Swiss Re - Leading Global Re/Insurer - Company presentation as of April 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Swiss Re – Leading Global Re/Insurer Company presentation as of April 2019

Swiss Re – Leading Global Re/Insurer

Overview and Capital P&C and L&H Corporate

Group Strategy Management Reinsurance Solutions

page 4 page 23 page 31 page 41

Life Asset Global Re/Insurance

Capital Management & Protection Gap

page 46 page 51 page 58

Swiss Re Group | Company presentation | April 2019 2

A truly global reinsurer1… Profitable long-term growth opportunities

• Reinsurance market growth of 4-5%3 p.a.

21%

• Differentiation through transactions, solutions and core Group financial

47% • No 1 reinsurer in High Growth Markets targets

• Life Capital open book 2015-18 GPW CAGR of 30% over-the-cycle

32%

• Corporate Solutions focusing on ROE target

Financial strength and defensive profile RoE ≥

Americas EMEA Asia

• Group SST ratio of 251%, well above target level of 220% risk free

• Capital strength remains resilient to market movements +700bps

…strongly diversified2 • AA- S&P credit rating, A.M. Best A+

12% • Strong diversification benefit

9% • Low investment risk4

38% ENW6 per

Sector-leading capital management share growth

40%

• Net solvency capital generation of USD 2.6bn5 +10% p.a.

• Dividend CAGR of 8% over 2012-2018

P&C Re Corporate Solutions

• Disciplined M&A strategy and organic deployment

L&H Re Life Capital • Special dividend & buy-backs of USD 6.2bn since 2014

1 Net premiums earned by region 3 10-year outlook: 5% for P&C reinsurance and 4% for L&H reinsurance; source: Swiss Re Institute 5 Average 2014-2019

2 Economic Net Worth by segment, excl. Group items 4 93% of credit bonds are investment grade rated 6 Economic net worth

Swiss Re Group | Company presentation | April 2019 3

Financial highlights

Overview and Group Strategy

Swiss Re Group | Company presentation | September 2018 4

Swiss Re Group at a glance

Swiss Re is a leading and highly diversified global re/insurer,

founded in Zurich (Switzerland) in 1863

• The financial strength1 of the Swiss Re Group is currently rated: Standard & Poor’s: AA- (stable); Moody’s Aa3 (stable); A.M. Best: A+ (stable)

• Swiss Re Group’s Swiss Solvency Test Ratio for 2019 is 251%

• AAA sustainability rating from MSCI (May 2018)

Reinsurance Corporate Solutions Life Capital

Offers traditional reinsurance products, The commercial insurance arm of the Group Manages closed and open life and health

insurance-based capital market instruments and provides risk transfer solutions to large insurance books and provides alternative

and risk management services globally and mid-sized corporations around the world access to the life and health risk pool, helping

through two segments – Property & Casualty to generate stable returns

and Life & Health

1 As at 26 March 2019

Swiss Re Group | Company presentation | April 2019 5

Swiss Re is well diversified across geographic regions and business

segments

Net premiums earned1 by segment Net premiums earned1 by region Economic Net Worth2 by segment

Life Capital Life Capital

Corporate 5% 12%

Solutions Asia

11% 21% Corporate P&C Re

Americas Solutions

P&C Re 38%

47% 9%

47%

L&H Re

37% EMEA L&H Re

32% 40%

Swiss Re benefits from geographic as well as business mix diversification and has the ability to reallocate capital to achieve

profitable growth

1 USD 34.5bn as at 31 December 2018; includes fee income from policyholders; does not reflect the exposure to HGMs through Principal Investments (PI)

2 Share of Swiss Re Group’s Economic Net Worth deployed across Business Units (excl. Group Items), 31 December 2018

Swiss Re Group | Company presentation | April 2019 6

Premium development by line of business and geography

Premiums earned and fee income by line of business Premiums earned and fee income by geography

(USD bn, CAGR in %) (USD bn, CAGR in %)

34.5 34.5

+5% +5%

14%

21%

25.4 25.4

28%

12%

20%

32%

30% 10%

42%

11%

27%

21%

47%

38%

26% 21%

2012 2018 2012 2018

Property Casualty Specialty Life Health Americas Europe (incl. middle East & Africa) Asia - Pacific

Swiss Re Group | Company presentation | April 2019 7

Our near-term priorities remain unchanged

Swiss Re’s strategic framework Near-term priorities Group financial targets

over-the-cycle

I

systematically allocate capital to risk pools / Large & tailored transactions

revenue streams Growth

through

Corporate Solutions RoE ≥

II III

systematic capital

allocation Life Capital

risk free

broaden optimise +700bps

and diversify client resources and High Growth Markets

base to increase access platforms to support

to risk capital allocation

Research & Development

Risk Knowledge ENW per

Technology

IV supporting capital

allocation

share growth

emphasise differentiation

People & Culture

+10% p.a.

We are a risk knowledge company that invests in risk pools

Swiss Re Group | Company presentation | April 2019 8

Based on three differentiation drivers, we have built leading insurance

businesses

Client Risk Capital

Access Knowledge Strength

Reinsurance Corporate Solutions Life Capital

P&C Reinsurance L&H Reinsurance

• Top 5-10 in Excess Layer market • Leading UK life & pension

• #1 global property • Top 2 global consolidator

reinsurer reinsurer • Growing in Primary Lead segment

• Leading L&H B2B2C platforms in

core markets

• #1 global reinsurer in High Growth Markets

Swiss Re Group | Company presentation | April 2019 9

We are benefiting from a more positive current environment and

promising long-term opportunities

Current market environment improved

Moderate

improvements in P&C …to benefit P&C Reinsurance and Corporate Solutions 5%

pricing…

overall market

Gradually increasing

growth

…to benefit the return profile of our investment portfolio

interest rates… expected1

Long-term opportunities remain

Risk pools continue

…we can access global risk pools through all Business Units

to grow…

9%

Opportunities in High

…we are the #1 global reinsurer in High Growth Markets

market growth

Growth Markets… expected in High

Growth Markets1

Protection gap still

…we develop innovative solutions to increase insurance coverage

expanding…

¹ Source: Swiss Re Institute; expected premium growth per annum in reinsurance in nominal USD terms over the next five years

Swiss Re Group | Company presentation | April 2019 10Focus areas of Annual Results 2018

• Group net income of USD 421m for FY 2018, despite the 2018 large natural catastrophes the Impacted by large

fourth highest year on sigma records in terms of large loss burden for the insurance industry losses and recent

• Group investment result impacted by change in US GAAP accounting guidance (ROI of 2.8%), change in US GAAP

while running yield remains stable at 2.9% accounting guidance

• Price quality improved by 1% and year-to-date Strong outcome of

• The treaty premium volume increased by 19% January renewals

• Life Capital transformation from closed book consolidator to dynamic primary B2B2C Life Capital in

business in motion transition

• 12% regular dividend per share increase to CHF 5.60 per share

Attractive capital

• New share buy-back programme1, in two tranches, consistent with Swiss Re’s capital management actions

management priorities

1 Subject to AGM 2019 approval; commencement of share repurchases subject to Board approval and legal and regulatory requirements being satisfied

Swiss Re Group | Company presentation | April 2019 11Second consecutive year with significantly higher than expected

large losses

Group ROE 700bps above 10yr US govt. bonds

Group Net Income Impact of change in US GAAP accounting guidance • After benign nat cat loss

years from 2012-2016 the

USD bn

insurance industry

4.6 14% experienced two elevated

4.4 loss years

4.2 12%

4.0 • Estimated claims from

10% multiple nat cat and man-

3.8

made disasters for Swiss Re

3.6

8% amounted to USD 3.0bn in

3.4 2018

6%

1.0

0.8 4%

0.6

0.4 2%

0.2

0.0 0%

2012 2013 2014 2015 2016 2017 2018

Swiss Re Group | Company presentation | April 2019 12Swiss Re’s strong economic earnings track record 2014-2018

EVM profit USD 608m EVM profit

Economic value is created if

new business avg. 2014 - 2018

total economic return generated USD 503m Total contribution to

for shareholders is above

expected total return

avg. 2014 - 2018

ENW

Represents total economic return

for taking risk (capital costs)

EVM profit generated for shareholders

USD 77m (economic earnings) and is the key

previous years’ element of gross excess capital

avg. 2014 - 2018

business generation

Capital cost release,

debt costs and tax

Includes base cost of capital USD 2 922m

EVM profit USD -183m (risk-free return and avg. 2014 - 2018

USD 3 425m

market risk premium)

investments avg. 2014 - 2018 avg. 2014 - 2018

and frictional capital costs

Total contribution to ENW forms the basis for Swiss Re’s attractive capital management actions

Swiss Re Group | Company presentation | April 2019 13Swiss Re’s total shareholder return is best tracked by ENW developments

ENW per share growth vs. total shareholder return1 ENW per share vs. share price development

130

120

300% Total return to shareholders

250% ENW per share growth 2 110

200% 100

150%

90

100%

50% 80

0%

70

ENW per share growth2 Total shareholder return Swiss Re share price (CHF) ENW per share (CHF)

EVM results represent the market relevant information aligned with total return to shareholders

1 Reflects share price development and dividends paid in USD; shown on a cumulative basis and indexed from 1 December 2005

2 Calculated as: (current-year closing ENW per share + current-year dividends per share) / (prior-year closing ENW per share + current-year opening balance sheet adjustments per share); shown on a cumulative basis and indexed

from 1 December 2005

Swiss Re Group | Company presentation | April 2019 14Swiss Re proposes attractive capital management actions

Regular dividend per share (CHF)

+3% +12%

12% regular dividend per share increase

5.00 5.60

4.85 Rebasing supported by long-term economic earnings and sustainable

capital generation

2017 2018 20191

Share buy-back programme (CHF bn) New share buy-back programme1

consistent with Swiss Re’s capital management priorities

• Up to CHF 1bn with no commencement pre-conditions

1.00

1.00 1.00

• Up to CHF 1bn contingent on 2019 Group excess capital development, e.g.

1.00 increase as a result of successful reduction of Swiss Re’s holding in ReAssure

2017/18 2018/19 2019/201 to below 50%

Very strong Group capitalisation, with Swiss Re’s Group SST ratio comfortably above the 220% target level

1 Subject to AGM 2019 approval; commencement of share repurchases subject to Board approval and legal and regulatory requirements being satisfied

Swiss Re Group | Company presentation | April 2019 15Swiss Re’s capital repatriation remains peer-leading

Dividends and share buy-back per share (CHF, CAGR in %)

+17%

9.20

8.65 8.90

8.00 8.25

7.90

7.50

1

4.20 3.30

4.40 3.40

3.30

4.15

4.00

1

3.00

5.60

4.60 4.85 5.00

3.85 4.25

3.50

2012 2013 2014 2015 2016 2017 2018 2019E

Ordinary dividends Special dividends and share repurchases

Swiss Re maintained its very strong capital position and is well positioned to respond to market opportunities while

continuing to focus on its capital management priorities

1 Share repurchase for 2019 includes share repurchase programme of up to CHF 1bn purchase value; subject to AGM 2019 approval; commencement of share repurchases subject to Board approval and legal and regulatory requirements being satisfied;

additional share repurchase programme of up to CHF 1bn contingent on 2019 Group excess capital development, e.g. increase as a result of successful reduction of Swiss Re’s holding in ReAssure to below 50%

Swiss Re Group | Company presentation | April 2019 16Value creation with increasing book value and paid dividends

Book value per share and accumulated paid dividends (CHF, CAGR in %)

+6% 137.99 138.57

131.92

119.62 121.79

30.35 35.20

18.50 40.20

25.75

90.76 93.26

3.00 10.50

107.64 103.37

101.12 96.04

87.76 91.72

82.76

2012 2013 2014 2015 2016 2017 2018

Book value per share Accumulated paid dividends

Swiss Re Group | Company presentation | April 2019 17Swiss Re maintains leadership in sustainability

Key actions in 2018

Close to

Responsible

100%

• Early mover in switching to ESG benchmarks in equity and credit markets

investing • USD 1.6bn of green bonds as of end FY 2018

assets considering ESG criteria

Sustainable

underwriting

•

•

Implemented thermal coal policy – 30% investment threshold extended to underwriting

Active in all renewable energy re/insurance and “lead market” for offshore wind risks

~3 400

wind and solar farms insured

Innovative

•

•

First county-level earthquake parametric cover in China

Largest sovereign-sponsored cat bond issued by the World Bank in Latin America

96

number of (sub-)sovereigns

solutions • Flood insurance for homeowners in Florida, based on proprietary flood model advised on climate risk resilience

Recognised • Externally recognised: AAA-rating in MSCI ESG assessment and top 3 in DJSI

leadership • Active participation in European and global expert groups

More public-private partnerships are crucial to strengthen resilience and mitigate effect of climate change

For further information on sustainability at Swiss Re please visit http://media.swissre.com/documents/Swiss_Re_ESG_Highlights.pdf

Swiss Re Group | Company presentation | April 2019 18R&D builds on our thought leadership position, bringing us

closer to the needs of our clients

How R&D drives value at Swiss Re: Drivers for underwriting

outperformance

Insurance “beta” ~450 FTE in

R&D improves top down Target Strategic

13 R&D teams

capital allocation leading to Liability Asset 50-60%

Portfolio Allocation

outperformance

Insurance “alpha”

R&D improves risk selection Product design

and further portfolio Product pricing

Underwriting

steering given allocation

criteria

>200 R&D

R&D provides services and Client services

initiatives

Thought-leadership

thought leadership enabling publications 40-50% ongoing (50%

higher pricing Curated data focusing on

technology)

Cost efficiency

R&D provides new ideas to

Business process

reduce the cost of generating disruption &

a given unit of revenue improvement

Swiss Re Group | Company presentation | April 2019 19Swiss Re’s tech strategy is embedded in our business strategy and

ensures effective innovation management

1 OUR CLIENTS OURSELVES 2

Increase our clients’ competitiveness Improve our value chain

Provide tools and solutions for clients’ value chains Apply technology to Swiss Re’s value chain

Examples: Magnum, Life Guide, CatNet, Liability Risk Drivers Examples: ATLAS, digital claims, document intelligence

Swiss Re

4 OUR DATA tech strategy OUR EXPOSURE 3

Harvest full potential of data Get closer to risk

Build up competitive advantage from proprietary data Seek access to risk pools through tech platforms

Example: Stargate platform Examples: iptiQ, elipsLife, dynamic parametric pricing platform, Pulse

Our tech strategy is implemented with a combination of in-house developments and strategic partnerships

Swiss Re Group | Company presentation | April 2019 20Swiss Re outperforms its peers with higher margins

Peer-leading margins • The differentiation approach has

enabled Swiss Re to generate higher

US GAAP net operating margins average 2012-18 margins and outperform

12% 7% • Swiss Re outperformed peers on

average by 6%pts since 2012, driven

by underwriting performance (risk

selection, capital allocation and

differentiation)

Swiss Re Group Reinsurance market ¹

Investment Underwriting Operating expenses

Swiss Re is leading insurance business that represents a highly rewarding combination for shareholders

¹ Based on weighted average of Munich Re, Hannover Re, SCOR and RGA

Swiss Re Group | Company presentation | April 2019 21We are committed to our over-the-cycle Group financial targets

Group return on equity Group ENW per share growth2

24.6%

13.7% 13.7% 17.0%

13.4%

10.5% 10.6%

11.0%

9.6% 10.8%

9.4% 9.6%

8.8% 9.2% 9.4% 9.4% Rf +

10% 10% 10% 10% 10% 10% 10% 10%

700 7.2%

bps1

5.4%

4.4%

1.0% 1.4%

2012 2013 2014 2015 2016 2017 2018 Over- 2012 2013 2014 2015 2016 2017 2018 Over-

the-cycle the-cycle

target target

actual 700 bps above 10y US Govt. bonds actual target

1 700 bps above 10y US Govt. bonds. Management to monitor a basket of rates reflecting Swiss Re’s business mix

2 The 10% ENW per share growth target is calculated as: (current-year closing ENW per share + current-year dividends per share) / (prior-year closing ENW per share + current-year opening balance sheet adjustments per share)

Swiss Re Group | Company presentation | April 2019 22Financial highlights

Capital Management

Swiss Re Group | Company presentation | September 2018 23We remain focused on our capital management priorities

I II

Swiss Re’s capital management priorities remain unchanged Group SST ratio

SST 18 SST 19 USD 7.9bn2

I. Ensure superior capitalisation at all times and maximise financial 269% 251% ordinary dividend

(FY 14 to FY 18)

flexibility Rating

Payout

1

AA-/Aa3/A+ ratio 46%

II. Grow the regular dividend with long-term earnings, and at a

minimum maintain it

Capital management priorities

IV III

III. Deploy capital for business growth where it meets our strategy and

profitability requirements USD 6.2bn3

special dividend &

buy-back

(FY 14 to FY 18)

IV. Repatriate further excess capital to shareholders

Extraordinary

Payout ratio 36%1 Business Acquisitions

reinvestments

1 Payout ratio

calculated as capital repatriation over total contribution to ENW; assumes AGM approval of the proposed ordinary dividend of CHF 5.60 per share and the unconditional share buy-back of up to CHF 1bn

2 Includes AGM 2019 proposal for ordinary dividend of CHF 5.60 per share

3 Includes AGM 2019 proposal for unconditional share buy-back programme of up to CHF 1bn

Swiss Re Group | Company presentation | April 2019 24Group capital position remains very strong, even after significant large

losses and continued peer-leading capital repatriation to shareholders

SST ratio development (USD bn, %)

• Group SST ratio remains very strong and

comfortably above the 220% target level

269%

261% 262%

80.0

251% • The SST ratio decreases by 18%pts mainly

due to lower risk-bearing capital reflecting

70.0

SST target

capitalisation1

60.0 capital repatriation, redemption of a

(220%) subordinated instrument and depressed

46.3

44.8 46.1

financial markets at year-end 2018. These

50.0

40.6

40.0 effects are partly offset by positive

30.0

contributions from underwriting activities

20.0 17.2 17.6 17.2 16.2 • Increase in MVM mainly driven by growth in

Asia

10.0

• Swiss Reinsurance Company Ltd solo ratio

also remains strong at 218% with USD

0

2016 2017 2018 2019

USD 5.3bn MVM USD 5.2bn MVM USD 5.9bn MVM USD 7.0bn MVM 14.3bn excess capital above the 100%

regulatory requirement

SST available capital SST economic target capital

Group SST ratio calculation

SST available capital SST risk-bearing capital - MVM2

SST economic target capital

= SST target capital - MVM2

1 SST 220% target capitalisation was only introduced in 2017

2 MVM = Market Value Margin = Minimum cost of holding capital after the one-year SST period until the end of a potential run-off period

Swiss Re Group | Company presentation | April 2019 25Swiss Re’s capital strength remains resilient to market movements

Group SST sensitivities

• Swiss Re uses a central proprietary risk model to

Resulting estimated Group SST ratio 2019 measure capital requirements, define risk

tolerance, risk limits and assess stress test

impacts

Equity markets (-25%) 248%

• Swiss Re remains strongly capitalised under strict

Equity markets (+25%) 254% risk limits curtailing the impact of market moves

on the Group SST ratio

Interest rates (-50bps) 239%

Interest rates (+50bps) 261%

Credit spreads (-50bps) 259%

Credit spreads (+50bps) 244%

Real estate values (-25%) 245%

Real estate values (+25%) 257%

220% 251%

Group SST target Group SST

capitalisation 2019

Swiss Re Group | Company presentation | April 2019 26Swiss Re maintains a leading capital position in the reinsurance sector and

industry

Group SST to Solvency II walk1

>280%

311%

251%

239%

210%

Group SST Risk measure Modelling differences Valuation Eligibility of capital Deferred taxes Group Solvency II Average of Average of

ratio 2019 (1-year risk) (discounting) ratio reinsurers2 insurers3

SST and Solvency II are both comprehensive economic and risk-based solvency regimes

Due to important differences, Solvency II equivalent ratio is significantly higher

For 2019, our comparable Group Solvency II ratio is estimated to be >30%pts higher than our Group SST ratio

1 Comparison was produced on a best effort basis using Swiss Re's SST calculation for 2019; For more details on differences between SST and Solvency II please refer to our “SST vs. Solvency II – comparison analysis” published on our website

(http://media.swissre.com/documents/2016_sst_presentation.pdf). Please note that the difference from “capital cost recognition” has been eliminated in 2017 with FINMA's change in SST ratio definition. Differences between SST and Solvency II also

explained in the booklet “Measuring economic performance & solvency at Swiss Re” published on our webpage.

2 Average of Munich Re, Hannover Re, SCOR

3 Average of Allianz, Aviva, Axa, Generali

Swiss Re Group | Company presentation | April 2019 27Strong solvency capital generation over the last five years

Swiss Re’s solvency capital generation – five year aggregated view from Group SST 2014 to 2019

More details on following slides

17.1 Capital management

-2.8 12.8

-1.5

-3.2

-14.0

-4.4

Economic earnings Capital deployment Other items (incl. fx)2 Net solvency Change in Capital repatriation3 Change in

(Total contribution (capital allocation)1 capital generation supplementary capital excess capital

to ENW)

yearly average

CHF 11 CHF 8 CHF 9

per share

• Solid economic earnings (USD 3.4bn on average) drove Swiss Re’s strong solvency capital generation over the last five years (USD 2.6bn net solvency capital

generation on average per year or CHF 8 yearly average per share)

• In line with its target capital structure, Swiss Re reduced its traditional funded subordinated debt instruments by USD 3.2bn and at the same time strengthened its

financial flexibility through the issuance of USD 2.7bn of pre-funded subordinated debt facilities at Group level (not counting as SST supplementary capital until

drawn)

• Over the period, Swiss Re implemented peer-leading capital repatriation of USD 14bn in total or USD 2.8bn per year, on average

1 Including model changes

2 SST available capital: includes change in other EVM items (including foreign exchange impacts on ENW) and change in SST valuation differences with EVM on a best effort basis; SST economic target capital: includes foreign

exchange, interest rate and other impacts on Swiss Re’s economic target capital on a best effort basis

3 Includes the sum of paid (2015 – 2018) and proposed 2019 dividends and public share buy-backs (a pro-rata share of the 2019 share buy-back programme with no commencement pre-conditions of CHF 0.9bn is used)

Swiss Re Group | Company presentation | April 2019 28Swiss Re’s target capital structure and financial flexibility is supported by

the Group’s strong funding platforms

Implementation and maintenance of target capital structure

USD bn Established funding platforms in all Business Units to fund capital & liquidity requirements

Corporate Life Group

Reinsurance Outlook

YE 2012 – YE 20181 Solutions Capital (SRL)

Continued focus on optimising capital structure and

Subordinated debt -2.02 +0.5

cost of capital

Continued focus on innovative, cost efficient

Contingent capital -0.23 +3.24 contingent capital instruments at Group Holding level

Support business growth in Life Capital in line with

Senior debt -6.9 +1.5

leverage targets

Letters of credit -4.5 In line with Reinsurance requirements

• SST supplementary capital includes traditional funded subordinated debt and funded contingent capital instruments. In line with Swiss Re’s target capital structure,

Swiss Re has reduced its traditional funded subordinated debt instruments by USD 1.5bn between YE 2012 and YE 2018

• At the same time, the Group has significantly strengthened its financial flexibility through senior debt deleveraging and the issuance of USD 1.0bn contingent capital

instruments at the Reinsurance level, a USD 0.5bn contingent capital instrument at the Group level (6-year non-dilutive senior exchangeable bond with anytime issuer

stock settlement) and USD 2.7bn pre-funded subordinated debt facilities at Group level (not counting as SST supplementary capital until drawn)

1 Change in supplementary capital is calculated using YE 2012 and YE 2018 figures

2 EUR 750m and USD 1bn subordinated fixed rate reset set-up callable notes issued in March and April 2019, respectively (not included in the table)

3 Reflects the issuance of USD 1.0bn in 2013 and redemption of the contingent capital instruments classified as equity issued in 2012 (USD 1.1bn)

4 Reflects USD 2.7bn pre-funded subordinated debt facilities (currently fully undrawn), and USD 0.5bn senior non-dilutive exchangeable bond with anytime issuer stock settlement

Swiss Re Group | Company presentation | April 2019 29Peer-leading capital repatriation

USD bn in year paid Ordinary dividends Special dividends and share buy-backs

USD 7.9bn USD 6.1bn

1.5 1.6 1.6 1.6 1.7 1.5 1.3

1.1 1.1 1.0

2015 2016 2017 2018 2019E2 2015 2016 2017 2018 2019E2

Per share in CHF 4.25 4.60 4.85 5.00 5.60 4.40 3.30 3.40 3.80 3.35

14.0 Swiss Re

Capital repatriation P&C Reinsurance L&H Reinsurance Corporate Solutions Life Capital

Group SST 2014-19¹

2.7 2.5

2.0

1.3 1.1 1.1

0.3 0.4 0.7 0.7 0.3 0.4 0.4

0.2 0.2 0.1

2015 2016 2017 2018 2015 2016 2017 2018 2015 2016 2017 2018 2015 2016 2017 2018

Received capital contribution Received capital contribution

of USD 1bn in 2017 of USD 1.6bn in 2016 for the

acquisition of Guardian

1 Capital repatriation includes dividends and share buy-backs paid in 2015-18 and projected for 2019

2 Capital repatriation includes AGM 2019 proposal for ordinary dividend and new unconditional share buy-back programme of up to CHF 1bn, of which a pro-rata share of CHF 0.9bn is used for SST

Swiss Re Group | Company presentation | April 2019 30Financial highlights

P&C and L&H Reinsurance

Swiss Re Group | Company presentation | September 2018 31We seek to benefit from a more positive environment and promising long-

term opportunities in the reinsurance market

Market environment improved

Moderate improvements in P&C reinsurance pricing developments

5%

Gradually increasing interest rates benefit our long tail lines in Life and Casualty overall market

growth1

Global economic growth increases demand in and from primary markets

Long-term opportunities remain

#1 global reinsurer in High Growth Markets, well positioned to take advantage of

projected growth

Mortality

Growth from innovative solutions to address the global protection gap protection gap

> USD 270 billion

As a knowledge company we benefit from the growing importance of R&D and technology

1 Source: Swiss Re Institute, expected growth per annum in reinsurance in nominal USD terms over the next five years

Swiss Re Group | Company presentation | April 2019 32Differentiation is at the heart of what we do

Core Transactions Solutions

Differentiation

Simplify and drive Add value to clients’

Deliver innovative deals by

efficiencies in our original business by

combining our knowledge

traditional business providing tech enabled

and capital

solutions

We access risk pools through the three pillars of our strategy

Swiss Re Group | Company presentation | April 2019 33We leverage technology in solutions to add value to our clients’ original

business and value chain

Selected examples of commercialised solutions in P&C and L&H Reinsurance

Pilot / Proof of concept

With clients and partners

Automotive Parametric Smart SwiftRe® Magnum

Solutions Homes

Development

Build resources and

infrastructures

Commercialisation Customer

Bring to market viable Liability Claims

Life Guide Retention

solutions Analytics Deep Dive

Management

Our innovation mind-set allows us to focus on commercialisation of proven solutions

Swiss Re Group | Company presentation | April 2019 34Swiss Re’s reinsurance client franchise represents the biggest source of

our competitive advantage

We have strong direct relationships with our customers… Direct relationships drive our access to large & tailored

transactions

P&C Reinsurance L&H Reinsurance EVM profit - new business (USD m)

% of premiums from non-

47% intermediated business, 96% CAGR 16%

FY 2018 700

600

500

…with distinct client interactions

400

Client example

300

200

100

Americas

APAC 0

EMEA 2010 2011 2012 2013 2014 2015 2016 2017 2018

Swiss Re

P&C Reinsurance L&H Reinsurance

Swiss Re Group | Company presentation | April 2019 35We have significantly grown and diversified our portfolio

Portfolio developments 2010-18

EVM premium (USD bn) Overall portfolio

Americas EMEA Asia CAGR of 7% from

CAGR 21% 2010 to 2018

15.4

CAGR 7%

12.6 CAGR 4%

3% 43%

10.9

34% 16%

Balanced global portfolios

7.4 7.8

3% 22%

1% 12%

17% 31%

15%

50% 36%

21%

28% 3.3 4%

3% 18%

18% 24% 27%

9% 12% 11%

16% 10% 7% 9% 5%

12%

15% 16% 12%

20%

14% 6% Increased diversification

2010 2018 2010 2018 2010 2018 of product lines

Property Nat Cat Casualty Specialty Life Health

Swiss Re Group | Company presentation | April 2019 36Net premiums earned Net operating margin1 (%) Combined ratio (%)

111.5

104.0

+5.6pts

4.3 93.5

2.9

USD 16.1bn

83.8 83.7

80.7 85.7

8.9 7.8

2012 2013 2014 2015 2016 2017 2018

in 2018

-3.9

-6.4

• Net impact of large nat cat events in 2018 5.0%pts above

USD 16.7bn

in 2017

-6.3 expectations. Favourable prior-year development positively

impacted the combined ratio by 0.9%pts

-1.3

2017 2018

Underwriting Investment Operating expenses

Net income (USD m, LHS), Return on equity (%, RHS)

• Decrease of net premiums earned driven by a reduction of Chinese quota shares and 4 000 26.7 26.0 26.7 30

22.4

US Casualty, partially offset by large transactions in Asia and the US 3 000

25

16.4 20

• Underwriting margin impacted by several large losses in both periods 2 000 15

3 228 3 564

2 990 3 008

• Decrease in investment margin driven by market value losses on equity securities 1 000 2 100 10

3.7

and lower realised gains from fixed income securities 370

5

0

-413 0

• Increase in the expense margin driven by the decrease in premiums earned -3.5

-1 000 -5

2012 2013 2014 2015 2016 2017 2018

Net income Return on equity

1 Net operating margin = EBIT / total revenues Swiss Re Group | Company presentation | April 2019 37P&C Reinsurance strategy in action

Portfolio split by region and line of business CORE

(% of net earned premium, USD bn) US GAAP operating expenses (USD m)

-3.9%

• Leveraging technology to achieve efficiency

Americas 1 159 1 114 across Swiss Re’s value chain

22%

EMEA

2017 2018

Asia

48%

SOLUTIONS – selected examples

30% ADAS risk score Data analytics

Working with OEM partners to Addressing strategic questions

improve the risk assessment of through a combination of the latest

increasingly automated vehicles data science methods with

Property bespoke advisory

6% 3% Liability

5% 3% 3% Motor TRANSACTIONS

37%

A&H Economic profit (USD m)

Marine

200 +5%

23% Engineering • >130 transactions closed in 2018

Credit 100 • Transactions contributed ~23% to

20% Other specialty economic profit in 2018

0

2017 2018

Swiss Re Group | Company presentation | April 2019 38Net premiums earned Net operating margin1 (%) Running yield and ROI (%)

3.8

3.5 3.5 3.4 3.3 3.4

3.2

-3.7pts

13.1 4.7

4.1 4.3

3.4 3.6 3.7

3.2

USD 12.7bn

4.8 9.4

3.3

in 2018 2012 2013 2014 2015 2016 2017 2018

13.7 Running yield ROI

11.4

USD 11.9bn

in 2017

-5.4 -5.3

• Slightly increasing running yield but lower ROI as prior period

positively impacted by significant net realised gains

2017 2018

Underwriting Investment Operating expenses

Net income (USD m, LHS), Return on equity (%, RHS)

• Increase in premiums earned reflected growth across all markets including large 1 500

16.2 15.3

20

transactions in Asia, intra-group retrocession agreements and favourable fx 1 000

12.8

11.1 15

8.9

10

• Decrease in underwriting margin due to unfavourable mortality experience in the 500

6.4

968 1 092

739 807 761

US, partially offset by favourable contribution from transactions 420 5

0

0

• Lower investment margin as prior period was positively impacted by significant net -462

-500

realised gains from sales of equity securities -5

-7.9

-1 000 -10

2012 2013 2014 2015 2016 2017 2018

Net income Return on equity

1 Net operating margin = EBIT / (total revenues – net investment result unit linked & with profit) Swiss Re Group | Company presentation | April 2019 39L&H Reinsurance strategy in action

Portfolio split by region and line of business CORE

(% of net earned premium, USD bn) US GAAP operating expenses (USD m)

0.5%

• Despite strong growth in the last years,

754 758 expense base remained stable

Americas

26% EMEA

2017 2018

43% Asia

SOLUTIONS – selected examples

Magnum Behavioural economics

30% Used by >60 insurers and Creating improvements across the

available in 26 countries; processes insurance value chain by helping to

more than 12m applications per enhance the way insurers connect

year; >1.3m devices in China with customers

10%

6% Mortality

TRANSACTIONS

Disability

11% Economic profit (USD m) • 24 transactions closed in 2018

Critical Illness

• Transactions contributed ~38% to

62% Medical 600 +86%

11% economic profit in 2018

Other 400

• Large and tailored deals in Asia drove

200

transactional growth in 2018

0

2017 2018

Swiss Re Group | Company presentation | April 2019 40Financial highlights

Corporate Solutions

Swiss Re Group | Company presentation | September 2018 412018 Corporate Solutions result impacted by large man-made and nat cat

losses

Net premiums earned Net operating margin1 (%) Combined ratio (%)

133.4

+12.4%pts 117.5

1.9 101.1

7.4 5.4 96.2 95.1 93.0 93.2

USD 3.9bn

in 2018

-11.7

-18.4 2012 2013 2014 2015 2016 2017 2018

-19.2 -11.1

• Profitability continues to be impacted by underwriting

USD 3.7bn

in 2017

-23.5

performance, driven by an increase in severity and frequency of

large man-made losses, and generally depressed rate levels, as

2017 2018 well as unfavourable prior-year development

Underwriting Investment Operating expenses

Net income (USD m, LHS), Return on equity (%, RHS)

• Premiums earned increased by 7.5% driven by growth in Primary Lead which more 400 9.6 12.5

15.5 20

than offset active pruning in US General Liability portfolio 7.4 6.0

200 319 357 10

196 279

• Underwriting margin improved driven by lower nat cat losses, partially offset by an 0

135

0

increase in severity and frequency of large man-made losses

-200 -405 -10

• Investment margin decreased due to lower realised gains from equities, partially -400 -741 -20

offset by increasing yields and a higher invested asset base -19.4

-600 -32.2 -30

• Operating expense margin improved driven by strong growth and continued focus -800 -40

on productivity measures 2012 2013 2014 2015 2016 2017 2018

Net income Return on equity

1 Net operating margin = EBIT / total revenues Swiss Re Group | Company presentation | April 2019 42Addressing Corporate Solutions underperformance

Drivers of underperformance Actions taken

• Difficult market environment: man- • Portfolio pruning started in 2017,

made losses above expectations continued in 2018 and

and price improvements not yet intensifying in 2019

sufficient after years of decline

• Continued focus on productivity

• Higher net exposures led to large Business update to

single event losses • Higher prices already be provided with

• Unfavourable PYD related to

experienced and expecting more Half-year 2019

structure1 and business mix Results

• Reinsurance programme

(Excess Layers and overweight

adjusted but to be revisited

US)

• High cost ratio because of on- • New experienced CEO started in

going investments and continued March 2019

lack of scale

Progress has been made and we will continue to address Corporate Solutions underperformance

Corporate Solutions remains core to Swiss Re and we continue to see long-term attractive potential in the business

1: Positive development on Corporate Solutions historical loss reserves remaining in Reinsurance

Swiss Re Group | Company presentation | April 2019 43Corporate Solutions remains focused on key priorities

Performance improvement actions Increase productivity Primary Lead

• US General Liability pruning actions started 18 • A combination of process improvements, cost • Extension of own domestic and international

months ago; time lag for improvements to be saving measures, use of technology and strong Primary Lead producing capabilities to 19 and 9

reflected in financials growth led to a lower operating expense ratio countries respectively

• Additional improvement actions initiated for less • Maintain focus on productivity to finance • Global network coverage for international programs

strategic segments which are further minimised or continuing investment into Primary Lead > 120 countries

partially exited capabilities

• Pursue sizable rate increases on underperforming

sub-segments and across the board

US General Liability repositioning / pruning Operating expense ratio (%)

(Gross premiums written)

22%

-30% 21%

20% 21.7

20.8

19%

19.4

18%

2016 2017 2018 2016 2017 2018

Own offices Network partners

Positive price momentum expected to continue

Corporate Solutions will continue to take targeted actions addressing business performance issues and price deficiencies

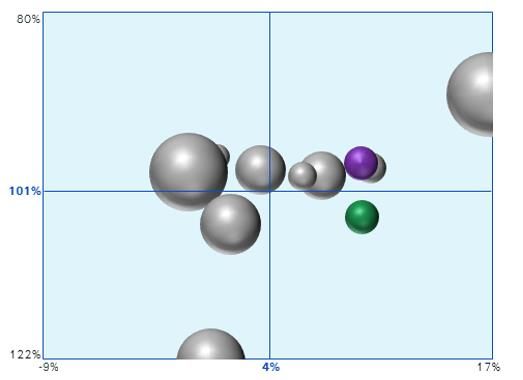

Swiss Re Group | Company presentation | April 2019 44Corporate Solutions has shown disciplined performance within its peer-

group

2012 – 2017 Average 2012 – 2018

2012 2013 2014

Combined ratio

Combined ratio

2015 2016 2017

Gross premiums growth

Corporate Solutions (Combined Ratio incl. Total financial contribution - TFC)

Corporate Solutions (Combined Ratio published)

Gross premiums growth Peers

Source: Swiss Re Institute

Note: Quadrants are determined based on average combined ratio and gross premiums compound annual growth rate (CAGR); premium growth & bubble size are in USD; Size of bubbles corresponds to GPW; From 2011-2014: Unchanged set of 8 peers,

2015: peer group reduced to 7 due to M&A. 2016: 10 peers, 3 players added to ensure comparison is representative of market

Swiss Re Group | Company presentation | April 2019 45Financial

Life Capitalhighlights

Swiss Re Group | Company presentation | September 2018 46UK life & pension closed book Group protection solutions through White-labelled individual protection products

Business consolidator intermediaries through distributors

Protection, annuities, unit-linked

Products insurance

Group life, disability, income protection Individual life, health and non-life protection

Pension providers, pension funds, corporates

Clients Insurers, banks, PE firms

and affinity groups

Distribution partners

UK Closed Book Market Reserves Group L&H Market GPW Individual L&H P&C personal lines

~ USD 440bn ~ USD 150bn ~ USD

~ USD

650bn

920bn

~

~ USD

USD 300bn

300bn

14% 1%ReAssure developments in 2018… …complemented by open book evolution 2019 outlook

Focus on

# new policies ReAssure IPO preparation

# iptiQ written in iptiQ

elipsLife premium distribution 120k

volume (USD m) partners

Enhancing access

19

450

Exceptional GCG: USD 818m

in 2018

to risk pools

with iptiQ platform

MS&AD stake increased to 25% 300

5

60k

IPO preparations continued 150 in 2016

2 Scale-up of

New Chairman and new CEO appointed 0

2009 2014 2018

in 2014 0

2014 2016 2018

elipsLife platform

Swiss Re Group | Company presentation | April 2019 48Exceptional Life Capital GCG; open book growth in line with expectations

Gross cash generation (USD m) Open book - Gross premiums written (USD m)

1196

998 1 567

945

818 CAGR 30%

721

1 039

521 543 868

709

2012 2013 2014 2015 2016 2017 2018 2015 2016 2017 2018

• Exceptional gross cash generation (GCG) driven by strong underlying • Gross premiums written increase reflects significant growth in open

emerging surplus, the sale proceeds from the initial 5% stake in book businesses:

ReAssure acquired by MS&AD and the finalisation of the 2017 Solvency

II position – iptiQ L&H increase driven by a large medex transaction

– elipsLife increase reflects strong growth on core as well as

• GCG 2016-2018 of USD 2.5bn at top end of USD 2.3-2.5bn target

medex business

range (significantly outperforming original target of USD 1.4-1.7bn)

Swiss Re Group | Company presentation | April 2019 49Life Capital open book businesses continue to grow

2016 2018

Weekly

policies sold1 545

2 755

~ 5x

# of Expansion of access to

distribution

partners

5 19 ~ 4x attractive risk pools

# of countries 5 7 +2

GPW2

(USD m) 247

412

+ 67%

Ambition to continue

# of clients < 8 000 ~ 12 000 + 50% growing at an accelerated

pace

# of countries 2 5 +3

1 Weekly policies sold in Q4 2016 and Q4 2018, respectively Swiss Re Group | Company presentation | April 2019 50

2 Reflects core business, i.e. excludes medex businessFinancial highlights

Asset Management

Swiss Re Group | Company presentation | September 2018 51Swiss Re’s investment portfolio

Other investments (incl. policy

Cash and cash equivalents

loans)

Mortgages and other 4%

5%

End loans Short-term investments

4% 4%

USD bn FY 2018

Equities

Balance sheet values 153.3 5%

Unit-linked investments -25.9 Government bonds

41%

With-profit business -4.8

Assets for own account 122.6

(on balance sheet only) Credit bonds

37%

Corporate Life End End

USD bn P&C Re L&H Re Solutions Capital Group items Consolidation FY 2018 FY 2017

Cash and cash equivalents 1.7 1.7 0.8 0.4 0.2 - 4.8 4.9

Short-term investments 2.5 1.2 0.5 1.2 - - 5.4 4.8

Government bonds 25.8 13.1 5.5 6.5 - - 50.9 54.7

Credit bonds 10.2 16.1 2.7 16.1 - - 45.1 47.1

Equities1 3.2 0.7 0.2 0.1 2.1 - 6.3 7.1

Mortgages and other loans 7.5 1.8 - 1.8 4.3 (10.9) 4.5 4.0

Other investments (incl. policy loans) 4.4 1.3 0.1 0.8 0.4 (1.4) 5.6 9.1

Total 55.3 35.9 9.8 26.9 7.0 (12.3) 122.6 131.7

1 Includes equity securities, private equity and Principal Investments Swiss Re Group | Company presentation | April 2019 52Return on investments (ROI) Investment portfolio positioning (USD bn) Net investment income (USD m, LHS)

Running yield (%, RHS)

140

128.0

122.6

120 9.8 3.2 3.2 3.3

10.2 4 000 3.5

2.8% 3.3%1

3.0 2.9 2.9 2.9

100 3.0

52.9 49.3 3 000

80 2.5

in 2018 2.0

60 2 000

3 610 3 386 3 396 1.5

3 178 3 099 3 132

40 53.2 51.1 2 860

1.0

1 000

20

3.9%

0.5

11.2 11.0

0 0.9 1.0 0 0.0

2012 2013 2014 2015 2016 2017 2018

2017 2018

in 2017 Cash and short-term investments

Net investment income Running yield

Government bonds

Credit investments

Equities and alternatives (incl. Principal Investments)

Other

• ROI driven by net investment • No significant net changes in the asset allocation • Net investment income of USD 3.4bn above prior year,

income, partially offset by market reflecting the impact of rising yields as well as additional

value losses across equities and • Net purchases and market value gains on direct income from alternative investments

alternative investments real estate largely offset by market value losses

on equity securities • Group fixed income running yield in line with prior year

• Excluding the estimated impact

of the change in US GAAP • Impairments remain low (USD 9m), reflecting a

accounting guidance, the ROI disciplined investment approach

would have amounted to 3.3%

1 ROI excluding the estimated impact of the new US GAAP accounting guidance on recognition and measurement of financial instruments Swiss Re Group | Company presentation | April 2019 53High quality portfolio drives the Group’s sustainable investment result

Credit bonds: USD 45.1bn Fixed income impairment trend

Below investment grade credit bonds represent approximately

half of peer average of 9%

USD m bps

4%

3%

60

Investment grade rated Typical default rate assumption (Single A) ~13bps 15

Non-investment grade rated

37

Not rated1 10

30

93% 22

3 15 5

2

1 5

Credit spread sensitivity on shareholders’ equity and ENW2 1

0 0

2015 2016 2017 2018

USD -1.9bn USD +2.0bn

Credit spreads +/-50bps

Fixed income impairments (USD m, LHS) ROI impact (bps, RHS)

High quality portfolio drives stable running yield of 2.9% for Impairment trend reflects significant reduction of high yield

2018 (quarterly running yield increased from 2.8% to 3.0% exposure in 2016

during 2018)

1 Determination of credit quality of non-rated securities, which includes catastrophe bonds and infrastructure loans, based on Swiss Re analysis

2 Sensitivity on both shareholders’ equity and economic net worth assumed to take effect on 31 December 2018; sensitivities are comparable but not exact

Swiss Re Group | Company presentation | April 2019 54Fixed income securities

Government Credit

USD m bonds bonds

End

FY 2017 54 658 47 128 • Decrease in government bonds driven by foreign

End exchange impacts as well as net sales and market value

FY 2018 50 876 45 076

losses stemming from rising interest rates across the US

and UK

• Credit bonds include corporate bonds (USD 40.8bn)

and securitised products (USD 4.3bn)

3%

4%

2%

14%

• Decrease in credit bonds driven by foreign exchange

3% 8%

impacts as well as market value losses stemming from

3%

40% 8% rising interest rates and wider credit spreads, partially

3% 48%

4%

offset by net purchases

6%

6% 29%

19%

United States United Kingdom

Germany Canada

France Australia

Italy China BBB A AAA AAEquities and alternative investments

Equity securities Exchange-traded funds

by sector Non-Cyclical Consumer Goods

End End Financials

1% 1%

USD m FY 2017 FY 2018 3%2% 1%

6% Information Technology

Equity securities 3 326 2 695 6% Cyclical Services

General Industrials

Private equity 1 382 1 463 7% 48%

Basic Industries

Hedge funds 359 327 12% Cyclical Consumer Goods

Non-Cyclical Services

Real estate 4 091 4 430 13% Resources

Principal Investments 2 422 2 109 Utilities

Real estate

Equity securities 539 341 by geography

3%

13% Switzerland

Private equity 1 883 1 768 US

Germany

Total market value 11 580 11 024 41% Other Direct

17% Indirect

• Decrease in equity securities mainly driven by net sales and market value losses

26%

• Increase in real estate driven by net purchases and market value gains Principal Investments

by sector

HGM Insurance

• Decrease in Principal Investments reflects market value losses, mainly driven by New 8% 5% PE Funds

China Life

Developed Market Insurance

15% Non Insurance

72%

Swiss Re Group | Company presentation | April 2019 56Swiss Re’s approach to responsible investing: we consistently integrate

ESG criteria across all asset classes

Switch to broad-based ESG benchmarks

Enhancement

focusing on higher ESG-rated investments

Focus on themes and create related

Inclusion mandates, such as green bonds,

renewable or social infrastructure

Exclusions based on the internal

Exclusion Sustainable Risk Framework. Avoid

investments related to thermal coal and tar sands

Governance • Responsible Investment Policy Signatories to • Principles for Responsible Investment (PRI)

• Voting Framework • ICMA Green Bond Principles

• Sustainability Risk Framework

Systematic integration of ESG criteria into investment process and portfolio

Close to 100% assets invested considering ESG criteria

Swiss Re Group | Company presentation | April 2019 57Financial highlights& Protection Gap

Global Re/Insurance

Swiss Re Group | Company presentation | September 2018 58Global cat losses totaled USD 165 billion in 2018, and 49% was uninsured

Swiss Re Group | Company presentation | April 2019 59Disaster losses still mostly uninsured

500

450

400

350 Economic

losses =

300

insured +

250 uninsured

losses

200

150

100

50

0

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2018

Insured losses Not insured 10-year moving average insured losses 10-year moving average total economic losses

Source: Swiss Re Institute

Swiss Re Group | Company presentation | April 2019 60Insured losses in 2018: USD 85 billion

Insured losses, 1970-2018 (USD bn at 2018 prices)

Hurricanes

160 Japan, NZ

Harvey, Irma,

earthquakes,

Hurricanes

Thailand flood

140 Katrina, Rita, Wilma

120

100 Camp Fire,

Hurricanes Ivan, Hurricane Typhoon Jebi

Charley, Frances Sandy

80

Winter Storm Lothar Hurricanes

Ike, Gustav

60

Hurricane Andrew WTC

40

20

0

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2018

Earthquake/tsunami Weather-related catastrophes Man-made disasters

Source: Swiss Re Institute

Swiss Re Group | Company presentation | April 2019 61Direct premiums as a % of GDP, 2017

United States • Swiss Re’s developed insurance

4% Canada “S-Curve” illustrates the various

Switzerland

Average advanced markets stages of insurance penetration

Germany • Insurance penetration rises most

sharply in middle-income

3% Spain

countries

South Africa

• With our focus on High Growth

Portugal United Kingdom Markets, Swiss Re is well

Italy

2% Morocco positioned to benefit from this

China trend

Brazil

Average emerging markets

Kenya

Mozambique Greece Ireland

1% India Russia

Cote d Ivoire

Ghana Angola

Ethiopia Egypt

Nigeria

0%

0.1 1 10 100

GDP per capita, 1000 USD

Source: Swiss Re Institute, S-Curve in non-life insurance 2017

Swiss Re Group | Company presentation | April 2019 62Lines of business1 (premium equivalents)

Property Cat Property Non-Cat

Premium

~USD 155 bn ~USD 80 bn potential

> USD 500

billion

and growing

Agro Mortality

~USD 30 bn ~USD 270 bn

Source: Swiss Re Institute

1 Excluding Morbidity, Other P&C and Emerging Risks; Protection Gap for Property Cat, Property Non-Cat, Agro and Mortality estimated at ~500bn vs Premium insured of ~900bn

Swiss Re Group | Company presentation | April 2019 63How to close the gap?

Economic Solution type Description

loss Foregone revenues

Damaged public Risk transfer solutions

physical assets

for (sub)sovereigns to cover

Macro their direct or indirect costs

gap Clean up costs

Emergency relief

Damaged Insurance schemes and pools

uninsured

Insured

private assets

Pooling to increase insurance penetration;

loss distribution and simplified products

Livelihood assistance, Simplified products distributed

rehabilitation of the poor Micro via aggregators such as

MFIs1, NGOs, and corporates

1 Monetary Financial Institutions

Swiss Re Group | Company presentation | April 2019 64Swiss Re Public Sector Solutions enables the Group to broaden our client

base and address the protection gap

Florida United Kingdom Turkey Bangladesh

United States Hurricane risk Flood risk Earthquake pool Flood insurance

• First dedicated public sector Flood risk

team in the reinsurance

Caribbean

industry Hurricane, earthquake Heilongjiang

• More than 400 transactions and excess rainfall risk Multiperil disaster risk

since 2011 Louisiana Beijing

Hurricane risk Agricultural risk

• Develop insurance,

reinsurance and capital California/Utah Vietnam

markets solutions on all Earthquake risk Agriculture yield cover

perils (natural disasters, Guangdong

weather risks, pandemics Typhoon/rainfall

and other health topics, Philippines

infrastructure, etc.) Earthquake and

tropical cyclone risk

• Global footprint Mexico

Earthquake/hurricane Pacific Islands

• Pioneer in emerging and Earthquake and

and livestock risk

industrialised markets tropical cyclone risk

Guatemala

Nat cat business

interruption risk

Pacific Alliance IDA countries

(CHL, COL, MEX, PER) Pandemic outbreak

Earthquake risk

Uruguay

Energy production

shortfalls due to drought African Risk Capacity Kenya India Thailand

Government drought Livestock Weather insurance Crop

insurance pool insurance for farmers insurance

Swiss Re Group | Company presentation | April 2019 65Swiss Re Group | Company presentation | April 2019 66

Corporate calendar & contacts

Corporate calendar

2019

17 April 155th Annual General Meeting Zurich

3 May Q1 2019 Key Financial Data Conference call

23 May Management Dialogues London

31 July H1 2019 Results Conference call

31 October 9M 2019 Key Financial Data Conference call

25 November Investors’ Day 2019 Zurich

Investor Relations contacts

Hotline E-mail

+41 43 285 4444 Investor_Relations@swissre.com

Philippe Brahin Daniel Bischof Manfred Gasser

+41 43 285 7212 +41 43 285 4635 +41 43 285 5516

Chris Menth Iunia Rauch-Chisacof

+41 43 285 3878 +41 43 285 7844

Swiss Re Group | Company presentation | April 2019 67Cautionary note on forward-looking statements

Certain statements and illustrations contained herein are forward-looking. These statements (including as to plans, objectives, targets, and trends) and illustrations provide current expectations of future events based on certain

assumptions and include any statement that does not directly relate to a historical fact or current fact.

Forward-looking statements typically are identified by words or phrases such as “anticipate”, “assume”, “believe”, “continue”, “estimate”, “expect”, “foresee”, “intend”, “may increase”, “may fluctuate” and similar expressions, or by

future or conditional verbs such as “will”, “should”, “would” and “could”. These forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the Group’s actual results of operations,

financial condition, solvency ratios, capital or liquidity positions or prospects to be materially different from any future results of operations, financial condition, solvency ratios, capital or liquidity positions or prospects expressed or

implied by such statements or cause Swiss Re to not achieve its published targets. Such factors include, among others:

• the frequency, severity and development of insured claim events, particularly natural catastrophes, man- • failure of the Group’s hedging arrangements to be effective;

made disasters, pandemics, acts of terrorism and acts of war; • the lowering or loss of one of the financial strength or other ratings of one or more Swiss Re companies, and

• mortality, morbidity and longevity experience; developments adversely affecting the Group’s ability to achieve improved ratings;

• the cyclicality of the insurance and reinsurance sectors; • uncertainties in estimating reserves;

• instability affecting the global financial system; • policy renewal and lapse rates;

• deterioration in global economic conditions; • uncertainties in estimating future claims for purposes of financial reporting, particularly with respect to large

• the effect of market conditions, including the global equity and credit markets, and the level and volatility of natural catastrophes and certain large man-made losses, as significant uncertainties may be involved in

equity prices, interest rates, credit spreads, currency values and other market indices, on the Group’s estimating losses from such events and preliminary estimates may be subject to change as new information

investment assets; becomes available;

• changes in the Group’s investment result as a result of changes in the Group’s investment policy or the • extraordinary events affecting the Group’s clients and other counterparties, such as bankruptcies,

changed composition of the Group’s investment assets, and the impact of the timing of any such changes liquidations and other credit-related events;

relative to changes in market conditions; • legal actions or regulatory investigations or actions, including those in respect of industry requirements or

• the Group’s ability to maintain sufficient liquidity and access to capital markets, including sufficient liquidity business conduct rules of general applicability;

to cover potential recapture of reinsurance agreements, early calls of debt or debt-like arrangements and • changes in accounting standards;

collateral calls due to actual or perceived deterioration of the Group’s financial strength or otherwise; • significant investments, acquisitions or dispositions, and any delays, unexpected costs, lower-than expected

• any inability to realize amounts on sales of securities on the Group’s balance sheet equivalent to their values benefits, or other issues experienced in connection with any such transactions;

recorded for accounting purposes; • changing levels of competition, including from new entrants into the market; and

• changes in legislation and regulation, and the interpretations thereof by regulators and courts, affecting us • operational factors, including the efficacy of risk management and other internal procedures in managing

or the Group’s ceding companies, including as a result of shifts away from multilateral approaches to the foregoing risks and the ability to manage cybersecurity risks.

regulation of global operations;

• the outcome of tax audits, the ability to realize tax loss carryforwards, the ability to realize deferred tax

assets (including by reason of the mix of earnings in a jurisdiction or deemed change of control), which

could negatively impact future earnings, and the overall impact of changes in tax regimes on business

models;

These factors are not exhaustive. Swiss Re operates in a continually changing environment and new risks emerge continually. Readers are cautioned not to place undue reliance on forward-looking statements. Swiss Re undertakes

no obligation to publicly revise or update any forward-looking statements, whether as a result of new information, future events or otherwise.

This communication is not intended to be a recommendation to buy, sell or hold securities and does not constitute an offer for the sale of, or the solicitation of an offer to buy, securities in any jurisdiction, including the United States.

Any such offer will only be made by means of a prospectus or offering memorandum, and in compliance with applicable securities laws.

Swiss Re Group | Company presentation | April 2019 68You can also read