Stewardship Report 2021/2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Stewardship Report 2021/2022

Contents

Introduction .......................................................................................................................................................................................................................................... 3

ESG Integration at Sygnia ........................................................................................................................................................................................................ 7

Collaboration and industry involvement ....................................................................................................................................................................10

The Year in Review ......................................................................................................................................................................................................................13

Proxy Voting Outcomes ..........................................................................................................................................................................................................14

Passive Investing ...........................................................................................................................................................................................................................22

Fixed Income ....................................................................................................................................................................................................................................28

Sygnia Infrastructure..................................................................................................................................................................................................................32

Multi-Manager Portfolios ........................................................................................................................................................................................................34

Private Investments.....................................................................................................................................................................................................................36

Conclusion and Outlook .........................................................................................................................................................................................................42

Page 2

Introduction

Who is Sygnia?

Sygnia is an innovative financial services group based in South Africa and listed on the main board of the

JSE and A2X markets. The company provides asset management, stockbroking and administration services

and a wide range of savings products to institutional and retail clients, supported by cutting-edge

technology platforms.

Sygnia is the largest international equity exchange traded fund (ETF) provider (and the second largest

overall) in South Africa. It offers investors the widest range of ETFs that track international equity markets

and manages over R32.2 billion in ETF investments. Sygnia has approximately R295.3 billion assets under

management and administration, with 64% staff- and management-owned (including a BEE staff scheme).

Transformation at Sygnia

As a proudly South African company, Sygnia remains committed to sustainable transformation in all its

spheres of operation. Transformation and gender equality strategies are a priority, with black and female

staff percentages increasing annually.

Gender equality is strongly promoted, with significant focus on the promotion of women to key

management positions. That commitment is reflected in the following statistics:

• The chairperson is a woman.

• 22% of the board of directors are women.

• 59% of staff are women.

• Many senior management positions are held by women, including Head: Special Projects; Head:

Employee Benefit Operations; Head: Institutional Administration; Head: Human Resources; Head: Retail

Business; Head: Marketing; Head: Risk Management; Head: Sygnia Itrix; and Head: Manager Research.

Sygnia is a level 2 BBBEE contributor

Sygnia takes a holistic approach to transformation, implementing strategies across the Group, and takes a

long-term view on compliance with the New FSC (Financial Sector Code). The ownership aspect was

partially addressed through the formation of the vendor-financed Ulundi Staff Trust for black staff and

management in 2013 and its successful value creation for eligible beneficiaries on its unwinding in the 2021

financial year.

Page 3

Sygnia has taken additional steps to address its B-BBEE standing, including:

• Changing the composition of its board of directors;

• Expanding B-BBEE staff training initiatives;

• Participating in the YES initiative.

Sygnia takes BEE ownership seriously

Magda Wierzycka

2001

• Set up Kagiso Asset Management as a joint venture between Kagiso Trust and Coronation Fund

Managers

2003–2006

• CEO of African Harvest Asset Management, largest 70% black-owned asset management company in

South Africa

• Created R300 million value for black shareholders when AH was sold to Cadiz Asset Management in

2006

Page 4

Sygnia

2012

• Set up vendor-financed Ulundi Trust – a broad-based BEE staff scheme that owns 20% of Sygnia

Asset Management

• Net-of-debt valuation as at 31 October 2015: R100 million

• Average allocation per participant: R3.5 million

2015

• Preferential allocation of Sygnia shares to BEE shareholders when Sygnia listed on the JSE on

14 October 2015 (stipulated in the formal pre-listing statement)

2016

• Enabled the acquisition of an additional 1% shareholding by a BEE investor

Corporate social responsibility: Education

Sygnia recognises that the future of South Africa rests in its youth, and we are determined to empower

them to become beneficiaries of a better future.

Sygnia’s key corporate social investment focus is on education, investing in initiatives from early childhood

development through to tertiary education programmes. Sygnia provides bursaries to scholars and supports

outreach education initiatives in under-resourced schools.

Sygnia’s corporate social investment objectives support:

• Programmes and organisations that facilitate improvement and access to training and learning in South

Africa;

• Projects that focus on the welfare and development of children;

• Projects that recognise and develop talent;

• Projects with clear and direct delivery objectives and in which administration costs are kept to a

minimum.

Sygnia is proud to partner with and support the following organisations:

Elkana Childcare

Elkana Childcare focuses on building a sustainable future through the development of social and

environmental awareness in the lives of children who live in severely adverse situations.

Page 5

The Homestead

The Homestead focuses on the healing, care and upliftment of street children. The organisation runs a

number of projects that focus on neglected, abused and vulnerable children who live and beg on the

streets. These projects aim to provide for physical needs (food, shelter, safety, clothing), psychosocial needs

(trauma counselling, behaviour modification, positive self-image and identity, etc.), developmental needs

(access to education, support to improve school performance, life-sustaining skills) and sporting and

recreational activities.

Andrew Murray House

Andrew Murray House is a registered child and youth care centre (children’s home). The home is

responsible for the care, support, protection and development of the children in its custody through various

therapeutic and developmental programmes.

Impact Trust

The Impact Trust runs programmes to identify the key value of resilience in learners. One of their

programmes is Routes to Resilience, which works with high school students and young work-seekers to

build leadership skills focused on sustainability and a sense of purpose – individually and in the community.

Mitchell’s Plain Bursary and Role Model Trust

The Mitchell’s Plain Bursary and Role Model Trust gives funding to students at one of 17 identified schools

in Mitchell’s Plain or to those who live in the area. The trust assists students with registration and/or tuition

fees for studies at higher education institutions and further-education and training colleges.

O Grace Land

O Grace Land provides a temporary safe haven for vulnerable young women who grew up in care homes

and institutions and are preparing to enter adult life. The organisation offers both life skills and transitional

support as the young women complete their education and prepare for the working world.

Ray Mhlaba Skills Training Centre

The Ray Mhlaba Skills Training Centre is a non-government funded organisation that is an extension

program of the Eastern Province Child and Youth Care Centre. Through development programs, the centre

focuses on equipping unemployed and underprivileged youth with knowledge and skills to obtain formal

employment or become entrepreneurs.

Regional Educare Council

Regional Educare Council specialises in early childhood development ("ECD") programmes. The

organisation's passion is the holistic improvement of the quality of education for children, and they motivate

and provide training programmes for ECD practitioners to encourage growth in the field.

Page 6VUSA Academy

The VUSA Academy creates social upliftment for children from underprivileged communities through

structured academic, sporting and recreational programmes. VUSA works predominantly with children from

five schools in the Langa community, none of which have the staff or resources to implement effective

sporting or extra-mural programmes for their learners.

LEAP Science and Maths Schools

For more than ten years, LEAP has developed unique, self-liberating high school education programmes for

marginalised children through the only network of independent, no-fee schools in South Africa. The

programme identifies student potential in high-need communities and offers free education for students

who study mathematics, physical science and English.

Won Life

Won Life is a registered non-profit organisation dedicated to improving the quality of education for the

learners in the community of Fisantekraal, just outside of Durbanville. This is achieved through four

education-based programmes: the Early Learning Centre (Grade R), Literacy Centre, High School Education

Centre and Teacher Mentorship Programme.

Christel House

Christel House transforms the lives of impoverished children through robust education and a strong

character development programme that is supported by regular healthcare, nutritious meals, guidance

counselling, career planning, family assistance and college and careers support.

Environmental, social and governance

integration at Sygnia

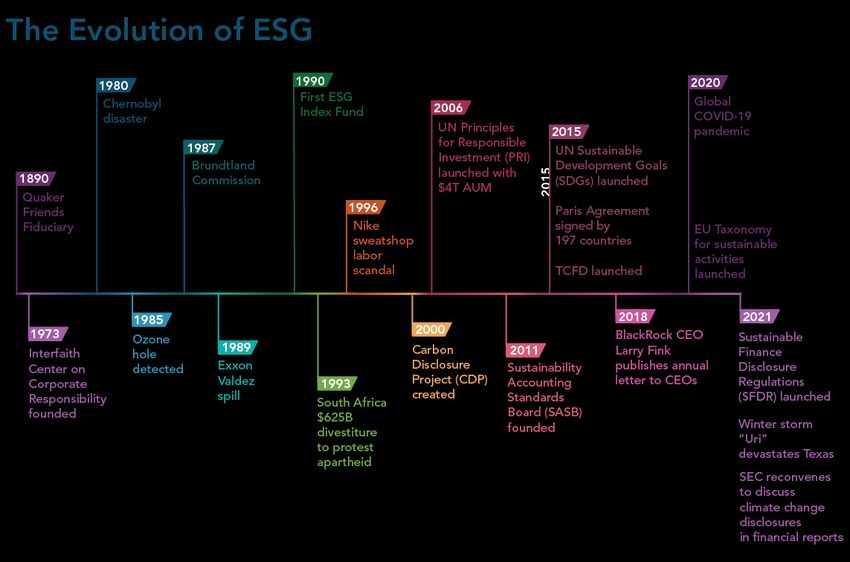

Environmental, social and governance (ESG) investing has evolved from what was known as socially

responsible investing (SRI) in the early 1960s, when portfolios excluded certain industries based on

involvement in particular business activities. SRI was initially a response to the Vietnam War, but other

events – such as the civil rights movement and the detection of the hole in the ozone layer – have

accelerated the growth of ESG.

Various guidelines and legislations have been developed to aid the evaluation of ESG investment factors.

Page 7Source: Dun & Bradstreet

Many approaches can be adopted to integrate ESG in the asset management industry. The table below

provides a brief guide to the typical ESG approaches used by the asset management industry globally.

Best-in-class Exclusions/Screening Thematic

Invests only in companies that Applies filters to lists of potential Targets a specific environmental or

lead their peer groups in ESG investments. social outcome; includes impact

performance; excludes investing. Invests in themes or

companies based on ESG assets specifically related to

criteria. sustainability.

Positive tilt Investing for impact Integration

Tilted towards sectors, Invests with the primary goal of Explicitly and systematically

companies or projects with achieving specific, positive includes ESG issues in investment

positive ESG characteristics; environmental/social benefits analysis and decisions.

excludes companies based on while delivering a financial return.

ESG criteria.

Page 8Because of the South African market’s size, it is a challenging one for pure ESG portfolios. Exclusion criteria

have the potential to create large active positions in an ESG portfolio. Sygnia has developed a sustainability

approach that offers products focused on having a positive impact while giving the investor market-related

returns.

The following industry frameworks and codes currently guide our approach:

• Compliance with the principles embodied in Regulation 28 of the Pension Funds Act ("Regulation 28")

in so far as it requires ESG considerations to be taken into account when devising investment

strategies for retirement funds;

• The principles embodied in the Code for Responsible lnvesting in South Africa ("CRISA"); and

• The principles embodied in the United Nations’ Principles of Responsible Investment.

Sygnia also reviews available research and industry best practices to ensure its approach remains relevant.

ESG integration at Sygnia can be broken down into multi-manager, passive and fixed income investments.

Products with ESG mandates may fall into any of these categories and are overarched by ongoing

shareholder activism. Sygnia also offers investment products with specific ESG mandates.

Multi-manager Passive/Equity Fixed income and infrastructure

• Documented ESG policy in • Proxy voting in • ESG issues increasingly form part

place collaboration with active of credit review as an assessment

managers in our multi- of non-financial risk

• Evidence to adherence of manager solutions

ESG policy • Engagement in the industry

• Low fees and accessibility around social, green and transition

• Proxy voting records to savings products for all bonds

• Engagement with

corporates

Products with ESG mandates

Shareholder activism

Page 9Collaboration and industry involvement

Code for Responsible Investing in South Africa

CRISA was launched on 19 July 2011 to encourage institutional investors and service providers to integrate

ESG issues into their investment decisions.

The five key principles of the code are:

1. An institutional investor should incorporate sustainability considerations, including ESG, into its

investment analysis and investment activities as part of the delivery of superior risk-adjusted returns to

the ultimate beneficiaries.

2. An institutional investor should demonstrate its acceptance of ownership responsibilities in its

investment arrangements and investment activities.

3. Where appropriate, institutional investors should consider a collaborative approach to promote

acceptance and implementation of the principles of CRISA and other codes and standards applicable to

institutional investors.

4. An institutional investor should recognise the circumstances and relationships that hold potential for

conflicts of interest and should proactively manage these when they occur.

5. To better enable stakeholders to make informed assessments, institutional investors should be

transparent about the content of their policies, how the policies are implemented and how CRISA is

applied.

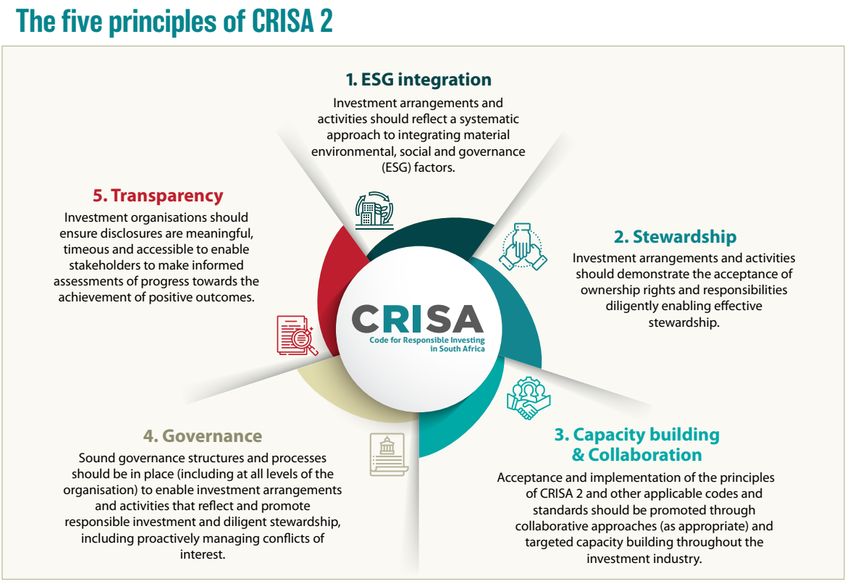

Page 10Code for Responsible Investing in South Africa 2 (CRISA 2)

CRISA 2, developed from CRISA 1, embodies a revision of the five principles to encourage stewardship and

responsible investing. CRISA 2 will come into effect for reporting on 1 February 2023.

CRISA 2 can be applied by any organisation in the investment industry or by related parties involved in or

providing investment services.

The five principles

The principles are relevant but completely voluntary and can be flexibly and proportionately applied should

companies choose to align with them.

The five principles of CRISA 2 and how they should be implemented:

1. ESG integration: Integrating material ESG factors into investment arrangements and activities.

2. Stewardship: Enabling diligent and effective stewardship by demonstrating acceptance of ownership

rights and responsibilities.

3. Capacity building and collaboration: Contributing to capacity building and collaboration of other

applicable codes in addition to CRISA 2.

Page 114. Governance: Governance should be implemented in an accountable manner by having sound governance

practices in place.

5. Transparency: Transparency should be promoted through meaningful disclosure to the attainment of

positive outcomes.

Objectives

While the main objective of CRISA 2 is to integrate stewardship and responsible investing into South

Africa’s governance framework, the code also aims to be relevant throughout the investment industry,

regardless of differentiating factors between organisations. CRISA 2 aims to foster integrated thinking

through the expansion of the six capitals (financial, manufactured, human, intellectual, social, and

relationship and natural capital) and the acknowledgement of the triple context (economy, society and

environment). In parallel with the innovation of sustainable investment products, this should incorporate the

United Nation’s Sustainable Development Goals and South Africa’s National Development Plans to achieve

a more equitable and inclusive economy and address specific South African issues.

Outcomes and application

By moving to an outcome-based approach, the code intends for companies to have a positive impact and

be more inclusive, innovative and resilient. Principle implementation to achieve these outcomes will not be

measured using metrics or targets. Companies can apply the principles proportionately as best suits them,

motivating the concept of “apply and explain”, whereby companies explain their interpretation of the

principles and their executed by the organisation.

Variances from CRISA 1 (2011)

At its core, CRISA 2 maintains the fundamentals of the first code. CRISA 2 was developed to embrace and

align with local and global enhancements that promote having policies in place that incorporate positive

ESG changes and encourages real action to implement these policies. By moving to an outcomes-based

approach under which the principles can be proportionately applied through the “apply and explain”

methodology, the code aims to be universally applicable regardless of investment strategy, asset class,

organisation size or any other factors. Additionally, more focus is placed on how to implement each

principle, while emphasising the significance of strong governance.

As part of its active citizenship, Sygnia participated in and submitted comments and feedback on the final

revised Code for public comment in November 2020. Sygnia uses the CRISA principals to guide our

responsible investing and will continue to do so with CRISA 2.

Page 12Association for Savings and Investments South Africa

(ASISA)

ASISA represents the collective interests of the country’s asset managers, collective

investment scheme management companies, linked investment service providers, multi-managers and life

insurance companies.

Sygnia has a representative member on the ASISA Responsible Investment Standing Committee, which

focuses on ESG-related issues. Its aim is to implement a strategy that enhances the uptake of responsible

investments in the South African market. The Committee works closely with the UN Principles for

Responsible Investment to integrate ESG factors into investment processes.

The year in review

The 26th United Nations Climate Change conference (COP26) was held in Glasgow, Scotland in the last

quarter of 2021, bringing together over 100 world leaders for two weeks to discuss a clear plan of action to

contain and mitigate climate change. The goal of the conference was for world leaders to recommit to

limiting the increase of the global average temperature to below 2° C and secure global net-zero emissions

by 2050.

Two key outcomes were the signing of the Glasgow Climate Pact and agreement on the Paris Rulebook.

The former sets out what must be done to tackle climate change, while the latter provides detailed

guidelines on how countries will achieve a zero-carbon future.

Following COP26, the first quarter of 2022 was particularly difficult, with the Russia-Ukraine war triggering

new ESG considerations, particularly in the energy and gas sector and the defence sector. Volatility and

global supply issues in the energy and gas sector led to speculation that some countries will renew their

own exploration and production of fossil fuels, but we view this as the perfect time to accelerate investment

into renewable energy.

Investments in defence companies also sparked some debate about their ESG compatibility. Like the

tobacco industry, defence sectors are often excluded from ESG screening, but the question arose as to

whether companies supplying Ukraine and NATO should be excluded for ostensibly contributing to

international peace and stability.

Sygnia is excited about the launch of National Treasury’s first national Green Finance Taxonomy, which is an

official classification or catalogue that defines a minimum set of assets, projects and sectors that may be

defined as "green", or environmentally friendly. It supports emerging national policy and voluntary private

sector initiatives to sustainable finance by reducing costs and uncertainty in classifying a core set of green

activities. National Treasury’s taxonomy is supported by the International Finance Corporation and will

ensure that South Africa aligns with global best practices.

Page 13South Africa’s taxonomy ensures that national priorities will be reflected while remaining aligned with

international trends. It takes account of the model adopted by the European Union, which identifies

activities that contribute to a set of six environmental objectives and includes requirements that activities

adhere to social safeguards and “do no significant harm” to any environmental objectives.

In particular, the Green Finance Taxonomy:

• provides clarity and certainty in selecting green investments in line with international best practices and

national priorities and standards;

• increases the credibility and transparency of green activities and helps unlock large-scale capital for

climate-friendly and green investment in South Africa;

• reduces financial risks through the enhanced management of environmental and social performance;

• reduces the costs associated with labelling and issuing green financial instruments;

• supports regulatory and supervisory oversight of the financial sector.

Sygnia looks forward to seeing what this taxonomy can bring to the industry.

Proxy-voting outcomes

Proxy voting has the power to influence corporate behaviour and has been identified as a tool that investors

can use to encourage better business practices. It currently forms part of Sygnia’s active ownership

approach.

Sygnia participates in shareholder votes by proxy and does not attend in-person meetings with investee

companies. After receiving and reviewing research, rationale and guidance from select active managers in

our stable, we submit proxy votes on the Sygnia domestic tracker funds.

Proxy voting outcomes

Sygnia voted on 753 resolutions in 2021/2022, with 61 dissenting votes.

Proxy votes by Sygnia domestic index-tracker funds

Resolutions voted for Resolutions voted against % against votes

2021 Q4 145 13 8.23%

2022 Q1 191 18 8.61%

2022 Q2 239 20 7.72%

2022 Q3* 117 10 7.87%

692 61

*2022 Q3 includes votes from 1 July 2022 to 31 August 2022.

Page 14As a multi-manager, Sygnia requests records of the proxy-voting actions taken on behalf of our investments

from all our underlying asset managers.

The table below summarises all votes submitted by our underlying active managers.

Proxy votes by active managers for 2021/2022

Resolutions Resolutions Resolutions Total per

Overall % against votes

voted for voted against abstained manager

Coronation 1 182 71 1 1 254 5.67%

Abax 1 009 58 1 1 068 5.43%

Ninety One 968 15 28 1 011 1.48%

All Weather 1 855 95 0 1 950 4.87%

Visio 938 137 0 1 075 12.74%

Fairtree 915 46 1 962 4.78%

Sygnia 692 61 0 753 8.10%

7 559 483 31 8 073 5.98%

Total

We have further categorised and tallied the dissenting vote totals as per the table below:

Dissenting votes by theme

Dissenting votes per category % dissenting votes per category

Capital structure 122 25.10%

Remuneration 128 26.67%

Board structure 136 28.33%

Strategy, audit & risk 59 12.29%

Environmental & social 3 0.63%

Other 38 7.92%

486 100.00%

Breakdown of the votes by theme

While not many dissenting votes shaped the environmental and social portion of the pie chart below, the

growing number of companies submitting resolutions associated with ESG developments (which are

favourably voted for) should be noted.

These resolutions are largely to increase disclosure and reporting on the climate and environmental impact

of a company and include the approval and/or implementation of strategic policies the company wishes to

enforce, to track progress they have made and set out targets they want to achieve.

Page 15Another common resolution reflected in the results was the re-election of directors. Many of the votes in

favour of individuals were justified by their certifications and their experience with ESG issues. This further

highlights the significance and rising corporate awareness of ESG factors, even filtering through to the

election of board directors. Board structure speaks to the governance pillar – the constitution of the board

will ensure the sustainability of the company and lead to improvements in the environmental and social

pillars.

Dissenting votes by theme

Remuneration

Board structure

26%

28%

Strategy, audit & risk

12%

Capital structure

25% Environmental &

social

Other

1%

8%

The board structure, remuneration and capital structure themes all link to the governance pillar,

emphasising that while the environmental and social pillars are important, the governance and structure of

the business drives the direction of the company.

In an ideal world, companies will always act with integrity and do not submit resolutions that bring the

aforementioned pillars into question. We do not live in an ideal world, however, so it is encouraging to see

that these three themes comprise the majority of the dissenting votes. This shows that shareholders are

using their votes to address issues, aligning the interests of all affected stakeholders.

Resolutions voted against under the remuneration theme mainly related to excessive remuneration,

unjustified premium proposals and inadequate disclosures of compensation.

Board structure-related resolutions that were voted against mainly related to independence. While most

candidates were seen as sufficiently experienced and qualified, concerns addressed conflicts of interest, a

lack of rotation and directors being on too many boards and having capacity constraints.

Page 16Resolutions for the capital-structure-themed dissenting votes included placing shares under the control of

the directors and giving directors general authority to allot and issue unissued shares.

Resolutions voted against in audit and risk addressed lack of rotation and concerns about independence,

while some resolutions were to discharge directors from liability. Justifications for voting against these

included the fact that directors should always be held accountable for their actions.

Case study 1: Naspers and Prosus

Governance

One of the most discussed resolutions voted on last year was the restructuring of Naspers and Prosus,

which was proposed in May, voted on in June and came into effect in August 2021. It granted Naspers

shareholders a tender offer of their existing ordinary shares for newly issued Prosus ordinary shares, which

caused a great deal of commotion and apprehension in the investor community. This led to asset managers

engaging with management about their concerns, predominantly about the devaluation of Naspers and how

to minimise the NAV discount in Naspers and Prosus over the long term.

Prior to deciding how we would proceed, we met and engaged extensively with our managers to discuss

their views and concerns about the restructuring.

Across the board, managers were concerned about the rationale of the overall transaction and worried that

a new share class would bring the governance further into question, as the rights of the minority

shareholders would weaken even more. The biggest concern was that the proposed exchange ratio did not

account for the Naspers discount with Prosus and did not appropriately compensate Naspers shareholders.

The fear that the NAV discount would widen and leave Naspers to become a stranded asset increased

considerably.

To address these concerns, a letter was collated and signed by the representatives of 36 local asset

managers with combined assets under management of over R3.6 trillion. These included 36One, Abax and

All Weather. Despite their dissenting views on the transaction, many managers noted that they would tender

their Naspers shares and convert them to Prosus shares should the resolution be passed. Other asset

managers who engaged directly with the management board included Allan Gray, Coronation, Investec and

Ninety One.

Following these manager meetings, Sygnia conducted a comprehensive analysis and made an informed

decision in the best interest of its funds. The discount on the buyout indicated a huge value unlock, and we

identified the potential benefit this could generate.

Taking this opportunity, we added value by adding alpha to our Life pooled funds, especially SLSWIX. Due to

regulatory restrictions, we were unfortunately unable to action this in our tracker funds (ITRIX and unit

trusts).

Page 17While this year’s Naspers and Prosus AGM offered some improvements, fundamental themes remained in

need of attention. Recurring key issues ranging from governance and audit committee issues to

remuneration policies were addressed but not resolved last year, and the reduced share price remained in

the spotlight.

Resolutions included the re-election of auditors, directors and audit committee members who had served

for an extended period and would not be following best governance practices should they continue in their

positions. This led to questions about their independence and the board’s rationale for recommending their

re-election. While many candidates possess a wealth of experience and qualifications, it was noted that

these were not unique skills and could be found in new candidates.

Remuneration outcomes last year evoked strong sentiment that existing policies did not align the interests

of management and shareholders. Management profited from the performance of a part of the business

they had no control over, while the market value of the holding company continued to fall.

The revised remuneration policy proposed this year reflected some positive adjustments, including the

removal of long-term incentives. In addition, short-term incentives now incorporate ESG and sustainability

targets. While this is encouraging, concerns remain about the substantial weighting these targets have in

the short-term incentive performance calculation, given that they are viewed to be quite subjective.

Moreover, a discount-linked short-term incentive was introduced to address the issue of the reduction in

NAV. Some asset managers feel this should have been explored and assessed when raised previously, but

its intention is to ensure that managers are only compensated on material improvement in the reduction of

NAV and ultimately to realign the interests of shareholders and management.

The charts below show the change in holdings across our managers for Naspers and Prosus from 31

December 2021 to 30 September 2022.

Naspers

16.00%

14.00%

12.00%

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

Coronation Laurium Ninety One Visio Abax All Weather Fairtree

Houseview

Equity Portfolio

2021/12/31 2022/03/31 2022/06/30 2022/09/30

Page 18Prosus

16.00%

14.00%

12.00%

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

Coronation Laurium Ninety One Visio Abax All Weather Fairtree

Houseview

Equity

Portfolio

2021/12/31 2022/03/31 2022/06/30 2022/09/30

Having the same theme of material issues over the past two years puts the company under constant

scrutiny and highlights the significance and necessity of good governance, and our external managers are

undoubtedly keeping a close eye on all submitted resolutions.

Case study 2: Standard Bank

Climate

Standard Bank, Africa’s largest bank by asset size, proposed several steps to achieve its group climate

policy commitments and targets at its annual general meeting (AGM) in May 2022. This came in the wake of

criticism from climate activists about the group’s involvement in an advisory role for the East African crude

oil pipeline and the group’s role in financing liquefied natural gas (LNG) development in Mozambique.

After approval of the group’s climate policy in 2021, shareholders voted overwhelmingly in favour of all three

resolutions relating to climate change in the 2022 AGM, meaning that the group must report on progress in

the calculation and disclosure of baseline-financed greenhouse gas emissions. Such emissions derive from

exposure to oil and gas, and the company aims to update its climate policy to include short-, medium- and

long-term targets for the group’s financed greenhouse gas emissions from oil and gas to align with the Paris

Agreement.

The chart below shows the changes in the weighting of Standard Bank across our managers for the period

31 December 2021 to 30 September 2022.

Page 19Standard Bank

7.00%

6.00%

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

Coronation Laurium Ninety One Visio Abax All Weather Fairtree

Houseview

Equity Portfolio

2021/12/31 2022/03/31 2022/06/30 2022/09/30

It is encouraging to see the group take active steps to report on its journey to net-zero carbon emissions by

2050. Over the past year the group also received approval for its annual report to society and its ESG report,

transformation report and the Task Force on Climate-Related Financial Disclosures climate-related

disclosure.

Case study 3: Sasol

Climate

Sasol is a global chemicals and energy company with operations in southern Africa, Asia, Europe and the

US. The company is a significant emitter of greenhouse and atmospheric gases, including of carbon dioxide,

methane, nitrogen oxide, volatile organic compounds and sulphur dioxide.

Sygnia and its external managers held conflicting views on whether Sasol would be able reach the targets

set out in its 2021 Climate Change Report. Concern was expressed about the report’s lack of detail around

the risks to achieve those targets and – based on methane leakage, which results in higher warming, and

the fact that new gas infrastructure could risk locking in emissions – whether replacing coal with natural gas

is a credible pathway to decarbonisation.

Manager proxy votes

Resolution: Approve climate change report

Manager Sygnia Ninety One Abax All Weather Fairtree

Vote Against For Against For For

* Votes are based on whether the share was held in the fund at the time of the AGM.

Page 20The change in Sasol holdings across our managers from 31 December 2021 to 30 September 2022 is

below:

Manager exposure to Sasol at each quarter end

6.00%

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

Coronation Laurium Ninety One Visio Abax All Weather Fairtree

Houseview

Equity Portfolio

2021/12/31 2022/03/31 2022/06/30 2022/09/30

The 2022 Sasol Climate Change Report addressed concerns about the transition from coal to gas,

recognising the importance of phasing out gas to reach its net-zero goal. However, due to gas’ lower

carbon footprint relative to coal, gas will be critical to reducing greenhouse gas (GHG) emissions in the

short to medium term and will include the introduction of LNG in a way that avoids potential infrastructure

lock-in. In the long term, Sasol’s preferred option would be to pursue a fossil fuel-free journey.

The bulk of Sasol’s carbon footprint is associated with its coal-dependent South African operations,

specifically its Secunda plant, which is one of the largest single-point sources of GHG emissions in the

world. Turning down boilers at the Secunda plant and using gas would reduce coal demand by

approximately 25%, which would help Sasol meet their air quality objectives and decrease their GHG

emissions.

Page 21Lifecycle of CO2e footprint of coal vs gas

Source: Sasol Climate Change Report 2022

Passive investing

Sygnia Itrix S&P Global 1200 ESG ETF

Exclusions/Screening

The Sygnia Itrix S&P Global 1200 ESG ETF tracks the S&P Global 1200 ESG Index, a subset of the S&P

Global 1200 index designed to measure the performance of securities that meet sustainability criteria while

maintaining the same overall industry group weights as the S&P Global 1200 Index.

Some sustainability criteria exclude companies based on business activities with a disqualifying UN Global

Compact score or based on specific business activities excluded from the eligible universe, as determined

by Sustainalytics. In addition to the exclusion criteria, each company gets a score for ESG issues, with the

top 75% of companies in each sector included.

Excluded business activities include:

• Tobacco: Companies directly or via an ownership stake of 25% or more invested in another company

that produces tobacco, or when tobacco or tobacco-related products and services account for more

than 10% of their revenue.

Page 22• Controversial weapons: Companies directly or via an ownership stake of 25% or more in another

company that is involved with cluster weapons, landmines, biological or chemical weapons, depleted

uranium weapons, white phosphorus weapons and nuclear weapons.

• Thermal coal: Companies that extract thermal coal or generate electricity from thermal coal or with a

level of involvement/exposure greater than 5%.

• Low UN Global Compact score: All companies at or below the bottom 5% of the UN Global Compact

score universe are ineligible.

This ETF provides exposure to the S&P Global 1200 with an ESG overlay. Its return profile is closely related

to the S&P Global 1200. The Sygnia Itrix S&P Global 1200 ESG ETF puts the world of sustainable investing

at your fingertips and offers extremely cost-effective access to a well-diversified portfolio of global stocks

while meeting sustainability criteria.

Based on the latest fund fact sheets, the table below provides an indicative comparison between the S&P

Global 1200 Index and the S&P Global 1200 ESG Index.

Indicator Global 1200 Global 1200 ESG Reduction in emissions

Carbon to value invested (metric tons

Co2e/$1 m invested) 79.42 68.65 -13.56%

Carbon to revenue (metric tons co2e/$1 m

revenues) 213.25 189.04 -11.35%

Weighted average carbon intensity (metric

tons co2e/$1 m revenues) 218.9 184.8 -15.58%

Fossil fuel reserve emissions (metric tons

co2e/$1 m invested) 1 170.08 877.61 -25.00%

*Comparison based on the latest index fund fact sheets for the S&P Global 1200 and S&P Global 1200 ESG and are not actual data

on the Sygnia Itrix S&P Global 1200 ESG ETF. Data are based on calculations by S&P. An explanation of these metrics is provided on

the S&P website: https://www.spglobal.com/spdji/en/documents/additional-material/spdji-esg-carbon-metrics.pdf.

Sygnia Itrix Solactive Healthcare 150 Index ETF and Sygnia Health

Innovation Global Equity Fund unit trust

Thematic and exclusions/screening

Industrial technology and processes have converged, benefitting the biotech industry, which includes

healthcare. An ageing population and the recent Covid-19 pandemic have accelerated healthcare

innovation, with BioNTech recently developing a successful SARS-CoV-2 vaccine quickly and safely,

leveraging decades of scientific experience. This area of healthcare is expected to grow exponentially, with

developments in genomic sequencing set to solve more healthcare conditions.

Page 23The Sygnia Health Innovation Fund offers access to global companies optimally positioned to benefit from

new health-related technologies and innovations, including pharmaceuticals, genomics, biotechnology,

nanotechnology, information technology, nutrition, well-being and fitness, genetic engineering, medical

robotics and medical 3D-printing technologies.

Fund construction includes the 150 largest healthcare companies in the developed world and satellite

investments in companies driving innovation in healthcare (e.g. biotechnology, genomics, digital health).

Companies are also screened based on ESG criteria.

We scored our Health Innovation Fund using the Thomson Reuters ESG methodology for an overall score of

73.09 out of 100.

Overall ESG

Name Weight ESG score

score

Oxford Sciences Innovation plc 1.94%

SBSA ITF Sygnia Health Innovation Genomics and

5.75% 50.17 2.88

Biotech Sub-Fund Seg

SBSA ITF Sygnia Health Innovation Global Equity Fund

73.57% 76.46 56.25

Seg

Prescient Global – Sygnia Health Innovation Global

18.01% 74.34 13.39

Equity Fund Class B

Sygnia Itrix Solactive Healthcare 150 ETF 0.73% 76.20 0.56

73.09

Companies in the portfolio include:

• Pfizer: Development/production of a wide range of medicines and vaccines in medical fields including

immunology, oncology, cardiology, endocrinology and neurology.

• Illumina: Global leader in DNA sequencing and array-based technologies for genetic and genomic

analysis, enabling the adoption of genomic solutions in research and clinical settings.

• Biomarin: World leader in developing and commercialising gene therapies for rare diseases. Biomarin

has a diverse pipeline that builds on its genetic and genomic expertise, manufacturing capabilities and

long-term partnering models.

Page 24Sygnia 4th Industrial Revolution Global Equity Fund (UCITS)

Exclusions/Screening

Sygnia prides itself on being an innovative fintech market disruptor that offers investors access to ground-

breaking, company-leading tech innovation, to which end the Sygnia 4th Industrial Revolution Global Equity

UCITS Fund was launched in November 2021. The Fund’s stock selection is based on the S&P Kensho New

Economy Indices, which provide exposure to companies that bring 4th Industrial Revolution themes to life.

Stocks within the universe are weighted by several criteria to determine their weighting in the Fund,

including fundamental valuation, price and earnings momentum, liquidity, market cap and sub-industry

weight. Finally, an adjustment to the allocation of the single stocks is made by applying an ESG screening

criteria.

ESG screening and methodology

A unique list of the underlying companies in each of the 25 Kensho New Economy subsector indices is

selected and rated out of 100 using ESG data provided by Refinitiv (Thomson Reuters). The selected

companies are then split into four quartiles based on their ESG scoring. The companies with the higher ESG

scoring receive higher weights in the portfolios.

• ESG score: 0–25, including 70% of the pre-ESG weight in final model,

• ESG score: 26–50, including 80% of the pre-ESG weight in final model,

• ESG score: 51–75, including 90% of the pre-ESG weight in final model,

• ESG score: 76–100, including 100% of the pre-ESG weight in final model.

Sygnia Itrix Sustainable Economy ETF

Impact and positive tilt

The growing interest in climate change and technologies that contribute to shaping the future led us to

launch the new Sygnia Itrix Sustainable Economy ETF. We believe this ETF meets the need in the

marketplace for innovative products focused on rapid advancements in technology, the global shift to

remote working, the increased use of smart technologies and institutional and individual focus on climate

change.

The ETF provides access to companies in the S&P Kensho Sustainable Technologies Index (KSUSTN),

which has an ESG overlay that screens out companies that generate revenue from thermal-coal

production/extraction or from shale, Arctic or oil-sands oil and gas extraction. Companies in violation of the

ESG screens are dropped, and the weights of the remaining constituents are scaled up to 100%.

Page 25The S&P Kensho Sustainable Technologies Index is made up of the seven component indices listed below.

S&P Kensho Advanced Manufacturing Index Measures the performance of companies focused on

enabling manufacturers to improve production

processes through digitalisation, automation, predictive

maintenance and optimisation of plant energy

conservation.

S&P Kensho Sustainable Staples Index Measures the performance of companies enabling

connected agricultural producers to enhance output

while reducing waste and resource exhaustion using

state-of-the-art sustainable practices.

S&P Kensho Clean Power Index Measures the performance of companies focused on

advances in clean technology and energy.

S&P Kensho Intelligent Infrastructure Index Measures the performance of companies that reflect the

transition to intelligent, adaptive and connected

infrastructure.

S&P Kensho Smart Transportation Index Measures the performance of companies focused on

autonomous and electric vehicle technology, commercial

drones and advanced transportation systems.

S&P Kensho Future Communication Index Measures the performance of companies focused on

advances in how people meet, collaborate and

communicate.

S&P Kensho Final Frontiers Index Measures the performance of companies focused on

technologies at the forefront of deep-space and deep-

sea exploration and development.

The ETF is broken up into four segments, providing access to companies involved with smart transportation

and manufacturing, sustainable agriculture, clean power, space exploration, intelligent infrastructure and

technologies that enable remote working.

The segments – and examples of companies likely to be included in them – are described below:

Sustainable infrastructure

Plug Power

Plug Power is building the hydrogen economy and is the leading provider of comprehensive hydrogen fuel

cell turnkey solutions. Amid an ongoing paradigm shift in the power, energy and transportation industries,

the company’s innovative technology powers electric motors with hydrogen fuel cells to address climate

change and energy security while providing efficiency gains and meeting sustainability goals.

Page 26Sustainable agriculture

Nutrien

Nutrien is the world's largest provider of crop inputs and services, playing a critical role in helping growers

increase food production in a sustainable manner. They produce and distribute over 27 million tons

of potash, nitrogen and phosphate products for agricultural, industrial and feed customers worldwide.

Combined with their leading agricultural retail network, which services over 500 000 grower accounts, they

are well positioned to meet the needs of a growing world and create value for our stakeholders.

Sustainable manufacturing

Boeing

As a leading global aerospace company, Boeing develops, manufactures and services commercial airplanes,

defence products and space systems for customers in more than 150 countries. As a top US exporter, the

company leverages the talents of a global supplier base to advance economic opportunity, sustainability

and community impact. Boeing’s diverse team is committed to innovating for the future, leading with

sustainability and cultivating a culture based on the company’s core values of safety, quality and integrity.

Sustainable society

Metaverse

Bloomberg projects that the metaverse market may reach a US$783 bn valuation in 2024, enabling people

to meet, collaborate and communicate online in the metaverse or in extended reality.

Features of the metaverse include:

• Enterprise collaboration frameworks (Zoom).

• Digital communities: Microsoft and Meta (Facebook) are building virtual worlds.

• Real estate in the metaverse has sold for more than US$500 000.

• Brands are teaming up with social game developers, e.g. Fortnite (Tencent) and Warcraft (Activision

Blizzard).

• Infrastructure supplies are ramping up production (Nvidia, Unity and Roblox). VR headset sales are

projected to surpass 34 million units by 2024 (Oculus, VIVE, Varjo, Pico).

• Google is looking into Web 3.0, which will allow composable smart contracts – programmable

blockchains that will allow rapid increases in innovation and entrepreneurship through a decentralised

internet.

Page 27Fixed income

Sygnia’s fixed income portfolios consist of tracker funds, multi-manager products and in-house actively

managed funds. Proxy voting does not apply to debt instruments, but there is scope for engagement within

debt instruments via debt arrangers, industry collaboration and at investor roadshows. We hold underlying

managers in our multi-manager products to account per the standards outlined in the previous section,

while for active funds we incorporate ESG considerations into the evaluation of potential investments and

engage with issuers through the appropriate fixed income forums.

Sygnia Money Market Fund Unit Trust

Impact

Sygnia has been a vocal advocate for lower fees to allow easier access to investments. Our ongoing

shareholder activism has also allowed us to be forthright about social change, and our Sygnia Money

Market Fund management fees are donated to fight corruption in South Africa.

The fund is suitable for investors who would like to make a meaningful difference in the South African

landscape by supporting non-political organisations that fight corruption in the public and private sectors.

Organisations that Sygnia donates to include:

• Helen Suzman Foundation

The Foundation’s liberalism is grounded in Helen Suzman’s legacy and draws on the history of liberal

thought in South Africa. It promotes liberal constitutional democracy and the rule of law, believing the South

African Constitution to be a liberal document. The preamble to the Constitution calls for “a society based on

democratic values, social justice and fundamental human rights” that aims to “free the potential of each

person” and in which “every citizen is equally protected by law”. The Foundation promotes good

governance, transparency and accountability and advocates for policies that translate the aspirations of our

Constitution into lived reality for all South Africans.

• Organisation Undoing Tax Abuse (OUTA)

OUTA is a civil society organisation focused on combatting fraud, corruption, maladministration and fruitless

and wasteful expenditure across government at local, provincial and national level and on holding

perpetrators to account.

• Ahmed Kathrada Foundation

The Foundation was formed in 2008 to continue the legacy of anti-apartheid struggle stalwart Ahmed

Kathrada and his generation. The Foundation is an independent, non-partisan entity. Kathrada, a former

Robben Island prisoner, served 26 years in jail alongside his fellow Rivonia Trialists for their stance against

the apartheid government. Kathrada’s life was characterised by his commitment to the best values and

principles of the South African liberation struggle, particularly that of non-racialism.

Page 28• Corruption Watch

Corruption Watch is a non-profit organisation launched in January 2012 that relies on the public to report

corruption to it. The NPO uses such reports as an important source of information to fight corruption and

hold leaders accountable.

• The Black Sash Trust

Founded in 1955, the Black Sash works towards the advancement and realisation of human rights and

social justice in South Africa as outlined in the South African Constitution. The organisation emphasises

social security and access to justice for all who live in South Africa, but particularly for women, children and

the most vulnerable. In the quest for the realisation of socioeconomic rights, the Black Sash monitors

government service delivery, disseminates information and advocates for policy and process changes.

• Council for the Advancement of the South African Constitution (CASAC)

CASAC was formed in September 2010 out of rising concern about the shift in the political culture in South

Africa and in the leadership of the ANC, and it has established itself as a key role player in the civil society

environment. CASAC’s driving motivation is that the Constitution provides the principled bedrock for the

operation of public and private power in South Africa.

CASAC is a project of progressive people who want to advance the South African Constitution as the

platform for democratic politics, the advancement of human rights and the socioeconomic transformation of

society. It subscribes to the principles and values enunciated in section 1 of the Constitution and promotes

the notion of progressive constitutionalism to advance the rights of citizens and protect human dignity.

CASAC’s key focus areas can be summarised as:

• Building a culture of human rights.

• Strengthening institutions of governance and the rule of law.

• Promoting accountability and integrity in public life.

Debt capital markets: ESG bond issuance

The first social and sustainability-linked bonds were issued in the debt capital market in 2021. More than

R7.3 bn worth of ESG bonds were issued in the first half of 2022, with only R1.3 bn of that issuance via

private placement. ABSA, FirstRand Bank and Investec Bank all issued inaugural ESG bonds.

Page 29JSE-listed ESG bonds as at 30 June 2022

14000

12000

10000

8000

R(m)

6000

4000

2000

0

2014 2015 2016 2017 2018 2019 2020 2021 2022

Green bonds Sustainability- linked Bonds Social Bonds

Source: RMB, JSE

Examples of JSE-listed ESG bonds

Barloworld sustainability-linked bond

Sygnia participated in the private placement of a sustainability-linked bond issued by Barloworld in June

2022 that raised a total of R1.1 bn across two notes.

The bond includes key-performance indicators (KPIs), which, if met, would result in a step-down in the

coupon payable, thereby reducing interest costs to the issuer. The bond also includes a step-up clause if

the KPIs are not met.

The KPIs are:

• Decreasing the lost-time injury frequency rate by 6%, resulting in a coupon adjustment of 2 basis points

per applicable period.

• Increasing solar-powered photovoltaic (PV) energy consumption by 20%, resulting in a coupon

adjustment of 3 basis points per applicable period.

Fortress sustainability-linked bond

Sygnia took up an allocation of a sustainability-linked bond in February 2022 issued by Fortress REIT Ltd, a

JSE-listed property fund.

The KPI focused on the installation of an additional 4.2 MWp solar capacity at properties owned by Fortress

from an existing, baseline capacity of 4.735 MWp. Should the KPI be met, the coupon would ratchet down

by 10 basis points per applicable period. However, if the KPI is not met, the coupon would ratchet up by 5

basis points per applicable period.

Page 30Barloworld gender-linked bond

The JSE has also seen an increase in the issuance of social bonds, including gender-linked bonds.

Barloworld came to market with an ESG-linked bond for which KPIs focus on gender diversity.

Unfortunately, Sygnia was at its maximum exposure (set by our credit committee) to this issuer at the time

of the auction and did not participate in this round.

The KPIs:

• Increasing the gender diversity in company leadership from a baseline of 44.9% across the Board and

Executive Committee to 50% by 2025.

• Growing the proportion of black, women-owned businesses in the company’s supply chain from a

baseline of 13.8% to 15% by 2025.

Although punitive step-up ratchets are applied to the coupon should targets not be met, these increases

are smaller than the corresponding step-down ratchets.

Sygnia Global Income Fund

In November 2021, Sygnia launched the Sygnia Global Income Fund, a dollar-denominated portfolio

domiciled in Ireland.

The Fund invests in a portfolio of investment-grade debt securities, cash deposits and money market

instruments, adopting a thematic approach whereby it invests primarily in debt securities specifically related

to environmentally sustainable activities (i.e. green bonds). As ESG is incorporated into the investment

process, the fund is currently classified as Article 6 per Sustainable Finance Disclosure Regulations criteria.

The voluntary International Capital Market Association (ICMA) Green Bond Principles 2018 are used as a

guide for the Fund’s thematic approach. Sygnia favours bonds that have been subject to independent green

bond verification and certification against a recognised external green standard or green bond scoring.

One of the ESG bonds held within the fund is described below.

Apple Bond (AAPL 2.85 02/23/23)

The bond is a fixed rate, semi-annual coupon bond that matures on 23 February 2023.

The use-of-proceeds bond allocates funds to the following eligible projects: renewable energy; energy

efficiency; pollution prevention and control; sustainable water and wastewater management; circular

economy adapted products, production technologies and processes; and green buildings.

EY audits the allocation of green bond proceeds to ensure compliance with the stated ESG requirements.

Page 31You can also read