30%

came with it.

-35%

-40%

c- 1

9

b -20 pr-20 n-2

0

g-2

0

t -2

0

c- 2

0

b -21 p r-2

1

n -21 g-21 c t -2

1

c -21

De F e A J u u Oc e Fe A Ju A u O De

A D

Source: Morning Consult Economic Intelligence

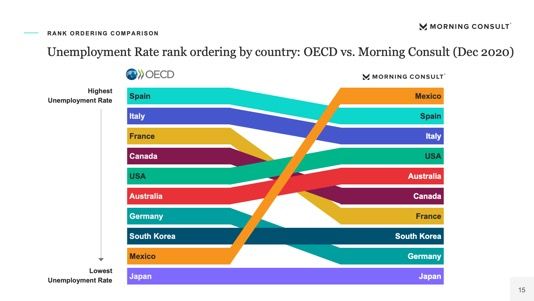

U.S. Economic Outlook | New Challenges for the New Year 12DETERIORATION IN GLOBAL CONFIDENCE POSES RISK TO U.S. ECONOMIC RECOVERY

• The rebound in global consumer confidence Morning Consult Index of Consumer Sentiment

continued to languish in December. For the (monthly averages, % change from beginning of pandemic)

third time in the last five months, the average 20%

change in Morning Consult’s ICS across all 12

major economies fell in December. From May

10% Japan

2020 to July 2021, average global consumer

France

confidence increased each month. Australia

• Even though U.S. consumer confidence appears 0% China

Mexico

stable in the face of the omicron variant, India

Russia

ongoing deterioration in global confidence acts -10% Canada

as a headwind to the U.S. economic recovery. U.K.

Germany

• China poses one of the largest risks to the U.S. Brazil

-20%

economy: While Chinese consumers remain U.S.

more optimistic about the economy relative to

October 2019, confidence has declined in -30%

recent weeks amid COVID-19 outbreaks and

growing housing market weaknesses. -40%

Prolonged lockdowns or business closures in

p-1

9

c- 1

9

r- 2

0

n-2

0

p-2

0

c- 2

0

ar- 2

1

n -21 p-2

1

c -21

China will likely exacerbate ongoing supply Se De M a J u Se De M Ju Se De

chain disruptions in the United States.

Source: Morning Consult Economic Intelligence. Index period is January 2020

for all countries except China, which is indexed to October 2019.

U.S. Economic Outlook | New Challenges for the New Year 13SECTION 3 EMPLOYMENT

DECEMBER’S SPIKE IN PAY LOSSES HIGHLIGHTS ECONOMY’S RESILIENCE

Share of U.S. adults who lost pay or income in the previous week, and • THE BAD: Morning Consult’s weekly lost pay or income

unemployment insurance initial claims tracker jumped in mid-December to reach its highest level

since June before easing in the week ending Dec. 25. The

Lost pay or income Initial claims, NSA Initial claims, SA spike was driven by the omicron variant as well as

seasonal factors, with companies laying off temporary

26% 3,000,000 hires brought on to accommodate the seasonal demand

July 31, July 31,

24% for workers.

2020: 2020:

2,500,000

$600 Sept. 4, $600 • THE GOOD: Based on Morning Consult’s data, rising

22% Sept. 4,

enhanced 2021: enhanced cases in mid-December produced a short and relatively

2,000,000 2021:

20% benefits $300 benefits

$300 mild increase in the incidence of lost pay. Given the

expire enhanced expire

enhanced stability of consumer confidence in the face of rising case

18% benefits 1,500,000

benefits

expire counts, businesses so far appear more concerned with

16% expire

1,000,000 retaining workers as a buffer against labor shortages than

14% with downsizing operations in case of potential demand

500,000 softening from omicron.

12%

• UNEMPLOYMENT CLAIMS MISS THE STORY: Morning

10% 0

Consult’s data provides novel insight into the omicron

Ja 0

M 1

21

No 0

0

No 1

1

Se 0

Se 1

M 1

Ja 0

M 21

21

No 0

0

No 1

1

Se 0

Se 1

M 1

l -2

2

-2

2

-2

l -2

2

l -2

2

2

-2

2

-2

variant’s true impact on employment since — unlike

l -2

2

2

-2

n-

v-

p-

n-

-

v-

p-

v-

p-

ar

ay

v-

Ju

p-

ar

ay

ay

Ju

Ju

ay

Ju

M

M

weekly unemployment insurance claims — the share of

adults experiencing pay or income losses is not

Source: Morning Consult Economic Intelligence, weekly surveys of a representative sample

influenced by changes in unemployment benefit eligibility.

of 20,000 U.S. adults on average

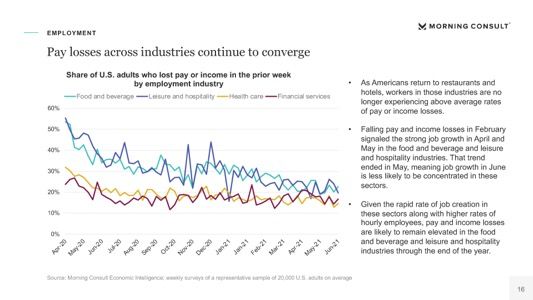

U.S. Economic Outlook | New Challenges for the New Year 15PAY LOSSES ACROSS DIFFERENT INDUSTRIES CONTINUE TO CONVERGE

• Pandemic-affected sectors are once again showing Share of U.S. adults who lost pay or income in the prior week, by employment industry

improved resilience to rising cases as consumers and (4-week moving average)

businesses adapt to living and working during the

pandemic with fewer disruptions to economic activity. Construction Financial services Food & beverage

• As of the week ending Dec. 25, 19.1% of workers in the Leisure & hospitality Manufacturing Technology

food and beverage industry reported a loss of pay or 60%

income. While the incidence rate remains higher than in

other industries, the food and beverage industry is no 50%

longer the outlier it once was.

• The relatively limited uptick in lost pay or income among 40%

food & beverage and leisure & hospitality workers during

the omicron surge provides an additional signal to out-of- 30%

work adults considering applying for jobs.

20%

• Looking ahead, the temporary and mild employment

impact of omicron on pandemic-affected industries will 10%

likely drive additional adults back into the labor force, as

was the case following the limited impact of the delta 0%

variant on pay losses.

Au 2 1

Au 2 0

Fe 1

M 21

O 1

N 21

O 1

O 0

N 20

Ju 1

O 0

Ju 0

Ju 1

Ap 1

Ju 0

D 21

1

Se 20

D 20

Ja 0

M 1

Se 21

2

-2

-2

2

2

-2

2

-2

2

-2

-2

2

-2

l-

b-

g-

n-

r-

-

p-

n-

-

g-

l-

ay

ar

-

ct

ct

p-

ec

ov

n-

-

ay

ct

ct

ec

ov

M

Source: Morning Consult Economic Intelligence; weekly surveys of a

representative sample of 20,000 U.S. adults on average

U.S. Economic Outlook | New Challenges for the New Year 16JOBS GROWTH SUFFERED A SETBACK IN LATE DECEMBER

U.S. (4-week moving average)

Note differences in scales

Unemployment Rate Employment to Population Ratio Labor Force Participation Rate

18% 50% 58%

16% 48% 56%

14% 46% 54%

12% 44% 52%

/ 21

/ 21

/20

/20

/21

/21

/21

/21

/21

/21

/21

/21

/21

/20

/20

/21

/ 21

/21

/21

/21

/20

/20

/21

/21

1/ 12

1/ 12

7/ 12

5/ 12

9/ 12

5/ 12

9/ 12

11/ 12

11/ 12

7/ 12

3/12

3/12

5/ 12

9/ 12

11/ 12

1/ 12

7/ 12

3/12

9/ 12

11/ 12

9/ 12

11/ 12

9/ 12

11/ 12

• Unemployment rate holds steady. Despite the rapid spread of the omicron • After peaking at 55.5% in early December, labor force participation

variant, unemployment held relatively steady over the month of December. dropped to 55.0% over the second half of the month. Seasonal factors and

Relative to prior surges, businesses appear to be responding with fewer the spread of the omicron variant likely contributed to the shrinking

layoffs this time, signaling that employers’ concerns about ongoing labor workforce. More than half of those leaving the labor force in December

shortages may be outweighing their desire to pre-empt possible pandemic moved from into the “Other” category, meaning that they did not identify as

impacts on business activity. homemakers, students, retirees or disabled.

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 17DECLINE IN LABOR FORCE PARTICIPATION MOSTLY DRIVEN BY VACCINATED ADULTS

U.S. labor force participation rate by vaccination status (4-week moving average) • Vaccinated adults drove the recent decrease in labor force

participation. As cases began to surge in December, vaccinated

Vaccinated Not vaccinated, and not planning to get it adults — who tend to be more concerned about contracting

57% COVID-19 — stopped looking for work and dropped out of the

labor force.

56%

• Labor force participation changed little for unvaccinated adults,

55%

suggesting that those who are not vaccinated and do not plan

54% to get a COVID-19 vaccine are less likely to opt out of working

53% due to health concerns associated with the pandemic, despite

the higher mortality rate among the unvaccinated.

52%

• Looking ahead, higher vaccination rates are unlikely to directly

51%

lead to higher labor force participation rates, but vaccinations

50% do play a critical, albeit indirect role in supporting job search

49% activity. The indirect impact of vaccinations on labor force

participation can already be felt: Vaccinations allowed the U.S.

/ 21

/ 21

1

1

1

21

/ 21

/ 21

3/21

/21

1/21

5/21

8/21

5/21

/21

/21

7/21

6/ 2

0/ 2

0/2

9/ 4/

economy to remain open during the delta and omicron case

9/ 18

12/ 4

11/ 13

11/ 6

9/ 11

10/ 9

10/ 2

12/ 1

11/ 2

10/ 2

9/ 2

12/ 1

12/ 2

10/ 1

11/ 2

10/ 3

surges, supporting the demand for workers despite rising cases

and encouraging out-of-work adults — vaccinated and

unvaccinated — to look for jobs.

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 18LABOR FORCE PARTICIPATION CONTRACTED SHARPLY FOR MIDDLE-INCOME ADULTS

U.S. unemployment rate by annual household income (4-week moving average) • In mid-December, joblessness for those with under $50,000

Note differences in scales in annual household income fell to nearly its lowest level

since the start of the series before flattening out over the

Under $50,000 $50,000-$99,999 $100,000 or more second half of the month. This group is the only one that has

26% 12% 8% not reached a new series low in terms of unemployment

within the past month. The lowest income group reported the

24% 10% 6%

least fluctuation in workforce membership recently, with the

22% 8% 4%

participation rate ranging between 48.4% to 48.6% over the

20% 6% 2% past six weeks.

/2 1

/2 1

/2 1

/2 1

11 /12 0

/2 0

/2 0

/2 0

/2 1

11 /12 1

/2 1

/2 1

/2 1

/2 1

3 /12 1

/21

/2 1

/2 1

/2 1

/2 1

/2 0

/2 0

/2 1

/21

/2

/2

/2

• The share of adults earning $50,000-$99,999 who said they

7/1 2

7/1 2

1/1 2

1/1 2

3 /12

11 /12

5/12

9/12

5/12

9/12

7/1 2

1/1 2

3 /12

5/12

9/12

11 /12

9/12

9/12

11 /12

9/12

11 /12

are currently working or looking for work declined sharply

over the second half of the month, falling from a series high

U.S. labor force participation rate by annual household income (4-week moving average)

Note differences in scales of 61.8% on Dec. 11 to 61.0% on Dec. 25.

• For those earning $100,000 or more, unemployment

50% 64% 74%

increased slightly over the second half of December. Adults

48% 62% 72% with higher incomes may have felt more able to separate

46% 60% 70% from jobs for seasonal reasons or to avoid exposure to the

omicron variant.

44% 58% 68%

/2 1

/2 1

/2 1

/2 0

/2 1

/2 1

11 /12 1

/2 1

11 /12 0

11 /12 0

/2 0

/2 1

11 /12 1

3 /12 1

/2 1

3 /12 1

/2 1

/2 0

/2 1

11 /12 1

/2 1

11 /12 0

/2 1

3 /12 1

/2

/2

/2

/2

/2

/2

/2

/2

/2

7/1 2

1/1 2

7/1 2

1/1 2

5/12

5/12

9/12

9/12

7/1 2

1/1 2

5/12

9/12

9/12

9/12

9/12

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 19GOVERNMENT DATA LIKELY TO REPORT FALLING UNEMPLOYMENT IN DECEMBER

Morning Consult high-income earners’ unemployment rate (4-week moving average) • Morning Consult’s unemployment rate for those in

vs. BLS unemployment rate (NSA) households earning $100,000 or more per year is strongly

positively correlated (.93) with the Bureau of Labor Statistics’

Morning Consult Bureau of Labor Statistics Forecast

headline unemployment rate. Midway through the month of

9%

December, high earners reported lower rates of joblessness

8% compared with a month prior.

7% • The BLS reference week falls in the first half of the month;

December’s unemployment number is therefore likely to

6%

stay flat around 3.9%.

5%

• Over the second half of December, Morning Consult found

4% that unemployment ticked slightly higher, but this occurred

after the period during which the BLS collects data for

3%

December and will likely not be reflected in government

2% data until the subsequent jobs report.

1%

0%

- 21

21

- 21

- 21

- 21

- 20

- 21

- 21

- 21

- 20

-20

-21

-21

-21

-21

-20

Jul-

Au g

Apr

Sep

May

Mar

Dec

Jan

Oct

F eb

Jun

Nov

Sep

Dec

Oct

Nov

Source: Morning Consult Economic Intelligence, Bureau of Labor Statistics

U.S. Economic Outlook | New Challenges for the New Year 20‘MORE MONEY’ TRUMPS OTHER MOTIVATORS FOR ACTIVE JOB SEEKERS

• Prior to the onset of omicron, more and more Share of active job seekers (both with and without jobs) who cited the following as what

workers in the United States were coming in off prompted them to look for work:

the sidelines and re-entering the labor force. At

the same time, a growing share of employed I wanted to earn more money 59%

workers are looking for a move.

• The reason for the uptick in active applicants is I ran out of savings 15%

clear: more money. In December, 59% of active

I wanted intellectual stimulation

applicants cited a desire to earn more money as or felt bored at my job 13%

a reason that prompted them to look for work,

dwarfing the next highest response. None of the above 9%

• While the prospect of a pay bump in a tight

My unemployment benefits ran out 8%

labor market is the primary driver, job seekers

also cited a lack of savings and a desire for

Other (please specify) 8%

intellectual stimulation as key motivators. If

savings continue to fall, more adults may begin Health concerns no longer

prevented me from working 8%

looking for work.

My home responsibilities no longer

prevented my ability to work 7%

Source: Morning Consult Economic Intelligence, survey conducted My investments or retirement fund

Dec. 14-18, 2021, among a representative sample of 2,191 U.S. adults. were not producing enough income 7%

Chart shows a subsample of 500 U.S. adults that were looking for

work in the past 4 weeks, with a margin of error of +/-4%.

U.S. Economic Outlook | New Challenges for the New Year 21GROWING SHARE OF PART-TIME WORKERS SEEK FULL-TIME WORK

• In December, the share of U.S. adults Would you like to work more than 35 hours per week? Of those who responded “No”, why?

who worked fewer than 35 hours per

week and said they would like to work

more hours inched higher to 48% from Yes Don't know No

Other family/

100%

personal

47% the month prior, continuing the

90% Other obligations

upward trend that began in August. 15%

80%

Child care

• The share of respondents who said 70% obligations

6% 37%

they did not want to work more than 60%

Health/

part-time also declined compared 50% medical 9%

limitations

to November. 40%

30% 16%

• Family or personal obligations other Retired/Social 17%

20%

than child care remained the most Security limit

10% on earnings School/

prominent reason for not wanting to training

0%

work more hours, but the share citing

0

1

20

20

0

0

1

21

21

1

1

0

20

21

1

21

20

20

21

21

21

Jun- 2

Jul -2

Jan-2

Ap r-2

Oc t-2

Jun- 2

Jul -2

Ap r-2

Oc t-2

health or medical limitations increased

Feb -

Aug -

May-

Se p-

Dec-

Mar-

Nov-

Aug -

May-

Se p-

Dec-

Nov-

from 13% to 16% between November

and December as concerns over the

omicron variant intensified.

Source: Morning Consult Economic Intelligence; monthly surveys of an average of 542 U.S. adults that worked

fewer than 35 hours per week, and 240 who did not want to work more than 35 hours per week in November.

U.S. Economic Outlook | New Challenges for the New Year 22OMICRON HAS YET TO RATTLE WORKERS

Share of employed U.S. adults who expect to experience a loss of • Workers who held onto their jobs

employment income in the next 4 weeks

in December largely expected to

avoid future pay losses, even in

the face of rising cases.

• Expectations for future

24.6%

23.2% employment income loss declined

22.4% 22.3% 22.3%

20.7% in December after nudging higher

19.8%

18.8% 19.1% the previous month. In December,

17.0% 16.7% 14.1% of employed U.S. adults said

14.6% 14.4% 14.1% they expected to lose income over

13.0% 13.3% 12.8% 13.5% 13.4%

the next 4 weeks after labor

metrics showed steady

improvement through the first half

of the month.

• Surveys are conducted mid-month,

meaning that December’s results

reflect workers’ level of concern

21

1

21

0

20

20

20

1

21

21

21

20

1

21

1

21

0

20

1

-2

l- 2

r-2

-2

-2

l- 2

-2

n-

p-

n-

c-

b-

g-

v-

p-

n-

v-

c-

ar

ct

g-

ay

even after news of omicron

Ju

ct

Ap

Ju

De

Ja

Ju

No

Fe

Au

Se

O

No

De

Ju

Au

M

Se

M

O

dominated the U.S. media.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among an average sample of roughly 1,000 employed U.S. adults

U.S. Economic Outlook | New Challenges for the New Year 23ACTIVE APPLICANTS DECLINED, THOUGH MORE THAN HALF OF WORKERS ARE STILL

OPEN TO JOB-SWITCHING

• While omicron did not elevate workers’ job-loss Share of U.S. workers actively applying for new positions (4-week moving average)

concerns, a smaller share of the total workforce

actively applied for new positions last month. In 20%

late December, 18.1% of employed workers

were actively applying for new positions, down

from 18.6% in late November.

• Despite the decrease in active applicants, 18%

employers worried about retaining their workers

are not yet out of the woods: While active

applicants fell, the share of workers open to

new positions climbed to a series high of 33.4%.

16%

In other words, a record-high share of workers

remain open to taking a new position.

• When new cases decrease, workers who are

open to new positions are likely to return to 14%

actively applying for them, driving quits higher

/2 1

/2 0

/2 1

/2 1

/2 1

/2 0

/2 1

/2 1

/2 1

/2 1

/2 1

/2 0

21

/21

/20

21 /

/

7/1 2

2

1/1 2

2

3 /12

4 /12

11 /12

2/12

5/12

6/12

8/12

9/12

2

2

11 /12

throughout 2022.

9/12

12/1

10 /1

12/1

10 /1

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 24LARGE SHARE OF WORKERS LOOKING TO RENEGOTIATE

Share of employed adults who have done the following in the past 12 months: • With job openings exceeding

job seekers, the average U.S.

worker is feeling emboldened to

Adults Men Women

use newfound leverage to ask

28% for increases in compensation

Asked for a raise 30%

and benefits.

25%

• In the last 12 months, 28% of U.S.

21% workers have asked for a raise,

Asked for a bonus 24%

16% 21% have asked for a bonus and

20% have asked for a promotion.

20%

Asked for a promotion 27% • Male workers were far more likely

13% to have negotiated than their

female colleagues. For example,

16%

Renegotiated your starting while 27% of male workers asked

21%

salary or benefit package

11% for a promotion this past year,

only 13% of female workers had

16%

Asked for an increase in the done so.

20%

number of paid vacation days

11%

Source: Morning Consult Economic Intelligence, survey conducted Dec. 14-18, 2021, among a representative sample of 1122 employed U.S. adults, with a margin of error of +/-3%.

U.S. Economic Outlook | New Challenges for the New Year 25MORE SOUTHERN WORKERS SATISFIED WITH BENEFITS, PAY

Share of employed adults who said they were “very satisfied” with each of the following • Workers in the South are more

aspects of their job: likely to express satisfaction with

their compensation and benefits,

South Midwest Northeast West

with the region ranking highest in

four of the five categories tracked

by Morning Consult — benefits,

51%

compensation, parental leave and

45% 45% paid time off.

42%

40% 40%

38% 38% • The West ranked highest among

36%

34% 33% the four regions in the share who

32%

31% 31% 30% said they were very satisfied with

29% 29% 29%

27% 27%

flexibility in work hours.

• Among the categories surveyed by

Morning Consult, U.S. workers

were overall more likely to say

they were very satisfied with

flexibility and vacation policies,

Benefits Compensation Flexibility in Maternity/ Paid time off/

work hours paternity leave Vacation policy while pay, overall benefits and

maternity/paternity leave lagged.

Source: Morning Consult Economic Intelligence, survey conducted Dec. 14-18, 2021, among a representative sample of 1122 employed U.S. adults, with a margin of error of +/-3%.

U.S. Economic Outlook | New Challenges for the New Year 26SECTION 4 SPENDING

U.S. ADULTS ALLOCATED ABOUT 34% OF MONTHLY HOUSEHOLD EXPENDITURES TO

HOUSING IN NOVEMBER, AND ABOUT 14% WENT TOWARD GROCERY PURCHASES

• Consumers continued to shift spending Reported average monthly spending in November by category, U.S. adults

toward discretionary categories as

incomes increased and lower spending $1,069

on staple goods and services freed up

space in monthly budgets.

• Soaring prices are discouraging Total = $3,105

▼ $11 from October

spending on housing, cars and food.

Spending at grocery stores and

restaurants was muted as higher $424

ingredient costs and worker wages

drove up prices in supermarket aisles $194

$142 $142 $135 $122 $113

and on menus. $101 $98 $95 $87 $78 $73

$65 $57 $44 $35

$32

• As expenditures declined on staple

categories like housing, cars and food,

Re tion

E d re l

m

e

Ap e

g

re

o n re p h o l

su s

ns as

Fu nt

y

p o re

s

T e rs

es

se ts

n

ea ure

el

ie

er

t io

nc

c

in

c

co

Ca

ra

fa

ca

G

ic

an

pa

consumers were left with more space

ilit

ot

ca odu

s

co

c

it

ra

a

rta

tra Air

au

rv

ou

le

ro

rn

H

ur

lth

uc

Ut

Al

st

G

r

H

in household budgets for discretionary in

re

ns

ri

H

lth

Ca

a

categories like travel, personal care

lc

ea

al

ic

a

H

bl

on

and apparel.

rs

Pu

rs

Pe

Pe

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 28TRANSPORTATION CATEGORIES AND DISCRETIONARY GOODS SAW A BOOST IN

SPENDING IN NOVEMBER

Percentage change in spending among U.S. adults from October to November 2021 • Total average spending changed little

from October to November, but

10% consumers continued to reallocate

7% purchases away from staple goods

6%

4% 4% 4% and toward transportation and other

3%

2% 2% 1% discretionary categories.

0% 0%

• Households spent less on housing,

0% -1% health care and food — though they

-1%

-2% -3%

also cut back on alcohol and

-5%

restaurant spending.

-11% • Housing and food prices continue

to climb amid ongoing shortages,

potentially discouraging spending

Ap n

Te e l

ce

ce

au g

H re

l

s

uc s

m

ea ery

es

rs

Al s

se e

ns cts

n

Fu els

re

ho

a

nt

re ilitie

io

io

Re usin

re rfar

r

Ca

co

itu

ca

ic

G

an

an

pa

u

at

ot

ra

lth tat

co

c

rv

Ca rod

le

ro

rn

in these categories.

i

ur

ur

H

lth

t

A

o

ea por

U

G

s

Ed

st

p

in

ns

ri

H

ca

• Transportation spending increased as

ca

tra

al

al

lic

H

on

the holiday season began, while goods

on

b

rs

Pu

rs

Pe

Pe

categories like apparel and furniture

also saw rising outlays.

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 29SECTION 5 PRICE EXPECTATIONS

INFLATION EXPECTATIONS DECLINED SLIGHTLY IN LATE DECEMBER DESPITE RISING CPI

Average inflation expectations for the next 12 months and historical inflation • U.S. adults said they expect prices to rise 5.3% on

growth over the previous 12 months average over the next 12 months (excluding outliers),

implying a slightly softer pace of price growth than that

Inflation expectations Year-on-year change in CPI

seen over the past 12 months according to the Bureau of

8.0% Labor Statistics’ consumer price index, which stood at a

November near 40-year high of 6.8% in November.

7.0%

October

• Unlike the highly volatile first half of the year, inflation

6.0% June expectations have essentially stabilized since peaking at

July August September

May 5.6% in mid-October.

5.0%

April • Observed inflation is likely to remain elevated through the

4.0% first quarter of 2022 as supply chain disruptions persist

and prices continue to come in above those from early

3.0% 2021. While inflation is likely to ease later in the year,

March

surging COVID-19 cases across the globe threaten to

2.0%

February derail progress with border closures and factory

1.0% shutdowns, which could limit the supply of goods

throughout next year.

3/ /21

7/ /21

5/ 21

12 /21

8/ /21

/2 1

5/ /21

7/ 21

2/ /21

4/ /21

8/ /21

12 /21

4/ /21

6/ 21

9/ 21

1

11/ 21

6/ /21

9/ 1/21

11/ /21

7/ 1

3/ /21

10 /21

10 9/2

/2

/2

/

/

3/

/

3/

8

14

22

28

20

/18

17

27

5

6

19

13

25

/4

13

10

24

27

31

1

/

2/

Source: Morning Consult Economic Intelligence, Bureau of Labor Statistics

U.S. Economic Outlook | New Challenges for the New Year 31THE SHARE OF ADULTS WHO ARE EXPECTING HIGHER PRICES DECLINED ACROSS MOST

CATEGORIES

Percentage-point change from October to November in the share of consumers who • Inflation has risen sharply across many categories as

said they expect prices to rise over the next 12 months in the following categories:

supply chain disruptions and strong consumer demand

drive up prices for cars, homes, grocery items and gas.

Food and groceries -4.1% • The share of consumers expecting further price increases

Electronics, computers or cellphones -2.8% decreased in nearly every category in November as

supply chain disruptions began to ease.

Energy and utility bills -2.1%

• Grocery prices — which spiked 6.4% year-on-year as of

A used car, pickup, van or sport utility vehicle -2.0%

November — had the biggest drop in the share of

A house or apartment -1.8% consumers expecting price increases. The pace of

A new car, pickup, van or sport utility vehicle -1.5% monthly price increases for this category peaked at 1.2%

in September and slowed in each subsequent month as

Motorcycles -1.5% supply chain disruptions began to ease.

Furniture -1.1%

Home appliances -1.0%

Home repairs, improvements or renovations -0.5%

Trips and vacations 0.2%

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 1,000 U.S. adults each

U.S. Economic Outlook | New Challenges for the New Year 32PRICE EXPECTATIONS FOR HOUSING OVER THE NEXT 12 MONTHS FELL IN NOVEMBER

Share of U.S. adults who expect housing prices to increase in the next 12 months, • The share of U.S. adults expecting price increases for

by community type housing over the next 12 months declined across all

community types, consistent with the recent slowdown in

the pace of annual price growth implied by the Case-

Rural Suburban Urban All U.S. adults

Shiller home price index.

• The latest shift in price expectations extended a roughly

The share of urban adults expecting price increases dropped,

70% flat trend over the past five months; while a slight majority

reversing a 3-month upward trend

continue to expect further price growth, the relative

60% stability of responses suggests people anticipate steadier

50% price gains, if not an actual slowdown.

• As monthly payment amounts fell for suburbanites, price

40%

expectations climbed; the recent fall in housing expenses

30% for those areas may be extending the runway for price

growth. Urban adults, meanwhile, reported a drop in price

20% expectations as payment amounts remained stable.

10%

0%

21

1

21

1

1

21

1

21

1

1

1

l- 2

-2

-2

r-2

-2

-2

-2

n-

n-

b-

g-

p

ay

ar

ct

v

Ju

Ap

Ju

No

Fe

Ja

Au

Se

O

M

M

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 33EXPECTATIONS FOR RISING FOOD PRICES DECLINED IN NOVEMBER

• 80% of adults ages 65 and older expect food prices to rise Share of U.S. adults expecting food prices to increase in the next 12 months,

over the next 12 months, up from 66% in February. People by age

in this age group, many of whom are retired and living off

fixed incomes, tend to worry more about inflation than 18-34 35-44 45-64 65 and over Adults

90%

working adults who can expect wages to rise in accordance

with prices. 80%

70%

• Those under age 35 — who tend to worry less about

inflation since rising wages might be expected to keep 60%

pace with price growth — were least likely to expect price

50%

increases. The gap between the oldest and youngest

adults expecting price growth widened to 36 percentage 40%

points from 27 points the prior month. 30%

• Overall, the share of adults expecting further price 20%

increases for food and groceries declined as supply chain 10%

congestion showed signs of easing in November compared

with the prior month, potentially alleviating some of the 0%

21

1

1

21

21

1

1

1

shortages that had driven up food costs.

1

1

-2

l- 2

-2

-2

-2

r-2

-2

n-

b-

g-

p

ar

ct

ay

v

Ju

Ap

Ju

No

Fe

Au

Se

O

M

M

Source: Morning Consult Economic Intelligence

U.S. Economic Outlook | New Challenges for the New Year 34SECTION 6 PERSONAL FINANCES, CONSUMER CREDIT AND HOUSING

THE SHARE OF HOUSEHOLDS WHERE EXPENSES EXCEEDED MONTHLY INCOME

DECREASED TO ITS LOWEST LEVEL SINCE JUNE

After you paid your recurring expenses last month, did you have any money left Of those who said their expenses were more than their

over that you could save or add to your savings? income, 75% earned less than $50,000 per year

No, our expenses were more than our income

No, our expenses roughly equaled our income with nothing left over

$100,000 or more

Yes, we had some money left over 5%

16% 14% 13% 12% 14% 14% 16% 15% 17% 16% 14%

25% 26% 25% 26% 25% 27% $50,000-

28% 26% 26% 26% 25%

$99,999

20%

Under

56% 61% 61% 63% 60% 61% 57% 58% 58% 59% 59% $50,000

75%

21

21

1

21

1

1

21

1

21

1

1

l- 2

-2

-2

r-2

-2

-2

n-

n-

-

b-

g-

p

ay

ar

ct

v

Ju

Ap

Ju

No

Fe

Ja

Au

Se

O

M

M

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults

U.S. Economic Outlook | New Challenges for the New Year 36FINANCIAL VULNERABILITY INCREASED IN DECEMBER

Share of adults lacking savings to pay basic expenses for a full month • The share of Americans who lack

savings to cover their basic expenses

Sept. 4, 2021:

June 2021: for a full month rose to 22.3% in

July 31, 2020: Federal

$600 per week States begin terminating unemployment December as inflation continued to

federal unemployment expanded federal unemployment benefits expire drive up costs for food, gas and other

benefits expire benefits (26 states total by Aug)

staple goods.

24.5%

22.8% 22.6% 23.1% 22.9% 22.6% • Financial vulnerability declined

21.9% 21.4% 22.3%

21.5% 21.0% 21.1% 21.5%

20.5% 20.7% gradually from June through

19.7%

18.7% 18.7% September, despite concerns over

17.4%

the delta variant and persistently low

workforce participation that limited

the share of adults earning paychecks.

• With the omicron variant driving up

case counts, employment may face a

setback, hurting wage incomes even

as costs are rising. Unlike earlier in the

pandemic, this lost income isn’t

expected to be replaced by

21

1

1

20

21

0

1

20

20

21

21

1

21

21

20

0

21

20

1

r- 2

-2

l-2

-2

-2

l-2

-2

n-

b-

g-

v-

p-

n-

c-

n-

v-

g-

p-

ay

ar

ct

c-

Ju

government transfers.

Ap

ct

Ju

De

No

Fe

Ja

Ju

Au

Se

O

No

De

Ju

Au

M

Se

M

O

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults

U.S. Economic Outlook | New Challenges for the New Year 37FEWER BOOMERS HAVE STUDENT LOANS, BUT THEY HAVE LARGER OUTSTANDING DEBTS

• In late December, the Department of Education extended the student loan • The policy will impact adults of all ages: While younger adults are more

payment pause until May. Payments had previously been set to resume on likely to say they have educational debt, baby boomers tend to report the

Feb. 1, 2022. largest total balances, possibly due to parents who assisted with loans for

their children.

Share of adults with educational debt, by generation

Average estimated total outstanding student loan balances, by generation

Gen Zers Millennials Gen Xers Baby boomers

18% Gen Zers Millennials Gen Xers Baby boomers

16%

14%

12%

10%

8% $23,084 $32,934 $31,875 $40,413

6%

4%

2%

0%

1

1

21

21

21

21

1

1

21

1

1

l- 2

-2

-2

r-2

-2

-2

n-

n-

-

b-

g-

p

ar

ct

ay

v

Ju

Ap

Ja

Ju

No

Fe

Au

Se

O

M

M

Correction: A previous version of this slide misidentified the generations associated with each average estimated total outstanding student loan balance.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among roughly 2,200 U.S. adults each. Average estimated outstanding loan balances are the average

estimated outstanding loan amount over the last 3 months, derived from monthly surveys of roughly 200 U.S. adults each over the past 3 months.

U.S. Economic Outlook | New Challenges for the New Year 38WHILE EVICTIONS DECLINED IN NOVEMBER, MISSED PAYMENTS SUGGEST THEY’LL

INCREASE AGAIN IN THE FUTURE

• The share of adults who reported receiving an eviction Share of adults that reported receiving an eviction notice

notice from their landlord decreased slightly in

November, ending a 2-month upward trend.

• However, the share of homeowners with mortgage or

rent payments who missed their monthly housing 7.7%

payments increased from 5.6% in August to 7.8% in 6.9%

6.4%

November, signaling that evictions are likely to increase 6.1%

in December. 5.5% 5.4% 5.4%

5.0% 5.1% 5.0%

• Looking further into 2022, the expiration of the federal 4.5%

eviction moratorium in August 2021 increases the

likelihood that missed housing payments will translate

into eviction notices. Like the expiration of federal

unemployment benefits, this policy change increases the

downside risk of future economic shocks caused by the

pandemic. If workers lose their jobs en masse in 2022,

the impact on the housing market will be more severe

21

1

1

21

21

21

1

1

21

1

1

l- 2

-2

-2

r-2

-2

-2

than anything experienced over the past two years.

n-

-

n-

b-

g-

p

ay

ar

ct

v

Ju

Ap

Ja

Ju

No

Fe

Au

Se

O

M

M

Source: Source: Morning Consult Economic Intelligence, monthly surveys conducted among an average monthly sample of 1,439 homeowners with mortgage and rent payments

U.S. Economic Outlook | New Challenges for the New Year 39REPORT AUTHORS

JOHN LEER

Chief Economist

@JohnCLeer

LEARN MORE

MorningConsult.com

KAYLA BRUUN FOLLOW US

@MorningConsult

Economic Analyst

@KaylaBruun

MEDIA & SPEAKING

INQUIRIES

press@morningconsult.com

JESSE WHEELER

Economic Analyst

@JesseSprWheeler

40ABOUT MORNING CONSULT

Morning Consult is a global enterprise technology company delivering

intelligent data to power leaders’ decisions. The company’s proprietary AI

technology, including both machine-learning and natural language processing

solutions, pairs with leading, high-frequency datasets and access to more than

100 million people globally in order to optimize decision-making. Morning

Consult’s proven approach gives users a leading advantage for more effective

decision-making at an unparalleled speed and scale.

41GET THE LATEST ECONOMIC ANALYSIS CLICK HERE TO SIGN UP

SECTION 7 METHODOLOGY

ECONOMIC MC E I D A T A I N T E L L I GE N C E C A P A B I L I T I E S

INTELLIGENCE Economic Intelligence collects over 15,000 daily responses on

key global macro economic indicators including:

Data Intelligence § Personal

Finances

§ Employment

Type

§ Pricing Effect

§ Supply

On Key Economic Indicators § Buying § Labor Market Expectations

Conditions Sizing § Demand

Morning Consult’s SaaS platform tracks key economic § Business § Future Price Expectations

Conditions Increases § Ability to Pay

indicators, including consumer sentiment, spending,

§ Employment § GDP

labor conditions, and more. Status expectations

Key Use Cases

T R A C K GL OB A L MON I T OR L A B OR & T R A C K I N F L A T I ON U N D E R S T A N D HOU S I N G

C ON S U ME R C ON F I D E N C E E MP L OY ME N T C ON D I T I ON S E X P E C T A T I ON S MA R K E T

Track global consumer confidence to Compare labor market conditions across Tracking consumer inflation expectations Tracking supply and demand of housing,

better understand and forecast consumer and within countries to identify job and the impact that has on consumer including buying and renting and ability to

spending. seekers with appropriate skill sets. spending and buying habits. make payments.

Available in 15 countries

USA CHINA JAPAN GERMANY UK FRANCE INDIA ITALY BRAZIL CANADA S KOREA RUSSIA AUSTRALIA SPAIN MEXICOWE USE RESPONSES TO FIVE DAILY SURVEY QUESTIONS TO MEASURE

CONSUMER SENTIMENT

Index of Cons. Index of Cons. Index of Current

Sentiment Expectations Conditions

(ICS) (ICE) (ICC)

❏ Better Now + % Pos. + % Pos.

Current Conditions: Would you say that you (and your family living

❏ Same - % Neg. - % Neg.

there) are better off or worse off financially than you were a year

❏ Worse

ago? + 100 + 100

❏ Don’t Know/No Opinion

Personal

Finances ❏ Will Be Better Off

12-Month Expectations: Now looking ahead — do you think that a + % Pos. + % Pos.

❏ Same - % Neg. - % Neg.

year from now you (and your family living there) will be better off

❏ Will Be Worse Off

financially, or worse off, or just about the same as now? + 100 + 100

❏ Don’t Know/No Opinion

❏ Good Times + % Pos. + % Pos.

12-Month Expectations: Now turning to business conditions in the

❏ Neither Good/Bad - % Neg. - % Neg.

country as a whole — do you think that during the next twelve

❏ Bad Times

months we’ll have good times financially, or bad times, or what? + 100 + 100

Business ❏ Don’t Know/No Opinion

Conditions 5-Year Expectations: Looking ahead, which would you say is more

❏ Good Times + % Pos. + % Pos.

likely — that in the country as a whole we’ll have continuous good - % Neg. - % Neg.

❏ Unem./Depression

times during the next 5 years or so, or that we will have periods of

❏ Don’t Know/No Opinion + 100 + 100

widespread unemployment or depression, or what?

Current Buying Conditions: Thinking about the big things people buy ❏ Good Time + % Pos. + % Pos.

Buying for their homes — such as furniture, a refrigerator, stove, television, ❏ Neither Good/Bad - % Neg. - % Neg.

Conditions and things like that. Generally speaking, do you think now is a good ❏ Bad Time

or bad time for people to buy major household items? ❏ Don’t Know/No Opinion + 100 + 100

avg. avg. avg.

ICS ICE ICC

U.S. Economic Outlook | New Challenges for the New Year 45WE USE RESPONSES TO FIVE DAILY SURVEY QUESTIONS TO MEASURE

CONSUMER SENTIMENT

THOUSANDS OF DAILY SURVEYS

Expanded

Unemployment Rate

Unemployment Rates

Labor Force Part-Time / Full-Time

Participation Rate Ratio

Employment to Employee Stickiness

Population Ratio Sentiment

✓ Consistent Cross-Country Data ✓ High Frequency Collection ✓ Detailed Demographic

Collection and Methodology & Reporting Segmentation Capabilities

U.S. Economic Outlook | New Challenges for the New Year 46LABOR MARKET METRICS

Morning Consult’s labor force calculations are simplified and standardized versions of those used by the Bureau of

Labor Statistics, the OECD and the International Labour Organization.

E MP LOY E D Working

U N E MP LOY E D Not working, but looking for work and not disabled

IN T HE LA B OR F OR C E Employed + Unemployed

Has a job, but is open to leaving current job or is actively

WILLIN G T O S WIT C H J OB S

applying for new jobs

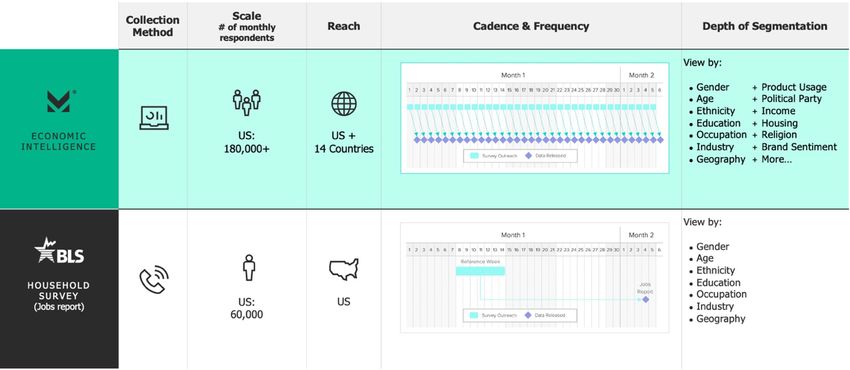

U.S. Economic Outlook | New Challenges for the New Year 47SURVEY COMPARISON

Morning Consult’s labor market data provides enhanced scale, frequency, and depth not captured in BLS data.

U.S. Economic Outlook | New Challenges for the New Year 48UNEMPLOYMENT RATE METHODOLOGY

Morning Consult’s unemployment rate calculation is a simplified version of the calculation used by the Bureau of Labor

Statistics.

Q3. Do you have a Q4. How would you describe

Q1. In the past week, did Q2. Did you actively look

disability that prevents

you do any work for pay for work in the past 4 your present employment

you from doing any kind

or profit? weeks? situation?

of work?

Job in the private sector

Job in government

No No No Self-employed

Homemaker

Yes Yes Yes Student

Retired

Unemployed

Other

Unemployed

( Actively

Searching & Able to Work ) Working in Private or Public Sector

(but answered Q1 “no”)

Unemployment

Rate = Labor Force

=

Worked in past

week

Working in Private or Public Sector

(but answered Q1 “no”) ( Actively

Searching & Able to Work )

U.S. Economic Outlook | New Challenges for the New Year 49© 2022 Morning Consult, All Rights Reserved.

You can also read