The Demand for EuroMillions Lottery Tickets

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Demand for EuroMillions Lottery Tickets:

An International Comparison1

Patrick Roger

LARGE, Université de Strasbourg, EM Strasbourg Business School, 61 Avenue de la Forêt Noire, 67085

Strasbourg Cedex, France

e-mail proger@unistra.fr

Abstract

In this article, we analyze the demand for EuroMillions tickets, a European

lottery game launched in 2004 and played simultaneously in nine countries with

the same rules and the same draws. Firstly, using the effective price methodology,

we show that price elasticities are very different across countries. In particular,

Spain and Portugal exhibit low price elasticity and high mean sales, meaning a

low sensitivity to jackpot increases. Ireland and the United Kingdom on the other

hand, exhibit very high long-run elasticity and a large sensitivity to jackpot

variations. The interpretation of these results is linked to lower per capita GDP in

the first two countries, to the development of much syndicated gaming in Spain,

and to the special tax regime in Portugal. Bookmaking activities and the highly

competitive betting market in the UK and Ireland partly explain the results. We

then show that cumulative prospect theory (Tversky and Kahneman (1992)),

though allowing participation in the lottery to be explained, does not improve the

estimation of the demand function.

Classification JEL : D81, H71

1

I wish to thank Serge Blondel, Jalal El Ouardighi, Bertrand Koebel, Jean-Marc Tallon (editor), two anonymous

referees, and my colleagues in the laboratory LARGE for their comments and suggestions that have allowed me to

improve earlier versions of this article.

Introduction

E uroMillions is a lottery launched in February 2004 in three countries, Spain,

France, and the United Kingdom. In October 2004, six other countries joined the pool:

Austria, Belgium, Ireland, Luxembourg, Portugal, and Switzerland. The main feature of

this lottery is a very low probability of winning the jackpot, approximately one chance in

76 million.2

To offer a single game on the European scale allows the pool of potential players to be

increased and prevents players from experiencing jackpot fatigue when faced with the

absence of winners, in particular in countries with small populations (Matheson and

Grote 2004). In fact, when it seems “impossible” to win the jackpot, the players abandon

the game, which increases the probability that there will not be a winner in the next

draw and ends up putting the survival of the game at risk.

On the other hand, a low probability of winning produces rollovers, i.e., the carrying

forward of jackpots not won from one drawing to the next. Rollovers produce two

conflicting effects. On the one hand, the game is more attractive when the jackpot

increases, while on the other hand, the probability of sharing the jackpot in the case of a

win also increases, which decreases the amount received by the winner.

The demand for lottery tickets is traditionally estimated by the effective price method.

The effective price is calculated as the difference between the cost of the ticket and its

expected value.3 The cost is known and generally stable over time, while the expected

value changes at each drawing for two reasons. The first is the existence of rollovers,

2

EuroMillions is one of the lotteries having the lowest probability of winning the jackpot.

3

Cook and Clotfelter (1993), Farrell et al. (1999), Forrest et al. (2000, 2002, 2008), Forrest and McHale (2007),

Geronikolaou and Papachristou (2007), Gulley and Scott (1993), Mason et al. (1997), Purfield and Waldron

(1999), Walker (1998), Wang et al. (2006).

which increase the expected value and reduce the effective price. The second, which is

not independent of the first, comes from the fact that the effective price depends on the

number of tickets sold, a number which influences the probability of rollover. The

method of estimation must take these two effects into account. These remarks show that

the estimation of the demand function for EuroMillions tickets presents a particular

interest because of the very low probability of winning and the numerous rollovers.4

The second interest of the present article comes from the international character of the

lottery that is played in nine countries with the same rules, draws and rollovers. To our

knowledge, there is no other comparable study, since international comparisons of

lotteries treat games which differ across countries (Garrett 2001). In this article, we

analyze the demand for tickets on the European level, then country by country,

examining two preference hypotheses. The first assumes the linearity of preferences

with respect to probabilities and is the most common hypothesis in the literature,

associated with the effective price method mentioned previously. However, it does not

allow participation in the game to be justified since the expected profitability of the

game is largely negative. The second preference hypothesis consists in assuming that the

objective probabilities are distorted in such a way that the perceived probability of

winning the jackpot is largely overestimated. This alternative is in line with the

hypothesis of the transformation of probabilities that one can find notably in Prospect

Theory (Kahneman and Tversky 1979; Tversky and Kahneman 1992) or in the rank-

dependent expected utility model (Quiggin 1982). It enables the demand to be estimated

but also the participation in an unfavorable lottery to be justified,5 since this objective is

not achieved in the classic model.

4

67.9 % of the drawings did not produce a jackpot winner between February 2004 and October 2008 (239

drawings). Even if the period is reduced, beginning in October 2004 (when six new countries entered), the

percentage is still 66.66%. In addition, two sequences of 12 consecutive drawings without a winner occurred

during this period.

5

The first attempts to resolve this problem introduced convex parts into the utility function (Friedman and Savage

(1948), Markowitz (1952)). Earlier models, widely used today, are based on the distortion of objective

probabilities.

One can note that certain authors attribute a “use value” to the very fact of playing, by interpreting participation in a game such as the lottery or EuroMillions as the purchase of a “right to dream”(Conlisk 1993; Forrest et al. 2002; Quiggin 1991). With this perspective, Kearney (2005), analyzed the effects of substitution between lotteries and other consumer goods and showed that the spending dedicated to lotteries did not substitute that for other games of chance, but in fact for spending on other consumer goods. Whichever hypothesis is adopted, the distortion of probabilities or the purchase of a dream, it largely involves the over-weighting of the jackpot when evaluating the lottery. This is why we also estimate the demand functions by replacing the effective price by the anticipated level of the jackpot, according to the model used by Forrest et al. (2002). We shall see however, that this approach does not improve the quality of the fit which is already very good in the standard approach. We assume, however, a different behavior for the player since, on the one hand, there is a classic price-demand relation, while on the other, the larger the quantity of the desired characteristic in the product (amount of the jackpot), the more the player is ready to pay. In this article, we demonstrate significant behavioral differences between countries. In particular, we show that players in the United Kingdom are very sensitive to variations of the jackpot (which corresponds to a decrease in the effective price, real or perceived, depending upon whether the probabilities are objective or deformed). The very competitive games environment that characterizes the United Kingdom can comprise an important reason for the higher sensitivity of players in this country, as recently demonstrated by Forrest et al. (2008). On the other hand, Spanish and Portuguese players are much less sensitive to these variations. Several explanations can be advanced. Differences in GDP per capita can constitute a first explanation for this surprising result. In fact, lotteries are often described as regressive taxation, hitting most particularly the low-income categories (Oster 2004). The culture of syndicated gaming (players play as a group) in Spain also leads to lower sensitivity, given the transaction and information-related costs between members of the group. Lastly one should note that, in Portugal, the winnings from all lotteries, with the

exception of EuroMillions, are taxed,6 which can explain the very high level of

participation and the lower sensitivity to variations of the jackpot.

On the European level, we obtain a long-run price elasticity equal to -0.9, which is

consistent with most of the results in the literature. Farrell et al. (1999) obtained an

elasticity of -1.05 for the United Kingdom, Forrest et al. (2002), -0.82, and Forrest and

McHale (2007), -0.91 for the most recent data. With regard to studies of American

lotteries, Gulley and Scott (1993) obtained elasticities equal to -1.15, -1.92, and -1.2 for

the lotteries of Massachusetts, Kentucky, and Ohio. On the other hand, we shall show

that there are large disparities between countries participating since the same

elasticities vary from -0.49 for Spain to -1.76 for the United Kingdom.

Farrell et al. (1999) interpreted the coefficient of lagged sales in the demand equation as

a measurement of the addictive character of the lottery. They obtained a coefficient of

0.33 for the United Kingdom lottery between November 1994 and February 1997. There

again, with respect to EuroMillions, the results vary considerably from one country to

another since the estimated coefficients vary from 0.2 for Spain to 0.67 for Ireland.

The article is organized as follows. Section 2 summarizes the EuroMillions rules and

presents the data used in the empirical study. Section 3 is dedicated to two models for

estimating the demand, according to the hypothesis adopted for preferences. The

empirical results at the European level are presented in section 4, while in section 5, the

results are detailed country by country. A final section provides conclusions and

proposes directions for further research.

6

We wish to thank an anonymous referee for having drawn our attention to this point.

EuroMillions Rules and Data Used

EuroMillions Rules

To fill in a EuroMillions ticket, the player first chooses five different numbers between 1

and 50, and then, in the second group, two different numbers between one and nine.

These two numbers are in general called “stars” in reference to the European flag.7

EuroMillions offers 12 ranks of winning that are summarized in table 1. The notation

n+m signifies that n correct numbers have been chosen in the first group of 50 numbers

and that m correct numbers come from the group of nine stars.

Table 1: Ranks of Winning, Distribution of Prizes, and Probabilities of

Winning

The column “% prize” gives a distribution of winnings according to the rank of winning

at the end of the study period. This distribution has been twice modified since the

launching of the game. The proportion reserved for rank 1 was initially 20%. It changed

to 22% in August 2004, and then reached its current level of 32% in February 2006.

This distribution is common in lotteries. The portions of the first and last ranks are

always large, but the reasons are different. A high jackpot makes the game attractive and

the existence of numerous “small winners” avoids discouraging players from betting on

the following drawing. One can expect therefore that the sales for a given drawing

7

Lotteries are generally based on the drawing of 5 to 7 numbers in groups of 35 to 55 numbers.

influence the sales for the following drawing since the global amount of these

consolation prizes is proportional to the sales.

EuroMillions also distinguishes itself from other lotteries by its international character

since it is played in nine countries under the same conditions with a single drawing. All

players face the same rules.8 We should mention however, that the cost of the ticket is

2 € in the euro zone, £1.5 in the United Kingdom, and 3.2 francs (CHF) in Switzerland.

As the tickets and the winnings are expressed with the same currency, we consider that

all of the amounts are euro-equivalent. It is the most natural choice since the countries

of the euro zone are the most numerous, and this presents an additional advantage

where the withholding of the organizer is 50%,which leads to equality in the number of

tickets with the amount redistributed (apart from rollovers).

Coming back to table 1, it is noted that the sum of the percentages of winning is only

94%. This is explained by the existence of a reserve fund intended to supply certain

jackpots. In fact, when the jackpot has just been won, the following one is generally 15

million, and it requires a volume of 46 million tickets sold to ensure the payment,9

which is much greater than the average sales.

When a jackpot is not won, (rollover), the amounts reserved at this rank (32% of total

winnings) will feed the jackpot for the following drawing, as well as a portion of the

reserve fund. The organizers of the game communicate the estimated amount of the

following jackpot with heavy radio, television, or print media advertising. Even if it is

not possible to obtain the exact amounts dedicated to these ads, it is obvious that this

communication has an effect on sales, in particular when the jackpot reaches very high

amounts after five or six rollovers. However, it is not so much the budget dedicated to

communication as the message itself that influences sales, this message in every case

summing up the single amount of the following jackpot.

8

It should be mentioned that winnings of the game are not taxed, except in Switzerland where the withholding at

source is 35%.

9

When the game started, and only three countries participated, there were several jackpots of €10 million.

Certain exceptional events also give rise to more intense advertising communication. This is the case when exceptional jackpots are offered, which are not the result of a series of rollovers. As we will stipulate further, our study period contained two events of this type, with respective jackpots of 100 and 130 million euros. These cases receive a special treatment in the demand estimation model. In summary, EuroMillions is the ideal lottery for an international comparison since numerous variables are controlled. The takeout rate by the organizer is the same in every country; in addition, it has stayed constant since the beginning of the game. This is not the case in other international comparisons appearing in the literature (e.g., Garrett 2001). Consequently, if differences appear in the demand functions, they cannot come from the design of the game, but are rather a consequence of behavioral differences or differences related to the environment of the game. The Data Our database is constructed from the site www.sojah.com, which is the official site regarding games of chance organized in France. It supplies time series of drawings and individual winnings, but also all the legal texts with regard to lotteries. Concerning EuroMillions, this site allows access to the data of all participating countries. Our database includes the first 197 drawings, from the day of launch (February 13, 2004) until November 16, 2007. We have mentioned in the introduction that six countries joined the first three at the 35th drawing. Consequently, we eliminate these first 35 drawings, including the day of entry of the six new countries, to avoid the bias induced by the attractiveness of the first drawing (increased by advertising communication related to the launch) for the players of these six countries. Finally, 162 drawings are included in the analysis that follows, starting on October 15, 2004. The following data will be used: the volume of sales, country by country, and the aggregate level;

the individual winnings for each rank of winnings;

the number of players winning at each rank, and in each country;

the effective jackpot (known only after the drawing), which is divided between the

first-rank winners;

the percentage of winnings reserved at each rank.10

It is worth noting that more than 80% of sales are made in four countries, Spain,

France, Portugal, and the United Kingdom. In addition, Portugal, with only 11 million

inhabitants, realizes a turnover comparable to that realized in France and in Spain and

greater than that in the United Kingdom, while the population of these countries is five

or six times higher. We will come back to this point below.

Descriptive Statistics

Table 2 presents the descriptive statistics with regard to the essential variables entering

into the estimation of the demand function, i.e., weekly sales, anticipated jackpot (the

calculation of which will be detailed in the following section), and the actual jackpot as it

appears in the database. In columns 2 and 3, we have added the populations of the

countries and the GDP per capita.11

Table 2: Descriptive Statistics of the Population, the GDP Per Capita,

and Weekly Sales*

10

This distribution underwent a single change during our study period. The portion reserved for the jackpot shifted

from 22 to 32%. This modification was compensated for by a decrease in the percentage dedicated to the reserve

fund, which shifted from 16 to 6%.

11

These data are given in 2006 $US and come from the website of the Conference Board and the Groningen Growth

and Development Centre (http://www.conference-board.org/economics/database.cfm).

For variables concerning the game itself, the table gives the following variables: minimum (Min), maximum (Max), mean (μ), standard deviation (σ), and coefficient of variation (μ/σ). As we’ve already mentioned, the range of variation is very broad, essentially due to rollovers. Several elements in the table are worth commenting upon, in particular, the situations of Portugal, the United Kingdom, and Luxembourg. Portugal is characterized by a high average level of sales, particularly if one considers the population, and by a low coefficient of variation of 0.38 (however, the coefficient for Spain is even lower). On the other hand, the United Kingdom is remarkable because of the low average level of sales, (there again with respect to the population) and a very high coefficient of variation. The two countries for which the GDP per capita is the lowest (Spain, Portugal) also have the lowest coefficient of variation. Knowing that the variations of sales from one week to another are essentially due to rollovers, a possible interpretation of this fact is that the players of the countries with low GDP are less sensitive to variations of the jackpot. This can be explained by the fact that the initial jackpot is 15 million, which already constitutes a very high amount for a low-income player. For example, the GDP per

capita of Portugal is equal to half that of Ireland, while its sales are three times higher.

In other words, a win of 15 million moves low-income players to wealth levels where the

marginal utility is negligible, or at least very low. In addition, lotteries are considered as

regressive taxation (Oster 2004) since they impact low-income populations.

Let us recall, however, that the situation of Portugal is very special as the winnings of

EuroMillions are not taxed, unlike those of other national lotteries. This can also be a

factor in the popularity of EuroMillions in Portugal.

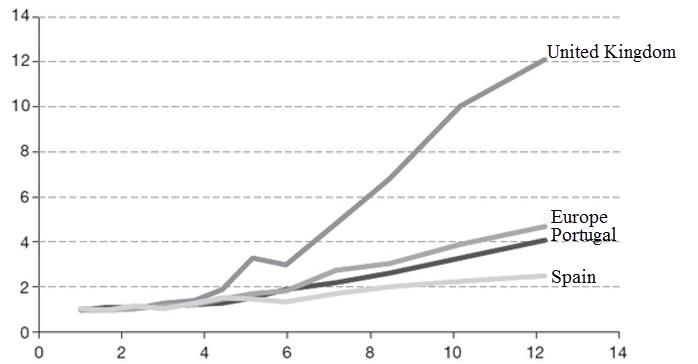

Figures 1 and 2 illustrate the influence of the jackpot on sales and its variation across

(selected) countries, during two sequences of 12 consecutive weeks without a jackpot

winner.

Figure 1: Standardized Sales as a Function of the Amount of the

Jackpot, after 12 Drawings without a Jackpot Winner in Portugal,

Spain, the United Kingdom, and Europe (9 Countries)

Sequence 1: November 18, 2005, to February 3, 2006

The initial level of sales is normalized to 1 for each country and represents the sales

when the jackpot is 15 million euros. In each of these figures, the Spanish and

Portuguese curves are situated below the average (corresponding to the aggregate levelfor Europe), while the curve for the United Kingdom is situated largely above the

average. This shows the significant differences in sensitivity to the increase of the

jackpot in each of these countries.

The case of the United Kingdom is special in that gaming activities (gambling)

constitute a very competitive market. There were 680 authorized bookmakers in 2006,

according to the NJPC report (National Joint Pitch Council). When the jackpot increases

(and therefore the effective price decreases), EuroMillions becomes more competitive

compared to other lotteries, or more generally compared to other forms of gambling

(horseracing, dog racing, or sports gambling) proposed by bookmakers (Forrest et al.

2008).

Figure 2: Standardized Sales as a Function of the Amount of the

Jackpot, after 12 Drawings without a Jackpot Winner in Portugal,

Spain, the United Kingdom, and in Europe (9 Countries)

Sequence 2: September 1, 2006, to November 17, 2006

Finally, the situation of Luxembourg is also worth noting. Table 2 shows that GDP per

capita is exceptionally high since it is 50% higher than that which immediately follows,Ireland, and three times higher than that of Portugal. These data however, must be considered with caution as thousands of bank and insurance company employees work in Luxembourg, while they are French, Belgian, or German residents and cross the border every day to go to work. This also indicates that it is impossible to identify the origin of the sales. It could be that a non-negligible portion of these sales come from cross-border workers. Estimation of the Demand for EuroMillions Tickets Specification of the Models Linear Preferences with Regard to Probabilities The usual method for estimating lottery sales is based on standard economic theory linking price and demand. However, the cost of the ticket is very stable over time (and even constant during our study). Therefore, it is not a good measure of price, simply because each ticket can also be seen as an investment characterized by an expected payoff. Because of this, most articles link demand to the effective price, defined as the difference between the cost of the ticket and its expected payoff (Gulley and Scott 1993; Scott and Gulley 1995; Walker 1998; Farrell et al. 1999; Forrest et al. 2001; Forrest et al. 2002; and Wang et al. 2006). The expected payoff is calculated here with respect to objective probabilities. Consequently a lowering of the effective price by one cent has the same effect whether the decrease is the result of an increase in the jackpot or the increase in the winnings of the intermediate ranks. This is why we have mentioned linearity with respect to probabilities in the title of this subsection. In the following subsection, we will discuss the case where players distort objective probabilities. The two principal factors determining the effective price are the volume of sales and the rollovers which increase the jackpot and decrease the price. Other factors may influence demand, such as the earnings of potential players or other demographic considerations. However, in the short run, these factors are stable and do not explain the variations in demand observed in Figure 3. This figure shows the evolution of ticket sales between

October 15, 2004, and November 16, 2007, i.e., 162 drawings. Considerable variations

appear, either progressively and in a few weeks, when several rollovers occur in a row,

or abruptly when an exceptional jackpot is offered. This is the case on two occasions

corresponding to drawings 122 (February 9, 2007, with a jackpot of 100 million) and 155

(September 20, 2007, with a jackpot of 130 million). These two points are circled in

Figure 3.

Figure 3: Evolution of Sales over Time (in Number of Tickets)

This time-series of sales is typical of a lotto-like game (see for example Farrell et al.

1999; Gulley and Scott 1993; Purfield and Waldron 1999; or Beenstock and Haitovsky

2001). The successive rollovers lead to significant increases in sales, and Figures 1 and 2

have shown that the sales curve is growing and convex over the sequences of drawings

when the jackpot was not won. Beyond the jackpot effect, one can also observe a positive

trend in the evolution of sales since our study period began immediately after the game

was launched. The number of tickets evolves from 20 million at the start of the period to

40 million at the end of it.

Figure 4 shows the evolution of the jackpot over the same period. It is clearly apparent

that the sales peaks correspond to the highest jackpots, whether these come fromrollovers or from exceptional events (which are also circled in Figure 4). In fact, the

correlation between these two series is 0.89.

Figure 4: Evolution of the Jackpot over Time (in €)

Finally, the growth of sales due to rollovers leads implicitly to a lower probability of

observing a rollover in the following drawing. Consequently, the amount of the rollover

is an essential determinant of the volume of sales, in as much as there is no longer any

withholding by the organizer on the rollover since it was already taken.

The pari-mutuel betting component of the game makes the estimation of demand

interesting in itself, because demand depends on effective price, itself determined by the

number of tickets sold (i.e., the demand). Therefore, the problem is resolved in two

steps. In the first step, the effective price is estimated from instrumental variables

influencing the demand, such as the announced jackpot, the sales trend, and the dummy

variables related to exceptional drawings. In the second step, the effective price

estimated in the first step is then injected into the second regression, which links

demand to this price.As we have already mentioned, the effective price is the difference between the cost of the ticket and the expected gain in holding it. The expected value of draw t is written as: where p is the probability of winning the jackpot (1/76275360), JAt is the anticipated jackpot, and ESt is the part of a jackpot that a player can expect to receive. Kt designates the expected value of winnings in ranks 2 to 12. We disregard the fact that rollovers may appear at lower ranks, and we assume that Kt is equal to €0.62, i.e., to the portion of the winnings reserved for ranks 2 to 12. We should mention, nevertheless, that a rollover at rank 2 happens 7 times, essentially at the start of the period. However, this simplifying hypothesis is without consequence since the sums not won are brought forward to the following ranks of the same draw. There is, therefore, no transfer to the following week. A second particularity is worth mentioning. From November 2005 to February 2006, 12 draws in a row did not bring any jackpot winner, driving the jackpot to 183 million finally shared between three players. The organizers then decided, probably to avoid jackpot fatigue, that the jackpot would be shared by second-rank winners, after 12 weeks in a row without a winner. This happened once on November 17, 2006. Cook and Clotfelter (1990), using the binomial law approximation of Poisson’s law, wrote equation (1) in the following form: Where p is the probability of winning the jackpot, c is the cost of the ticket, τ is the takeout rate (50% for EuroMillions), Qt is the number of tickets sold for the drawing t, Rt-1 is the amount of the rollover accrued from the previous drawings, βt is the portion of the winnings reserved for the jackpot, and αt the portion intended for lower ranks (see Table 1). Over the study period, αt is constant and equal to 62%. As we have already indicated, βt rose from 22% to 32% in February 2006, but this increase was made to the

detriment of the part of the reserve funds that dropped from 16% to 6%, without modifying the portion of the lower ranks. Not less than αt + βt < 1 of it remained due to the existence of the reserve funds. The variable Qt is obviously not known in equation 2. The first step of the process is to approximate it using variables known prior to date t. In fact, it involves determining the conditional expectation of sales with respect to known information prior to the draw, i.e., where It – 1 is the information available prior to draw t taking place. For this first step, our estimation uses traditional variables as follows: Where EVENT is a dummy variable taking into account the two exceptional jackpots, TEND is a drawing number to reflect a possible trend in the evolution of sales, and PART measures the portion of the winnings reserved for the jackpot. It is equivalent to a dummy variable since it only assumes two values, 22% and 32%. As previously, JAt designates the anticipated jackpot. HALO is a dummy variable that represents a possible Halo effect such as that observed by Farrell et al. (1999) and Grote and Matheson (2007). A lagged adjustment of sales has been observed after a big jackpot win. In practical terms, when there is a series of rollovers during which the jackpot increases each week, the demand follows the same trend up until the jackpot has been won. To simplify, the halo effect means that players take two weeks before readjusting their demand after the jackpot has been won (instead of immediately adjusting it after the win.) Consequently, over two successive weeks, an evolution of sales is observed in a direction opposite that of the jackpot. Therefore, the dummy variable HALO is worth 1 at draw t if the product (Qt – 1 – Qt – 2) (JAt – 1 – JAt – 2) is otherwise negative or 0. The presence of Qt – 1 in equation 3 does not reflect a focus on a time series of sales. This variable takes into account the reinvestment of small winnings in the next draw, a common phenomenon in this type of game. Farrell et al. (1999) consider that the

coefficient of this variable measures the addictive character of this lottery. An alternative interpretation, demonstrated by Thaler and Johnson (1990) is known as the house money effect. The players “lose” their aversion to risk since in a way they are playing with the money from the organizer, the company Française des Jeux. This being the case, we could have created a variable “small win” to measure this effect, such as the amount won in the two last ranks. Since this amount is strictly proportional to the number of tickets sold (the percentage remaining constant during the study period), the two choices are equivalent. This remark also explains why we use the ordinary least squares in the estimation of equation 4 (Walker and Young 2001). Non-Linear Preferences with Regard to Probabilities The basic disadvantage of the standard modeling procedure presented in the previous section is its relative inconsistency, since it allows the variations in demand to be explained, but not the existence of demand. In fact, in the approach, which consists of considering the effective price as the difference between the cost of the ticket and the expectation of winning, there is nothing that allows one to understand why the players are ready to pay this price. As we mentioned in the introduction, an alternative approach consists of considering the distortion of the objective probabilities, such as perhaps proposed in the rank-dependent expected utility models of Quiggin (1982) or in the Cumulative Prospect Theory (CPT) developed by Kahneman and Tversky (1979) and Tversky and Kahneman (1992). The essential elements of the latter model are provided in the appendix. We should simply remember here that low probability events corresponding to the extreme results of a lottery are over-weighted, while medium- or high-probability events are under-weighted. In addition, risky prospects are evaluated on the basis of the winnings and losses that may result therefrom. If the parameters estimated by Tversky and Kahneman (1992) are adopted, it is easy to show that participation in EuroMillions has a positive value (Pfiffelmann 2010). Table 3 summarizes the probability of the possible results and the weights associated with the CPT. The last column indicates the weight/probability ratio. This ratio is less than one for the unique situation of loss. It is, on the other hand, decreasing with

respect to the probability of winning, resulting in a considerable overvaluation of the

weight given to the jackpot, thus leading to a positive evaluation of participation in the

game.

Table 3: Probabilities of Winning and Associated Decision Weights

With regard to demand sensitivity to an increase in the jackpot, let us recall that CPT

weighting does not depend on the winnings themselves, but on their rank.

Consequently, the addition of a rollover to the jackpot does not change the weighting

since the order of the ranks of winning does not change. In addition, the individual

earnings from ranks 2 to 12 are determined solely by the totalizator principle, thereby

rendering the individual gain of these ranks insensitive to demand.12 A second over-

weighting of the jackpot comes from the distribution of winnings in Table 1. The

winning percentage allocated to rank 2 is more than 4 times less than that for rank 1

12

For example, the correlation of individual winnings in the ranks 4 to 12 with the number of tickets sold is not

significant. In these ranks, the variation of individual winnings is more related to the non-random selection of

numbers by players than the number of tickets sold. At rank 2, this analysis is no longer relevant, since 7 drawings

did not produce a rank 2 winner and the corresponding amounts were moved to rank 3.while the mean number of winners in rank 2 is 14 times greater. In average, this means

that the mean individual earnings in rank 2 is 60 times less than the jackpot, even in the

absence of a rollover. This explains why, in the framework of the CPT, the “value” of a

ticket is almost exclusively derived from rank 1 earnings.13

The following empirical study takes into account the large over-weighting of the jackpot

in a non-linear model with respect to probabilities by adding to the method of effective

price an analysis in which effective price is replaced by the jackpot in the second step of

the regression.14 The results do not differ greatly from those obtained with the effective

price. This is not surprising, even if the non-linear preferences better reflect the

behavior of the players. In our data set, price variations come essentially from rollovers;

therefore effective price variations come from jackpot variations and not from earnings

from other ranks. There is thus no reason why the non-linear approach should give

better results.

Estimation by Instrumental Variables

The following regression (Model I) is used to estimate AVt.

Introducing (the square of the jackpot) as an independent variable is justified by the

convexity of the relation usually observed between sales and the amount of the jackpot

(Forrest et al. 2002; Wang et al. 2006). Beenstock and Haitovsky (2001), while using

13

Note, however, that our reasoning is simplified by implicitly assuming that players only buy one ticket. In reality,

the variations of demand in the case of an increase in the jackpot come from new players, but also from players

increasing their bet . . . and therefore the probability of winning.

14

Forrest et al. (2002) use this same approach to evaluate “buying a dream” in the participation in the game. We

also add that in the CPT, the evaluation function is slightly concave with regard to winnings. One must therefore

use as an explanatory variable, the jackpot raised to a power less than 1 (0.88 in the estimations of Tversky and

Kahneman). However, retaining this concavity parameter, the correlation between JA and JA0.88 is 0.998.the sales logarithm as a dependent variable, use the square of the jackpot logarithm as an independent variable in order to take account of the non-linearity of the relation linking jackpot and sales. To evaluate equation (4), a prediction of the announced jackpot for the next draw (JAt) is necessary. We cannot, however, use all of the information in the database since the jackpot supplied is either the jackpot actually announced when there were winners for the previous draw (15 million is announced in most cases), or the actual jackpot thus calculated after the draw. We must therefore estimate JAt from information available in the information group It – 1. When there are winners in the t – 1 draw, we adopt the jackpot proposed in the database. When there is a rollover, we assume that the sales remain identical, but we allocate the reserve funds in full to the jackpot of the following draw. This is an approximation since the organizers use the reserve funds strategically. More precisely, when the jackpot is “low,” the full amount of the reserve funds is allocated to the following jackpot. After several rollovers, only part (unknown before the draw) of the funds are reallocated to the next jackpot. Therefore, our estimation is very precise for the first weeks of rollover, but somewhat optimistic when the jackpot reaches very high amounts (despite our conservative estimation that mitigates the error due to approximation). Figure 5 illustrates this point for a sequence of 12 draws without a winner. The jackpot coming from the database is compared (dashed line JR) with our estimation (bold line JA). To take exceptional jackpots into account, the variable EVENT takes the value of the jackpot announced on the two corresponding dates and takes the value 0 for all other drawings.

After having estimated the coefficients of equation (4), we reintroduce the estimated

values into equation 2 in order to calculate the expected value of the game AVt. The

effective price is then equal to Pt = c – AVt with c = 2 €.

Figure 5: Actual Jackpots (JR) and Anticipated Jackpots (JA) in a

Sequence of Drawings without a Jackpot Being Won

Second Estimation Step

Linear Preferences with Regard to Probabilities

The second step in the demand estimation process links sales to the effective price

obtained in the first step, by means of the following equation:

This formulation using logarithms for lagged sales, exceptional jackpots, and effective

prices enable β3 to be interpreted directly as short-run price elasticity of ticket sales. The

long-run elasticity is equal to β3/(1 – β2). Equation 5 is comparable to that used by

Forrest et al. (2002) and Wang et al. (2006), which are sufficiently close so as toeliminate any need to distinguish two days of the week since EuroMillions has only one

drawing per week. Here, the variable LEVENT equals the logarithm of EVENT, when EVENT

is other than 0 and 0 elsewhere.

Non-Linear Preferences with Regard to Probabilities

In the context of non-linear preferences presented in the previous section, the second

step consists of evaluating the following equation:

We have previously seen that the essential characteristic of CPT, in the case of

EuroMillions, is the over-weighting of the jackpot. Consequently, what differentiates the

linear and non-linear approaches is essentially the weight allotted to the jackpot.

Aggregate Empirical Study

Estimation by Instrumental Variables

Equation 4 contains the variable Qt – 1: consequently, the estimation is performed for 161

drawings, beginning on October 22, 2004. Table 4 summarizes the results obtained. The

variable , representing the square of the jackpot, has been divided by 108 to obtain a

regression coefficient on the same order of magnitude as that of JAt.

Table 4: Model I: Estimation of Weekly Sales*Seven of the eight coefficients are largely significant at the 0.1% level. Not surprisingly, the SHARE coefficient is non-significant. The jackpot announced for draw t includes the part allocated to the reserve funds in draw t - 1. The change in the percentage allocated to the jackpot from 22% to 32% by reducing the reserve funds was already integrated into the variable JAt. With regard to the variable HALO, Grote and Matheson (2007) note that a halo effect corresponds to successive drawings with decreasing sales but increasing jackpot. While the halo effect only occurred six times during the study period, the HALO coefficient is significant. The adjusted R2 is 0.967, therefore very close to 1, and the statistic F is equal to 665.65, which demonstrates the quality of the estimation when the independent variables are known before the draw t. Effective Price Method in the Second Step For the effective price model, the estimated equation in the second step of the regression is written as (model IIa):

In this equation, the values of LEVENT are either 0 or ln(JAt) (rather than considering a

dummy variable) when there are exceptional jackpots, so as to take into account the

difference between the amounts of these exceptional jackpots. The results are

summarized in Table 5. All coefficients are largely significant and we shall examine

more specifically the short-run price elasticity equal to -0.615 with a Student statistic of

-29.45. Unsurprisingly, this result indicates a downward sloping demand. Ceteris

paribus, a lowering of 1% of the effective price leads to a growth of 0.615% in the

number of sales. However, the ceteris paribus is restricted here, as a 1% decrease in the

effective price has long-term effects on demand since lagged sales enter into the

estimation with a significant coefficient.

Table 5: Model IIa: Estimation of Weekly Demand*

Consequently, the long-run elasticity is measured as β3/ (1 – β2) and equals -0.892. This

result is in line with the one obtained by Forrest and McHale (2007) in their analysis of

EuroMillions and the British lottery. The maximization of profits by the organizer

assumes a long-run elasticity price equal to -1 since the takeout rate is 50%.15 The result

15

Indeed, if the organizer sells100 tickets at 2 €, the withholding is 100 €, approximately equal to the effective price

of all of the tickets. A lowering of the takeout rate of 0.5% leads therefore, to a lowering of the effective price by

1%. But the volume of sales increases by 1% if the elasticity is equal to -1. Consequently, 101 tickets are sold andobtained can therefore lead to the conclusion that sales are not maximized with the current design and that the effective price must be increased. However, caution is necessary before reaching such a conclusion for two reasons. The first is related to rollovers. During the study period, the variation of effective price is essentially due to rollovers, and less so to the variation of the number of players from one draw to the next. It is not obvious, therefore, that a lowering of effective price due to a different cause would impact the demand in the same way. The second, and more subtle, reason for caution is that long-run elasticity is obtained through a regression of sales (logarithm) on effective price (logarithm) using aggregated data at the European level. However, the European aggregate of sales can hide very different national situations. Figures 1 and 2 presented in section 2 highlight the important behavioral differences across countries such as Spain, Portugal, and the United Kingdom. For this reason, equation 5 will be estimated again in the following section country by country to refine the interpretation of the elasticities and to assess how well the model fit the various national contexts. Nonlinear Preferences in the Second Step Table 6 is equivalent to Table 5, when the effective price is replaced by the estimated jackpot so as to take into account the strong jackpot over-weighting when preferences are non-linear. Coefficients for estimated and exceptional jackpots are multiplied by 10 9 to ensure readability. Results are practically identical in terms of quality of estimation. This tends to show that it is indeed the jackpot that is essential in the determination of the demand, more than the effective price. To be able finally to come to a decision, one must however have data with significant price modifications related to reasons other the profit is then equal to 0.495 × 2 × 101 = 100. Because of this, the level of elasticity is indeed that which maximizes the organizer's profit.

than rollovers, such as, for example, the modification of the takeout rate or changes in

the distribution of winnings.

Table 6: Model IIb: Estimation of Weekly Demand*

International Comparison

Linear Preferences

Equation (5) is evaluated in each of the nine participating countries, retaining the

national sales levels as the dependent variables. It is important to notice that the

effective price is the same in all countries, since all players face the same jackpot and

winning probabilities in whatever country they play.16 However, sales time series Qt can

vary across countries.

Consequently, the coefficients β2 and β3 vary across countries depending on the behavior

of national players, and, more precisely, their reactions to jackpot variations. The

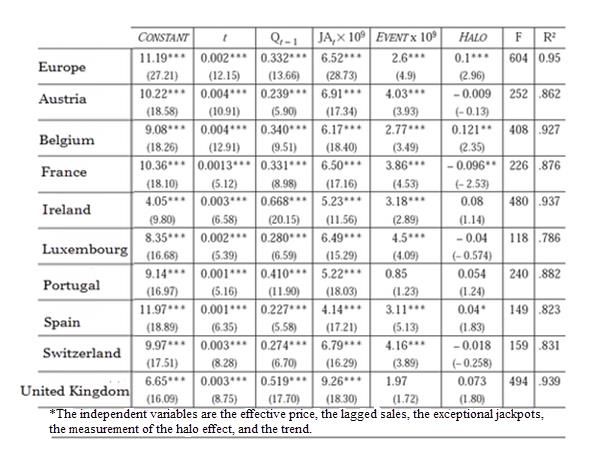

essential results of the national analyses are summarized in Table 7.

16

We mention, however, that the change of the rate of exchange can have a slight effect on the effective price

compared to winnings.Table 7: Estimation of Weekly Sales, Country by Country*

The model performs well in all countries since the significant coefficients are the same

as the aggregate level with the exception of the HALO effect, which is significantly present

in only two countries.17 The lower significance of the variable EVENT in Portugal and the

United Kingdom should also be mentioned, this variable being significant at the 1% level

versus 0.1% at the aggregate level.

Very clear differences are observed for the coefficients β2 and β3 from one country to

another.

17

To a lesser degree, the HALO effect is present in Spain and in the United Kingdom (significant at the threshold of

10%).The influence of lagged sales is much clearer for Ireland and the United Kingdom and leads to much higher long-run elasticities (in absolute values). Comparing the United Kingdom to Spain is particularly interesting. Players in the United Kingdom react very strongly to jackpot increases, especially when it reaches high levels after several rollovers, thereby producing high short-run elasticity. Due to the difference between lagged sales coefficients, the difference in long-run elasticities is even higher. However, Spain is a special case as shown in the excellent article by Garvia (2007), due to the development of syndicated gaming for historical reasons, traced back to the nineteenth century and the existence of the Christmas lottery. The prohibition of the Spanish lottery in 1861 and the reform of the Loteria Nacional which followed, made the cost of gaming considerably higher, leading to the marked development of syndicated gaming among the working classes. Garvia mentions that, for the Christmas lottery, 90% of players participate collectively, notably between work colleagues or within the family. Because of this, collective gaming has become a custom in Spain. It is therefore not surprising that the price elasticity of demand is weak, since it is easier to play the same amount each week for the members of a syndicate, particularly when numerous players are involved in the decisions. This elasticity can be interpreted in terms of high transaction costs. National specificities show that interpretation of long-run elasticities at the aggregate level must be made with a certain degree of caution, for two reasons. The first is that our analysis and those performed in other studies on the same theme focus essentially on the reactions to jackpot changes since they are the primary causes of price changes. Consequently, lowering the price by 1% due to a modification of the state’s takeout rate might not have the same effect on demand as an equivalent lowering due to a rollover, and these differences would vary across countries. The second reason is simply due to the difference between and where denotes the sales for country k at date t. For a draw in which the level of sales corresponds to the average sales in each country over the three-year period considered in our study, and supposing a price increase of 1% because of a change in the takeout rate, the sales will drop by an average

of 0.579% based on national elasticities, but by 0.615% based on aggregated elasticity.

These percentages would be 0.93% and 0.9% respectively for long-run elasticities.

Non-Linear Preferences

Table 8 is the counterpart of Table 7 when the effective price is replaced by the

estimated jackpot in the analysis of sales, country by country. Here again, very similar

results are found to those obtained at the aggregate level. The R2 are practically identical

and the F statistics are slightly lower in most cases. As we have mentioned above, this is

not surprising since price changes are produced mainly by rollovers. Obviously, very

different results would have been produced if the price variation came from a

modification of winnings at lower levels because of the weight/probability ratios

presented in Table 3. Mention could be made, for example, of the British lottery for

which the organizing company Camelot decided to allocate a “super jackpot” at the

second rank of winnings on September 19, 1998.18 Sales dropped by 7.1% compared to

the previous Saturday while the effective price dropped from £0.55 to £0.28.

Table 8: Estimation of Weekly Sales, Country by Country*

18

This example is cited by Forrest et al. (2002), p. 487.This example, while anecdotal, shows that price decreases do not have the same effect and that the design of the game is important. This could lead to the conclusion that it is useless to propose “small prizes” since players seem to be mainly attracted by the amount of the jackpot. These consolation prizes are very useful for the organizer, however, since on the one hand, they prevent the phenomenon of jackpot fatigue and on the other, they constitute a sort of investment for the organizer, in that a non-negligible portion of the winnings is reinvested in the following drawing, as shown by the lagged sales coefficients in the regressions (house money effect and/or addiction). Effective Price Paid in Various Countries To conclude this empirical study, we illustrate the effect of differences in elasticity when calculating the mean effective price paid by players in various countries. As players in the United Kingdom are very sensitive to jackpot variations, they would be expected to

enter late in the game when successive draws produce no winners. In other words, their

participation increases strongly when the effective price is low, i.e., when the jackpot is

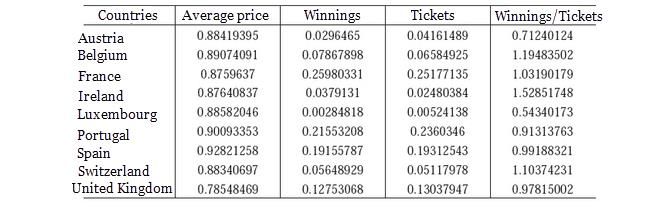

high. Table 9 illustrates this point. The mean effective price paid by a British player is

0.785 € (or the equivalent in £), while the Spanish player pays on average 0.928 €,

which represents a difference of about 50%.

Table 9: Mean Effective Price Paid by Players in Each Country in the

Share of the Winnings and Outlay in Each Country

The third and fourth columns of the table give the proportions of tickets played of

winnings, while the last column indicates the ratio of winnings per ticket played. The

ratio for British players could be higher because of their “opportunistic” behavior. This

is not the case since it is equal to 0.978, while the ratio for Spanish players 0.982.19 This

result is not as surprising as it seems, because of the nonlinearity between the number

of tickets played and the number of winners of a jackpot. As the latter is very low, it is

natural to observe significant differences between mean actual winnings and

expectations of winning. This phenomenon clearly appears for countries with small

populations. They show “extreme” ratios depending only on the number of jackpots won

in these countries. For example, the ratio for Ireland is very high (1.53) and this is due

solely to the winning of a jackpot of €115 million.

19

One could comment wittingly by remarking that British players seem more rational (or opportunistic), but less

willing to take chances than Spanish players!Conclusion EuroMillions is a lottery that is particularly well suited for making international comparisons on the European level since players in nine participating countries face the same conditions of play, the same draws, and the same rollovers. The national environments are different, however, which leads to variable sensitivities with respect to variations in the jackpot or the effective price of the ticket. The aggregate analysis shows that frequent rollovers due to the low probability of winning, induce significant variations in the effective price. Long- (or short)-run elasticity is on the order of -0.9 (or -0.6), i.e., greater than -1, a level which maximizes sales. These results are consistent with those elsewhere in the literature. However, they mask significant national disparities. More precisely, the short-run elasticities are very low in Spain and Portugal compared with those of the United Kingdom. We have interpreted these results by drawing on the regressive character of lotteries, on the one hand, and on national contexts, on the other, including the development of syndicated gaming in Spain, the particular taxation situation for EuroMillions in Portugal and the very competitive gaming environment in the United Kingdom (Forrest and McHale 2007). However, these interpretations need a more in-depth examination, for example, to separate the effect of income from the effect of taxation in Portugal. We have shown that the introduction of non-linear preferences to the Kahneman- Tversky model does not greatly improve the estimation, even if they are more satisfying from a theoretical point of view in explaining the participation in the game. The similarity of results is due to the very specific data associated with games of this type: variations of price are almost exclusively due to rollovers, which makes it difficult to clearly separate the effective price effect from the jackpot effect. Our study suggests several lines of research. An important question for the organizers of games of chance is to determine if “national” and “international” lotteries are substitutable or complementary products (Forrest et al. 2008). This question will

become more important in France in the near future because of the liberalization of games of chance. In addition, this question presents the problem of free-riding. Forrest and McHale (2007) show that in the United Kingdom, the (national) lottery and EuroMillions are complementary rather than substitutable products. In this case, it can be profitable for a private or public organizer to “ride on the back of” the EuroMillions jackpot, (fed in large measure by the bets of players from other countries) by proposing a national game with a design close to that of EuroMillions. In this regard, one might question the strategy of the company Française des Jeux, which in October 2008, transformed the rules of the French game, Loto, so that the new Loto resembles EuroMillions. A second line of research, already explored in various countries (Roger and Broihanne 2007; Farrell et al. 2000), consists of examining the choice of player combinations in the framework of EuroMillions, so as to determine if the preferred numbers (conscious selection) differ between countries. However, the historical data are still insufficient since there is only one draw per week. One can already observe, however, that the individual winnings in the last ranks are an increasing function of the average of the numbers drawn, marking a preference for small numbers, a preference demonstrated in all studies of this type. Appendix Consider a lottery X defined by X = ((xj, pi), i = – m, . . ., n) where the results xi are ranked in ascending order and pi denotes the associated probabilities of occurrence. The negative (positive) indexes are associated with losses (winnings), losses and winnings being defined with respect to a given reference point. In our case, lottery X represents

the 13 possible results for the player, i.e., the 12 ranks of winnings and the most probable situation in which the player wins nothing (and therefore loses the bet c = 2 €). The evaluation function for the lottery is written as: where X+ = max(X, 0) and X– = min(X, 0). The function V is defined as follows: The evaluation function v proposed by Kahneman and Tversky (1979) takes account of the aversion to losses and is written as: Where λ is the aversion to loss parameter and α < 1 represents the marginally decreasing effect of winnings and losses on the evaluation of the lottery. The probability distortion function retained by Tversky and Kahneman (1992) is in the following form:

The distinction between w+ and w– is related to possibly different values for the

parameter γ. It has been estimated at 0.614 for winnings and 0.694 for winnings by

Tversky and Kahneman (1992).

References

Beenstock, Michael, and Yoel Haitovsky. 2001. “Lottomania and other Anomalies in the

Market for Lotto.” Journal of Economic Psychology 22:721–744.

Clotfelter, Charles. T., and Philip J. Cook. 1990. “On the Economics of State Lotteries.”

Journal of Economic Perspectives 4 (4): 105–119.

Conlisk, John. 1993. “The Utility of Gambling.” Journal of Risk and Uncertainty 6:255–

275.

Cook, Philip J., and Charles T. Clotfelter. 1993. “The Peculiar Scales Economies of

Lotto.” American Economic Review 83 (3): 634–643.

Donkers, Bas, Bertrand Melenberg, and Arthur van Soest. 2001. “Estimating Risk

Attitudes Using Lotteries: A Large Sample Approach.” The Journal of Risk and

Uncertainty 22 (2): 165–195.

Farrell, Lisa, Edgar Morgenroth, and Ian Walker. 1999. “A Time-Series Analysis of UK

Lottery Sales: Long and Short Run Price Elasticities.” Oxford Bulletin of

Economics and Statistics 61: 513–526.

Farrell, Lisa, Roger Hartley, Gauthier Lanot, and Ian Walker. 2000. “The Demand for

Lotto: The Role of Conscious Selection.” Journal of Business & Economic

Statistics 18 (2): 228–241.

Farrell, Lisa, and Ian Walker. 1999. “The Welfare Effects of Lotto: Evidence from the

UK.” Journal of Public Economics 72:99–120.

Forrest, David, David Gulley, and Robert Simmons. 2000. “Elasticity of Demand for UK

National Lottery Tickets.” National Tax Journal 53:853–863.

———. 2008. “The Relationship between Betting and Lottery Play.” Economic Inquiry

forthcoming, DOI: 10.1111/j.1465–7295.2008.00123.x.You can also read